Sample Category Title

President Trump Shifts Tone And Appears Presidential

The eyes of the world have been hooked on President Trump overnight as he delivered his first speech to congress. There was an element of surprise for viewers because Trump actually appeared Presidential during his speech, following what has been quite a rough first 40 days in office.

While the US markets slipped lower and there was still no real clarity provided towards how Trump will implement his campaign promises, the shift in tone from the US President was more guided towards how he publically appeared after winning the election back in November where he soothed investor's nerves with messages around the need for partnership and peace. Nevertheless, the undertone of "America First, And Always" was still very much present but the US President was at least not just pushing his far-right agenda on this occasion.

I believe that the USD should now strengthen over the near-term, not because of President Trump's speech but because Federal Reserve officials are providing ongoing clues to the market that a possible interest rate rise in March is not something to completely rule out of the equation. While the markets might not have been pricing in a US interest rate rise this month, US economic data is maintaining its consistent strength and the Federal Reserve is maintaining its public intention towards raising US interest rates around three times in 2017.

Basically my opinion is that the markets will now begin to shift focus away from Trump slightly, and more importantly begin to price in the possibility that the Federal Reserve could pull the trigger in March.

Gold slipping from its highs

Gold has continued its weakness early Wednesday morning and if this momentum continues, it looks like the precious metal will enter a three-day losing streak. The main catalyst for the near three-month high seen late last week was due to investors hedging against political risk, but I believe that Gold is at risk to further losses as investors begin to price in at least the possibility that the Federal Reserve could pull the trigger and raise interest rates this month.

Investors need to be aware to the risks that Federal Reserve officials do appear to be preparing the financial markets for another US interest rate rise fairly soon, even if it does not occur as early as March.

GBPUSD still at risk

While it might appear like the GBPUSD is attempting to consolidate after suffering three days of successive losses, there are still risks ahead for the British Pound and it wouldn't surprise me if the Cable dipped even lower.

When it comes to the technicals, I am going to keep my eye out for whether the GBPUSD closes below 1.2350 in trading today because this would be seen as a possible signal that the Pound is at risk to falling back towards 1.20.

From a fundamental basis, the impending delivery of Article 50 from Theresa May and the reemergence of a Scottish Referendum round 2 threat later in the future does favour a negative outlook for the Pound.

Australia avoids recession!

Australia has managed to continue its remarkable run of 25 years recession free after it was confirmed early this morning that the Australian economy has not slipped into a recession.

The AUDUSD has popped higher on the news, but I still feel that the Australian currency is likely to surrender some more of its gains over the past couple of weeks.

India GDP reading exceeds expectations

This might not have been viewed as the most critical data release of the week by any means, but the GDP reading from India has defied expectations with the economy growing at 7%. Although this represents a slowdown from the previous level at 7.4%, it has defied the forecast just below 6.5% and counters the fears that the controversial note ban from the government last year was going to derail the outstanding economic progress that India has made over the past couple of years.

Perhaps it will take more time and there will be a bit of a lag before it can really be analysed what impact the completely unexpected, and controversial decision to withdrawal highdenomination banknotes as part of an anti-corruption drive is going to have on the Indian economy.

US: Limited New Information About Trumponomics In Trump’s Joint Address To Congress

Overnight, President Trump delivered his joint address to Congress. Overall, the speech gave an overview of Trump's accomplishment so far and what he wants to focus on throughout his presidency and thus the speech included little new information. The speech was not only about economics but also about crime, immigration, border control and Obamacare.

From a market perspective, it was most interesting to hear what Trump had to say on his tax reform and infrastructure, as we have not had much new information since his election victory. However, as somewhat expected, the speech was scant on details on his economic policy. Trump repeated that he is working on a 'historic tax reform', which will lower taxes significantly for both corporates and persons. He also hinted that the US needs to fix its taxation of imports and exports without being specific about whether we should expect border adjustment taxation (as suggested by Paul Ryan) or old-style tariffs.

On infrastructure, Trump said the time has come for 'a new program of national building' and that he will ask 'Congress to approve legislation that produces a $1 trillion investment in the infrastructure of the United States'.

