Sample Category Title

AUD/USD: Aussie Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.84% against the USD and closed at 0.7523.

LME Copper prices declined 0.4% or $25.0/MT to $5782.0/MT. Aluminium prices rose 1.2% or $23.0/MT to $1881.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7513, with the AUD trading 0.13% lower against the USD from yesterday's close.

Earlier today, in China, Australia's largest trading partner, the consumer price index (CPI) advanced 0.8% YoY in February, falling short of market expectations for a rise of 1.7% and rising at its slowest pace since January 2015. The CPI had climbed 2.5% in the previous month. On the other hand, the nation's producer price index increased more-than-expected by 7.8% on an annual basis in February, accelerating at its fastest pace in nearly nine years and compared to market expectations for an advance of 7.7%. In the previous month, the index had advanced 6.9%.

The pair is expected to find support at 0.7479, and a fall through could take it to the next support level of 0.7444. The pair is expected to find its first resistance at 0.7578, and a rise through could take it to the next resistance level of 0.7642.

The currency pair is trading/showing convergence with its 20 Hr and 50 Hr moving average.

EUR/USD: German Industrial Production Grew At Its Quickest Pace Since August 2016 In January

For the 24 hours to 23:00 GMT, the EUR declined 0.25% against the USD and closed at 1.0539.

Macroeconomic data indicated that Germany's seasonally adjusted industrial production rebounded more-than-expected by 2.8% on a monthly basis in January, notching its highest level in five months, suggesting that the industrial sector has returned to growth-path at the beginning of the year. Markets expected the nation's industrial output to rise 2.7%, following a revised drop of 2.4% the prior month.

The greenback gained ground against its key counterparts, after robust ADP's jobs data in US pointed to underlying strength in the economy that could encourage the Federal Reserve to raise interest rates next week.

Data revealed that ADP's private sector employment advanced by 298.0K in February, posting its largest increase since December 2015 and beating market consensus for a rise of 187.0K. The private sector employment had recorded a revised gain of 261.0K in the previous month. Also, the nation's MBA mortgage applications climbed 3.3% in the week ended 03 March 2017, following a rise of 5.8% in the previous week. On the contrary, the nation's final wholesale inventories fell more-than-anticipated by 0.2% on a monthly basis in January, compared to an increase of 0.9% in the preceding month and following a drop of 0.1% in the preliminary print.

In the Asian session, at GMT0400, the pair is trading at 1.0530, with the EUR trading 0.09% lower against the USD from yesterday's close.

The pair is expected to find support at 1.0515, and a fall through could take it to the next support level of 1.0499. The pair is expected to find its first resistance at 1.0559, and a rise through could take it to the next resistance level of 1.0587.

Moving ahead, all eyes would be on the European Central Bank's (ECB) interest rate decision, scheduled to be announced later in the day. Additionally, in the US, initial jobless claims data, set to release later today, will be on investor's radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

GBP/USD: OBR Raises Britain’s GDP Growth Forecasts In UK’s 2017 Spring Budget

For the 24 hours to 23:00 GMT, the GBP declined 0.29% against the USD and closed at 1.2167.

Yesterday, UK's Finance Minister, Philip Hammond, in his Budget speech, stated that Britain's economy is likely to feel the pain of Brexit more sharply in the coming years despite showing resilience so far. Hammond added that the UK economy will grow faster than previously forecast in 2017, as the Office for

Budget Responsibility (OBR) expects economic growth of 2.0% in 2017, up from the 1.4% predicted in November. However, he also mentioned that growth will slow down over the next three years, as he set the course for government spending with Britain preparing to leave the European Union. Moreover, inflation was forecasted to be 2.4% this year and 2.0% in both 2018 and 2019.

In the Asian session, at GMT0400, the pair is trading at 1.2158, with the GBP trading 0.07% lower against the USD from yesterday's close.

Overnight data indicated that UK's RICS house price balance remained steady at 24.0 in February, compared to market expectations of a fall to a level of 23.0.

The pair is expected to find support at 1.2127, and a fall through could take it to the next support level of 1.2096. The pair is expected to find its first resistance at 1.22, and a rise through could take it to the next resistance level of 1.2242.

Amid a lack of economic releases in UK today, investors will look forward to global events for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

USD/JPY: Japanese Yen Trading Marginally Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.41% against the JPY and closed at 114.44.

In the Asian session, at GMT0400, the pair is trading at 114.45, with the USD trading a tad higher from yesterday’s close.

