Sample Category Title

European Central Bank Continues Carefully Along Its Rate Cut Path

Summary

The European Central Bank (ECB) delivered a widely expected 25 bps cut to its Deposit Rate to 3.50% at today's monetary policy announcement, but remained relatively cautious about the pace of future easing. The ECB said domestic inflation and wages are elevated, but that labor cost pressures are moderating. The ECB was also guarded with regards to policy guidance, saying it remains data-dependent, and will take a meeting-by-meeting approach to its monetary policy decisions.

Regarding its economic projections, the ECB lowered its GDP growth forecasts but, importantly, revised its core CPI inflation forecasts slightly higher, in part due to persistent services inflation. Indeed, given the Eurozone productivity and cost backdrop, we believe the risks are tilted toward underlying inflation subsiding more slowly than generally expected. We remain comfortable with our view for an ECB rate pause in October, to be followed by a 25 bps Deposit rate cut in December, which would see the Deposit rate end 2024 at 3.25%. Our view also remains that the ECB will continue lowering its policy rate at a steady 25-bps-per-quarter pace (that is, every other meeting) in 2025, which would see the policy rate reach 2.25% by the end of next year.

European Central Bank Cuts Rates, Keeps Future Easing Options Open

The European Central Bank (ECB), as widely expected, cut its Deposit Rate by 25 bps to 3.50% at today's monetary policy announcement. In lowering interest rates, the ECB described inflationary pressures as still elevated but moderating. Accordingly, the announcement included a mixture of both hawkish and dovish comments. The ECB said:

- Domestic inflation remains high as wages are still rising at an elevated pace, but also that labor cost pressures are moderating, and profits are partially buffering the impact of higher wages on inflation.

- The outlook for core inflation has been revised slightly higher, as services inflation has lingered.

- Financing conditions remain restrictive, and economic activity is still subdued, reflecting weak private consumption and investment.

The ECB was noncommittal regarding the future outlook for policy rates, saying it “will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction” of its monetary policy stance. The ECB also said that it is “not pre-committing to a particular rate path.”

In terms of the ECB's updated economic projections, the central bank lowered its GDP growth forecast for each and every year through its forecast horizon, and now sees Eurozone growth of 0.8% in 2024, 1.3% in 2025 and 1.5% in 2026. These are moderately softer than our own growth forecasts over the same period. Importantly, however, the ECB's forecasts indicated a slower ebbing in underlying inflation pressures than previously. The ECB projects core CPI inflation (that is, CPI ex food and energy) of 2.9% for 2024 and 2.3% for 2025, a touch higher than in the June projections. The core CPI forecast for 2026 of 2.0% is unchanged, and in line with the ECB's inflation target.

We also note some “hawkish leaning” comments from ECB President Lagarde in the post-meeting press conference. Lagarde said domestic inflation is not satisfactory and the ECB must be resilient in its approach. She also said there was a relatively short period of time until the ECB's October monetary policy meeting. Considering ECB President Lagarde's comments, and the upward revision to the ECB's core inflation projections, we remain comfortable with our view for an ECB rate pause in October, to be followed by a 25 bps Deposit rate cut in December, which would see the ECB's Deposit rate end 2024 at 3.25%.

Eurozone: Unimpressive Economic Growth, Lingering Inflation

Following a period of stagnation in the second half of last year, the Eurozone economy has returned to an expansion path during 2024, although the pace of growth has been unimpressive. Q2 GDP rose just 0.2% quarter-over-quarter and 0.6% year-over-year, and the underlying details were also subdued in tone. Q2 consumer spending actually fell 0.1% quarter-over-quarter, while much of the headline Q2 GDP growth stemmed from increased government spending and exports. Sentiment surveys have been mixed in recent months, although they did appear to get an Olympics-related boost in August, as the services PMI rose to 52.9 while the manufacturing PMI was steady at 45.8.

While economic indicators have been mixed, we believe the outlook remains for overall moderate and positive economic growth in the quarters ahead. With employment continuing to grow gradually, Eurozone real household income trends remain on a favorable path. For example, real employee compensation rose 2.5% year-over-year in Q2 while real household disposable income rose 2.6% in Q1, both well in excess of the 0.5% gain registered for consumer spending in Q2. Lower interest rates should ultimately be supportive of the Eurozone consumer, and we note that loans to households have picked up slightly in recent months.

The outlook for business investment is not quite as sanguine, given declining profit growth (that is, year-over-year declines in net entrepreneurial income) and falling capacity utilization. Our estimate of Eurozone core ex-housing investment fell 1.2% year-over-year in Q2, and the prospects for a sharp rebound in investment spending seem limited in the near term. That said, we believe an improving outlook for Eurozone consumers should outweigh the clouded outlook for businesses, and we believe Eurozone economic expansion can continue, albeit at a modest pace.

