Sample Category Title

Bank of Canada Remains Wary

- Bank monitoring risks to outlook given uncertainties about developments abroad

- These risks and slack in the domestic economy means current policy stance still appropriate

As-expected, the Bank of Canada held the overnight rate steady at 0.50% today. Recent developments appear to align with the Bank's base case forecast with global growth strengthening. In Canada, the Bank noted that recent data point to the economy growing at a slightly stronger pace than its 1.5% forecast. While the headline inflation rate rose in January, this reflected temporary effect of rising energy prices that in part rose because of the implementation of carbon pricing measures in Alberta and Ontario. As such the Bank said it is "looking through these effects" and noted that the core prices measures substantiate that the economy continues to run with "material excess capacity."

Our Take:

While financial markets debate the timing of the next hike by the US Fed, there is little anticipation that the Bank of Canada will move off the sidelines. The Bank's uneasiness about the global economic outlook and policy developments in the US were noted again today's brief statement. The Committee reiterated that there is slack in the domestic labour market pointing to the slow pace of wage gains and hours worked as evidence. The Bank also remains concerned about exports which they say continue to face "competitiveness challenges."

Despite presenting an upside risk to the fourth quarter's growth forecast, the tone of the statement seems lukewarm about the economy given the focus on the persistence of excess capacity and pressures on exports. This did little to alter the market's assessment that there is about only a one in three chance that the Bank will hike rates late this year.

Our forecast is that Canada's economy will grow at faster pace this year. We expect tomorrow's Q4 real GDP report to confirm the economy grew at a 1.8% annualized pace with a 0.2% increase in December providing a solid handoff to 2017. That momentum combined with mild recovery in the oil & gas sector will be sufficient to offset any weakening in the housing market and keep the economy growing at an above-potential pace. Against this backdrop, underlying measures of inflation are forecast to gradually increase to 2%. In the near term however uncertainty about potential policy initiatives by the new US Administration and their impact on Canada sets up for the Bank to stay on the side-lines.

Bank of Canada Paints a Dovish Picture Once Again

The Bank of Canada met expectations today, once again holding its key policy interest rate unchanged at 0.5%. Indications that fourth quarter growth likely beat the Bank's expectations were counterbalanced against ongoing competitiveness challenges.

The Bank of Canada made clear its view that recent gains in inflation are likely to be temporary, and that its three new measures of core inflation continue to point to economic slack.

Moreover, the challenges the Bank identified at its last policy decision, namely the high level of the Canadian dollar (in broad terms), and elevated bond yields are still in play. The statement noted this fact, while also mentioning that ongoing gains in employment have come with subdued growth in wages and hours worked, in contrast to the United States.

Key Implications

This was another dovish statement from the Bank of Canada. The statement accompanying the rate decision continued the tone of recent communications, namely that the level of the loonie and movements in bond yields are not seen as helpful given the economic slack still remaining in Canada.

Indeed, the Bank of Canada once again contrasted the current economic situation in Canada with that in the U.S., with the clear message that unlike south of the border, the Bank of Canada will not be tightening monetary policy any time soon.

Today's statement provides further confirmation of our view that the Bank of Canada will not be taking its foot off the accelerator. Over the near term, given the still significant economic uncertainties, particularly beyond Canada's borders, we continue to see the risks to monetary policy as tilted towards further easing.

US Consumer Spending up 0.2% in January But Volumes Decline

- The US nominal personal consumer expenditures (PCE) inched up 0.2% in January though the increase entirely reflected rising prices.

- The volume of sales declined 0.3% as auto sales pulled back and warmer-than-usual temperatures were likely to blame for a large pullback in spending on utilities.

Nominal spending on durable goods declined 0.3%, led by a 2.1% pullback in motor vehicle and parts sales that was flagged by an earlier-reported slowing in unit vehicle sales in the month. Sales of nondurable goods rose 1.0%, but entirely reflecting higher prices (including an 8% jump in gasoline prices). The volume of nondurable sales was unchanged in January. Spending on services was unchanged in nominal terms but declined 0.2% in real-terms although weakness was largely concentrated in an 11.8% drop in the volume of spending on electricity & natural gas as warmer-than-usual winter temperatures resulted in less need for home heating.

