Sample Category Title

EUR/GBP Weekly Outlook

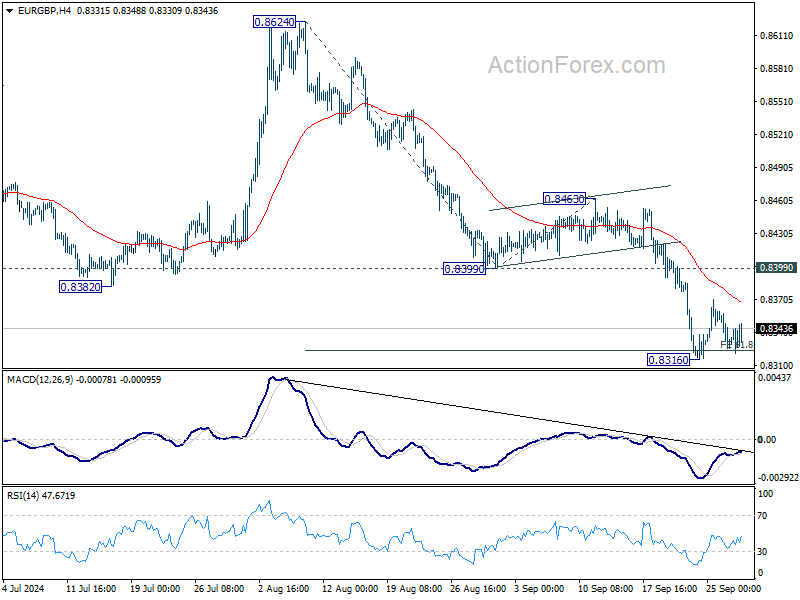

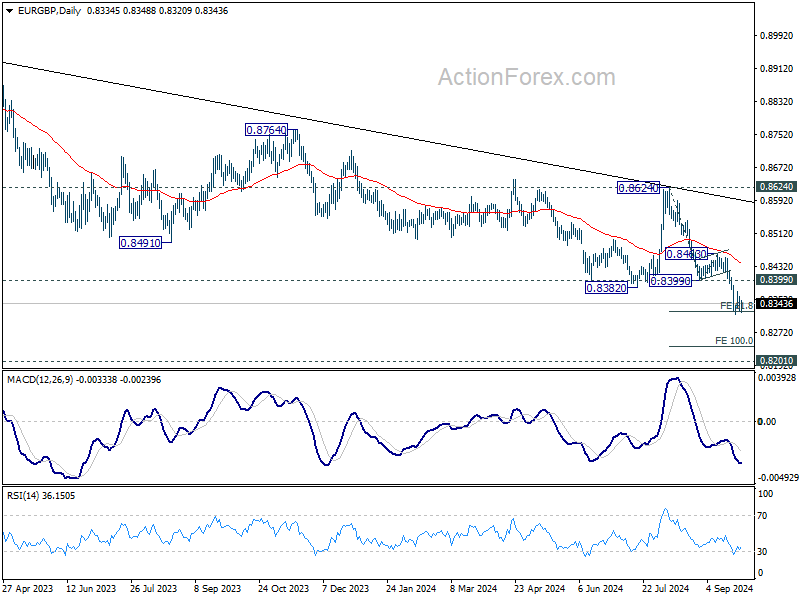

EUR/GBP's fall from 0.8624extended lower last week but recovered after hitting 61.8% projection of 0.8624 to 0.8399 from 0.8463 at 0.8324. Initial bias stays neutral this week for consolidations, and outlook will stay bearish as long as 0.8399 support turned resistance holds. On the downside, below 0.8316 will resume the fall from 0.8624 to 100% projection at 0.8237 next.

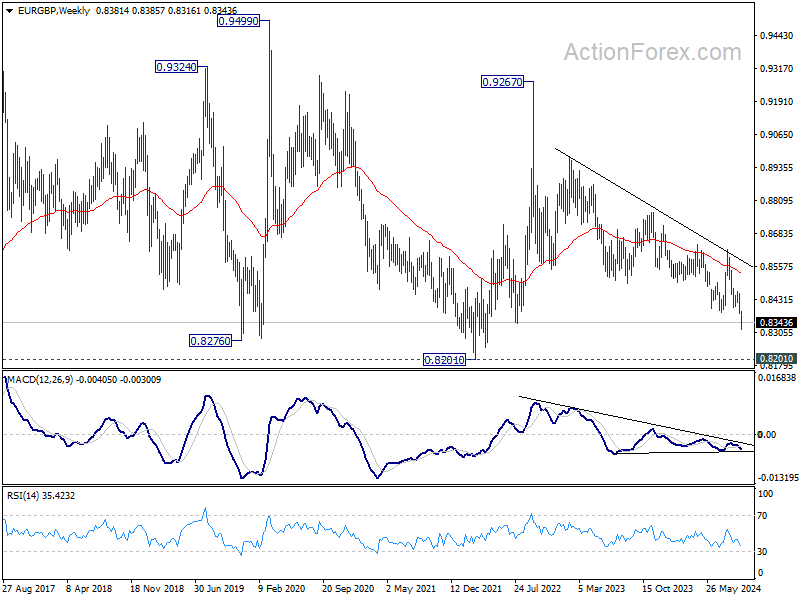

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.

