Sample Category Title

BTCUSD Retreats from 1-Month High

- BTCUSD pulls back after touching the 70,000 mark

- The bears eye the 50-day SMA as next crucial target

- Momentum indicators are skewed to the downside

BTCUSD (Bitcoin) had a very strong July, with the price reaching the 70,000 psychological mark for the first time in more than a month. Since then, it has been experiencing a downside correction, which is on track to test the 50-day simple moving average (SMA).

Should selling pressures persist, the price may face 63,400, a region that acted both as support and resistance in recent months and overlaps with the 50-day SMA. Further declines could then cease around the May support of 60,150. Sliding beneath that floor, Bitcoin may challenge the April bottom of 56,483.

On the flipside, if the bulls attempt to erase the latest setback, the April resistance of 67,270 could curb initial advances. Piercing though that zone, the price could revisit its recent one-month peak of 70,015. A violation of that territory could pave the way for the May-June double top region of 71,955.

In brief, BTCUSD has come under selling pressure in the past few sessions after its rally reached overbought conditions. Moving forward, the outcome of a test of the 50-day SMA could decide Bitcoin’s next move.

BoE cuts Bank Rate by 25bps to 5.00% in 5-4 tight vote

BoE cut the Bank Rate by 25 bps to 5.00% today, in a closely contested 5-4 vote. Governor Andrew Bailey, Deputy Sarah Breeden, new Deputy Clare Lombardelli, known dove Swati Dhingra, and Dave Ramsden voted in favor of the cut. Chief Economist Huw Pill, Megan Greene, Jonathan Haskel, and Catherine Mann voted against the change.

In the accompanying statement, BoE stated it is now "appropriate to reduce slightly the degree of policy restrictiveness." The central bank noted that the impact of past external shocks "has abated" and there has been "some progress" in moderating inflation risks.

Despite the cut, BoE emphasized that restrictive policy will continue to weigh on economic activity, leading to a looser labor market and reducing inflationary pressures.

(BOE) Bank Rate reduced to 5%

Monetary Policy Summary, August 2024

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 31 July 2024, the MPC voted by a majority of 5–4 to reduce Bank Rate by 0.25 percentage points, to 5%. Four members preferred to maintain Bank Rate at 5.25%.

The Committee has published an updated set of projections for activity and inflation in the accompanying August Monetary Policy Report.

Twelve-month CPI inflation was at the MPC's 2% target in both May and June. CPI inflation is expected to increase to around 2¾% in the second half of this year, as declines in energy prices last year fall out of the annual comparison, revealing more clearly the prevailing persistence of domestic inflationary pressures. Private sector regular average weekly earnings growth has fallen to 5.6% in the three months to May, and services consumer price inflation has declined to 5.7% in June. GDP has picked up quite sharply so far this year, but underlying momentum appears weaker.

The Committee's framework for assessing the medium-term outlook for inflation distinguishes between first and second-round effects. The MPC has been focused on second-round effects that capture more persistent inflationary pressures. The Committee continues to monitor the accumulation of evidence from a broad range of indicators.

The Committee expects the fall in headline inflation, and normalisation in many indicators of inflation expectations, to continue to feed through to weaker pay and price-setting dynamics. A margin of slack should emerge in the economy as GDP falls below potential and the labour market eases further. Domestic inflationary persistence is expected to fade away over the next few years, owing to the restrictive stance of monetary policy.

However, there is a risk that inflationary pressures from second-round effects will prove more enduring in the medium term. A stronger-than-expected path for demand, and structural factors such as a higher equilibrium rate of unemployment, could affect domestic wage and price-setting more persistently. Furthermore, the degree of restrictiveness of monetary policy could be less than embodied in the Committee's current assessment.

In balancing these considerations, at this meeting, the Committee voted to reduce Bank Rate to 5%. It is now appropriate to reduce slightly the degree of policy restrictiveness. The impact from past external shocks has abated and there has been some progress in moderating risks of persistence in inflation. Although GDP has been stronger than expected, the restrictive stance of monetary policy continues to weigh on activity in the real economy, leading to a looser labour market and bearing down on inflationary pressures.

Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The Committee continues to monitor closely the risks of inflation persistence and will decide the appropriate degree of monetary policy restrictiveness at each meeting.

Minutes of the Monetary Policy Committee meeting ending on 31 July 2024

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying August 2024 Monetary Policy Report.

2: Global activity was projected to have expanded steadily over recent quarters. US GDP had grown by 0.7% in 2024 Q2, somewhat stronger than had been expected. Euro-area GDP had grown by 0.3% in Q2, in line with expectations. Recent outturns for consumer price inflation in the United States and the euro area suggested some further normalisation toward central banks' targets.

3: The Committee discussed developments in internationally traded goods prices, noting the presence of a range of risks that could be material for the UK inflation outlook. Although Chinese export prices had recently been higher than expected, they could pose a downside risk if past weakness were to re-emerge. That said, the effects on UK inflation would only be significant if competitive effects also generated spillovers to the price inflation of traded goods exported by other countries. Set against that, there were upside risks to goods prices from the risk of greater trade fragmentation and increased trade restrictions. A broadening of recent disruption to shipping routes could affect the supply of goods whose production was concentrated in particular regions. Upside risks to commodity prices from geopolitical developments, including from events in the Middle East, also remained.

4: The level of sterling was also likely to be an important driver of UK import prices. The effective exchange rate had appreciated further since the Committee's previous meeting, such that it was over 3% higher than its level at the start of this year. The appreciation was likely to weigh on the outlook for UK import prices and inflation, all else equal, but the extent of pass-through was likely to depend on the underlying driver of the appreciation.

