Sample Category Title

‘Iran Deal’ Headlines Replaced by ‘US Had Struck Military Targets in Iran’

What a week it has been – and it is not over! It started with renewed Middle East tensions, sending oil prices up to $115pb, then tensions eased and markets breathed a sigh of relief thanks to the US’ unwillingness to escalate, while euphoria kicked in on news that even a peace proposal had come to the table.

Meanwhile, the week’s most closely monitored earnings went extremely well. Chip stocks rallied on better-than-expected results from Samsung and AMD, while the Nasdaq renewed record after record. The good mood got a further sugar coating from falling sovereign yields, as declining oil prices also pulled inflation expectations lower and softened central banks’ policy outlooks.

All of a sudden, the potential ‘Iran deal’ headlines are replaced by news that the US had ‘struck military targets in Iran after the country fired on three Navy destroyers sailing in the Strait of Hormuz’, suggesting that we’re back to square one. US crude rebounded past the $98pb level and is consolidating just below the $97pb mark, while Brent is settling above $101pb at the time of writing.

We have no idea how the situation will evolve, but the track record of the past two months is not really encouraging, and the Friday close is always a critical moment as the US tends to make decisive moves during no-market hours to give investors time to digest the information, hoping to push volatility into Monday and eventually drown out bad news with encouraging — often unfounded — announcements.

It has admittedly worked well so far… Since the start of the war, the S&P 500 has hit fresh record highs nine times, if my count is right. US futures are in positive territory this morning, European appetite is somewhat less.

On the earnings front, Whirlpool warned that record-low sentiment — due to the Iranian war and the doubling of gasoline prices — has plunged demand for appliances to a level the company says could lead to a ‘recession-level industry decline’. The stock plunged 12%, while the tech-heavy S&P 500 was busy flirting with fresh ATHs. Oh well...

Anyway, we have one more thing to watch before this week’s closing bell, and that’s the US jobs report. The US economy has been in a phase of low hiring and low firing, with the latest jobs data suggesting that the slowdown is not as bad as feared. Earlier this week, the ADP report printed lower-than-expected job additions of 109K, but the number did not sound alarming — and the data certainly got diluted amid more exciting war and tech earnings headlines.

Headlines remain dominated by geopolitical tensions, but today’s official jobs data still deserves attention. The median forecast in the latest Bloomberg survey points to 65K new nonfarm job additions in the US last month, with average wage growth rebounding from 3.5% to 3.8% y-o-y.

As I repeated several times earlier this week, estimates diverge remarkably. Some expect the US jobs market to have added a significantly lower number of jobs compared to the median forecast, pointing to thousands of job cuts from Big Tech names due to AI replacement and the ongoing immigration struggle, while others predict that massive AI spending is creating jobs and should at least limit the AI-related slowdown. We will see where the data lands today.

As for the market reaction, I would expect a stronger-than-expected set of figures to keep Federal Reserve (Fed) hawks in charge, without necessarily taming equity appetite — the latter will likely depend on war headlines.

A softer-than-expected set of jobs figures, on the other hand, could revive dovish Fed expectations and provide further support to equity valuations, provided that war headlines leave some room for reaction and wage growth remains reasonable. By reasonable, I mean a figure in line with — or ideally softer than — the 3.8% yearly expectation, while uncertainty about oil prices remains very, very high.

And this last part is important, because some Fed members are growing more concerned about the inflation outlook than the health of the jobs market — a notable shift compared to the pre-war narrative, mind you. That change — from worrying about a softening labour market to worrying about overheating price pressures — puts inflation/wages figures front and centre, while making the headline NFP somewhat secondary when it comes to guessing the Fed’s next move. The best outcome for the market would be relatively strong job additions paired with relatively softer wage growth.

Speaking of good data, here’s something that made me smile. Bank of England (BoE) officials are apparently worried that the UK’s economic data looks too good to be true — and, more importantly, that it may be sending a misleading signal to markets, making the job of setting monetary policy even trickier than it already is amid Middle East jitters. In fact, first-quarter growth has consistently come in strong since 2022, only to fade later in the year. It probably has to do with consumer behaviour and post-Covid spending habits — or so it is said — and the fact that the ONS has not found a way to smooth out the numbers enough for seasonally adjusted figures to be fully consistent. If that pattern repeats again, the BoE could end up tightening policy more than necessary in its fight against inflation, and into a more rapidly deteriorating UK economic outlook than early-year data suggests.

