Sample Category Title

Sunset Market Commentary

Markets

News agency Reuters reported just before the start of European trading that Russian President Putin would be open to talks on a ceasefire deal in Ukraine with the US. He wants a carve-up of four regions in the south—east of Ukraine that Russia annexed in 2022, but doesn’t fully control. It caused a positive start on stock markets, rebounding somewhat after yesterday’s geopolitical escalation (Putin’s signing of updated nuclear doctrine). Ukrainian President Zelensky reiterated in response that his country won’t make concessions on sovereignty or territory. Main European equity indices currently gain around 0.50%. Hotter-than-expected October UK CPI data served as a reminder that the government’s fiscal booster severely ties the Bank of England’s hands. Headline inflation rose by 0.6% M/M to 2.3% Y/Y (from 1.7%). Core CPI accelerated to 0.4% M/M (3.3% Y/Y from 3.2%). Goods prices rose by 0.8% M/M (-0.3% Y/Y from -1.4%) and services costs by 0.4% M/M (5% Y/Y from 4.9%). UK money markets barely discount a cumulative 50 bps of additional rate cuts over the next 9 months. UK Gilts sell-off today, but do so in a bearish steepening instead of flattening fashion. UK yields add 1.2 bps (2-yr) to 7.1 bps (30-yr). Sterling is slightly stronger at EUR/GBP 0.8330. The ECB’s Q3 negotiated wage data were today’s sole other date point of interest. Wage growth accelerated from 3.5% Y/Y in Q2 to an EMU record high of 5.4% driven by a 8.8% increase in Germany (quickest since 1993). Wage inflation adds to stronger-than-expected Q3 GDP growth and more sticky price pressures in October. Investors continue reducing 50 bps rate cut bets by the ECB at its December policy meeting. ECB vice-president de Guindos confirmed that prudence is needed. Current projections don’t show a risk of undershooting the 2% inflation target. The impact on the overall European bond market could have been possible bigger if it weren’t for the lingering geopolitical event risk. Ukraine now also firing UK long term missiles (Storm Shadow) is a point in case. German yields add 2.9 bps (2-yr) to 4.3 bps (10-yr). EUR/USD dips from 1.06 to 1.0550.

The Flemish Community today tapped its outstanding 3.125% Jun2034 benchmark for €1bn (books above €8.3bn). The deal was prices at 24 bps over the Belgian OLO curve (vs guidance at OLO+28 bps area). Flandres now raised €3.75bn YTD via regular benchmarks, the upper end of the targeted €3.25-3.75bn in its funding plan. A sustainable benchmark (€1.25bn raised vs €1.25-1.50bn target) and €0.25bn in EIB funding (target) are this year’s other long term funding sources so far. No private placements (€0.75-1bn) have been done so far. The total amount raised (€5.25bn) compares with a €6.55bn target. Next year, Flanders is looking at around €5bn in new long-term funding.

News & Views

The ECB in its biannual Financial Stability Review highlighted several risks including “rising global trade tensions and a possible further strengthening of protectionist tendencies”. With economic growth now a bigger threat than inflation, the ECB is worried that trade developments may have an adverse impact on (global) growth, inflation and asset prices. Against the backdrop of already tepid growth, it is markedly more explicit about the bloc’s fiscal risks. The ECB pointed to “elevated debt levels and high budget deficits”. In an echo to the sovereign debt crisis around 12 years ago, the ECB mentioned a potential resurgence of market concerns over debt sustainability. The combination of low growth and high government debt makes it more difficult to address other pressing matters such as defense spending and climate-related investments, the central bank said. Other concerns the ECB mentions include high borrowing costs and weak growth dragging on corporate balance sheets, as well as credit risks for SME’s and lower-income households. In a context of “elevated macro-financial and geopolitical uncertainty” a warning was issued for a sudden sharp reversal in certain market segments given high asset valuations.

French far-right leader Le Pen today threatened to topple PM Barnier’s coalition government if her party’s cost-of-living concerns were not addressed by the 2025 budget. She told RTL radio that if the government crosses this “red line”, the Rassemblement National will vote no-confidence. Le Pen said that RN opposes increasing the tax burden on households, entrepreneurs or pensioners and that so far these demands were not reflected. Barnier’s coalition is a fragile one after snap parliamentary elections last summer didn’t produce an absolute majority for any party. The far-left tabled a vote of no-confidence already earlier this year but that failed since it lacked the support of RN. Since the elections, France’s credit risk premium has risen to surpass the one for Belgium, Portugal and Spain.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.70; (P) 154.25; (R1) 155.21; More...

Intraday bias in USD/JPY remains mildly on the upside for retesting 156.74. Firm break there will resume the whole rally from 139.57 towards 161.94 high. On the downside, though, break of 153.27 will resume the correction towards 38.2% retracement of 139.57 to 156.74 at 150.18.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

