Sample Category Title

U.S. Inflation Print Expected to Tee Up First Fed Interest Rate Cut Since 2020

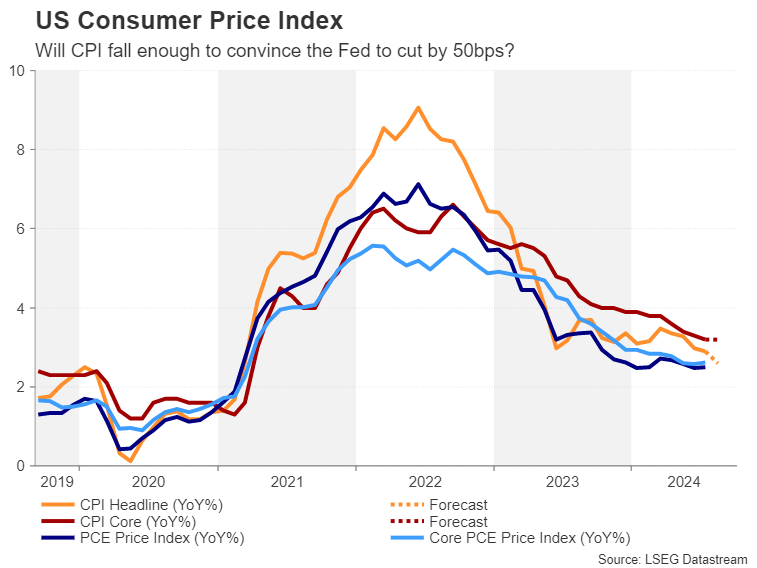

Headline U.S. inflation for August on Wednesday is expected to fall to 2.5% after dipping below 3% in July for the first time since 2021, setting up the U.S. Federal Reserve to cut interest rates for the first time since 2020.

Falling gasoline prices likely accounted for much of that slowing, but we also expect further signs of broader easing in price pressures. We look for core (excluding food & energy) inflation to slow to 3.1% from a year ago after a 3.2% reading in July on a modest 0.1% month-over-month increase. Rising rent prices still account for a disproportionate share of annual consumer price index growth—60% of core price growth over the last two months by our count. But, an earlier slowing in current market rent price growth has begun to filter more significantly into slower shelter CPI readings as leases are renewed. Rents are expected to post slower (though still positive) growth in August.

Excluding shelter, inflation has been hovering near the Fed’s target level through the summer. The share of CPI basket items reporting price growth above 3% has fallen below the pre-pandemic average, at just 25%. A gradual softening in the U.S. economic growth backdrop—with lower job openings flagging softening labour demand and the unemployment rate drifting gradually higher—has also increased confidence that broader inflation pressures will continue to slow. The economy hasn’t crumbled in a way that would push the Fed to panic, but it is increasingly clear that interest rates are higher than they need to be. We look for the Fed to kick off a rate-cutting cycle with a 25 basis point cut to the fed funds target range at the FOMC meeting this month.

Week ahead data watch

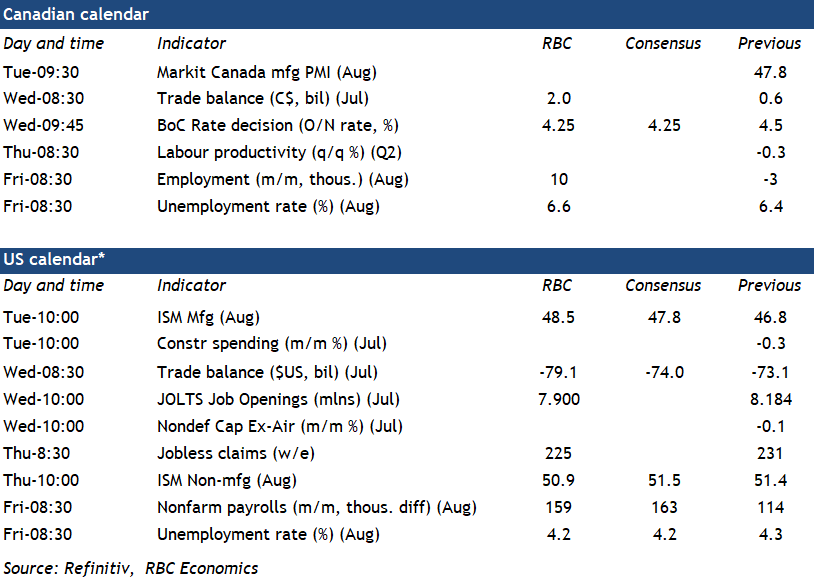

In Canada, second quarter national balance sheet numbers should show the household net worth likely improved as loan growth remained slow, and strong equity markets boosting the value of financial asset holdings.

According to Statistics Canada’s early indicator, core wholesale sales likely fell by 1.1% in July, given lower sales were observed in the motor vehicle and motor vehicle parts and accessories subsector and in the personal and household goods subsector.