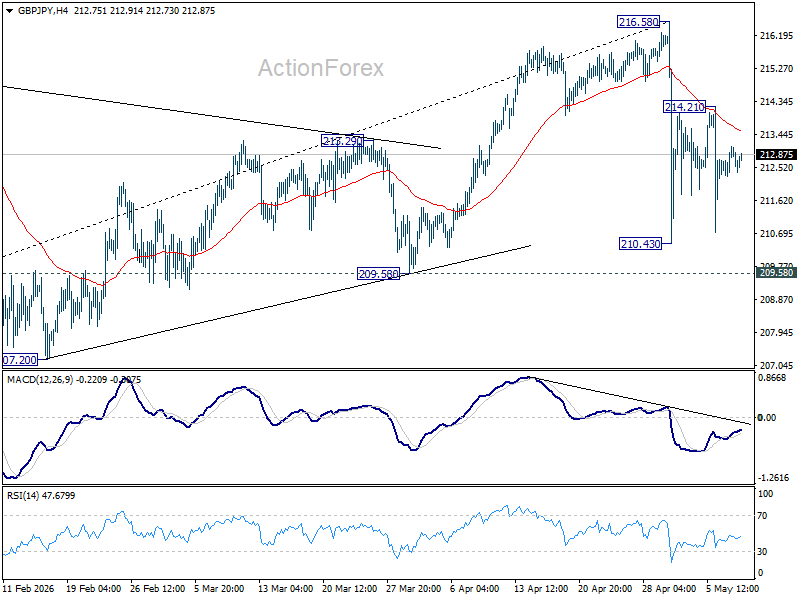

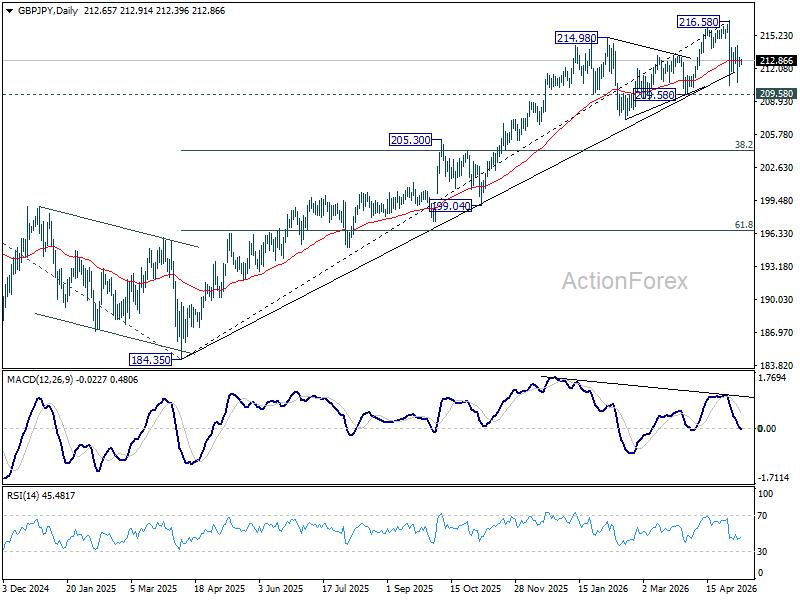

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.27; (P) 212.70; (R1) 213.11; More...

Intraday bias in GBP/JPY remains neutral and outlook is unchanged. Further decline is expected as long as 214.21 holds. Below 210.43 will target 209.58 support first. Break will target 38.2% retracement of 184.35 to 216.58 at 204.28. However, firm break of 214.21 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.45) will argue that it's already in medium term down trend for 184.35 support.