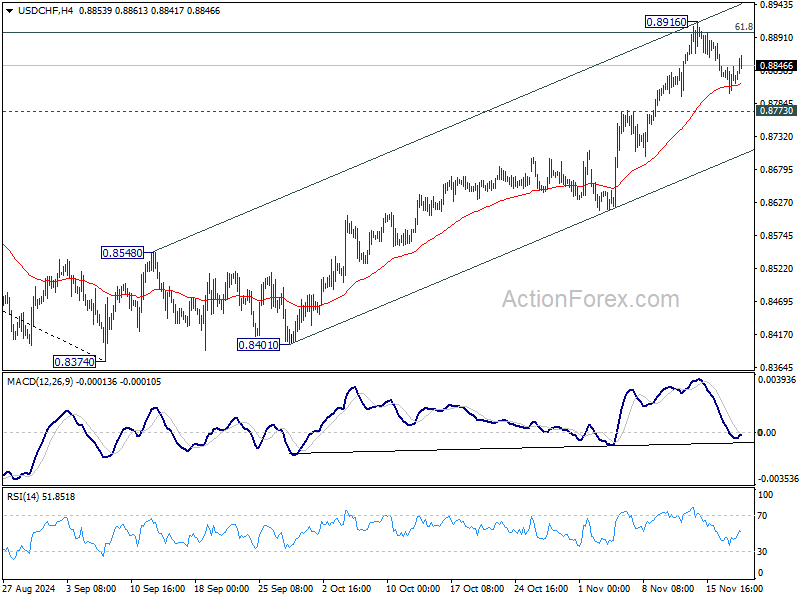

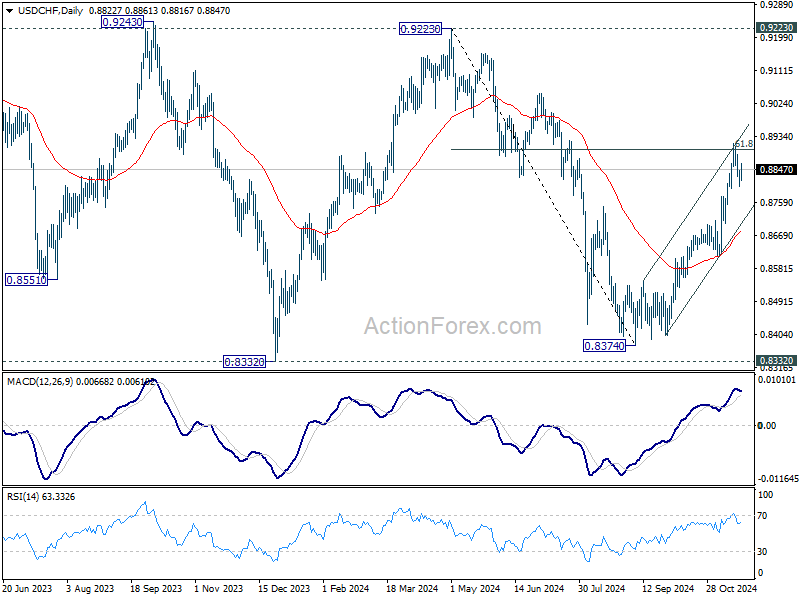

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8789; (P) 0.8836; (R1) 0.8870; More…

USD/CHF is staying in consolidations below 0.8916 and intraday bias remains neutral. Further rally is expected as long as 0.8773 resistance turned support holds. On the upside, break of 0.8916 and sustained trading above 61.8% retracement of 0.9223 to 0.8374 at 0.8899 will pave the way back to 0.9223 key resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