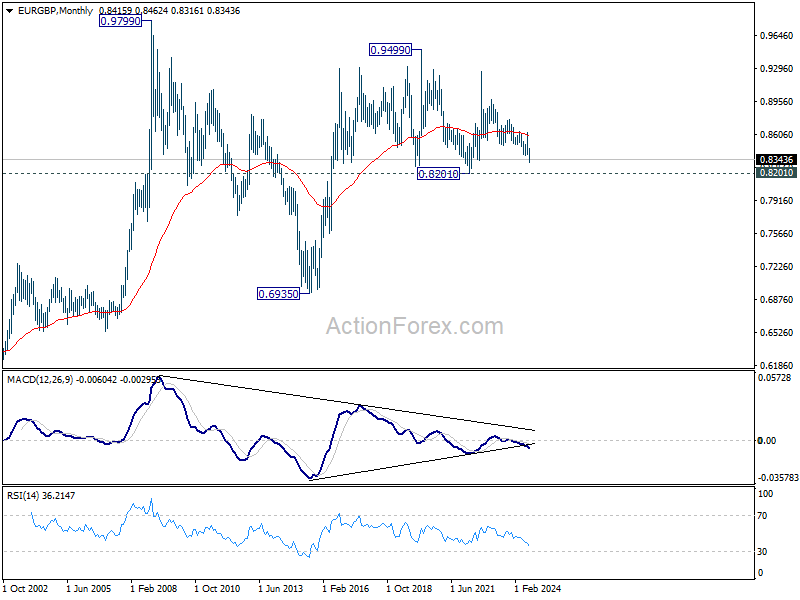

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

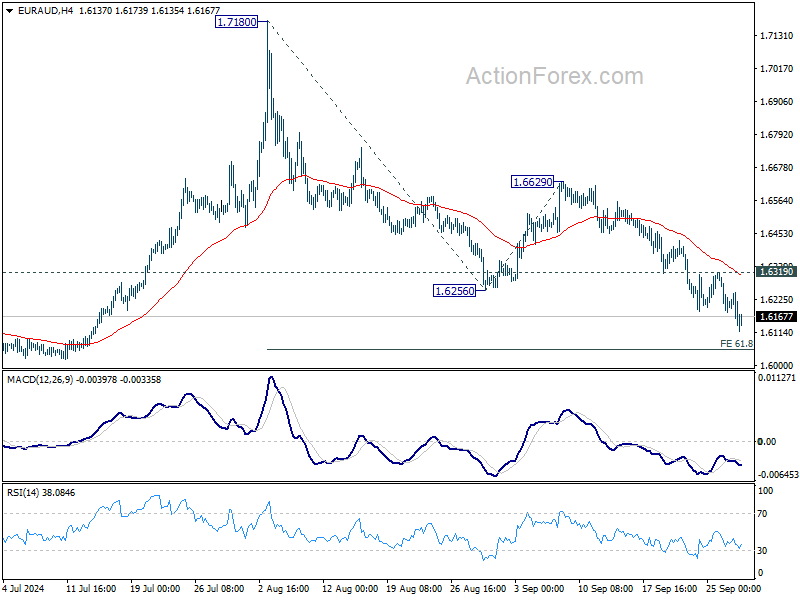

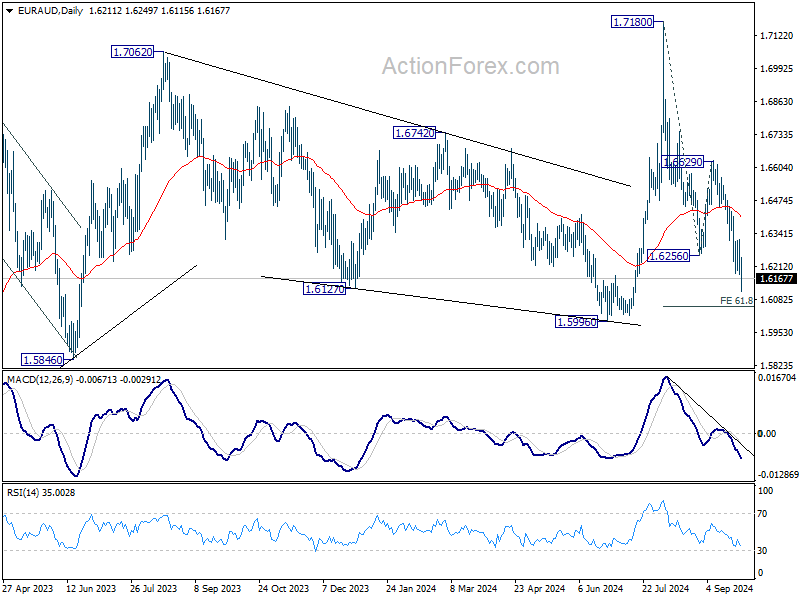

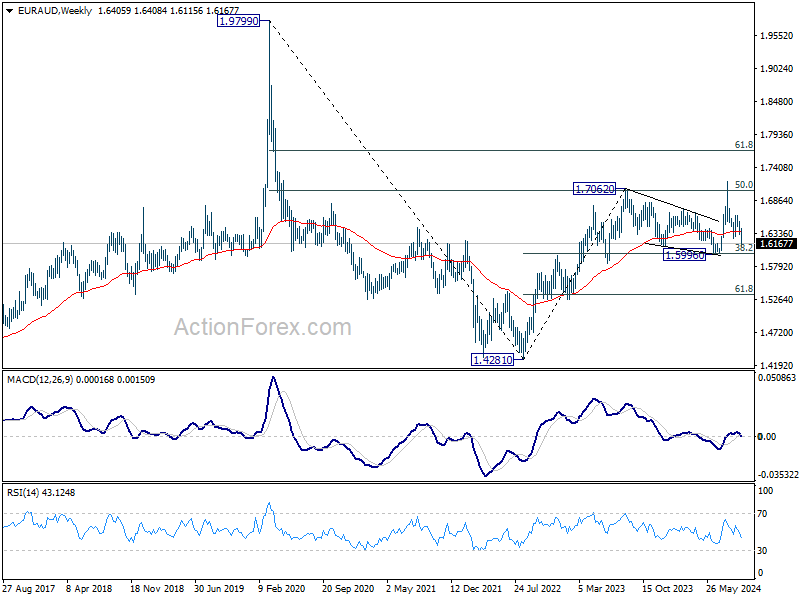

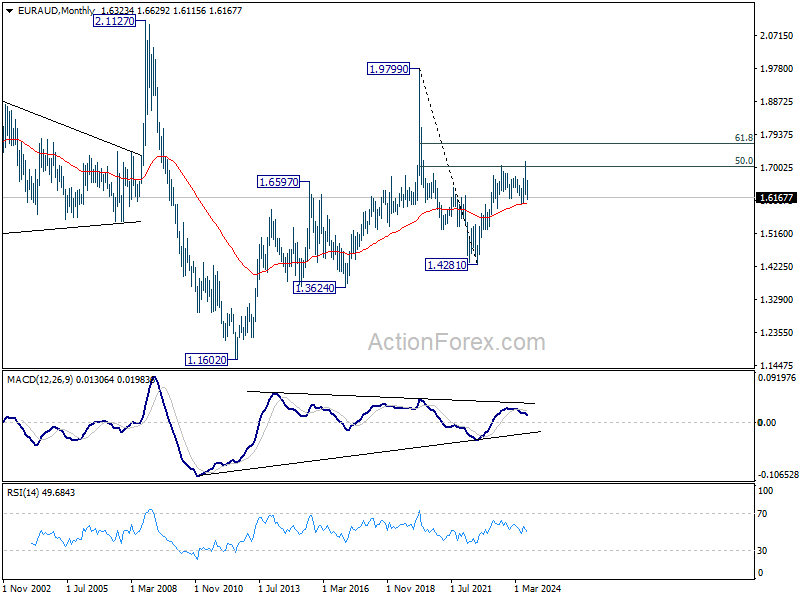

EUR/AUD Weekly Outlook

EUR/AUD's fall from 1.7180 resumed by breaking through 1.6256 last week. Initial bias stays on the downside this week for 61.8% projection of 1.7180 to 1.6256 from 1.6629 at 1.6058. Strong support should be seen from 1.5996 to contain downside and bring rebound. On the upside, above 1.6319 resistance will turn intraday bias neutral first.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still in favor to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5999) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

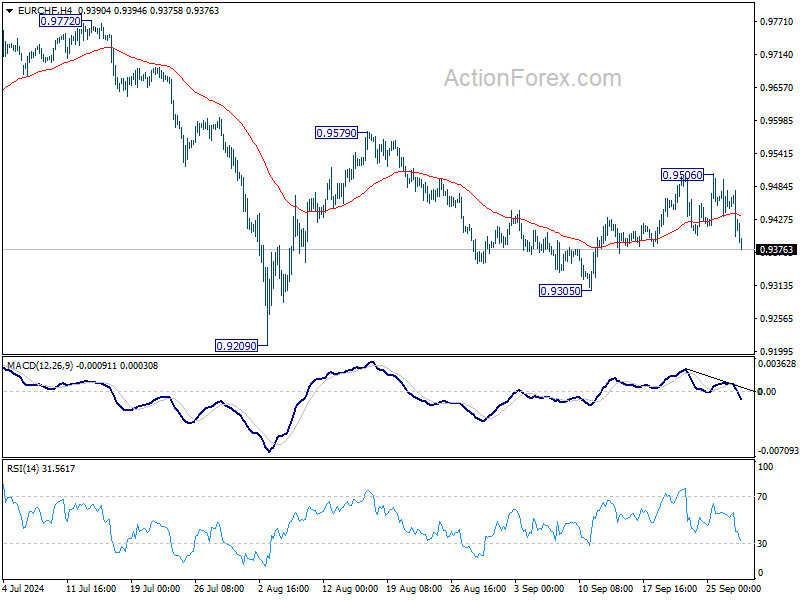

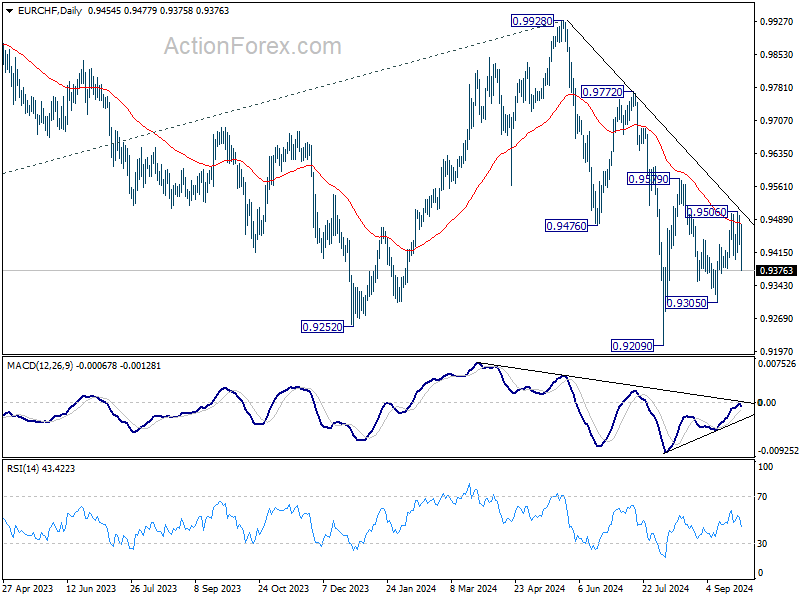

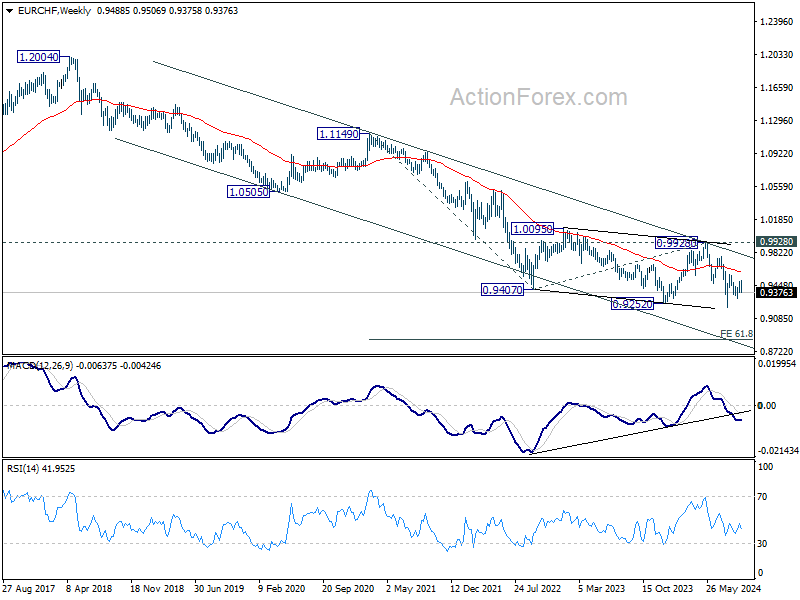

EUR/CHF Weekly Outlook

EUR/CHF reversed after edging higher to 0.9506 but stays above 0.9305 support. Initial bias remains neutral this week first. On the upside, above 0.9506 will resume the rebound from 0.9305 to 0.9579 resistance. However, break of 0.9305 will resume the fall for 0.9579 to retest 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