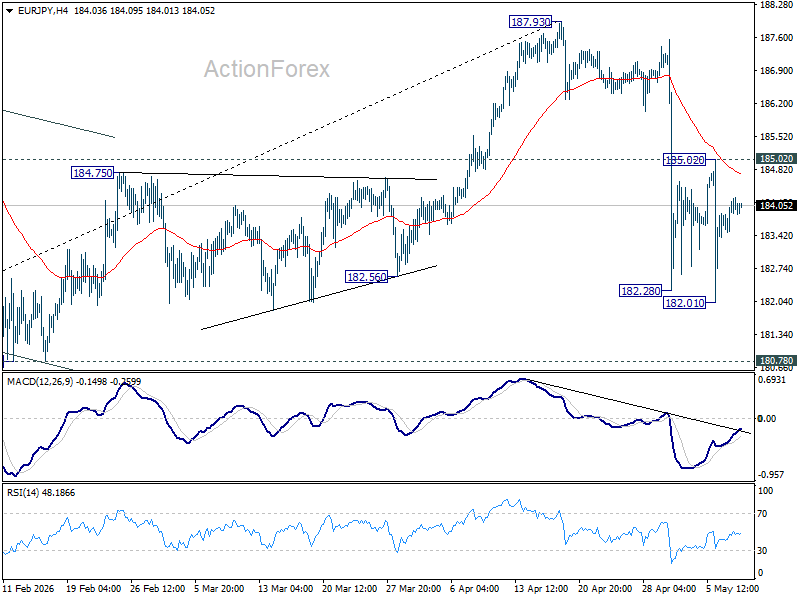

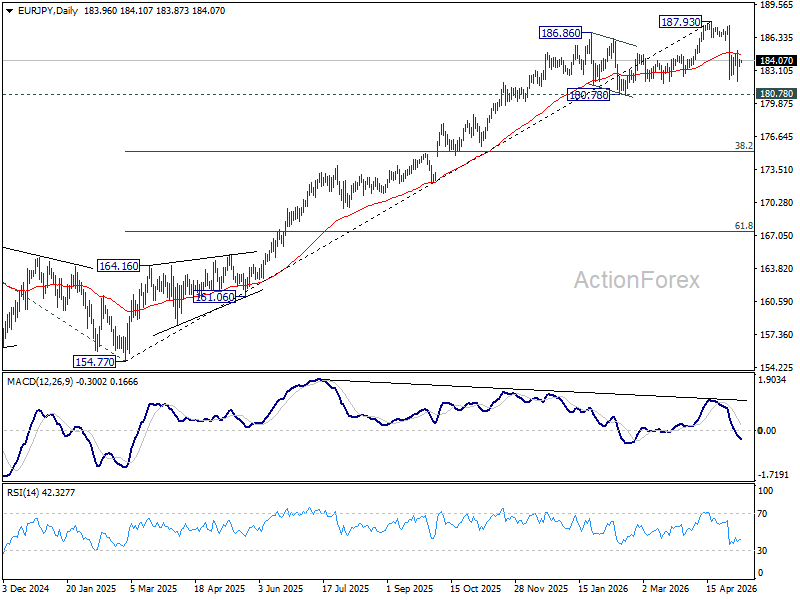

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.58; (P) 183.92; (R1) 184.33; More...

Intraday bias in EUR/JPY remains neutral for the moment. Risk will stay on the downside as long as 185.02 resistance holds. Break of 182.01 will resume the fall from 187.93 to 180.78 support next. However, firm break of 185.02 will turn bias back to the upside for stronger rebound.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 177.76) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

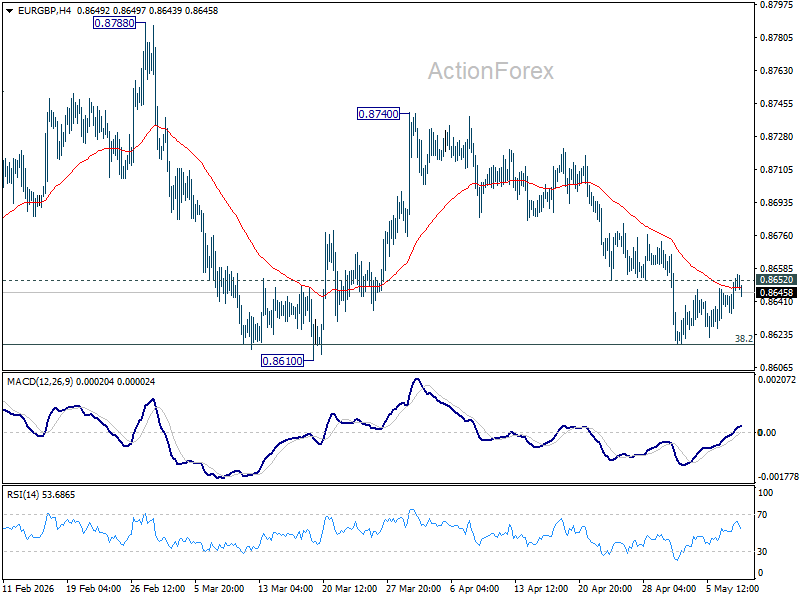

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8642; (P) 0.8649; (R1) 0.8662; More…

Intraday bias in EUR/GBP stays neutral first. On the upside, firm break of 0.852 resistance should confirm short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.8675) and above. On the downside, decisive break of 0.8610 key support carry larger bearish implications and pave the way to 0.8466 fibonacci level next.

