Sample Category Title

EUR/CHF Daily Outlook

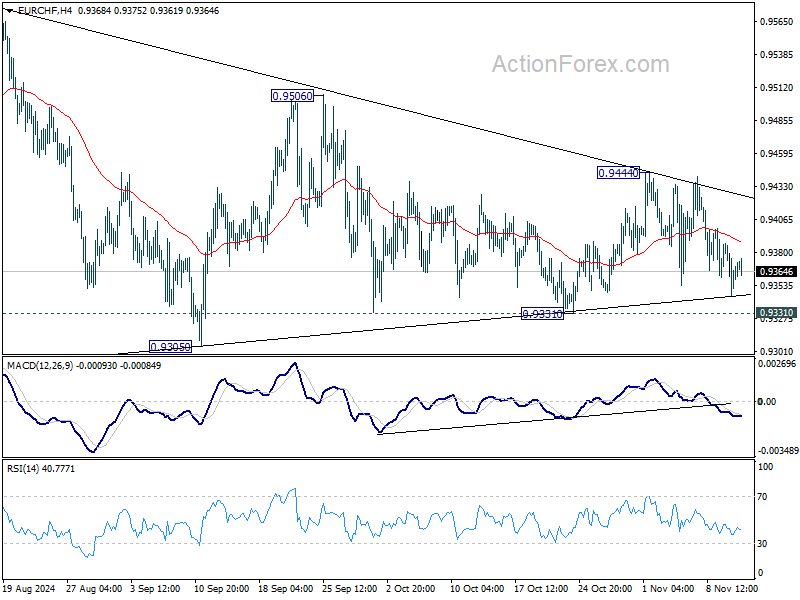

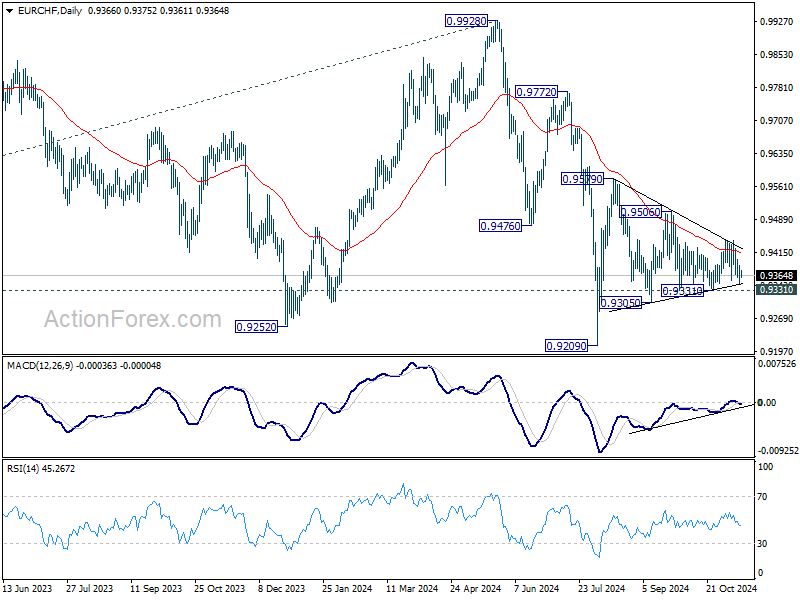

Daily Pivots: (S1) 0.9346; (P) 0.9368; (R1) 0.9389; More....

No change in EUR/CHF's outlook as range trading continues inside converging triangle. On the downside, break of 0.9331 will target 0.9305 support first. Firm break there will bring retest of 0.9209 low. On the upside, break of 0.9444 will bring stronger rally to 0.9506 resistance next.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9419) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

