Sample Category Title

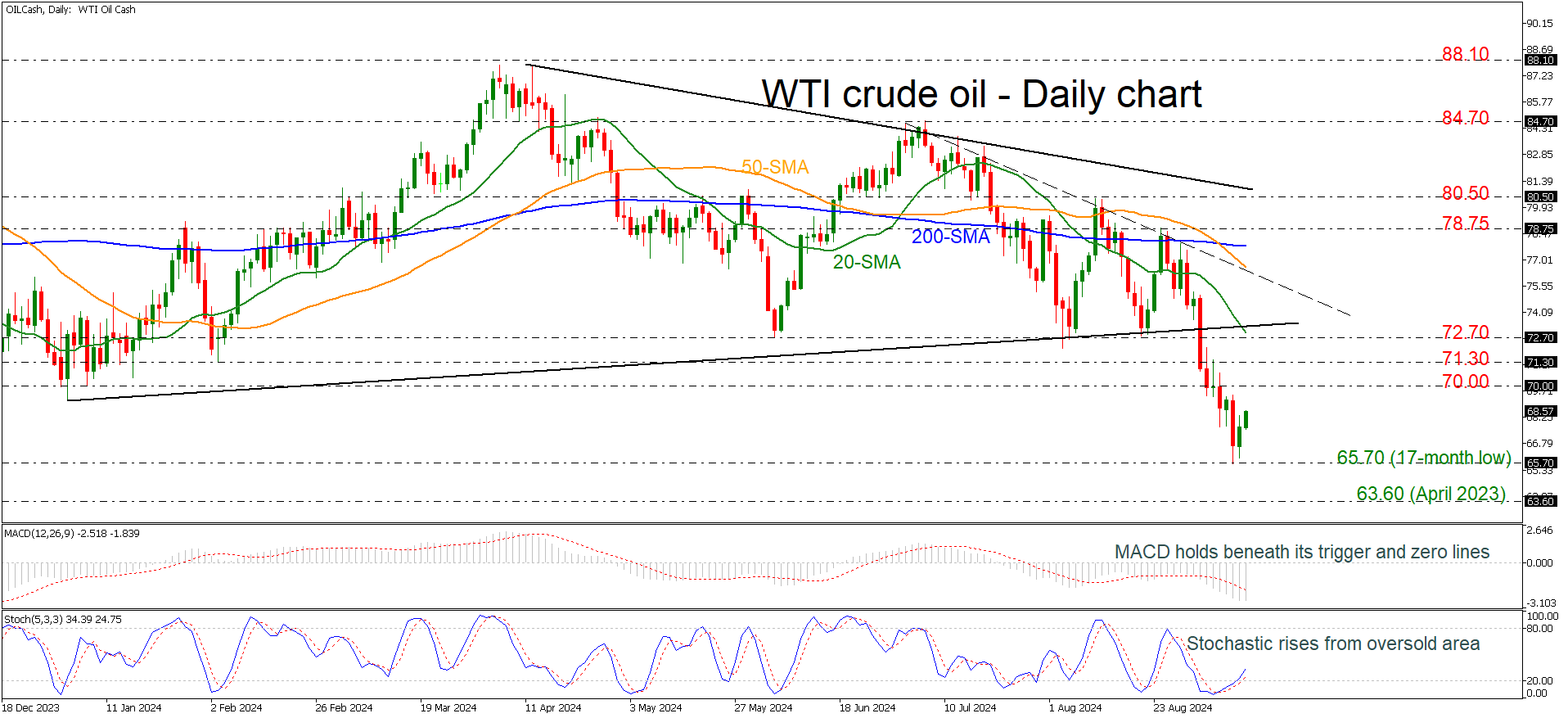

WTI Crude Oil Recoups Some Losses After Sell-off

- WTI crude oil rises from 17-month low

- Momentum oscillators gain some ground

WTI crude oil has finally climbed higher from the 17-month low of 65.70 after the aggressive selling interest from the 78.75 resistance. Over the last three weeks, the commodity has lost more than 16%, switching the outlook to strongly bearish.

According to technical oscillators, the MACD is losing its negative momentum and is ticking slightly up, while the stochastic oscillator is heading north after the bullish crossover within its %K and %D lines in the oversold area. Both are indicating that the sharp selling interest may come to an end.

If the market continues the upside rally, then the price may find resistance at the 70.00 psychological level ahead of the 71.30 and 72.70 levels. A jump above the uptrend line and the 20-day simple moving average (SMA) could find immediate obstacle at the short-term descending trend line at 76.60, which overlaps with the 50-day SMA.

In the negative scenario, a downturn beneath the multi-month low could boost the sell-off until the next support which is taken from the bottom in April 2023 at 63.60.

In brief, oil prices have been in a significant downward move since July 3 and only a jump above the 84.70 resistance level may switch the outlook to bullish.