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Sustained break there will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least. For now, risk will stay mildly on the downside as long as 55 D EMA (now at 0.8680) holds, in case of recovery.

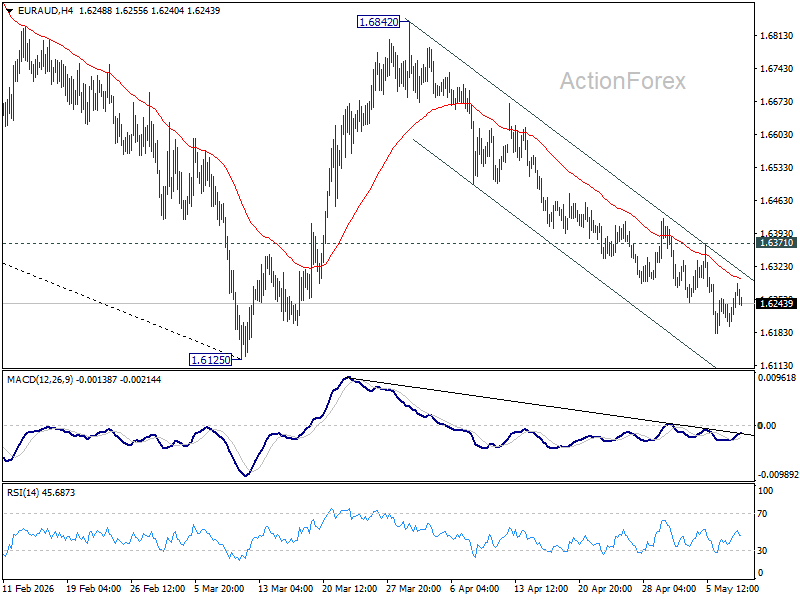

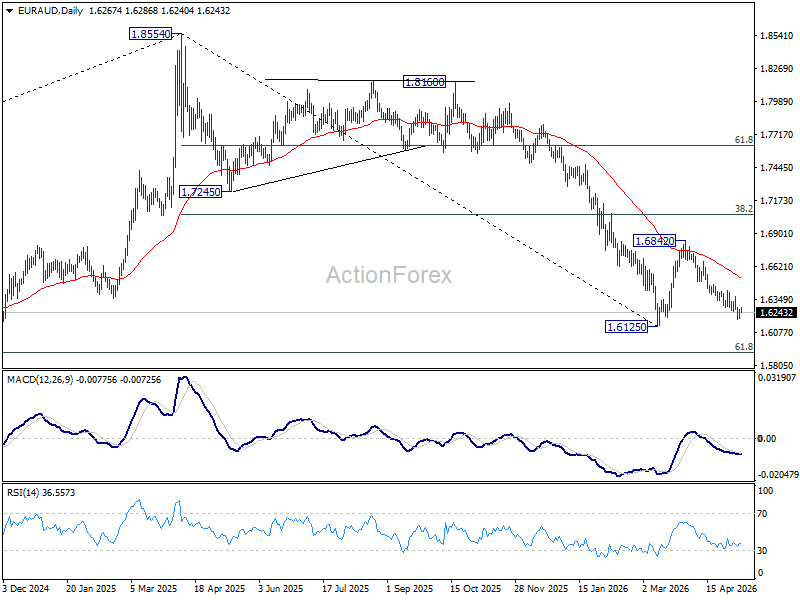

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6216; (P) 1.6248; (R1) 1.6298; More...

Further decline is expected in EUR/AUD with 1.6371 resistance intact. Decisive break of 1.6125 low will confirm resumption of whole down trend from 1.8554. However, firm break of 1.6371 will indicate short term bottoming and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7069) holds, even in case of strong rebound.

