Sample Category Title

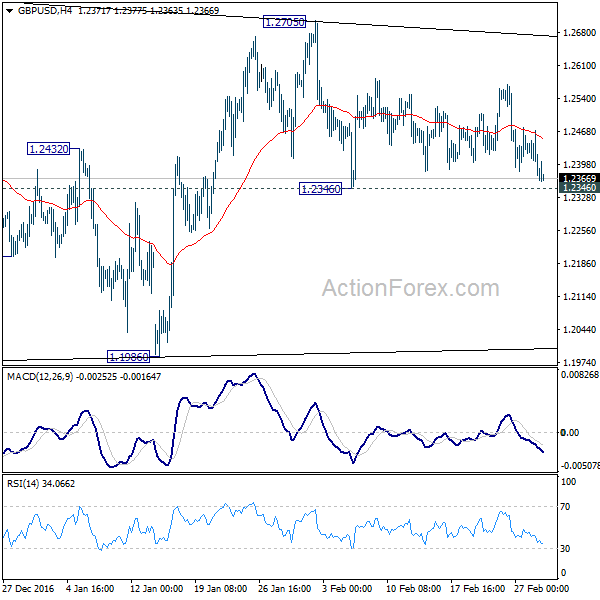

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2345; (P) 1.2408; (R1) 1.2442; More...

GBP/USD dips mildly today but stays above 1.2346 minor support. Intraday bias remains neutral for the moment and outlook is unchanged. Price actions from 1.1946 are viewed as a consolidation pattern, with rise from 1.1986 as the third leg. In case of another rise, we'd expect upside to be limited by 1.2774 to bring larger down trend resumption. On the downside, below 1.2346 will revive the case that such consolidation is completed at 1.2705 already. In that case, intraday bias will turn back to the downside for retesting 1.1946 low.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

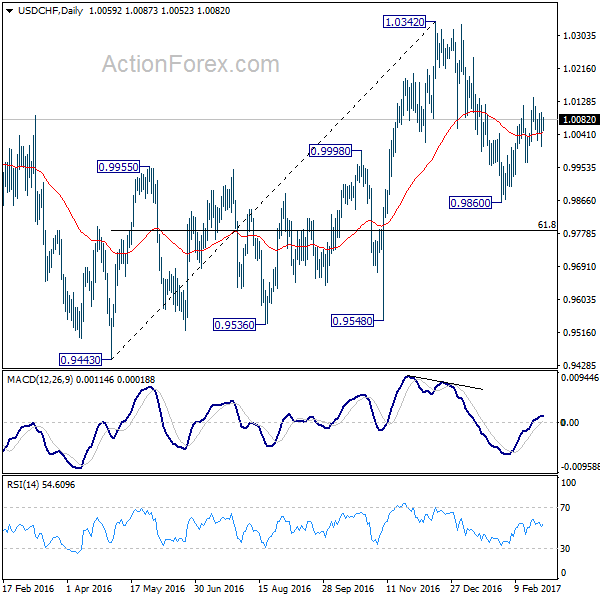

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0011; (P) 1.0056; (R1) 1.0102; More.....

USD/CHF recovers mildly today but stays in range of 0.9966/1.0140. Intraday bias remains neutral for the moment. With 0.9966 support intact, further rise is in favor. Above 1.0140 will turn bias to the upside and target a test on 1.0342 resistance. Based on neutral medium term outlook, we'd be cautious on topping at around 1.0342. Meanwhile, break of 0.9966 will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

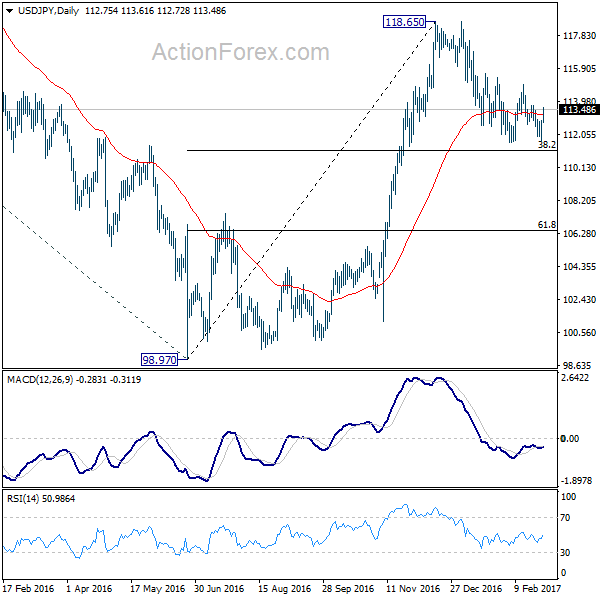

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.99; (P) 112.44; (R1) 113.20; More...