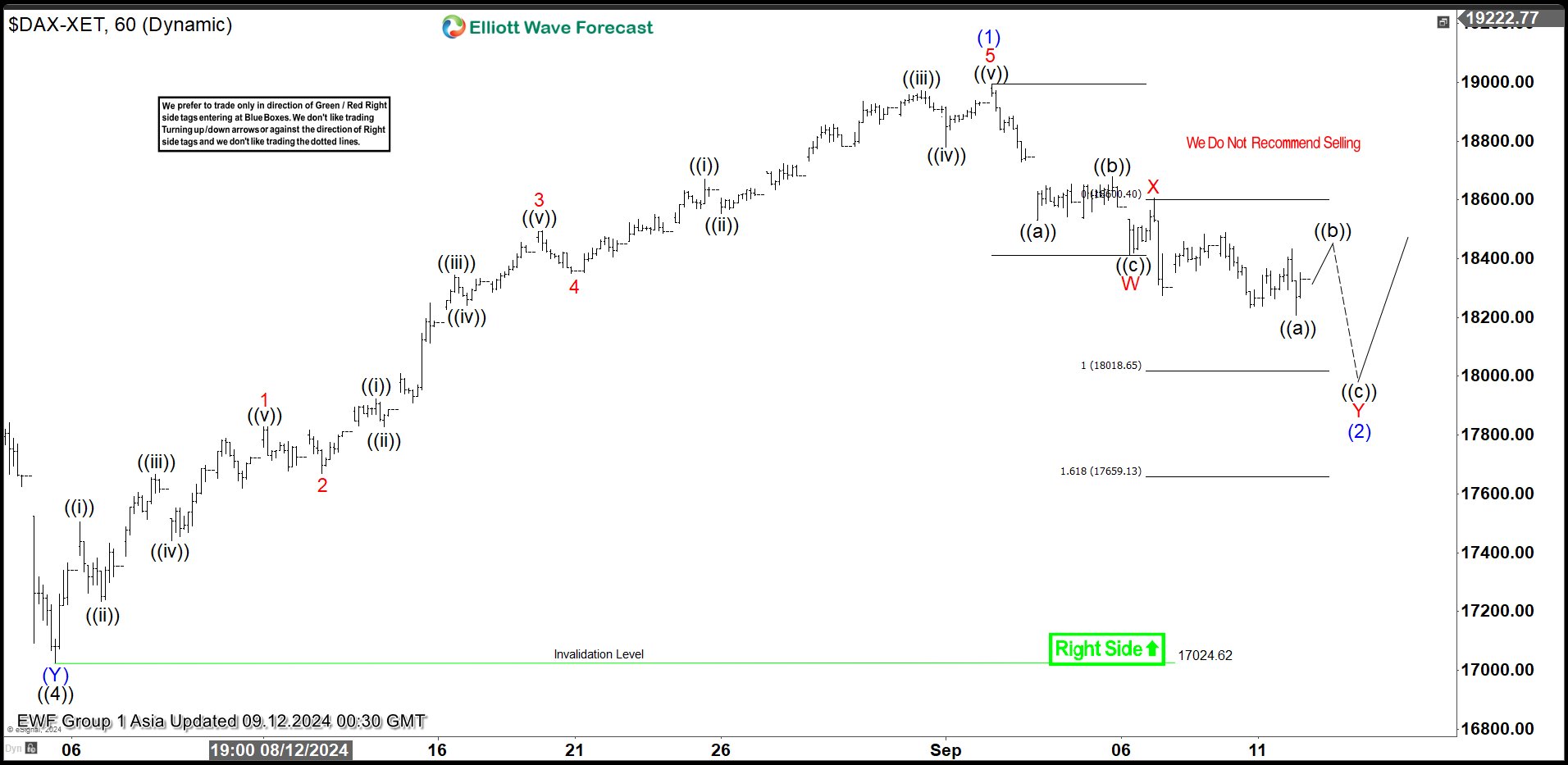

Elliott Wave Intraday Analysis Expects DAX to Turn Higher Soon

Short Term Elliott Wave view on DAX suggests that the Index is correcting cycle from 8.5.2024 low in 3, 7, or 11 swing before it resumes higher. The pullback on 8.5.2024 towards 17024.6 ended wave ((4)). The Index has turned higher in wave ((5)) with internal subdivision as an impulse Elliott Wave structure. Up from wave ((4)), wave ((i)) ended at 17505.23 and wave ((ii)) pullback ended at 17233.07. Wave ((iii)) higher ended at 17666.82 and pullback in wave ((iv)) ended at 17439.87. Wave ((v)) higher ended at 18920.1 which completed wave 1 in higher degree. Dips in wave 2 ended at 17669.64.

Up from wave 2, wave ((i)) ended at 17921.99 and wave ((ii)) ended at 17827.08. Wave ((iii)) higher ended at 18344.22 and wave ((iv)) ended at 18240.17. Wave ((v)) higher ended at 18495.28 which completed wave 3 in higher degree. Pullback in wave 4 ended at 18349.98. Final leg wave 5 ended at 18990.78 which completed wave (1) in higher degree. Wave (2) pullback is in progress to correct cycle from 8.5.2024 low as a double three Elliott Wave structure. Down from wave (1), wave W ended at 18414.13 and wave X ended at 18607.79. Expect wave Y to extend lower to correct cycle from 8.5.2024 low in 7 swing towards 17659.1 – 18018.6 area before it turns higher. As far as pivot at 17024.62 low stays intact, expect pullback to find support in 3, 7, 11 swing for more upside.