Week Ahead – ECB Poised to Cut Again, US CPI to Get Final Say on Size of Fed Cut

- ECB is expected to ease again, but will it be another ‘hawkish cut’?

- US CPI report will be the last inflation update before September FOMC

- UK monthly data flurry begins with employment and GDP numbers

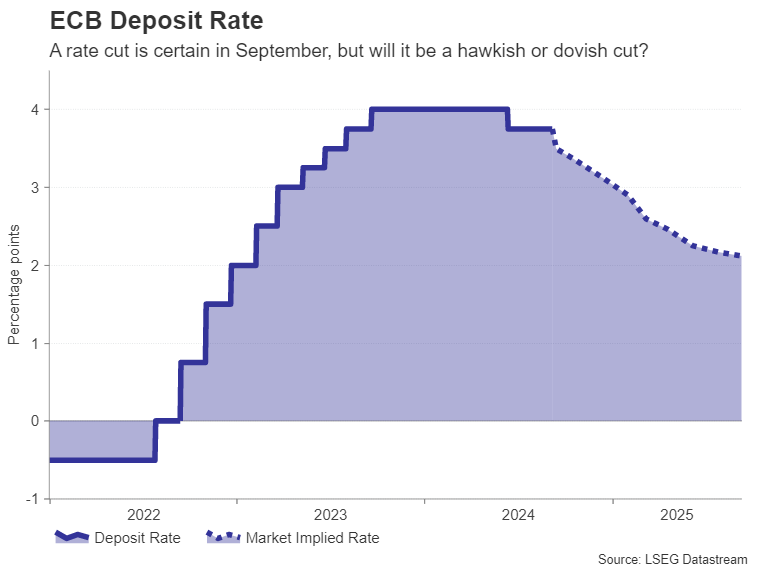

ECB to cut rates for second time

The European Central Bank’s carefully choreographed rate-cutting cycle got off to an awkward start in June after last-minute data upsets. For credibility’s sake, policymakers had only one choice – press ahead with the planned 25-basis-point rate reduction but present it as a ‘hawkish cut’.

Fortunately for the doves and struggling European businesses, the case for further policy easing has strengthened since the last gathering in July when rates were kept on hold. Headline inflation dipped to 2.2% y/y in August and the rebound in euro area growth has been tepid.

The current economic backdrop has potentially set the stage for downward revisions to the ECB’s quarterly inflation and GDP projections, which are due to be published on the day of the meeting on Thursday. More to the point, President Christine Lagarde may now feel that she can tone down the emphasis on “data-dependent and meeting-by-meeting approach” and confidently flag further cuts ahead.

There is one problem, however, and that is the uptick in services CPI in August, which rose to the highest since October 2023, reaching 4.2% y/y. Whilst this isn’t concerning enough to prevent the ECB from sounding more dovish at the September meeting, Lagarde will likely maintain some caution in her press briefing.

If Lagarde signals a rate-cut path that’s shallower than what investors have priced in, the euro could resume its uptrend, having taken a knock from a somewhat firmer US dollar.

Will US CPI back case for 50-bps cut?

Talking of the dollar, it’s been navigating through choppy waters lately amid the ongoing uncertainty about whether the Fed will lower rates by 25 bps at its upcoming meeting or by 50 bps. The Fed’s much awaited policy shift finally came in August at the central banks’ annual symposium in Jackson Hole.

Chair Powell acknowledged the cracks that have started to appear in the labour market and in doing so, he opened the door to a possible 50-bps move in September. Much of the commentary since then hasn’t supported the need for aggressive action as the data has been mostly solid.

The big question is how much will the Fed prioritize its employment mandate over price stability when upside risks to inflation remain? The ISM’s prices paid gauges for both manufacturing and services edged up in August even as employment contracted for the former and barely grew for the latter.

Wednesday’s CPI report will be the last piece of the jigsaw ahead of the September decision and should provide some clarity as to what to expect. The headline CPI rate cooled to 2.9% y/y in July and is expected to fall again to 2.6% in August. The core rate, however, is forecast to have stayed unchanged at 3.2%.

If the above numbers are confirmed, the Fed is more likely to deliver a ‘dovish cut’ of 25 bps. But there would have to be a significant downside surprise for there to be a realistic chance of a 50-bps reduction.

Investors have priced in a close to 40% probability of a 50-bps cut so there is room for disappointment, with the dollar possibly turning higher if the CPI data is more or less in line with expectations or stronger.

Producer prices will follow on Thursday and Friday’s preliminary survey on consumer sentiment in September by the University of Michigan will be important too, particularly the one- and five-year inflation expectations.

