Sample Category Title

Bitcoin Price Restarts Bullish Surge: Is The Next Peak Near?

Key Highlights

- Bitcoin price started a fresh surge after it cleared the $65,000 resistance zone.

- BTC surpassed a major bearish trend line with resistance at $63,200 on the 4-hour chart.

- Gold prices rallied further and traded above the $2,675 resistance.

- EUR/USD is consolidating losses above the 1.0850 zone.

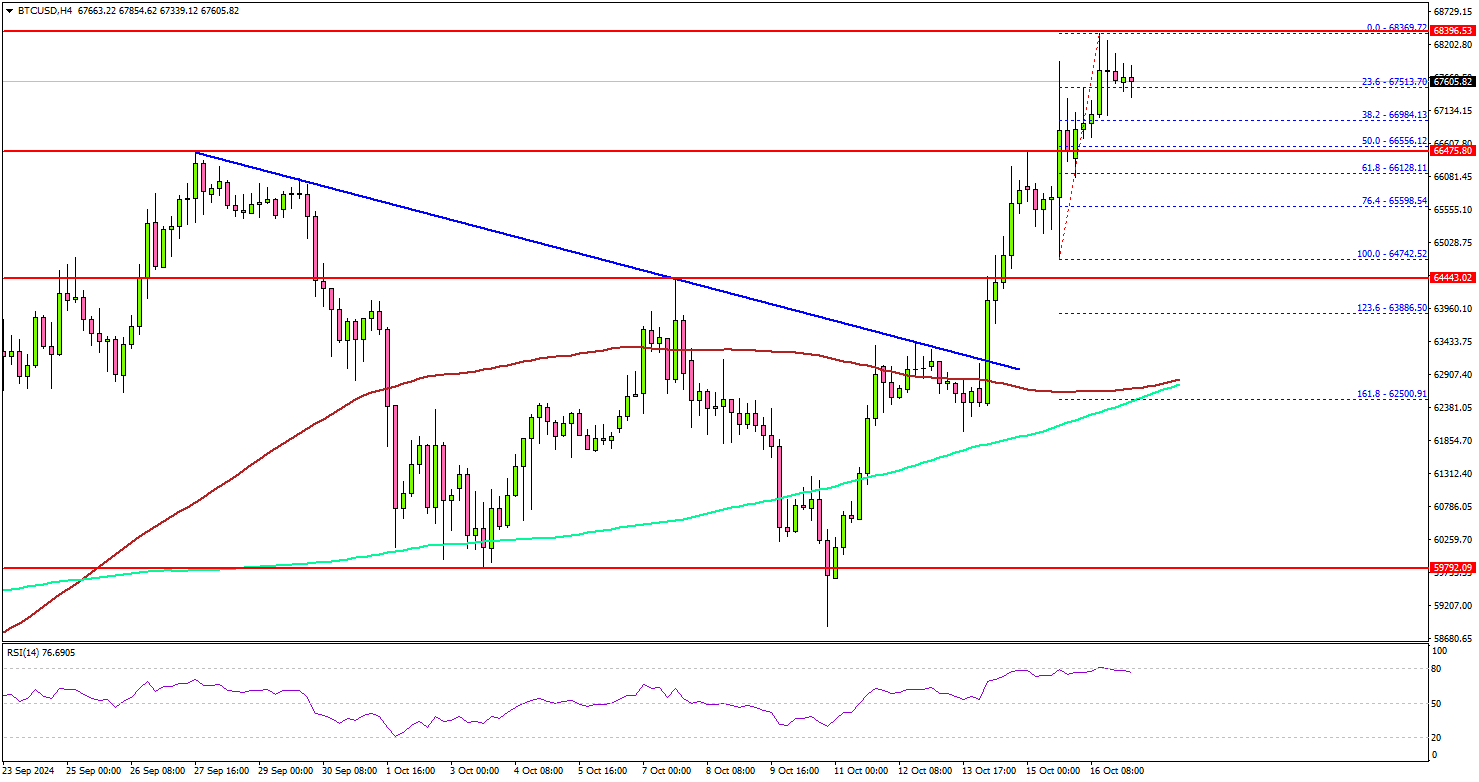

Bitcoin Price Technical Analysis

Bitcoin price started a fresh increase above the $62,500 resistance zone. BTC/USD climbed the $64,000 and $65,000 levels to move into a positive zone.