Even in the context of this underwhelming Eurozone growth outlook, lingering concerns about the inflation outlook, and how quickly inflation pressures are subsiding, have remained. Services inflation in particular has remained elevated, as pointed out in the ECB's announcement, with the latest reading showing a 4.2% year-over-year gain in August. Wage pressures have started to diminish, with the Q2 compensation per employee slowing to 4.3% year-over-year and the ECB's Indicator of Negotiated Wages slowing to 3.6%. Still, current wage growth trends remain above those that prevailed in the decade prior to the pandemic. Moreover, for now, current wage trends likely remain above levels that are consistent with underlying inflation returning to 2% on a sustained basis, particularly given the lack of any pickup in productivity. In terms of productivity, Q2 GDP per employed person actually fell 0.3% year-over-year, in contrast to average growth of 0.8% in the decade prior to the pandemic. We believe ECB policymakers will want to see a further slowing in wage growth, and/or improvement in productivity, to become increasingly confident that domestic inflationary pressures are subsiding. Indeed, in the current productivity and cost backdrop, we see risks that underlying inflation pressures subside more slowly than generally expected. For these reasons, and unless and until the productivity and cost backdrop changes, our view remains that the European Central Bank will continue lowering its policy rate at a steady 25-bps-per-quarter pace (that is, every other meeting), which would see the policy rate reach 2.25% by the end of next year.

September Flashlight for the FOMC Blackout Period

Summary

- Data released since the last FOMC meeting on July 31 make a compelling case for the Committee to begin easing the stance of monetary policy at its upcoming meeting on September 18. Inflation remains a bit above the Fed's target of 2%, but momentum in consumer prices clearly is slowing. Meanwhile, the labor market, the other half of the Fed's dual mandate, has softened.

- As stated by Fed Chair Jerome Powell, "the time has come for policy to adjust." The only question is the magnitude of the rate cut on September 18. Will the FOMC cut rates by 25 bps or sanction a 50 bps reduction?

- We expect the Committee will cut rates by 25 bps at the September 18 meeting based on recent remarks from Fed officials indicating that most favor a go-slow approach at this juncture. That said, some notable Fed officials, including FOMC Chair Powell and Vice Chair Williams, have refrained from commenting on how large a reduction may be warranted in the near term, keeping the door open to a larger cut in September. Therefore, we would not be totally surprised if the FOMC opted for a 50 bps rate cut instead.

- We look for the median dot in the dot plot to shift down by 50 bps to 4.625% for year-end 2024, indicating the median participant thinks another 50 bps of rate cuts after the September meeting will be appropriate by the end of the year. For 2025, we expect the median dot to fall to 3.375%, implying 125 bps of additional easing next year.

- We think that the run of 17 consecutive FOMC meetings without a dissent may be broken at this meeting. If, as we expect, the FOMC cuts rates by 25 bps, then we can envision more dovish voting members of the Committee potentially dissenting in favor of a larger reduction. Conversely, if the FOMC opts for a 50 bps rate cut, then hawkish voting members could dissent, preferring a 25 bps rate reduction instead.

"The Time Has Come for Policy to Adjust"

Data released since the last FOMC meeting on July 31 make a compelling case for the Committee to begin cutting the federal funds rate at its upcoming meeting on September 18. For starters, inflationary pressures continue to subside. Although the year-over-year change in the core PCE price index, which Fed policymakers believe is the best measure of the underlying rate of consumer price inflation, remains above the central bank's target of 2%, momentum in consumer prices is slowing. The index rose at an annualized rate of only 1.7% between April and July, down sharply from the 4.5% annualized rate of change that was registered between December and March (Figure 1). In short, the FOMC has made additional progress recently in fulfilling the "stable prices" component of its dual mandate.

Turning to the other side of the dual mandate, the risks to "maximum employment" are rising. Although payrolls rebounded in August with a 142K monthly gain, up from only 89K in July, the underlying pace of job creation clearly has downshifted. Whereas payrolls rose at an average monthly pace of 207K in the first half of the year, the economy created only 116K jobs per month on average between June and August (Figure 2). Furthermore, the unemployment rate has trended up from 3.7% at the turn of the year to 4.2% in August. Softening in labor market conditions should help to put downward pressure on wage gains, thereby leading to further price growth moderation in coming months. In that regard, average hourly earnings were up 3.8% on a year-ago basis in August, which represents a significant slowing from the 5.9% increase that was registered in March 2022.

With the risks to the two sides of the dual mandate becoming more skewed toward the labor market, the time to begin easing monetary policy appears to have arrived. Federal Reserve Chair Jerome Powell signaled as much in his August 23 Jackson Hole speech when he stated "the time has come for policy to adjust." The only question appears to be the magnitude of the rate cut on September 18. That is, will the FOMC reduce its target range for the federal funds rate by 25 bps or by 50 bps?

We look for the FOMC to cut rates by 25 bps on September 18 based on our sense of the Committee's reaction function at present. Recent remarks from Fed officials indicate most favor a go-slow approach at this juncture. For example, Federal Reserve Governor Christopher Waller, who we consider a bellwether of the Committee, said in a speech after the August jobs report that he expects cuts to be done "carefully." Earlier in August, Fed Governor Michelle Bowman and Federal Reserve Bank of Boston President Susan Collins both indicated support for a "gradual" pace of cuts should inflation continue to ease. Philadelphia Fed President Patrick Harker noted the need to start bringing the fed funds rate down "methodically."