DAX 60 Minutes Elliott Wave Chart

DAX Elliott Wave ChartDAX Elliott Wave Video

https://www.youtube.com/watch?v=YbaZfXCij8w

ECB Expected to Cut Deposit Rate for Second Time This Year

Markets

US yields finished 0.3 bps (30-yr) to 4.6 bps (2-yr) higher yesterday in a volatile session. The (trade-weighted) dollar approaches first resistance at 101.92/102 (101.68 close). EUR/USD came within striking distance of the 1.10 mark. For most of US trading hours, the key question was whether a small upward surprise in monthly US core CPI (0.3% M/M instead of 0.2%) was sufficient to completely close the door on a 50 bps rate cut by the Fed next week. In the end, money markets reduced bets on such a start, but the door remains open. The upward surprise came especially from shelter costs and was for a large part compensated for by lower energy prices. Core US CPI could nevertheless remain sticky above 3% Y/Y for somewhat longer than earlier anticipated. The US Treasury’s $39bn 10-yr Note auction was strong with the auction yield 1.4 bps below the WI yield. The bid-cover (2.64) was also above the 6-month average (2.53). An AI-driven rally pulled US stock markets up to 2.17% higher for the Nasdaq.

The ECB is expected to cut its deposit rate for a second time this year by 25 bps, to 3.50%. As announced in March, they will also reduce the spread between the main refinancing rate and the deposit rate from the current 50 bps to only 15 bps implying an MRR rate cut of 60 bps, from 4.25% to 3.65%. Updated GDP and CPI forecasts will be closely watched for clues on the monetary policy trajectory going forward. However, we don’t expect big changes apart from perhaps some minor downward revisions to this year’s GDP and headline CPI data. Recall that ECB staff in June plotted a 0.9%-1.4%-1.6% growth path for 2024-2026 and a 2.5%-2.2%-1.9% inflation trajectory. While keeping an easing bias, we don’t expect the central bank to pre-commit to specific actions at coming meetings. The short intermeeting period between September 12 and October 17 suggests that bar any big surprise, the central bank might be more inclined to sit the October meeting out and stick with the currently, quarterly, rate-reduction scheme with a next 25 bps move coming only in December. Unlike the Fed, the ECB’s options for making policy less restrictive are smaller given limited room towards neutral territory in the current, stubborn, (core) inflationary environment. EMU money markets currently attach a 40% probability to a follow-up rate cut in October. Even if Lagarde holds back from giving any guidance for October, we believe that market speculation will remain in a context where most central banks are making their monetary policies less restrictive. This suggests that any market reaction on today’s statement and Q&A session (higher ST EUR rates and stronger EUR) could be modest and in any case temporary in nature.

News & Views

Insiders say the European Commission is examining its options to roll over several hundreds of billions of euros of EUNextGen bonds issued during the Covid-era. At the heart of the issue are the ones issued to finance the grants distributed to the member states. Unlike the loans, which have to be paid back by member states from 2031 on, the EC has no means outside the budget to repay those bonds when they start maturing. The amount of grants currently disbursed is some €170bn but could increase to as much as €357bn. Leaving the matter unaddressed would result in yearly debt repayments and interest costs of around €30bn from 2028 on – an amount that roughly equals a sixth of the EU’s current annual spending. Former ECB president Draghi in his report on European competition earlier this week warned for this looming budget squeeze given the unwillingness (for now) of EU member states to give the Commission revenue-raising powers or additional money. It was Draghi too who floated the idea of rolling over the debt. The topic is a controversial one, especially for the likes of Germany who’s constitutional court only approved the EUNextGen programme on the grounds it was a one off and time-limited. Changing the terms requires unanimous backing of all member states.

The UK Royal Institution of Chartered Surveyors (RICS) said the house price balance edged up to 1% in August, a significant jump from the -18% recorded in July (and vs consensus of -14%). It was the first positive outcome since October 2022 and has come a long way from the a post-GFC low at -64.5% exactly one year ago. All subindices posted improvements compared to July with price expectations (from 9% to 14%), sales expectations (37%) and new buyer enquiries (15%) al rising solidly. Agreed sales (6%) climbed to the highest level since May 2021.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU activity data rolled in, dragging the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is moving to a better in to balance. The pivot weakened the technical picture in US yields. A string of weak eco data and a risk-off market climate pushed and kept the 10-yr sub 4%. We think we could be up to three 50 bps rate cuts this year.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. EUR/USD 1.1276 (2023 top) serves as next technical references.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Recent better UK activity data and a cautious assessment of BoE’s Bailey at Jackson Hole are pushing EUR/GBP lower in the 0.84/0.086 range.