Greenback Strengthens Once More Against All Major Peers

Markets

US bond yields surged after having had the day off on Monday for Veteran’s Day. Net daily changes varied between 8.7 and 13.1 bps across the curve spectrum as President-elect Trump’s reflationary politics continue to reverberate. Expectations for a (much) looser fiscal policy lift those for US growth at a time when CPI inflation has yet to hit the 2% central bank target. With Germany now having set the election date at February 23, we’ll be looking for the fiscal narrative to gain traction in the country and more broadly in Europe as well. US CPI not being at target will still have been the case in October. Numbers are released later today. Headline inflation is seen to accelerate from 2.4% to 2.6% y/y. Core inflation would match September’s 3.3%. Any beat, however small, would cast further doubt on another December 25 bps rate cut. Markets already pared the odds sharply to about 60%. Minneapolis Fed Kashkari yesterday said that “if we saw inflation surprises to the upside between now and then, that might give us pause” when asked what could cause the Fed not to cut rates next month, deviating from the September dot plot. Kashkari is live commenting at Bloomberg when the CPI numbers come out. Stock markets succumbed to the yield pressure. Wall Street eased off the record highs, the Dow Jones underperforming. Europe’s Stoxx50 slipped 2.25%. A technical acceleration kicked in after the index lost support around 4800. Widening interest rate differentials (European swap rates rose between 0.7-4.6 bps) and the risk-off created the perfect environment for the USD. The greenback strengthened once more against all major peers. EUR/USD tested the 1.06 big figure. It avoided a break yesterday (1.062) but continues to trade on the backfoot this morning (1.061), suggesting ongoing, by default dollar strength. USD/JPY extends its meteoric rise that’s been going on since mid-September to beyond 155 currently. We expect to see some Japanese government and central bank officials to become increasingly vocal about the matter. Gilts underperformed Bunds on “sticky” (BoE chief economist Pill) wage growth but sterling couldn’t benefit. Perhaps the UK currency is eying other important data that’s upcoming, including Friday’s GDP numbers and next week’s CPI. EUR/GBP jumped back above 0.83 but the technical picture remains a fragile one.

News & Views

The Federal Reserve Bank of New York consumer survey showed households’ inflation expectations declined slightly across the whole spectrum of horizons in October. One-year ahead inflation expectations eased 0.1%pt to 2.9%, three-year ahead expectations declined 0.2%pt to 2.5% and the 5-y gauge softened to 2.8%. Home price growth expectations (3.0%) were unchanged and stayed in a tight band since August 2023. Labor market expectations improved with households reporting a lower likelihood of higher unemployment (-1.7%pt to 34.5%, the lowest since Feb 2022) and personal job loss (-0.3%pt to 13.0%). Consumers see a higher likelihood of finding a job if they were laid off. Median expected household income growth as unchanged at 3.0%. That was also the case for spending growth 4.9%, but this parameter stays well above pre-pandemic levels. Perceptions of credit access compared to a year ago improved in October. The average perceived probability of missing a minimum debt payment over the next three months decreased by 0.3%pt to 13.9%, the first decrease since May 2024. Perceptions about households’ current financial situations compared to a year ago improved.

Australian quarterly wage growth figures for Q3 for the third consecutive quarter printed at 0.8% Q/Q. The Y/Y measure eased to 4.1% to 3.5%. The rise was slightly more modest than expected. Annual growth in the private sector was 3.5% in the September quarter 2024. This is the lowest private sector annual growth since the September quarter 2022. Public sector annual growth (+3.7%) was higher than in the same quarter last year (+3.5%), but lower than the recent peak (+4.2%) seen in December quarter 2023. The Reserve bank of Australia expects wage growth to ease to 3.4% at the end of the 2024 and 3.2% end 2025. However, for these kinds of wage growth levels to be compatible with inflation sustainably returning to 2-3% a further rise in productivity is probably needed. Money markets currently still only fully discount a first RBA rate cut in the summer of next year. The Aussie dollar remains under pressure from USD strength (AUD/USD 0.6525) but in this move recently outperformed the likes of the euro (EUR/AUD 1.626).

EUR/USD Daily Outlook

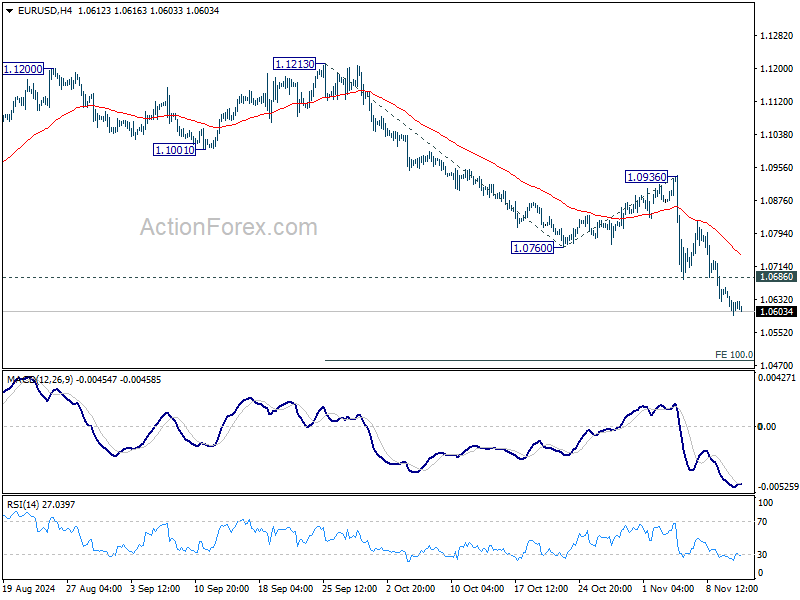

Daily Pivots: (S1) 1.0591; (P) 1.0627; (R1) 1.0659; More...

