Sample Category Title

European Open Briefing

Global Markets:

- Asian stock markets: Nikkei up 0.15 %, Shanghai Composite rose 0.75 %, Hang Seng gained 1.15 %, ASX 200 lost 0.20 %

- Commodities: Gold at $1210 (+0.70 %), Silver at $17.13 (+1.20 %), WTI Oil at $48.30, Brent Oil at $51.30

- Rates: US 10 year yield at 2.58, UK 10 year yield at 1.24, German 10 year yield at 0.48

News & Data:

- Japan Machine Orders MoM (Jan): -3.20% (est -0.10%, prev 6.70%)

- Japan Machine Orders YoY (Jan): -8.20% (est -3.70%, prev 6.70%)

- AU Credit Card Balances (Jan): A$51.5bn (prev A$52.8bn)

- AU Credit Card Purchases (Jan): A$24.6bn (prev A$ 27.7bn)

CFTC Positioning Data:

- EUR net short 59k vs 51k previous

- GBP net short 81k vs 70k previous

- JPY net short 54k vs 50k previous

- AUD net long 51k vs 51k previous

- CAD net long 29k vs 30k previous

- CHF net short 10k vs 12k previous

- NZD net short 4k vs 3k previous

Markets Update:

The US Dollar weakened overnight. The US employment data on Friday was solid, but since the market is already counting on a rate hike on Wednesday, it is not enough to keep the USD rally going.

The Euro broke above the level of 1.07 in Asia. It cleared a major resistance area between 1.0670 and 1.0680, and this signals that the rally could extend to 1.0825 soon.

Meanwhile, USD/JPY is likely to face further pressure soon. Support is seen at 114.00/20. Should it break below that, a deeper correction seems likely.

The Aussie Dollar bounced as well. The major support area between 0.75 and 0.7520 held, and it is on its way to test 0.76 again. Should it break above 0.7620 resistance, it could have another test of 0.7740 soon.

Upcoming Events:

- 09:00 GMT – Italian Industrial Production

- 13:30 GMT – ECB President Draghi speaks

- 14:00 GMT – ECB Member Constancio speaks

- 16:30 GMT – ECB Member Praet speaks

The Week Ahead:

