Sample Category Title

Asian Market Update: Trump Promises Tax Relief And $1T Infrastructure Investment

Trump promises tax relief and $1T infrastructure investment

Asia Mid-Session Market Update: Trump promises tax relief and $1T infrastructure investment; China manufacturing PMIs top estimates; Aussie GDP recovers

US Session Highlights

(US) Fed's Kaplan (moderate, voter): Should begin removing accommodation; path of rates more important than exact timing - CNBC

(US) Q4 PRELIMINARY GDP ANNUALIZED Q/Q: 1.9% V 2.1%E; PERSONAL CONSUMPTION: 3.0% V 2.6%E

(US) JAN ADVANCE GOODS TRADE BALANCE: -$69.2B V -$66.0BE

(US) Q4 PRELIMINARY GDP PRICE INDEX: 2.0% V 2.1%E; CORE PCE Q/Q: 1.2% V 1.3%E

(US) DEC S&P / CASE-SHILLER 20-CITY M/M: 0.93% V 0.70%E; Y/Y: 5.58% V 5.40%E; HOUSE PRICE INDEX (HPI): 192.61 V 192.14 PRIOR

(US) JAN PENDING HOME SALES M/M: -2.8% V +1.0%E; Y/Y: +2.7% V -2.0% PRIOR (falls to one-year low)

(US) Feb Chicago Purchasing Manager Index: 57.4 v 53.5e (highest since Dec 2014); new orders 59.2 v 49.1 prior

(US) FEB RICHMOND FED MANUFACTURING INDEX: 17 V 10E; Volume of new orders 24 v 15 prior

(US) FEB CONSUMER CONFIDENCE: 114.8 V 111.0E (highest since 2001)

(CO) Colombia Jan National Unemployment Rate: 11.7% v 8.7% prior; Urban Unemployment Rate: 13.4% v 11.4%e

(US) Fed's Dudley: Case for raising rates "has become a lot more compelling"; animal spirits have been unleashed after the election - CNN international taped interview

(US) Senior Trump officials reportedly disagree on border adjustment tax; said to still lack sufficient votes to pass the Senate - press

US markets on close: Dow -0.1%, S&P500 -0.3%, Nasdaq -0.6%

Best Sector in S&P500: Utilities

Worst Sector in S&P500: Consumer Discretionary

Biggest gainers: ALB +9.8%, PCLN +5.6%, ADM +3.5%, AES +3.5%, ENDP +2.7%

Biggest losers: SIG -12.8%, TGT -12.2%, PRGO -11.7%, FTR -10.9%, ETFC -7.2%

At the close: VIX 12.9 (+0.8pts); Treasuries: 2-yr 1.30% (+10bps), 10-yr 2.36% (-1bp), 30-yr 2.97% (-2bps)

US movers afterhours

BGFV: Reports Q4 $0.35 v $0.32e, R$266M v $266Me- Guides Q1 $0.12-0.18 v $0.05e; Guides Q1 SSS "positive mid-single-digit range"; +16.0% afterhours

WTW: Reports Q4 $0.20 v $0.18e, R$267.4M v $271Me; Guides initial FY17 $1.30-1.40 v $1.12e; +10.5% afterhours

LOGM: Reports Q4 $0.62 v $0.59e, R$88.0M v $87.3Me; Guides Q1 $0.72-0.76 v $0.60e; +7.5% afterhours

ROST: Reports Q4 $0.77 v $0.75e, R$3.51B v $3.45Be; Launches $1.75B share repurchase program (~6.5% of market cap); -0.8% afterhours

CRM: Reports Q4 $0.28 v $0.25e, R$2.29B v $2.27Be; -3.0% afterhours

CHUY: Reports Q4 $0.18 v $0.17e, R$79.1M v $81.4Me- Guides initial FY17 $1.11-1.15 v $1.19e; SSS +1-2%; -3.3% afterhours

EVHC: Reports Q4 $1.15 v $1.24e, R$1.39B v $1.40Be; Guides Q1 $0.75-0.81 v $0.99e; -12.1% afterhours

SRPT: Reports Q4 -$0.71 v -$1.26e, R$5.4M v $5.0Me; -14.3% afterhours

PANW: Reports Q2 $0.63 v $0.62e, R$422.6M v $430Me; Adds $500M to buyback plan; Guides Q3 $0.54-0.56 v $0.71e, R$406-416M v $453Me; -20.0% afterhours