January spending growth was outpaced by a 0.4% rise in personal incomes, led by a 0.4% increase in employee compensation. The saving rate inched up to 5.5% from 5.4%. Annual growth in the headline PCE deflator rose to 1.9% (its highest level since October 2012) but the key core measure held steady at December's 1.7% year-over-year rate of increase.

Our Take:

Much (although not all) of the weakness in spending volumes in January reflected a sharp weather-related pull-back in utilities spending that will reverse as temperatures return to normal. With electricity output also tracking below seasonal normal in February, however, that rebound is likely to be more of a March/April story. The weak starting point to spending in Q1 (January spending in volume terms is little changed relative to its Q4 average) and the prospect for weak utilities spending to persist in February points to downside risk to our forecast for a 2.4% increase in consumer spending in the current quarter with a gain closer to 1 1/2% looking more likely. Nonetheless, much of the expected slowing in Q1 can be explained by transitory factors. Labour markets continue to improve and interest rates are still-low. Looking through monthly/quarterly volatility, we expect the underlying consumer demand backdrop remains constructive.

Higher Inflation Cuts into Purchasing Power and Real Spending Pulls Back in January

Personal income rose 0.4% in January, slightly above market expectations for 0.3%. Controlling for inflation and removing taxes, however, real disposable personal income fell 0.2%.

Spending rose by 0.2% in nominal terms, below the consensus call for a 0.3% gain. In real terms, spending fell 0.3%, a larger decline than the median estimate for -0.1%. The decline in spending was widespread. Durable goods led the way, falling 0.8%. Services spending fell 0.2%, while non-durable goods spending was virtually flat (-0.04%).

Consumer prices rose 0.4% in the month, pushing year-on-year inflation to 1.9% (from 1.6% in December). Core prices (ex food & energy) were up 0.3% month-on-month - the strongest gain in ten years - but year-on-year price growth held steady at 1.7%.

The personal saving rate edged up to 5.5% in January from 5.4% in December.

Key Implication

The downside of rising inflation is a decline in real purchasing power. This was the story in January. The turn-up in energy prices means that households are no longer seeing the purchasing power gains that they did over the past couple of years. This puts the onus for growth on stronger wage gains to drive increases in income and therefore spending. Fortunately, with the labor market continuing to tighten, this remains a good bet.

It wasn't just energy prices that pushed higher in the month. The rise in core prices was also noteworthy. While core inflation is still below 2% on a year-on-year basis, the momentum is certainly in the upward direction. With economic slack continuing to diminish, it is likely to push toward the Fed's 2% by the end of this year.

Market expectations have moved to increasingly expecting the Fed to lift interest rates at its next meeting in March given the hawkish rhetoric from many recent Fed spearkers. With the soft pace of real spending in this report, we would expect these odds to diminish somewhat. Nonetheless, the push higher in inflation means that every upcoming meeting will be in play.

Dollar Extends Rally as Positive Sentiments Continue

Dollar continues to ride on speculation of March rate hike and positive response to president Donald Trumps' Congress address. Released from US, personal income rose 0.4% in January while spending rose 0.2%. Headline PCE accelerated to 1.9% yoy but missed expectation of 2.0% yoy. Core PCE was unchanged at 1.7% Yoy, below expectation of 1.8% yoy. ISM manufacturing will be a key piece of data to look at and strong reading could give Dollar's rally more fuel. Fed will also release Beige Book economic report in the afternoon. For the time being, the greenback will like stay firm. Technically, 1.0493 support in EUR/USD and 114.94 resistance in USD/JPY should be watched.