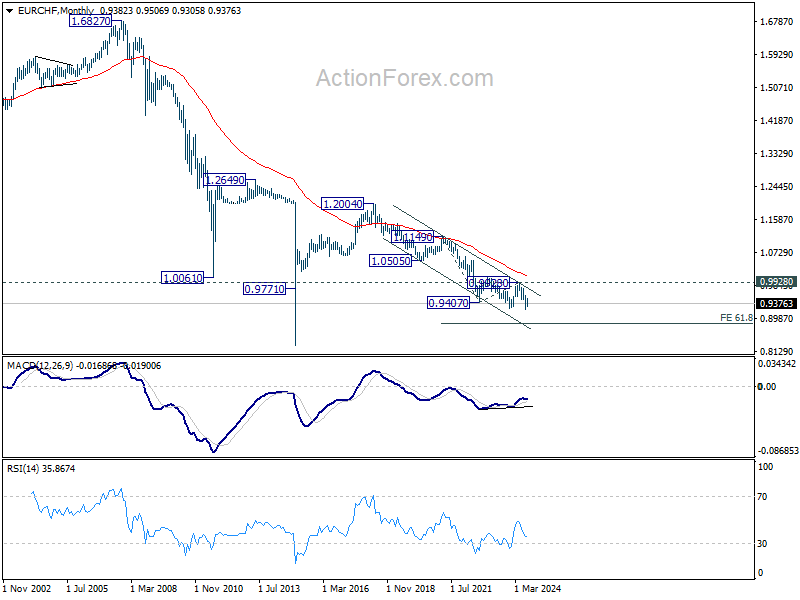

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

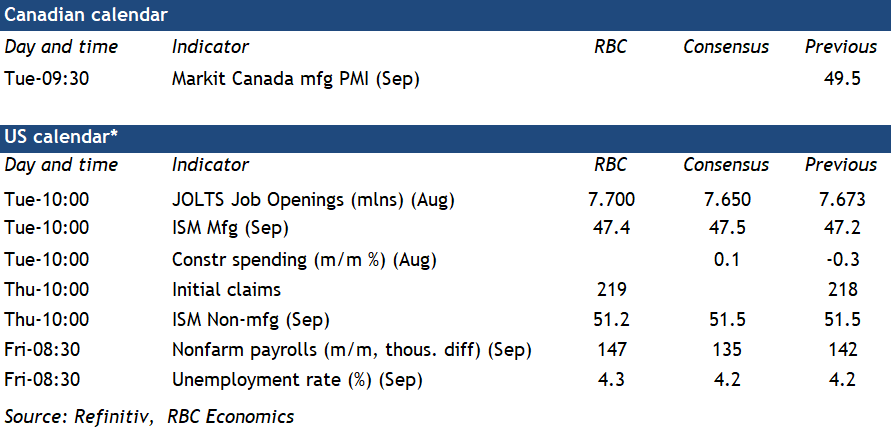

Summary 9/30 – 10/4

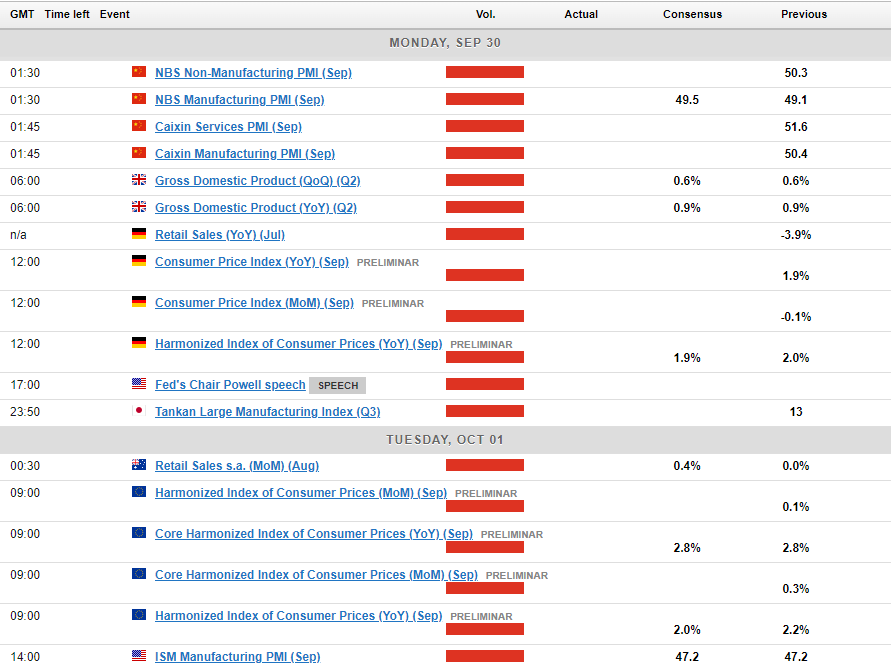

Monday, Sep 30, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Aug P | -0.50% | 3.10% |

| 23:50 | JPY | Retail Trade Y/Y Aug | 2.60% | 2.60% |

| 01:00 | NZD | ANZ Business Confidence Sep | 50.6 | |

| 01:30 | AUD | Private Sector Credit M/M Aug | 0.50% | 0.50% |

| 01:30 | CNY | NBS Manufacturing PMI Sep | 49.5 | 49.1 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Sep | 50.4 | 50.3 |

| 01:45 | CNY | Caixin Manufacturing PMI Sep | 50.5 | 50.4 |

| 01:45 | CNY | Caixin Services PMI Sep | 51.5 | 51.6 |

| 05:00 | JPY | Housing Starts Y/Y Aug | -3.00% | -0.20% |

| 05:00 | JPY | Consumer Confidence Index Sep | 36.7 | |

| 06:00 | EUR | Germany Import Price Index M/M Aug | -0.30% | -0.40% |

| 06:00 | GBP | GDP Q/Q Q2 F | 0.60% | 0.60% |

| 07:00 | CHF | KOF Economic Barometer Sep | 102 | 101.6 |

| 08:30 | GBP | M4 Money Supply M/M Aug | 0.20% | 0.30% |

| 08:30 | GBP | Mortgage Approvals Aug | 64K | 62K |

| 12:00 | EUR | Germany CPI M/M Sep P | 0.10% | -0.10% |

| 12:00 | EUR | Germany CPI Y/Y Sep P | 1.90% | |

| 13:45 | USD | Chicago PMI Sep | 46.5 | 46.1 |

| 21:45 | NZD | Building Permits M/M Aug | 26.20% | |

| 22:00 | NZD | NZIER Business Confidence Q3 | -44 | |

| 23:30 | JPY | Unemployment Rate Aug | 2.60% | 2.70% |

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 12 | 13 |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 14 | |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q3 | 32 | 33 |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q3 | 27 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 11.10% | |

| 23:50 | JPY | BoJ Summary of Opinions |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Aug P | |

| Forecast: -0.50% | Previous: 3.10% | ||

| 23:50 | JPY | Retail Trade Y/Y Aug | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 01:00 | NZD | ANZ Business Confidence Sep | |

| Forecast: | Previous: 50.6 | ||

| 01:30 | AUD | Private Sector Credit M/M Aug | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 01:30 | CNY | NBS Manufacturing PMI Sep | |

| Forecast: 49.5 | Previous: 49.1 | ||

| 01:30 | CNY | NBS Non-Manufacturing PMI Sep | |

| Forecast: 50.4 | Previous: 50.3 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Sep | |

| Forecast: 50.5 | Previous: 50.4 | ||

| 01:45 | CNY | Caixin Services PMI Sep | |

| Forecast: 51.5 | Previous: 51.6 | ||

| 05:00 | JPY | Housing Starts Y/Y Aug | |

| Forecast: -3.00% | Previous: -0.20% | ||

| 05:00 | JPY | Consumer Confidence Index Sep | |

| Forecast: | Previous: 36.7 | ||

| 06:00 | EUR | Germany Import Price Index M/M Aug | |

| Forecast: -0.30% | Previous: -0.40% | ||

| 06:00 | GBP | GDP Q/Q Q2 F | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 07:00 | CHF | KOF Economic Barometer Sep | |

| Forecast: 102 | Previous: 101.6 | ||

| 08:30 | GBP | M4 Money Supply M/M Aug | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 08:30 | GBP | Mortgage Approvals Aug | |

| Forecast: 64K | Previous: 62K | ||

| 12:00 | EUR | Germany CPI M/M Sep P | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 12:00 | EUR | Germany CPI Y/Y Sep P | |

| Forecast: | Previous: 1.90% | ||

| 13:45 | USD | Chicago PMI Sep | |

| Forecast: 46.5 | Previous: 46.1 | ||

| 21:45 | NZD | Building Permits M/M Aug | |

| Forecast: | Previous: 26.20% | ||

| 22:00 | NZD | NZIER Business Confidence Q3 | |

| Forecast: | Previous: -44 | ||

| 23:30 | JPY | Unemployment Rate Aug | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | |

| Forecast: 12 | Previous: 13 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | |

| Forecast: | Previous: 14 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q3 | |

| Forecast: 32 | Previous: 33 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q3 | |

| Forecast: | Previous: 27 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | |

| Forecast: | Previous: 11.10% | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