Politics

(US) US President Trump: To provide massive tax relief for middle class; To seek $1T infrastructure investment program financed through public and private capital - speech to Congress

(US) Pres Trump said to be open to a legal pathway for undocumented immigrants - NY Times

(IQ) President Trump's new Executive Order on immigration will reportedly drop Iraq from the list of nations facing a travel bank - US press

Asia Key economic data:

(CN) CHINA FEB CAIXIN MANUFACTURING PMI: 51.7 V 50.8E (8th consecutive expansion)

(CN) CHINA FEB MANUFACTURING PMI (GOVT OFFICIAL): 51.6 V 51.2E; NON-MANUFACTURING PMI: 54.2 (4-month low) V 54.6 PRIOR

(JP) JAPAN FEB FINAL PMI MANUFACTURING: 53.3 V 53.5 PRELIM

(JP) JAPAN Q4 CAPITAL SPENDING Y/Y: 3.8% V 0.8%E; EX-SOFTWARE Y/Y: 3.3% V 1.1%E

(JP) JAPAN FEB DOMESTIC VEHICLE SALES Y/Y: 13.4% V 8.6% PRIOR

(AU) AUSTRALIA Q4 GDP Q/Q: 1.1% V 0.8%E; Y/Y: 2.4% V 2.0%E

(AU) AUSTRALIA FEB AIG MANUFACTURING INDEX: 59.3 v 51.2 PRIOR; 15-year high; 5th month of expansion

(AU) AUSTRALIA FEB CORELOGIC RPDATA HOUSE PRICES M/M: 1.4% V 0.7% PRIOR

(KR) SOUTH KOREA FEB TRADE BALANCE: $7.2B V $4.9BE

(HK) Macau Feb Gaming Rev MOP22.99B v MOP21.5Be; y/y: +17.8% v +10%e

Asia Session Notable Observations, Speakers and Press

Asia tracking slightly firmer, with Nikkei225 a clear outperformer on weaker JPY; USD/JPY has added to gains with the case for March Fed rate hike growing rapidly in the wake of stronger economic data (Richmond Fed index and Chicago PMI today) and notably more hawkish Fed-speak (typically a dove, New York's Dudley said case for March is more compelling). Rates on the short end of the curve spiked higher, while the Vix closed at its highest level of 2017.

Reaction to US President Trump's first address before the joint session of Congress (first year's equivalent to State of the Union) has been largely positive among the pundits and initial surveys, though critics would point to lack of substantive policy proposals; Most notably, Trump called for $1T public-private investment in infrastructure, reiterated intent to repeal/replace Obamacare, and again pledged massive tax relief for middle class.

China PMI data were mostly positive, particularly on the Manufacturing front; Official manuf print was a beat at 51.6 V 51.2E as key components such as New Export Orders and Employment hit multi-month highs; Caixin PMI also improved and is now in expansion for 8 months, with resident economist noting fastest increase in new export business since September 2014, post-Lunar New Year employment demand, and sharp rise in input costs.

Australia Q4 GDP was also a beat after a surprising q/q contraction in Q3. Terms of Trade component jumped 9.1% v 4.5% prior thanks to higher commodity prices, consumption improved to +0.7% v +0.3% prior, and capital investment rose a solid +2.6% v -2.7% prior.

China

(CN) China Labor Minister: Expect employment to remain relatively stable in 2017 despite complex situation - press

Japan

(JP) Japan Coast Guard claims 3 China Coast Guard vessels entered its waters - financial press

(JP) Japan Fin Min Aso: Economic growth is more important than fiscal balance

(JP) BOJ Gov Kuroda: Fiscal policy and BOJ easing can have synergy effects - press

Australia

(AU) Australia Treasurer Morrison: GDP data confirms Australia's successful change in economy

Asian Equity Indices/Futures (00:30ET)

Nikkei +1.5%, Hang Seng +0.1%, Shanghai Composite +0.5%, ASX200 -0.1%, Kospi +0.3%

Equity Futures: S&P500 +0.2%; Nasdaq +0.2%; Dax +0.2%; FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET

EUR 1.0550-1.0590; JPY 112.75-113.60; AUD 0.7635-0.7700; NZD 0.7130-0.7190

Apr Gold -0.8% at $1,244/oz; Apr Crude Oil +0.1% at $54.07/brl; May Copper +0.9% at $2.74/lb

(US) Weekly API Oil Inventories: Crude: +2.5M v -0.9M prior (5th build in the past 6 weeks)