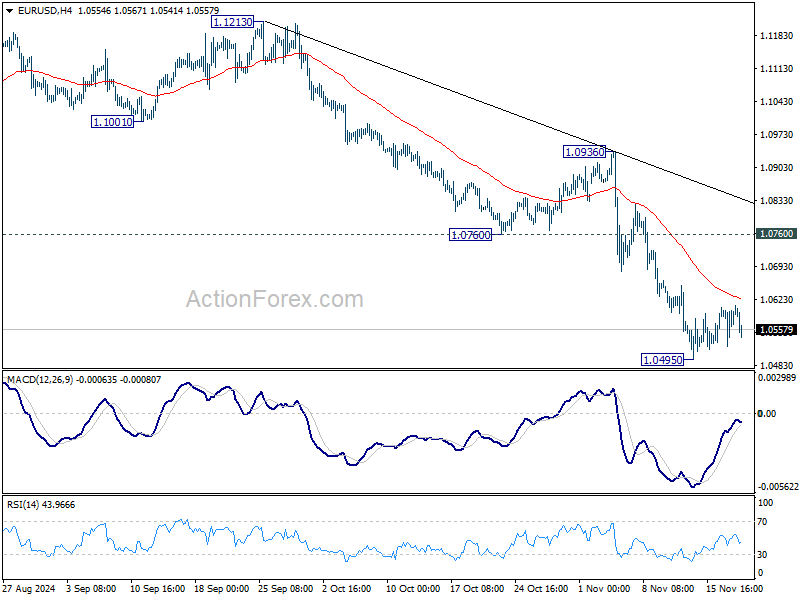

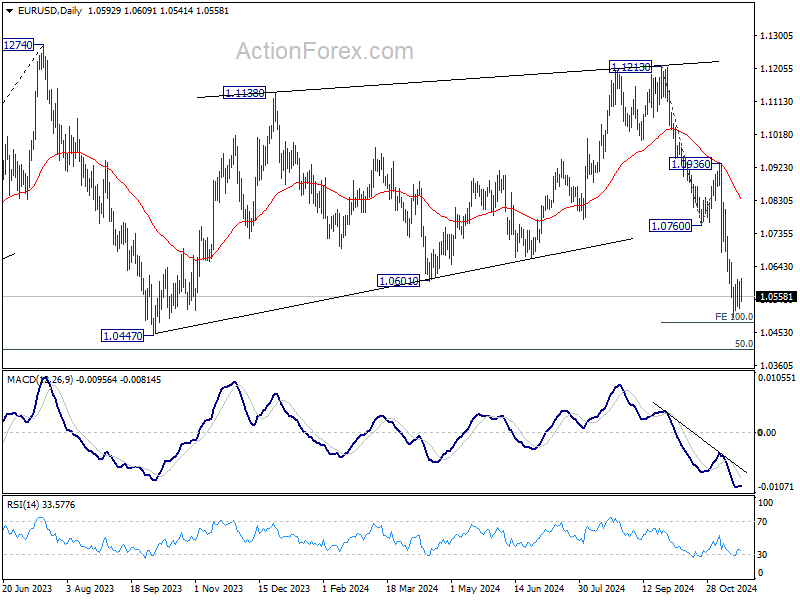

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0545; (P) 1.0574; (R1) 1.0625; More...

EUR/USD is still bounded in consolidations above 1.0495 temporary low and intraday bias remains neutral. Outlook stays bearish with 1.0760 support turned resistance intact. . On the downside, firm break of 1.0495 will resume the fall from 1.1213 to 1.0447 support and then 1.0404 key fibonacci level next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2634; (P) 1.2662; (R1) 1.2711; More...

GBP/USD's recovery extended higher today but lost momentum well ahead of 55 4H EMA. Intraday bias remains neutral at this point. Outlook stays bearish with 1.2842 support turned resistance intact. On the downside, break of 1.2596 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

Sterling Gains Slightly as UK Inflation Accelerates; Euro Struggles Despite Wage Surge

Sterling posted modest gains today after the UK reported stronger-than-expected rebound in headline inflation for October. More importantly, both core CPI and services price growth also increased, indicating that underlying inflation is gaining momentum.

This resurgence in inflation diminishes the likelihood of BoE implementing another rate cut in December. Market expectations have adjusted accordingly, with swaps markets now assigning only a 15% probability to a rate reduction next month. This shift aligns with BoE's recent emphasis on a measured and gradual approach to policy easing. The central bank has stressed the need for additional time to assess the impact of the Autumn Budget before making further monetary adjustments.

In contrast, Euro failed to gain traction despite robust wage growth data from the Eurozone. ECB reported that negotiated wages in the third quarter rose by 5.42% yoy, a significant jump from the 3.54% growth in the second quarter. This also marks the fastest wage growth since early 1993. However, Euro remained subdued as concerns over sluggish economic activity overshadowed the inflationary pressures from rising wages.

The ongoing weakness in the Eurozone's economic performance is expected to keep ECB on track for another 25b rate cut in December. While the central bank may proceed with this cut, the pace of easing next year is anticipated to slower as policymakers balance the need to support growth with the risks of fueling inflation.

Overall for the day, however, Dollar is the strongest one, followed by Sterling, and then Canadian. Yen is the worst, followed by Kiwi and then Aussie. Euro and Swiss Franc are mixed in the middle.

Technically, EUR/USD's recent decline from 1.1213 might be ready to resume through 1.0495 temporary low soon. But the main question is whether it could draw enough support from 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404 to bring near term bullish reversal. Decisive break of 1.0404, however, will raise the chance of reversal and target 61.8% retracement at 1.0199.

In Europe, at the time of writing, FTSE is up 0.17% DAX is up 0.44%. CAC is up 0.41%. UK 10-year yield is up 0.040 at 4.480. Germany 10-year yield is up 0.036 at 2.380. Earlier in Asia, Nikkei fell -0.16%. Hong Kong HSI rose 0.21%. China Shanghai SSE rose 0.66%. Singapore Strait Times fell -0.38%. Japan 10-year JGB yield rose 0.0044 to 1.069.