Dollar index resumes rebound

Dollar index jumps to as high as 101.88 so far today and the break of 101.79 resistance indicates resumption of whole rebound from 99.23. Further rise should be seen back to retest 103.82 high. At this point, there is no clear sign of up trend resumption yet. Therefore, we'd be cautious on topping around there. But, as the index depended 99.11/43 support zone, the medium term up trend is expected to resume sooner rather than later. Meanwhile, on the downside, break of 100.66 minor support will turn focus back to 99.23 instead.

UK PMI manufacturing missed expectation

UK PMI manufacturing dropped to 54.6 in February, down from 55.9, and missed expectation of 55.7. Nonetheless, Markit noted that "the UK manufacturing sector continued its solid start to the year." And, "although rates of expansion in output and new business lost impetus in February, growth remained comfortably above the long-run averages. The survey is signalling quarterly manufacturing output growth close to the 1.5 per cent mark so far in the opening quarter which, if achieved, would be one of the best performances over the past seven years." Also from UK, mortgage approvals rose to 69.9k in January while M4 money supply rose 0.9% mom. BR shop price index dropped -1.0% yoy in February.

Also from Europe, Swiss SVME PMI rose to 57.8 in February, above expectation of 55.5. UBS consumption indicator rose to 1.43 in January. Eurozone PMI manufacturing was revised lower by 0.1 to 55.4 in February. Germany PMI manufacturing was reviewed lower to 56.8 while France PMI manufacturing was revised down to 52.2. Italy PMI manufacturing rose to 55.0 in February. From Germany, unemployment dropped -14k in February while unemployment rate was unchanged at 5.9%. German CPI accelerated to 2.2% yoy in February

China PMI manufacturing solid

The official China PMI manufacturing rose to 51.6 in February, above expectation of 51.2. PMI non-manufacturing dropped to 54.2. Caixin PMI manufacturing rose to 51.7. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group, said in the release that "the Chinese manufacturing economy continued to recover in February. But it is premature to jump to the conclusion that the recovery is entrenched." And, "the second quarter is likely a key period to look at for future trends."

Elsewhere, Australia GDP grew 1.1% qoq in Q4, above expectation of 0.7% qoq. New Zealand terms of trade rose 5.7% qoq in Q4. Japan capital spending rose 3.8% in Q4.

