Sample Category Title

Dollar Firm as CPI Likely to Confirm Disinflation Stalemate

The financial markets are intently focused today on US inflation data. Expectations are that both the headline CPI and core CPI remained unchanged in October from the previous month's readings of 2.4% and 3.3%, respectively.

This stagnation in disinflation supports the notion that bringing inflation back to Fed's 2% target may prove increasingly challenging in its final stages.

Adding to inflationary concerns are fiscal and trade policies from President-elect Donald Trump, which could create further upward pressure on prices in the coming year.

Such an outlook would likely prompt Fed to maintain cautious and gradual pace in lowering interest rates.

In currency markets, the Dollar has shown strength this week, holding its position as the top performer. However, it remains contained below last week’s highs against commodity currencies. In contrast, Yen is lagging, followed by Sterling and Euro, while Swiss Franc positions around the middle.

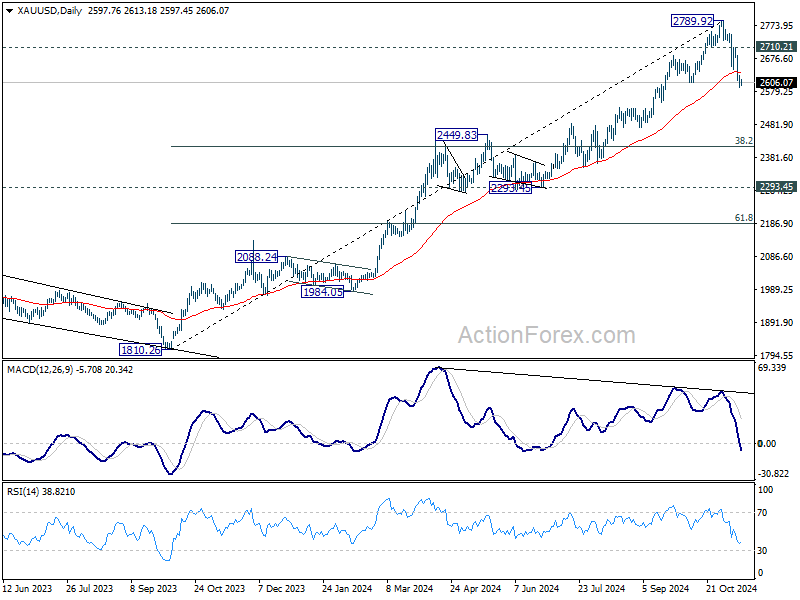

Technically, Gold's break of 55 D EMA strengthens the case that fall from 2789.92 is corrective the whole five-wave rally from 1810.26. Further decline is now expected as long as 2710.21 minor resistance holds. Next target is 38.2% retracement of 1810.26 to 2789.92 at 2415.68, which sits inside 2293.45/2449.83 support zone.

In Asia, at the time of writing, Nikkei is down -1.73%. Hong Kong HSI is down -0.99%. China Shanghai SSE is down -0.23%. Singapore Strait Times is up 0.14%. Overnight, DOW fell -0.86%. S&P 500 fell -0.29%. NASDAQ fell -0.09%. 10-year yield rose 0.125 to 4.432.

Barkin says Fed well-positioned to respond to economic changes

Richmond Fed President Thomas Barkin noted that the economy is "in a good place" and that Fed is now positioned to react flexibly to evolving economic conditions.

Speaking at an event overnight, Barkin highlighted that interest rates are balanced—elevated from recent lows but no longer at peak levels—providing Fed with room to adjust policy as needed.

Barkin observed that more price-sensitive consumer base is contributing to moderating inflation pressures, suggesting that demand adjustments are naturally aiding Fed's inflation objectives.

Additionally, he pointed to the resilience of the labor market, with companies retaining employees and maintaining lower turnover rates, which has provided stability and boosted productivity.

Fed's Kashkari highlights inflation as key factor for December rate decision

Minneapolis Fed President Neel Kashkari pointed to inflation as the primary driver that could influence Fed’s policy direction at its next meeting. He stated that any decision to pause rate cut would require an "inflation surprise" before then.

“If we saw inflation surprises to the upside between now and then, that might give us pause,” Kashkari said at an event, noting that significant changes in the labor market are less likely given the limited time before the December meeting.