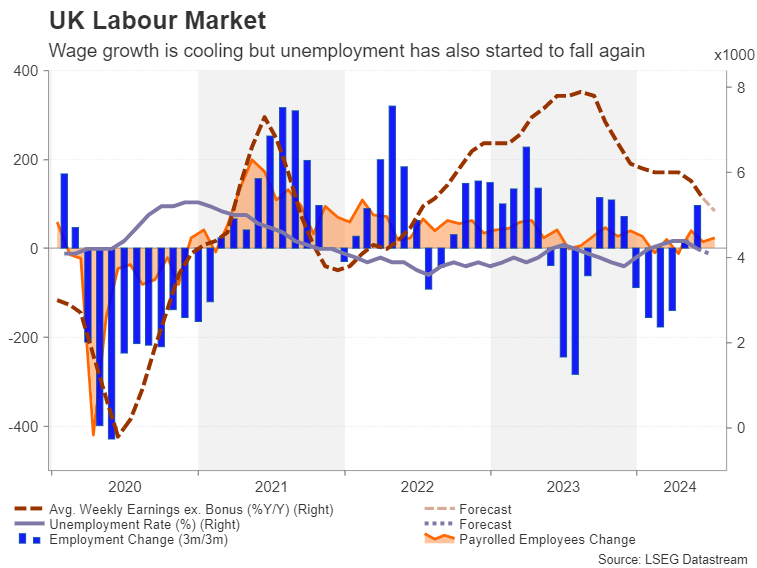

Pound eyes UK releases as BoE decision looms

The Bank of England is expected to buck the central bank trend in September and keep rates on hold when it meets on the 19th. The UK economy bounced back strongly in the first half of 2024 and with wage growth and services inflation still elevated, the BoE can afford to pause after cutting rates for the first time this cycle in August.

But the decision may yet end up being a much closer call than anticipated depending on the incoming slew of data ahead of the September meeting. On Tuesday, the employment report for July will be watched for further signs that the UK’s labour market is stabilising after significant job losses at the start of the year.

The unemployment rate declined 0.2 percentage points to 4.2% in June, but another big drop might not be so welcome as wage growth is finally headed towards levels that would be more consistent with inflation of 2.0%. A pickup in hiring could refuel wage pressures, hindering the BoE’s fight against inflation.

The spotlight on Wednesday will be on the July GDP readings, which include a breakdown of services and manufacturing sectors.

The odds for no change in September currently stand at around 75% so sterling could come under heavy pressure if next week’s releases disappoint and push up the probability of a 25-bps cut closer to 50%.

Spotlight on Asia at start of week

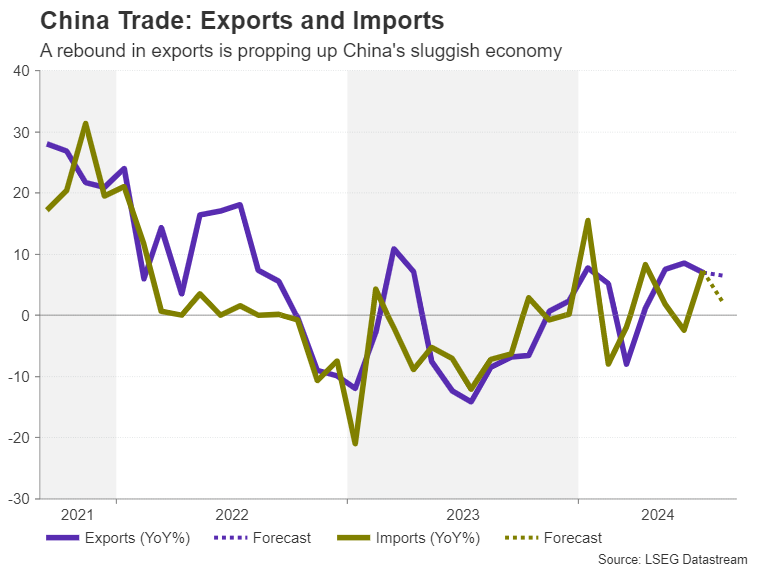

Amid lingering worries about China’s sluggish economy, CPI and PPI numbers on Monday followed by trade figures for August on Tuesday might attract some attention for risk-sensitive currencies such as the Australian dollar. There’s been a decent rebound in exports in recent months. Another strong print in August might provide some boost to risk appetite in the short term but do little in lifting the overall gloom about China’s economic outlook.

In Japan, it will be a busy week for data, the highlight of which will be Monday’s GDP revision. Second quarter GDP growth is expected to be revised higher from the initial estimate of 0.8% y/y. A higher-than-anticipated figure could boost expectations of another rate hike by the Bank of Japan this year, bolstering the yen’s latest rally.

Weekly Focus – Focus on US CPI and ECB meeting

This week, we published our updated macroeconomic projections for the main economies and the Nordics. We expect euro area and US growth rates to converge as the US economy is now losing steam, and the euro area economy is gradually picking up speed. We expect inflation to stabilise close to central bank targets by next year and interest rates to decline significantly, albeit not back to zero. The risk picture has changed, as upside inflation risks are less pronounced while downside growth risks have risen. That said, soft landing remains our base case. Nordic economies are expected to follow the trend and witness accelerating growth towards 2025. Read more on Nordic Outlook - Normalising economies, with risks, 3 September.