Tuesday, Oct 1, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Sep F | 49.6 | 49.6 |

| 00:30 | AUD | Retail Sales M/M Aug | 0.40% | 0.00% |

| 00:30 | AUD | Building Permits M/M Aug | -4.30% | 10.40% |

| 06:30 | CHF | Real Retail Sales Y/Y Aug | 2.60% | 2.70% |

| 07:30 | CHF | Manufacturing PMI Sep | 48.2 | 49 |

| 07:45 | EUR | Italy Manufacturing PMI Sep | 49.4 | 49.4 |

| 07:50 | EUR | France Manufacturing PMI Sep F | 44 | 44 |

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 40.3 | 40.3 |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 44.8 | 44.8 |

| 08:30 | GBP | Manufacturing PMI Sep F | 51.5 | 51.5 |

| 09:00 | EUR | Eurozone CPI Y/Y P | 1.90% | 2.20% |

| 09:00 | EUR | Eurozone CPI Core Y/Y P | 2.70% | 2.80% |

| 13:30 | CAD | Manufacturing PMI Sep | 49.5 | |

| 13:45 | USD | Manufacturing PMI Sep F | 47 | 47 |

| 14:00 | USD | ISM Manufacturing PMI Sep | 47.8 | 47.2 |

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 55 | 54 |

| 14:00 | USD | Construction Spending M/M Aug | 0.20% | -0.30% |

| 23:50 | JPY | Monetary Base Y/Y Sep | 0.80% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Sep F | |

| Forecast: 49.6 | Previous: 49.6 | ||

| 00:30 | AUD | Retail Sales M/M Aug | |

| Forecast: 0.40% | Previous: 0.00% | ||

| 00:30 | AUD | Building Permits M/M Aug | |

| Forecast: -4.30% | Previous: 10.40% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Aug | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 07:30 | CHF | Manufacturing PMI Sep | |

| Forecast: 48.2 | Previous: 49 | ||

| 07:45 | EUR | Italy Manufacturing PMI Sep | |

| Forecast: 49.4 | Previous: 49.4 | ||

| 07:50 | EUR | France Manufacturing PMI Sep F | |

| Forecast: 44 | Previous: 44 | ||

| 07:55 | EUR | Germany Manufacturing PMI Sep F | |

| Forecast: 40.3 | Previous: 40.3 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | |

| Forecast: 44.8 | Previous: 44.8 | ||

| 08:30 | GBP | Manufacturing PMI Sep F | |

| Forecast: 51.5 | Previous: 51.5 | ||

| 09:00 | EUR | Eurozone CPI Y/Y P | |

| Forecast: 1.90% | Previous: 2.20% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y P | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 13:30 | CAD | Manufacturing PMI Sep | |

| Forecast: | Previous: 49.5 | ||

| 13:45 | USD | Manufacturing PMI Sep F | |

| Forecast: 47 | Previous: 47 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | |

| Forecast: 47.8 | Previous: 47.2 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | |

| Forecast: 55 | Previous: 54 | ||

| 14:00 | USD | Construction Spending M/M Aug | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 23:50 | JPY | Monetary Base Y/Y Sep | |

| Forecast: 0.80% | Previous: 0.60% | ||

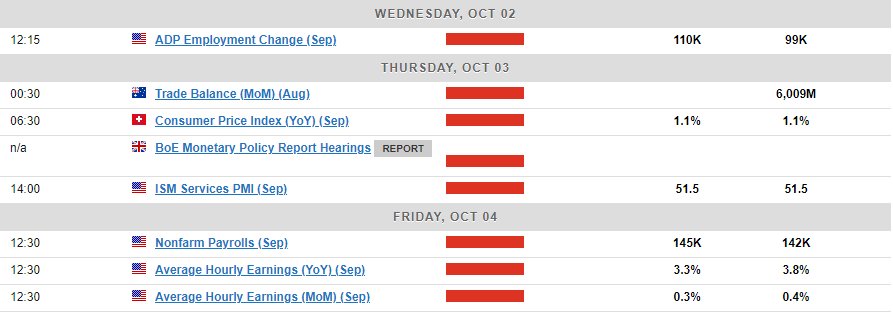

Wednesday, Oct 2 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 09:00 | EUR | Eurozone Unemployment Rate Aug | 6.40% | 6.40% |

| 12:15 | USD | ADP Employment Change Sep | 120K | 99K |

| 14:30 | USD | Crude Oil Inventories | -4.5M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 09:00 | EUR | Eurozone Unemployment Rate Aug | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 12:15 | USD | ADP Employment Change Sep | |

| Forecast: 120K | Previous: 99K | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -4.5M | ||

Thursday, Oct 3, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | 5.50B | 6.01B |

| 06:30 | CHF | CPI M/M Sep | -0.10% | 0.00% |

| 06:30 | CHF | CPI Y/Y Sep | 1.10% | 1.10% |

| 07:45 | EUR | Italy Services PMI Sep | 51.4 | |

| 07:50 | EUR | France Services PMI Sep F | 48.3 | 48.3 |

| 07:55 | EUR | Germany Services PMI Sep F | 50.6 | 50.6 |

| 08:00 | EUR | Eurozone Services PMI SepF | 50.5 | 50.5 |

| 09:00 | EUR | Eurozone PPI M/M Aug | 0.80% | |

| 09:00 | EUR | Eurozone PPI Y/Y Aug | -2.10% | |

| 08:30 | GBP | Services PMI Sep F | 52.8 | 52.8 |

| 12:30 | USD | Initial Jobless Claims (Sep 27) | 220K | 218K |

| 13:45 | USD | Services PMI Sep F | 55.4 | 55.4 |

| 14:00 | USD | ISM Services PMI Sep | 51.5 | 51.5 |

| 14:00 | USD | Factory Orders M/M Aug | 5% | |

| 14:30 | USD | Natural Gas Storage | 47B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | |

| Forecast: 5.50B | Previous: 6.01B | ||

| 06:30 | CHF | CPI M/M Sep | |

| Forecast: -0.10% | Previous: 0.00% | ||

| 06:30 | CHF | CPI Y/Y Sep | |

| Forecast: 1.10% | Previous: 1.10% | ||

| 07:45 | EUR | Italy Services PMI Sep | |

| Forecast: | Previous: 51.4 | ||

| 07:50 | EUR | France Services PMI Sep F | |

| Forecast: 48.3 | Previous: 48.3 | ||

| 07:55 | EUR | Germany Services PMI Sep F | |

| Forecast: 50.6 | Previous: 50.6 | ||

| 08:00 | EUR | Eurozone Services PMI SepF | |

| Forecast: 50.5 | Previous: 50.5 | ||

| 09:00 | EUR | Eurozone PPI M/M Aug | |

| Forecast: | Previous: 0.80% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Aug | |

| Forecast: | Previous: -2.10% | ||

| 08:30 | GBP | Services PMI Sep F | |

| Forecast: 52.8 | Previous: 52.8 | ||

| 12:30 | USD | Initial Jobless Claims (Sep 27) | |

| Forecast: 220K | Previous: 218K | ||

| 13:45 | USD | Services PMI Sep F | |

| Forecast: 55.4 | Previous: 55.4 | ||

| 14:00 | USD | ISM Services PMI Sep | |

| Forecast: 51.5 | Previous: 51.5 | ||

| 14:00 | USD | Factory Orders M/M Aug | |

| Forecast: | Previous: 5% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 47B | ||

Friday, Oct 4, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:45 | CHF | Unemployment Rate M/M Sep | 2.60% | 2.50% |

| 06:45 | EUR | France Industrial Output M/M Aug | 0.40% | -0.50% |

| 08:00 | EUR | Italy Retail Sales M/M Aug | 0.20% | 0.50% |

| 08:30 | GBP | Construction PMI Sep | 53.1 | 53.6 |

| 12:30 | USD | Nonfarm Payrolls Sep | 135K | 142K |

| 12:30 | USD | Unemployment Rate Sep | 4.20% | 4.20% |

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.30% | 0.40% |

| 14:00 | CAD | Ivey PMI Sep | 50.3 | 48.2 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:45 | CHF | Unemployment Rate M/M Sep | |

| Forecast: 2.60% | Previous: 2.50% | ||

| 06:45 | EUR | France Industrial Output M/M Aug | |

| Forecast: 0.40% | Previous: -0.50% | ||

| 08:00 | EUR | Italy Retail Sales M/M Aug | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 08:30 | GBP | Construction PMI Sep | |

| Forecast: 53.1 | Previous: 53.6 | ||

| 12:30 | USD | Nonfarm Payrolls Sep | |

| Forecast: 135K | Previous: 142K | ||

| 12:30 | USD | Unemployment Rate Sep | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 12:30 | USD | Average Hourly Earnings M/M Sep | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 14:00 | CAD | Ivey PMI Sep | |

| Forecast: 50.3 | Previous: 48.2 | ||

Markets Weekly Outlook – Will the NFP Report Validate Rate Cut Optimism?