Tuesday, March 14th

- 07:00 GMT – German CPI

- 10:00 GMT – German ZEW Economic Sentiment

- 10:00 GMT – Euro Zone Industrial Production

- 10:00 GMT – Euro Zone ZEW Economic Sentiment

- 12:30 GMT – US PPI

- 21:45 GMT – New Zealand Current Account

Wednesday, March 15th

- 07:45 GMT – French CPI

- 08:15 GMT – Swiss PPI

- 09:30 GMT – UK Unemployment Rate

- 09:30 GMT – UK Claimant Count Change

- 09:30 GMT – UK Average Hourly Earnings

- 10:00 GMT – Italian CPI

- 12:30 GMT – US CPI

- 12:30 GMT – US Retail Sales

- 14:00 GMT – US NAHB Housing Market Index

- 14:30 GMT – US Crude Oil Inventories

- 18:00 GMT – Federal Reserve Rate Decision

- 18:00 GMT – FOMC Statement

- 18:30 GMT – FOMC Press Conference

- 21:45 GMT – New Zealand GDP

Thursday, March 16th

- 00:30 GMT – Australian Employment Change

- 00:30 GMT – Australian Unemployment Rate

- 03:00 GMT – Bank of Japan Rate Decision

- 06:30 GMT – Bank of Japan Press Conference

- 08:30 GMT – SNB Rate Decision

- 08:30 GMT – SNB Statement

- 10:00 GMT – Euro Zone CPI

- 12:00 GMT – Bank of England Rate Decision

- 12:30 GMT – US Building Permits

- 12:30 GMT – US Housing Starts

- 12:30 GMT – US Philadelphia Fed Manufacturing Index

- 12:30 GMT – US Initial Jobless Claims

Friday, March 17th

- 10:00 GMT – Euro Zone Trade Balance

- 12:30 GMT – Canadian Manufacturing Sales

- 13:15 GMT – US Industrial Production

- 13:15 GMT – US Manufacturing Production

- 14:00 GMT – US CB Leading Index

- 14:00 GMT – US Michigan Consumer Sentiment

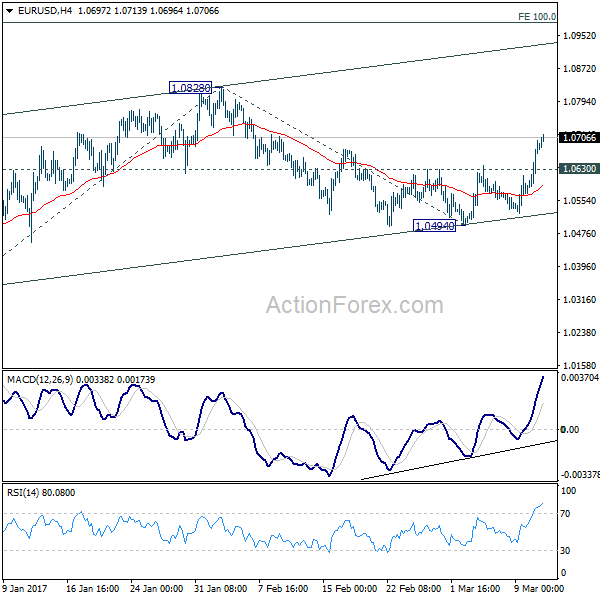

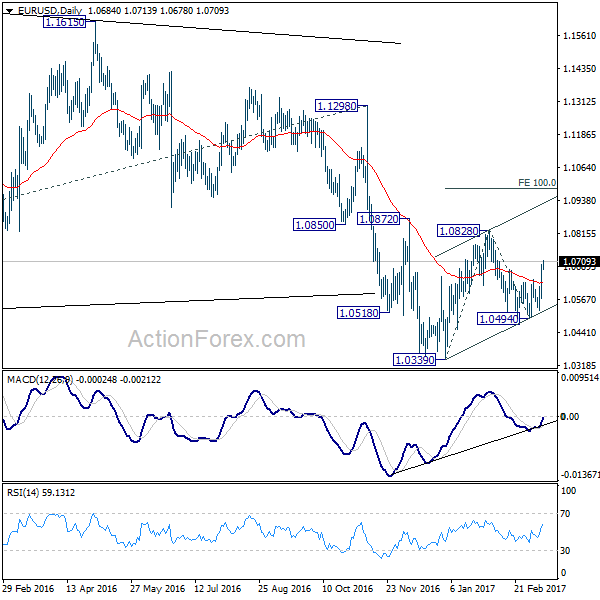

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0595; (P) 1.0647 (R1) 1.0723; More.....

EUR/USD's rise from 1.0494 extends to as high as 1.0713 today so far. Intraday bias remains on the upside for 1.0828 resistance and above. Note again that rise from 1.0339 low is seen as a corrective move. Hence, we'd expect upside to be limited by 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. The larger down trend is still expected to resume later. On the downside, break of prior resistance at 1.0630 will turn bias back to the downside for retesting 1.0494 low.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