As the risk of inflation remaining too high for too long has abated, central banks can afford to front-load rate cuts compared to what we expected before. We have revised our calls both for the Fed and the ECB. We now expect the Fed to conduct 25bp rate cuts at each meeting until summer next year, starting this month. We expect the ECB to cut rates by 25bp both in next week's meeting, and again in December, and follow with three more cuts in 2025. If we are right, policy rate would land at 3.00-3.25% in the US and at 2.50% in the euro area by year-end 2025. Our forecast remains hawkish relative to market pricing, and the risks are tilted towards even lower rates.

The week in financial markets played an already familiar tune as risk appetite was poor on most days and volatility increased, while USD and short-term interest rates declined. Underperformance in the tech sector has been linked to sector rotation and earnings disappointments, but rising stock market volatility is also in line with weaker macro momentum and tighter liquidity in the global financial system, as central banks continue to taper their balance sheets.

Next week's main event will be the ECB meeting on Thursday where a 25bp cut now seems like a done deal. Wage growth in euro area declined significantly in the second quarter to 4.3% y/y from 4.8% y/y in Q1, measured by the ECB's closely watched compensation per employee measure. Hence, despite service inflation remaining high for now, ECB can be more confident that underlying price pressures are abating, and inflation will return to target. But even so, weak productivity and labour force growth suggest that euro area's potential growth remains weak. At roughly similar growth rates, the euro area is more prone to overheating and re-emerging inflationary pressures compared to the US.

Next week's key data point will be the US August CPI due on Wednesday. We forecast headline inflation easing to +0.1% m/m SA (2.5% y/y) but core inflation remaining steady at +0.2% m/m SA (3.2% y/y). On the political front, Kamala Harris and Donald Trump will have their first face-off in a live debate on Tuesday evening US time. Read more about the current outlook from our first US Election Monitor - Latest data shows Harris in a narrow lead, 6 September. Also, in China focus will be on Monday's CPI data. We expect rising headline inflation to 0.7% y/y from 0.5% in July, but core inflation will likely stay lower. China August trade data is released on Tuesday, and it will be interesting to see whether China's exports continue to reflect the persistent weakness in global manufacturing.

August Employment: Size of September Rate Cut Remains Unsettled

Summary

The August employment report indicated that while the jobs market is not unraveling, it continues to clearly weaken. Employers added 142K jobs in August, which was a bit less than expected, but came on the heels of another significant downward revision to prior months' hiring. Over the past three months, employers have added 116K jobs, a notable deceleration from the 207K average pace in the first half of the year. The breadth of hiring improved slightly over the month but continues to be concentrated in less-cyclically sensitive industries.

The unemployment rate ticked down to 4.2% in August from 4.3%, offering some comfort that labor market conditions are not deteriorating in a non-linear way. However, joblessness has continued to rise on trend, with the Sahm Rule indicator, at 0.57, still above the threshold historically associated with recession. The rise in the broader U-6 measure of unemployment, which also captures under-employment, to a new cycle high demonstrates further signs of softening beyond the Employment Situation report's marquee nonfarm payroll numbers.

An especially strong or weak employment report could have crystallized the 25 or 50 bps rate cut debate for the FOMC's upcoming meeting. Instead, today's data have offered something for both the hawks and the doves on the Committee.

We have been projecting a 50 bps rate cut at the September FOMC meeting for the past month, and for now we are leaving that forecast unchanged. That said, neither outcome would surprise us at this point, and we will be listening to the remaining remarks from Fed officials before the black out period and waiting for Wednesday's CPI report for final clues. Regardless of what shakes out in September, we are confident that a series of rate cuts are coming in the months ahead. Any additional labor market cooling would be unwelcome for the FOMC, and as a result shifting the stance of monetary policy from restrictive to neutral over the next year or so remains our base case.

Labor Market Still Cooling, but Expansion Remains Intact

Nonfarm payrolls grew by 142K in August, a bit weaker than the Bloomberg consensus forecast that was looking for a 165K gain and our expectation for a 145K increase. Downward revisions to job growth in the prior two months pushed the three-month moving average for nonfarm payroll growth down to 116K. This marks a notable deceleration from the average monthly job growth of 207K in the first half of the year and 251K in 2023. Furthermore, the hefty 818K downward revision to the level of employment in March implied by the preliminary annual benchmark revision suggests the current pace of hiring could be even lower if the Bureau of Labor Statistics' methodology is continuing to overstate the boost to payrolls generated by new firms.

Job growth in August was a bit more broad-based than it was in July. The labor market diffusion index, a measure of the breadth of hiring across industries where higher numbers imply more broad-based hiring, rose to 53.2 from 47.8 in July, but this remains a fairly narrow hiring base relative to earlier in this expansion and the 2010s cycle (chart). Employment growth continues to be led by hiring in less cyclically-sensitive industries such as health care & social assistance (+44K), leisure and hospitality (+46K) and government (+24K). Construction employment also posted a strong 34K increase in the month, but elsewhere hiring was tepid with just a 8K increase for profession and business services and contractions in manufacturing (-24K), retail trade (-11K) and information (-7K).