Intraday bias in EUR/USD remains on the downside for the moment. Fall from 1.1213 should target 100% projection of 1.1213 to 1.0760 from 1.0936 at 1.0483. On the upside, above 1.0686 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.0760 support turned resistance holds.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

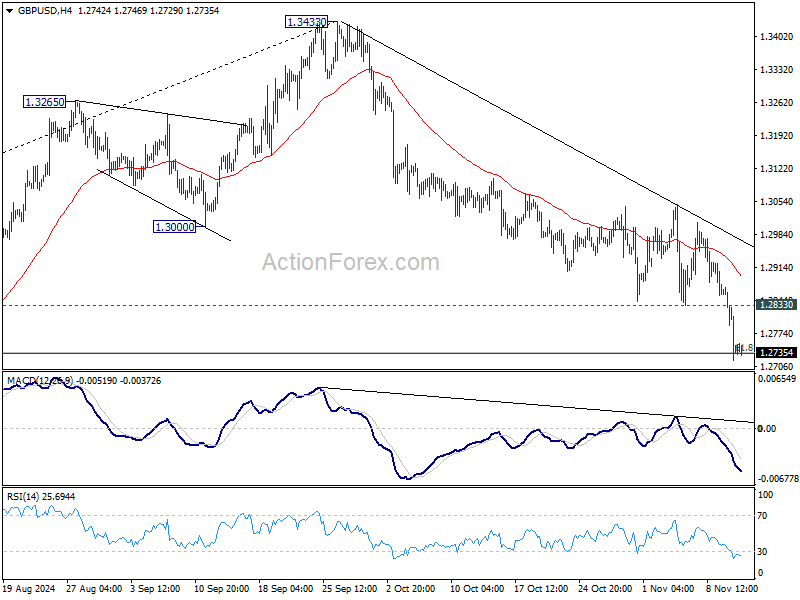

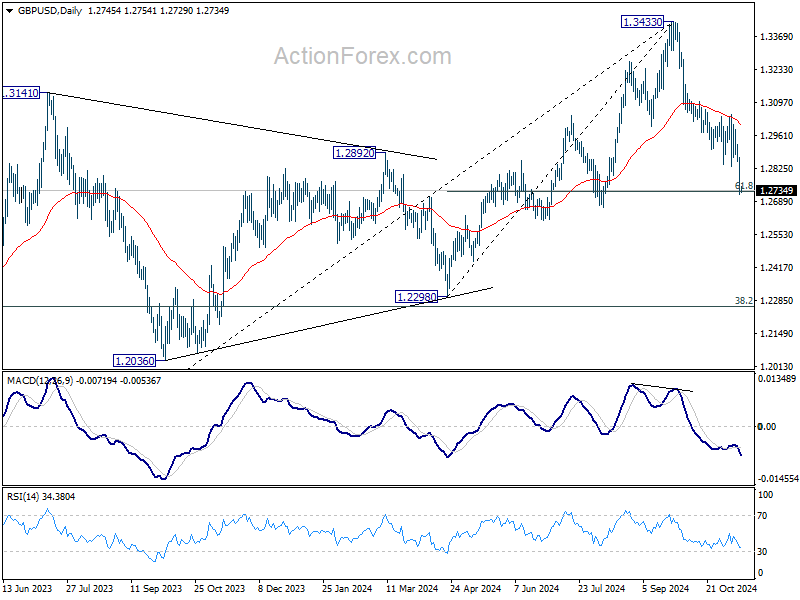

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2685; (P) 1.2781; (R1) 1.2843; More...

Intraday bias in GBP/USD stays on the downside at this point. Decisive break of 61.8% retracement of 1.2298 to 1.3433 at 1.2732 will extend the decline from 1.3433 to 1.2298 key support. On the upside, above 1.2833 support turned resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