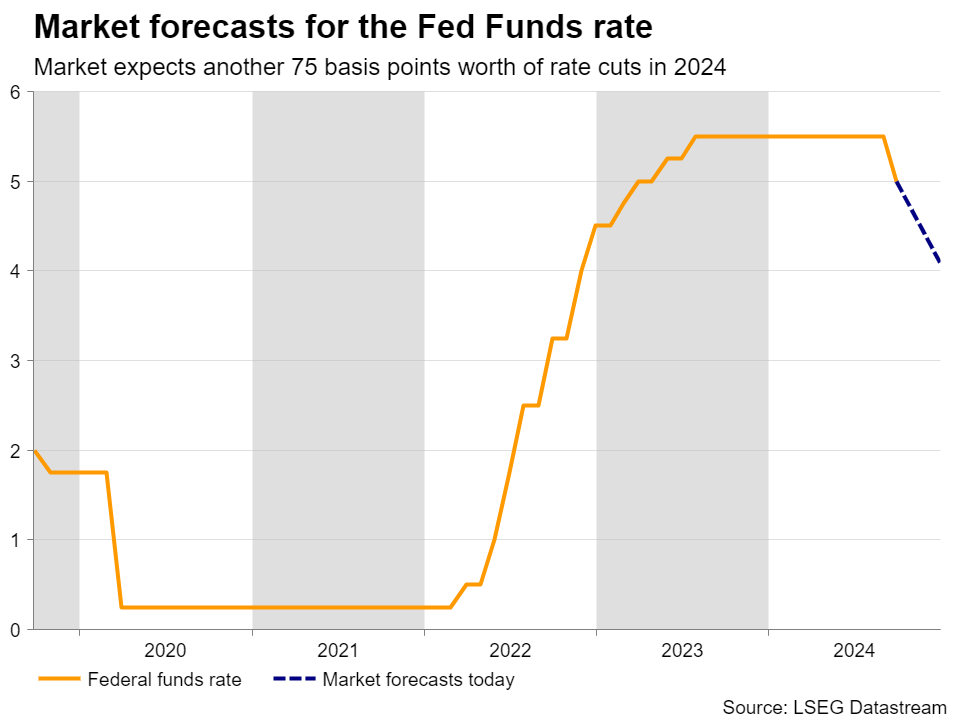

- Fed policymakers maintain a dovish stance, and market participants are pricing in a potential 50 basis point rate cut in November.

- The US dollar hit a fresh YTD low, while Gold and Silver continued to advance.

- The week ahead features key data releases, including Eurozone inflation and US nonfarm payrolls, which could shape central bank policies and market sentiment.

Week in Review: Fed Policymakers Deliver Dovish Rhetoric

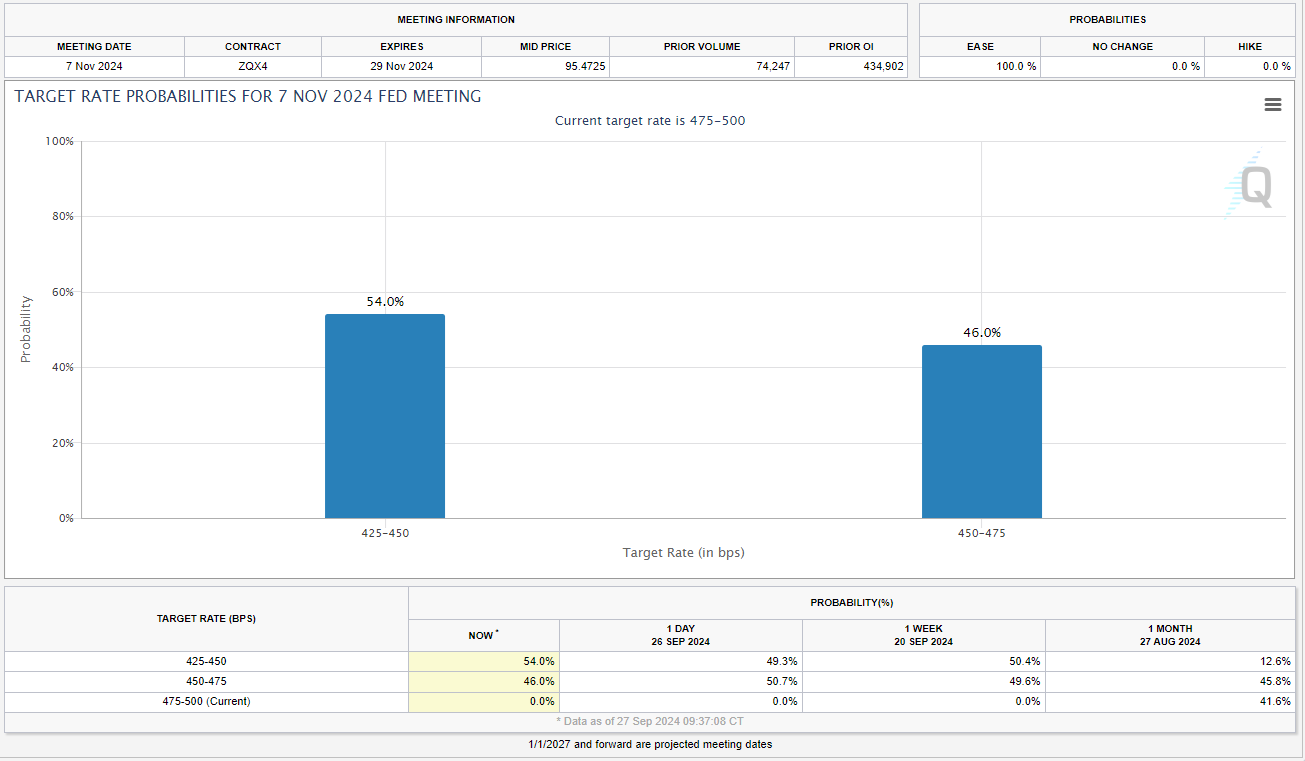

As the week wraps up, US data continues its downward trend, with the Fed’s preferred inflation measure maintaining pressure for a potential 50 basis point rate cut in November. Market participants are increasingly factoring in this cut, with the probability now exceeding 50%.

Source: CME FedWatch Tool (click to enlarge)

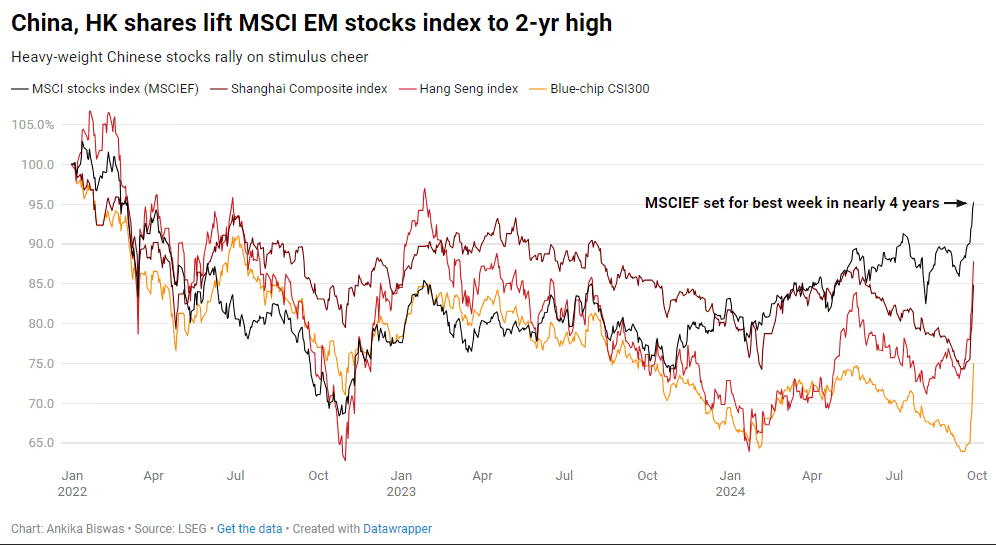

The week started with a stimulus package from China which helped propel Emerging Market (EM) stock indexes on track for their best week in 4 years. From South Africa to India emerging markets and EM currencies have done well and the Shanghai composite index logged its biggest weekly gain since 2008.

Source: LSEG Workspace (click to enlarge)

Comments from Fed Policymakers have struck a rather dovish chord of late which has emboldened market participants. The softer data from the US and uncertain geopolitical risks and tensions are also playing a key role in the current market dynamic.

No surprise that the precious metals arena continues to rise with both Gold and Silver rising this past week to fresh highs. Gold reaching a high of $2685/oz this week before a pullback has it languishing in the mid 2650’s at the time of writing.

Oil prices struggled to hold onto early week gains despite OPEC + updating its longer term outlook. The cartel says it sees peak oil demand to only be reached in 2050 as a result of emerging market demand. Brent traded at a low of around 71.00 on Thursday before a modest bounce ahead of the weekend.

On the FX front the US Dollar hit a fresh YTD low on Friday and struggled for the majority of the week. As things stand markets are now more dovish on the Fed than the ECB and BoE which have helped both currencies eke out impressive gains to the greenback.