The unemployment rate offered further signs of the jobs market continuing to weaken on trend, even if it is not falling apart. As expected, the jobless rate ticked down from 4.3% in July to 4.2% as a jump in unemployment due to temporary layoffs largely, albeit not entirely, reversed. However, even with the downtick, the unemployment rate is still up from 3.8% a year ago. In a similar vein, the Sahm Rule recession indicator, at 0.57, is still above the historical threshold associated with a recession (chart). Under-employment continues to move up as well, with the broader U-6 unemployment measure, which includes people who are working part-time but would like full time work, rising to a new cycle high of 7.9% (chart).

The unemployment rate offered further signs of the jobs market continuing to weaken on trend, even if it is not falling apart. As expected, the jobless rate ticked down from 4.3% in July to 4.2% as a jump in unemployment due to temporary layoffs largely, albeit not entirely, reversed. However, even with the downtick, the unemployment rate is still up from 3.8% a year ago. In a similar vein, the Sahm Rule recession indicator, at 0.57, is still above the historical threshold associated with a recession (chart). Under-employment continues to move up as well, with the broader U-6 unemployment measure, which includes people who are working part-time but would like full time work, rising to a new cycle high of 7.9% (chart).

Average hourly earnings grew a touch more than expected in August, up 0.4% over the month and 3.8% over the past year. Yet despite the uptick, we believe concerns about labor costs keeping inflation uncomfortably high can be put aside for now. The overall loosening in the labor market suggests wage pressures continue to abate, while the somewhat firmer trend in productivity growth this cycle (1.6% since 2019) suggests nominal wage growth does not need to slow much further to be consistent with 2% inflation. Separately released data this week showed the four-quarter average of unit labor costs, which can be thought of as the productivity-adjusted cost of labor, up just 1.2% over the past year (chart).

In our view, today's jobs report further reinforces that the start of the Fed's easing cycle is upon us, and a reduction in the federal funds rate is coming at the September 17-18 FOMC meeting in less than two weeks. The much more difficult question is whether the Committee will agree to a 25 or 50 bps rate cut. This morning's employment data offer something for both the hawks and the doves on the Committee. The tepid pace of nonfarm payroll growth, still-triggered Sahm Rule and a slew of other labor market indicators suggest that the labor market has cooled considerably in recent months. With the federal funds rate well-above most estimates of neutral, the case for moving expeditiously to a more neutral policy stance is not hard to make in our view.

That said, the July employment report sparked fears that the labor market was deteriorating in a non-linear way, and those fears seem to have been mitigated for the time being. Initial jobless claims have edged down in recent weeks, the unemployment rate partially reversed its July-increase, and nonfarm payroll growth remains comfortably in positive territory despite its slower pace. Furthermore, inflation is not all the way back to the central bank's 2% target on a year-over-year basis, and the inflation scars from the past few years will not be quickly forgotten by some members of the FOMC.

We have been projecting a 50 bps rate cut at the September FOMC meeting for the past month, and for now we are leaving that forecast unchanged. That said, neither outcome would surprise us at this point, and based on what we know now it feels like a true coin flip between 25 and 50 bps. As we go to print, financial markets are also assigning toss-up probabilities between the two outcomes. Governor Waller is scheduled to speak on the economic outlook at 11am EST today, and we will be watching his comments closely given his history as a bellwether among the Committee. Another important factor likely will be next week's CPI report, to be released on Wednesday, September 11. Our CPI preview report can be found here.

Regardless of what shakes out in September, we are confident that a series of rate cuts are coming in the months ahead. Any additional labor market cooling would be unwelcome for the FOMC, and as a result shifting the stance of monetary policy from restrictive to neutral over the next year or so remains our base case.

Sunset Market Commentary

Markets

August nonfarm payrolls to settle the debate once and for all… Or not. The US economy added 142k jobs in August, compared to 165k consensus. Most other metrics printed near consensus as well. The unemployment rate ticked lower from 4.3% to 4.2%, the participation rate stabilized at 62.7% and wage growth even accelerated somewhat more than expected (to 0.4% M/M and 3.8% Y/Y). However, as we feared the report needed to be perfect across the board to stop recent market momentum (shifting towards 50 bps rate cuts). And it wasn’t. June and July payrolls faced a combined downward revision of 86k, making the total miss some 109k. It explains why US Treasuries extended their rally after some initial volatility with new cycle lows (in yields) across the curve. The jury remains out though with investors building in some caution ahead of the weekend. The dollar initially suffered from the loss of interest rate support. The trade-weighted greenback came close to testing the December 2023 & August 2024 low at 100.50. USD/JPY similarly aimed at 141.70. EUR/USD set an intraday high at 1.1155 to currently trade back near opening levels at 1.1111. NY Fed Williams said it’s appropriate to start a process of rate cuts. He didn’t comment on the potential size of a first move. By not pushing back against a 50 bps liftoff, we think it’s similar to giving the agreeing nod. A speech by Fed Waller on the economic outlook is still scheduled later today. We hold our view that the Fed could this year opt for three consecutive rate cuts by 50 bps.