USD/JPY rebounded ahead of 111.58 after forming a temporary low at 111.68. But it's still staying in range of 111.58/114.94. Intraday bias continues to remain neutral. The corrective fall from 1118.65 could extend lower. But we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound. On the upside, above 114.94 resistance should confirm completion of pull back from 118.65. In such case, intraday bias will be turned back to the upside for retesting 118.65.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

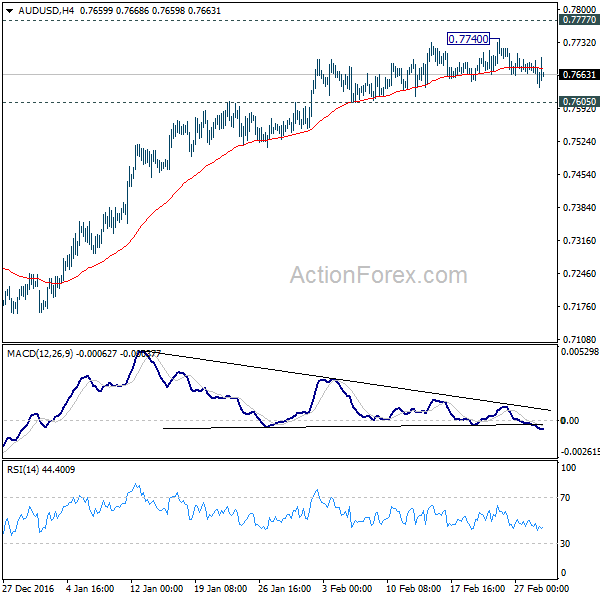

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7636; (P) 0.7665; (R1) 0.7684; More...

AUD/USD weakens mildly today but stays in range of 0.7605/7740. Intraday bias is still neutral at this point. Another rise cannot be ruled out. However, considering bearish divergence condition in 4 hour MACD, upside should be limited by 0.7777/7833 resistance zone and bring near term reversal. On the downside, break of 0.7605 support will indicate that rise from 0.7158 has completed already and turn bias back to the downside for 55 day EMA (now at 0.7566) first.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8186) and above.

European Open Briefing

Global Markets:

- Asian stock markets: Nikkei up 1.40 %, Shanghai Composite gained 0.40 %, hang Seng rose 0.30 %, ASX 200 down 0.30 %

- Commodities: Gold at $1243 (-0.90 %), Silver at $18.30 (-0.90 %), WTI Oil at $54.10 (+0.20 %), Brent Oil at $56.65 (+0.25 %)

- Rates: US 10-year yield at 2.42, UK 10-year yield at 1.15, German 10-year yield at 0.21

News & Data:

- Australia GDP Q4 (QoQ) 1.1% (prev -0.50%)

- Australia GDP Q4 (YoY) 2.4% (prev 1.80%)

- China Non-Manufacturing PMI Feb 54.2 (prev 54.6)

- China Manufacturing PMI Feb 51.6 (prev 51.3)

- China Caixin Manufacturing PMI Feb 51.7 (prev 51.0)

- Japan Manufacturing PMI Feb 53.3 (prev 53.5)

- Australia AIG Manufacturing Index Feb: 59.3 (prev 51.2)

- South Korea Trade Balance (USD) Feb 7223m (prev 3196m)

- Fed's Dudley: Case for hikes is becoming more compelling

- Fed's Williams: Raising rates sooner leaves room for more rate hikes this year if needed

- Fed's Bullard: Fed closer to achieving goals today more than anytime in last 60 years

Markets Update:

The US Dollar came under pressure during the speech by US President Trump, but resumed its rally as the market switched its focus back to the hawkish comments by several Fed members. Trump failed to deliver details about his planned economic plan, but there was not much of a reaction in the stock market. S&P 500 futures were only slightly lower, and most of the Asian indices are up on the day.