Kashkari reiterated that while the US economy remains strong, inflation has yet to fully return to the 2% target. He emphasized that it could still take a year or two to achieve this target, particularly given the lingering effects of housing inflation, though he noted recent cooling in that area as “encouraging.”

On the broader outlook for monetary policy, Kashkari described the current stance as "modestly restrictive," suggesting that it is just slightly contractionary in effect. He acknowledged that the neutral rate remains uncertain but expected more clarity over the coming year as the Fed monitors the economy’s response to rate changes.

Japan’s PPI rises 3.4% yoy in Oct, highest since mid-2023

Japan’s PPI rose from 3.1% yoy to 3.4% yoy in October, surpassing market expectations of 3.0% and marking the highest annual increase since July 2023. On a monthly basis, PPI advanced by 0.2%, reflecting sustained inflationary pressure within Japan’s production sector.

The data also revealed a less pronounced decline in Yen-based import prices, down -2.2% yoy compared to a -2.5% drop in September, signaling that import costs may be stabilizing. This relative improvement aligns with a 4.3% mom increase in Yen's exchange rate. However, on a monthly scale, import prices saw a notable 3.0% rise after a -2.8% decrease in September.

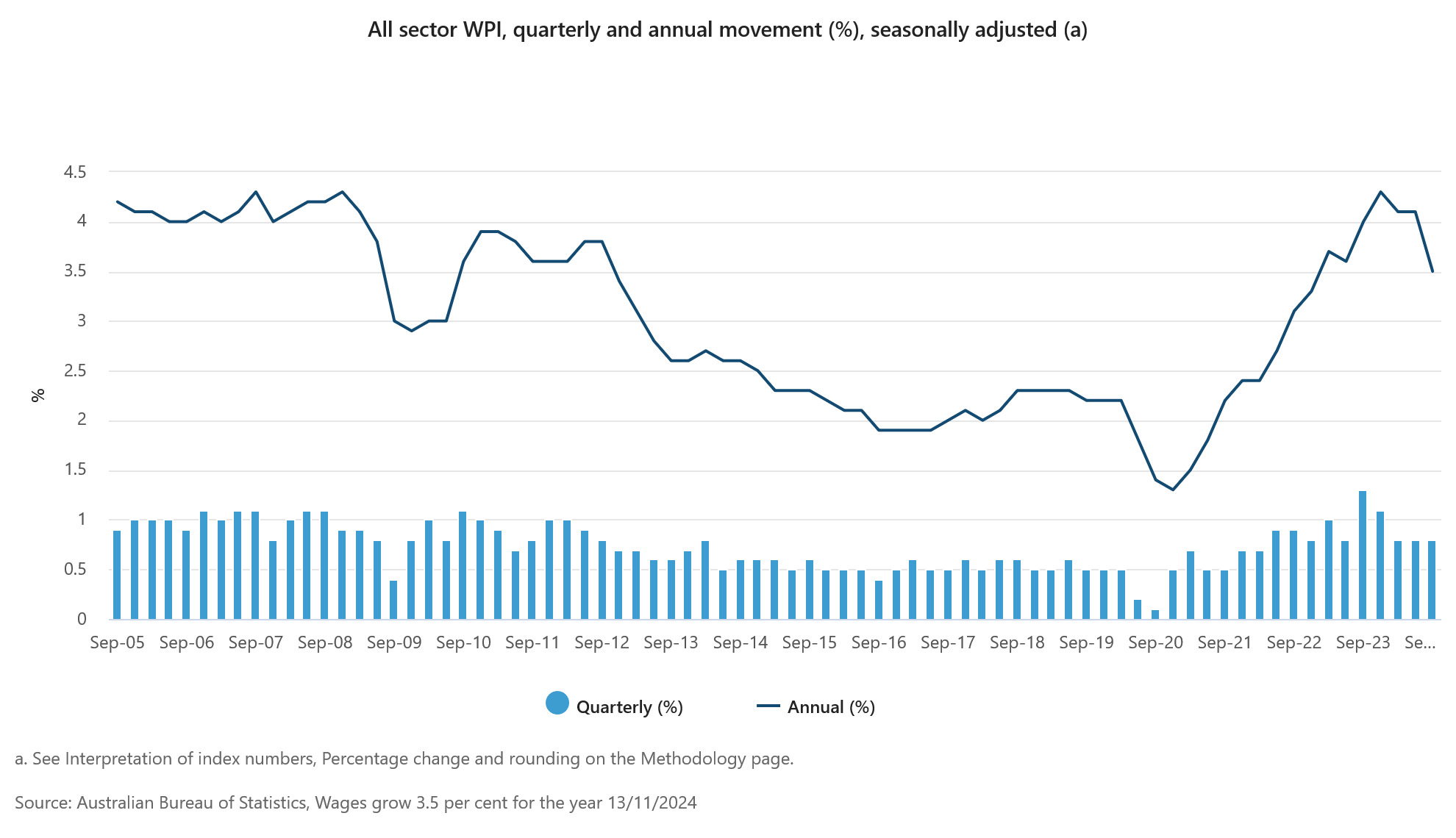

Australia's wage growth slows as public sector outpaces private for first time since 2020

Australia's wage growth softened in Q3, with the Wage Price Index rising by 0.8% qoq, slightly missing the forecast of 0.9%. On an annual basis, wage growth slowed from 4.1% yoy to 3.5% yoy, falling short of the expected 3.6% yoy and marking the lowest annual increase since Q4 2022. This deceleration follows four consecutive quarters of 4% or higher wage growth, pointing to easing in wage-driven inflation pressures.

For the first time since late 2020, public sector wage growth surpassed that of the private sector. Public sector wages rose by 3.7% yoy, higher than the 3.5% yoy recorded in the same quarter last year but down from the recent high of 4.2% yoy in Q4 2023, lowest since Q3 2022.

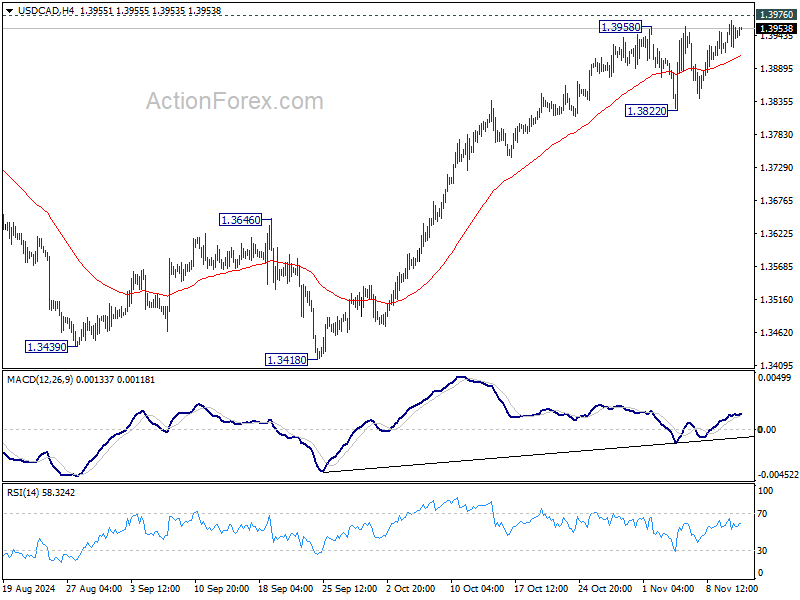

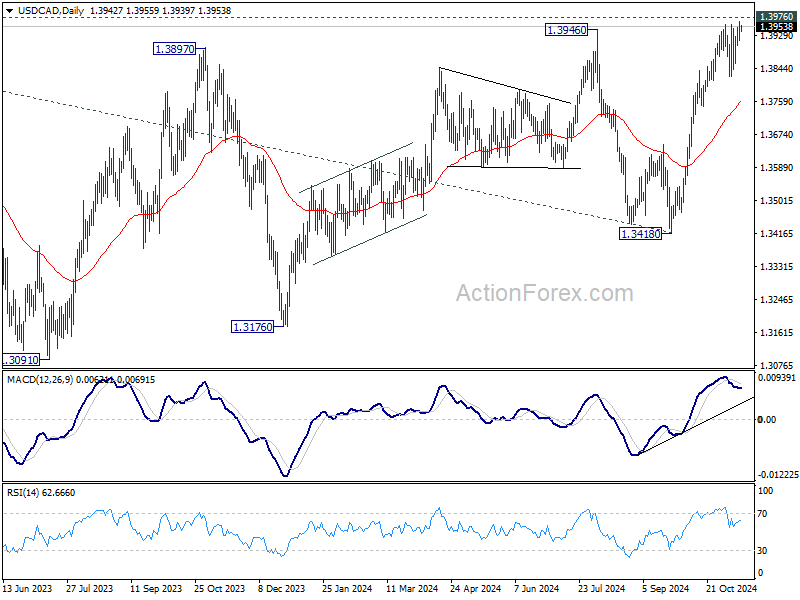

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3943; (R1) 1.3969; More...