In the speech, Trump also said that he believes in free but fair trade. Yesterday, we wrote that there is a risk that the US will take protectionist measures against WTO rules and a new story on Reuters supports this. The story says that the US administration is looking to simply ignore WTO rules going forward, as the US is only 'subject to laws and regulations made by the US government'.

On foreign policy, Trump repeated that the US 'strongly supports NATO' but that member countries 'must meet their financial obligations'.

In a recent interview, Treasury Secretary Steven Mnuchin said that the administration hopes to see the economic plan passed before Congress' August recess but that it is an ambitious deadline and it could easily slip further into the year. He also said that he expects the biggest growth impact from next year, supporting our long-held view.

While the market reaction after Trump's speech was fairly muted as expected, markets reacted to hawkish Fed comments by Williams and Dudley before the speech sending US yields higher and EUR/USD lower. Dudley (voter, dovish) said that the case for tightening has become 'a lot more compelling' and that the 'risks to the outlook are now starting to tilt to the upside'. Williams (non-voter, neutral) said that he expects the Fed to consider a March hike seriously. Both were on the hawkish side compared to the minutes, which signalled that only 'a few' FOMC members seem ready to hike already in March. This only makes Janet Yellen's speech on Friday more interesting, as we have had mixed signals from the Fed recently. Our base case is still that the Fed skips March. Markets now price in a March hike by nearly 70%, a May hike by nearly 85% and 1.3 hikes are priced in by June.

Swiss KOF Index Climbs 5.2 Points In February

'The strong Swiss franc is still a challenge for a very large number of companies.' - Swissmem (based on Investing.com)

Data released on Tuesday revealed that the Swiss KOF leading indicator surged markedly over the month of February, pointing to better-than-expected growth in the country's economy. The KOF Swiss Economic Institute reported the KOF index added 5.2 points in February, which is strongly above its long-term average, jumping to 107.2 from an upwardly revised reading of 102.0 registered in the preceding month. The upmove was mainly driven by the positive trend established in the manufacturing and hospitality sectors coupled with favourable signals from the financial, exporting and construction industries. Furthermore, the KOF said that the upgraded sentiment in manufacturing came mainly from paper, textile, architects and machine-building sectors, whilst other industries posted almost no change over the observed period. Apart from that, the report revealed the KOF had also revised upwards its confidence in the country's manufacturing on the back of generally more optimistic assessment of incoming orders along with a positive outlook for production and employment. Overall, the KOF report suggested that the Swiss economy should expand at an above-average growth pace in the months to come.

US Economy Confirms 1.9% Growth In Q4 Despite Higher Consumer Spending

"The marked improvement in the survey evidence recently suggests that growth will continue at a decent pace in the first half of this year too." - Paul Ashworth, Capital Economics

The US economy grew less than expected in December quarter even in spite of higher consumer spending observed in the reported period. Figures released on Tuesday showed the US economy grew at an annualised pace of 1.9% in the Q4, following a strong 3.5% reading registered in the preceding quarter and falling behind analysts' expectations for a 2.1% rise. In the report, the Commerce Department highlighted that the economic growth was mainly boosted by consumer spending that was revised to 3.0% from 2.5% reported previously. With household spending accounting for no less than 70% of the American economic activity, analysts around the world remained optimistic on the overall growth in the country in the months ahead. Furthermore, the report revealed that the surge in purchases by consumers in the final quarter of 2016 was mainly driven by higher sales of new cars and trucks. Apart from that, Americans were seen to have spent more on health care. On balance, inventory investment was revised down to $46.2B from $48.7B, while spending on equipment rose a more modest 1.9% instead of 3.1% originally estimated. Moreover, there were changes in trade figures, with imports climbing 8.5% along with a sharp 4.0% decline in observed in exports.

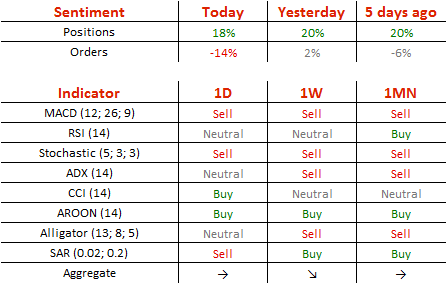

EUR/USD Positioned For Major Fall

'Trump made no suggestions on how he would pay for his plans.' – Bloomberg

Pair's Outlook

The common European currency opened Wednesday's trading against the US Dollar near the 1.0575 level. However, during the first hours of the day's trading the rate moved lower, and passed the closest support level before a large range without any level of significance. Due to that fact the currency exchange rate positioned itself for a major fall, as the closest support was at the 1.0491 level, where the weekly S1 located at. It is likely that the rate will fall to this support soon, and there it will be stopped for at least a while, as the lower Bollinger band is closing in to support the weekly S1.

