Sample Category Title

NZ First Impressions: RBNZ Survey of Expectations, Q4 2024

Near term inflation expectations have dropped back, but longer-term expectations are up.

Inflation expectations

- One year ahead: 2.05% (Prev: 2.40%, down 35 points)

- Two years ahead: 2.12% (Prev: 2.03%, up 9 points)

- Five years ahead: 2.24% (Prev: 2.07%, up 17 points)

- Ten years ahead: 2.19% (Prev: 2.03%%, up 16 points)

The latest survey of inflation expectations was a mixed bag, but is unlikely to cause much alarm at the RBNZ about either the up or downside risks for inflation. On balance, inflation expectations look consistent with the RBNZ’s medium-term inflation target.

In the detail, expectations for inflation over the coming year have dropped sharply, falling to 2.05% (down from 2.4% previously). That’s consistent with the sharp falls in actual inflation over the past year and our forecast that inflation will remain close to 2% over the coming year.

However, inflation at longer horizons has picked up. Notably, the closely watched measure of expected inflation in two-years’ time has increased to 2.1% (up from 2% last quarter). We also saw expectations for inflation 5 and 10 years ahead rising to 2.2% (both up about 20 ppts compared to the previous survey).

The lift in longer-term inflation expectations follows sharp falls last quarter and leaves them at levels that are still close to the RBNZ’s target.

Overall, we think that today’s survey and other recent data will leave the RBNZ feeling comfortable that pricing behaviour is now well aligned with their medium-term target. Consistent with that, we expect that the RBNZ will deliver another 50bp rate cut next week.

But even with inflation expectations looking well contained, today’s survey highlights that the risks for inflation are not all in one direction. While inflation has fallen sharply over the past year (especially in relation to import prices), we are still seeing strong increases in some domestic costs (like local council rates and insurance chares). Those continued cost increases are limiting the decline in overall inflation. And with related risks for inflation expectations, such costs warrant continued close attention as we head into the new year. We expect that the RBNZ will adopt a more gradual and data dependent approach to policy changes next year.