That noted, other Fed officials, including FOMC Chair Powell and Vice Chair John Williams, have refrained from commenting on how large a reduction may be warranted in the near term, keeping the door open to a larger cut in September. Although not our base case view, we readily acknowledge that the Committee may opt for a 50 bps cut in light of inflation having slowed considerably and in an effort to stave off the labor market cooling beyond the point of comfort.

Regardless of the size of the rate cut at the upcoming meeting, we look for the FOMC to ease significantly in the coming months. The stance of monetary policy, which we measure by the real fed funds rate, is quite restrictive at present (Figure 3). The “neutral” real rate is unobservable, but many analysts, including us, estimate it to be in the vicinity of 1.0%-1.5%. With the real rate currently standing at nearly 3%, the FOMC needs to cut the nominal fed funds rate considerably in coming months to get back to neutral. Otherwise, Federal Reserve policymakers risk driving the economy into recession with an overly tight stance of monetary policy. We look for the Committee to cut rates by 225 bps by mid-2025.

Looking for a Downward Shift in the Dots

The quarterly Summary of Economic Projections (SEP), which aggregates the individual macroeconomic forecasts of the 19 FOMC members, will be published at the conclusion of the September 18 meeting. Notably, the last SEP, which was published following the June FOMC meeting, showed the median FOMC member thought that only one 25 bps rate cut would be appropriate by the end of this year (Figure 4). As noted above, however, the risks to the Fed's two mandates have become evenly balanced since the publication of the last SEP, if not tilted toward the labor market in our view. Consequently, the dots for are likely will shift down. But by how much?

We expect the 2024 median dot to fall to 4.625%, implying two additional 25 bps cuts this year (after the September 18 meeting) and consistent with most officials anticipating a measured pace of rate cuts going forward. The dispersion of dots, however, is likely to be unusually wide considering the 2024 projection period will only cover the two remaining meetings of the year (November 7 and December 18). We would not be surprised to see at least one dot as low as 4.125%, and for the upper end of the distribution to indicate just 25 bps of easing this year (a dot of 5.125%).

In the June SEP, the median dot suggested participants anticipated a federal funds rate of 4.125% at year-end 2025. However, given the clear renewed progress in reducing inflation as well as the softening in the jobs market since then, we expect the median dot in 2025 to fall to 3.375%, implying 125 bps of additional easing next year. Compared to the June SEP, we think the 2026 median dot likely will sink 25 bps lower to 2.875%, closer to most participants' estimates of neutral. The upcoming SEP also will provide projections for 2027 for the first time, and we expect the median estimate to be near participants' estimates of the longer run federal funds rate. We do not expect the longer-run median dot of 2.75% to change at this meeting.

The dot plot will garner the most market attention, but the FOMC likely will make some changes to other parts of the SEP. In June, the median forecast for the unemployment rate at the end of 2024 was 4.0%. With the jobless rate currently sitting at 4.2%, an upward revision to that level or even a tick higher seems probable. We also think some downward revisions to inflation in the SEP for this year seem likely. We estimate the Q4/Q4 rate of headline PCE inflation this year will be 2.5% compared to the June SEP estimate of 2.6%, while core PCE inflation is likely be up 2.7%.

Dissenting Voices

Dissents by FOMC voters at policy turning points are not uncommon. For example, the FOMC decided in June 2019 to keep rates on hold for the fourth consecutive meeting. However, James Bullard, who at the time was the president of Federal Reserve Bank of St. Louis, dissented because he preferred a 25 bps rate cut. The Committee then reduced its target range for the fed funds rate at its next meeting in July, but Boston Fed President Eric Rosengren and Esther George, president of Kansas City Fed, both dissented because they wanted to keep rates on hold. A few years later, the FOMC tightened policy by 25 bps in March 2022, the first rate hike in the post-pandemic period. However, St. Louis Fed President Bullard dissented because he preferred a 50 bps increase at that meeting. The Committee accelerated the pace of tightening in June 2022 with a 75 bps rate hike, provoking a dissent by Kansas City Fed President George who preferred a 50 bps increase.

As demonstrated by the absence of dissents in the 17 meetings since the June 2022, the Committee has been more or less unified in its views regarding the appropriate stance of policy over that period. With the FOMC likely to cut rates on September 18 for the first time in more than five years, we would not be surprised to see that streak come to an end. If, as we expect, the FOMC cuts rates by 25 bps, then we can envision more dovish voting members of the Committee (e.g., San Francisco Fed President Mary Daly) potentially dissenting in favor of a larger reduction in the target range for the federal funds rate. Additionally, some dovish members of the Committee who are non-voters this year (e.g., Chicago Fed President Austan Goolsbee) could argue during the meeting that a 50 bps cut is appropriate. Conversely, if the FOMC opts for a 50 bps rate cut, then a hawkish voting member or two of the Committee (e.g., Governor Michelle Bowman or Richmond Fed President Thomas Barkin) could dissent, preferring a 25 bps rate reduction instead.

