Sample Category Title

US PPI up 0.2% mom, 1.7% yoy in Aug

US PPI rose 0.2% mom in August, matched expectations. PPI services rose 0.4% mom while PPI goods was unchanged. PPI less foods, energy, and trade services rose 0.3% mom.

For the 12 month period, PPI advanced 1.7% yoy, slowed from 2.1% yoy. PPI less foods, energy and trade services moved up 3.3% yoy.

US initial jobless claims rises slightly to 230k

US initial jobless claims rose 2k to 230k in the week ending September 7, slightly below expectation of 231k. Four-week moving average of initial claims rose 500 to 231k.

Continuing claims rose 5k to 1850k in the week ending August 31. Four-week moving average of continuing claims fell -2k to 1853k.

ECB cuts deposit rate by 25bps to 3.75%

ECB followed expectations by lowering the deposit rate by 25 bps to 3.75%. The main refinancing rate was adjusted to 3.65%, as the spread between the two rates is now set at 15 bps. Moving forward, the ECB emphasized its commitment to a "data-dependent" and "meeting-by-meeting" approach, avoiding any pre-commitment to a specific rate path.

In its accompanying statement, ECB highlighted that recent inflation data had been largely in line with projections. Inflation is expected to rise again towards the end of the year, primarily due to the base effect from last year’s sharp energy price falls. The central bank anticipates inflation will decline closer to its target in the second half of 2025.

Updated inflation forecasts show headline inflation averaging 2.5% in 2024, 2.2% in 2025, and hitting 1.9% by 2026. Core inflation is projected to fall from 2.9% in 2024 to 2.3% in 2025, and eventually reach 2.0% in 2026.

On the growth front, there was a slight downward adjustment in the outlook. The Eurozone economy is now expected to expand by 0.8% in 2024, with growth improving to 1.3% in 2025 and 1.5% in 2026.

(ECB) Monetary policy decisions

The Governing Council today decided to lower the deposit facility rate – the rate through which it steers the monetary policy stance – by 25 basis points. Based on the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission, it is now appropriate to take another step in moderating the degree of monetary policy restriction.

Recent inflation data have come in broadly as expected, and the latest ECB staff projections confirm the previous inflation outlook. Staff see headline inflation averaging 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026, as in the June projections. Inflation is expected to rise again in the latter part of this year, partly because previous sharp falls in energy prices will drop out of the annual rates. Inflation should then decline towards our target over the second half of next year. For core inflation, the projections for 2024 and 2025 have been revised up slightly, as services inflation has been higher than expected. At the same time, staff continue to expect a rapid decline in core inflation, from 2.9% this year to 2.3% in 2025 and 2.0% in 2026.

Domestic inflation remains high as wages are still rising at an elevated pace. However, labour cost pressures are moderating, and profits are partially buffering the impact of higher wages on inflation. Financing conditions remain restrictive, and economic activity is still subdued, reflecting weak private consumption and investment. Staff project that the economy will grow by 0.8% in 2024, rising to 1.3% in 2025 and 1.5% in 2026. This is a slight downward revision compared with the June projections, mainly owing to a weaker contribution from domestic demand over the next few quarters.

The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

As announced on 13 March 2024, some changes to the operational framework for implementing monetary policy will take effect from 18 September. In particular, the spread between the interest rate on the main refinancing operations and the deposit facility rate will be set at 15 basis points. The spread between the rate on the marginal lending facility and the rate on the main refinancing operations will remain unchanged at 25 basis points.