EUR/USD Makes U-Turn, Risk of More Downsides

Key Highlights

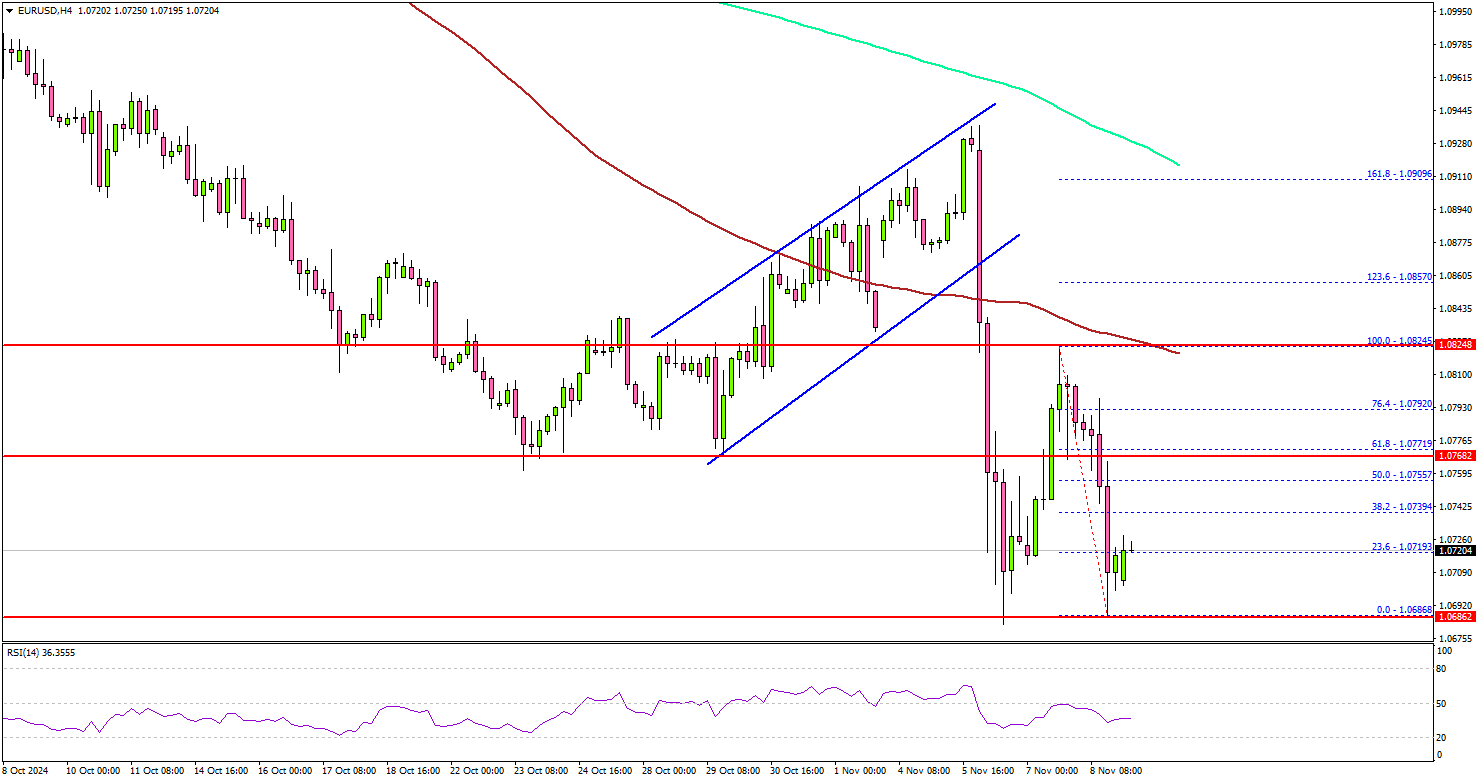

- EUR/USD started a fresh decline from the 1.0945 resistance.

- It traded below a rising channel with support at 1.0880 on the 4-hour chart.

- Gold started a downside correction below the $2,700 level.

- Bitcoin rallied to a new record high above $80,000 and might continue to rise.

EUR/USD Technical Analysis

The Euro started a fresh decline after it failed to surpass 1.0950 against the US Dollar. EUR/USD traded below the 1.0850 support to enter a bearish zone.

Looking at the 4-hour chart, the pair traded below a rising channel with support at 1.0880. It settled below the 1.0800 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

A low was formed at 1.0686 and the pair is now consolidating losses. It is trading near the 23.6% Fib retracement level of the recent decline from the 1.0825 swing high to the 1.0686 low.

On the downside, immediate support sits near the 1.0685 level. The next key support sits near the 1.0650 level. Any more losses could send the pair toward the 1.0620 level.

On the upside, the pair could face resistance near the 1.0755 level. The first key resistance is near the 1.0775 level or the 61.8% Fib retracement level of the recent decline from the 1.0825 swing high to the 1.0686 low.

A close above the 1.0775 level could set the tone for another increase. The next major resistance could be 1.0800, above which the price could accelerate higher toward the 1.0820 resistance.

Looking at Bitcoin, the bulls remain in action and they might even aim for a move toward the $85,000 level in the near term.

Upcoming Economic Events:

- China’s M2 Money Supply (YoY) (Oct) - Forecast +1.2%, versus +6.8% previous.

BoJ affirms core stance: Rate hikes to proceed gradually if economic outlook holds

BoJ's Summary of Opinions from its October 30-31 reiterated its "basic thinking" that it will adjust the degree of monetary accommodation if the outlook for economic activity and prices unfolds as expected. Emphasizing the importance of "communicating effectively" this core message, BoJ aims to manage market expectations carefully.