The pair is expected to find support at 113.77, and a fall through could take it to the next support level of 113.1. The pair is expected to find its first resistance at 114.93, and a rise through could take it to the next resistance level of 115.42.

With no major economic releases in Japan today, trading trend in the JPY is expected to be determined by global macroeconomic news.

The currency pair is showing convergence with its 20 Hr moving average trading above its 50 Hr moving average.

USD/CHF: Swiss Inflation Rises At Highest Monthly Rate In Five Years In February

For the 24 hours to 23:00 GMT, the USD rose 0.2% against the CHF and closed at 1.0148.

On the data front, Switzerland's consumer price index (CPI) jumped more-than-anticipated by 0.5% on a monthly basis in February, accelerating at its fastest pace in five years. The CPI registered a flat reading in the prior month, while markets were anticipating it to climb 0.2%.

In the Asian session, at GMT0400, the pair is trading at 1.0152, with the USD trading marginally higher from yesterday's close.

The pair is expected to find support at 1.0129, and a fall through could take it to the next support level of 1.0106. The pair is expected to find its first resistance at 1.0166, and a rise through could take it to the next resistance level of 1.0180.

Moving ahead, Switzerland's unemployment rate data for February, slated to release in some time, will garner significant amount of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

USD/CAD: Canada’s Housing Starts Surprisingly Jumped In February

For the 24 hours to 23:00 GMT, the USD rose 0.62% against the CAD and closed at 1.3492.

In economic news, Canada's seasonally adjusted housing starts unexpectedly advanced to a level of 210.2K in February, confounding market consensus for a drop to a level of 200.0K and compared to a revised level of 208.9K in the previous month. Moreover, the nation's building permits climbed 5.4% MoM in January, more than market expectations for a rise of 3.0% and after recording a revised fall of 4.4% in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.3497, with the USD trading slightly higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3430, and a fall through could take it to the next support level of 1.3364. The pair is expected to find its first resistance at 1.3531, and a rise through could take it to the next resistance level of 1.3566.

Ahead in the day, market participants will focus on Canada's new house price index for January.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Chinese Inflation And UK House Prices Overnight

Market movers today

The second ECB meeting of 2017 takes place today. The ECB acknowledged that ‘there are no signs yet of a convincing upward trend in underlying inflation' at the last meeting in January. Even as headline inflation reached 2.0% in February, we do not expect the ECB to deviate from this stance. Mario Draghi has outlined four objectives for monetary policy, including that inflation convergence should (1) affect the medium term, (2) be durable, (3) be self-sustained (i.e. prevail when monetary easing ceases) and (4) be region wide. While we definitely see improvements across the region, we do not believe the inflation figures satisfy the four objectives, particularly not with core inflation staying below 1.0%. We therefore do not expect any policy changes today.

EU leaders will gather today and tomorrow for the European Council meeting to discuss the economic situation in Europe.

Weekly US jobless claims are due to be released at 14:30 CET. Claims have been trending lower since early 2016 and last week, data showed initial claims falling by 19,000 to 223,000 in the week ending 25 February, the lowest reading since 1973. The low claims figures are consistent with job growth above 250,000, although admittedly the link is fairly weak.

Selected market news

Chinese inflation and UK house prices overnight. China reported a 7.8% y/y surge in producer price inflation in February (previous: 6.9%, survey: 7.7%), painting quite a different picture than the consumer price inflation, which came in at 0.8% (previously: 2.5%, survey: 1.7%). However, the apparent divergence between the two measures should be seen in light of the decline in food prices. Adjusting for this, CPI was relatively stable at 2.2% and therefore within the government's comfort zone. Taken together, the inflation report could therefore support further moderate tightening by policy makers. Also overnight, UK RICS house prices showed an unchanged level in February, with the index coming in at +24 (January: +25, survey: +23).

In terms of data, the US ADP report was yesterday's highlight. The report came out strong with a reading of 298,000 jobs in February, the highest reading since December 2015, clearly pointing to upside risks to Friday's US employment. In Europe, German industrial production rose a healthy 3.0% in January, but should be seen in light of the 2.4% decline the month before (although this was revised higher from 3.0%). In the UK, Chancellor Hammond revised the 2017 GDP forecast higher to 2.0% in the budget, which otherwise did not deliver any major changes.

The ADP report added to the bearish sentiment on fixed income markets yesterday. In the US, yields were higher but also in Germany, where the 10Y rose by 5bp. Meanwhile, the S&P500 index broke a two-day losing streak, as the increase in interest rate expectations lifted financial stocks. The sub-sector was higher by 0.7%, while the overall index gained a more modest 0.1%.This morning, stocks in Asia are struggling, with energy shares in particular under pressure after Brent crude oil prices fell 5.4% yesterday on a surge in US inventories.