Key ECB interest rates

The Governing Council decided to lower the deposit facility rate by 25 basis points. The deposit facility rate is the rate through which the Governing Council steers the monetary policy stance. In addition, as announced on 13 March 2024 following the operational framework review, the spread between the interest rate on the main refinancing operations and the deposit facility rate will be set at 15 basis points. The spread between the rate on the marginal lending facility and the rate on the main refinancing operations will remain unchanged at 25 basis points. Accordingly, the deposit facility rate will be decreased to 3.50%. The interest rates on the main refinancing operations and the marginal lending facility will be decreased to 3.65% and 3.90% respectively. The changes will take effect from 18 September 2024.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

The Eurosystem no longer reinvests all of the principal payments from maturing securities purchased under the PEPP, reducing the PEPP portfolio by €7.5 billion per month on average. The Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

EUR With Potential Weakness Ahead of ECB Decision: EURUSD and EURJPY

Fundamental Analysis

Today, September 12, 2024, the European Central Bank (ECB) is expected to cut interest rates by 60 basis points, marking a significant adjustment in its monetary policy. The main refinancing rate could drop to 3.65% in response to slowing inflation, which reached 2.2% in August. This move reflects growing concerns about the eurozone's weakening economic growth. Christine Lagarde's speech and updated economic forecasts will be crucial to understanding the future direction of monetary policy and its impact on the EURUSD pair, which may experience volatility.

Despite easing inflation and slower wage growth, strength in some service sectors raises uncertainty about the extent of future rate cuts. While the 60 basis point reduction is almost certain, the long-term outlook will depend on the evolution of key economic indicators and how the ECB manages the balance between growth and price stability.