One member indicated that if economic conditions progress as anticipated, BoJ could "raise the policy interest rate gradually," reaching 1.0% in the second half of fiscal 2025 at the earliest.

Conversely, another member expressed caution, noting the difficulty in confidently conveying a medium-term policy rate path due to "high uncertainties" surrounding the neutral interest rate and the transmission mechanism of monetary policy.

RBNZ 1-yr inflation expectation down, 2-yr’s up

RBNZ's latest Survey reveals that expectations for one-year-ahead annual inflation dropped significantly by -35 basis points from 2.40% to 2.05%, extending a steady downward trend in inflation expectations since Q2 2023. On the other hand, two-year inflation expectations inched up to from 2.03% 2.12% .

For wage inflation, one-year-ahead expectations decreased modestly by -7 basis points to 2.81%, while two-year projections rose from 2.86% to 3.16%.

Growth expectations improved. The mean one-year-ahead GDP growth expectation jumped by 61 basis points to 1.60%, with a smaller increase of 7 basis points for two-year growth expectations to 2.17%.

On the interest rate front, the survey points to further monetary easing ahead. OCR is expected to be 4.20% by the end of Q4 2024, with a sharper decline to 3.33% anticipated by Q3 2025. OCR is currently at 4.75% following a recent 50bps cut in October.

China’s CPI falls back to 0.3% yoy, PPI down -2.9% yoy

In October, China’s CPI grew only 0.3% yoy, below the expected 0.4% yoy, and marking a slight drop from September’s 0.4% yoy. Core CPI, which excludes food and energy prices, rose marginally from 0.1% yoy to 0.2% yoy, suggesting minimal underlying inflationary momentum. Month-over-month, CPI fell by -0.3%, further indicating subdued domestic demand.

Since March last year, China's CPI growth has been hovering around zero, contributing to concerns over prolonged deflationary trends and lackluster domestic consumption. Cumulatively, CPI has grown by only 0.3% from January to October, far below the government's annual target of 3%. These figures underscore subdued consumer activity and insufficient demand to drive price increases.

Meanwhile, China’s PPI saw steeper-than-expected decline, slipping from -2.8% yoy to -2.9% yoy, marking the 25th consecutive month of negative growth. This drop was deeper than market forecasts of -2.5% yoy and signals ongoing pricing pressures within the production sector.

Fed’s Kashkari warns of trade war inflation risks, eyes data for Dec cut

Minneapolis Fed President Neel Kashkari conveyed cautious optimism about the US. inflation outlook during his appearance on CBS's "Face the Nation" on Sunday. Acknowledging that "a lot of progress " was made in reducing inflation, he emphasized that the job is not yet complete, but noted that the economy is "on a good path" toward 2% inflation.

Kashkari anticipates another rate cut in December, contingent upon forthcoming economic data. He stressed the importance of monitoring "what the data looks like" before making a definitive decision.

Addressing concerns about renewed trade war under the new administration, Kashkari remarked that one-time tariffs "shouldn't have an effect long run on inflation."

However, he cautioned that escalating "tit-for-tat" tariff measures between countries could lead to greater uncertainty and have more significant economic implications.

ECB’s Holzmann signals December rate cut, but awaits new forecasts for final decision

Austrian ECB Governing Council member Robert Holzmann indicated that a rate cut in December is "possible". "There is nothing at the moment that would argue against that", he added.

But he alos emphasized that "does not mean it will automatically happen". He emphasized the importance of ECB's upcoming forecasts and data, which will inform the final decision in December.