Meanwhile, the Dollar remains strong as the market sees a rate hike this month as possible. EUR/USD fell from 1.0590 back to 1.0550, and USD/JPY rallied to a high of 113.60 so far. USD/CAD had a significant rally as well. The pair rose from 1.3160 in yesterday's early NY session to a high of 1.3310 and extended gains to 1.3325 in Asia. If the focus remains on the Fed instead of Trump, the Dollar could rise further.

The Australian Dollar fell slightly amid the broad USD strength, but less than its peers. GDP data was strong and beat expectations, which supported the currency.

Upcoming Events:

- 08:45 GMT – Italian Manufacturing PMI

- 08:50 GMT – French Manufacturing PMI

- 08:55 GMT – German Manufacturing PMI

- 08:55 GMT – German Unemployment Change

- 08:55 GMT – German Unemployment Rate

- 09:00 GMT – Euro Zone Manufacturing PMI

- 09:30 GMT – UK Manufacturing PMI

- 13:00 GMT – German CPI

- 13:30 GMT – US Core PCE Price Index

- 13:30 GMT – US Personal Income

- 13:30 GMT – US Personal Spending

- 13:30 GMT – Canadian Current Account

- 14:45 GMT – US Manufacturing PMI

- 15:00 GMT – US ISM Manufacturing PMI

- 15:00 GMT – Bank of Canada Interest Rate Decision

- 15:30 GMT – US Crude Oil Inventories

- 18:00 GMT – FOMC Member Kaplan speaks

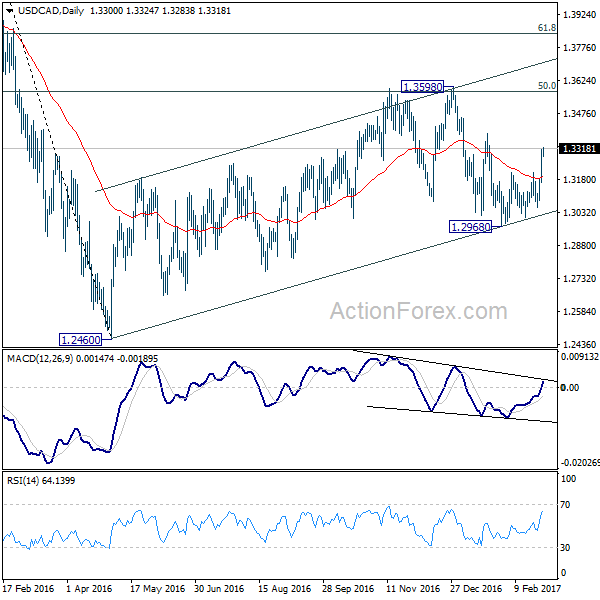

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3204; (P) 1.3259; (R1) 1.3354; More...

USD/CAD's strong rally and break of 1.3211 resistance indicates resumption of rebound from 1.2968. Also, it should confirm completion of pull back from 1.3598. Intraday bias is now back on the upside for 1.3598 first. Break will extend the larger rally from 1.2460 towards next fibonacci level at 1.3838. On the downside, though, below 1.3164 minor support will turn bias back to the downside for 1.2968 support instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Dollar Lifted by Trump Optimism and Fed Speculations

Dollar strengthens broadly as markets took US president Donald Trump's address to Congress positively. Dollar index is back at 101.60, comparing to yesterday's low at 100.78 and is having key near term resistance at 101.79 in sight. Strength in greenback is most notable against Canadian Dollar, which was dragged down by oil price yesterday. On the other hand, the Japanese Yen is sold off broadly today on return to risk appetite. Asian indices are generally higher with Nikkei gaining nearly 1.5% at the time of writing. Focus will now turn to economic data from you, including personal income and spending, and ISM manufacturing, to solidify the strength in Dollar's rebound.

No extreme comments from Trump

While Trump's State of the Union address sent little details to the markets, the positive tone was taken well by traders. And possibly more importantly, there were no extreme comments that unnerved traders. On tax reform, Trump noted that his team "is developing historic tax reform that will reduce the tax rate on our companies so they can compete and thrive anywhere and with anyone" and would also "provide massive tax relief for the middle class". He did not specify the controversial border adjustment tax in his speech.