Technical Analysis

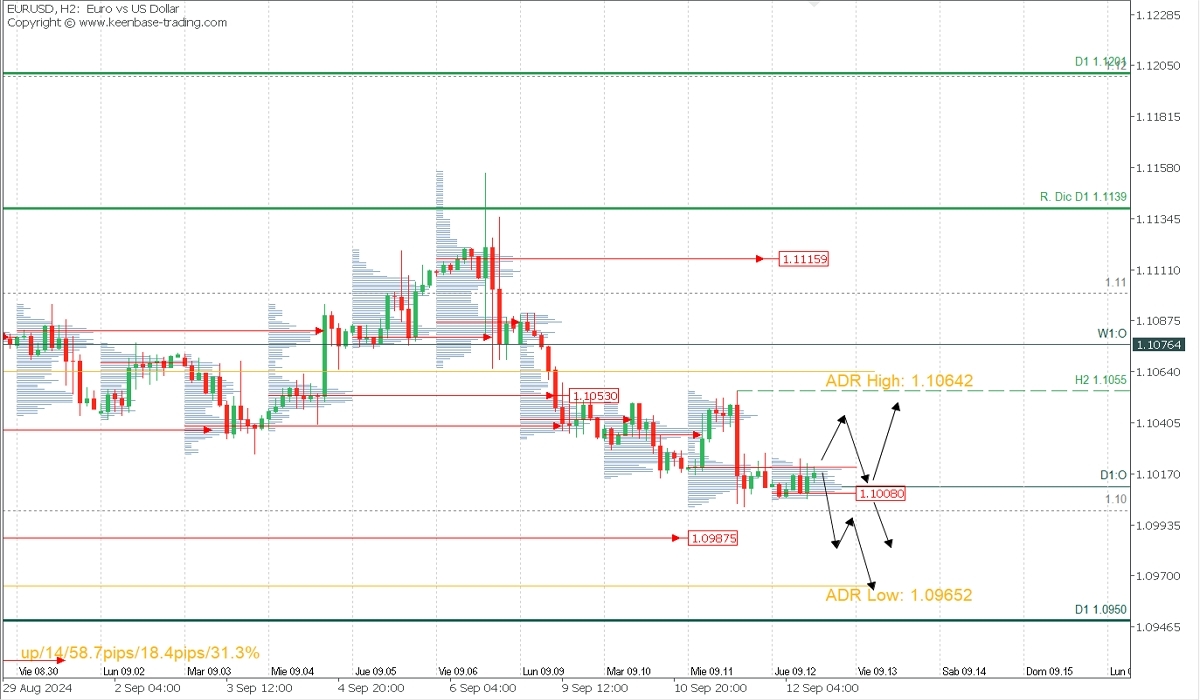

EURUSD

Supply Zones (Sellers): 1.1020 and 1.1044

Demand Zones (Buyers): 1.1008 and 1.0987

Consolidation below yesterday’s supply zone around 1.1020 suggests weak buying interest. As long as the pullback stays below this area, renewed selling is expected towards the uncovered POC* at 1.0987, with a potential extension to the bearish range at 1.0965. A rebound above 1.1020 may seek liquidity at the high-volume node around 1.1044 before resuming the decline toward 1.0987. The bearish scenario holds as long as the pullback does not decisively break above the last intraday resistance at 1.1055.

If the ECB cuts rates less than expected, there will be an upward reaction in the euro, potentially breaking key intraday resistance. Consider entering sell positions only after a confirmed exhaustion/reversal pattern (ERP) below 1.1020. If no pattern forms, wait for a rebound toward the next selling zone at 1.1044 and confirm the sell entry with an M5 technical setup. Avoid early, unconfirmed entries.

Technical Summary

Bearish continuation scenario: Sell below 1.1020 with TP at 1.0987, 1.0965, and 1.0950. This scenario is invalidated if the price breaks above 1.1055.

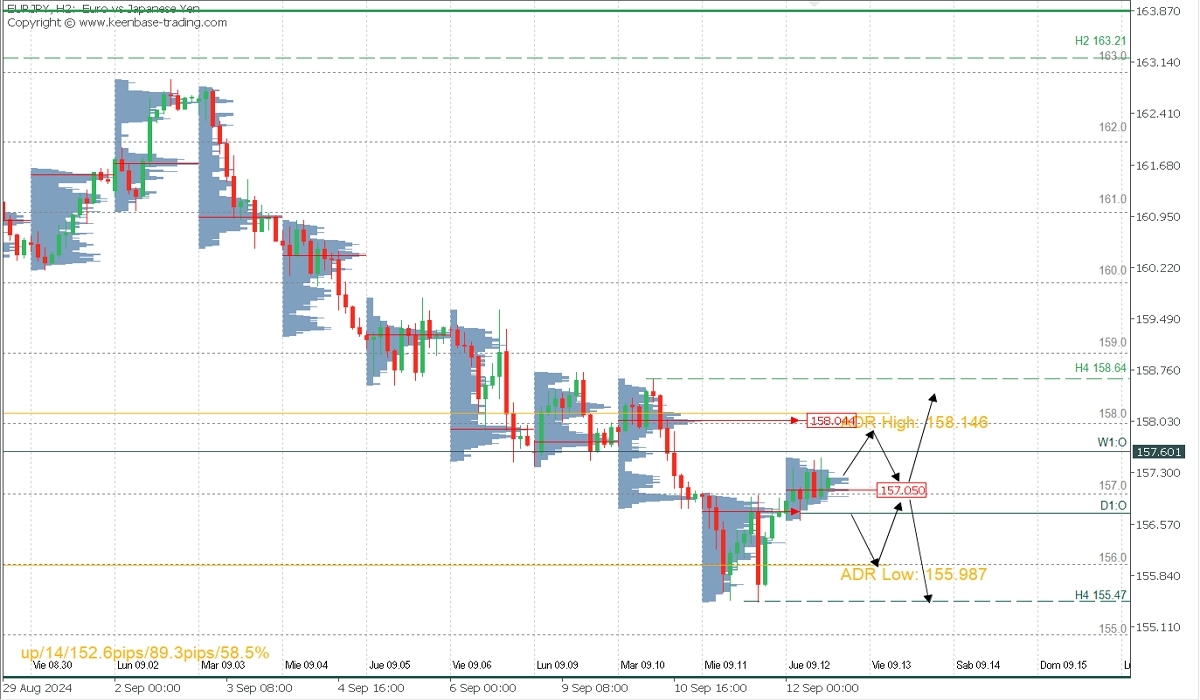

EURJPY

Supply Zones (Sellers): 158.00

Demand Zones (Buyers): 156.73 and 157.05

The yen’s broad correction against its counterparts has also supported the euro in recent hours. As long as prices remain above the demand zone between 156.73 and 157.00, a rebound toward the closest supply zone at 158.00 is expected. A break of 158.00 threatens the last validated intraday bearish resistance at 158.64. A decisive break or confirmation with two upward moves will reverse the current bearish trend. However, a strong reaction at the supply zone and a drop below 156.70 suggest weakness in bulls, potentially extending the decline to the daily range at 156.00.