5: The market-implied path for Bank Rate was relatively little changed since the Committee's June meeting and the path that had been assumed in the May Monetary Policy Report. In the Bank's latest Market Participants Survey (MaPS), all respondents had expected the next move in Bank Rate to be downwards. Expectations on the timing of that move were finely balanced with a significant majority of respondents expecting the reduction to occur either at this MPC meeting or the subsequent one in September. That was consistent with market pricing for this meeting, which implied a close-to-evens probability of a 25 basis point reduction in Bank Rate. The median profile for Bank Rate in the August MaPS implied a cumulative 50 basis point reduction by the end of this year, unchanged from the June survey and also broadly in line with market pricing.

6: Turning to UK activity, GDP had grown by 0.7% in 2024 Q1, with that strength appearing to have continued into Q2. Growth in the first half of the year had been stronger than expected at the time of the May Report. Business surveys had continued to point to underlying growth of around 0.3% per quarter, somewhat weaker than headline GDP growth.

7: The Committee discussed the risks around the outlook for domestic demand, which were judged to be skewed to the upside. Households' real income growth had continued to be supported by the reversal of the previous energy shock, although this had appeared to raise savings more than consumption so far. While flat retail sales volumes pointed to continued elevated savings, improvements in indicators such as the GfK major purchases balance suggested a risk that consumption growth could strengthen by more than had been expected in the projection in the August Report. As set out in Box C in the August Report, there was a risk that the impact of higher interest rates on spending had been more modest and would occur earlier than was expected in the Committee's latest modal projections, suggesting upside risks to the outlook for spending. Set against that, corporate insolvency rates had continued to rise, although they had remained well below their historical averages.

8: Twelve-month CPI inflation had fallen back to the MPC's 2% target in May and had remained at that level in June. Inflation was expected to increase to around 2¾% over the second half of this year, owing largely to a smaller expected drag from domestic energy bills.

9: The Committee discussed the latest accumulated evidence on the degree of persistence in pay growth and domestic price inflation. Annual private sector regular average weekly earnings growth had continued to fall back, albeit to a still elevated level, in line with the projection at the time of the May Report. The continued downward trajectory in pay growth had been driven by the normalisation of short-term inflation expectations and some further easing in labour market tightness, although pay growth had remained in excess of rates explained by Bank models. Services consumer price inflation had declined in 2024 Q2 but had remained elevated and had been higher than expected at the time of the May Report.

The immediate policy decision

10: The Monetary Policy Committee sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

11: The Committee had been briefed on the Government's 29 July statement on immediate public spending pressures. The Government had announced that any changes in the stance of fiscal policy would be set out in the Budget on 30 October. These would be incorporated in the November Monetary Policy Report projections.

12: Twelve-month CPI inflation had returned to the MPC's 2% target in May and June. CPI inflation was expected to increase to around 2¾% in the second half of this year, as declines in energy prices last year fell out of the annual comparison, revealing more clearly the prevailing persistence of domestic inflationary pressures.

13: The Committee's framework for assessing the medium-term outlook for inflation distinguished between first and second-round effects. The MPC was focused on second-round effects that captured more persistent inflationary pressures. The Committee noted that there were several potential paths for inflation.

14: The Committee expected the fall in headline inflation, and normalisation in many indicators of inflation expectations, to continue to feed through to weaker pay and price-setting dynamics. A margin of slack should emerge in the economy as GDP fell below potential and the labour market eased further. Domestic inflationary persistence was expected to fade away over the next few years, owing to the restrictive stance of monetary policy. The modal projection in the August Monetary Policy Report was one representation of this. Conditioned on the market-implied path of interest rates, CPI inflation was projected to fall back to 1.7% in two years' time and to 1.5% in three years.

15: However, there was a risk that inflationary pressures from second-round effects would prove more enduring in the medium term. A stronger-than-expected path for demand, and structural factors such as a higher medium-term equilibrium rate of unemployment, could affect domestic wage and price-setting more persistently. Furthermore, the degree of restrictiveness of monetary policy could be less than embodied in the Committee's current assessment. This was reflected in the risks around the August Report modal inflation projection being skewed somewhat to the upside throughout the forecast period. Mean CPI inflation was projected to be 2.0% and 1.8% at the two and three-year horizons respectively.

16: The Committee also continued to monitor the accumulation of evidence from a broad range of indicators.

17: There remained considerable uncertainty around statistics derived from the ONS Labour Force Survey, making it more difficult to gauge the underlying state of labour market activity. Based on a broad set of indicators, the MPC judged that the labour market continued to loosen but that it remained relatively tight by historical standards.

18: Private sector regular average weekly earnings growth had fallen to 5.6% in the three months to May, in line with expectations in the May Report, and broadly in line with alternative indicators of wage growth.

19: Services consumer price inflation had been 5.7% in June, unchanged from May and stronger than had been expected in the May Report, but broadly as expected since the MPC's previous meeting and lower than earlier in the year.

20: Following weakness in the second half of 2023, UK GDP growth had picked up sharply around the turn of the year and has been stronger than expected in the May Report. Business surveys had continued to point to weaker underlying GDP growth of around 0.3% per quarter.

21: Different members placed different probabilities on the extent to which the current restrictive policy stance would lead inflationary pressures to continue to unwind, or whether adverse inflationary dynamics would prove more enduring, possibly as a result of more structural factors or greater momentum in demand. The Committee recognised that the stance of monetary policy could remain restrictive even if Bank Rate were to be reduced from its current level.