Looking at the 4-hour chart, the price surpassed a major bearish trend line with resistance at $63,200. It settled above the $65,000 level, the 200 simple moving average (green, 4 hours), and the 100 simple moving average (red, 4 hours).

The increase was such that the price soared above the $67,500 level. It even spiked above $68,000 before the bears appeared. The price is now consolidating gains. Immediate support is near the $66,800 level.

The next key support sits at $66,400. A downside break below $66,400 might send Bitcoin toward the $64,500 support. Any more losses might send the price toward the $63,500 support zone.

On the upside, the price could face resistance near the $68,500 level. The next key resistance is at $69,200. A successful close above $69,200 might start another steady increase. In the stated case, the price may perhaps rise toward the $71,500 level or even a new all-time high.

Looking at EUR/USD, the pair saw a lot of bearish moves and recently started a consolidation phase above the 1.0850 support.

Today’s Economic Releases

- US Initial Jobless Claims - Forecast 258K, versus 258K previous.

- US Retail Sales for Sep 2024 (MoM) – Forecast +0.3%, versus +0.1% previous.

- US Industrial Production for Sep 2024 (MoM) – Forecast -0.2%, versus +0.8% previous.

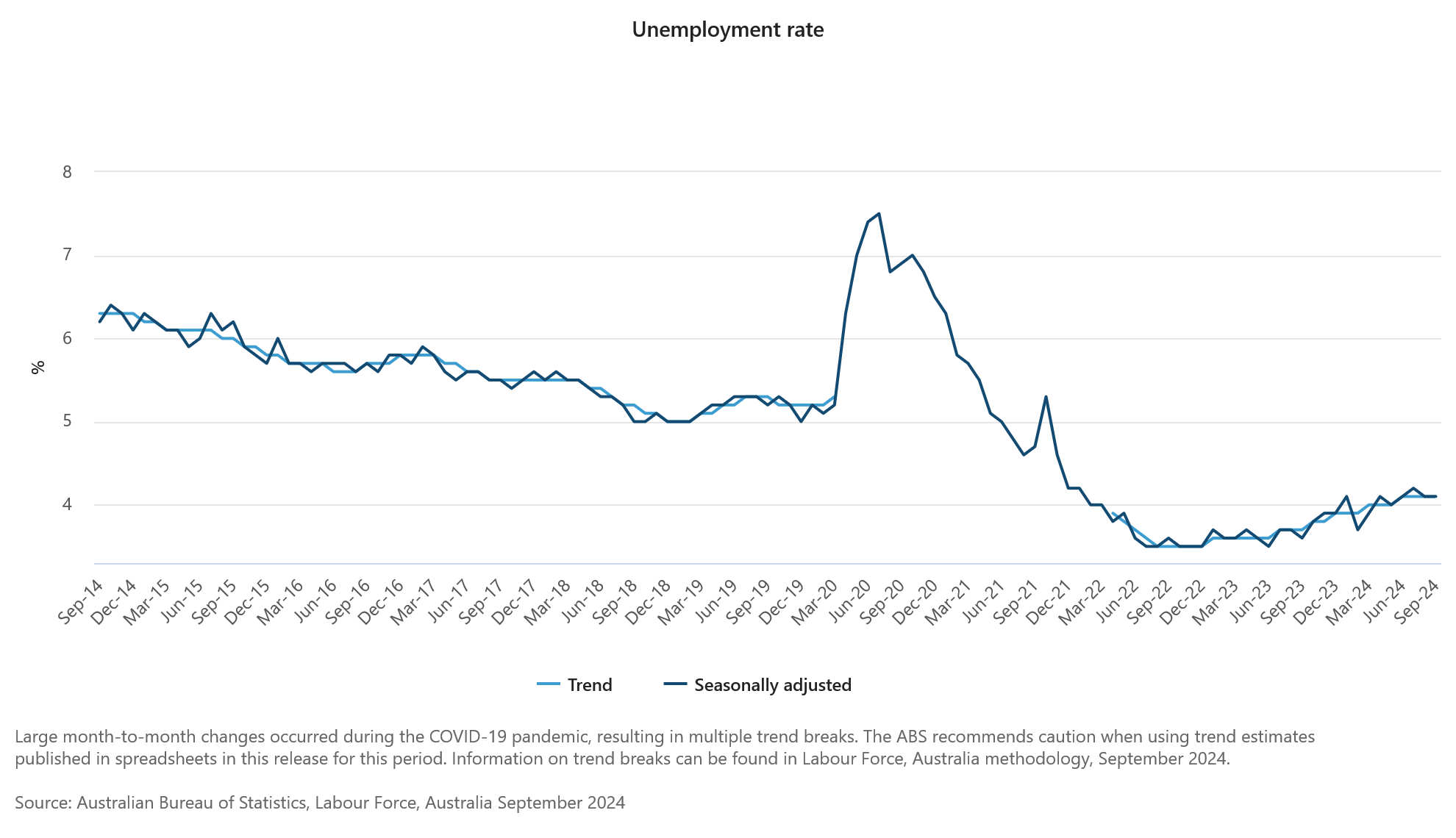

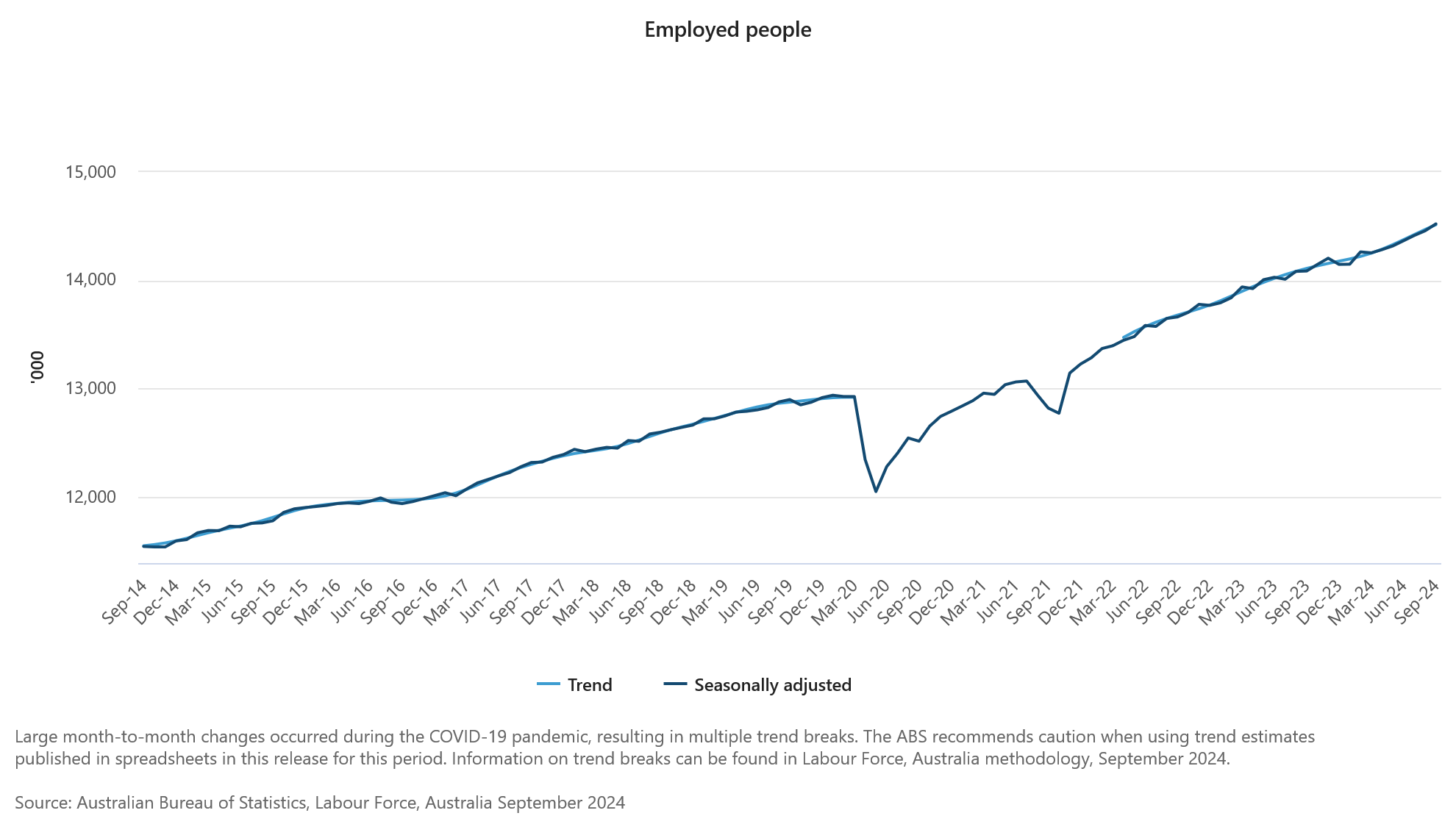

Australia’s employment grows 64.1k in Sep, unemployment rate unchanged at 4.1%

Australia's employment figures for September showed stronger-than-expected growth, with 64.1k jobs added, significantly exceeding forecast of 25.2k. Full-time employment led the gains, rising by 51.6k, while part-time jobs increased by 12.5k.