If the ECB cuts rates less than expected, buying will be triggered toward 158.00 or higher. However, if expectations are met or exceeded, the fall could target the bearish range and potentially break the current support at 155.47.

Technical Summary

Corrective bullish scenario (with a smaller-than-expected cut): Buy above 157.00 with TP at 158.00, and only consider 158.64 if a decisive break occurs.

Bearish scenario: Sell below 157.00 with TP at 156.00 or 155.47 on extension.

POC Explained

POC (Point of Control): The level or zone where the highest concentration of volume occurred. If a bearish move followed, it is considered a selling zone and forms resistance. Conversely, if a bullish move followed, it is a buying zone, typically located at lows and forms support.

Euro Flat Ahead of ECB Decision

The euro continues to show limited movement and is almost unchanged on Thursday. EUR/USD is trading at 1.1010 in the North American session at the time of writing.

ECB expected to deliver 25 bps cut

The European Central Bank meets later today and the markets are expecting a rate cut of 25 basis points, which bring down the key rate to 3.5%. This would mark the second rate cut after an initial 25-bps reduction in June. A jumbo 50-bps cut is also a possibility but I expect the ECB to play it safe and deliver a modest cut of 25-bps.

Inflation has fallen to 2.2% its lowest level since July 2021 and is close to the ECB’s target of 2%, although core CPI is higher at 2.8%. Wage growth has eased and eurozone GDP for Q2 was revised downwards to 0.2%, which means that conditions are favorable for another rate cut at today’s meeting.

If inflation remains low, the ECB could try to squeeze one final rate cut before year’s end and continue trimming in early 2025. ECB President Lagarde has ditched forward guidance, saying that rate decisions will be data-dependent. Still, the ECB has widely telegraphed that it will lower rates today and it’s no secret that the central bank is looking to continue cutting if the data is favorable.

The ECB will also release updated economic forecasts today and investors will be looking for hints about future rate policy. If Lagarde sends a dovish message about future rate cuts, it would likely hurt the euro, which has gained 1.1% against the US dollar since late August.

EUR/USD Technical

- EUR/USD is testing resistance at 1.1023. Above, there is resistance at 1.1044

- There is support at 1.0991 and 1.0970

NZD/USD Looking for a Reason to Recover: External Background May Help

NZD/USD is attempting to recover from yesterday’s decline on Thursday and is heading towards 0.6148. The pair came under downward pressure on 29 August, and since then its attempts to stabilise have not brought any tangible result. The ambiguous US inflation release has increased bets that the Federal Reserve will ease monetary policy very cautiously next week. This means a 25-basis-point interest rate cut.

The Reserve Bank of New Zealand has already started its easing cycle, with a launch in August. At that time, the RBNZ cut interest rates by 25 basis points, marking the first reduction in four years. The RBNZ is expected to lower borrowing costs at each of the two meetings scheduled for this year, with a 50-basis-point rate cut possible at one of these meetings.

The consensus forecast suggests that the cash rate will be 3.00% by the end of 2025, down from 5.25% now. As for the latest statistics, annual food inflation in New Zealand eased to 0.4% in August from the previous 0.6%. This is a good signal, enabling the RBNZ to maintain its global easing stance.