22: Five members preferred a 0.25 percentage point reduction in Bank Rate at this meeting. It was appropriate to reduce slightly the degree of policy restrictiveness. The impact from past external shocks had abated and there had been some progress in moderating risks of persistence in inflation. There had been a normalisation in inflation expectations, and forward-looking indicators such as the Decision Maker Panel survey pointed to waning wage and price pressures. The recent strength in services inflation had in part continued to reflect more volatile components of this series. Although GDP had been stronger than expected, the restrictive stance of monetary policy continued to weigh on activity in the real economy, leading to a looser labour market and bearing down on inflationary pressures. For some of these members, the decision was finely balanced. Inflationary persistence had not yet conclusively dissipated, and there remained some upside risks to the outlook.

23: Four members preferred to maintain Bank Rate at 5.25% at this meeting. The upside news to services inflation and GDP outturns relative to the May Report, along with continued elevated wage growth, suggested that second-round effects were having a greater impact on wage and price-setting behaviour in the economy beyond what was embodied in the modal forecast. External factors, such as international food and energy prices, had played the major role in reducing headline inflation to date. By contrast, underlying domestic inflationary pressures appeared more entrenched. These members thought that there was a greater risk of more enduring structural shifts, such as a rise in the medium-term equilibrium rate of employment, a fall in potential growth and a rise in the long-run neutral interest rate, contributing to domestic inflationary persistence. They preferred to maintain the current level of Bank Rate until there was stronger evidence that these upside pressures would not materialise.

24: Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further. The Committee continued to monitor closely the risks of inflation persistence and would decide the appropriate degree of monetary policy restrictiveness at each meeting.

25: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be reduced by 0.25 percentage points, to 5%.

26: Five members (Andrew Bailey, Sarah Breeden, Swati Dhingra, Clare Lombardelli and Dave Ramsden) voted in favour of the proposition. Four members (Megan Greene, Jonathan Haskel, Catherine L Mann and Huw Pill) voted against the proposition, preferring to maintain Bank Rate at 5.25%.

Operational considerations

27: On 31 July, the stock of UK government bonds held for monetary policy purposes was £690 billion.

28: As discussed in Box A in the August Monetary Policy Report, the Committee would vote on the target for the reduction in the stock of UK government bonds held for monetary policy purposes over the 12-month period from October 2024 to September 2025 at its September 2024 meeting.

29: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

Sam Beckett was present as the Treasury representative.

David Roberts was present on 23 and 29 July, and Jonathan Bewes on 29 July, as observers for the purpose of exercising oversight functions in their roles as members of the Bank's Court of Directors.

30: On behalf of the Committee, the Chair expressed his appreciation to Jonathan Haskel for his contributions to the work of the MPC since becoming a member in 2018.

GBP/USD Under Pressure as Market Anticipates Bank of England Rate Decision

The British pound sterling continues to decline steadily against the US dollar. The GBP/USD pair is trending towards 1.2848.

On the one hand, the pressure from the USD rate is evident. On the other hand, investors are awaiting the outcome of today's Bank of England meeting and its decision on interest rates.

There is speculation that the BoE will lower the interest rate from 5.25% to 5.00% today. The inflationary environment, coupled with the state of the employment market in the UK, supports this adjustment. The probability of a rate cut is currently estimated at 65%.

An early move towards monetary policy easing is considered possible for the Bank of England. However, the regulator's tone in its statements may be relatively cautious, indicating that the BoE is unlikely to lower the rate rapidly. A certain degree of conservatism can be expected from the Bank of England, which will only act if it is fully confident about the economic conditions.

This potential decision is already factored into GBP quotes. The future movements in GBPUSD will be directly influenced by the details provided in the Bank of England's accompanying statement.