Sunset Market Commentary

Markets

The US was at the center of attention yesterday with the August inflation figures. The spotlights today were aimed at Frankfurt. The European Central Bank delivered on the widely expected 25 bps rate cut that brought the deposit rate at 3.5%. It cut the MRO and MLF rates by 60 bps (3.65% and 3.90% resp.) in a technical adjustment to narrow the corridor again. In a system of excess liquidity this has no practical implications and says nothing about the monetary stance as such. Updated forecasts showed no change to the headline inflation outlook compared to June: 2.5%, 2.2% and 1.9% through 2024-2026. Core inflation was upped slightly to 2.9% and 2.3% for the running and next year, owing to higher-than-expected services inflation. Still-elevated wages are responsible but the ECB is seeing those labour cost pressures moderating. Core inflation should eventually decline to 2% in 2026 (no change). Growth was lowered 0.1 ppts across the policy horizon (0.8%, 1.3% and 1.5%) mainly due to a weaker contribution from domestic demand. With the recovery continuing to face headwinds, growth risks remain tilted to the downside. These growth & inflation dynamics as well as growing conviction of reaching the 2% target (especially over 2025) allow for a lesser degree of monetary restriction but ongoing vigilance remains warranted. The ECB sticks to a data-dependent approach and does not pre-commit to anything. Given the short time span between this meeting and the next - Lagarde during the presser confirmed the 6-week span is indeed limited - we believe the ECB will skip the rate cut occasion on October 17 and gets back at it in December. Questions about what to expect next/beyond October were easily deflected. Lagarde obviously did not want to validate current market expectations of (give or take) another 50 bps of cuts this year and instead explained painstakingly detailed how they came to today’s unanimous decision. Lagarde also took her time to throw some flowers to her predecessor Draghi and his extensive report earlier this week. That says something on her intentions of not wanting to reveal anything that carried a shred of new information. Markets reacted accordingly with near-zero movement in EUR/USD (1.103) or yields. German rates do add between 1 (30-yr) and 5.2 bps (2-yr) but the bulk of the move happened already before the decision. The ECB outcome coincided with some second-tier US data. But both jobless claims (230k) and PPI numbers (headline 0.2% m/m and 1.7% y/y, core 0.3% m/m and 2.4%) came in too close to expectations to move a needle.

News & Views

Swedish headline inflation fell by 0.6% M/M in August, more than the 0.4% decline expected. Headline inflation fell below the Riksbank’s 2% inflation target for the first time since July 2021 (1.9% Y/Y from 2.6% vs 2.1% expected). The central bank’s preferred CPIF inflation gauge (using fixed mortgage rates) similarly fell by 0.5% M/M to 1.2% Y/Y (from 1.7% vs 1.4% consensus). Excluding energy, CPIF fell by 0.3% M/M to stabilize at 2.2% Y/Y. Food (-0.4%), electricity (-6.1%), transport (-2.7%) and package holidays’ prices (-19.1%) all decreased in August. Higher clothing prices (+5%) only partly offset these price drops. Today’s inflation numbers strengthen market bets that the Swedish central bank will cut its policy rate at all of this year’s three remaining policy meetings, the upper end of the Riksbank’s own 2 to 3 times guidance. The Swedish krone didn’t suffer from the CPI miss (EUR/SEK 11.44). Next month, Statistics Sweden will introduce flash estimates for inflation, called Flash CPI. The Flash CPI is a preliminary figure and will be published five working days before the regular publication (first release Oct 8).

The International Energy Agency released its September Oil Market Report. Global oil demand growth continues to decelerate, with reported 1H24 gains of 800k b/d y/y the lowest since 2020. The chief driver of this downturn is a rapidly slowing China. Outside of China, oil demand growth is tepid at best. World supply rose by 80k b/d to 103.5m b/d, with outages caused by a political dispute in Libya combined with maintenance in Norway and Kazakhstan offset by higher flows from Guyana, Brazil and elsewhere. The IEA fears that OPEC+ may be staring at a substantial surplus even if its extra curbs were to remain in place with non-OPEC+ supply rising faster than overall demand. Early September, the oil cartel announced to postpone by two months the start of their planned unwinding of extra voluntary production cuts. Brent crude prices fell from $80/b+ levels at the start of the month to currently $71/b on growth slowdown/recession fears.

Graphs

European 2-yr swap yield unhindered by telegraphed ECB rate cut. Looks for a return higher after hitting 2.4% support yesterday.

EUR/USD shrugs at today’s policy decision as ECB offered no guidance on what to expect next.

EuroStoxx50 stages a cautious rebound after kicking off September on terrible footing.

EUR/SEK: Swedish crown holds steady despite CPI miss boosting bets for 3 more Riksbank rate cuts this year.

NZ Dollar Drifting Ahead of Manufacturing Data

The New Zealand dollar is showing little movement on Thursday. NZD/USD is trading at 0.6139 at the time of writing, up 0.05% on the day.

New Zealand’s Manufacturing PMI expected to improve

New Zealand’s manufacturing sector has been in the doldrums, as the manufacturing PMI has posted 17 consecutive declines. Friday’s PMI is expected to improve to 47 in August, up from 44 in July (a reading below 50 points to contraction). The New Zealand economy has deteriorated and in August the Reserve Bank of New Zealand responded with its first rate cut since March 2020. The RBNZ has joined the club, as most major central banks have lowered rates and the Federal Reserve is poised to do so next week.