Technical analysis of NZD/USD

The NZD/USD H4 chart shows that the market has completed a downward wave, reaching 0.6106. A corrective structure is forming today, aiming for 0.6150 (testing from below). The correction could extend to 0.6166. Subsequently, the price might decline to 0.6070, potentially continuing the trend towards the local target of 0.6050. This scenario is technically supported by the MACD indicator, whose signal line is below zero and pointing strictly downwards.

The NZD/USD H1 chart shows that the market has formed a consolidation range around 0.6140 and extended it down to 0.6106. Today, the market is correcting the downward wave, with the target for a correction of at least 0.6157. Once the correction is complete, the downward wave could develop towards 0.6069. This scenario is also technically supported by the Stochastic oscillator, whose signal line is below 50 and pointing strictly towards 80. Subsequently, a decline to 20 is expected.

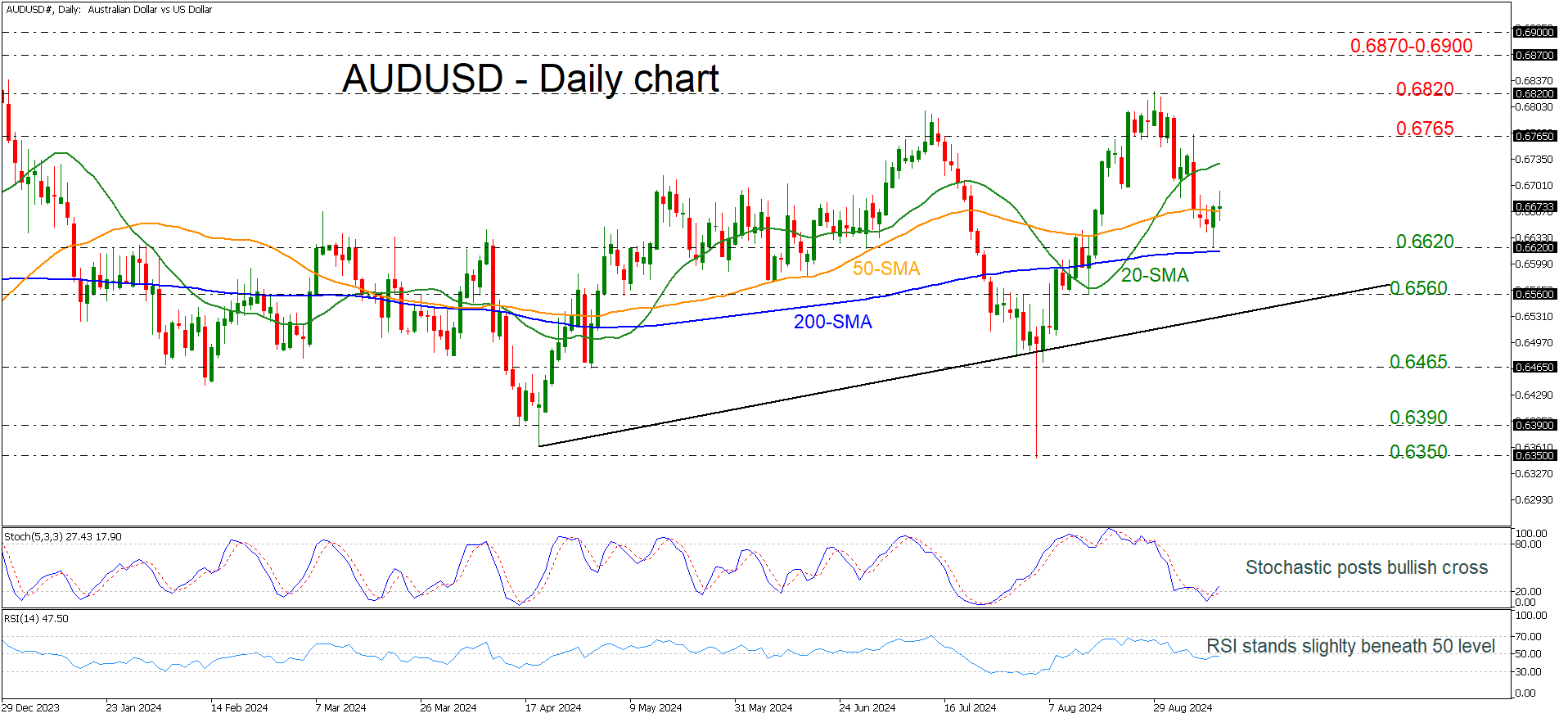

AUDUSD Remains Above 200-day SMA

- AUDUSD battles with 50-day SMA

- Stochastics point north but RSI flattens

AUDUSD had a bullish start on Thursday, with the price flirting with the 50-day simple moving average (SMA) at 0.6670.

Momentum signals are neutral-to-bullish, with the RSI appearing to be heading south, while the stochastic oscillator has reversed higher after the bullish crossover within its %K and %D lines in the oversold area.

Should the price continue to decline, the 0.6620 support could be a significant barrier to keep in mind because it overlaps with the 200-day SMA. Below that, the focus could shift straight to 0.6560, which is close to the short-term uptrend line.

On the other hand, a recovery could retest the 20-day SMA at 0.6730 before turning attention to the 0.6765 resistance. Moving higher, the 0.6820 bar should be another tough obstacle for traders as the price paused its uptrend at the end of August.