Focus turns to Europe next week as the ECB is expected to cut its deposit rate for a second time this year by 25 bps, to 3.50%. As announced in March, they will also reduce the spread between the main refinancing rate and the deposit rate from the current 50 bps to only 15 bps implying an MRR rate cut of 60 bps, from 4.25% to 3.65%. Updated GDP and CPI forecasts will be closely watched for clues on the monetary policy trajectory going forward. However, we don’t expect big changes apart from perhaps some minor downward revisions to this year’s GDP and headline CPI data. Recall that ECB staff in June plotted a 0.9%-1.4%-1.6% growth path for 2024-2026 and a 2.5%-2.2%-1.9% inflation trajectory. While keeping an easing bias, we don’t expect the central bank to pre-commit to specific actions at coming meetings. The short intermeeting period between September 12 and October 17 suggests that bar any big surprise, the central bank might be more inclined to sit the October meeting out and stick with the currently, quarterly, rate-reduction scheme with a next 25 bps move coming only in December. Unlike the Fed, the ECB’s options for making policy less restrictive are smaller given limited room towards neutral territory in the current, stubborn, (core) inflationary environment.

News & Views

The Food and Agricultural Organization’s Food Price Index eased slightly to 120.7 points in August. Decreases in sugar prices, meat and cereals outweighed increases in vegetable oils and dairy products. The y/y index is down 1.1%. Breaking down into its components, the cereal price index fell on dropping wheat exports prices. The vegetable oil index was up 1 point to the highest level since January 2023. Indonesian output remained below full potential, lifting world palm oil prices more than enough to offset lower prices for soy, sunflower and rapeseed oil. Dairy prices (+2.8 points) rose thanks to surging import and tight supplies driving those for milk. Butter quotations reached an all-time high. Falling poultry and pig prices (lacklustre import vs ample export stock) weighed down on the meat price index (-0.9 points). Sugar, finally, fell to the lowest level since October 2022 (-5.7 points) on an improving production outlook for the 2024/2025 season in Thailand and India.

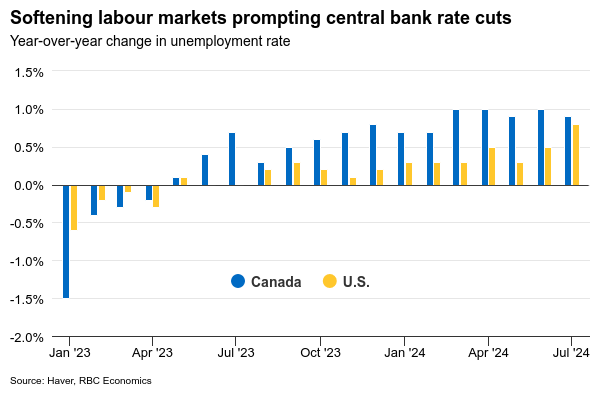

• Canadian payrolls came in at 22.1k in August, the first net job growth in three months’ time. It was, however, slightly less than the 25k hoped-for and came fully on the account of part-time employment (+65.7k vs -43.6k full-time jobs shed). The unemployment rate rose to a higher-than-expected 6.6%, which was the highest since May 2017 barring the 2020-2021 pandemic period. Statistics Canada describes August employment as “little changed”, extending the status quo to four months. Today’s numbers confirm the ongoing cooling of the labour market and vindicate the Bank of Canada which cut rates earlier this week for a third time straight. The 25 bps pace may be upped to 50 bps in October, depending on the economic data. Canadian money markets price in a cumulative 100 bps of cuts over the remaining two meetings of 2024. The fallout for the Canadian Loonie is contained thanks to broad USD weakness. USD/CAD is trading just south of the 1.35 big figure.

Graphs

USD/CAD: Loonie and USD weakness cancel each other out

US 2-yr yield sets minor new cycle low after downward payrolls revisions

Trade-weighted dollar (DXY) comes close to testing Dec23/Aug24 low as payrolls fail to break reigning (50 bps rate cut) momentum

S&P 500: neutral start as key indices try to avoid a further drop

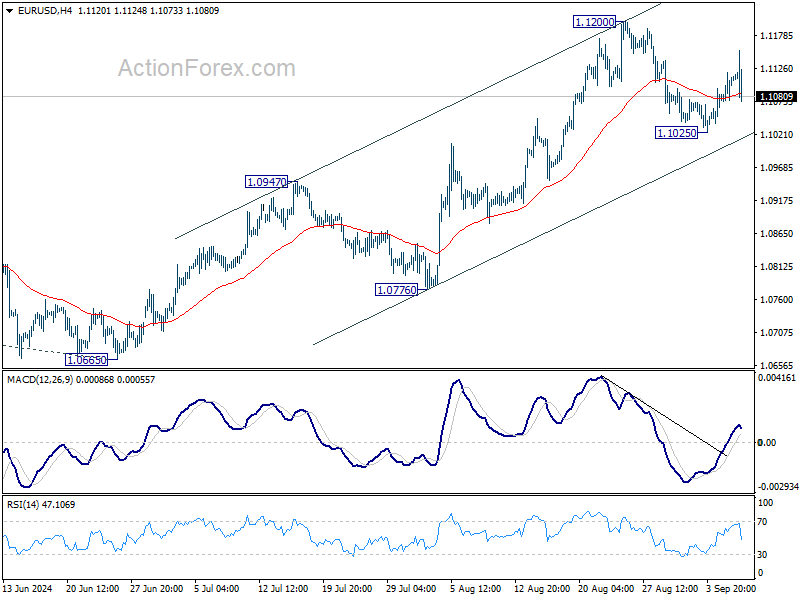

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1084; (P) 1.1102; (R1) 1.1129; More....