ECB to Cut Rates by 25bp

In focus today

Today, the ECB is widely expected by both analysts and markets to deliver a 25bp rate cut. The moderation in the labour market and economic activity since the June meeting should lead to a further increase in the confidence of the disinflationary process being on track, in particular given the slowdown in wage growth. For more details, please see ECB preview - Dialling back, but pace uncertain, 5 September.

In Norway, the Regional Network survey is released, providing insights into capacity utilisation, which could be decisive for Norges Bank's message on 19 September. Although Norges Bank advised markets in June against speculating on rate cuts this year, recent domestic and global developments have considerably increased the probability of a rate cut in 2024. If capacity utilisation metrics turn over significantly, we stand ready to adjust our current call for the first Norges Bank rate cut to not come until March 2025.

In Sweden, CPI for august is released. We expect CPIF inflation to drop significantly to 1.1% y/y in August, 0.6 pp. below the Riksbank's forecast. Our forecast for CPIF excl. energy at 2.1% y/y aligns closely with the Riksbank's view. If correct, focus is on how the Riksbank will handle such an outcome in its monetary policy.

Economic and market news

What happened overnight

In Japan, wholesale inflation for August was lower than expected at -0.2% m/m and 2.5% y/y, compared to consensus of 0.0% m/m and 2.8% y/y. The surprise was due to the yen's rebound, which eased import cost pressures. The slowdown, expected to impact consumer prices in the months ahead, could influence the timing of the Bank of Japan's (BoJ) next rate hike. Moreover, this morning, the hawkish BoJ member Tamura stated that rates must rise to at least 1% by late next year, as the likelihood of achieving the 2% inflation target sustainably has improved. Tamura's comment, the first to specify a target rate, follows other BoJ members advocating for continued hikes despite market turmoil.

What happened yesterday

In the US, headline inflation in August was close to expectations at 0.2% m/m SA and 2.5% y/y (cons: 0.2% m/m SA, 2.6% y/y). Core inflation was slightly higher than expected at 0.3% m/m SA (cons: 0.2%), while the yearly figure matched expectations. The modest upside surprise was mostly driven by shelter prices, while price pressures elsewhere in the services sector, in core goods as well as in food and energy were close to expectations. Shelter, and more precisely the contribution from owners' equivalent rent (OER) rose to the highest level since January. However, it should be noted that shelter CPI lags changes in the actual rental/real estate market by 10-11 months, implying that this should not be seen as a sign of re-accelerating inflation pressures. Hence, the print does not derail the Fed from cutting rates next week but supports our case of a 25bp cut. After the release, markets priced the odds of 25/50bp cuts at 85%/15% in favour of a smaller move.

Kamala Harris emerged as the stronger candidate in the presidential debate against Donald Trump. Harris conveyed a more forward-looking vision, while Trump mainly focused on criticizing the current administration and lacked clarity on his own initiatives. Republican strategists noted that while Trump's performance was not seen as a major setback, his re-election bid appeared more uncertain. A YouGov flash poll showed 43% of viewers saw Harris as the winner, compared to 28% for Trump, with 30% undecided.

Harris now also seems to be the clear favourite according to prediction markets. However, the race remains close, particularly in the swing states. For details on the US election, see our US Election Monitor, 6 September, which we plan to update bi-weekly until election day.

The markets reacted to the debate by sending the USD and yields slightly lower, suggesting that expectations of Trump pursuing more expansionary fiscal policies and protectionist measures remain intact. Yesterday's price action likely provides a good gauge for how markets may react to election news going forward, though the longer-term implications are less clear-cut.

In the UK, the monthly GDP figure for July was weaker than expected at 0.0% m/m (cons: 0.2%, prior: 0.0%), signalling an economy starting to lose steam, while the 3M/3M measure printed at 0.5% (cons: 0.6%, prior: 0.6%). The downside surprise was broad-based, driven by declines in industrial and manufacturing production as well as construction, while services continued to contribute positively. That said, it should be noted that this data is of volatile nature, and hence that the topside risk to demand is still in place - in line with the Bank of England's expectation.

Equities: Global equities rose yesterday, led by US large-cap, cyclical growth stocks. This movement was prompted by a slightly higher-than-expected CPI, which sent the short end of the yield curve higher in the US, thereby reducing the likelihood of a 50-basis point cut next week. Hence, equity investors see it as a relief that the Fed may not need to implement a double cut, implicitly indicating that the economic outlook remains solid. Additionally, there was a significant cyclical rotation, with energy being the worst performer and tech performing exceptionally well. If yesterday's boost to equities had been driven by strong growth or demand numbers, we would have likely seen more broad-based gains, and energy would not have underperformed so significantly. It is also important to note the negative correlation between bonds and equities on a CPI day. This indicates significant progress in the inflation normalization process and a shift in investor views on inflation. In the US yesterday, the Dow closed up by 0.3%, the S&P 500 by 1.1%, the Nasdaq by 2.2%, and the Russell 2000 by 0.3%. Asian markets soared this morning, with some of the most cyclical and tech-heavy markets up more than 3%. US futures are also trending higher, with European futures up by more than 1%.