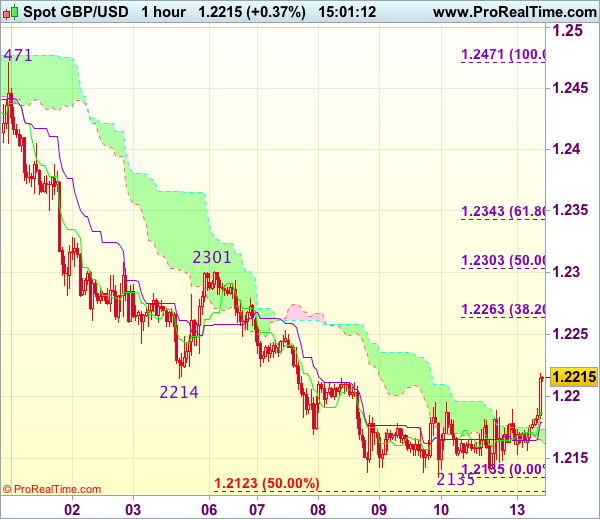

Trade Idea : GBP/USD – Buy at market level

GBP/USD - 1.2215

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2197

Kijun-Sen level : 1.2189

Ichimoku cloud top : 1.2173

Ichimoku cloud bottom : 1.2162

New strategy :

Buy here, Target: 1.2320, Stop: 1.2180

Position : -

Target : -

Stop : -

Current rally above indicated resistance at 1.2195 suggests a temporary low is possibly formed at 1.2135 last week and consolidation with upside bias is seen for retracement of recent decline, hence further gain to 1.2260-65 (38.2% Fibonacci retracement of 1.2471-1.2135) would be seen, however, break of 1.2301-03 (previous resistance and 50% Fibonacci retracement) is needed to signal low is formed, bring a stronger rebound to 1.2340-45 (61.8% Fibonacci retracement) later.

In view of this, we are looking to turn long here. Below the Kijun-Sen (now at 1.2190) would defer and risk weakness to 1.2170 but said support at 1.2135 should hold. Only break there would abort and signal recent decline has resumed and extend weakness to 1.2100.

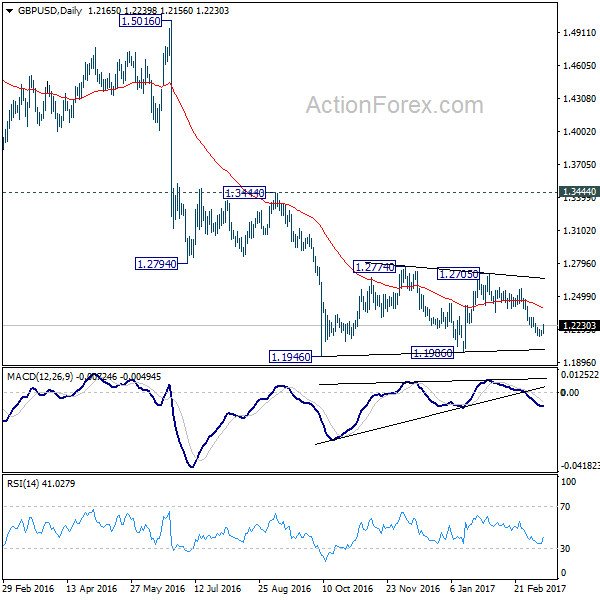

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2133; (P) 1.2160; (R1) 1.2187; More...

GBP/USD's rebound from 1.2133 extends higher today. But still, such rise is seen as a correction. Intraday bias stays neutral first. At this point, we'd still expect upside of recovery to be limited by 1.2346 support turned resistance and bring fall resumption. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. On the downside, below 1.2133 will turn bias to the downside for retesting 1.1946/86 support zone. Break of 1.1946 will confirm our bearish view. However, sustained break of 1.2346 will dampen out view and turn focus back to 1.2569 resistance first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