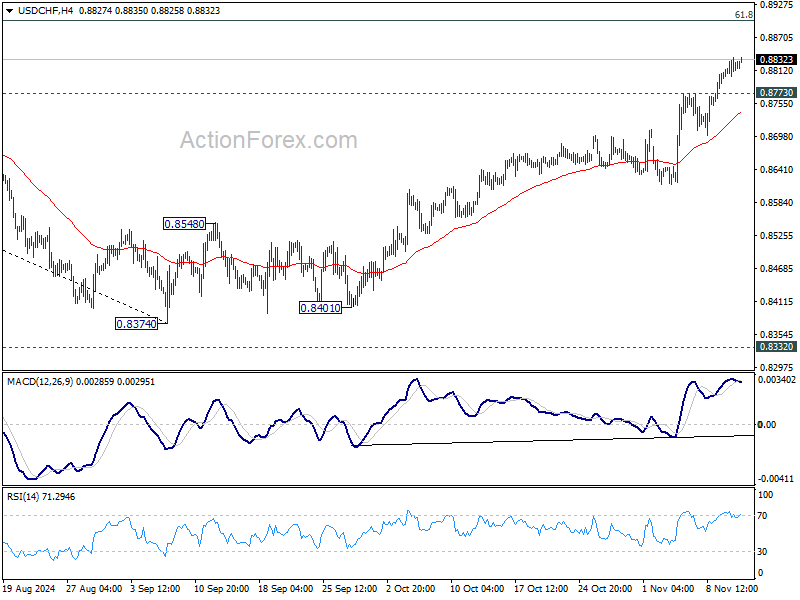

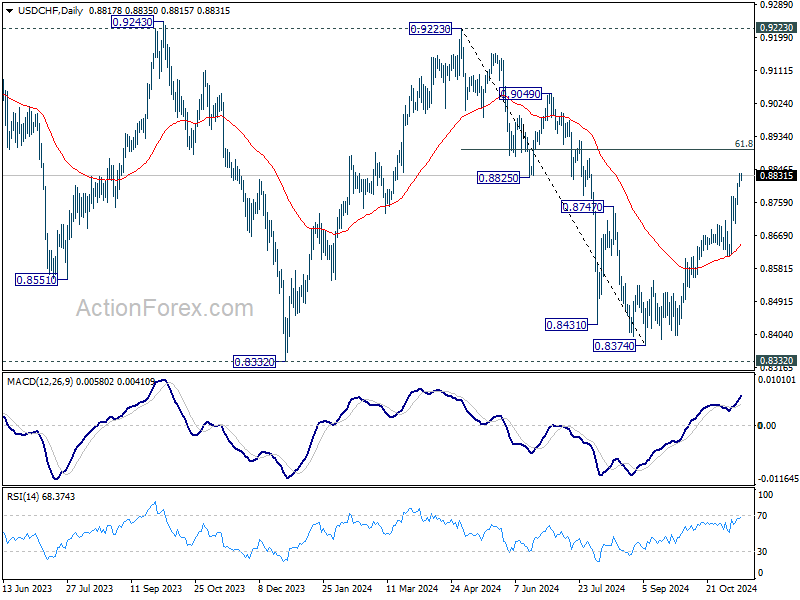

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8780; (P) 0.8808; (R1) 0.8845; More…

Intraday bias in USD/CHF stays on the upside for the moment. Current rise from 0.8374 should target 61.8% retracement of 0.9223 to 0.8374 at 0.8899. Sustained trading above there will pave the way towards 0.9223 high. On the downside, below 0.8773 support will turn intraday bias neutral again and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