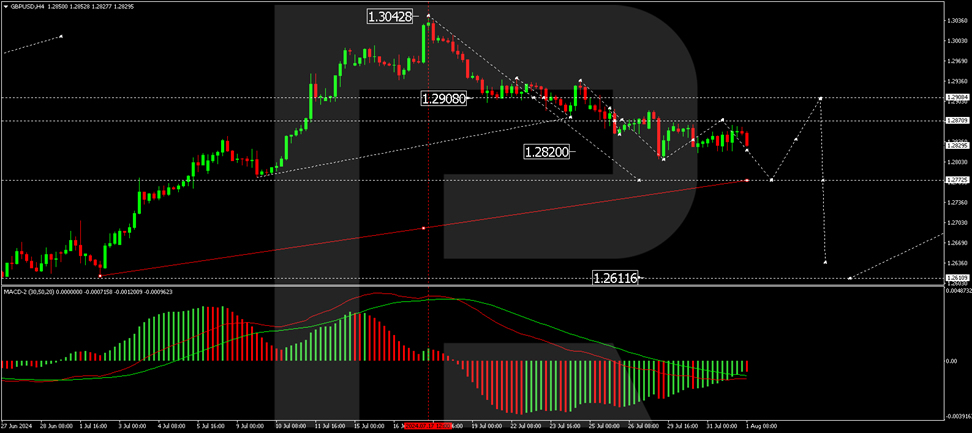

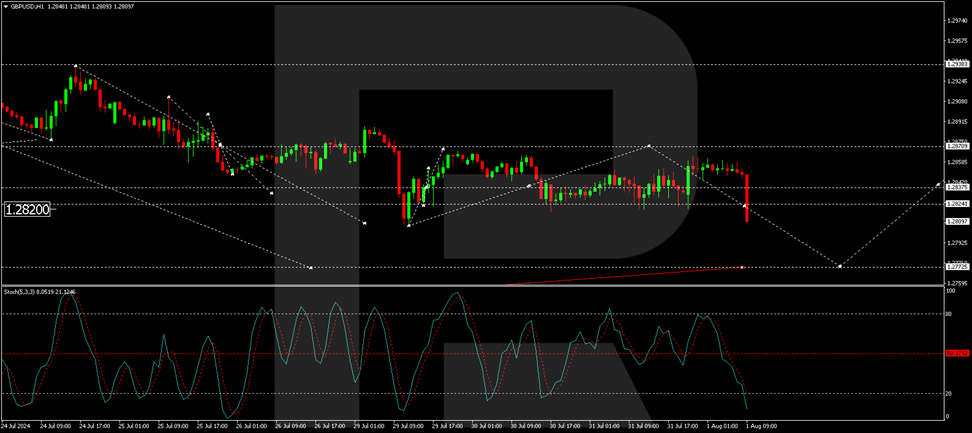

Technical Analysis: GBP/USD

On the H4 chart of GBP/USD, the market has executed a decline wave to 1.2820 and a subsequent correction to 1.2867. Today, the market continues its downward movement towards 1.2772. After reaching this level, we will assess the probability of a correction to 1.2870 (testing from below). After the correction is complete, we expect the beginning of a new decline wave to the local target of 1.2611. This scenario is technically supported by the MACD indicator, which shows the signal line below the zero mark and pointing downwards.

On the H1 chart of GBP/USD, a correction wave is currently underway towards 1.2867. Today, the formation of the next downward wave to the initial target of 1.2772 is in progress. After reaching this level, we will evaluate the likelihood of a new correction wave towards 1.2870. Following the completion of the correction, we expect a new decline wave to 1.2770. This scenario is technically confirmed by the Stochastic oscillator, with its signal line positioned below 50 and continuing to decline towards 20.

Investors and traders should closely monitor the BoE's statement for any indications of future policy direction, as it will be crucial in determining the short to medium-term trajectory of the GBP/USD pair.

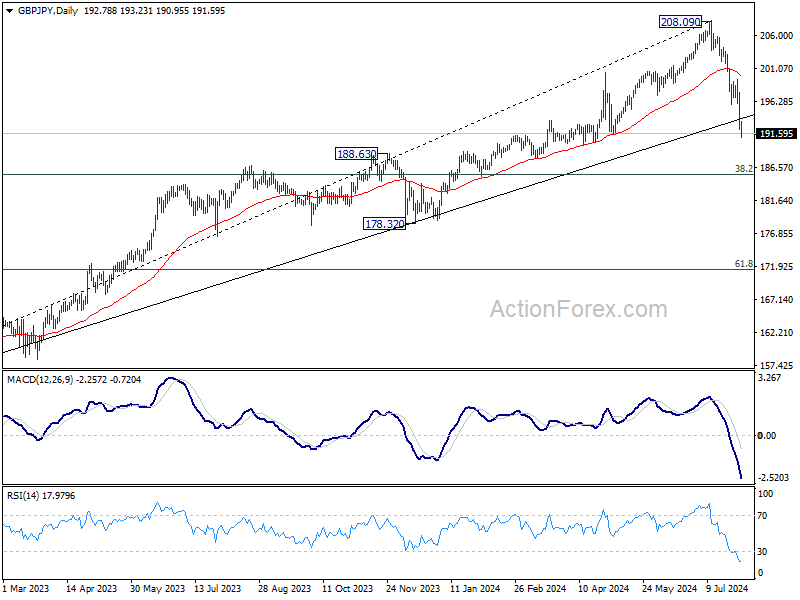

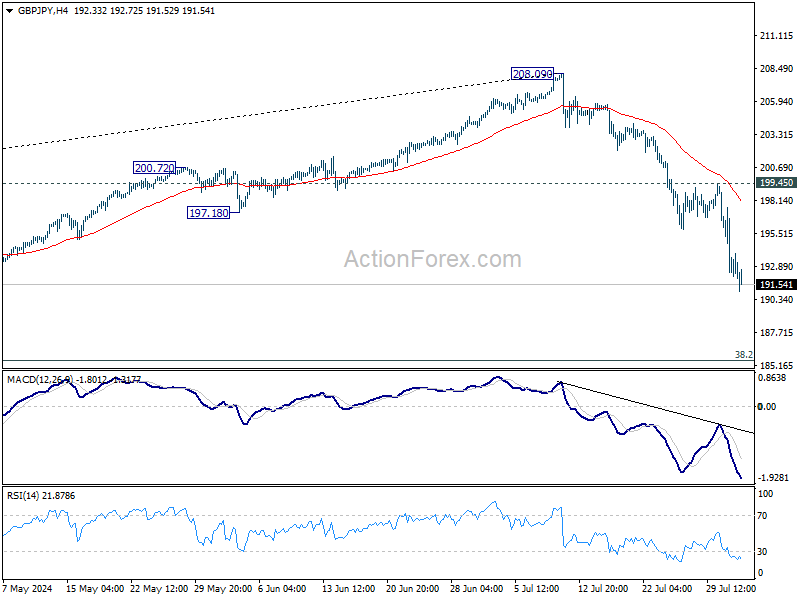

GBPJPY Selling Drama Stretches Below 200-EMA

- GBPJPY’s massive sell-off continues, reaches 3-month low

- Short-term risk bearish but oversold conditions detected

- BoE policy announcement might influence GBP at 11:30 GMT

GBPJPY suffered another bold attack this week, giving back 8% of its value since its peak at a 16-year high of 208.09 on July 11. With downside pressures intensifying below the 200-day exponential moving average (EMA) today, more sellers could join the market.