The RBNZ will be looking to continue lowering rates, as the cash rate of 5.25% remains high and is weighing on economic activity and households. Inflation has dropped to 3.3%, which is close to the target of between 1% and 3%. The central bank meets next on Oct. 9 and there is pressure on the RBNZ to follow up with a second straight rate cut.

In the US, today’s inflation numbers were a mix. Headline producer prices rose 1.7% Y/Y in August, following a downwardly revised 2.1% gain in July and just below the market estimate of 1.8%. However, core PPI rose from 2.3% to 2.4%, below the estimate of 2.5%. Today’s PPI data didn’t budge the market pricing of a Fed rate cut, with an 87% probability of a 25-bps cut next week, according to the CME FedWatch tool. Still, not everybody is on board for small cut – JP Morgan is projecting that the Fed will deliver a jumbo 50-bps reduction.

NZD/USD Technical

- NZD/USD is testing resistance at 0.6134. Above, there is resistance at 0.6160

- There are support lines at 0.6110 and 0.6084

AUD/USD Edges Higher as Inflation Expectations Eases

The Australian dollar has posted slight gains on Thursday. In the European session, AUD/USD is up 0.16%, trading at 0.6684 at the time of writing.

Australia’s inflation expectations dip to 4.4%

Australia’s consumer inflation expectations eased to 4.4% in September, down slightly from 4.5% in August but above the forecast of 4.1%. The small decline reflects the path of inflation, which is moving lower but at a slow pace, a source of concern for the Reserve Bank of Australia.

The RBA has made considerable progress in the battle with inflation but inflationary pressures remains sticky despite elevated interest rates. Most major central banks have cut rates in the new era of lower inflation but the RBA is yet to join the club.

Inflation fell to 3.5% in July, down from 3.8% but above the market estimate of 3.4%. This remains well above the RBA’s target of between 2 and 3 percent. Governor Bullock has said that it’s too early to consider lowering rates but the markets are more dovish and expect an initial rate cut later in the year. The RBA meets next on Sept. 24 and is expected to maintain the cash rate at 4.35%, although an unexpected figure from next week’s employment report could mean some suspense before the rate announcement.

The Federal Reserve meets on Sept. 18 and the markets have fully priced in a rate cut. The Fed has held rates at the 5.25-5.50% target for over a year and this initial cut could have a significant impact on the financial markets. The most likely scenario is a modest 25-bps cut but JP Morgan is projecting a jumbo 50-bps cut.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6693. Above, there is resistance at 0.6711

- 0.6657 and 0.6639 are the next support levels

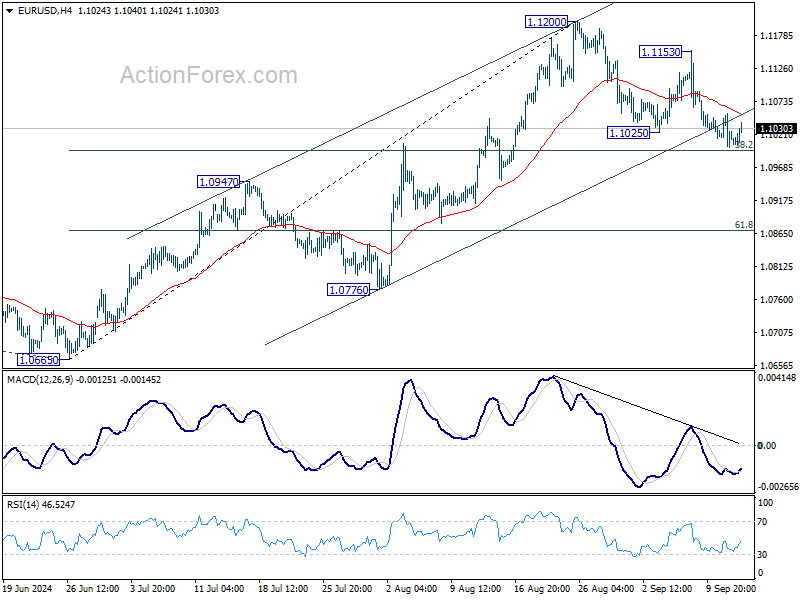

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0991; (P) 1.1023; (R1) 1.1044; More....

Intraday bias in EUR/USD stays neutral despite current mild recovery. Focus stays on 38.2% retracement of 1.0665 to 1.1200 at 1.0996. Strong rebound from there will retain near term bullishness. Break of 1.1153 will indicate that larger rally is resuming through 1.1200 resistance to 1.1274 high. However, sustained break of 1.0996 will indicate reversal and turn bias to the downside for 1.0947 resistance turned support next.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Euro Recovers Ground as ECB Cuts Rates; Gold Surges to Record High

Euro made a modest recovery following ECB's decision to cut deposit rate by 25bps, a move widely anticipated by the markets. The rate cut, decided unanimously, brings the deposit rate to 3.75%. During her post-meeting press conference, ECB President Christine Lagarde provided no surprise, reiterating the central bank’s commitment to a “data-dependent” and “meeting-by-meeting” approach. Lagarde stressed that policymakers would not rely on any single data point but instead assess a wide range of indicators. Importantly, she noted that ECB is not pre-committing to any specific future rate path, leaving the door open for adjustments depending on evolving economic conditions.