Asian Market Update: China Inflation Data Diverge With A Pop In Wholesale And A Slump In Retail

China inflation data diverge with a pop in wholesale and a slump in retail

US Session Highlights

Appaloosa's David Tepper: market on multiple basis is kind of full, but seeing synchronized growth globally; short bonds, long US and European stocks; thinks Central Banks, ECB in particular, will have to play catch-up following French elections

(US) FEB ADP EMPLOYMENT CHANGE: +298K V +187KE; Jan revised higher, weather helped

(US) Q4 FINAL NONFARM PRODUCTIVITY: 1.3% V 1.5%E; LABOR COSTS: 1.7% V 1.6%E

(US) JAN WHOLESALE INVENTORIES (FINAL) M/M: -0.2% V -0.1%E; WHOLESALE TRADE SALES M/M: -0.1% V +0.5%E

(US) DOE CRUDE: +8.2M V +1.5ME; GASOLINE: -6.5M V -1.5ME; DISTILLATE: -2.7M V -1.5ME (largest weekly drop in gasoline stocks since 2011); total production rose by 56K bbls

US markets on close: Dow -0.3%, S&P500 -0.2%, Nasdaq +0.1%

Best Sector in S&P500: Healthcare

Worst Sector in S&P500: Energy

Biggest gainers: HRB +14.9%, TRIP +6.1%, PPG +6.0%, COH +33%, M +3.1%

Biggest losers: MRO -8.7%, MUR -6.7%, DVN -6.5%, CHK -6.1%, NFX -5.4%

At the close: VIX 11.9 (+0.4pts); Treasuries: 2-yr 1.37% (+4bps), 10-yr 2.55% (+4bps), 30-yr 3.15% (+4bps)

US movers afterhours

APRI: Announces sale of Ex-U.S. Vitaros Assets and Rights to Ferring Pharmaceuticals; +32.3% afterhours

VVUS: Reports Q4 $0.54 v -$0.09e, R$81.8M v $15.3M y/y; +26.9% afterhours

ELF: Reports Q4 $0.19 v $0.13e, R$76.4M v $74.4Me- Guides initial FY17 $0.40-0.43 v $0.36e, R$285-295M v $281Me; Adj EBITDA $61-64M; +16.2% afterhours

SMTC: Reports Q4 $0.37 v $0.35e, R$140M v $138Me; Guides Q1 $0.39-0.43 v $0.37e, Rev $138-146M v $141Me, gross margin 58.6-59.7%, capex $10.0M; +7.1% afterhours

TGTX: Announces Proposed Public Offering of Common Stock for an indeterminate amount through Jefferies; -3.4% afterhours

CWH: Reports Q4 $0.14 adj v $0.09e, R$670M v $676Me; -4.8% afterhours

RATE: Reports Q4 $0.16 v $0.18e, R$113.6M v $122Me; Guides Q1 adj EBITDA $26-28M, R$115-118M v $113Me; -10.5% afterhours

TLRD: Reports Q4 -$0.19 v -$0.11e, R$793M v $824Me; Guides FY17 $1.47-1.75 v $2.12e; -29.2% afterhours

Politics

(US) Former US Ambassador to China Jon Huntsman said to accept Pres Trump's offer to serve as Ambassador to Russia - press

(US) Pres Trump said to consider sending up to 1K troops to Kuwait to serve as reserve force in a battle against ISIS - press

Asia Key economic data:

(CN) CHINA FEB CPI M/M: -0.2% (first decline in 4 months, biggest decline in 9 months) V +1.0% PRIOR; Y/Y: 0.8% (2-year low) V 1.7%E

(CN) CHINA FEB PPI Y/Y: 7.8% V 7.7%E; 6th consecutive and biggest increase since Sept 2008

(JP) JAPAN DEC LABOR CASH EARNINGS Y/Y: 0.5% V 0.4%E ; REAL EARNINGS (EX-INFLATION) Y/Y: 0.0% V +0.1% PRIOR

(JP) JAPAN FEB M2 MONEY STOCK Y/Y: 4.2% (highest since Aug 2015) V 4.2%E; M3 MONEY STOCK Y/Y: 3.6% V 3.6%E

Asia Session Notable Observations, Speakers and Press

Asia indices are largely lower, tracking the 3rd consecutive down day in the S&P500. Nikkei225 is among the few gainers, helped by weaker JPY in the wake of a blowout ADP jobs report that sent US Treasury yields and USD higher across the board. Benchmark 10-year yield rose as high as 2.58% - the highest level of 2017 - while Fed Funds futures now price in over 40% chance of 2 rate hikes in the first half of the year.