Despite edging higher to 1.1153, intraday bias in EUR/USD is turned neutral with subsequent retreat. Corrective pattern from 1.1200 could extend with another leg, and break through 1.1025. But outlook will stay bullish as long as 1.0947 resistance turned support holds. Firm break of 1.1200 will resume larger rally to 1.1274 high.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

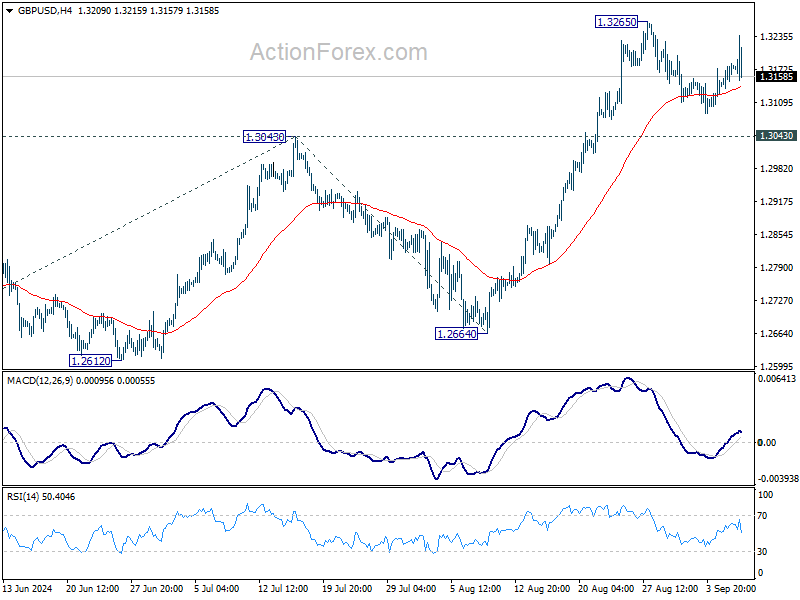

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3150; (P) 1.3168; (R1) 1.3199; More...

Intraday bias in GBP/USD remains neutral as it's still bounded in consolidations below 1.3265. While another retreat cannot be ruled out, downside should be contained above 1.3043 resistance turned support to bring rebound. On the upside, above 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. However, firm break of 1.3043 will indicate short term topping and turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