Unemployment rate remained steady at 4.1%, slightly better than the expected 4.2%. Participation also increased by 0.1% to 67.2%, indicating higher workforce engagement. Monthly hours worked saw a modest rise of 0.3% mom.

Over the past year, employment has grown by 3.1%, outpacing the civilian population growth of 2.5%. This pushed the employment-to-population ratio to a historical high of 64.4%, reflecting robust labor market conditions.

Australia’s NAB business confidence drops to -6 in Q3, inflation pressures ease slightly as margins squeezed

Australia’s NAB quarterly Business Confidence declined from -2 to -6 in Q3. Business conditions also dropped from 5 to 2, with trade conditions falling from 9 to 5, profitability slipping from 2 to 0, and employment conditions down from 5 to 3, signaling softer economic momentum.

Leading indicators weakened, with expected business conditions for the next 3 months falling from 11 to 10, and for the next 12 months from 15 to 12. Forward orders remained negative at -4, and capacity utilization eased from 83.6% to 83.0%. Capital expenditure plans also declined from 24 to 19, indicating reduced investment expectations.

Cost pressures remained persistent. Labor costs grew 1.2%, up from 1.1%, and purchase costs increased to 1.0%, up from 0.9%. Final product price growth, however, slowed from 0.6% to 0.4%, and retail price growth remained steady at 0.7%, suggesting inflationary pressures are easing but at the expense of business margins.

NAB Head of Australian Economics Gareth Spence noted, “Labor cost growth remains elevated, and wage costs are the top issue affecting business confidence. While purchase cost growth persists, the marked drop in final product price growth suggests progress on inflation, though margins are under pressure.”

Full Australia quarterly NAB business confidence release here.

Japan’s exports fall -1.7% yoy in Sep, first decline in 10 months

Japan's exports in September dropped by -1.7% yoy to JPY 9.038T, marking the first annual decline in 10 months. This slump was driven by weaker demand from key trading partners. Exports to China, Japan's largest market, fell by -7.3% yoy, while those to the US dropped by -2.4% yoy.

On the other hand, imports rose modestly by 2.1% yoy to JPY 9.333T, leading to a trade deficit of JPY -294B, the third consecutive monthly shortfall.

In seasonally adjusted terms, there was a small improvement. Exports grew by 2.0% mom to JPY 8.956T, while imports fell by -1.2% mom to JPY 9.144T. This led to a seasonally adjusted trade deficit of JPY -187B.

GBP Price Action Ideas: GBP/USD, GBP/JPY and EUR/GBP

- The GBP has been declining against the USD due to softer-than-expected UK economic data, leading to expectations of more aggressive rate cuts by the Bank of England.

- GBP/USD is at a crucial level of 1.3000, a break below which could lead to further downside.

- GBP/JPY is showing signs of a potential breakout, with price coiling between the 100 and 200-day moving averages.

- EUR/GBP is near the YTD low, with immediate resistance at 0.8400. The pair’s future direction will depend on the GBP’s strength and the ECB’s decision.

The GBP has steadily declined against the greenback in recent weeks, while remaining stable against the Euro. This weakness in the British pound is attributed to market participants pricing in more aggressive rate cuts due to softer-than-expected data.

The Euro meanwhile continues to engage in a tug of war with the GBP but appears to be winning at present, much to my surprise. The JPY yen has been the major loser of late, unable to capitalize on GBP weakness. GBP/JPY continues to inch higher as there remains weakness in the Japanese Yen ahead of the election at the end of the month.

UK Inflation Data Surprise

This morning the UK’s Office for National Statistics released a mild Consumer Price Index (CPI) report for September. It showed that annual inflation dropped to 1.7%. While prices were expected to slow down, they were predicted to decrease to 1.9% from 2.2% in August. Monthly inflation stayed the same.