USD/CAD breached 1.3958 briefly but upside is capped below 1.3976 key resistance. Intraday bias stays neutral first. Further rise is is expected as long as 1.3822 support holds. On the upside, decisive break of 1.3976 key resistance will confirm larger up trend resumption. On the downside break of 1.3822 support will bring deeper pullback towards 55 D EMA (now at 1.3762).

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

Gold Faces a Setback: Can It Rebound Soon?

Key Highlights

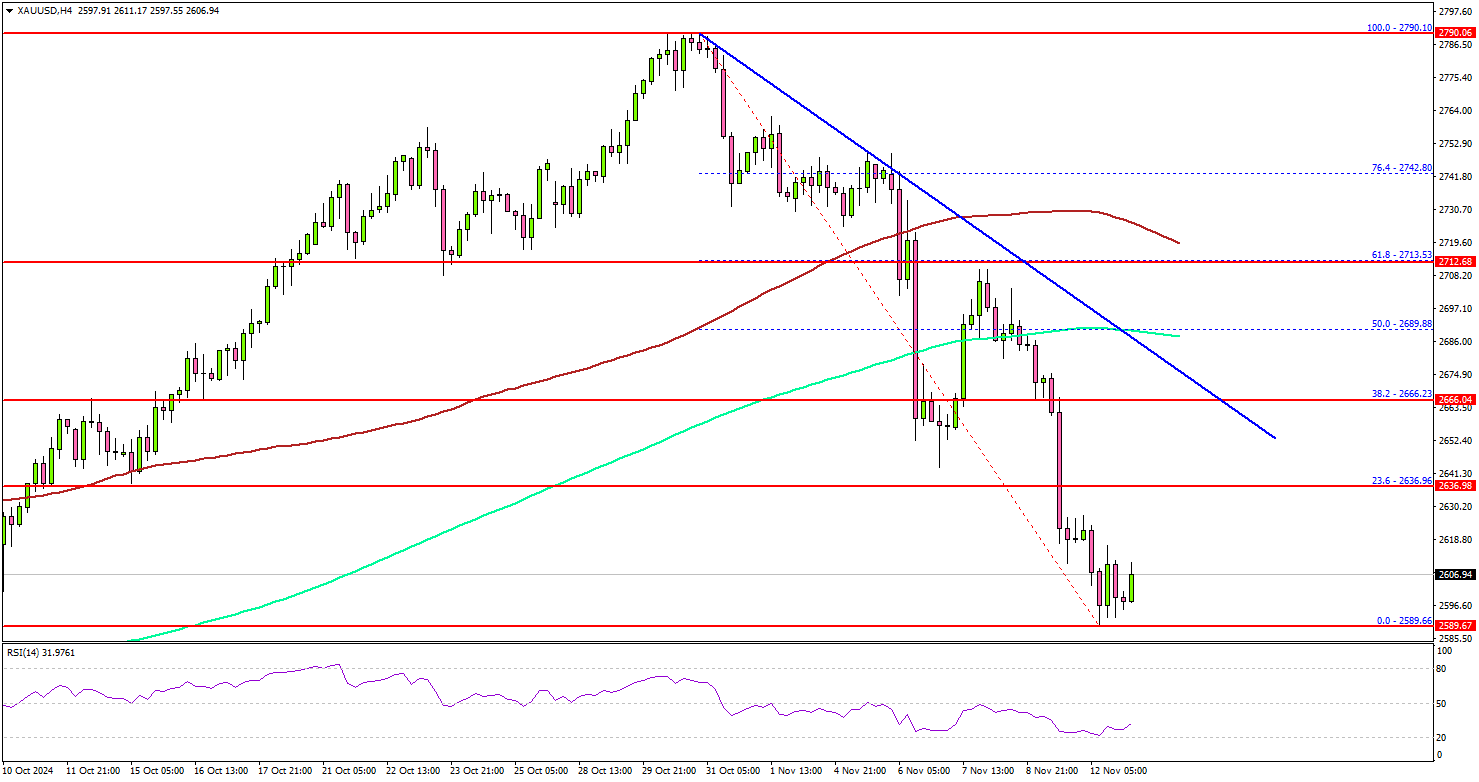

- Gold started a sharp downside correction below the $2,665 support.