Trump criticized Obamacare, suggesting that "mandating every American to buy government-approved health insurance was never the right solution for America". His administration is planning to "lower the cost of health insurance" instead. Trump also reiterated the proposed infrastructural spending worth of as much as USD 1T. According to the Trump, "to launch our national rebuilding, I will be asking the Congress to approve legislation that produces a USD 1T investment in the infrastructure of the United States, financed through both public and private capital, creating millions of new jobs".

March Fed hike speculations heat up

On the markets, the speculation for a March Fed hike is getting heat up again. San Francisco Fed president John Williams said he expected a rate hike to get "serious consideration" during the March 14-15 meeting in Washington. And he also noted that there was no need to delay the move. New York Fed president William Dudley said that the case for rate hike "has become a lot more compelling" with recent economic data. According to Bloomberg's rate tool, markets are pricing in more than 70% chance of a hike this month, doubling last week's pricing.

BoJ cut short debt purchases

In Japan, BoJ lowered the purchase of short-maturity debt, one to three years" to JPY 320b, down from JPY 400b in its previous operation on February. Purchases of three to five year debts were also lowered to JPY 400b, down from JPY 420b. Analysts saw that as a move to fine tune the yield curve control. Meanwhile, BoJ governor Haruhiko asked investors not to read too much into daily operations. BoJ board member Takehiro Sato urged the central bank to be flexible in the yield targets. He noted that "it is appropriate to flexibly adjust" the BOJ's yield curve targets if market long-term interest rates rise reflecting improvements in the economy and price outlook.

BoC and PMIs to highlight the day

On the data front, Australia GDP grew 1.1% qoq in Q4, above expectation of 0.7% qoq. New Zealand terms of trade rose 5.7% qoq in Q4. Japan capital spending rose 3.8% in Q4. China PMI manufacturing improved to 51.6 in February, non-manufacturing PMI dropped to 54.2. Caixin PMI manufacturing rose to 51.7.

PMI data will be one of the focuses today. Swiss will release SVME PMI and UBS consumption indicator. Eurozone will release PMI manufacturing final and German CPI flash. UK will release PMI manufacturing, mortgage approvals and M4. US will release personal income and spending, ISM manufacturing and construction spending. Fed will also release Beige Book report. BoC will announce rate decision and is widely expected to stand pat.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3204; (P) 1.3259; (R1) 1.3354; More...

USD/CAD's strong rally and break of 1.3211 resistance indicates resumption of rebound from 1.2968. Also, it should confirm completion of pull back from 1.3598. Intraday bias is now back on the upside for 1.3598 first. Break will extend the larger rally from 1.2460 towards next fibonacci level at 1.3838. On the downside, though, below 1.3164 minor support will turn bias back to the downside for 1.2968 support instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q/Q Q4 | 5.70% | 4.00% | -1.80% | -1.10% |

| 23:50 | JPY | Capital Spending Q4 | 3.80% | 0.60% | -1.30% | |

| 0:01 | GBP | BRC Shop Price Index Y/Y Feb | -1.00% | -1.40% | -1.70% | |

| 0:30 | AUD | GDP Q/Q Q4 | 1.10% | 0.70% | -0.50% | |

| 1:00 | CNY | Manufacturing PMI Feb | 51.6 | 51.2 | 51.3 | |

| 1:00 | CNY | Non-manufacturing PMI Feb | 54.2 | 54.6 | ||

| 1:45 | CNY | Caixin PMI Manufacturing Feb | 51.7 | 50.8 | 51 | |

| 7:00 | CHF | UBS Consumption Indicator Jan | 1.5 | 1.5 | ||

| 8:30 | CHF | SVME PMI Feb | 55.5 | 54.6 | ||

| 8:45 | EUR | Italy Manufacturing PMI Feb | 53.5 | 53 | ||

| 8:50 | EUR | France Manufacturing PMI Feb F | 52.3 | 52.3 | ||

| 8:55 | EUR | Germany Manufacturing PMI Feb F | 57 | 57 | ||

| 8:55 | EUR | German Unemployment Change Feb | -10k | -26k | ||

| 8:55 | EUR | German Unemployment Rate Feb | 5.90% | 5.90% | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Feb F | 55.5 | 55.5 | ||