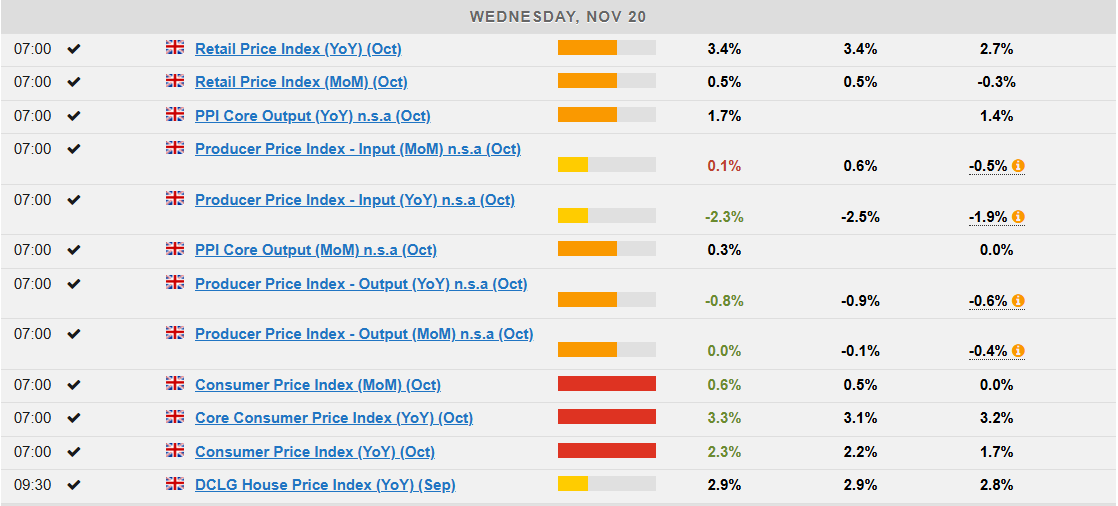

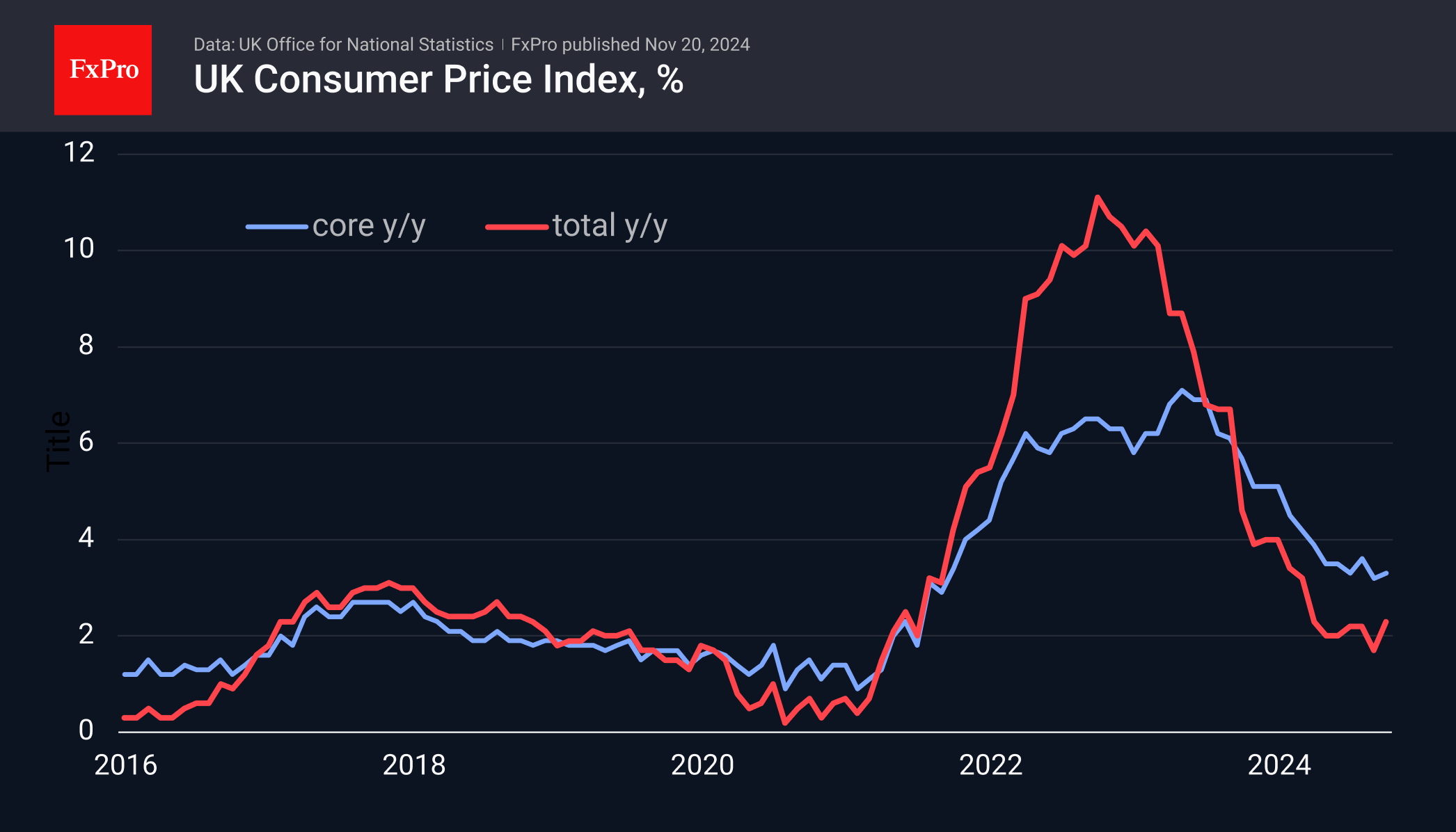

UK CPI jumps to 2.3% in Oct, core CPI rises to 3.3%

UK CPI reaccelerated from 1.7% yoy to 2.3% yoy, above expectation of 2.2% yoy. Core CPI (excluding energy, food, alcohol and tobacco) rose by 3.3% yoy, ticked up from prior month's 3.2% yoy and above expectation of 3.1% yoy.

CPI goods annual rate rose from -1.4% yoy to -0.3% yoy, while the CPI services annual rate rose from 4.9% yoy to 5.0% yoy.

On a monthly basis, CPI rose by 0.6% mom, above expectation of 0.5% mom.

Japan's exports rebound by 3.1% yoy in Oct, but trade deficit persists

Japan's exports rose 3.1% yoy in October, reaching JPY 9,427B, a strong recovery from the -1.7% yoy decline in September, which marked a 43-month low.

This rebound was primarily driven by a 1.5% yoy increase in shipments to China, buoyed by strong demand for chipmaking equipment. However, exports to the US, Japan's largest trading partner, fell -6.2% yoy, reflecting weakness in auto shipments.

On the import side, growth remained modest at 0.4% yoy, totaling JPY 9,888B. This resulted in a trade deficit of JPY -461B for the month, the fourth straight month of shortfall.