USD/CNY PBOC SETS YUAN MID POINT AT 6.8798 V 6.8750 PRIOR

(CN) PBOC to inject combined CNY30B v CNY30B prior in 7-day, 14-day and 28-day reverse repos

(CN) China MoF sells 1-yr bonds at 2.73% v 2.71%e, bid-to-cover 1.67x and 10-yr bonds at 3.26% v 3.26%e, bid-to-cover 2.87x

(JP) BOJ To buy ¥320B (prior ¥400B) in 1-3yr JGBs

Asia equities/Notables/movers by sector

Consumer discretionary: 880.HK SJM Holdings -3.1% (FY16 result); HVN.AU Harvey Norman -5.8% (Macquarie cuts rating); PRR.AU Prima BioMed +9.1% (confirms granted US patent); 9603.JP HIS -3.5% (Q1 result); 1928.hk Sands China +4.2%, 1128.HK Wynn Macau +3.9% (Macau gaming rev)

Financials: 535.HK Gemdale Properties and Investment Corp +2.0% (profit alert); 27.HK Galaxy Entertainment Group +4.7% (FY16 result)

Industrials: 2343.HK Pacific Basin Shipping +7.1% (FY16 result)

Technology: ACX.AU Aconex +0.3% (signs pact); 6502.JP Toshiba Corporation +1.0% (seeks bids for chip unit)

Materials: DRM.AU Doray Minerals +1.5% (H1 result); RSG.AU Resolute Mining -4.0% (Baillieu Holst cuts rating)

Utilities: 6370.JP Kurita Water Industries +6.9% (first buyback in 2 years)

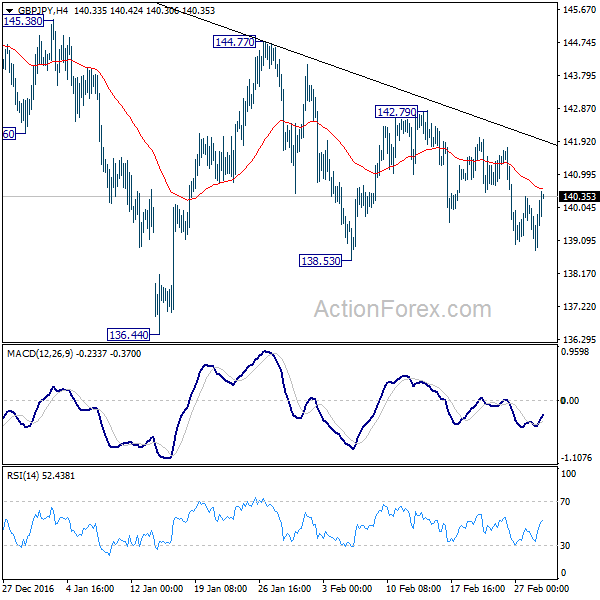

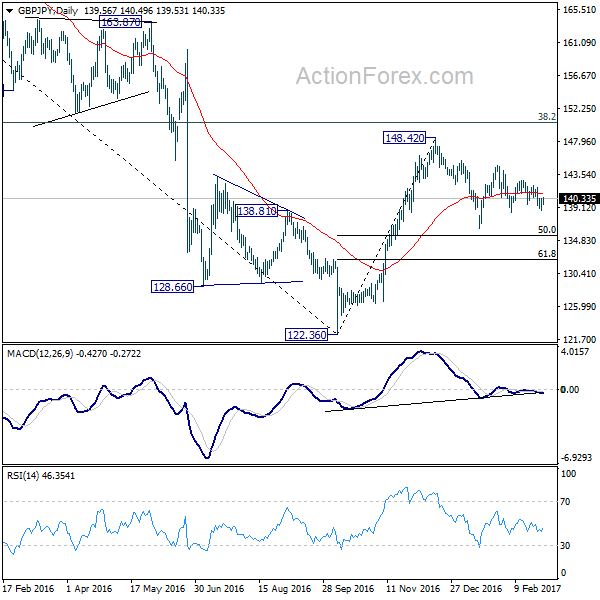

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.84; (P) 139.57; (R1) 140.34; More...

GBP/JPY is still bounded in range of 138.53/142.79 and intraday bias remains neutral for the moment. Overall, price actions from 148.42 are seen as a corrective pattern. Below 138.53 will bring deeper fall, possibly through 136.44 support. But strong support could be seen at 50% retracement of 122.36 to 148.42 at 135.39 to bring rebound. Above 142.79 will turn bias back to the upside for 144.77 and above.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern with a test on 122.36 low next. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement at 167.78.