In the broader currency market, Yen emerged as the strongest performer for the day so far. Euro followed closely behind, buoyed by post-ECB relief, while Sterling also saw modest gains. On the weaker side, Swiss Franc and Canadian dollar lagged, with Dollar underperforming too. Meanwhile, Australian and New Zealand Dollars traded in middle positions.

Technically, Gold finally surges to new record high today. Near term outlook will now stay bullish as long as 2510.93 support holds. Next target is 61.8% projection of 2364.18 to 2531.52 from 2471.76 at 2575.17.

In Europe, at the time of writing, FTSE is up 0.65%. DAX Is up 0.79%. CAC is up 0.61%. UK 10-year yield is down -0.0086 at 3.763. Germany 10-year yield is up 0.0076 at 2.123. Earlier in Asia, Nikkei rose 3.41%. Hong Kong HSI rose 0.77%. China Shanghai SSE fell -0.17%. Singapore Strait Times rose 0.72%. Japan 10-year JGB yield rose 0.0124 to 0.866.

US PPI up 0.2% mom, 1.7% yoy in Aug

US PPI rose 0.2% mom in August, matched expectations. PPI services rose 0.4% mom while PPI goods was unchanged. PPI less foods, energy, and trade services rose 0.3% mom.

For the 12 month period, PPI advanced 1.7% yoy, slowed from 2.1% yoy. PPI less foods, energy and trade services moved up 3.3% yoy.

US initial jobless claims rises slightly to 230k

US initial jobless claims rose 2k to 230k in the week ending September 7, slightly below expectation of 231k. Four-week moving average of initial claims rose 500 to 231k.

Continuing claims rose 5k to 1850k in the week ending August 31. Four-week moving average of continuing claims fell -2k to 1853k.

ECB cuts deposit rate by 25bps to 3.75%

ECB followed expectations by lowering the deposit rate by 25 bps to 3.75%. The main refinancing rate was adjusted to 3.65%, as the spread between the two rates is now set at 15 bps. Moving forward, the ECB emphasized its commitment to a "data-dependent" and "meeting-by-meeting" approach, avoiding any pre-commitment to a specific rate path.

In its accompanying statement, ECB highlighted that recent inflation data had been largely in line with projections. Inflation is expected to rise again towards the end of the year, primarily due to the base effect from last year’s sharp energy price falls. The central bank anticipates inflation will decline closer to its target in the second half of 2025.

Updated inflation forecasts show headline inflation averaging 2.5% in 2024, 2.2% in 2025, and hitting 1.9% by 2026. Core inflation is projected to fall from 2.9% in 2024 to 2.3% in 2025, and eventually reach 2.0% in 2026.

On the growth front, there was a slight downward adjustment in the outlook. The Eurozone economy is now expected to expand by 0.8% in 2024, with growth improving to 1.3% in 2025 and 1.5% in 2026.

Japan's wholesale price growth slows sharply to 2.5% yoy in Aug as Yen rebounds

Japan's corporate goods price index decelerated to 2.5% yoy in August, falling below market expectations of 2.8% yoy, marking the first slowdown in eight months. The data reflects a cooling in price pressures, which has been reinforced by a significant 7.4% appreciation in Yen during the month.

The stronger Yen drove a steep slowdown in Yen-based import prices, with the annual growth rate dropping sharply from 10.8% yoy in July to just 2.6% yoy in August. This marks a considerable easing in import costs, offering some relief to Japanese businesses relying on foreign goods.

On a month-to-month basis, CGPI fell by -0.2% mom, while import prices measured in yen contracted significantly by -6.1% mom. The sharp fall in import costs suggests that the stronger yen is playing a key role in softening inflationary pressures, especially in the context of global commodity prices.

BoJ's Tamura advocates for gradual rate increase to 1% neutral mark

BoJ board member Naoki Tamura indicated in a speech today that the likelihood of achieving 2% inflation target sustainably is improving. As a result, the central bank needs to gradually raise interest rates to neutral levels.

Tamura estimated Japan's neutral interest rate, or the rate that neither stimulates nor slows down economic activity, to be at least around 1%.

He added, "As such, it's necessary to push up our short-term policy rate at least to around 1% by the latter half of the fiscal year ending March 2026 to sustainably achieve the BoJ's price goal."

In light of growing labor shortages and rising wage pressures, Tamura warned that inflation risks were increasing. Companies are responding to tight labor market conditions by raising wages and passing on higher costs through price hikes.

Tamura underscored the need to "raise interest rates at an appropriate timing, and in several stages," in order to keep inflation under control.

This marked the first time a BoJ policymaker had publicly specified a target level for raising short-term interest rates.