CHFJPY Wave Analysis

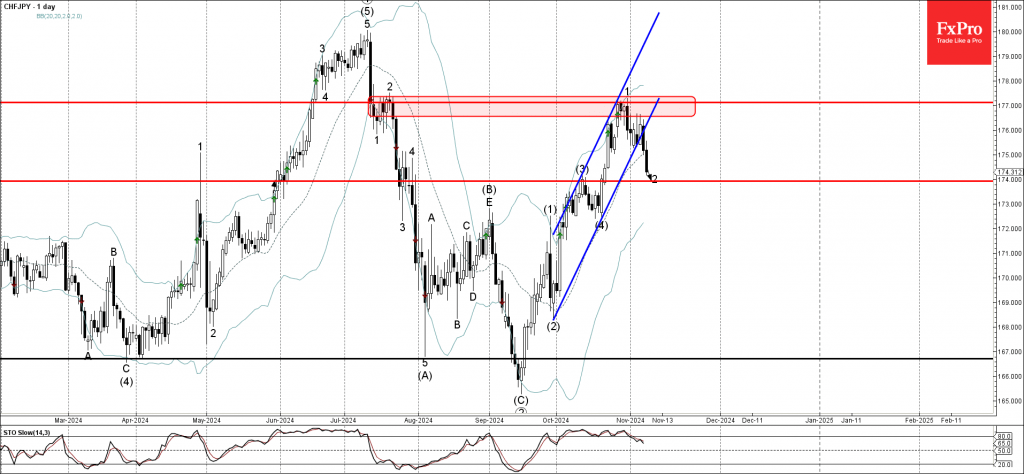

- CHFJPY broke daily up channel

- Likely to fall to support level 174.00

CHFJPY currency pair under bearish pressure after the earlier breakout of the support trendline of the sharp daily up channel from the end of September.

The breakout of this up channel accelerated the active minor corrective wave 2, which started earlier from the key resistance 177.00, which has been reversing the pair from July.

Given the strongly bullish Yen sentiment seen across the currency markets today, CHFJPY currency pair can be expected to fall to the next support level 174.00 (target price for the completion of the active wave 2).

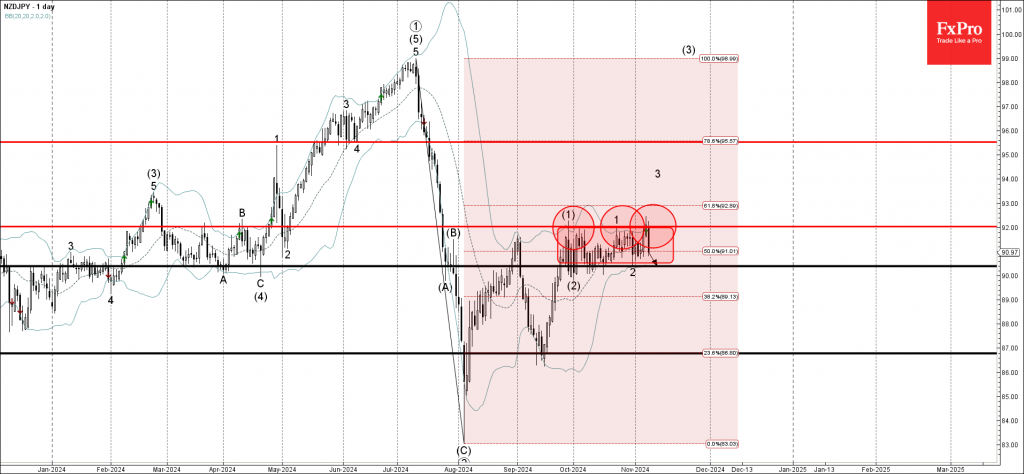

NZDJPY Wave Analysis

- NZDJPY reversed from resistance level 92.00

- Likely to fall to support level 90.40

NZDJPY currency pair recently reversed down from the resistance level 92.00, which is the upper boundary of the narrow sideways price range inside which the pair has been moving from September.

The resistance level 92.00 was strengthened by the upper daily Bollinger Band and by the nearby 61.8% Fibonacci correction of the downward impulse from July.

NZDJPY currency pair can be expected to fall to the next support level 90.40 (lower boundary of the aforementioned price range).