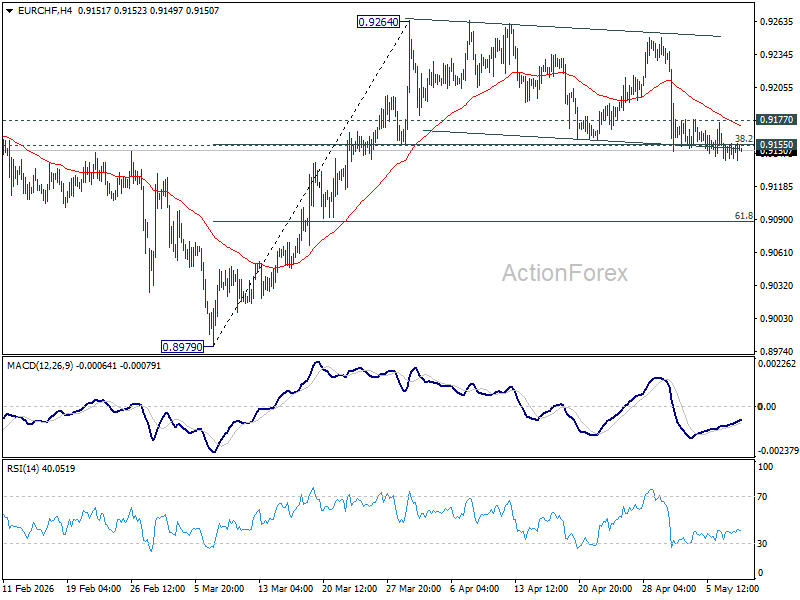

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9142; (P) 0.9151; (R1) 0.9161; More....

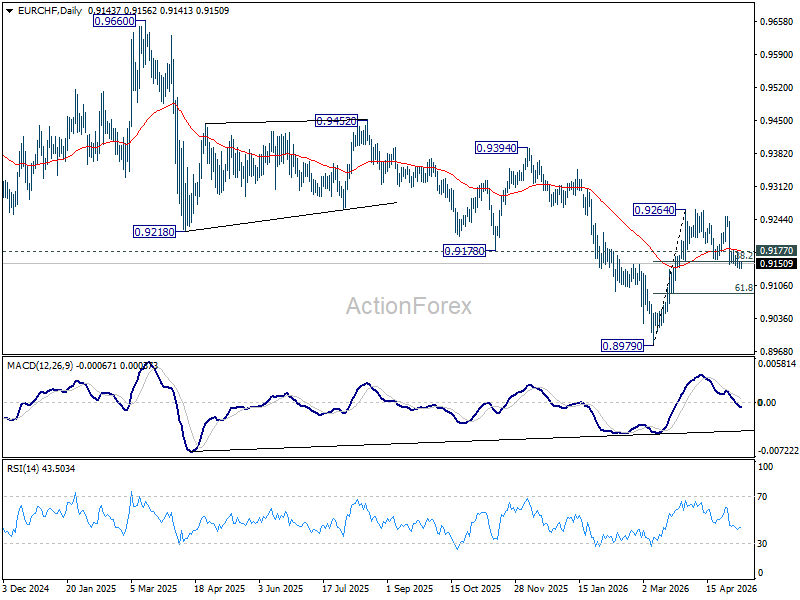

EUR/CHF is still defending 0.9155 cluster support (38.2% retracement of 0.8979 to 0.9264 at 0.9155) support. Intraday bias stays neutral for the moment. On the upside, above 0.9177 minor resistance will bring stronger rebound back to 0.9264 resistance. However, sustained trading below 0.9155 will turn bias back to the downside for deeper pullback to 61.8% retracement at 0.9088 and possibly below.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9268) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