This sets up an interesting week for Global Markets with the Euro Area inflation release and the US jobs report. Both events could be key in shaping the respective policies of each of the Central Banks with market participants fully pricing in a rate cut from the ECB in October. Will the Euro Area inflation report and US jobs report confirm such moves?

The Week Ahead: EU Inflation and US Jobs Data

The week ahead is packed with high impact data releases in both developed and emerging markets. Next week, investors will have the chance to hear from numerous Fed members, including Fed Chair Powell on Monday. However, since the dot plot already provides a clear indication of the Fed’s future plans, upcoming data, particularly Friday’s non-farm payrolls, might garner more attention.

Asia Pacific Markets

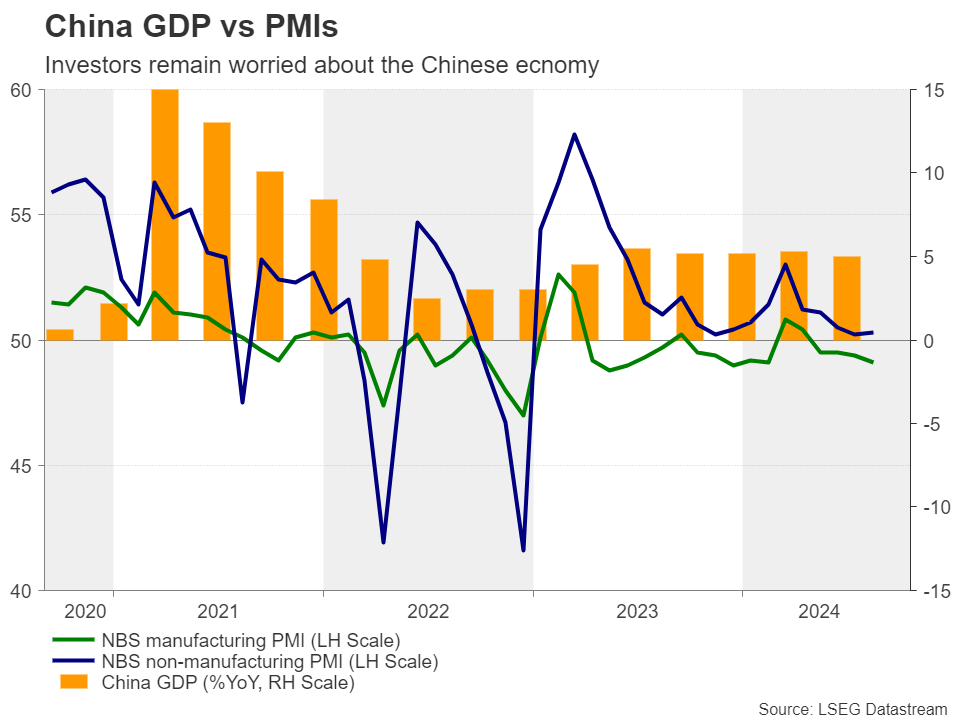

In Asia, On Monday, China will release the official PMIs for September. In August, the composite PMI was at 50.1, barely above the 50 threshold that distinguishes expansion from contraction. It remains to be seen if business activity improved this month or slipped into contractionary territory. Of course it’s way too early to see if the stimulus will have an impact on actual production numbers as that will take some time to filter through to the data but the print will be an intriguing one nonetheless and could set the early risk tone for the week.

Japan has a new Prime Minister who is seen as someone who will support policy normalization by the BoJ and support Governor Ueda in his endeavor. The week ahead brings the release of the BoJ summary of opinions from the most recent Central Bank meeting. Governor Ueda stated that the BoJ will continue to raise rates if the economy aligns with their outlook. Consequently, investors might scrutinize the summary for clues about the likelihood of another rate hike before year-end.

Japan’s employment data for August, set to be released during the Asian session on Tuesday, along with the Tankan survey on Thursday, could also influence investors’ perspectives.

Europe + UK + US

In developed markets, Eurozone inflation numbers will be in focus as markets expect to see a further slowdown in inflationary pressure. This has ramped up bets of another rate cut from the ECB at its October meeting.

Unemployment figures are due next week and have remained at historically low levels for some time. While no immediate changes are expected, the labor market outlook appears to be softening, with labor shortages becoming slightly less of an issue.

In the UK, it’s a relatively quiet week with GDP data on Monday the only highlight. As cable holds the high ground, the week ahead could see a potential pullback ahead of the NFP release.

US markets are the most intriguing with ISM services and manufacturing data coming out before the all important NFP report. When it comes to the job market, recent benchmark revisions have shaken confidence in the data, while leading surveys on hiring demand are declining. Additionally, consumer confidence readings indicate that households are beginning to feel the effects of a cooling economy. A significant downside miss could weigh heavily on the US Dollar and thus reignite recessionary fears.

Unemployment rate at or below 4.4% would be ideal. Any uptick could further complicate matters going forward for the Federal Reserve and may have a massive impact on the size of the rate cut the Central Bank deliver in November.

Chart of the Week

This week’s focus is on the S&P 500 given the recent rally and technical patterns at play.

The S&P is on course for its third consecutive week of gains and could face some form of correction next week. However the overall trend remains extremely bullish with the recent triangle pattern breakout hinting at a bullish target around the 6170 area.

The index may retest the top of the triangle pattern which rests around the 5650 handle before a potential move higher. This would be ideal for would be longs looking to get involved.

Immediate resistance on the upside rests around the 5910 handle before the psychological 6000 handle comes into focus.

S&P 500 Daily Chart – September 27, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 5669

- 5650

- 5538

Resistance:

- 5771

- 5910

- 6000

The Weekly Bottom Line: Government Shutdown Averted as Price Pressures Continue to Ease

U.S. Highlights

- The Federal Reserve’s preferred inflation metric, the core PCE index, continued to cool in August with the 3- and 6-month annualized trends converging closer to the Fed’s 2% target.

- Federal Reserve officials who spoke this week noted that the slowing labor market was a key consideration in their monetary policy decision last week and that further rate cuts were expected moving forward.

- Congress managed to pass a continuing resolution this week to fund the federal government through December 20th, removing the risk of a government shutdown until after the upcoming election.

Canadian Highlights

- Canada’s jobs market loosened again in July, with the ratio of job vacancies-to-unemployed workers falling further below its 2019 average.

- Canada’s economy grew by a better-than-expected 0.2% month-on-month in July. Still, third quarter growth will likely come in well shy of the BoC’s 2.8% projection.

- Population growth eased through Q2, although at 7.3% the temporary resident share of Canada’s population is far away from the federal target of 5% by 2027.

U.S. – Government Shutdown Averted as Price Pressures Continue to Ease

The first week of fall was largely consumed by lingering consternation regarding the Federal Reserve’s latest monetary policy decision. Federal Reserve officials who spoke this week provided further clarity on the central bank’s rationale to go big with the first rate cut in over four years, as the latest reading on inflation showed price pressures continued to cool in August. Financial markets were little changed on the week, with Treasury yields rising a few basis-points and the S&P 500 up 1.0% as of the time of writing.

Friday’s personal income & spending data release for August showed that the health of the American consumer remained favorable on aggregate through the end of the summer. Real personal consumption expenditures rose 0.1% relative to July, with goods spending roughly flat while service expenditures expanded. Consumers continued to receive support from healthy real disposable personal income gains (+3.1% year-on-year in August), although this growth has continued to moderate. This has led to some slowing in consumer spending, which has helped to push the three- and six-month annualized percentage change in core PCE inflation closer to the Fed’s 2% target after the flare-up earlier in the year (Chart 1).

With inflation pressures continuing to cool, the Federal Reserve’s downward policy path trajectory appears to continue to be supported by the incoming data. Federal Reserve officials who spoke this week broadly echoed the statements of Chair Powell last week, noting that the balance of risks has shifted towards the labor market and that ensuring a soft landing would merit looser financial conditions moving forward. Although the majority of officials who spoke this week were focused on downside risks to the economy, Governor Bowman, the lone dissenting vote from last week’s decision, noted that inflation risks remained elevated and that this would necessitate caution moving forward. Market pricing is roughly 50/50 between a quarter- and a half-point cut at the next meeting in November as of the time of writing.

Markets will likely be equally focused on fiscal policy risks moving forward with the U.S. election now less than six weeks away. Thankfully, Congress managed to avoid the risk of a government shutdown this week by passing a continuing resolution through to December 20th. However, with federal government funding and the debt limit suspension both now expiring at the end of the year, fiscal risks are likely to remain top-of-mind in the final two months of the year.

Looking ahead to next week, the biggest item on the docket will be the September employment report released on Friday, with consensus expectations for a gain of 130k jobs. This will likely cap-off the weakest quarter for job gains since the onset of the pandemic (Chart 2). Markets will also be watching Chair Powell’s speech at the National Association for Business Economics Annual Meeting on Monday, in addition to the Vice-Presidential debate in New York City on Tuesday.