The most important print however came from services inflation which has been a sticky point for the Bank of England. According to the ONS, services inflation dropped more than expected, from 5.6% to 4.9%. This was not only below what experts predicted but also much lower than the Bank of England’s forecast of 5.5%. This softer result could lead to more interest rate cuts in the upcoming Bank of England meetings this year.

All is not lost for the UK and the Pound as the Bank of England are still priced in to cut rates at around the same pace as the Federal Reserve. Initially the pound had been benefitting from the potential of rate divergence with the US Dollar in particular, however any such hopes appear to have been dashed following the latest UK inflation report.

Technical Analysis

GBP/USD

From a technical standpoint, GBP/USD is at a very important level with the 1.3000 psychological level in play. A daily candle close below this level could open up further downside for the pair.

A daily candle close below the 1.3000 will face support around the 1.2950 handle which an area of confluence which houses the 100-day MA. Below this we do have the long term ascending trendline as well which could come into play for the first time since the previous touch on August 8.

There are two scenarios that could develop in the day/days ahead. The first one being a bounce of the 100-day MA and a retest of the 1.3000 or potentially the 1.3100 handle (pink box on the chart) before the downtrend continues.

The second scenario, is a continued selloff until a touch of the trendline before a bounce occurs. At this stage both of these events are plausible as I do not see enough bearish pressure for a clean break of the ascending trendline at this stage. Now I could be wrong and we of course may break through the trendline as well, but I believe such a move may require a catalyst of sorts before it materializes.

Support

- 1.2950 (100-day MA)

- 1.2900

- 1.2793 (200-day MA)

Resistance

- 1.3040

- 1.3100

- 1.3143

GBP/USD Daily Chart, October 16, 2024

Source: TradingView.com (click to enlarge)

GBP/JPY

GBP/JPY has been inching its way higher since bottoming out on August 5. There was another push down to the mid 180s on September 16 before the move higher began once more.

GBP/JPY appears poised for a breakout after looking at recent price action. Price has been coiling between the 100 and 200-day MA since October 4. Usually when price is constricted in such a way, the longer the breakout takes the more aggressive it is.

On a daily timeframe a break and daily candle close below the 190.00 lower swing high would invalidate the bullish trend.

For now though a break to the upside seems more plausible based on price action and the overall trend.

GBP/JPY Daily Chart, October 16, 2024

Source: TradingView.com (click to enlarge)

Support

- 193.40 (200-day MA)

- 190.00

- 187.60

Resistance

- 195.40 (100-day MA)

- 198.00

- 200.00

EUR/GBP

EUR/GBP remains near the YTD low around the 0.8300 handle. The pair is enjoying a bullish bounce today but there does appear to be significant technical hurdles if the GBP is to lose more ground to the Euro.

Immediate resistance rests at 0.8400 with a key area of confluence resting just above. The region between 0.8425-0.8450 plays host to the 50 and 100-day MAs as well as the most recent swing high.

Conversely, should the GBP strengthen in light of the ECB decision on Thursday then the 2022 lows around 0.8200 may become a real possibility.

EUR/GBP Daily Chart, October 16, 2024

Source: TradingView.com (click to enlarge)

Support

- 0.8311

- 0.8250

- 0.8200

Resistance

- 0.8400

- 0.8425

- 0.8447

US Dollar Index (DXY) Outlook: DXY Breaches the 100-day MA, Will Rally Continue?

- The US Dollar Index (DXY) continues to advance due to a lack of impactful US data and expectations of robust retail sales.

- Donald Trump’s comments on tariffs and the Federal Reserve’s independence.

- The DXY faces technical challenges, with the RSI in overbought territory, but the overall outlook remains bullish.

Most Read:

The US Dollar Index (DXY) continues its advance with the lack of high impact US data keeping the greenback on the front foot. A move lower in the DXY may need a batch of softer US data which thus far has not been forthcoming. US retail sales this week is expected to remain robust which will keep the Dollar supported.

Yesterday, Donald Trump addressed an event where he highlighted two key market issues: tariffs and the Federal Reserve’s independence. He took a notably hawkish stance on protectionism, specifically focusing on U.S. car imports from Europe and Mexico. Regarding the Fed, he stated he wouldn’t interfere with its independence, yet asserted that the president should have a voice in rate decisions.

As elections draw closer in the US we may see demand for the US Dollar increase. The uncertainty around the election could help the US Dollars safe haven appeal and thus keep the greenback advancing until after the election.

Markets are now expecting less aggressive Fed rate cuts in November and December which does bode well for the USD. Policymakers from the Federal Reserve continue to caution around the rate cut cycle, Governor Waller elaborated on this in a speech delivered at Stanford University.