Seasonally adjusted data showed exports declining -0.7% mom to JPY 8,882B, while imports ticked up 0.2% mom to JPY 9,239B, leading to a seasonally adjusted trade deficit of JPY -358B.

Australia Westpac leading index hits 0.26%, decisive breakaway from year-long sluggishness

Australia's Westpac Leading Index moved decisively into positive territory in October, rising from -0.20% in September to +0.26%.

This marks a significant shift, as the index had been hovering in slight negative territory, between -0.3% and flat, for most of the past year. The October reading is not only the first clear above-trend result since November 2023 (+0.16%) but also the strongest since July 2022 (+0.63%).

The improvement in the index provides a "constructive signal" for the economy’s future momentum. Westpac’s outlook aligns with this shift, forecasting an acceleration in economic growth from a nadir of 1.0% in mid-2024 to 1.5% by year-end and 2.4% by the end of 2025.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2634; (P) 1.2662; (R1) 1.2711; More...

GBP/USD's recovery extended higher today but lost momentum well ahead of 55 4H EMA. Intraday bias remains neutral at this point. Outlook stays bearish with 1.2842 support turned resistance intact. On the downside, break of 1.2596 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

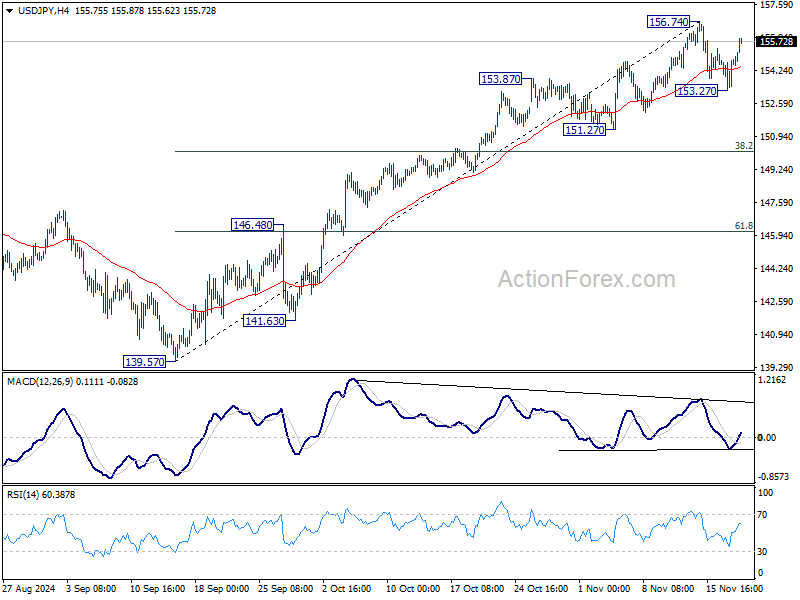

USD/JPY Outlook: Larger Bulls Returning to Play After Shallow Correction

USDJPY bounced on Wednesday, gaining 0.7% in Asian / European trading as immediate threats of stronger escalation of the war in Ukraine started to fade, while Trump trade continues to underpin dollar.

Fresh rally retraced almost 76.4% of shallow pullback (156.74/153.28), signaling that correction from new multi-month peak (156.74) might be over).

The notion is supported by Tuesday’s strong downside rejection which left long-tailed daily Doji candle and formed a bear trap under daily Tenkan-sen (154.44) which proved to be a solid support.

Daily Tenkan/Kijun-sen remain in bullish configuration and positive momentum is strong, adding to bullish scenario, in which violation of 156.67/74 (Fibo 76.4% of 161.95/139.57 / / Nov 15 high) would open way for further gains and unmask psychological 160 barrier.

Near-term bias is expected to remain firmly with bulls while the price stays above daily Tenkan-sen, guarding Tuesday’s spike low (153.28) and daily Kijun-sen (152.80).

Res: 156.00; 156.74; 157.86; 158.86.

Sup: 155.42; 154.44; 154.00; 153.28.

AUD/USD Consolidates After Recent Gains

The Australian dollar against the US dollar is currently experiencing a pause in its recent upward trajectory, stabilising around 0.6525 on the H4 chart. After three sessions of gains, the currency pair is undergoing a period of consolidation, likely preparing for a return to a stable ascending trend.

The slight retreat in the US dollar, driven by profit-taking after its rally and anticipation of new developments in the US Treasury under President Donald Trump, has influenced the performance of the AUD.

The minutes from the Reserve Bank of Australia's latest meeting highlight the bank's commitment to maintaining a restrictive monetary policy until inflation consistently approaches the target range. The RBA remains open to adjusting its policy stance in response to changing economic conditions, with market expectations leaning towards a potential rate cut in the coming months, with a 37% probability in February and 58% in April.

Technical analysis of AUD/USD

H4 chart: The AUD/USD pair is currently in a phase of correction following a downturn that saw the local decline target at 0.6440 reached. The market is forming a corrective wave towards 0.6543. If this correction is completed, a new downtrend towards 0.6380 is anticipated. The MACD indicator supports this bearish AUD/USD outlook, positioned below the zero line and poised to descend to new lows.

H1 chart: On the H1 chart, AUD/USD is approaching the correction target near 0.6543, forming a consolidation pattern just below this level. The breakout from this consolidation is expected to be downwards, initiating another phase of decline. The immediate target for this decline is set at 0.6464. The Stochastic oscillator reinforces this bearish forecast, with its signal line pointing downwards towards the 20 mark, indicating potential further declines.