FI: Today's main event is the ECB meeting. A 25bp cut seems to be a done deal, and markets will therefore focus on guidance and the updated staff projections at the meeting. On Friday, the broad wage measure - compensation per employee - showed a noticeable decline in the annual wage growth in Q2 from 4.8% y/y to 4.3% y/y, and this has likely dampened some of the concern related to the still elevated domestic inflation measures in August. We expect Lagarde to confirm that ECB is entering the dialling back phase, but we do not expect a commitment to a specific timing of further cuts; thus, we do not anticipate that it will deviate from the meeting-by-meeting and data-dependent approach to the policy rate changes, thereby keeping its guidance's optionality and flexibility. Markets are pricing 62bp this year and 126bp in 2025. See ECB preview - Dialling back, but pace uncertain, 5 September.

FX: While the USD gained modestly in yesterday's session the most notable G10 move was the sell-off in NOK which stopped just around the 12.00 figure in EUR/NOK before the Norwegian currency found some well-needed support from Brent crude moving back above USD 70/bbl. EUR/SEK remains in the low 11.40s while USD/JPY failed to extend a move below 142. Finally, EUR/CHF rebounded just short of the 0.93-level before finding a newly weekly high around 0.94.

ECB Meets as Fed Doves Wave Goodbye to Jumbo Cut

The latest US CPI data, and the reaction to data was mixed on Wednesday. The good news is that the headline inflation fell from 2.9% to 2.5% in August, and sank significantly below the 3% level where it was resisting since last summer. The drop in food and energy prices helped easing pressure in the headline figure. But core inflation – which excludes volatile food and energy prices – came in line with the expectations on a yearly basis, and slightly higher-than-expected on a monthly basis. Cost of housing and travel were responsible for the stickiness in core inflation.

While the retreat in food prices is the continuation of the post-pandemic supply chain improvement story, and easing in energy prices is due to global geopolitical and economic factors, the stickiness in housing remains an issue that the Federal Reserve (Fed) must address with its rate policy. Therefore, yesterday’s data came to wave goodbye to the 50bp cut hopes at next week’s FOMC meeting. The probability of a 50bp cut melted to 13%, pulling the probability of a 100bp cut this year down with it.

The US yields fell and the US dollar rebounded. Equities first slid on moodiness that the Fed would cut less than projected before the CPI data release then rebounded on optimism that if the Fed cuts less it’s because economy is doing relatively fine. The S&P500 gained 1% and closed the session above its 50-DMA. The Dow Jones and the Russell 2000 gained around 0.30%. Technology stocks led gains leading to a more than 2% jump in Nasdaq 100, but the energy sector remained under pressure despite a rebound in oil prices after Hurricane Francine ran over key oil production zones in the Gulf of Mexico - that produces around 15-17% of the US total production - and where oil producers had to shut around 25% of their operations.

But we know that it will take more than a hurricane or a war in the Middle East to push oil prices sustainably higher in the foreseeable future. The demand concerns are growing, OPEC turns cautious, and Citi goes a step further, stating that 'there’s no room for any more barrels' in the market. They argue that not only should the cartel avoid increasing production, but it must also cut an additional one million barrels per day throughout 2025 to balance the market."

Nvidia’s has another problem

High demand... Nvidia’s CEO Jensen Huang said yesterday that the demand for its advanced chips is ‘so great’ that customers are frustrated if they don’t get their chips fast enough. ‘Everyone wants to be first and everyone wants to be most’ he said – first-world problems. His words gave a boost to Nvidia, and the stock rallied more than 8% yesterday, defying the AI fatigue. VanEck’s semiconductor ETF jumped more than 5%.

EUR/USD tests 1.1000 ahead of ECB decision

The US dollar jumped and extended gains in Asia this morning. The USDJPY rebounded after having tested the 140 waters, Cable flirted with the 1.30 support – as British growth stagnated for the second month in a row, and the EURUSD tested the 1.10 level.

The European Central Bank (ECB) will meet and most likely deliver its second 25bp cut later today. A 25bp cut is fully baked in the market prices, but there is room to act on what comes next. The Eurozone economies have been slowing, Germany is having hard time keeping its head above water, the right-wing parties are surging (even in Germany and France), no one sees the end of the tunnel in the Ukrainian war, and even China is not there to help the European luxury brands afloat.

In this gloomy context, some ECB members will be tempted to cut more than the 50bp baked in the market prices for this year, but some members will remain cautious pointing at the risk of inflation uptick. Therefore, Lagarde’s post-meeting presser will show the direction the euro will take from here. If Lagarde sounds like she and her colleagues remain concerned about the inflation risks, the EURUSD could find support near the 1.10 level and make another attempt on the 1.12 in the coming weeks. But if she shows growing concerns about the gloomy economic outlook, it will be the right time and the right reason for the EURUSD to return below the 1.10 mark. The economic and political setup have the potential to tilt expectations toward a series of three 25bp cuts starting from today. The latter would require a dovish adjustment to ECB expectations and the euro’s valuation.