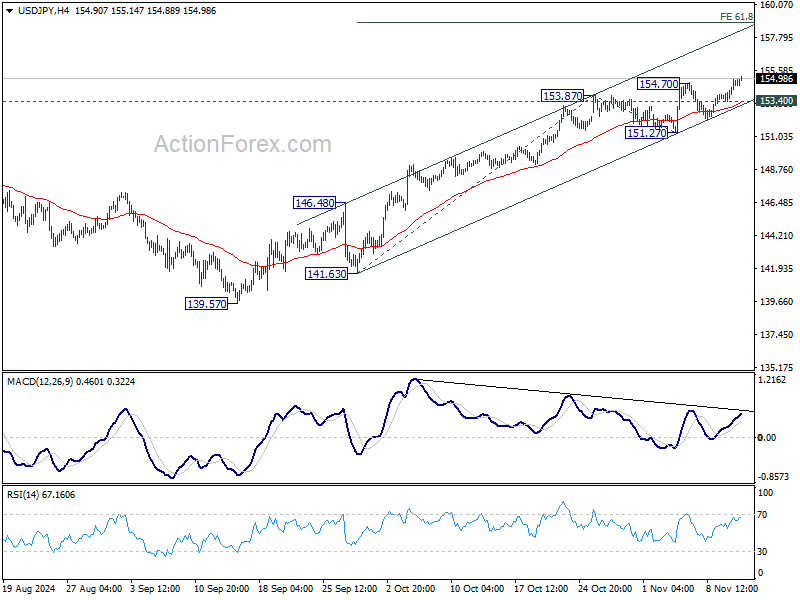

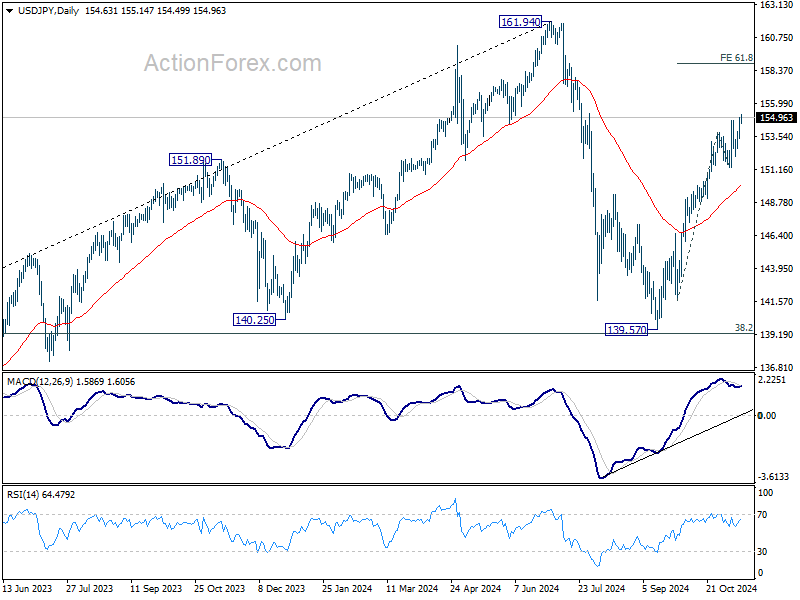

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.72; (P) 154.32; (R1) 155.23; More...

USD/JPY's rally resumed by breaking 154.70 and intraday bias is back on the upside. Current rise from 139.57 will 61.8% projection of 141.63 to 153.87 from 151.27 at 158.8. On the downside, below 153.40 minor support will turn intraday bias neutral again first. But further rally is expected as long as 151.27 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

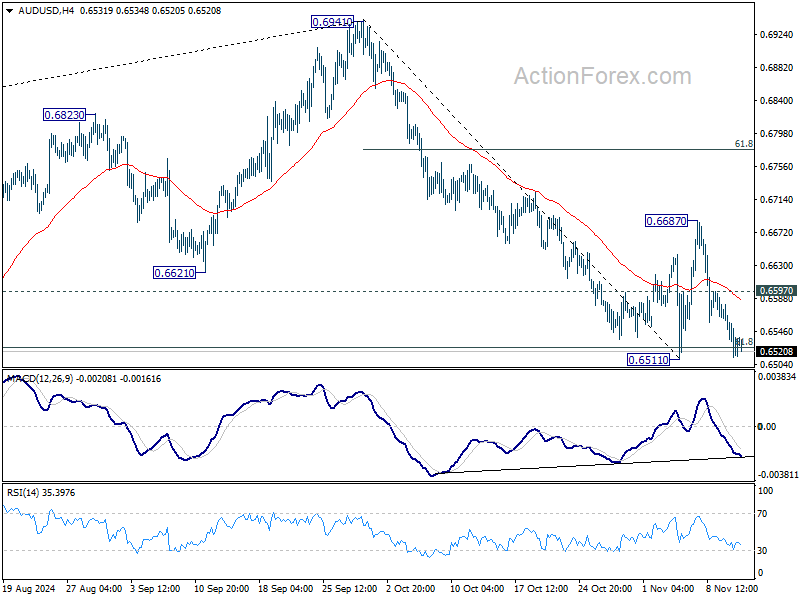

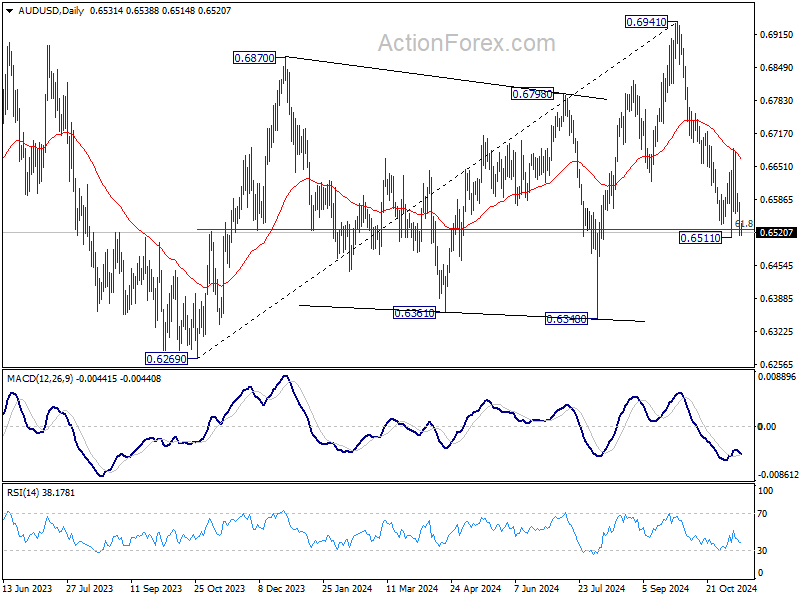

AUD/USD Daily Report

Daily Pivots: (S1) 0.6505; (P) 0.6543; (R1) 0.6573; More...