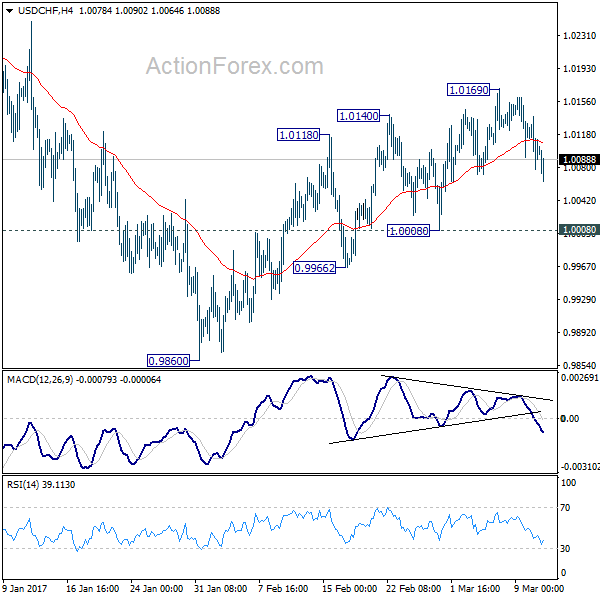

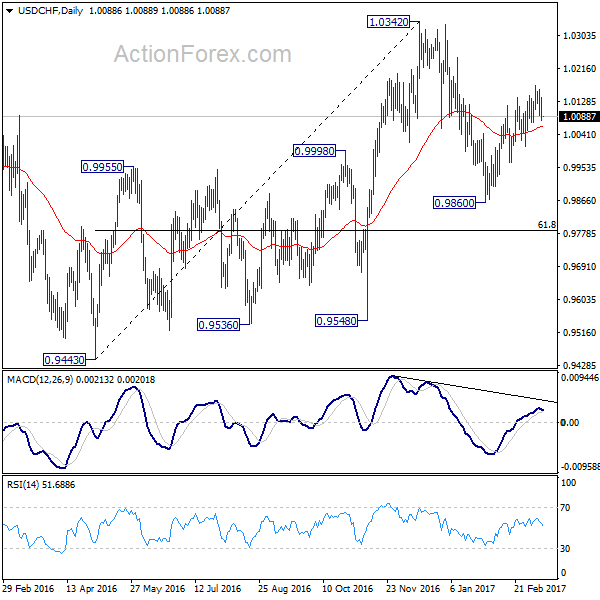

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0078; (P) 1.0107; (R1) 1.0135; More.....

Intraday bias in USD/CHF remains neutral for the moment. Upside momentum has been very unconvincing with bearish divergence condition in 4 hour MACD. But the pair holds well above 1.0008 support so far, making another rise in favor. Above 1.0169 will turn bias to the upside and target a test on 1.0342 resistance. Based on neutral medium term outlook, we'd be cautious on topping below 1.0342. On the downside, break of 1.0008, however, will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

Trade Idea : EUR/USD – Buy at 1.0660

EUR/USD - 1.0707

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0696

Kijun-Sen level : 1.0651

Ichimoku cloud top : 1.0579

Ichimoku cloud bottom : 1.0570

Original strategy :

Buy at 1.0560, Target: 1.0660, Stop: 1.0525

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0660, Target: 1.0760, Stop: 1.0625

Position : -

Target : -

Stop : -

As the single currency has risen again after finding renewed buying interest at 1.0669, suggesting recent upmove from 1.0493 low is still in progress and bullishness remains for this move to extend further gain to 1.0730-35 (50% projection of 1.0572-1.0699 measuring from 1.0669), however, loss of near term upward momentum should prevent sharp move beyond 1.0745-50 (61.8% projection) and reckon 1.0760 (1.618 times projection of 1.0495-1.0640 measuring from 1.0525) would hold on first testing.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as 1.0560-70 should limit downside, bring another rise later. Below the Kijun-Sen (now at 1.0651) would defer but only break of previous resistance at 1.0615 would abort and signal top is formed.