| 9:30 | GBP | PMI Manufacturing Feb | 55.7 | 55.9 | ||

| 9:30 | GBP | Mortgage Approvals Jan | 68.5k | 67.9k | ||

| 9:30 | GBP | M4 Money Supply M/M Jan | -0.50% | |||

| 13:00 | EUR | German CPI M/M Feb P | 0.60% | -0.60% | ||

| 13:00 | EUR | German CPI Y/Y Feb P | 2.10% | 1.90% | ||

| 13:30 | USD | Personal Income Jan | 0.30% | 0.30% | ||

| 13:30 | USD | Personal Spending Jan | 0.30% | 0.50% | ||

| 13:30 | USD | PCE Deflator M/M Jan | 0.50% | 0.20% | ||

| 13:30 | USD | PCE Deflator Y/Y Jan | 2.00% | 1.60% | ||

| 13:30 | USD | PCE Core M/M Jan | 0.30% | 0.10% | ||

| 13:30 | USD | PCE Core Y/Y Jan | 1.80% | 1.70% | ||

| 15:00 | CAD | BoC Rate Decision | 0.50% | 0.50% | ||

| 15:00 | USD | ISM Manufacturing Feb | 56 | 56 | ||

| 15:00 | USD | ISM Prices Paid Feb | 68 | 69 | ||

| 15:00 | USD | Construction Spending M/M Jan | 0.60% | -0.20% | ||

| 15:30 | USD | Crude Oil Inventories | 0.6M | |||

| 19:00 | USD | Fed Beige Book |

Is The U.S. Federal Reserve Preparing To Hike Rates?

Key Points:

- Federal Reserve has largely achieved their dual mandate.

- Inflationary pressures rising within U.S. domestic economy.

- March FOMC meeting likely to be a `live' event.

The past week has seen an uptick in hawkish rhetoric from a range of US Federal Reserve members suggesting that the central bank could be preparing us all for the start of a cycle of tightening. In particular, the Fed's Williams and Harker have been front and centre in the veritable public relations blitz, suggesting that the FFR has been 'abnormally' low for too long. Therefore, there is a real chance the March FOMC meeting could be a live one. However, let's take a look at the underlying economic data that could be used to support a rate hike.

The US labour market has continued to strengthen throughout the past six months with the current headline rate reaching 4.6% in December. This level of unemployment is effectively below the natural rate and should be something that the central bank looks to when assessing the growing risk of inflation.

In addition, the US average hourly earnings metric has continued to strengthen over much of the last year. This is likely another metric that the central bank will take serious consideration of as they attempt to get ahead of any potential inflationary pressures within the economy.

Inflation has also been on the march within the domestic economy with the latest figure from February, 2017, showing a gain exceeding forecasts, of 2.5%. Subsequently, there is a definite trend within the available data showing an upward move of inflation that isn't looking like abating any time soon. In fact, much of 2016 showed solid gains in headline inflation which has placed additional pressure on the Fed to act on rates.

Subsequently, it would appear that the central bank has largely met their dual mandates of full employment and stable price inflation. However, the latter could be at risk in the medium term if the Federal Funds Rate (FFR) remains at the historically low level further stimulating the economy. Although there has been some relatively robust debate on whether to raise the expected range for inflation in the medium term there is little support for headline rates above 3.0%.

It would therefore appear that there is a mounting case for the FOMC to act on rates in March given that the vast majority of indicators that support their mandate have been fulfilled. The question must be asked that if the current economic environment is not conducive to rate rises…when will it be. Ultimately, the Federal Reserve is highly likely to raise rates by 25bps in March given the underlying inflationary pressure evident within the economy. Subsequently, it makes sense to consider the March event a live meeting and to position accordingly.

The Dollar-Yen Downtrend Could Be Over

Key Points:

- Recent downtrend could be about to end.

- 100 day EMA continues to push the pair higher.

- Rally could see the 115 handle challenged again.

The Dollar-Yen looks like it is on a cruise course to break free of its medium-term downtrend in the near future. Specifically, the pair is fast running out of room to consolidate unless it finally crosses back below the 100 day moving average. However, given a number of other technical readings, resistance is looking significantly weaker than support at this point.

First and foremost, it's important to take a look at that declining trend line a little more closely. Notably, it has proven rather resistant to attempts to push higher recently which would generally, and quite rightly, suggest that a reversal is now on the way. However, unlike previous attempts at breaking the trend, we don't have much in the way of resistance other than the trend line itself.