Canada – Second Verse...Same as the First

It’s been clear for some time that the Canadian economy is operating with slack. The Bank of Canada certainly reinforced as much in their summer Monetary Policy Report, but perhaps the clearest signal is that Canada’s unemployment rate has jumped 1.6 percentage points from its 2023 low. This week’s economic dataflow simply reinforced this narrative. The payrolls report – which grabs fewer headlines than it’s timelier Labour Force Survey counterpart but shares a stronger correlation with GDP for many industries – showed that payrolls expanded by 0.2% month-on-month in July. Although this counts as an above-trend gain, it was paired with another sizeable decline in job vacancies, suggesting that the demand for future workers continues to shrink. Meanwhile, the job vacancy to unemployment ratio (a closely watched indicator of job market tightness) dropped yet again, pointing to further loosening (Chart 1).

The softening up in the labor market squares with what we’re seeing in the monthly GDP data. Canada’s economy managed to post a better-than-expected 0.2% monthly advance in July, but August’s preliminary estimate is calling for no growth. For the third quarter overall, industry-based GDP performances so far are flagging significant downside risk to the Bank of Canada’s hefty Q3 2.8% growth projection. This implies an even larger build-up of slack than policymakers had anticipated and provides some justification for a market that’s almost fully built in a 50 basis-point point move from the Bank of Canada at the October meeting. Also helpful from this perspective is the fact that crude oil prices continue to fall, weighed down this week by Saudi Arabia’s announcement that regardless of market conditions, they will begin increasing output on December 1st – doing away with their $100 per barrel unofficial price target.

Lastly, Canada’s headline GDP growth has been flattered by robust population gains but, on a per capita basis, the economy is shrinking. This week’s population report confirmed this soft trend extended through the second quarter. Indeed, Canada’s population surged 3% year-on-year in Q2, against just a 0.9% increase in real GDP (Chart 2). Now, for a federal government trying to wrap their arms around Canada’s ballooning population, the report had some things to like. Namely, growth edged down from the prior quarter on the back of a smaller increase in temporary residents. In an encouraging sign for the government, non-permanent inflows have cooled for three straight quarters, although they remain elevated. Less encouraging was that the share of Canada’s population accounted for by temporary residents rose to 7.3% and could push even higher in the next quarter or two. This is a far cry from the government’s stated goal of getting this share down to 5% by 2027.

All told, Canadian events this week echoed many of the same trends that have been evident for the economy for some time and provided little scope to change our outlook on rates. Second verse, same as the first.

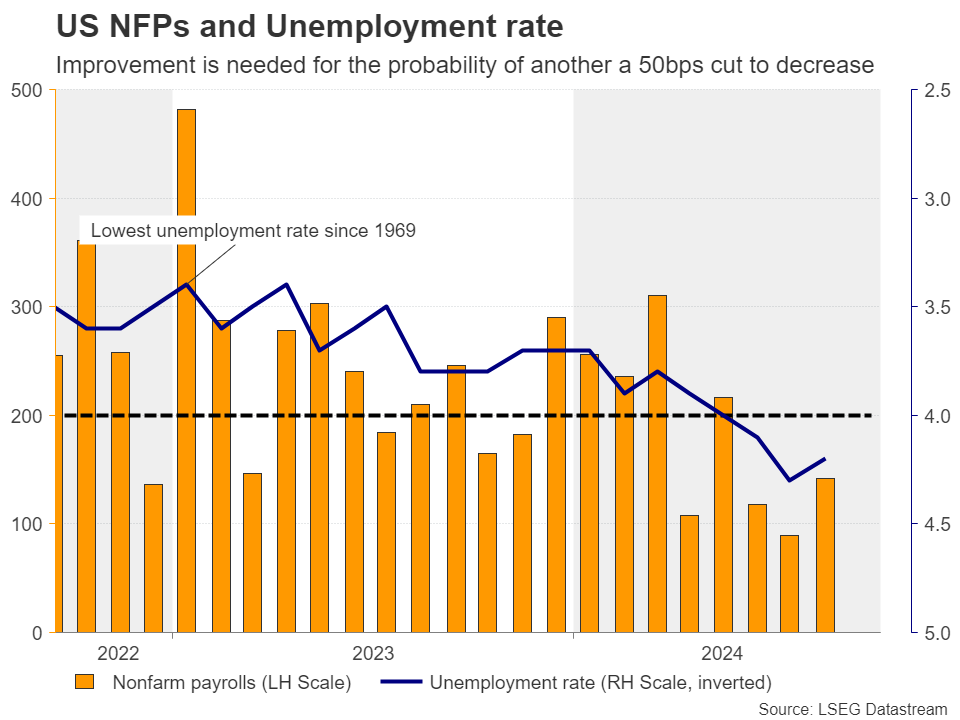

U.S. Unemployment Rate Likely Inched Higher in September

All eyes will be on U.S. jobs data on Friday for signs of weakness after the U.S. Federal Reserve kicked off its easing cycle with an outsized 50 basis point cut in September.

The Fed took pains to frame the cut (larger than earlier 25 basis point cuts from most other advanced economy central banks) as the beginning of a “recalibration” process rather than driven by urgent concerns about the economy. But, U.S. labour markets have shown signs of softening, even if at a very gradual pace, and Fed Chair Jerome Powell has reinforced that further weakening is a concern for the central bank.

The unemployment rate ticked down to 4.2% in August, but that only partially reversed an increase to 4.3% in July that triggered the so-called “Sahm Rule” recession indicator—when the three-month moving average of the unemployment rate rises by 0.5% or more relative to its low during the previous 12 months. In short, even the gradual increases in the U.S. unemployment rate to date have not happened historically outside of recessions. Job counts have continued to rise with much of the increase in unemployment coming from longer job searches for new entrants into the labour force, particularly younger workers, rather than layoffs, and initial jobless claims have remained low.

But the average 116,000 increase in payroll employment over the last three months was the softest since early 2021, and early estimates from the Bureau of Labor Statistics already have flagged that payroll employment earlier this year is overcounted by about 818,000 jobs. Hiring demand has continued to slow with job openings back down to pre-pandemic levels. Layoffs are still low, but they have been creeping gradually higher. Like the Sahm Rule for the unemployment rate, this is also unusual outside of recessions. Survey data suggests consumers are less confident in the job market than they were, and wage growth has been slowing.

Our base case assumption remains that labour markets are normalizing rather than faltering. We look for payroll employment to rise 147k in September and for the unemployment rate to tick back up to 4.3%—still historically low but up 0.5 percentage points from a year ago. Interest rates impact the economy with significant lags, and the Fed’s start to interest rate cuts will help limit headwinds from monetary policy in the year ahead. An exceptionally large government budget deficit also helps demand in the U.S. economy. Still, labour markets will be analyzed for further red flags with risks tilted to the downside for it, and the Fed’s policy rates.

Week ahead data watch

Weekly Economic & Financial Commentary: Consumer in the Spotlight

Summary

United States: Consumer in the Spotlight

- The personal income and spending data this week show that inflation remains in check, shed light on the staying power of the consumer and paint a more constructive backdrop for household finances moving forward. Real estate should be a beneficiary of lower interest rates as the Fed eases policy, yet housing activity remains slow.

- Next week: ISM Manufacturing (Tue.), ISM Services (Thu.), Employment (Fri.)

International: Eurozone Economy at Risk of Renewed Stumble

- The Eurozone September manufacturing and services PMIs were disappointing, with output and orders both softening, although they also indicated an overall softening in price pressures. We expect Eurozone expansion to continue, but now expect a slower pace of recovery than previously. Elsewhere, it was a busy week for international central banks. China, Sweden, Switzerland, Hungary, the Czech Republic and Mexico all lowered interest rates, while Australia held monetary policy steady.

- Next week: China PMIs (Mon.), Japan Tankan Survey (Tue.), Eurozone CPI (Tue.)

Credit Market Insights: Is the Tide Turning for Commercial Real Estate?

- When the Fed cut the policy rate by 50 bps last week, it marked what should be the beginning of the end of the worst CRE downturn since the global financial crisis. Although there are no shortage of obstacles ahead for CRE, the gap between the amount of maturing debt in need of refinancing and the available capital should be reduced with lower rates, thus limiting the extent to which stress mounts further.

Topic of the Week: Reasons Not to Panic About Looming Port Strikes

- Thousands of dockworkers are set to strike at East and Gulf coast U.S. ports this upcoming week if the International Longshoremen's Association (ILA) and the United States Maritime Alliance (USMX) cannot come to an agreement regarding wage negotiations. While work stoppages at these ports cannot be ruled out, and a prolonged worker stoppage could disrupt supply chains, our sense is that worries about major supply disruption are overstated.

Week Ahead – NFP on Tap Amid Bets of Another Bold Fed Rate Cut

- Investors see decent chance of another 50bps cut in November

- Fed speakers, ISM PMIs and NFP to shape rate cut bets

- Eurozone CPI data awaited amid bets for more ECB cuts

- China PMIs and BoJ Summary of Opinions also on tap

Will the Fed opt for a back-to-back 50bps rate cut?

Although the dollar slipped after the Fed decided to cut interest rates by 50bps and to signal that another 50bps worth of reductions are on the cards for the remainder of the year, the currency traded in a consolidative manner this week even with market participants penciling around 75bps worth of cuts for November and December. A back-to-back double cut at the November gathering is currently holding a 50% chance according to Fed funds futures.