Governor Waller elaborated further stating that the baseline expectation remains to gradually lower the policy rate over the coming year, regardless of short-term developments. When questioned about the job market’s current state, Waller noted, “The labor market is still robust, even though labor demand is easing.”

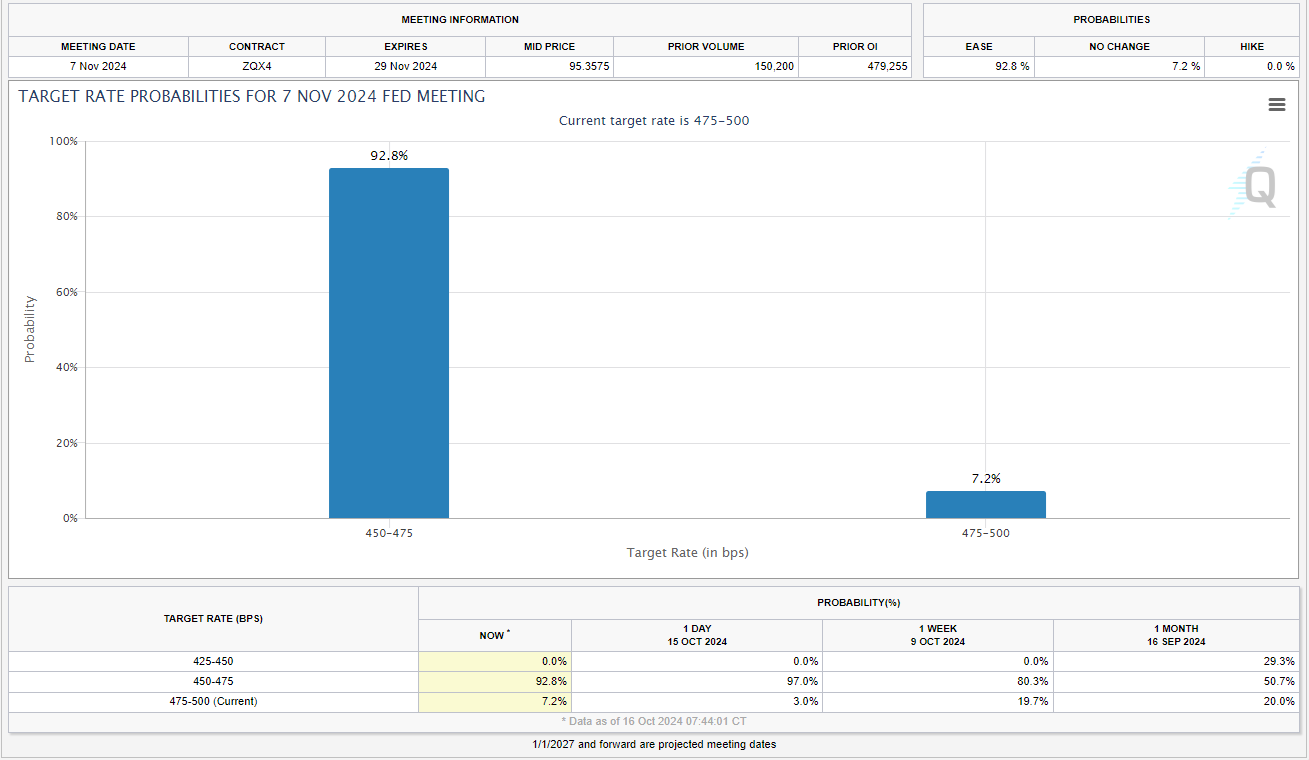

US Federal Reserve Rate Cut Probabilities, November Meeting

Source: CME FedWatch Tool

The outlook for the Dollar remains bullish despite some technical concerns. How much further can the rally go?

Economic Data Ahead

The week ahead is a relatively quiet one when it comes to high impact US data. The only notable event on the calendar this week is retail sales which market participants believe will come in better than expected.

Technical Analysis – US Dollar Index

The US dollar’s rally has been an impressive one, but there are a host of challenges that lie in wait from a technical perspective.

Firstly the RSI on the daily has finally crossed into overbought territory. Now, the issue with this is markets can oftentimes be in overbought on the RSI but continue to rise. Having broken above the 100-day MA for the first time since July with a daily candle close above this MA setting the tone for further gains.