However, past drops below the 200-day EMA have been brief and quickly reversible. Encouragingly, the RSI and stochastic oscillator are currently both deeply oversold, which suggests that the aggressive sell-off may pause soon.

The 61.8% Fibonacci retracement of the 2024 upleg is within breathing distance at 189.94 and could immediately tackle downside forces ahead of the 188.22 support area taken from March. Failure to pivot there could see an extension towards the 185.00 mark, which overlaps with the 78.6% Fibonacci level.

On the upside, a move above the 200-day EMA and the 50% Fibonacci mark of 193.40 could initially stall somewhere between the broken support trendline from December 2023 at 194.20 and the 38.2% Fibonacci of 196.87. Even higher, the pair could gain fresh bullish traction towards the 20- and 50-day EMAs at 199.60 and then up to the 23.6% Fibonacci number of 201.16.

Overall, GBPJPY may continue to face selling pressures in the short term, but given the oversold signals and the nearby protective zone of 189.94, the bearish momentum could soon slow down.

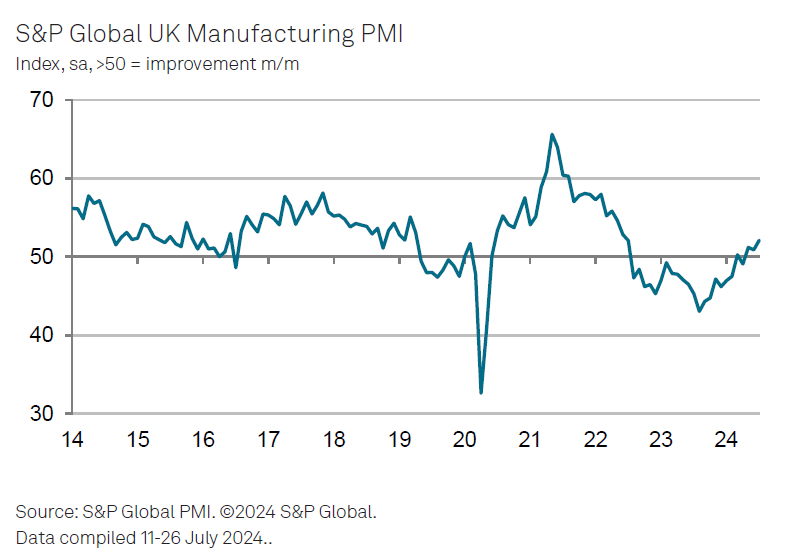

UK manufacturing PMI finalized at 52.1, inflation pressure moving to manufacturing sector

UK PMI Manufacturing was finalized at 52.1 in July, up from June's 50.9. Production growth was the fastest since February 2022, while input price inflation hit an 18-month high.

Rob Dobson, Director at S&P Global Market Intelligence, noted that UK manufacturing has started the H2 on an "encouragingly solid footing." July saw increased production and new orders, with staffing levels rising for the first time since September 2022. Confidence reached its highest level in two-and-a-half years, with 60% of companies expecting output to rise over the next 12 months.

However, inflationary pressures are a "blot on the copybook", with input costs rising at the highest rate in 18 months. The ongoing Red Sea crisis and related freight issues are driving up prices. Selling prices also increased at the fastest rate since mid-2023. BoE is likely to remain cautious about loosening monetary policy due to these inflationary pressures "pivoting away from services and towards manufacturing."

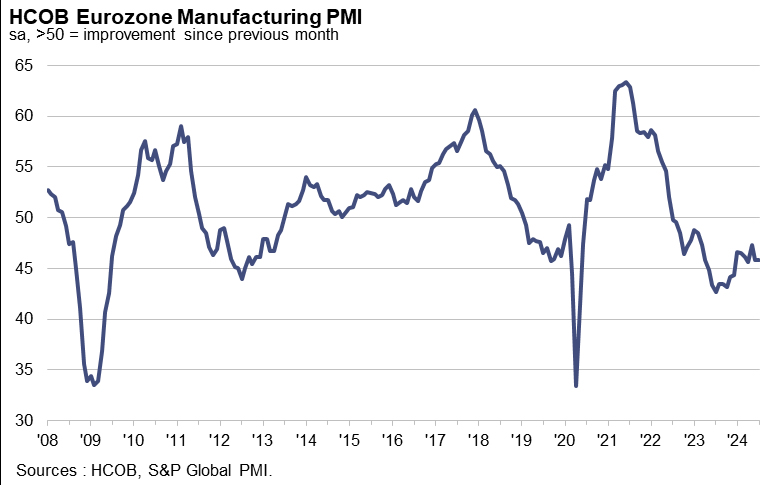

Eurozone PMI manufacturing finalized at 45.8, recovering taking a hit

Eurozone's PMI Manufacturing was finalized at 45.8 in July, unchanged from June, indicating ongoing contraction. PMI Manufacturing Output fell from 46.1 to 45.6, a 7-month low. Input costs increased at the fastest rate in a year and a half.