Intraday bias in AUD/USD remains neutral for the moment. On the upside, above 0.6597 minor resistance will turn bias back to the upside for 0.6687 first. Firm break there will target 61.8% retracement of 0.6941 to 0.6511 at 0.6777. On the downside, break of 0.6511 will resume the fall from 0.6941 instead.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

Dollar Up, Oil Down – Eyes on US CPI

The US yields pushed higher and the dollar rally gained further momentum yesterday, as investors continued to surf on the idea that Donald Trump’s pro-growth policies and tariffs would boost inflation in the US and limit the Federal Reserve’s (Fed) capacity to ease the monetary policy as much as previously anticipated. Yesterday’s data showed an improved economic optimism in the US in November. The US 2-year yield, for example, which best captures the rate expectations, is up by 85bp since the September dip, we could see a similar jump in the US 10-year yield. Minneapolis Fed President Neel Kashkari said that he’ll be looking at the inflation data to decide whether he would back another rate cut in December. And activity on Fed funds futures gives no more than 62% for another 25bp in December, before the release of the latest US CPI update today.

Inflation regains importance

The CPI data has regained importance since Donald Trump was re-elected President of the US. Jobs data remains crucial for the Fed’s policy path, as the last thing the Fed wants is to panic and lose control of the situation, but the Fed’s victory over inflation looks more vulnerable today than it did a month ago. And that’s supportive of the US dollar.

Of course, October figures won’t tell much about the Trump effect on consumer prices. We must wait a few months before we start seeing the impact of Trump on numbers. But the higher the numbers, the lower the December cut expectations. And I sense that today’s numbers may not sooth the doves’ nerves: the US headline inflation is expected to have climbed from 2.4% to 2.6%, while core inflation is seen steady near 3.3% - still significantly above the Fed’s 2% policy target. Any upside pressure in figures should continue to drive capital into the US dollar. But the US dollar has hit the overbought market conditions following a 6% rebound since the beginning of October. Therefore, any weakness in the data could help tame demand in the short-run, trigger a minor correction and give the US dollar bulls opportunity to strengthen their bullish positions for the year end. Voices calling for a further slide of EURUSD toward parity are growing.

But wait! The US dollar’s strength will likely hit a speed bump, and the initial rally will probably continue at a lower speed, because the USD appreciation, and other currencies’ depreciation, will boost inflation expectations in the rest of the world and lead to a slower-than-otherwise easing in other central bank rate policies.

Still, the US dollar outlook is comfortably bullish at the moment as there is room for a further retreat in dovish Fed expectations.

Oil under pressure

The barrel of US crude is testing the $68pb offers to the downside on sluggish Chinese, global demand, ample supply from non-OPEC countries, and the absence of fresh tensions from the Middle East. Add to that the fact that OPEC cut its oil demand forecast for fourth consecutive month this week, and you have a comfortably bearish picture in crude oil.

In numbers, OPEC expects the global oil consumption to increase by 1.8 mbpd in 2024 – just under 2%. And it’s more optimistic than many bank forecasts, Aramco’s own forecasts and roughly the double of the IEA’s estimation. The latter will release their latest report on Thursday.

Under these circumstances, the oil bears keep control in their hands. Trend and momentum indicators remain comfortably bearish, the RSI indicator isn’t close to overbought market conditions – meaning that there is room for the selloff the extend in the short run, and the $70/71pb range – that shelters the minor 23.% Fibonacci retracement and the 50-DMA – is crowded with offers. The major upside risk (besides geopolitical risks) is another delay to the end of OPEC production restriction plans. I see that coming big as a mountain. But that decision will certainly not come before the 1st of December, at OPEC’s next scheduled meeting, unless we see an accelerated meltdown in oil prices that would necessitate an early announcement from the cartel. For now, price rallies are interesting top selling opportunities. Solid resistance is seen into $70/71 range and the key resistance to the actual negative trend stands at the 72.85pb level, the major 38.2% Fibonacci retracement on the summer to now selloff.

The downside pressure in oil prices weigh on oil company valuations, but the downside in oil companies’ share prices remain limited by optimism that Donald Trump loves oil companies and will want them to pump and sell as much as possible to lower energy prices. Exxon for example is trading near $120 per share, a few dollars below an ATH level defying weaker oil prices.