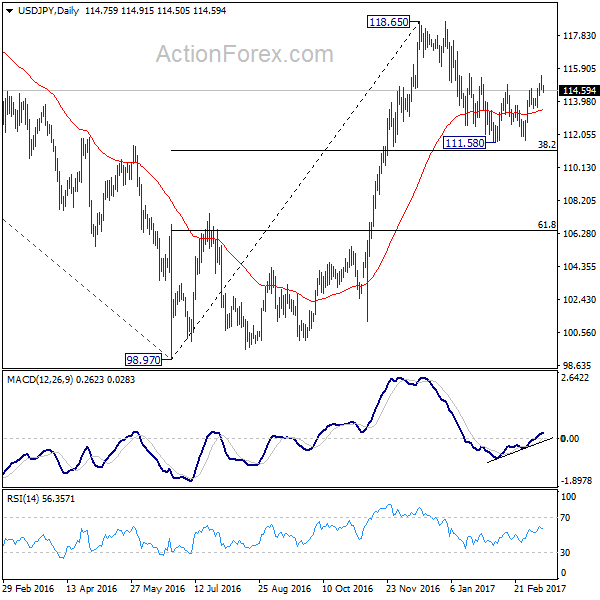

USD/JPY Daily Outlook

Daily Pivots: (S1) 114.42; (P) 114.96; (R1) 115.28; More...

Intraday bias in USD/JPY remains neutral for consolidation below 115.49 temporary top. Deeper retreat could be seen to 4 hour 55 EMA (now at 114.20). But downside should be contained well above 113.60 support and bring another rally. As noted before, corrective decline from 118.65 should have completed with a a double bottom pattern (111.58, 111.68). Above 115.49 should turn bias to the upside and pave the way for a test on 118.65. Decisive break there will extend whole rise from 98.97 and target 125.85 high next. However, break of 113.60 will invalidate our view and turn bias back to the downside for 111.58/68 support zone instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

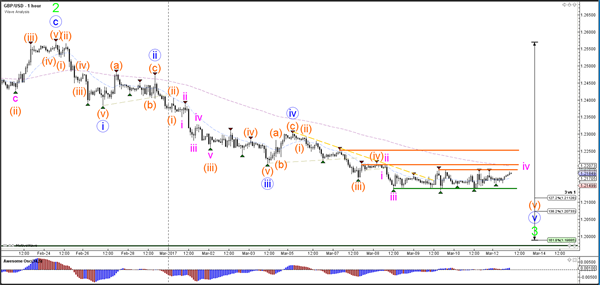

EUR/USD Bullish Momentum Reaches 1.0750 Resistance Zone

Currency pair EUR/USD

The EUR/USD broke above the resistance trend line (dotted red) of the consolidation zone (red/green) and has reached the 61.8% Fibonacci retracement level of wave 2 (purple). Any of the Fibonacci levels could be a resistance spot but a break above the 100% level invalidates the wave 1-2 structure.

The EUR/USD is showing strong momentum in the bullish 5th wave (orange) within wave C (blue). The momentum could indicate a potential for wave 4 (pink) and another wave 5 (pink) within wave 5 (orange).

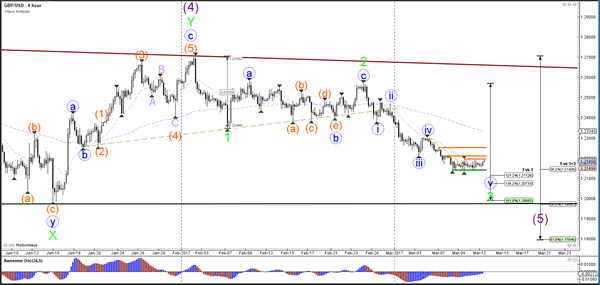

Currency pair GBP/USD

The GBP/USD is moving sideways in a consolidation zone and price has both horizontal support (orange) and resistance (orange) nearby. A bearish break below support (green) could see price move towards 1.20 which is a psychological round level, previous bottom (green) and 161.8% Fibonacci target.

The GBP/USD remains bearish in my view as long as price stays below horizontal resistance levels (orange). The divergence between the bottoms could indicate that a bearish break of support (green) might lack strength. A break above resistance (orange) invalidates the wave 4 (pink) correction.