- A connecting bearish trend line is forming with resistance at $2,670 on the 4-hour chart.

- Bitcoin traded to a new high at $89,998 on TitanFX before it saw a pullback.

- The US CPI could rise 2.6% in Oct 2024 (YoY), up from 2.4%.

Gold Price Technical Analysis

Gold prices struggled above $2,775 against the US Dollar. The price started a fresh decline and traded below the $2,720 and $2,700 support levels.

The 4-hour chart of XAU/USD indicates that the price declined below the $2,665 support, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours).

The decline even gained pace below $2,620. Finally, the price tested the $2,590 zone before it started a consolidation phase. On the downside, initial support is near the $2,590. The first major support is near the $2,580 level.

The main support is now $2,550. A downside break below the $2,550 support might call for more downsides. The next major support is near the $2,525 level.

On the upside, immediate resistance is near the $2,635 level or the 23.6% Fib retracement level of the downward move from the $2,790 swing high to the $2,589 low. The first major resistance sits near the $2,665 level.

There is also a connecting bearish trend line forming with resistance at $2,670 on the same chart. A clear move above the $2,670 resistance could open the doors for more upsides. The next major resistance could be $2,700, above which the price could rally toward the $2,720 level.

Looking at Bitcoin, the price gained pace for a move above the $88,500 level before it saw a short-term rejection near $90,000.

Economic Releases to Watch Today

- US Consumer Price Index for Oct 2024 (MoM) – Forecast +0.2%, versus +0.2% previous.

- US Consumer Price Index for Oct 2024 (YoY) – Forecast +2.6%, versus +2.4% previous.

- US Consumer Price Index Ex Food & Energy for Oct 2024 (YoY) – Forecast +3.3%, versus +3.3% previous.

Australia’s wage growth slows as public sector outpaces private for first time since 2020

Australia's wage growth softened in Q3, with the Wage Price Index rising by 0.8% qoq, slightly missing the forecast of 0.9%. On an annual basis, wage growth slowed from 4.1% yoy to 3.5% yoy, falling short of the expected 3.6% yoy and marking the lowest annual increase since Q4 2022. This deceleration follows four consecutive quarters of 4% or higher wage growth, pointing to easing in wage-driven inflation pressures.

For the first time since late 2020, public sector wage growth surpassed that of the private sector. Public sector wages rose by 3.7% yoy, higher than the 3.5% yoy recorded in the same quarter last year but down from the recent high of 4.2% yoy in Q4 2023, lowest since Q3 2022.

Japan’s PPI rises 3.4% yoy in Oct, highest since mid-2023

Japan’s PPI rose from 3.1% yoy to 3.4% yoy in October, surpassing market expectations of 3.0% and marking the highest annual increase since July 2023. On a monthly basis, PPI advanced by 0.2%, reflecting sustained inflationary pressure within Japan’s production sector.

The data also revealed a less pronounced decline in Yen-based import prices, down -2.2% yoy compared to a -2.5% drop in September, signaling that import costs may be stabilizing. This relative improvement aligns with a 4.3% mom increase in Yen's exchange rate. However, on a monthly scale, import prices saw a notable 3.0% rise after a -2.8% decrease in September.

Fed’s Kashkari highlights inflation as key factor for December rate decision

Minneapolis Fed President Neel Kashkari pointed to inflation as the primary driver that could influence Fed’s policy direction at its next meeting. He stated that any decision to pause rate cut would require an "inflation surprise" before then.

“If we saw inflation surprises to the upside between now and then, that might give us pause,” Kashkari said at an event, noting that significant changes in the labor market are less likely given the limited time before the December meeting.

Kashkari reiterated that while the US economy remains strong, inflation has yet to fully return to the 2% target. He emphasized that it could still take a year or two to achieve this target, particularly given the lingering effects of housing inflation, though he noted recent cooling in that area as “encouraging.”

On the broader outlook for monetary policy, Kashkari described the current stance as "modestly restrictive," suggesting that it is just slightly contractionary in effect. He acknowledged that the neutral rate remains uncertain but expected more clarity over the coming year as the Fed monitors the economy’s response to rate changes.