Among countries, Greece led with a PMI of 53.2, a 7-month low. Spain recorded 51.0, a 6-month low. Ireland reached a 5-month high at 50.1, but the Netherlands fell to 49.2, a 6-month low. Italy showed a 4-month high at 47.4, France hit a 6-month low at 44.0, Germany a 3-month low at 43.2, and Austria a 4-month low at 43.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that the belief in the Eurozone's recovery "is taking a hit." He emphasized that the decline in production has "intensified" doubts, prompting a likely downgrade in GDP growth forecast from 0.8%. Industrial activity weakened broadly, with only Greece and Spain seeing meaningful growth, though momentum there also slowed. Austria and Germany displayed the greatest weakness.

WTT: Top Trade Ideas for August

For the month of August, I have my eyes set on three pairs for my swing trading opportunities during the course of the month. Asides these three, most of my other trade ideas will be executed on lower timeframes, and with more conservative targets in mind. Do note, as always, that these are my personal ideas, and do not serve as a financial advise.

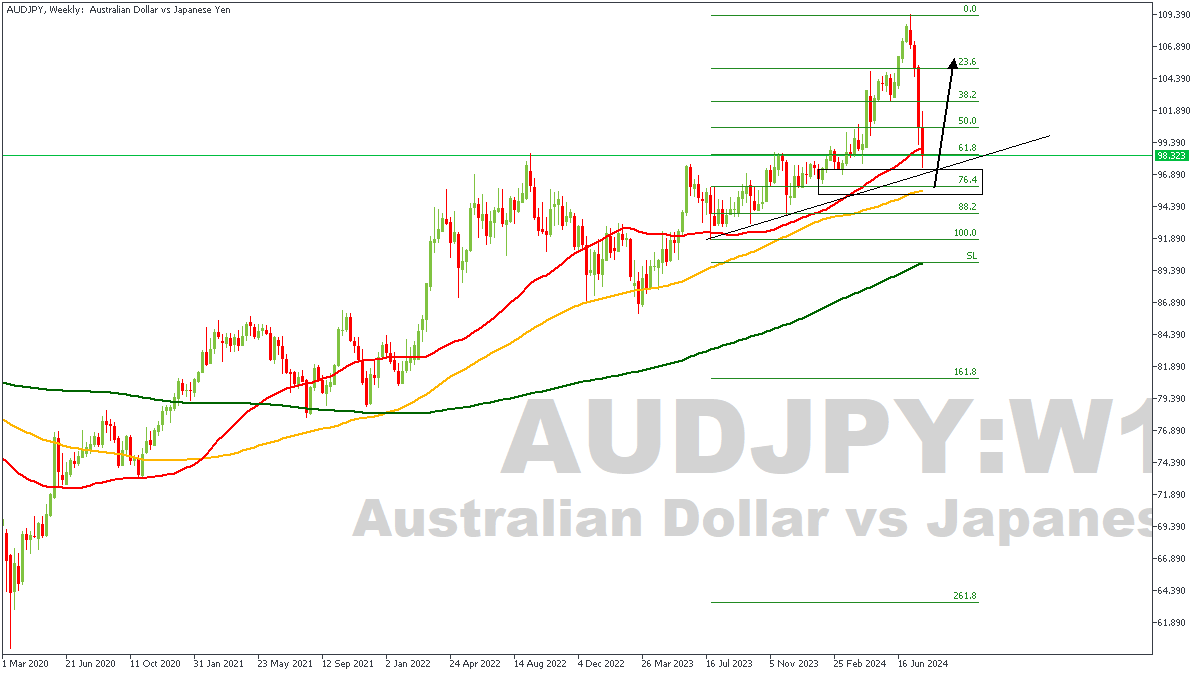

AUDJPY – W1 Timeframe

Without altering or challenging the course of the moving averages and their bullish array, we see price head into the 100-period moving average on the weekly timeframe of AUDJPY as a likely area of support. In line with this, we also see the weekly timeframe demand zone which overlaps the weekly timeframe pivot, and the trendline support that cuts across them both; come within the reach of the price action – implying quite simply that prices may reverse bullish from the area of confluence.

Analyst’s Expectations:

- Direction: Bullish

- Target: 105.246

- Invalidation: 95.165

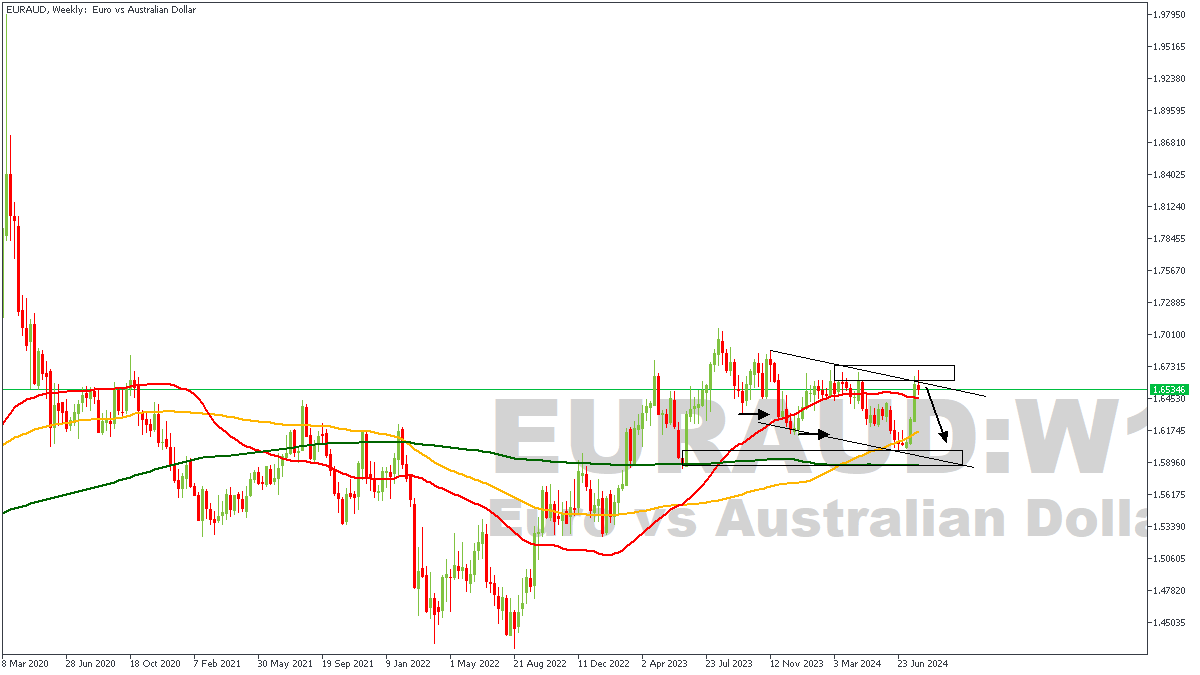

EURAUD – W1 Timeframe

There is a descending channel on the weekly timeframe of EURAUD; which means the outcome could be a breakout, or a formidable rejection. To the left of the current price point, we see price has broken structure downwards a few times in the past, leading me to look for the supply zone responsible for the bearish break of structure. That supply zone, coupled with the trendline resistance, as well as the overbought RSI (Relative Strength Index) are my basis for expecting a bearish outcome from all of this.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.62553

- Invalidation: 1.68862

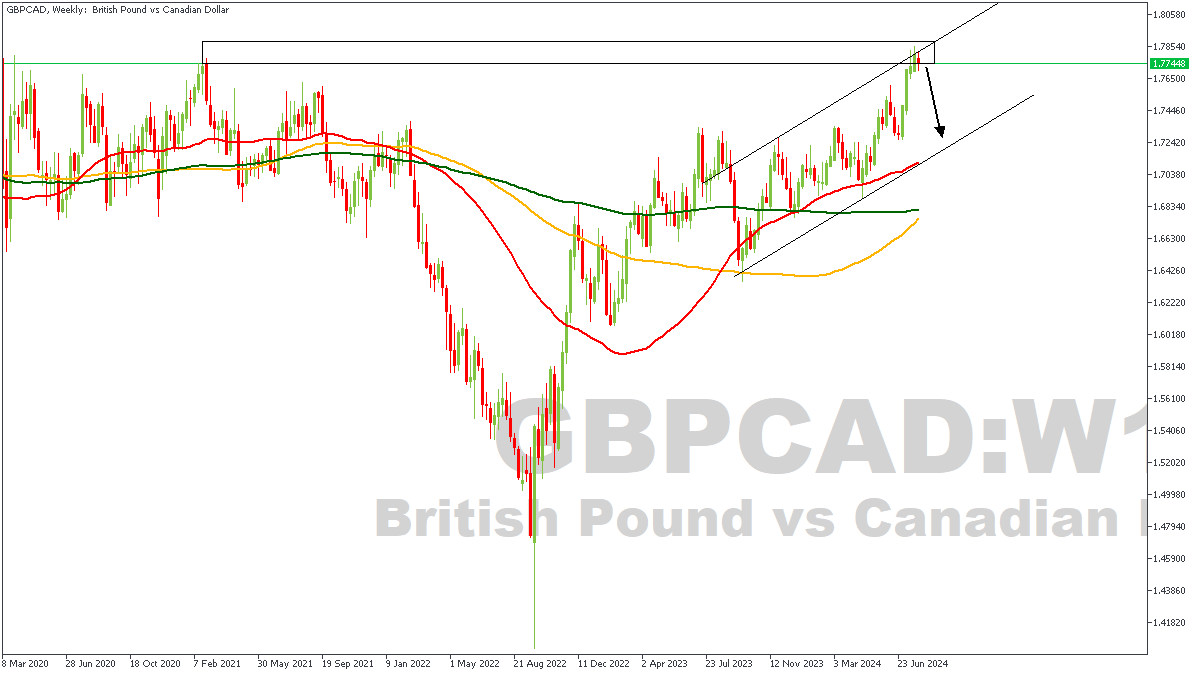

GBPCAD – W1 Timeframe

On the weekly timeframe chart of GBPCAD as shown on the chart, we see price trade into the weekly timeframe supply zone, whilst staying within the confines of a rising channel. Price has initially been rejected off the intersection of the resistance trendline, and the supply zone, and may very well reverse completely from the highlighted zone; albeit, lower timeframes hold the trigger for a bearish scenario.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.73661

- Invalidation: 1.78949

USD/JPY Falls Below 150 Yen Per Dollar

The yen was last this strong in mid-March this year. News from central banks contributed to the decline in USD/JPY.

Yesterday, the Bank of Japan raised interest rates to levels not seen in the past 15 years. Conversely, the Fed kept rates unchanged as expected but "opened the door" for a possible cut in September, according to Reuters. This news weakened the USD and provided a bullish boost to U.S. stock markets.

This shift highlights the collapse of the "carry trade" strategy, where high U.S. rates and low Japanese rates supported the rise of USD/JPY. From early 2023 to the July peak in 2024, USD/JPY rose by about 23%, but it started declining amid news of Bank of Japan's currency interventions.