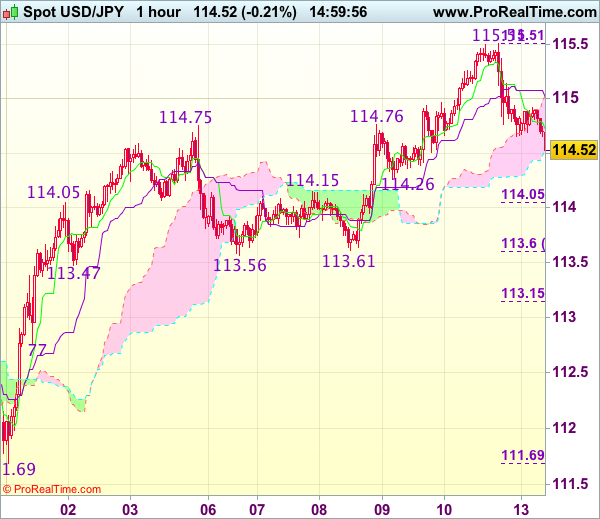

Currency pair USD/JPY

The USD/JPY broke above the resistance top (dotted red) of the wave 1 (blue) but momentum is lacking so far and price has retraced back below the broken resistance point (dotted red). Price could be retracing as long as price stays above support (green lines).

The USD/JPY could be building a wave 1-2 (orange) but a break below the 100% Fibonacci level invalidates wave 2 (orange).

Trade Idea : USD/JPY – Exit long entered at 114.70

USD/JPY - 114.62

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 114.71

Kijun-Sen level : 115.01

Ichimoku cloud top : 115.05

Ichimoku cloud bottom : 114.54

Original strategy :

Bought at 114.70, Target: 115.70, Stop: 114.35

Position : - Long at 114.70

Target : - 115.70

Stop : - 114.35

New strategy :

Exit long entered at 114.70

Position : - Long at 114.70

Target : -

Stop : -

Although the greenback recovered after finding support at 114.65, renewed selling interest emerged at 114.92 and dollar has fallen again today, suggesting near term downside risk remains for the fall from 115.51 top (last week’s high) to bring at least a retracement of recent upmove to 114.26 support but reckon downside would be limited to 114.00-05 (38.2% Fibonacci retracement of 111.69-115.51) and price should stay well above strong support at 113.56-61), bring rebound later.

In view of this, we are exiting our short position entered at 114.70 and stand aside for now. Above the Kijun-Sen (now at 115.01) would suggest an intra-day low is formed, bring a stronger rebound to 115.25-30 but still reckon said resistance at 115.51 would cap upside. Only break there would revive bullishness and extend recent upmove to previous resistance at 115.62, then towards 115.90-00.

We Have Several Speeches From ECB Members

Market movers today

We have several speeches from ECB members, but they are unlikely to provide markets with additional information regarding the statements from the ECB from last week.

The UK parliament will vote on a bill that would authorise Prime Minister Theresa May to begin negotiations for a Brexit. Hence, this week may be the week where May decides to ‘trigger' Brexit.

Furthermore, focus will be on the Dutch election as well as the FOMC meeting. The FOMC meeting seems to be a done deal in terms of a rate hike. The markets will be looking for information on how many hikes the Federal Reserve will do in 2017.

In Scandi markets, focus will be on Swedish inflation as well as the Norges Bank meeting. See more below and our publication Scandi Markets Ahead: Norges Bank meeting and focus on "weak" NOK, 12 March 2017, where there is a special section on the NOK.

Selected market news

Asian equities posted some small gains across the region this morning on the back of the positive US labour market report released on Friday last week, as well as the positive data from China this morning. Chinese industrial production data for January and February released this morning showed gains of more than 6%, while the service sector expanded more than 8%.

Focus in the Asian markets will be on the FOMC meeting as well as the Bank of Japan meeting this week. The oil price continues to slide this morning. We have seen small movements in the major currencies this morning. The EUR/USD has moved above the 107 level in Asian trade.

There were increased tensions between the Netherlands and Turkey over the weekend, as ministers from Turkey were barred from campaigning in the Netherlands. However, even though this might give support to Geert Wilders' campaign, the dispute is not expected to have a major impact on the Dutch election.