Looking at the short-term picture, the bullish outlook reemerged following the unsuccessful attempt to break below the 200-day SMA. For a bull market, traders need to wait for a clear close above 0.6820.

Overall, AUDUSD is currently holding a positive profile both in the medium- and long-term timeframes.

EUR/USD Outlook: EUR/USD Awaits ECB’s Verdict

EURUSD stays in a quiet mode early Thursday as traders reduced speed ahead of key event of the day – ECB policy decision.

The central bank is widely expected to cut rates by 25 basis points to 3.5%, after June’s 0.25% rate cut.

With today’s cut being almost certain, markets turn focus towards ECB’s next steps, looking for the dynamics of ECB’s action in the near future.

While some expect the central bank to deliver another 25 basis points cut in October, arguing that inflation continues to ease and is near 2% target and economic growth is anemic, with no significant changes in economic picture expected, others point to persisting inflation risk which requires cautious approach.

This fits within ECB’s mantra that any future decision will be based on incoming data and taken meeting by meeting.

Near-term price action is in a sideways mode for the second day and holding just above pivotal 1.10 support zone (psychological / Fibo 38.2% of 1.0666/1.1201).

Technical picture is weakening as the price broke below MA’s (10/20-d) and bearish momentum is strengthening, with long upper shadow on Wednesday’s candlestick pointing to strong supply.

Dovish comments from ECB policymakers would raise pressure on euro, with firm break of 1.10 to open way for deeper pullback towards 1.0947/33 (55DMA / 50% retracement), guarding the top of rising daily cloud (1.0893).

Conversely, the single currency may receive fresh boost from more hawkish ECB’s stance, with lift above daily Tenkan-sen (1.1078) to sideline immediate downside risk.

Res: 1.1051; 1.1078; 1.1091; 1.1119.

Sup: 1.1000; 1.0947; 1.0933; 1.0893.