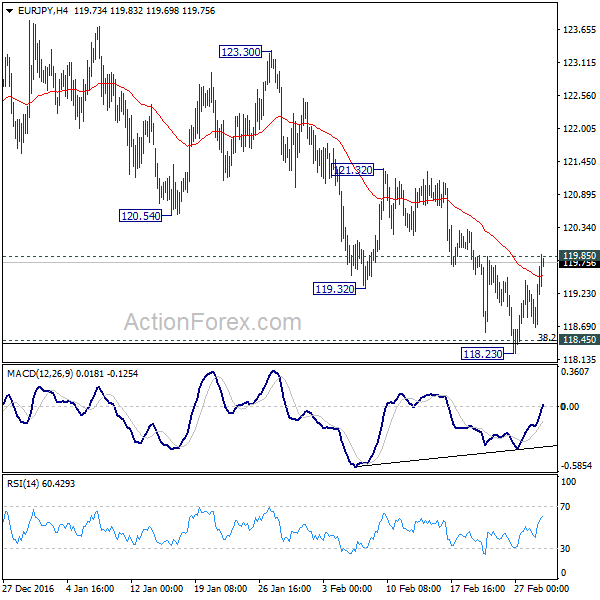

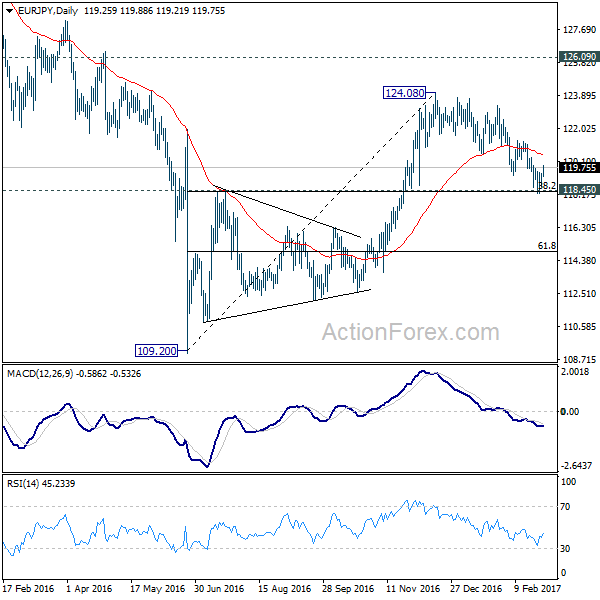

EUR/JPY Daily Outlook

Daily Pivots: (S1) 118.79; (P) 119.09; (R1) 119.51; More...

EUR/JPY's rebound and breach of 119.85 minor resistance argue that a short term bottom is formed at 118.23, on bullish convergence condition in 4 hour MACD. The development also argue that it has defended 118.45 cluster support (38.2% retracement of 109.20 to 124.08 at 118.39). Intraday bias is back on the upside for 121.31 resistance. Break will indicate completion of whole corrective fall from 124.08 and turn near term outlook bullish for this resistance. On the downside sustained break of 118.39/45 will argue that whole rise from 109.20 has completed and turn outlook bearish for 61.8% retracement at 114.88 and below.

In the bigger picture, price actions from 109.20 medium term bottom are seen as part of a medium term corrective pattern from 149.76. There is prospect of another rise towards 126.09 key resistance level before completion. But even in that case, we'd expect strong resistance between 126.09 and 141.04 to limit upside, at least on first attempt. Nonetheless, decisive break of 118.45 cluster support (38.2% retracement of 109.20 to 124.08 at 118.39) will argue that rise from 109.20 is completed and turn outlook bearish for 61.8% retracement at 114.88 and below.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

US PCE Core Inflation For January Is Due To Be Released Today

Market movers today

US PCE core inflation for January is due to be released today. PCE inflation has been quite flat at around 1.7% since August with no clear trend. We estimate PCE core was 0.25% m/ m and 1.7% y/y in January. The release will be particularly interesting in light of the recent repricing of the probability of a hike at the coming March meeting – now at 70%.

US ISM manufacturing for February is also due out today. The preliminary manufacturing PMI showed a small decline and the same may be true for ISM given that ISM has recently been a bit higher than PMI. However, regional PMIs have been quite strong.