In FX, USD/JPY approached 114.60 in Asia session, just shy of US hours high, while AUD/USD fell to 7-week lows near 0.75. NZD/USD was also sold off on USD strength, falling below $0.79 for the first time since early Jan.

Energy sector was the worst performer on the S&P500 for the 2nd straight day, remaining in the doldrums in the wake of the latest inventories data that showed little evidence of production curbs - DOE increase was the 9th straight build and also the highest in 3 weeks. Weakness in the energy space in Australia and Hong Kong reflected falling oil prices.

China inflation data was the highlight of the economic calendar for the session with what is now a trifecta of surprises, following unexpected trade deficit overnight and return of FX reserves about $3T earlier. Feb PPI rose for the 6th straight month and to its highest level since Sept 2008 thanks to recent jump in commodity prices. Conversely, CPI fell m/m for the first time in 4 months, and y/y figure hit a 2-year low after a near-3-yr high last month. Food component shrank sharply, down 4.3% after rising 2.7% previously, as NBS noted that the number of tourists declined last month with seasonality around the timing of Lunar New Year continuing to play a part in data distortions. Also of note, PBoC skipped its daily open market operations in reverse repos, claiming that liquidity in the banking system basically stable while also setting CNY weaker for the 3rd straight day.

In Japan, Toshiba was hit especially hard on press speculation of expanded loss related to nuclear ops as well as rising challenges of meeting the deadline for releasing already delayed Q3 earnings report.

China

(CN) China listed banks NPL ratio may reach 1.8% in 2017 v 1.7% prior - Chinese press

(CN) ANZ: Expect China to move back to trade surplus in the coming months - Chinese press

(CN) China regulators said to have ordered banks to inspect their internal controls - Chinese press

Japan

(JP) Japan Fin Min Aso: Keeping FY20 primary budget surplus a goal

(JP) Japan foreign min Kishida: North Korea to be important theme of US State Sec Tillerson's visit; Aware that all options are on the table - press

Australia/New Zealand

(AU) Australia PM Turnbull: Political friction causing a risk to AAA rating: Australia has a credible path to a surplus to help maintain its AAA rating - AFR

(AU) Australia Newcastle Feb coal exports -12.2% m/m at 11.6M tons - financial press

(NZ) BNZ lowers New Zealand Q4 GDP forecast to 0.4% from 0.6% following weak manufacturing report - press

Korea

(KR) Economic Research Institute of Industrial Bank of Korea: Economic retaliation by China to Korea's THAAD system may cost Korea GDP about 1.1pct - Korean press

(KR) South Korea Finance Ministry monthly report: Export recovery to continue; Domestic demand remains weak

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.3%, Hang Seng -1.0%, Shanghai Composite -0.9%, ASX200 -0.3%, Kospi -0.1%

Equity Futures: S&P500 flat; Nasdaq flat; Dax flat; FTSE100 flat

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0530-1.0547; JPY 114.30-114.60; AUD 0.7510-0.7535; NZD 0.6895-0.6915

Apr Gold -0.4% at $1,205/oz; Apr Crude Oil +0.6% at $50.59/brl; May Copper flat at $2.59/lb

SLV: iShares Silver Trust ETF daily holdings fall to 10,303 tonnes from 10,350 tonnes prior; 11-month low

(CN) PBoC skips open market operations for today's session v injecting CNY30B yesterday

(CN) PBOC SETS YUAN MID POINT AT 6.9125 V 6.9032 PRIOR; 3rd straight weaker setting; weakest CNY setting since Jan 12th

(JP) Japan MoF sells ¥2.21T in 0.1% 5-year JGB bonds; avg yield -0.118% v -0.089% prior; bid-to-cover 2.86x (lowest since Oct 2015) v 4.26x prior

(AU) Australia 10-yr govt bond yield rises to 2.84%; 15-month high

Asia equities/Notables/movers by sector

Consumer discretionary: 419.HK Huayi Tencent Entertainment Company -4.8% (FY16 guidance); TTS.AU Tatts Group +2.6% (ACCC comments); NEC.AU Nine Entertainment +2.7% (Macquarie raises rating)

Financials: 832.HK Central China Real Estate -4.8% (profit warning)