Ergo, with policymakers Christopher Waller and Neel Kashkari clearly favoring slower reductions going forward, the current market pricing suggests that there may be upside risks in case more officials share a similar view, or if incoming data corroborates so.

Next week, investors will have the opportunity to hear from a plethora of Fed members, including Fed Chair Powell on Monday, but given that the dot plot is already a relatively clear guide of how the Fed is planning to move forward, incoming data may attract more attention, especially Friday’s nonfarm payrolls.

ISM PMIs and NFP report to attract special attention

But ahead of the payrolls, the ISM manufacturing and non-manufacturing PMIs for September, on Tuesday and Thursday respectively, may be well scrutinized for early signs of how the world’s largest economy finished the third quarter. If the numbers agree with Powell’s view after last week’s decision that the economy is in good shape, then the dollar could gain as investors reconsider whether another bold move is necessary.

However, for the dollar to hold onto its gains, Friday’s jobs report may need to reveal improvement as well. Currently, the forecasts are suggesting that the world’s largest economy added 145k jobs in September, slightly more than August’s 142k, with the unemployment rate holding steady at 4.2%. Average hourly earnings are seen slowing somewhat, to 0.3% m/m from 0.4%.

Overall, the forecasts are not pointing to a game-changing report, but any upside surprise coming on top of decent ISM prints and less-dovish-than-expected commentary by Fed policymakers could very well act as the icing on the cake of a bright week for the US dollar. Wall Street could also cheer potentially strong data, even if it translates into slower rate cuts ahead, as more evidence that the US economy is not heading into recession is nothing but good news.

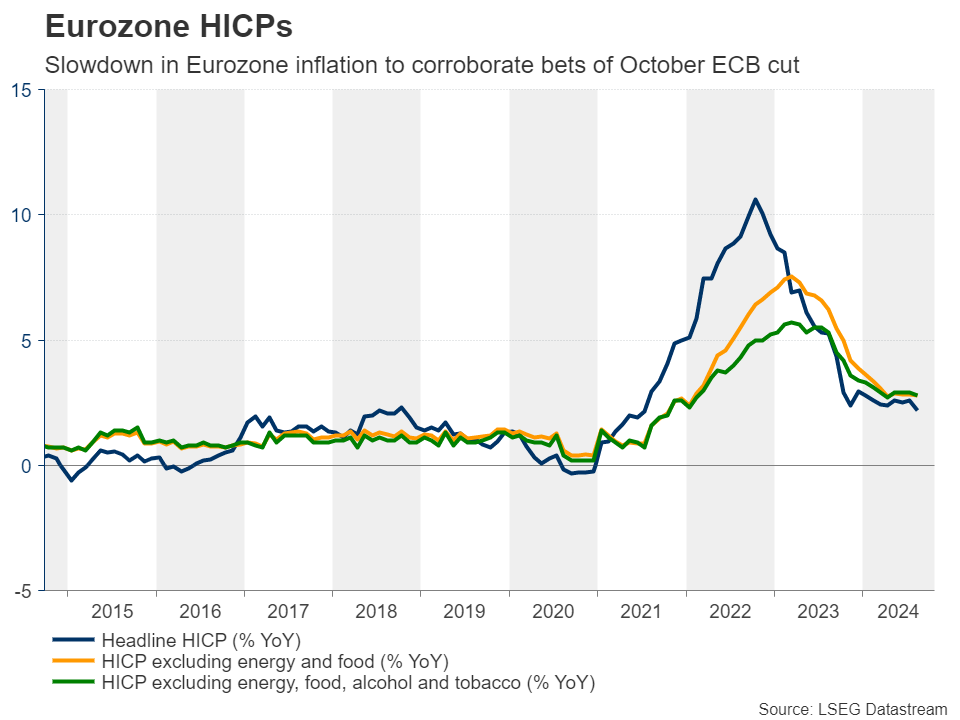

Eurozone inflation in focus amid split ECB

In the Eurozone, the spotlight is likely to fall on the preliminary CPI data for September, due out on Tuesday. Even though Lagarde and her colleagues did not offer explicit signals regarding an October reduction, the disappointing PMIs encouraged market participants to increase bets of such an action. Specifically, the probability of a 25bps reduction at the October 17 meeting is currently at around 75%.

Having said that though, a Reuters report citing several sources noted yesterday that the October decision is seen as wide open. The report mentioned that the doves will fight for a rate cut following the weak PMIs, but they will likely face resistance from the hawks, who will argue for a pause. Some sources are talking about a compromise solution in which rates are kept on hold but reduced in December if data doesn’t improve.

Yet, the market’s base case scenario is rate cuts in both October and December, and a set of CPI numbers pointing to further slowdown in Euro area inflation could solidify that view.

Euro/dollar could slip in such a case and extend its decline if the US data corroborates the notion that there is no need for the Fed to continue with aggressive rate reductions. That said, for a bearish reversal to start being considered, a decisive dip below the round figure of 1.1000 may be needed, as such a break may confirm the completion of a double top formation on the daily chart.

Will the Chinese PMIs signal contraction?

From China, we get the official PMIs for September on Monday. The composite PMI stood at 50.1 in August, just a tick above the 50 boom-or-bust zone that separates expansion from contraction, and it remains to be seen whether business activity improved this month, or whether it slipped into contractionary territory.

This week, the People’s Bank of China (PBoC) announced a series of stimulus measures to support economic activity and help the deeply wounded property sector. Yet, market participants were not particularly excited, with oil prices plunging due to easing concerns about supply disruptions in Libya and following reports that Saudi Arabia is ready to abandon its target of $100 per barrel.

The announcements of the Chinese measures did little to lift hopes that demand in the world’s top crude importer may be restored, as investors may still be holding the view that more fiscal help is needed.

With that in mind, a set of disappointing PMIs could encourage some further selling in oil prices, though any pullbacks in the aussie and the kiwi are likely to prove limited as these risk-linked currencies now seem to be enjoying the increase in broader risk appetite, which is evident by the latest rally on Wall Street.

BoJ’s Summary of Opinions also on the agenda

In Japan, the BoJ releases the Summary of Opinions from the latest decision, where policymakers kept interest rates unchanged but revised up their assessment on consumption due to rising wages. Governor Ueda said that they will keep raising rates if the economy moves in line with their outlook and thus, investors may dig into the summary for clues and hints on how likely another rate hike is before the end of the year.

Japan’s employment data for August, due out during the Asian session Tuesday, and the Tankan survey on Thursday, may also help in shaping investors’ opinion.

Weekly Focus – China Makes a Big Push to Turn the Economy

The big news this week was the barrage of new stimulus measures from China. At an economic briefing on Tuesday, People's Bank of China and financial regulators announced a wide range of measures to shore up the ailing economy: the policy rate was cut by 30bp, Reserve Requirement Ratios for banks were cut by 50bp, measures to increase buying in the stock market was launched and mortgage rates on existing loans will be cut by 50bp. On top of this reports suggested China's big banks will be recapitalized with 1 trillion CNY (142 billion USD). On Thursday, China top leaders dedicated their monthly meeting in the Politburo to the economy, which is not normally the case in September. They sent a clear signal that stimulus will be stepped up across the board and turning the economy has the number one priority now. It is the biggest round of stimulus since the current crisis started three years ago and could turn out to be China's 'whatever-it-takes' moment. We now see upside risk to our growth estimate of 4.8% this year and next.

The Chinese stock market rallied strongly all week and is up 15% from the start of the week (offshore stocks); albeit coming from very low levels. The CNY also strengthened significantly. It is probably not a coincidence the measures were launched a week before China goes into the one-week National Holiday starting on Tuesday as policy makers hope for the measures to lift confidence when millions of families get together across China.

It has also been an eventful week on the data front. Flash PMIs from the euro zone and US kicked off the week with disappointing readings. Euro manufacturing PMI slipped further to 44.8 from 45.8 signalling clear contraction and raising the chance that the ECB could cut rates again next month. Service PMI also dropped, although it was probably more related to the end of the Olympics. US manufacturing PMIs also disappointed but the service PMI stayed at robust levels alleviating recession fears. Focus is also still on US labour market data as they are key for Fed policy. This week provided a mixed bag with the 'jobs plentiful' index in the consumer confidence survey falling yet again signalling a further rise in unemployment. However, initial jobless claims was better than expected.

On the geopolitical front we saw escalation in the Middle East with extensive Israeli attacks in Lebanon (see Geopolitical Radar - Up the escalation ladder in the Middle East, 26 September). It is still not having much impact on markets, though, and oil prices actually dropped this week from USD75 per barrel to USD71.5 per barrel as Saudi Arabia plans to increase supply and a new agreement in Libya is also set to put more oil on the market.

Risk sentiment was generally improving this week with global stocks moving higher while bond yields and the USD moved broadly sideways. Metal prices saw a strong rally following the Chinese stimulus announcements.

Focus the coming week will be on the US labour market report where both payrolls and the unemployment rate will be key for guiding Fed policy. ISM for both manufacturing and services are also due. In the eurozone, the Flash CPI for September will be a key input going into the October meeting. We expect euro area HICP inflation to decline to 1.7% y/y (consensus 2.0% y/y) in September from 2.2% in August after lower-than-expected data this week from France and Spain.