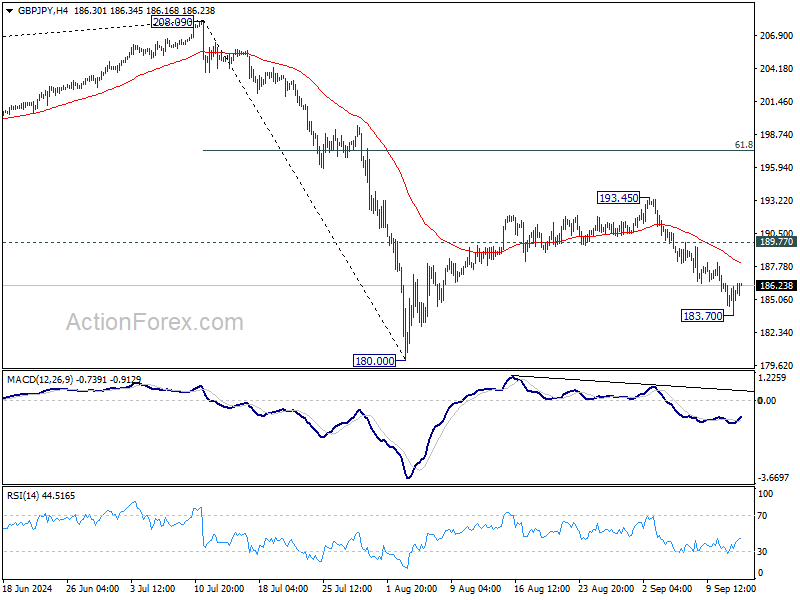

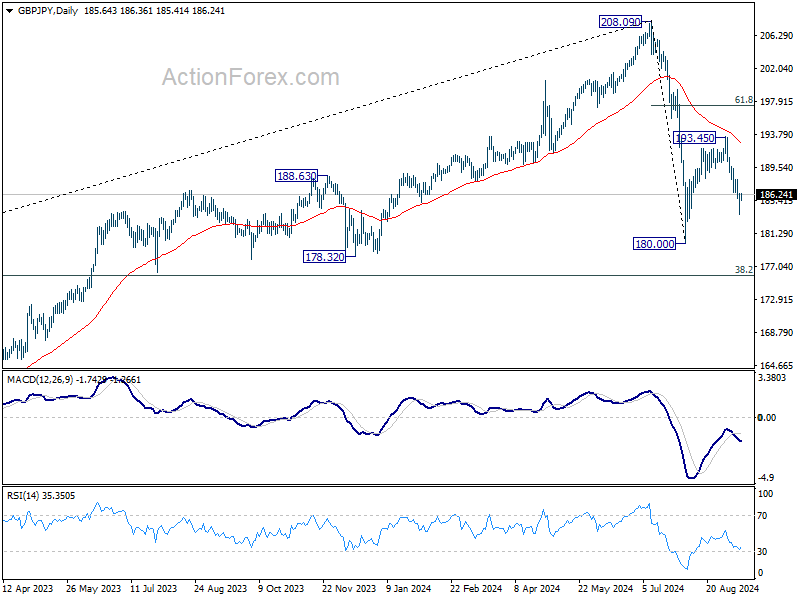

GBP/JPY Daily Outlook

Daily Pivots: (S1) 184.10; (P) 185.29; (R1) 186.86; More...

Intraday bias in GBP/JPY is turned neutral with current recovery.. But further decline is expected as long as 189.77 resistance holds. Below 183.70 will bring retest of 180.00 low. Break there will resume whole fall from 208.09 to 175.94 fibonacci level.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