Traders' Sentiment

SWFX traders still have not changed their opinion regarding the pair, as 52% of open positions remain long. Meanwhile, 61% of trader set up orders are to sell the Euro.

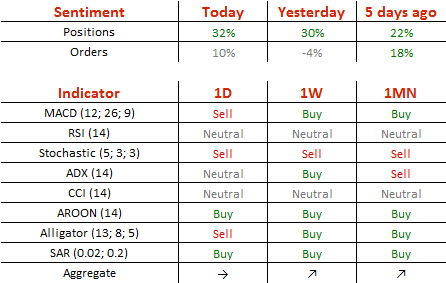

GBP/USD: Key Support Broken, Weakness Expected

'On top of soft data from the UK recently ... these fresh signals of a 'hard Brexit' and the risk of another Scottish referendum, enhances our view that the broader outlook for sterling remains negative.' – IronFX (based on Business Recorder)

Pair's Outlook

Buck's strength caused the Cable to slide further down, breaching the strong demand cluster at 1.24. From this point on more, more bearish momentum is likely to follow, as the 55-day SMA pierced the 100-day one on Monday, providing a signal to sell the Pound. The breach of the key support cluster also indicates that the Sterling could relatively soon retest the 1.20 mark. A drop that low is yet to occur, but today trade is expected to close circa 1.2320, while being supported by the weekly S2 slightly lower. Meanwhile, technical indicators retain mixed signals, unable to confirm the possibility of the negative outcome.

Traders' Sentiment

Bulls gave in again, as they now take up 59% of the market, compared to 60% on Tuesday. At the same time, the portion of orders to sell the British currency increased from 49 to 57%.

USD/JPY Attempts To Break The Down-Trend

'I think the Fed will get a green light [to raise rates] unless a very bad [U.S.] jobs data comes out next week.' – Yukio Ishizuki, Daiwa Securities (based on Reuters)

Pair's Outlook

Trump's speech yesterday boosted the US Dollar, causing the USD/JPY currency pair to recover from its intraday low of 111.75. However, the Buck was unable to post solid gains against the Yen, thus, the down-trend remains preserved. Following yesterday's events, the Greenback is likely to retain its strength and continue outperforming the Japanese currency. The closest resistance is located around 113.15, formed by the 20-day SMA, the bearish trend-line and the weekly R1, which should technically limit the gains. A breach of this area would open the door for a surge to the cluster circa 114.50, namely the upper border of the bears six-week consolidation trend.

Traders' Sentiment

Today two thirds (66%) of all open positions are long, compared to 65% yesterday. The share of buy orders inched up from 48 to 55%

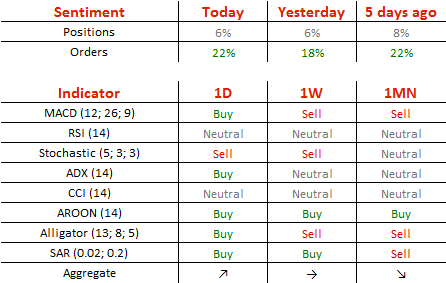

Gold Retreats Below 1,250 Level

'There were no new policy announcements there and a lot of it is already built into the U.S. dollar.' - Jeffrey Halley, OANDA (based on Reuters)

Pair's Outlook

During the early hours of Wednesday's trading session the yellow metal was in its third consecutive session of losses, as the bullion's price retreated below the 1,250 mark and it even had touched the 1,242.42 level. Gold is likely to fall until it reaches the support provided by the uptrend line, which has been pushing the commodity price higher since December 21. On Wednesday the line's support was located at 1,240.14 level. However, if that support is passed, the metal will face a strong support cluster, which begins at 1,236.39.

Traders' Sentiment

Traders have not changed their opinion, as 53% of open positions remain long on Wednesday. Meanwhile, 61% of trader set up orders are to buy the bullion.