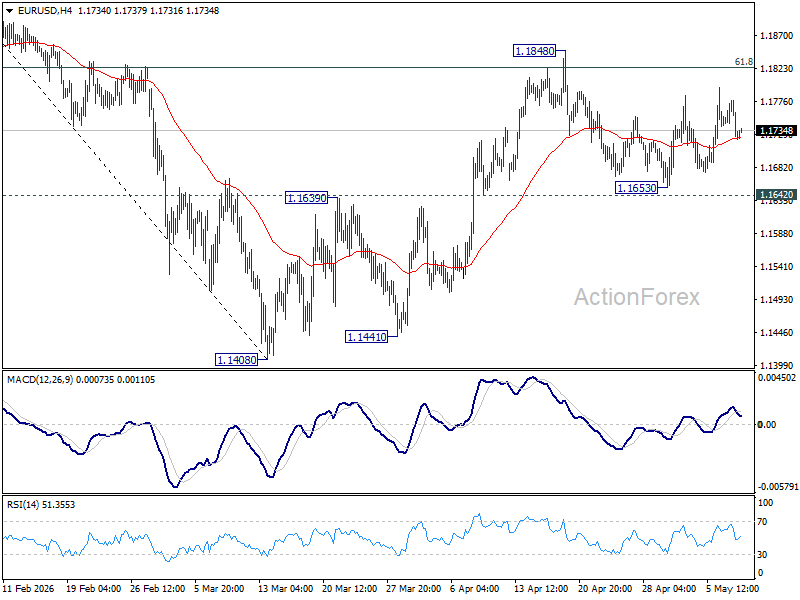

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1705; (P) 1.1743; (R1) 1.1762; More….

Intraday bias in EUR/USD remains neutral as sideway trading continues. With 1.1642 support intact, rise from 1.1408 is expected to continue. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