Industrials: 3808.HK Sinotruk -2.0% (FY16 guidance); 9064.JP Yamato Holdings +1.8% (Nomura raises rating); 6472.JP NTN Corp +2.4% (Mizuho raises rating)

Technology: 6502.JP Toshiba Corporation -6.9% (Japan press speculates co. having difficulty in preparing Q3 earnings before deadline and nuclear writedown may rise); YPB.AU YPB Group +6.5% (receives order); QMS.AU QMS Media +2.2% (APN shows interest)

Materials: 2362.HK Jinchuan Group International Resources -1.1% (guidance); WHC.AU Whitehaven -4.4% (Spot coking coal firms on China buying before contract talks)

Energy: 931.HK China LNG Group -6.0% (profit warning); 883.HK CNOOC -2.1%, WPL.AU Woodside Petroleum -1.2%, BPT.AU Beach Energy -1.8%, STO.AU Santos -3.3% (oil falls over 5% in US session); 5017.JP Fuji Oil Co -2.2% (SMBC cuts rating)

Utilities: 6841.JP Yokogawa Electric Corp -2.8% (Credit Suisse cuts rating)

Trade Idea: AUD/USD – Hold short entered at 0.7605

AUD/USD – 0.7510

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Sold at 0.7605, Target: 0.7450, Stop: 0.7635

Position: - Short at 0.7605

Target: - 0.7450

Stop: - 0.7635

New strategy :

Hold short entered at 0.7605, Target: 0.7450, Stop: 0.7585

Position: - Short at 0.7605

Target: - 0.7450

Stop:- 0.7585

As aussie has fallen again after meeting renewed selling interest at 0.7633 earlier this week and the breach of previous support at 0.7543 adds credence to our view that top has been formed at 0.7741 and bearishness remains for the fall from there to bring retracement of recent upmove, hence further weakness to 0.7493 support is likely, below there would extend fall to 0.7449 support which is likely to hold on first testing.

In view of this, we are holding on to our short position entered at 0.7605. Only above said resistance at 0.7633 would risk a stronger rebound to 0.7665 (61.8% Fibonacci retracement of 0.7741-0.7543) but only break there would abort and suggest the retreat from 0.7741 has ended, bring a stronger rebound to 0.7700 but price should falter well below said resistance at 0.7741, bring another decline.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

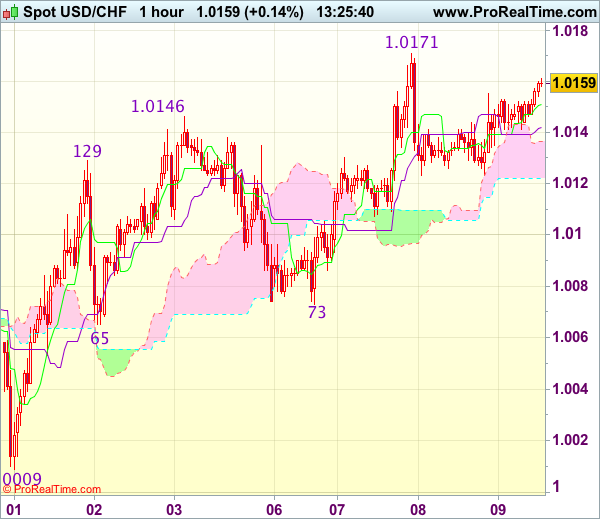

Trade Idea : USD/CHF – Buy at 1.0080

USD/CHF - 1.0158

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0151

Kijun-Sen level : 1.0142

Ichimoku cloud top : 1.0136

Ichimoku cloud bottom : 1.0122

Original strategy :

Buy at 1.0080, Target: 1.0200, Stop: 1.0045

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0080, Target: 1.0200, Stop: 1.0045

Position : -

Target : -

Stop : -

Although the greenback has rebounded after finding support at 1.0123 yesterday, break of this week’s high at 1.0171 is needed to signal recent erratic rise from 0.9861 low has resumed and extend further gain to 1.0200-10 but near term overbought condition should limit upside to 1.0220-25 and price should falter below previous chart resistance at 1.0248. If said resistance at 1.0171 continues to hold, then further consolidation would take place and risk of another retreat to 1.0123 cannot be ruled out, however, reckon downside would be limited to 1.0100 and support at 1.0173 should hold, bring another rise later.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as support at 1.0073 should limit downside. A drop below 1.0065 support would abort and signal top is formed instead, risk weakness to 1.0040-45 but reckon support at 1.0009 would remain intact.