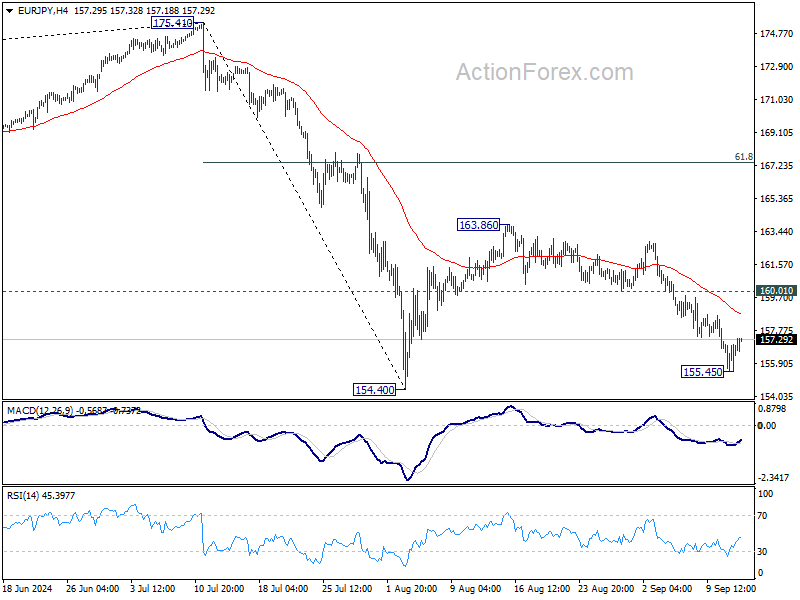

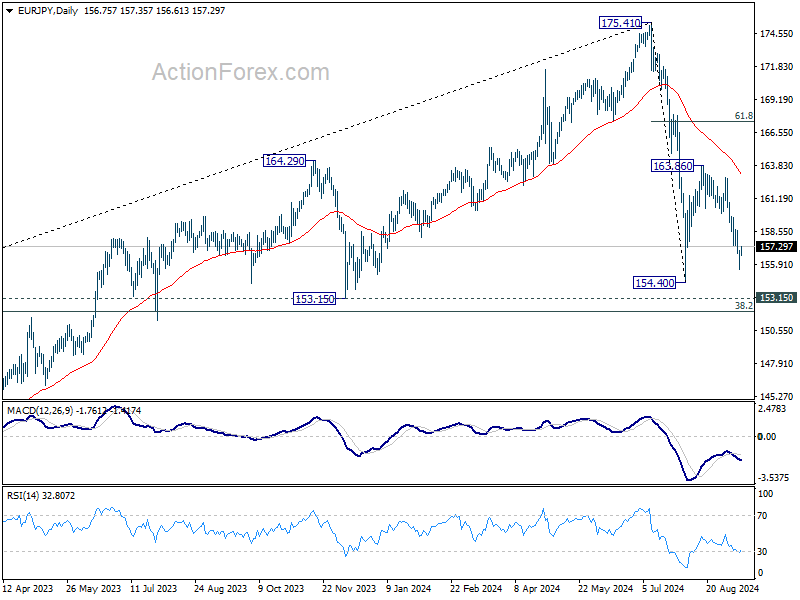

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.78; (P) 156.43; (R1) 157.41; More....

Intraday bias in EUR/JPY is turned neutral again with current recovery. But further decline is expected as long as 160.01 support turned resistance holds. Below 155.45 will bring retest of 154.40 low. Firm break there will resume whole decline from 175.41 to 153.15 support.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

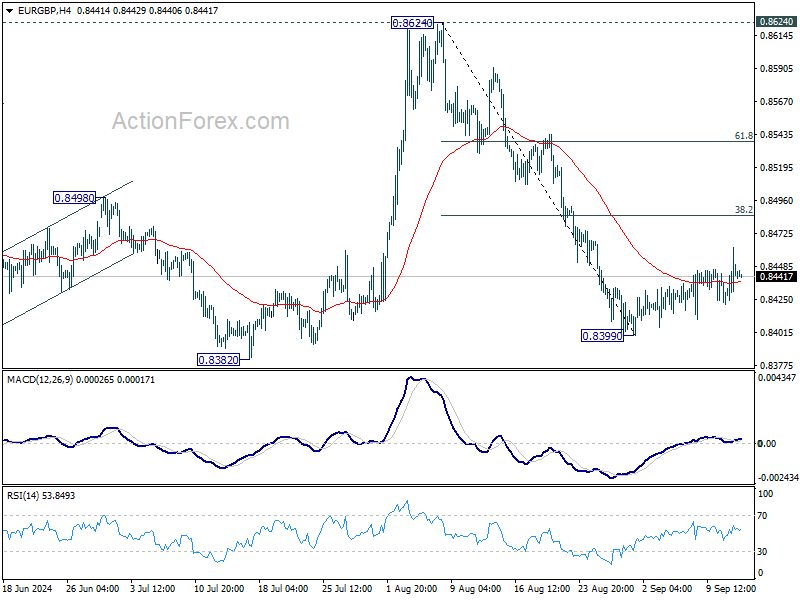

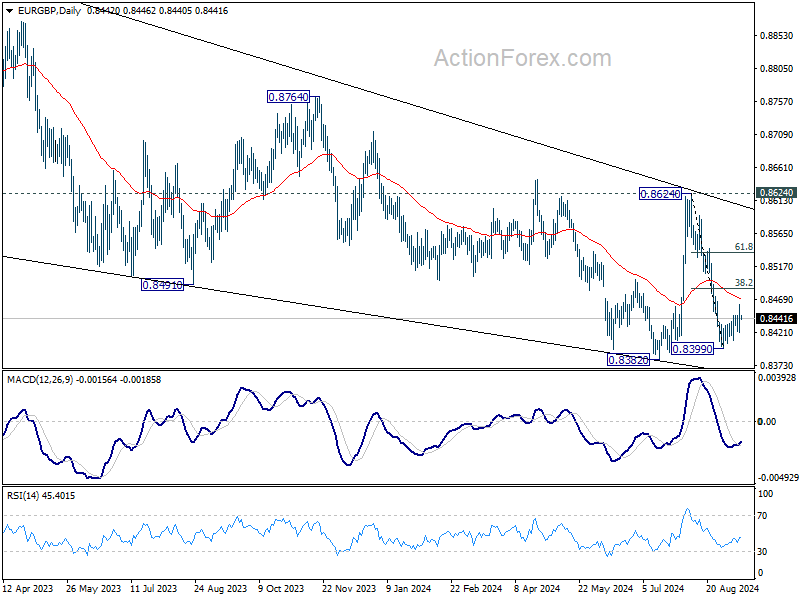

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8421; (P) 0.8443; (R1) 0.8463; More...