Immediate resistance is at the confluence area which houses the 200-day MA around the 103.70 handle with further resistance areas resting at 104.00 and the psychological 105.00 handle.

Conversely a retracement here may find support at 103.00, 102.16 and 101.00

US Dollar Index Chart, October 16, 2024

Source: TradingView (click to enlarge)

Support

- 103.00

- 102.16

- 101.00

Resistance

- 103.70

- 104.00

- 105.00

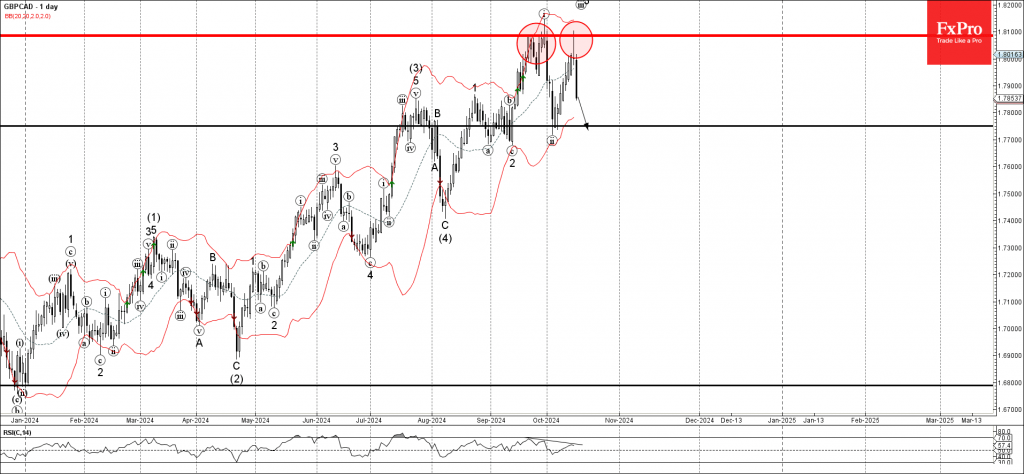

GBPCAD Wave Analysis

- GBPCAD reversed from resistance zone

- Likely to fall to support level 1.7750

GBPCAD currency pair recently reversed down from the key resistance zone between the strong resistance level 1.8085 (which stopped the previous impulse wave i) and the upper daily Bollinger Band.

The downward reversal from this resistance zone created the well-formed daily Japanese candlesticks reversal pattern Shooting Star Doji.

Given the strength of the resistance level 1.8085 and the bearish divergence on the daily RSI, GBPCAD currency pair can be expected to fall further to the next support level 1.7750 (former low of wave ii from the start of this month).

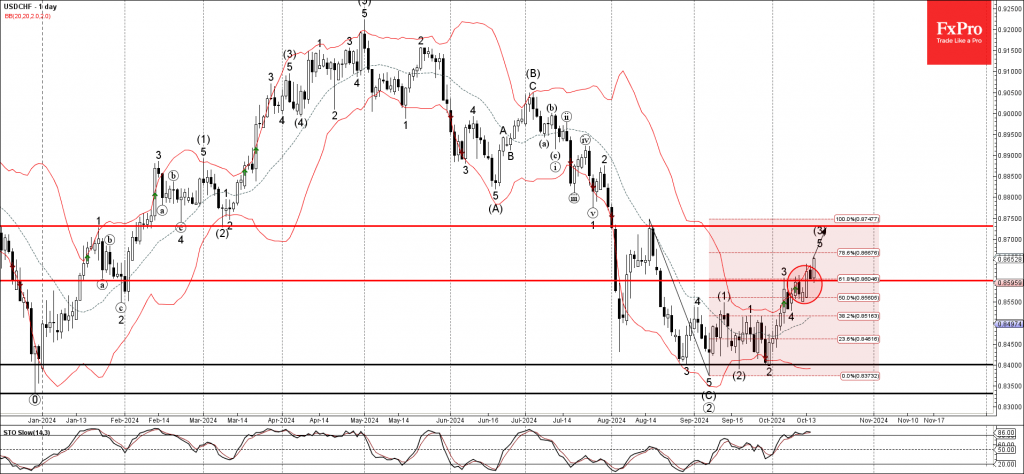

USDCHF Wave Analysis

- USDCHF broke resistance zone

- Likely to rise to resistance level 0.8730

USDCHF currency pair recently broke the resistance zone between the resistance level 0.8600 (which stopped the previous impulse wave 3) and the 61.8% Fibonacci correction of the downward impulse from August.