Barkin says Fed well-positioned to respond to economic changes

Richmond Fed President Thomas Barkin noted that the economy is "in a good place" and that Fed is now positioned to react flexibly to evolving economic conditions.

Speaking at an event overnight, Barkin highlighted that interest rates are balanced—elevated from recent lows but no longer at peak levels—providing Fed with room to adjust policy as needed.

Barkin observed that more price-sensitive consumer base is contributing to moderating inflation pressures, suggesting that demand adjustments are naturally aiding Fed's inflation objectives.

Additionally, he pointed to the resilience of the labor market, with companies retaining employees and maintaining lower turnover rates, which has provided stability and boosted productivity.

Australia: Wage Inflation Moderating as Expected

First Impressions: The WPI rose 0.8% in the September quarter, on par with Westpac’s forecast and below the market consensus of 0.9%. The market range was from 0.8% to 1.0%. On an annual basis, wages are up 3.5%yr, down from 4.1%yr in June and the peak of 4.2%yr in December 2023. Wage inflation has continued to moderate through 2024, with the six-month annualised pace holding at 3.2%yr compared to 4.9%yr in December 2023. There are no changes to Westpac’s wage forecasts.

In the September quarter, the Wage Price Index (WPI) rose 0.8% (3.5%yr), on par with Westpac’s forecast but a touch softer than the market consensus of 0.9%. It is also below the RBA’s expectation which pointed to a 0.9%qtr rise in both the September and December quarters of 2024. Wage inflation peaked at 4.3%yr in December 2023 and has been drifting lower through 2024, with the six-month annualised pace dropping from 4.9%yr in December 2023 to 3.2%yr in September 2024.

The more critical private sector wages rose 0.8% and this time, was also matched by a 0.8% increase in public sector wages.

The ABS provides (in non-seasonally adjusted terms) the contributions to the quarterly increase in the WPI from Awards, Enterprise Bargaining and Individual Arrangements. Comparing September 2024 to September 2023, the contribution from Enterprise Bargaining has softened to a contribution of 0.46ppt compared to 0.66ppt a year earlier. Individual Arrangements continue their downtrend, contributing 0.59ppt compared to a September 2023 print of 0.74ppt. Meanwhile, the Awards/Minimum Wage contribution was just 0.36ppt compared to 0.63ppt a year earlier.

As the Wage Price Index came in just as Westpac expected, we see no reason to change our end 2024 forecast of 3.2%yr and the June 2025 forecast of 2.9%yr. The RBA is currently forecasting annual wages growth to print 3.4%yr for end 2024 and hold at that rate through to June 2025.

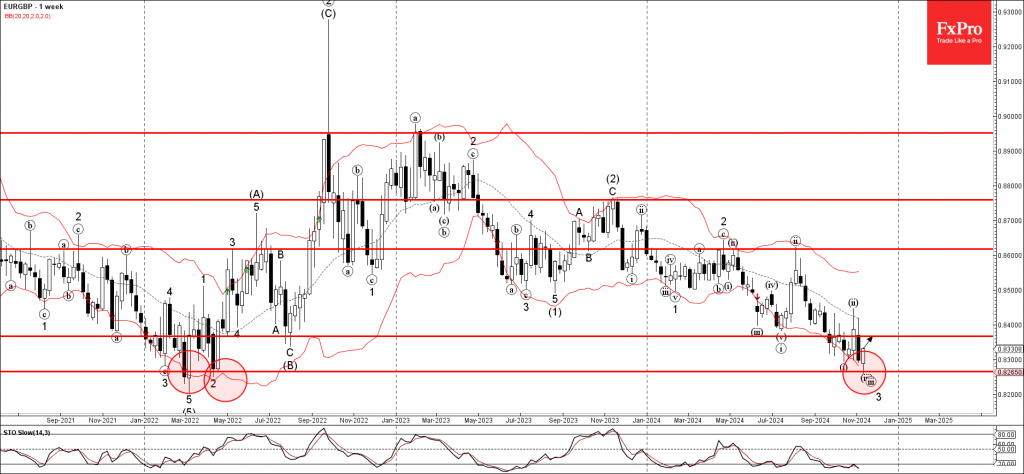

EURGBP Wave Analysis

- EURGBP reversed from long-term support level 0.8265

- Likely to rise to resistance level 0.8365

EURGBP currency pair previously reversed up from the long-term support level 0.8265 (former powerful support from the start of 2022) coinciding with the lower weekly Bollinger Band.