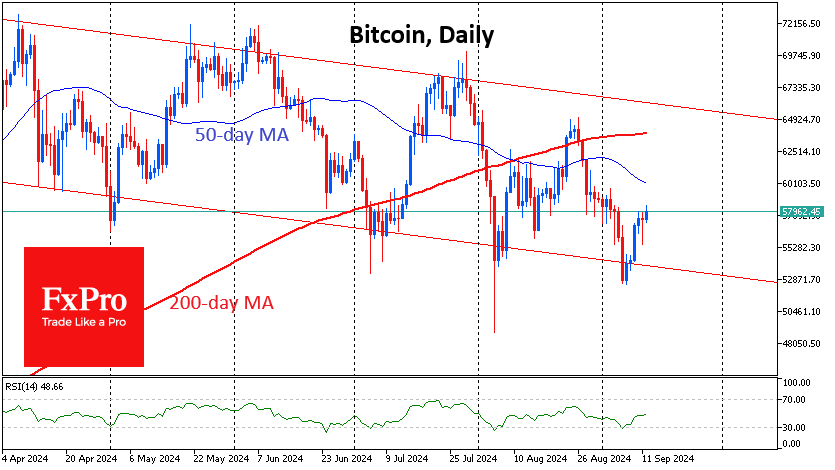

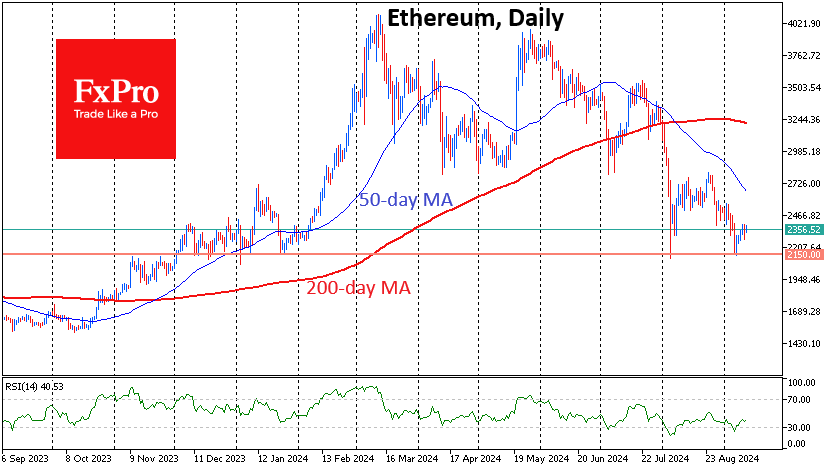

Crypto Market Surpasses Milestone

Market picture

US financial markets closed higher on Wednesday despite a rough start to the day. A strong performance from the technology sector helped the crypto market cross the $2 trillion mark, up 3% in 24 hours. The positive sentiment in the market continued into Thursday morning, setting the market up for further gains, potentially through to Wednesday evening next week, when the Federal Reserve announces its interest rate decision.

Bitcoin gained 2.5% in 24 hours, underperforming the broader market, but the price briefly broke above $58K on Thursday morning, something it had failed to do in previous days. A rebound from the lower boundary of the descending corridor could see Bitcoin top out at around $65.5K by the end of the month, with interim stops at $60K and $64K, the 50 and 200-day moving averages, respectively.

Ethereum is trading near $2350 but remains heavy, struggling to add 1% for the day and has yet to break above highs on Wednesday, which closed with a decline. The second most widely traded cryptocurrency has found support below $2150 but has yet to see a confident rebound.

News background

Another recalculation saw the first cryptocurrency’s mining difficulty rise by 3.58% to an all-time high of 92.67 T. The average hash rate for the period since the previous change was 662.34 EH/s, indicating bitcoin miners’ confidence in the prospects of digital gold. At the same time, fresh price corrections could intensify selling due to a global decline in risk appetite, Glassnode noted.

Bitwise expects the crypto market to shift to growth in October-November after the end of US macroeconomic and political uncertainty. September is historically the worst month for Bitcoin.

Bitcoin will continue to grow regardless of the outcome of the US presidential election in November, Matrixport believes, citing BTC’s growth under both the Trump and Biden administrations. The next US president will have a greater impact on the country’s regulation of the crypto market.

BTC is moving from weak hands to strong hands, CryptoQuant noted. The number of bitcoins held by short-term holders is declining, while long-term holders are accumulating the asset.

The PayPal and Venmo teams have integrated the Ethereum Name Service (ENS). PayPal and Venmo app users can enter the recipient’s ENS domain directly into the search field when sending digital assets to automatically identify wallets connected to the service.