GBP/USD, GBP/JPY Price Action Ideas Post UK Inflation Release

- UK Inflation rises to a 6-month high of 2.3% in October, driven by services inflation.

- GBP/USD faces downside pressure but could rally if the daily candle closes above 1.2680.

- GBP/JPY shows mixed technical signals with a potential for upside in the short term.

The GBP received a shot in the arm this morning owing to an uptick in UK inflation data. Market participants immediately repricing their rate cut expectations down to around 59 bps through December 2025, from a previous 65bps.

The impact on the GBP was immediate with a 40-odd pip rally for GBP/USD and around 80 pips for GBP/JPY.

UK Inflation Challenge

The UK continues its battle with inflation, and more importantly services inflation which ticked up slightly from September with a print of 5% vs the prior month’s 4.9%. The increase in headline inflation might also be a concern now as the annual inflation rate rose to 2.3% in October 2024, the highest in six months, compared to 1.7% in September.

Markets were expecting an uptick in headline inflation to around 2.2% while the MoM inflation number came in at 0.6% above the estimated 0.5% as well. The concern however remains with the service inflation number which is keeping headline inflation elevated.

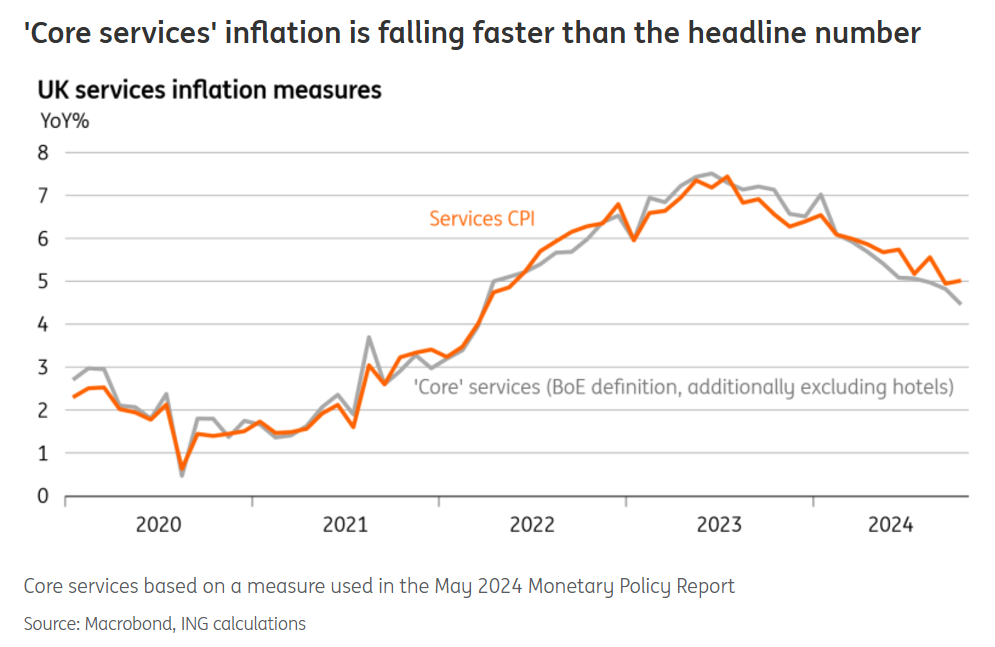

Looking more closely at the data and a lot of the stickiness in the October number comes from categories that the Bank considers less important or less likely to show lasting inflation. This would include things like rent, airfares and package holidays which could in part explain the uptick in services inflation.

A good example of this is when looking at the core services inflation which strips out the data of rent and airfare and we have an entirely different narrative. Given there is no single definition for this, however it has been aptly broken down by ING Think which showed the ‘core services number’ had actually dropped from 4.8% to 4.5% in October.

Source: ING Think

This does not change a thing for the BoE when it comes to the upcoming December policy meeting. I still expect a 25bs cut following the recently released GDP numbers from the UK. Growth is beginning to turn sour, much like the European Union. This is something the BoE would like to avoid and in my opinion may factor heavily at the December meeting.

Based on probabilities, market participants are now pricing in around an 85% chance of a hold at the December 19 meeting with a possible rate cut in February given a 50% chance. This should in theory lend some support to the GBP as the US is expected to cut in December and the Bank of Japan is likely to continue hiking rates in 2025. Will such a move and a GBP recovery come to fruition?

Technical Analysis

GBP/USD

From a technical standpoint, GBP/USD rose in the early part of the week but failed to hold onto any material gains. The weakness in the US Dollar Index did not yield any significant gains for the GBP and with the DXY looking at a recovery today, Cable may face further downside pressure.

At present the key level around the 1.2680 handle is proving a tough nut to crack with UK inflation data helping the GBP/USD to break above this level but failing to find acceptance. If a daily candle close above this handle occurs, bulls may be emboldened which could push cable higher.

A move above the 1.2680 handle may face resistance at 1.2750 and 1.28200 (which is where the 200-day MA rests). The next key hurdle for bulls will be the 1.3000 psychological level which may prove to be a hurdle too far.

Looking at the potential for a break to the downside and the most recent swing low at 1.2600 will be the first area of support before the 1.2500 and 1.2450 handles come into focus.

The driving force behind any move is likely to come from the US Dollar Index (DXY) and its performance in the coming days. Further US Dollar strength could facilitate a retest of the 1.2500 handle.