Intraday bias in EUR/GBP remains neutral as consolidation from 0.8399 short term bottom is extending. Stronger recovery might be seen but upside should be limited by 38.2% retracement of 0.8624 to 0.8399 at 0.8485. Break of 0.8399 will bring retest of 0.8382 low. Firm break there will resume larger down trend. However, sustained break of 0.8485 will bring stronger rally to 61.8% retracement at 0.8538 and possibly above.

In the bigger picture, as long as 0.8624 resistance holds, down trend from 0.9267 is expected to continue. Firm break of 0.8382 will target 0.8201 (2022 low). However, decisive break of 0.8624 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

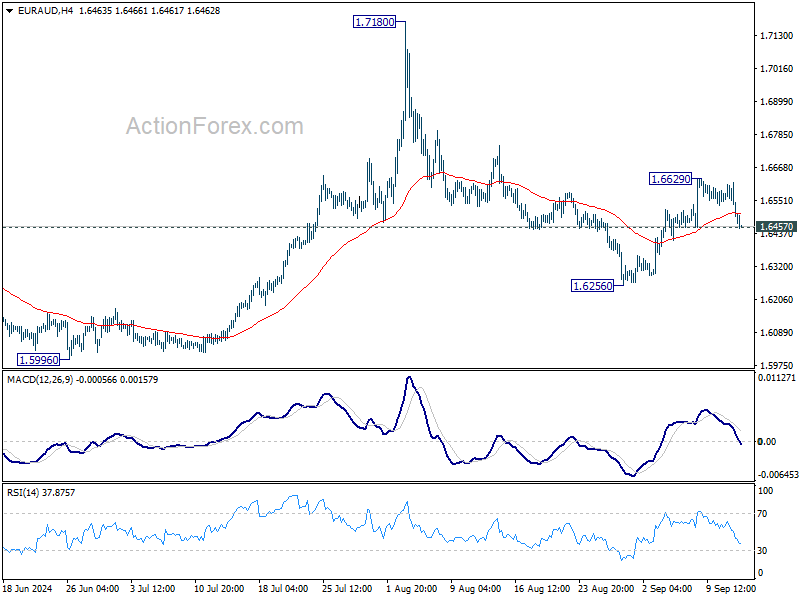

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6459; (P) 1.6539; (R1) 1.6579; More...

Intraday bias in EUR/AUD is turned neutral with current retreat. Rebound from 1.6256 is still in favor to continue as long as 1.6457 support holds. Above 0.6629 will turn bias back to the downside for retesting 1.7180 high. However, firm break of 1.6457 support will suggest that the rebound has completed already, and turn bias back to the downside for 1.6256 again.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

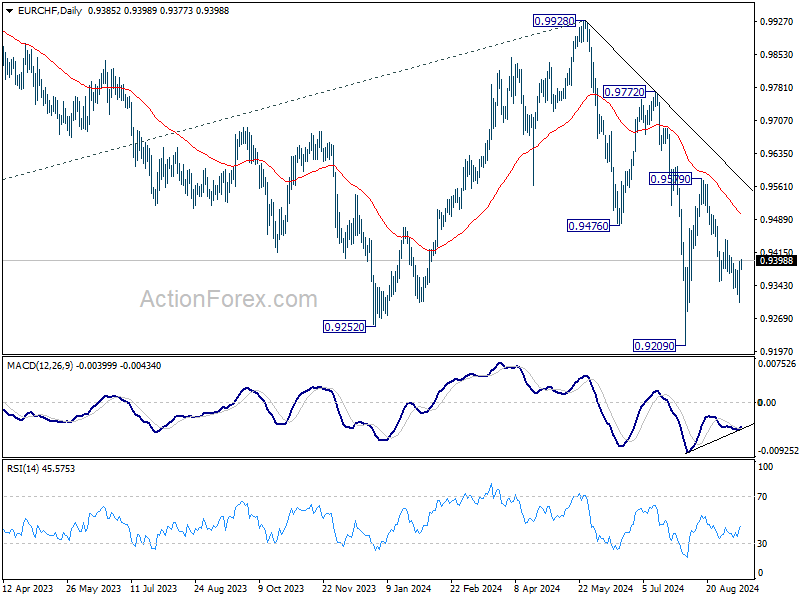

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9329; (P) 0.9363; (R1) 0.9419; More....

A temporary low as formed at 0.9305 in EUR/CHF with current recovery and intraday bias is turned neutral for consolidations. Deeper decline is still expected with 0.9444 resistance intact. Below 0.9305 will resume the fall from 0.9579 to retest 0.9209 low. Nevertheless, firm break of 0.9444 will argue that the pull back from 0.9579 has completed as a correction, and bring further rally back to this resistance.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.