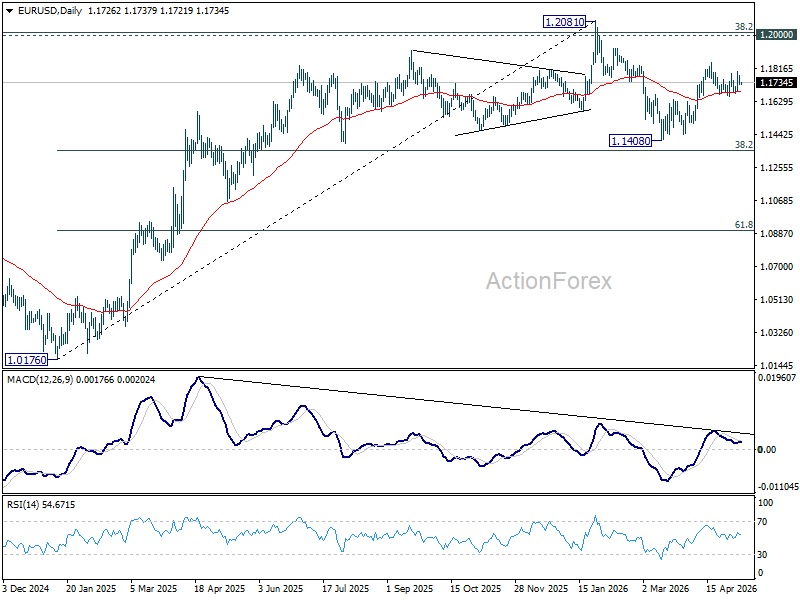

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

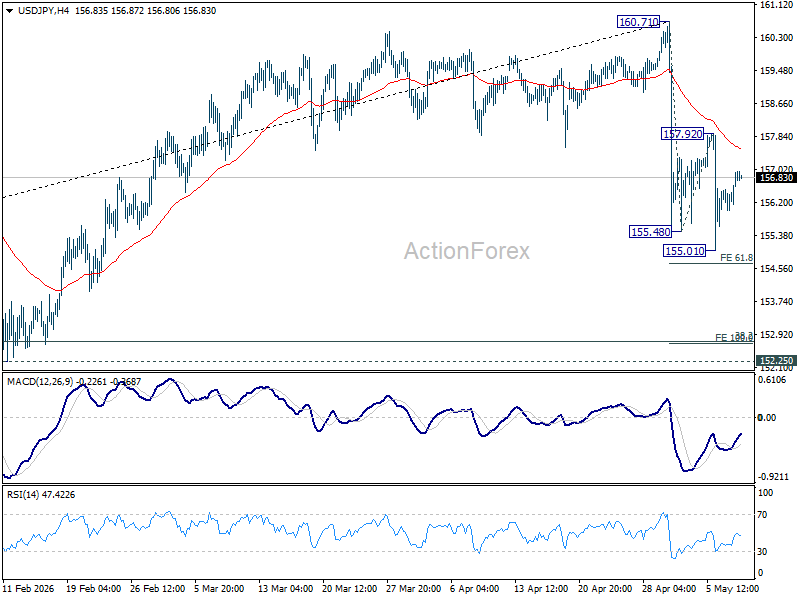

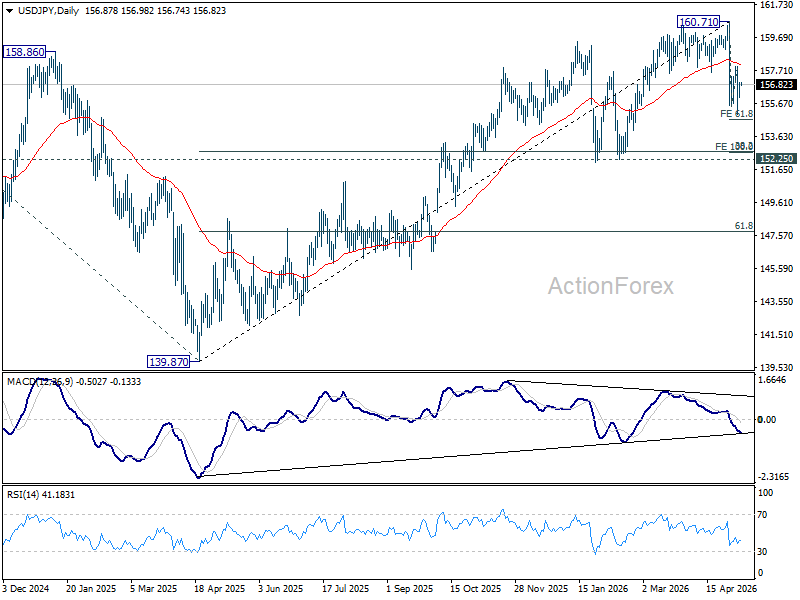

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.32; (P) 156.64; (R1) 157.26; More...

Intraday bias in USD/JPY remains neutral first, and risk will stay on the downside as long as 157.92 resistance holds. Below 155.01 will resume the fall from 160.71 to 61.8% projection of 160.71 to 155.48 from 157.92 at 154.68. Firm break there will target 100% projection at 152.69. That would be close to key 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). However, firm break of 157.92 will turn bias back to the upside for stronger rebound.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.01) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