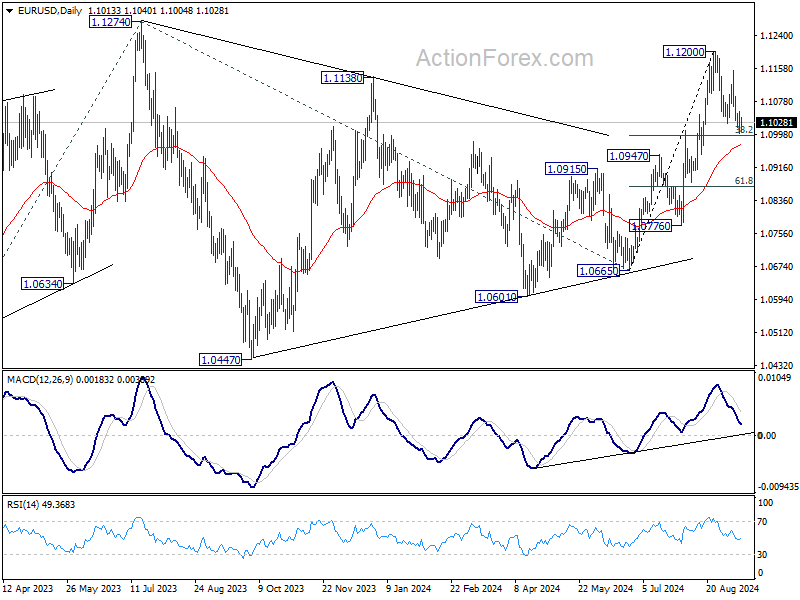

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0991; (P) 1.1023; (R1) 1.1044; More....

Intraday bias in EUR/USD stays neutral despite current mild recovery. Focus stays on 38.2% retracement of 1.0665 to 1.1200 at 1.0996. Strong rebound from there will retain near term bullishness. Break of 1.1153 will indicate that larger rally is resuming through 1.1200 resistance to 1.1274 high. However, sustained break of 1.0996 will indicate reversal and turn bias to the downside for 1.0947 resistance turned support next.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Aug | 1.00% | -14% | -19% | -18% |

| 23:50 | JPY | BSI Large Manufacturing Index Q3 | 4.5 | -2.5 | -1 | |

| 23:50 | JPY | PPI Y/Y Aug | 2.50% | 2.80% | 3.00% | |

| 01:00 | AUD | Consumer Inflation Expectations Sep | 4.40% | 4.50% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | 3.65% | 3.65% | 4.25% | |

| 12:15 | EUR | ECB Deposit Rate | 3.50% | 3.50% | 3.75% | |

| 12:30 | CAD | Building Permits M/M Jul | 22.10% | 6.50% | -13.90% | |

| 12:30 | USD | PPI M/M Aug | 0.20% | 0.20% | 0.10% | 0.00% |

| 12:30 | USD | PPI Y/Y Aug | 1.70% | 1.80% | 2.20% | 2.10% |

| 12:30 | USD | PPI Core M/M Aug | 0.30% | 0.20% | 0.00% | |

| 12:30 | USD | PPI Core Y/Y Aug | 2.40% | 2.50% | 2.40% | |

| 12:30 | USD | Initial Jobless Claims (Sep 6) | 230K | 231K | 227K | 228k |

| 12:45 | EUR | ECB Press Conference | ||||

| 14:30 | USD | Natural Gas Storage | 49B | 13B |

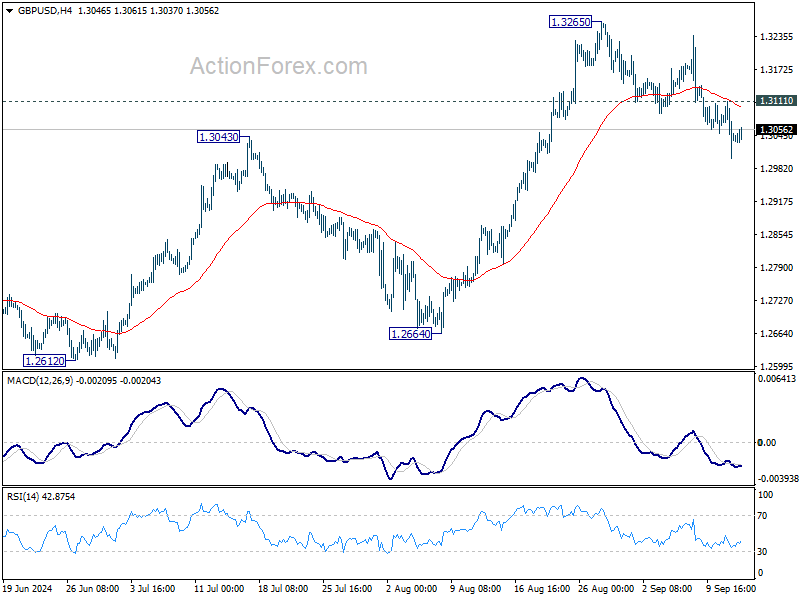

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2993; (P) 1.3052; (R1) 1.3103; More...