The breakout of this resistance zone accelerated the minor impulse wave 5 of the higher order impulse wave (3) from September.

Given the continuation of the bullish US dollar sentiment, coupled with significant Swiss franc outflows, USDCHF currency pair can be expected to rise further to the next resistance level 0.8730 (former monthly high from August).

Sunset Market Commentary

Markets

EUR/GBP spiked from 0.8325 to 0.8375 following September UK inflation numbers, but the euro isn’t strong enough these days to profit from GBP-weakness. Even as UK yields drop 8 bps (30-yr) to 11 bps (2-yr) across the curve. Headline inflation was flat in M/M-terms, resulting in the first sub-2% inflation print since April 2021. As is for Europe and the ECB, inflation is expected to move back above the BoE’s 2% inflation target toward year-end as energy base effects switch signs. Transport-related prices (petrol prices,…) and services costs (-0.3% M/M; mainly airfares) were the main monthly negative contributors. Core CPI slowed to 0.1% M/M and 3.2% Y/Y (from 3.6% Y/Y; lowest since September 2021). Services inflation recorded a first below-5% Y/Y figure since May 2022 (4.9% from 5.6%), again mainly because of the volatile airfare component. Core services inflation likely slowed less, from 5.5% Y/Y to 5.3% Y/Y, warning against overinterpretation of today’s numbers. In combination with yesterday’s waning wage pressure, they nevertheless suffice for the Bank of England to pursuit governor Bailey’s more activist approach. The parallel with the ECB remains. The BoE started off with a 25 bps rate cut in August (albeit a close 5-4 call), next skipped a meeting in September, to make monetary policy again less restrictive in November (25 bps rate cut discounted). Backed by a new Monetary Policy Report, the market expects the BoE to prepare the road for more regular rate cuts from there on. The UK government’s 2025 budget (presented at the end of the month) is a wildcard, but we don’t expect it to derail the BoE’s plans.

Trading on main European and US markets is uneventful, counting down to tomorrow’s ECB policy meetings and US weekly jobless claims and retail sales. Core bonds regain some additional ground with German Bunds outperforming US Treasuries in the process. Brent crude prices hold near the recent sell-off lows around $74/b while EUR/USD treads water just below 1.09. European stock markets (-0.5%) fail to recover from yesterday’s ASML-triggered setback. Key US indices start the session fairly mixed.

News & Views

The Economic Experts survey, a quarterly study conducted by the Ifo Institute and the Swiss Economic Policy Institute, shows that experts from around the world expect inflation rates to remain above central banks’ targets. Ifo researcher Niklas Potrafke concludes that “due to these stagnating inflation expectations, central banks could hold back on further interest rate cuts.” Worldwide, inflation could reach 4% in 2024, 3.9 % next year and 3.6 % in 2027. Inflation expectations for 2024 in Western Europe (2.5%) and North America (2.7%) are well below the global average. For 2027, experts still expect 2.1% in Western Europe and 2.4% in North America. In other parts of Europe, inflation expectations for 2027 are higher: 2.7% for Northern Europe, 3% for Southern Europe, and 5.9% for Eastern Europe. Among the regions with particularly high inflation expectations of more than 20% are South America and large parts of Africa.

Czech National Bank (CNB) board member Holub explained why he dissented at the September 25 monetary policy meeting. At that meeting, the CNB decided to cut the policy rate by 25 bps to 4.25%. Holub voted for a 50 bps reduction. Holub’s risk assessment is slightly more anti-inflationary while the Board in general sees risks to meeting the inflation target as mainly balanced. Current inflation and the near target outlook combined with moderate downside risks, according to Holub allow a forward looking approach to monetary policy with the focus on the medium term. Finetuning on the basis of incoming data is less appropriate given lags in the transmission of policy. At the same time, the economy is developing below potential and is recovering slowly. Fiscal policy has been restrictive throughout the year, hampering the economic recovery, in particular household consumption. Fed and ECB cuts are reducing the risk of a significant weakening of the korona even as domestic demand is weak. In this context, Holub sees risks that the negative effects of an excessively tight monetary policy would result in lower growth and inflation easing below target. Holub still votes at the November 7 meeting, but leaves the board in December. KBC expects the CNB to cut rates at the 3 upcoming meetings to 3.5% in February when a longer pause might kick in or what even might be the’ low’ of the cycle.