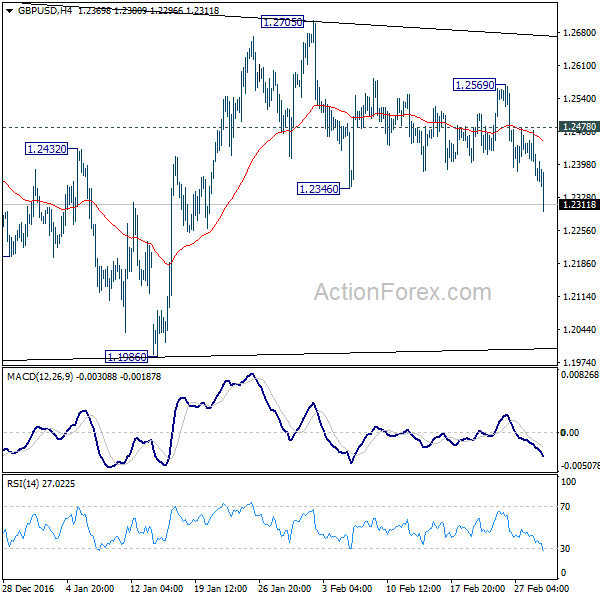

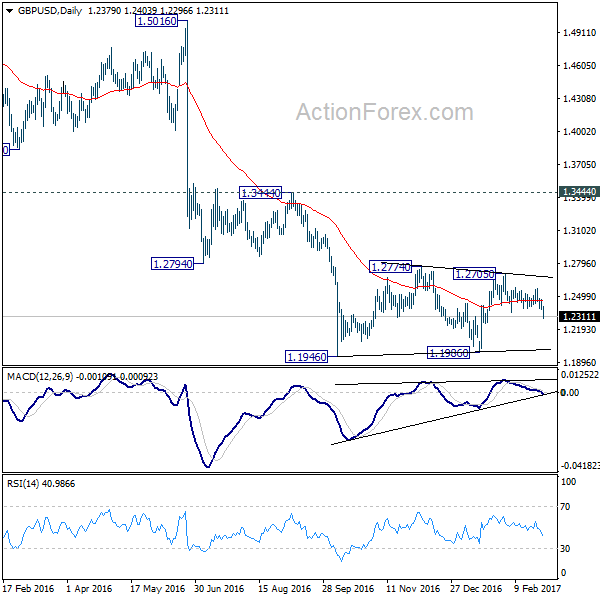

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2345; (P) 1.2408; (R1) 1.2442; More...

GBP/USD's sharp fall today and break of 1.2346 indicates that rebound from 1.1986 has completed at 1.2705 already. Intraday bias is turned back to the downside for retesting 1.1946/86 support zone. The consolidation pattern from 1.1946 has possibly completed at 1.2705 too. Break of 1.1946 will confirm our bearish view and resume the larger down trend. Nonetheless, on the upside, above 1.2478 minor resistance will delay the bearish case and turn bias neutral first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q/Q Q4 | 5.70% | 4.00% | -1.80% | -1.10% |

| 23:50 | JPY | Capital Spending Q4 | 3.80% | 0.60% | -1.30% | |

| 00:01 | GBP | BRC Shop Price Index Y/Y Feb | -1.00% | -1.40% | -1.70% | |

| 00:30 | AUD | GDP Q/Q Q4 | 1.10% | 0.70% | -0.50% | |

| 01:00 | CNY | Manufacturing PMI Feb | 51.6 | 51.2 | 51.3 | |

| 01:00 | CNY | Non-manufacturing PMI Feb | 54.2 | 54.6 | ||

| 01:45 | CNY | Caixin PMI Manufacturing Feb | 51.7 | 50.8 | 51 | |

| 07:00 | CHF | UBS Consumption Indicator Jan | 1.43 | 1.5 | 1.5 | 1.38 |

| 08:30 | CHF | SVME PMI Feb | 57.8 | 55.5 | 54.6 | |

| 08:45 | EUR | Italy Manufacturing PMI Feb | 55 | 53.5 | 53 | |

| 08:50 | EUR | France Manufacturing PMI Feb F | 52.2 | 52.3 | 52.3 | |

| 08:55 | EUR | Germany Manufacturing PMI Feb F | 56.8 | 57 | 57 | |

| 08:55 | EUR | German Unemployment Change Feb | -14K | -10k | -26k | |

| 08:55 | EUR | German Unemployment Rate Feb | 5.90% | 5.90% | 5.90% | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb F | 55.4 | 55.5 | 55.5 | |