GBP/USD Daily Chart, November 20, 2024

Source: TradingView.com (click to enlarge)

Support

- 1.2600

- 1.2500

- 1.2450

Resistance

- 1.2680

- 1.2750

- 1.2820

GBP/JPY

GBP/JPY has been inching its way lower since topping out just shy of the psychological 200.00 handle. A pullback helped yesterday by renewed safe haven flow also helped GBP/JPY push further away from the 200.00 handle.

Looking at the technicals and we have some mixed signals. We have a death cross formation as the 100-day MA crossed below the 200-day MA hinting at downside momentum. The candlesticks on the other hand show a sharp rejection following the brief stint below the MAs yesterday with the daily candle finishing as a hammer candlestick hinting at further upside.

The mixed signals do not make it easier, however when combining this with the fundamentals, further upside seems more likely in the short-term. The question is will the 200.00 handle prove a step too far for bulls?

A move higher from current prices for GBP/JPY could face resistance at 198 and 199.30 respectively.

A move lower will first require a daily candlestick close below the two MAs resting around the 194.30-194.60 range. A break of this zone could push GBP/JPY toward the 192.50 and 190.00 handles respectively.

GBP/JPY Daily Chart, November 20, 2024

Source: TradingView.com (click to enlarge)

Support

- 194.30 (200-day MA)

- 192.50

- 190.00

Resistance

- 198.00

- 199.30

- 200.00

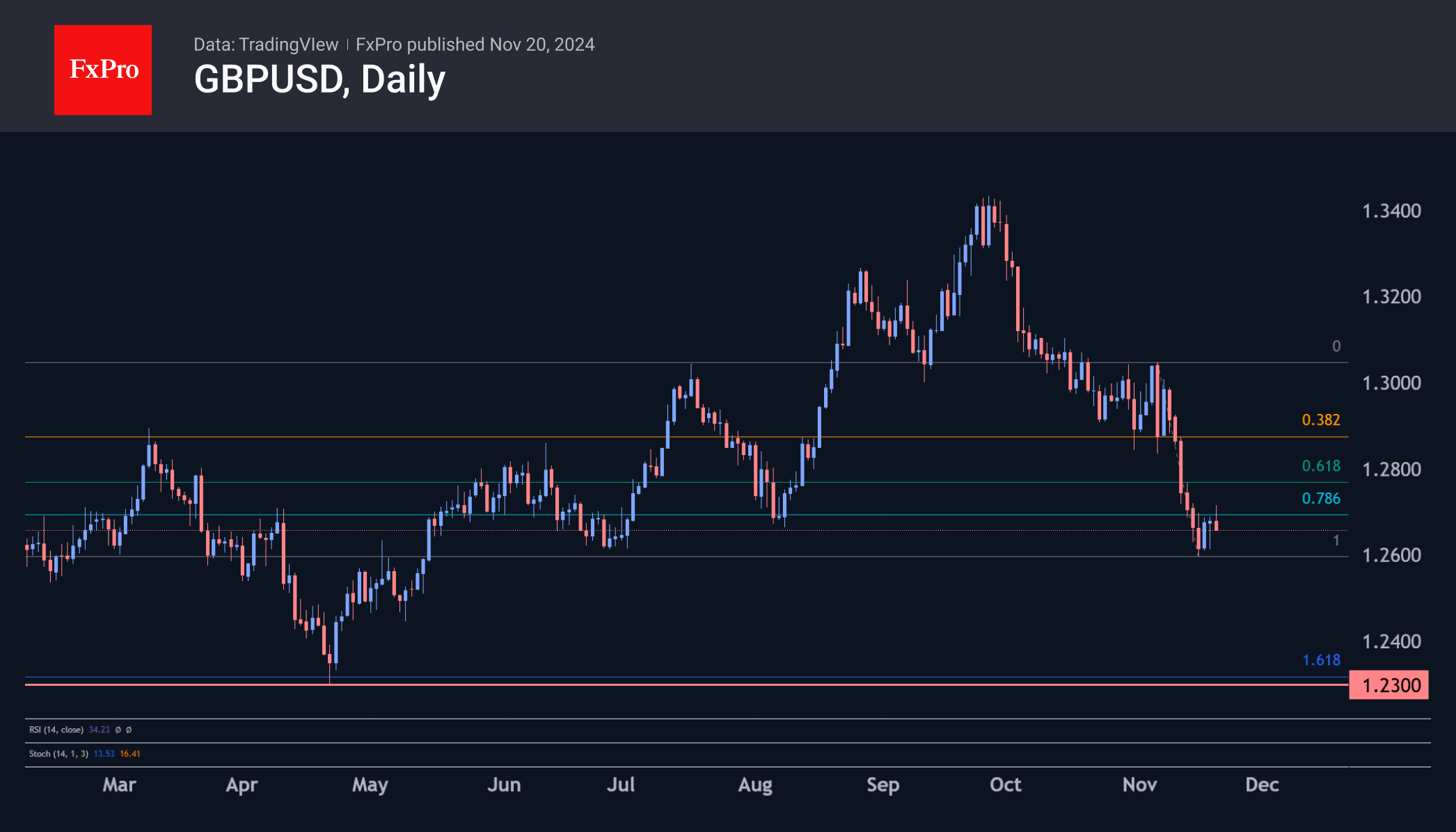

Pound Falls Despite Acceleration in Inflation

UK inflation beat expectations and accelerated markedly, but this only temporarily boosted the Pound. GBPUSD came under further selling when it broke above 1.2700.