On July 25, analysing the USD/JPY chart, we:

→ Constructed a descending channel (shown in red);

→ Predicted a scenario with a technical rebound from the lower boundary of the red channel.

Since then, USD/JPY climbed to the psychological mark of 155 yen per dollar on July 30, where the downtrend resumed after a false breakout.

How might the USD/JPY situation develop?

Technical Analysis of USD/JPY Today:

→ The chart forms a structure of swing extremes A-B-C-D-E-F-G. Notably, each subsequent recovery is about 50% of the previous downward impulse, indicating dominant supply forces. The expanding channel, shown in purple, also confirms this.

→ The psychological level of 150 yen per dollar may act as support, mirroring the resistance at 155 yen. Today's price action shows signs of demand activation below 150.

Therefore, it's possible that:

→ After a decline of over 8% from peak A, bears may want to take profits;

→ A corrective move H→I towards the upper purple boundary could form.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

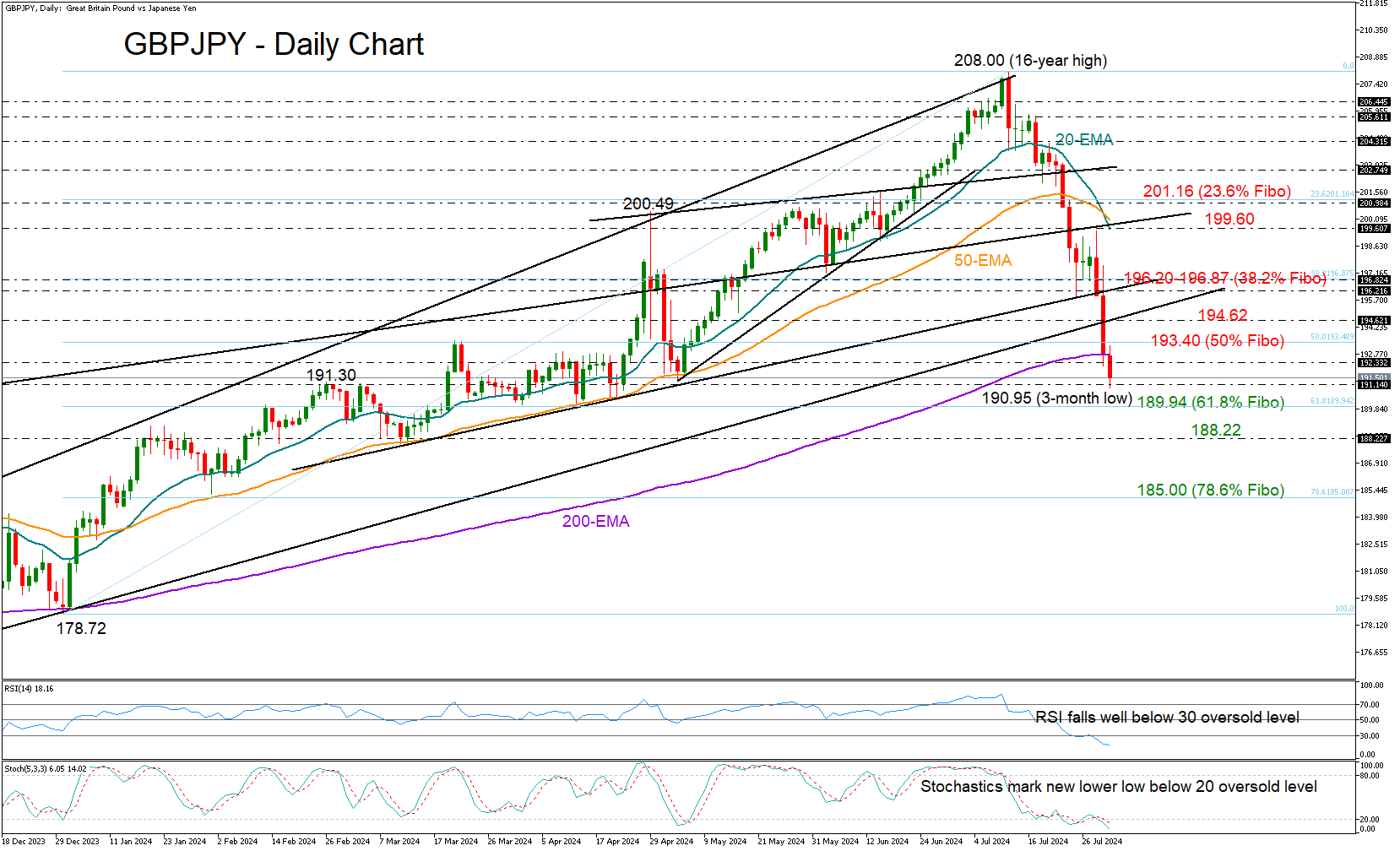

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.80; (P) 194.20; (R1) 196.23; More...

GBP/JPY's fall from 208.09 continues today and intraday bias stays on the downside. Current decline is a larger scale correction and should target 185.49 fibonacci level. For now, outlook will continue to stay bearish as long as 199.45 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in W MACD, 208.09 might be a medium term top and fall from there could already be correcting whole up trend from 148.93 (2022 low). Risk will now stay on the downside as long as 55 D EMA (now at 199.93) holds. Deeper fall would be seen to 38.2% retracement of 148.93 to 208.09 at 185.49.