USD Surges after a Salvo of FOMC and Trump Remarks

Overnight, the US dollar outperformed most of its major counterparts following a barrage of hawkish remarks from FOMC officials, as well as comments on infrastructure spending by President Trump before Congress. The dollar rally was triggered by New York Fed President Dudley, who indicated that the case for a rate hike has become "a lot more compelling". Considering that Dudley usually maintains a neutral tone with regards to policy, these hawkish hints probably came as a surprise to many market participants, and revived some hopes with regards to a March hike. The chorus of optimistic FOMC comments continued with St. Louis Fed President Bullard and San Francisco Fed President Williams, both of which indicated that a near-term rate hike is a considerable possibility.

While investors were still digesting these remarks, President Trump stepped up to the rostrum to deliver his first address to Congress. Although the President did not offer much detail on tax reform, he did provide some specifics on infrastructure spending. He said that he will ask Congress to approve legislation that produces USD 1 trillion worth of investment in infrastructure. These comments added extra fuel to the USD rally ignited by Fed policymakers. USD/JPY surged after it hit support near the key obstacle zone of 111.60 and subsequently, it crushed three resistance (now turned into support) barriers in a row. At the time of writing, the rate looks to be headed towards the 113.80 (R1) resistance line, where a decisive break is possible to open the way for the crossroad of the 114.40 (R2) zone and the downside resistance line taken from the peak of the 19th of January. Nevertheless, although the pair may continue trading north for a while, we maintain the view that the short-term path remains sideways. The rate has been oscillating between 111.60 and 115.50 since the 11th of January.

As for our view with regards to the next rate increase, we stick to our guns that June is a much more likely candidate than March. Even though the probability for a March rate hike rose to 36% according to the Fed funds futures, we insist that this percentage is somewhat optimistic for a variety of reasons. First, the rotation of voting rights has turned the FOMC more dovish this year, something that was confirmed by the minutes of the latest policy meeting, which revealed a cautious stance by the Committee overall. Second, even after Trump's overnight address, uncertainty around fiscal policy has not dissipated given that there is still a lot to be cleared up, especially with regards to spending and taxes. Finally, economic data do not call for an immediate hike yet, in our opinion. In order for us to reevaluate this view, we would need three things to happen in the next days: January's core PCE price index to accelerate today, Fed Chair Yellen to echo similar remarks with Dudley in her speech on Friday, and February's average weekly earnings, due next week, to accelerate notably.

BoC to take the sidelines amid improving data

Today, the highlight will be the Bank of Canada rate decision. The forecast is for the Bank to remain on hold. At its latest gathering, the BoC maintained a neutral bias with regards to policy in the meeting statement. However, Governor Poloz was quick to backpedal on that stance in the press conference following the decision. He said another rate cut remains on the table should downside risks materialize, leading investors to price in a higher probability for further easing. Since that meeting, economic data and developments have been encouraging, on balance. The labor market tightened notably in January and GDP growth rebounded in November, on a monthly basis. What's more, oil prices have remained elevated in the aftermath of the OPEC consensus, while inflation data for February came in on a solid footing, with both the headline and the core rates rising. Perhaps something worrisome for the Bank is that its signals for further easing did not manage to materially weaken the CAD, which has remained strong against most of its major counterparts. Bear in mind that when they last met, BoC officials expressed their discontent about the appreciation of the currency following the US election. Taking all these into account, we share the view that the Bank is likely to remain sidelined. In such a case, market focus will quickly turn to the statement accompanying the decision, as there is no press conference. Given the progress in economic data, we expect the tone of the statement to remain neutral, something that could prove positive for CAD. However, there is the possibility for another warning about the strength of the Loonie, considering that the currency has traded sideways against most of its major peers since then. Such a warning could offset some of the potential positive reaction in CAD.

USD/CAD jumped overnight following Fed officials' and Trump's remarks and is currently headed toward the 1.3340 (R1) zone. We believe that the pair is possible to continue trading higher in the days to come, but a relatively optimistic statement from the BoC today could be the catalyst for a corrective setback. A dip back below 1.3300 (S1) is possible to confirm the case for such a retreat and perhaps aim for the 1.3220 (S2) support zone, marked by the peaks of the 7th and 22nd of February.