Today EIA will report on US crude stocks last week. Yesterday, API was said to report that stocks rose 2.5mb last week. Hence, the market will be positioned for a similar rise in the official numbers from EIA.

In Scandies, we expect the Norwegian PMI for February to confirm the tendency for gradual improvement in manufacturing. The market will also focus on Riksbank Minutes.

Selected market news

US President Trump failed to deliver much new information on his policies at his speech to the Congress yesterday. He reiterated some of the key parts of this economic programme, e.g. his plans on spending USD1tn on public infrastructure and taxing imports. He also mentioned intensions of lowering taxes for persons and corporations. He did not provide much further details than what has already been presented. In turn, the market reaction to the speech was relatively muted.

Instead two speeches from members of the Federal Reserve attracted more attention. Dudley (voter, dovish) said that the case for tightening has become ‘a lot more compelling' and that the ‘risks to the outlook are now starting to tilt to the upside'. Williams (non-voter, neutral) said that he expects the Fed to consider a March hike seriously. The hawkish comments sent US rates higher and EUR/USD lower.

Activity in the Chinese manufacturing sector continues to progress. February's manufacturing PMIs surprised on the upside. The official PMI rose to 51.6 from 51.3 and the Caixin PMI rose to 51.7 from 51.0. Both were expected to drop slightly.

Finally, API was said to report yesterday, that US crude stocks rose 2.5mb last week. It indicates that the upwards trend in US crude stocks continues despite recent production cuts from OPEC trying to force them lower.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.3732; (P) 1.3774; (R1) 1.3836; More...

Intraday bias in EUR/AUD remains neutral for the moment. At this point, we'd still expect strong support from 1.3671 to contain downside to complete the correction from 1.6587. This is supported by bullish convergence condition in 4 hour MACD. Break of 1.3900 resistance will confirm short term bottoming and turn bias back to the upside for 1.4289 resistance. However, sustained break of 1.3671 will invalidate our view.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. We'd expect strong support from 1.3671 key level to contain downside and bring rebound. Up trend from 1.1602 should not be finished and will resume later. Break of 1.4721 resistance will indicate completion of such correction and turn outlook bullish for retesting 1.6587 high. However, sustained break of 1.3671 will invalidate our bullish view and would turn focus back to 1.1602 long term bottom.

USD Surges As Markets Back March Fed Rate Hike

- Trump offers no new details on spending or tax after Dow breaks 12 day winning streak;

- Dudley and Williams strike hawkish tone sending March implied probability to 66%;

- USD boosted by March repricing while Gold falters at key resistance;

- Fed speeches and plenty of data releases to come today.

It should be quite a busy start to European trading on Wednesday, with investors having to absorb a lot of information from across the pond while at the same time manufacturing data from across Europe will come thick and fast throughout the morning.

All eyes were on Donald Trump's appearance before Congress on Tuesday evening as investors hoped the new President would shed some detail on the 'big' spending plans and 'phenomenal' tax reforms that have propelled equity markets in the US to record high levels. Unfortunately, despite Trump's more upbeat approach by his own standards, he once again stuck to his generic yet bold pledges which as of yet, don't appear to have disappointed investors too much.

While it's understandable that these things take time to plan and implement properly, markets have been way ahead of the game since Trump's victory and there comes a time when we need to know exactly what they're rallying on. It will be interesting to see what the lack of detail in Trump's address does to the rally's momentum, with the Dow having already snapped its 12 day winning streak ahead of the President's speech.

The markets are actually far more interested in what the US central bank had to say on Tuesday, with William Dudley and John Williams striking quite a hawkish tone and achieving something others, including Chair Janet Yellen, have failed to do, putting a March rate hike firmly on the table. Markets had previously not fully bought in, or come close for that matter, but with implied rate hike odds from Reuters now at 66% this month, it would appear these comments really struck a chord with investors.

Dudley – a permanent voter on the FOMC – claimed the case for tightening is now a lot more compelling, while Williams –who doesn't vote until next year – claimed a rate increase is up for 'serious consideration' at the meeting this month. The greenback has been boosted considerably by these comments and should the dollar index break through 101.75 on the back of them, we could finally see it regain its upward momentum. Gold naturally suffered following these comments after earlier in the week failing to hold above $1,260, a move that could have propelled it back towards $1,300.