But note that, even though oil giants are happy to see oil-friendly Donald Trump take the reins of the US, they prefer price over volume and Exxon’s CEO even said that Trump shouldn't bail on the Paris climate deal and doesn't see a big near-term boost in US oil output.

All Eyes on US CPI

In focus today

Today's most important data release will be the US October CPI, where we expect inflation to slow down in both headline (+0.1% m/m SA, from +0.2%) and core (+0.2% m/m SA, from +0.3%) terms. In annual terms, headline inflation could still appear to accelerate due to base effects stemming from a low reading a year ago (headline forecast 2.5% y/y, from 2.4%).

In the euro area, focus turns to industrial production data for September, which will show how actual production fared. The data is interesting as hard data has been better compared to PMIs in the manufacturing sector.

In Sweden, Riksbank minutes will be released at 09.30 CET. Since the decision to cut by 50bp was unanimous, all board members appear to stand behind the message in the monetary policy update that indicated a weaker real economy that led to the jumbo cut. Still, we look for any cracks in the façade and expect Riksbank to move more slowly going forward.

Economic and market news

What happened yesterday

In the US, the NFIB's small business optimism index showed a slight improvement in overall sentiment in October, increasing to 93.7 from 91.5. General uncertainty reached an all-time-high ahead of the election, but we have seen similar movements ahead of previous elections as well. Labour market indicators were little changed, while job openings and hiring plans remained slightly below pre-pandemic levels. Similarly, inflation indicators saw only minor changes, with firms' "price plans"-index staying just slightly above pre-covid levels. Overall, US businesses remain in good shape especially now that political uncertainty is set to gradually ease.

In politics, the Republicans moved closer to clinching the House, with Edison Research projecting another race win, bringing them to at least 216 seats - just two seats short of the 218-majority threshold. Winning the House would complete a Republican sweep, giving Trump full leverage to proceed with his agenda. As noted earlier this week, this scenario could widen the budget deficit, public debt, and potentially lead to renewed inflationary pressures.

In the euro area, Olli Rehn, Finnish central bank chief, said that the ECB is likely to continue cutting rates, potentially reaching the neutral level in H1 2025. While the direction is clear, Rehn highlighted that the pace and size of cuts will depend on the inflation outlook, the dynamics of underlying inflation and monetary policy transmission. We believe that November PMIs will weigh more heavily than usual on the size of the December ECB rate cut, where we project a 25bp cut.

In Germany, the ZEW indicator declined in November, with the downtick being broad-based. The assessment of the current situation declined further to -91.4 (cons: -85.0, prior: -86.9), its lowest level since May 2020. Similarly, the expectations component fell to 7.4 (cons: 13.2, prior: 13.1), indicating that last month's uptick was temporary. It shall be very interesting to see whether PMIs and Ifo for November mirror this development as was the case in October when all measures improved. Overall, we remain negative on the economic outlook for Germany as the manufacturing sector continues to record falling activity. A clear risk for the growth outlook is a significant deterioration in the labour market, which is weakening as visible in Q3 where employment declined for the first time since Covid, and an increasing number of companies are using short-term working schemes.

On the political front, the leaders of Germany's major parties have agreed to host the snap elections on 23 February 2025. Later today, German Chancellor Scholz is expected to announce the date of a vote of confidence in the government, which likely could happen on 16 December. For more details regarding the political disarray in Germany, please see Research euro area: Fiscal policy to slow growth in 2025 - but mind the RFF, 7 November.

In the UK, BoE Chief Economist Huw Pill (hawk) emphasized that the central bank's efforts to tame inflation are not over, given persistent underlying inflation momentum. Pill highlighted Tuesday's labour market data, which showed continued sticky wage growth, underscoring that BoE still has work to do on inflation. The labour market report also showed the unemployment rate ticking higher to 4.3% in the most recent three-month period, slightly above consensus of 4.1% and the previous figure of 4.0%. However, this is related to the very low June figure of 3.7% dropping out in September. Given that the measure is also based on the low-quality LFS data, focus should be on wage growth. Looking ahead, next week's October inflation release is key, where we will likely see a slight increase due to energy price adjustments. We remain positive on GBP, targeting EUR/GBP at 0.81 in 6M.

In commodities space, OPEC lowered its forecast for global oil demand growth for 2024, while also trimming its 2025 projections, owing to weaker activity in China and other Asian markets. The cut marks the cartel's fourth consecutive downward revision in the 2024 outlook. For the remainder of 2024 we expect the oil price to climb higher towards USD80/bbl.