| 09:30 | GBP | PMI Manufacturing Feb | 54.6 | 55.7 | 55.9 | 55.7 |

| 09:30 | GBP | Mortgage Approvals Jan | 69.9k | 68.5k | 67.9k | 68.3k |

| 09:30 | GBP | M4 Money Supply M/M Jan | 0.90% | -0.10% | -0.50% | |

| 13:00 | EUR | German CPI M/M Feb P | 0.60% | 0.60% | -0.60% | |

| 13:00 | EUR | German CPI Y/Y Feb P | 2.20% | 2.10% | 1.90% | |

| 13:30 | USD | Personal Income Jan | 0.40% | 0.30% | 0.30% | |

| 13:30 | USD | Personal Spending Jan | 0.20% | 0.30% | 0.50% | |

| 13:30 | USD | PCE Deflator M/M Jan | 0.40% | 0.50% | 0.20% | |

| 13:30 | USD | PCE Deflator Y/Y Jan | 1.90% | 2.00% | 1.60% | |

| 13:30 | USD | PCE Core M/M Jan | 0.30% | 0.30% | 0.10% | |

| 13:30 | USD | PCE Core Y/Y Jan | 1.70% | 1.80% | 1.70% | |

| 15:00 | CAD | BoC Rate Decision | 0.50% | 0.50% | ||

| 15:00 | USD | ISM Manufacturing Feb | 56 | 56 | ||

| 15:00 | USD | ISM Prices Paid Feb | 68 | 69 | ||

| 15:00 | USD | Construction Spending M/M Jan | 0.60% | -0.20% | ||

| 15:30 | USD | Crude Oil Inventories | 0.6M | |||

| 19:00 | USD | Fed Beige Book |

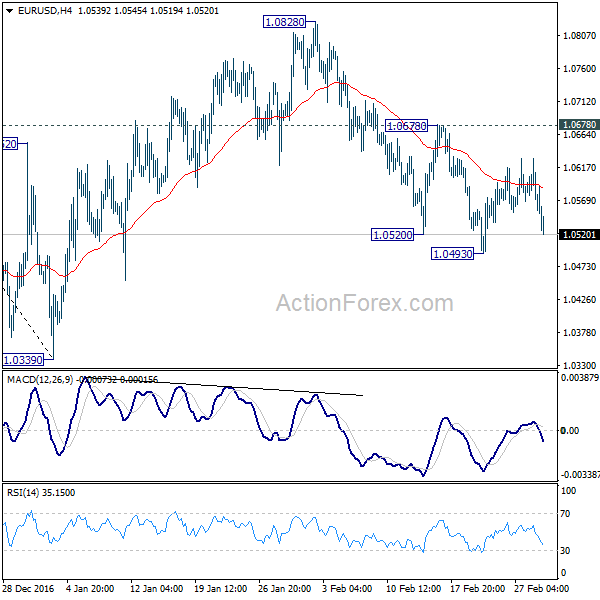

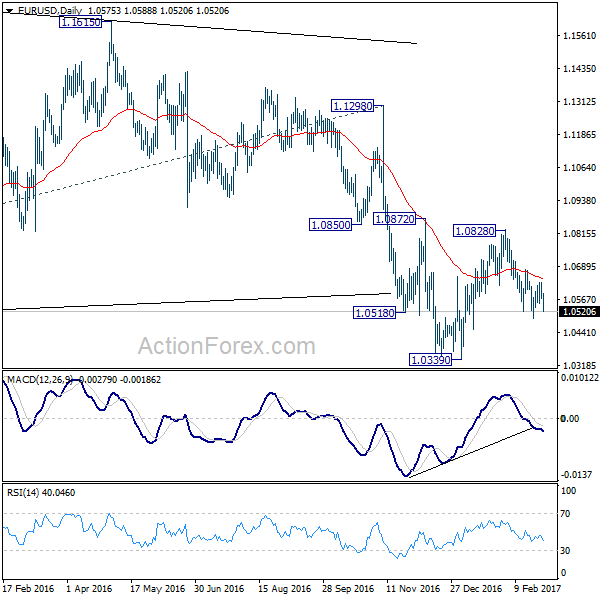

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0550; (P) 1.0590 (R1) 1.0616; More.....

EUR/USD drops sharply today but stays above 1.0493 so far. Intraday bias remains neutral with bearish outlook. With 1.0678 minor resistance intact, deeper decline is still expected. We're viewing fall from 1.0828 as resuming the larger down trend. Below 1.0493 will target 1.0339 low first. Break will confirm our bearish view and target parity. However, break of 1.0678 will dampen our view and turn focus back to 1.0828 resistance instead.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0011; (P) 1.0056; (R1) 1.0102; More.....

USD/CHF strengthens notably today but stays in range of 0.9966/1.0140. Intraday bias remains neutral for the moment. With 0.9966 support intact, further rise is in favor. Above 1.0140 will turn bias to the upside and target a test on 1.0342 resistance. Based on neutral medium term outlook, we'd be cautious on topping at around 1.0342. Meanwhile, break of 0.9966 will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