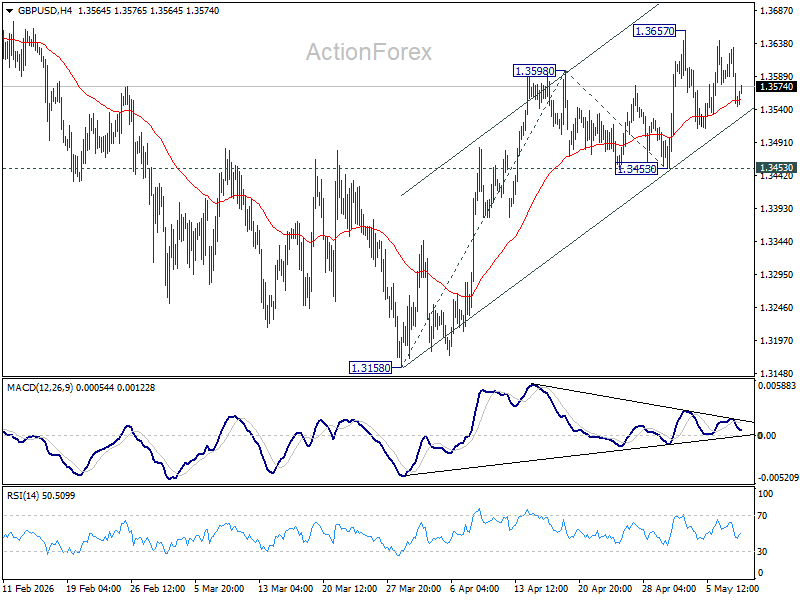

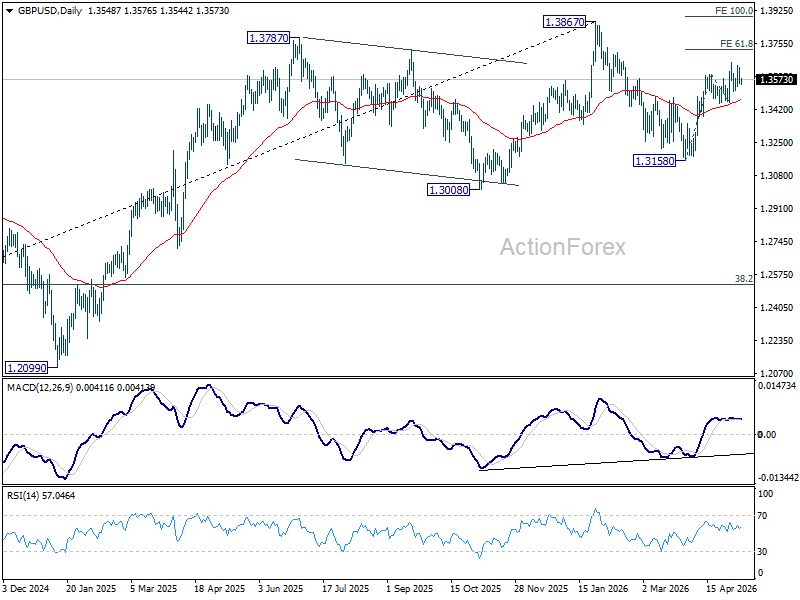

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3522; (P) 1.3577; (R1) 1.3607; More...

Intraday bias in GBP/USD stays neutral at this point, as sideway trading continues. Further rise is expected with 1.3453 support intact. On the upside, above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

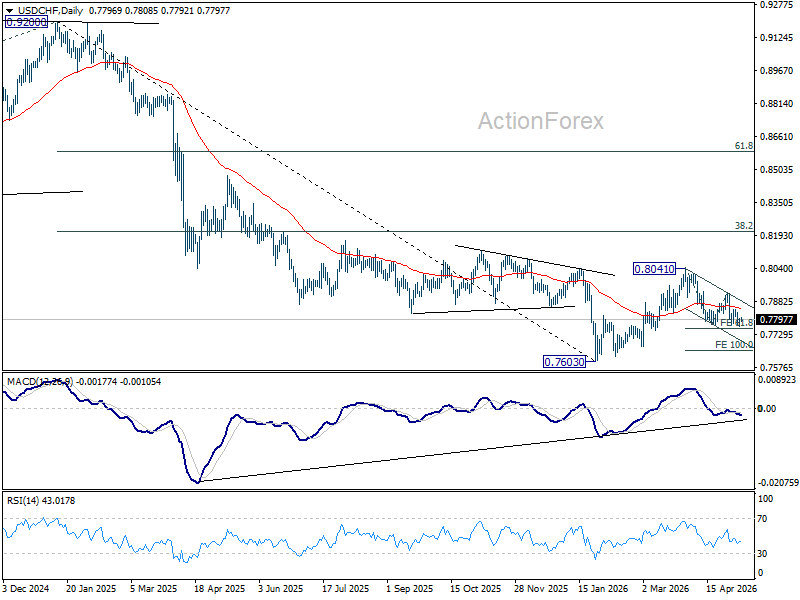

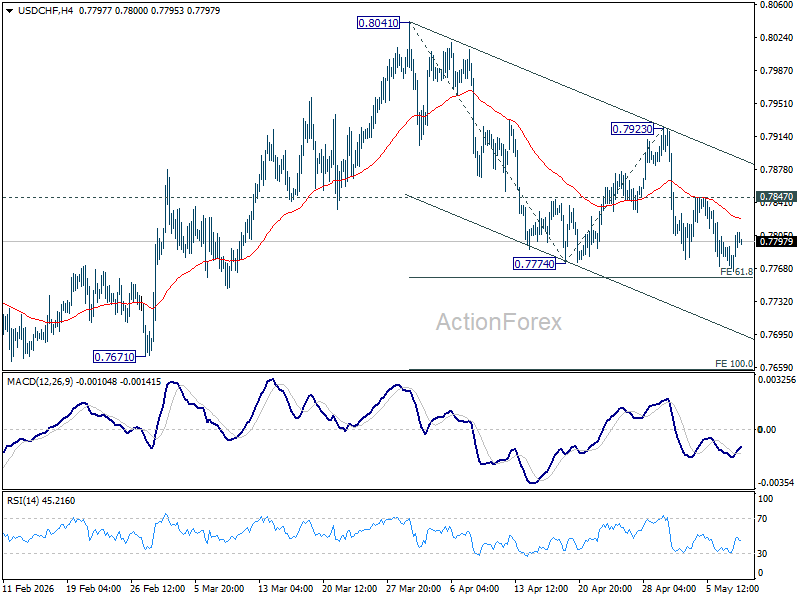

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7778; (P) 0.7793; (R1) 0.7822; More….

Intraday bias in USD/CHF remains mildly on the downside for 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758. Firm break there will extend the fall from 0.8041 to 100% projection at 0.7656. On the upside, above 0.7847 minor resistance will turn bias neutral again.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).