Whilst it is true that the 28.6% Fibonacci retracement will be capping upsides somewhat, this is about the only additional source of resistance currently present on the daily chart. Specifically, the RSI and Stochastics are both neutral which leaves the pair with plenty of gains to claim before risking moving into overbought territory.

Conversely, support is highly robust and this should force the USDJPY to move higher as its consolidation phase comes to an end. As is made clear above, the 100 day EMA continues to be a source of dynamic resistance and we can even see a loose double bottom forming up. Moreover, the current zone of support around the 111.59 mark has been a local trough three times in as many months.

Setting these readings aside, the price action seen since the Dollar-Yen began its decline would typically result in a breakout to the upside eventually. More precisely, a falling wedge is becoming quite obvious now and its end is nearly in sight. As a result, the air could move as high as the 115.00 mark within the next few sessions.

Ultimately, we will just have to wait and see if the pair can muster the strength to reverse its recent downtrend. However, as discussed above, the technicals definitely seem to suggest that we can see that trend line broken. Although, as always, keep an eye on the fundamental side of things which could upset the forecast, especially as we assess the aftermath of Trump's address.

Trump Blows Trumpet But Is Light On Detail (Again)

President Trump's address was high on rhetoric and light on detail, leaving the market underwhelmed.

The address to Congress was released a good hour before the main event this morning. Mr Trump followed it word for word with no surprises or add-ons leaving the street (and myself) with the feeling of being underwhelmed. Again the President was high on policy and rhetoric and light on details. Given the legislative agenda, the Houses of Congress are going to be very busy indeed over the next six months getting it all done. I suspect though that most of what has been announced are already built into the price of the USD today.

The S+P, Dow and Nasdaq are unchanged with the USD drifting ever so slightly higher against most of the majors as I guess it has become a case of no news is ever so slightly good news. Attention will now turn to Fed Chair Yellen's speech on Friday which should have more impact if she is hawkish. Over the last ten days, a plethora of other Governor's have been upbeat and hawkish, and a follow-on by Mrs Yellen would put March's FOMC unexpectedly “live.” This would almost certainly lead to another bout of USD strength.

Looking around the G-10 space today post-speech,

EUR/USD

Sitting at the session lows at 1.0555 as it continues it drift lower from New York. Euro has support at 1.0550 and 1.0530 with critical support at 1.0495.

Resistance is at 1.0590 and then stronger at 1.0630. Euro continues to drift aimlessly to the nuances of the USD as French political worries recede. (for now)

USD/JPY

Had rallied in New York as bond yields firmed and Trump's tax plans circulated. There is definitely a hint of a short squeeze here as well as traders had nervously eyed key long-term support around 111.50 in the previous sessions.

USD/JPY sits at the top of its range in Asia this morning with resistance at 113.80 initially. Support appears at 112.75 intra-day.

GBP/USD

As Brexit D-Day approaches, GBP has remained capped on any rally towards the 1.2600 level. Today's speech won't affect that dynamic. GBP is trading 1.2370 at the moment with support at 1.2345 and then the 1.2250 area.

AUD/USD

Completely ignored the speech to remain around 7670 this morning. It has even shrugged off better than expected GDP this morning at +2.4% YoY as the resource rally digs Australia out of the hole.

Aud continues to be firmly anchored in the 7600/7740 range it has traded in all of February. Intra-day resistance lies at 7700. Bring a good book to read.

USD/CNH

Ignored better than expected Manufacturing PMI's as general USD strength sees the pair trade to the top of its range at 6.8650. Yellen's speech and the trajectory of U.S. interest rates seem likely to have a far greater effect on the CNH and EMFX in general then Mr.Trump for now.

USD/CNH remains mired in its 2-week range of 6.8400 to 6.8700 with eyes turned to Friday now to break the deadlock.

GOLD

The USD strength has weakened the hands of Gold bulls. A reduction in the levels of perceived risk around the world and the very extended speculative long positioning sees Gold eyeing support at 1242. A move through here could see more stop-loss selling emerge with the next support at the 1236 area on the short term charts.

Resistance intra-day is at the 1248 area.

Summary

Mr Trump's highly anticipated speech was a highly scripted damp squib in the end. No news was good news, and this sees the USD slightly bid in Asia although, with so much built into the price, the longevity of the move into Europe is perhaps doubtful.

The highlight of the week now becomes Chair Yellen's speech on Friday for signals as to whether March's discounted FOMC meeting is in fact “live.”