CPI rose 0.6% in October, and annual inflation accelerated from 1.7% to 2.3%, the highest since March. These fluctuations around the target do not yet look like a significant threat of a second wave of inflation. Therefore, they are unlikely to force the Bank of England to revise its monetary easing plans significantly.

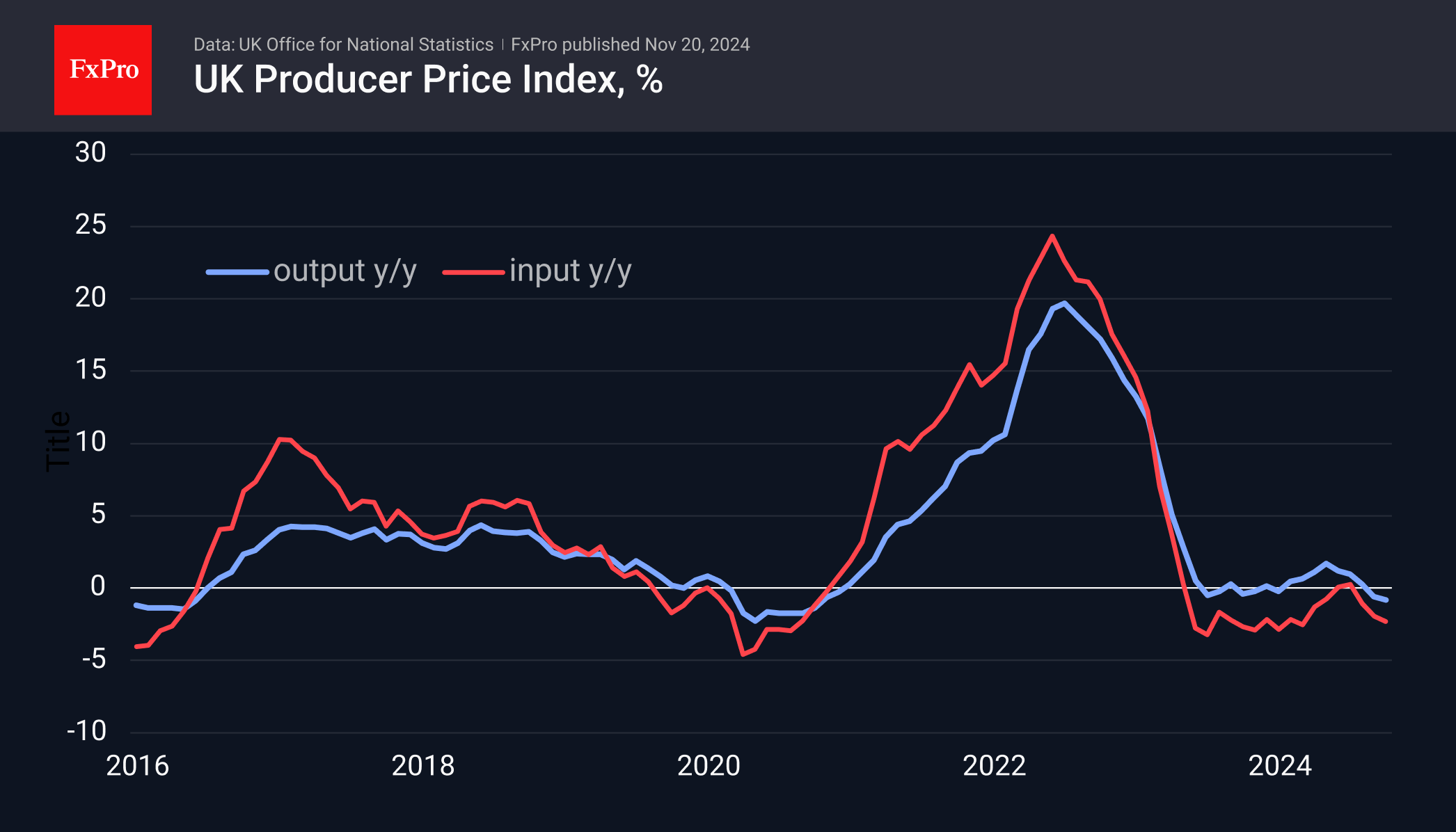

The leading indicator of inflation – producer prices – also came in above expectations. Most importantly, they stay below last year’s levels. The Input Producer Price Index fell 2.3% year-on-year in October, compared with 1.9% in the previous month. The Output PPI accelerated its decline to -0.8% from -0.6%. Although both indices are well above estimates (-3.0% and -1.0% respectively), they are still disinflationary.

The jump in the overall price is due to the largest annual rate increase in owner-occupiers’ housing costs since 1992. Technically, this is not a one-off factor that promises to spread through the economy in the coming months. It is not the result of an overheating economy, so it makes no sense to talk about the formation of a sustained inflationary spiral.

Technical analysis

The British Pound surged impulsively on the better-than-expected news, but the rally lost steam after touching the 1.2700 level. The pair’s rally at the end of last week came to a halt at this level, making it a short-term resistance. This failure to leap forward after the positive news could signal the end of the corrective consolidation. Confirmation of this bearish outlook will come with a fresh failure below 1.26 and a potential target near 1.23, which coincides with this year’s lows.