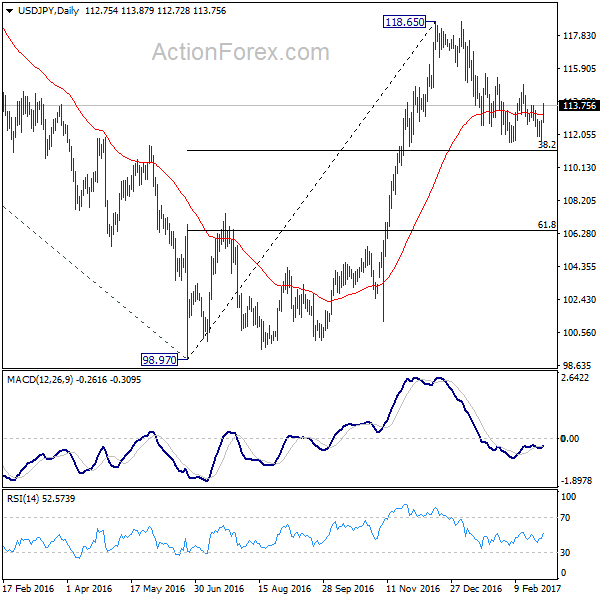

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.99; (P) 112.44; (R1) 113.20; More...

USD/JPY rebounds strongly today but stays below 114.94 so far and intraday bias remains neutral first. Price actions from 118.65 are viewed as a corrective move. Firm break of 114.94 resistance will indicate that it's completed, on a double bottom pattern (111.58, 111.68). In such case, intraday bias will be turned to the upside for retesting 118.65. Also, the whole rise from 98.97 is likely resuming. On the downside, in case of another fall, we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2345; (P) 1.2408; (R1) 1.2442; More...

GBP/USD's sharp fall today and break of 1.2346 indicates that rebound from 1.1986 has completed at 1.2705 already. Intraday bias is turned back to the downside for retesting 1.1946/86 support zone. The consolidation pattern from 1.1946 has possibly completed at 1.2705 too. Break of 1.1946 will confirm our bearish view and resume the larger down trend. Nonetheless, on the upside, above 1.2478 minor resistance will delay the bearish case and turn bias neutral first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

US Data and Fed Speeches Key as USD Tests Highs

The Dow's longest winning streak in 30 years may have come to an end and Donald Trump may well have coasted through his appearance in Congress offering no details to back up his bold policies, but investors remain undeterred on Wednesday as US indices prepare to open higher once again.

The rally in equity markets appeared to slow in the days leading up to Trump's appearance which suggested that investors were seeking more substance to back the President's bold plans but once again we were made to sit through more of the same rhetoric without any backlash from investors. It's difficult to say how long they will be willing to tolerate so much talk and no action but for now at least, it appears investors have faith in him to deliver even if it's going to take longer than planned. Should Trump fail to live up to the high expectations he's set himself then the impact could be significant.

What's helping to maintain the upbeat sentiment is the optimism coming from within the Fed. Not so long ago the market feared the mere prospect of a single rate hike but now they're taking the prospect of three comfortably within their stride. Perhaps the promise of more activity on the fiscal side combined with evidence of a much improved labour market is helping allay the fears that previously held the market back.

The Fed is certainly coming across more hawkish as of late and comments on Tuesday from William Dudley and John Williams strongly backed up views from other policy makers recently that March is very much a live meeting. I think it's clear right now that the Fed wants the market to perceive every meeting as live and even a week ago this was clearly not the case for March. At above 60% for March and 70% for May, the Fed has done a much better job at guiding market expectations and I'm sure Robert Kaplan and Lael Brainard will be keen to do more of the same today. I still think the Fed will likely move in May which would again drive home the message that every meeting is live, as this would be the first meeting without a press conference that it has raised rates in this cycle.

The dollar is rallying today on the back of these more hawkish Fed expectations and yields on US Treasuries are also higher. The US dollar index is seriously testing its range highs today, a break of which would see it trading at its highest level since 11 January and could trigger another surge in the greenback.

With plenty of data to come today - including income, spending, PCE inflation (the Fed's preferred measure) and two manufacturing PMIs - there are plenty of potential catalysts for such a move, should the numbers warrant it.