As for the rest of today's highlights

During the European day, we get the final manufacturing PMIs for February from several European nations and the Eurozone as a whole. From Germany, we also get the preliminary CPI print for February. The forecast is for the rate to have risen above 2%, which could raise speculation that the Eurozone's overall CPI, due to be released tomorrow, may follow suit and accelerate further. Something like that could support the euro.

From the UK, we get the manufacturing PMI for February. Expectations are for the index to have ticked down, but to have remained elevated well-above the 50 mark separating expansion from contraction. Although the reaction in GBP may be somewhat negative, we doubt that such a print will be particularly worrisome for BoE policymakers.

From the US, we get a plethora of economic data. Let's kick off with personal income and spending data for January. The forecast is for income to have risen at the same pace as previously, while spending is expected to have slowed, but to have still grown at a healthy rate. We also get the ISM manufacturing PMI for February and expectations are for the index to have held steady. Finally, we get the core PCE price index for January, though no forecast is available. Given that this is the Fed's favorite inflation measure, and that this rate has been range-bound since February 2016, we expect it to attract a lot of attention as investors try to gauge the timing of the next rate hike. A potential increase in this rate could amplify further market expectations with regards to a March hike, as it could confirm that underlying inflationary pressures have begun to accelerate, something already indicated by the accelerating core CPI for the same month.

From Canada, we get the Markit manufacturing PMI for February, though this is likely to be overshadowed by the BoC meeting.

We have only one speaker scheduled for today: Dallas Fed President Robert Kaplan.

USD Still In A Limbo, Even As Fed Rate Expectations Rise

Sunrise Market Commentary

- Rates: Fed paves way for March rate hike

A handful of Fed governors, including heavyweight NY Fed Dudley, said that the case for a March rate hike became very compelling. The market implied probability of a March move surged to 80% and pulled US Treasuries lower. US President Trump's speech before Congress turned out to be a non-event. We expect more selling pressure today. - Currencies: Trump doesn't help the dollar, but the Fed does

Yesterday evening Fed governors Williams and Dudley hinted that a March Fed rate hike has become ever more likely. The dollar started a gradual rebound. However, the upside momentum was hampered as President Trump failed to give any details on fiscal policy. Still, the US eco data and Fed rate expectations might support further USD gains.

The Sunrise Headlines

- US equities opened weaker despite very strong US eco data and failed to recover losses ahead of Trump's speech. Japan outperforms in Asia on the back of a weaker yen as the prospect of an imminent Fed rate hike propels USD.

- Several Fed governors jolted markets into higher expectations for a March rate hike (80% probability), with comments that suggested they are worried about waiting too long in the face of pending economic stimulus from Washington.

- President Trump turned from the ominous language that characterized his campaign as he delivered an impassioned plea for Congress to capitalize on a political uprising and unite behind major overhauls of health care and tax laws.

- The ECB said it will test euro zone banks on their resilience to sharp changes in interest rates, simulating scenarios from sudden monetary tightening to the lending freeze that followed Lehman Brothers' collapse.

- China's factory activity (PMI's) expanded faster than expected in February as domestic and export demand picked up, adding to signs that the global economy is regaining momentum even as fears grow of a surge in trade protectionism.

- Australia's economy bounced back to robust growth in the fourth quarter of last year (1.1% Q/Q), fuelled by a jump in corporate profits linked to rising commodity prices, a surge in exports and higher household spending.

- Today's eco calendar heats up with manufacturing PMI/ISM's in the EMU, UK and US. Germany (CPI) and the US (PCE) publish inflation data, the BoC decides on its policy, Germany taps the market and the Fed releases the Beige Book.

Currencies: USD Still In A Limbo, Even As Fed Rate Expectations Rise

Dollar propelled by March rate hike bets

On Tuesday, USD trading was confined to tight ranges ahead of US president Trump's testimony before Congress. However, it didn't take till the Trump testimony for the dollar to catch a renewed bid. Late in the US session, Fed governors Williams and Dudley gave strong hints on a March rate hike, as the Fed is reaching its goals on inflation and unemployment. The dollar reversed the intraday losses against the euro and the yen. EUR/USD finished the session at 1.0576. USD/JPY closed the day at 112.77. The gains were modest, as investors might still have been cautious to place big USD bets ahead of the Trump speech.