There's plenty of action still to come today including manufacturing PMIs throughout the morning from around Europe – which follows two strong manufacturing PMIs from China overnight – as well as income, spending, inflation and manufacturing data from the US. The Fed will remain in focus as we hear from Robert Kaplan and Lael Brainard – both FOMC voters – and we'll also get oil inventory data from EIA.

EUR/GBP Daily Outlook

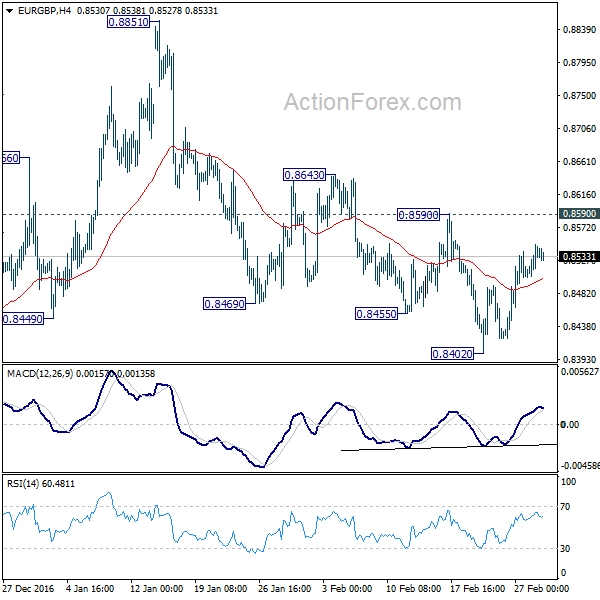

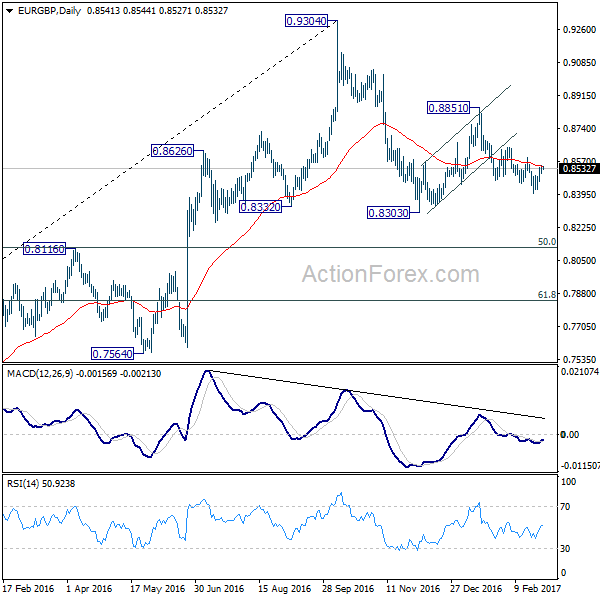

Daily Pivots: (S1) 0.8511; (P) 0.8530; (R1) 0.8560; More...

Intraday bias in EUR/GBP remains neutral for the moment. With 0.8590 resistance intact, we're holding on to our bearish view. That is, fall from 0.8851 is the third leg of the whole corrective pattern from 0.9304. Below 0.8402 will turn bias to the downside for 0.8303 first. Break will confirm our bearish view and target 0.8116 key cluster support level. However, on the upside, break of 0.8590 resistance will dampen our view and turn bias back to the upside.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).

US Dollar Regains Control And Starts Bullish Wave-3

Currency pair EUR/USD

The EUR/USD broke the support trend line (dotted blue). A break below the previous bottom (green line) indicates that wave 2 (purple) has most likely been completed. A bullish bounce at the support level could extend the correction within wave 2.

The EUR/USD is probably building an ABC (green) zigzag correction unless price manages to break the support and 127.2% Fibonacci target. In that case the wave formation is probably a 123 rather than an ABC (green) within larger waves 3 of the 4 hour chart.

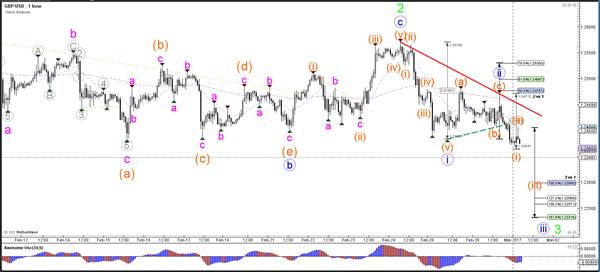

Currency pair GBP/USD

The GBP/USD showed a bearish breakout below support (dotted blue), which could see price start a wave 3 (blue/green). Price needs to reach the 161.8% Fibonacci target to confirm a wave 3 (blue).