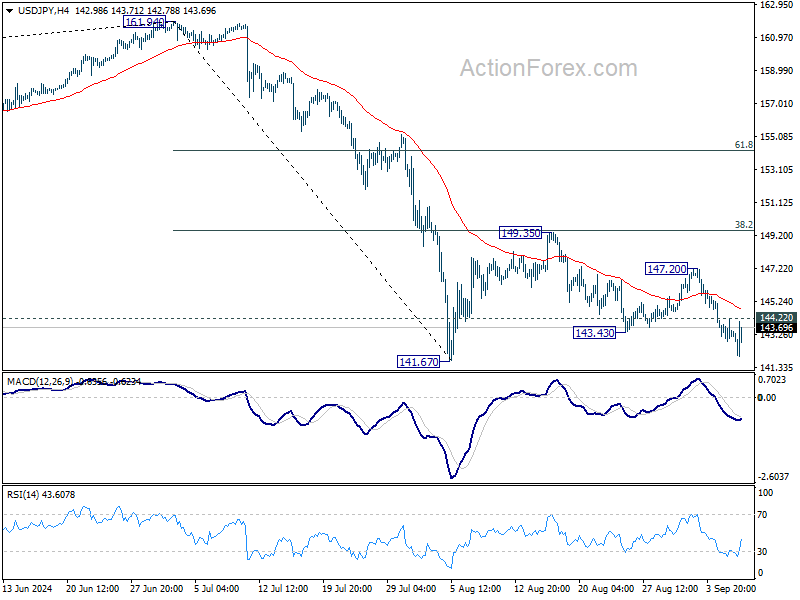

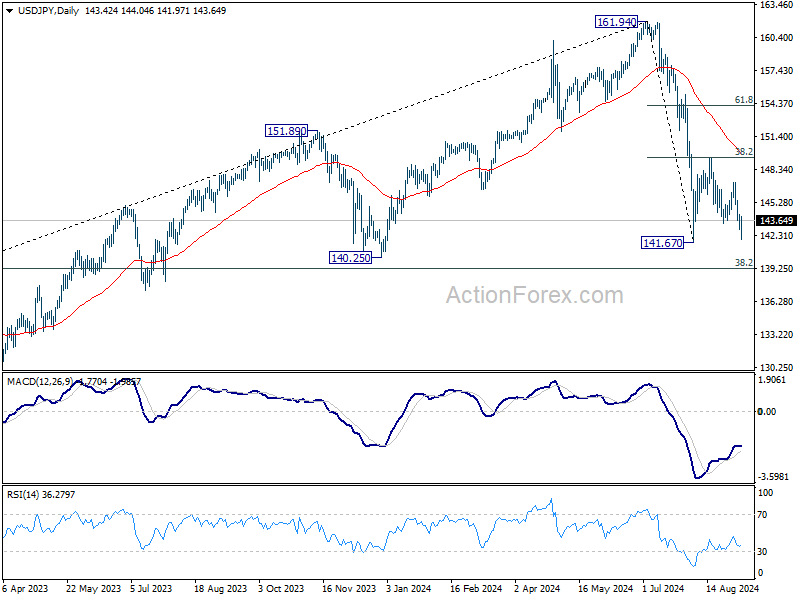

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.79; (P) 143.51; (R1) 144.17; More...

Intraday bias in USD/JPY stays on the downside for the moment. Firm break of 141.67 support will resume whole decline from 161.95 high, for 140.25 support next. On the upside, above 144.22 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 147.20 resistance holds, in case of recovery.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.24) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

US: Hiring Rebounded in August, While the Unemployment Rate Ticked Down to 4.2%

Non-farm employment rose by 142k in August, slightly below the consensus forecast calling for a gain of 165k. Job gains in the two prior months were revised lower by 86k.

- Over the past three months, payroll gains have averaged 116k, in line with recent months but considerably below the 202k averaged over the prior twelve-month period.

Private payrolls rose 118k, with most of the gains concentrated in leisure & hospitality (+46k), health care & social assistance (+44.1k) and construction (+34k). Government hiring chipped in with 24k jobs in August.

In the household survey, a stronger gain in civilian employment (+168k) outstripped a further increase in the labor force (+120k) – pushing the unemployment rate down 0.1 percentage points to 4.2%. The labor force participation rate held steady at 62.7%.

Average hourly earnings (AHE) were up 0.4% month-on-month (m/m) – an acceleration from July's 0.2% gain. On a twelve-month basis, AHE ticked up to 3.8% (from 3.6% in July).

Key Implications

This morning's employment report provided further evidence that the labor market is cooling. Not only did job growth come in below the consensus forecast, but revisions to prior months also showed a weaker pace of job creation. That said, it wasn't all bad news. The unemployment rate partly reversed some of July's uptick – thanks to a sharp reversal in temporary layoffs following a spike in July – while aggregate weekly hours rose by a healthy 0.3% m/m, or the largest monthly gain since March.

Fed officials have been clear in recent communication: rate cuts are imminent. However, market participants are still wrestling with whether the FOMC will cut by 25 or 50 basis points at its next meeting in less than two-weeks. Clearly the labor market has cooled over the past year, but we feel there isn't enough evidence to suggest that the recent softening is the start of a more serious deterioration in underlying fundamentals. Absent a change to this view, we expect three quarter-point rate cuts from the Fed by year-end.

Canada’s Labour Market Continued to Cool in August

Canada's labour market added a modest net 22k new positions, roughly on expectations. However, all the gains were in part-time job positions, which rebounded 66k after losses in July. Full-time positions gave back 44k.

Growth in the labour force outpaced job gains, pushing the unemployment rate up two tenths to 6.6%, slightly higher than expected. Once again, strong population (+96k) and labour force (+82.5k) growth swamped the more modest growth in employment.

Looking across sectors, job gains were concentrated in education services (+1.7% month-on-month (m/m), 25K), health care and social assistance (+0.9% m/m, 25k) and finance, insurance and real estate (+0.8%m/m, +11k).

The unemployment rate has now risen 1.5 percentage points (p.p.) since April 2023, but over the past year it has risen the most for youth (+3.2 p.p. to 14.5%). And job market prospects did not improve much for students in August either, with their unemployment rate rising to 16.7%, versus 12.9% last summer and the highest since 2012.

Lastly, total hours worked declined slightly in August (-0.1% m/m), leaving them up 1.4% over the past year. Wage growth cooled modestly to 5.0% year-on-year in August.

Key Implications

August's jobs report managed a gain in jobs, but apart from that the story continues a be further cooling in Canada's labour market. In Wednesday's Bank of Canada's interest rate announcement, Governor Macklem characterized Canada's economy as having "enough slack". This continued weakening in the job market suggests slack continues to build in the labour market, pointing to the need for further interest rate cuts.

The labour market is giving the OK for the Bank of Canada to continue its gradual quarter-point cut per rate announcement pace. We expect the Bank to cut interest rates in two more quarter point moves in October and December this year (see rates forecasts).