Overnight, the focus was on the testimony of US president Trump. The US president hardly gave any specifics on the budget, tax cuts or on any other economic topic. Even so, the dollar extended its gains. The Trump speech was USD disappointing, but investors adapted positions on the rising likelihood of a March Fed rate hike. USD/JPY trades in the 113.50 area. BOJ member Sato said that the BOJ could raise the Target for the 10-year bond yield before the 2% target is reached. For now, his comments didn't help the yen. USD strength prevails. Even so, the USD gains against the euro are modest. EUR/USD is changing hands in the mid 1.05 area. Australian Q4 growth was reported at a strong 1.1% Q/Q and 2.4%. AUD/USD spiked temporary to the 0.77 area, but the move was soon reversed on overall USD strength (currently 0.7670).

Today, German HICP inflation is expected to have risen to 2.1% Y/Y in February from 1.9% Y/Y, a psychological issue in Germany. We join the consensus, but an upward surprise would increase chances for the EMU inflation to reach 2%. In US, the ISM manufacturing confidence is expected to have risen to 56.2 from 56. Recent surveys put the risk for an upward surprise (57/58?). The PCE (consumption) and PI (income) are expected to have risen 0.3% M/M each. Attention might go to the PCE deflators. The headline is expected to have risen to 2% Y/Y from 1.6%. In that case, the FOMC could formally say that the inflation target is reached. Of late, the focus for USD trading was on US fiscal policy (Trump speech). However, at this stage, it is the Fed talk that really matters. The probability of a March Fe rate hike has risen to 80%. The rise in short-term US yields should be USD supportive. The first reaction of EUR/USD to the rise in Fed rate hike expectations is modest. Even so, in this context we can't but the start the day with a USD positive bias. The Fed rate expectations should outweigh the disappointment on any details on fiscal policy from president Trump.

Global context. The dollar corrected lower since the start of January, but bottomed out three weeks ago supported by Trump's tax promise. Underlying euro weakness due to political uncertainty in the area is a factor too. Recent Fed comments were also USD supportive. Initially, it had little impact on yields and on the dollar. However this might change as chances on a March rate hike are sharply rising. We see 1.0874 as solid resistance and favour a sell EUR/USD on upticks approach. 1.0494 is first intermediate support. The downside test of USD/JPY was rejected. USD/JPY 111.60/111.16 (Range bottom/38% retracement of the 99.02/118.66 rally) remains key support. We keep a USD positive bias longer term, as the dollar might still get additional interest support if the Fed continues its normalisation process.

EUR/USD: USD succeeds only modest gains on Fed rate hike expectations

EUR/GBP

EUR/GBP drifting north of 0.85

Yesterday, sterling traded again with a tentatively negative bias. EUR/GBP drifted further north of 0.85. Cable hovered in the lower half of the 1.24 big figure for most of the day.. At a hearing before lawmakers, new MPC member Charlotte Hogg faced tough questions on monetary policy, including the management of the stock of assets on the BoE's balance sheet. Her assessment and tolerance on the inflation overshoot sounded rather dovish. In the press, the Scottish PM kept the door open for a second ‘indyref', as she was unhappy on the way PM May handles the EU views of Scotland. In both cases, the impact on sterling trading was limited. EUR/GBP closed the session at 0. 8543. Cable finished the day at 1.2380.

Today, the UK manufacturing PMI is expected little changed at 55.8. Markets will keep an eye at the Brexit vote in the House of lords. UK May might lose the vote for an amendment over the rights of EU citizens living in the UK. A negative outcome might complicate the Brexit timetable. The headlines might be slightly GBP negative. The overall context of USD strength will also affect sterling trading. That said, we have the impression that sterling sentiment has softened a bit of late. So, it is difficult for cable to outperform EUR/USD as is often the case with USD strength. Early last week, the euro sell-off pushed EUR/GBP to the 0.84 area, but a sustained break lower didn't occur. There is currently no clear driver for sterling trading. Longer term, we have a sterling negative view, as the Brexit will negatively impact the UK economy. We maintain a neutral bias on sterling shortterm.

EUR/GBP: drifting higher from the recent lows, but to sustained trend