Equities: Global equities declined yesterday, led by significant selloffs in Europe and Asia. Some of the "Trump trades" are still ongoing, but as mentioned previously, also some China-related rotations are going on, with materials sectors experiencing the most significant losses across indices. Notably, despite the downturn in global equities, yields were higher, cyclicals outperformed, and the VIX moved slightly lower. This suggests that the market is not fearful of the growth outlook but is instead adjusting to a new reality. In the US yesterday: Dow -0.9%, S&P 500 -0.3%, Nasdaq -0.1%, and Russell 2000 -1.8%. Most Asian markets are lower this morning, as are most European and US futures.

FI: The US-German yield divergence continued to 206bp on the 10y point, which is 6bp wider than on Monday. European real rates rose markedly with e.g. the 5y5y EUR real swap rate up 6bp on the day.

FX: US yields continued to climb, diverging substantially from euro area rates and pushed EUR/USD temporarily below 1.06 for a new year-low. Scandies showed resilience versus the euro but lost out against the greenback. The Chinese yuan also weakened against the USD as an reflection of the anticipation of new US tariffs hitting China over the next year.

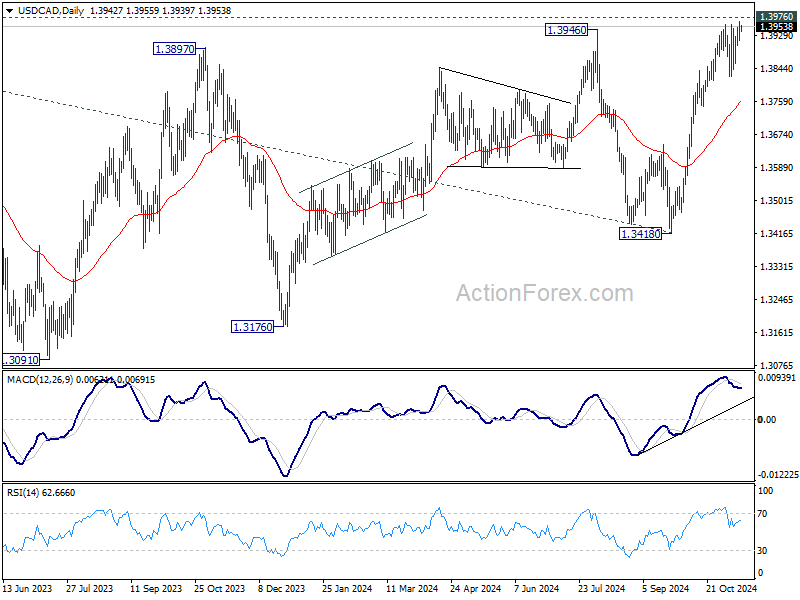

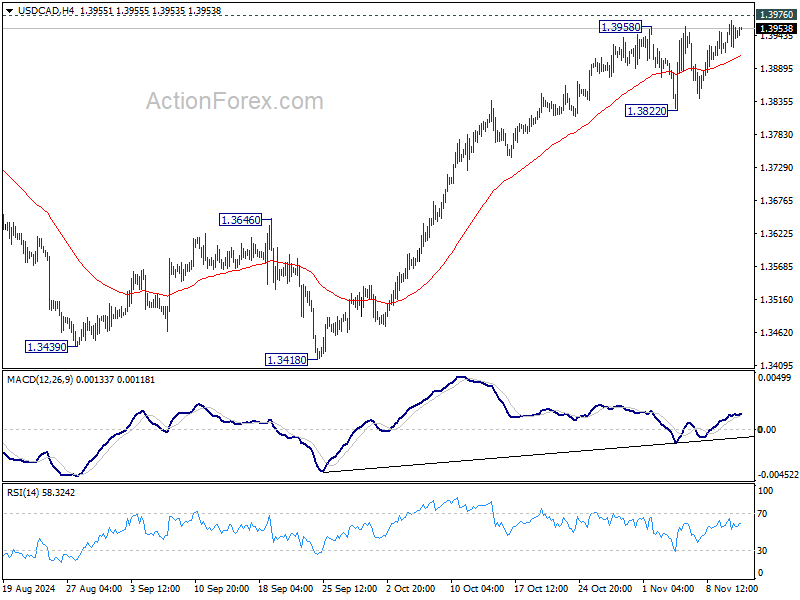

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3943; (R1) 1.3969; More...

USD/CAD breached 1.3958 briefly but upside is capped below 1.3976 key resistance. Intraday bias stays neutral first. Further rise is is expected as long as 1.3822 support holds. On the upside, decisive break of 1.3976 key resistance will confirm larger up trend resumption. On the downside break of 1.3822 support will bring deeper pullback towards 55 D EMA (now at 1.3762).

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.