Intraday bias in GBP/USD stays mildly on the downside at hits point. Fall from 1.3265 short term top is in progress for 55 D EMA (now at 1.2949). Sustained break there will bring deeper fall to 1.2664 key support. On the upside, above 1.3111 minor resistance will turn intraday bias neutral first. But risk of another pull back remains as long as 1.3265 resistance holds.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

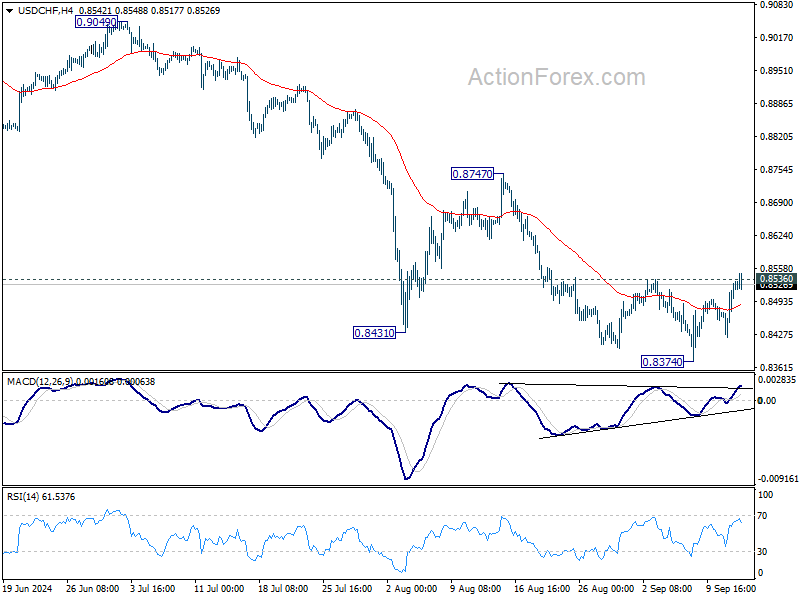

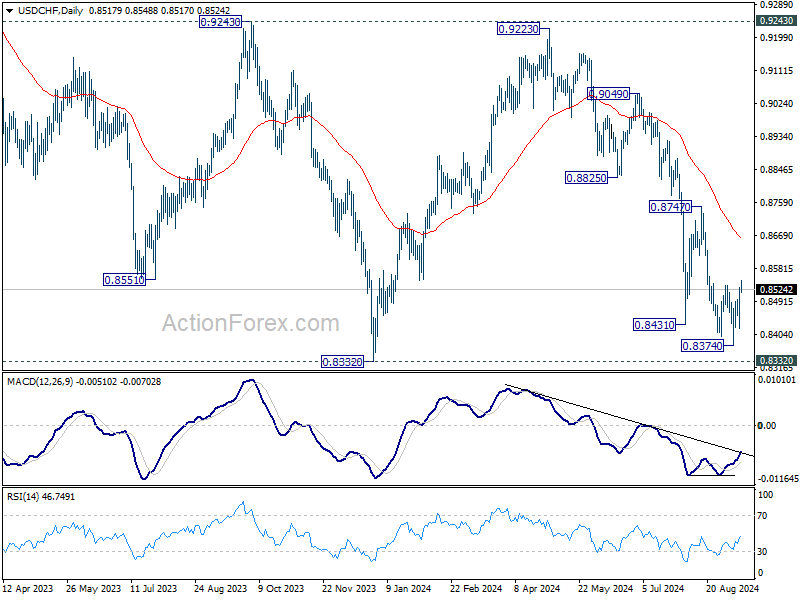

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8453; (P) 0.8491; (R1) 0.8561; More…

Focus remains on 0.8536 resistance in USD/CHF. Rejection by this resistance will retain near term bearishness. Break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8536 resistance will now confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

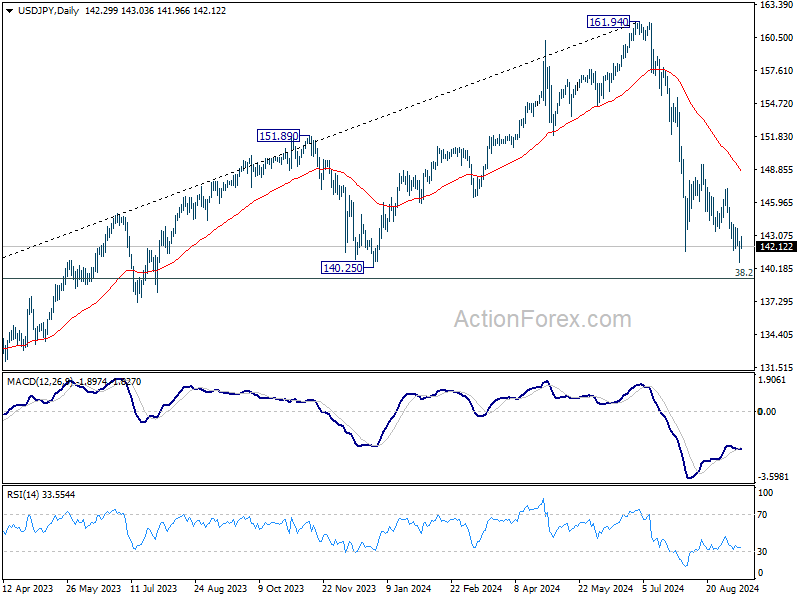

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.20; (P) 141.87; (R1) 143.04; More...

USD/JPY is staying in consolidation above 140.70 temporary low and intraday bias remains neutral at this point. Outlook will remain bearish as long as 147.20 resistance holds. On the downside, break of 140.70 will resume the fall from 161.94 to 140.25 support, and possibly to 139.26 fibonacci level too.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. Strong support could be seen there to bring rebound. But in any case, risk will stay on the downside as long as 55 W EMA (now at 148.93) holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.