The GBP/USD completed an ABC (orange) zigzag correction and broke below the support trend line (dotted green). There could be 5 wave (orange) within wave 3 (blue) if price reaches beyond the 138.2% Fibonacci target.

Currency pair USD/JPY

The USD/JPY challenged the bottom of wave 1 (blue line) and invalidation point of the wave structure but did not break below it. The wave 1-2 (blue) therefore is still valid. Price has broken above the resistance (orange line), which could indicate that the bearish correction has been completed.

The USD/JPY has broken above the resistance (orange line), which could indicate that the bearish correction has been completed.

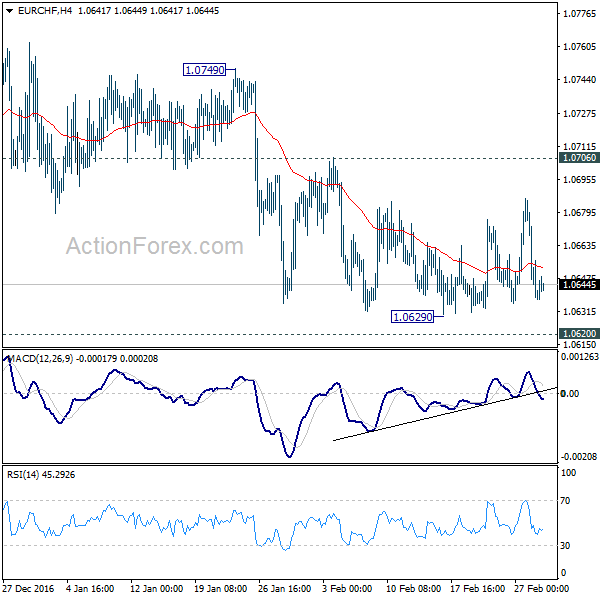

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0622; (P) 1.0653; (R1) 1.0669; More...

EUR/CHF's recovery was limited well below 1.0706 resistance and weakened again. Nonetheless, it's staying in range of 1.0629/0706. Intraday bias remains neutral for the moment. As 1.0706 resistance stays intact, deeper decline is still expected in the cross. Firm break of 1.0620 key support level will extend the larger decline from 1.1198 to 1.0485 fibonacci level. However, break of 1.0706 resistance will indicate short term bottoming and turn bias back to the upside. Further break of 1.0749 resistance will raise the chance of medium reversal.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Such correction is still in progress. Sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485. On the upside, break of 1.0897 resistance is needed to confirm completion of such fall. Otherwise, outlook will stay bearish.

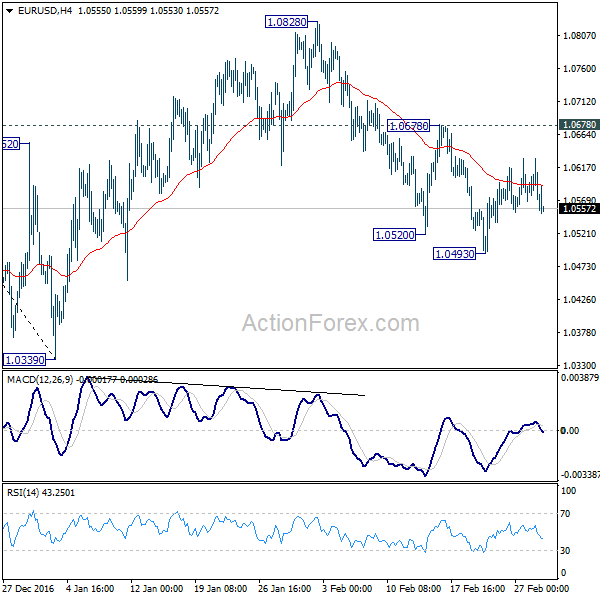

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0550; (P) 1.0590 (R1) 1.0616; More.....

EUR/USD dips mildly today but stays above 1.0493 temporary low so far. Intraday bias remains neutral for the moment. With 1.0678 minor resistance intact, deeper decline is still expected. We're viewing fall from 1.0828 as resuming the larger down trend. Below 1.0493 will target 1.0339 low first. Break will confirm our bearish view and target parity. However, break of 1.0678 will dampen our view and turn focus back to 1.0828 resistance instead.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.