The upward reversal from the support level 0.8265 stopped the previous impulse wave 3.

Given the strength of the nearby support level 0.8265 and the oversold weekly Stochastic, EURGBP currency pair can be expected to rise to the next resistance level 0.8365.

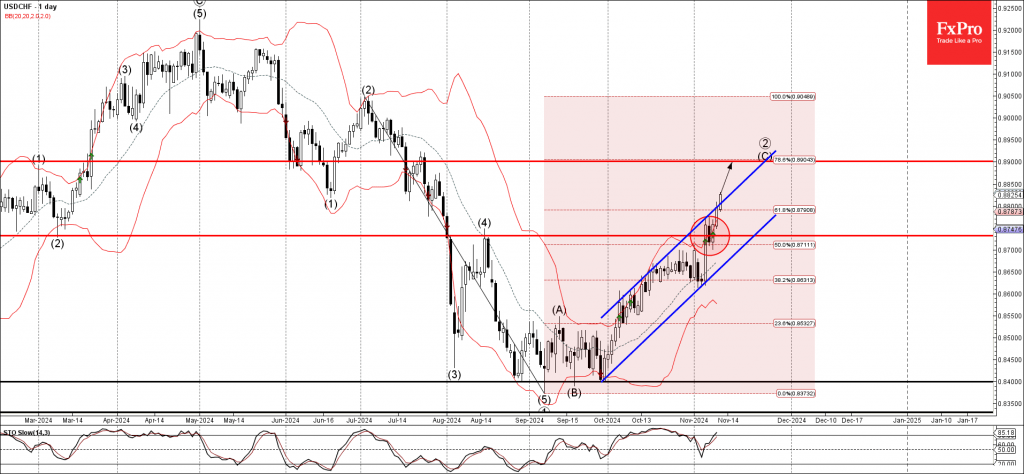

USDCHF Wave Analysis

- USDCHF rising inside impulse wave (C)

- Likely to reach resistance level 0.8900

USDCHF currency pair continues to rise inside the medium-term impulse wave (C), which previously broke the resistance level 0.8730 coinciding with the 50% Fibonacci correction of the downward impulse from July.

The active impulse wave (C) belongs to the longer-term upward impulse sequence (2) from the start of September.

USDCHF currency pair can be expected to rise to the next resistance level 0.8900 (target price for the completion of the active impulse wave (C)).

EURGBP Sell Off Takes a Breather

- EURGBP is in the green today, a tad below 0.8340

- Euro bulls are trying to recover some of their recent losses

- Momentum indicators have turned bearish

The bulls’ failed attempt to push EURGBP above the 100-day simple moving average (SMA) in early November resulted in a protracted sell off, which got an extra boost after Trump’s win. The continued ECB dovishness coupled with the negative newsflow from Germany have also contributed to EURGBP trading at the lowest level since March 2022. EURGBP is edging slightly higher today, with the medium-term trend from the mid-November 2023 peak acting as resistance.

Meanwhile, momentum indicators have turned bearish. The Average Directional Movement Index (ADX) is edging tentatively higher, above its 25-threshold, and thus pointing to a muted bearish trend in EURGBP. Similarly, the RSI has dropped below its midpoint, revealing some degree of bearish pressure. Importantly, the stochastic oscillator has returned to its oversold area. It can hover in this region for a while before showing any signs of a bullish breakout.

Should the bears remain optimistic, they could try to keep EURGBP below the November 20, 2023 descending trendline and then stage another downleg towards the 0.8202-0.8221 area. The January 8, 2012 and March 7, 2022 lows currently reside there, along with the August 8, descending trendline. If successful, the door would then be open to a multi-year low.

On the flip side, the bulls are keen for a move above both the November 20, 2023 trendline and the 0.8304 level. Higher, they could test their determination against August 4, 2022 low at 0.8339 level, which stands a tad below the 50-day SMA at 0.8363. More importantly, a move above the 0.8375-0.8406 region could reverse the current bearish trend.

To sum up, EURGBP bears are in control and potentially preparing for the next downleg, provided the newsflow supports their intentions.