Sample Category Title

Elliott Wave Intraday Analysis: USDJPY Correcting Larger Degree

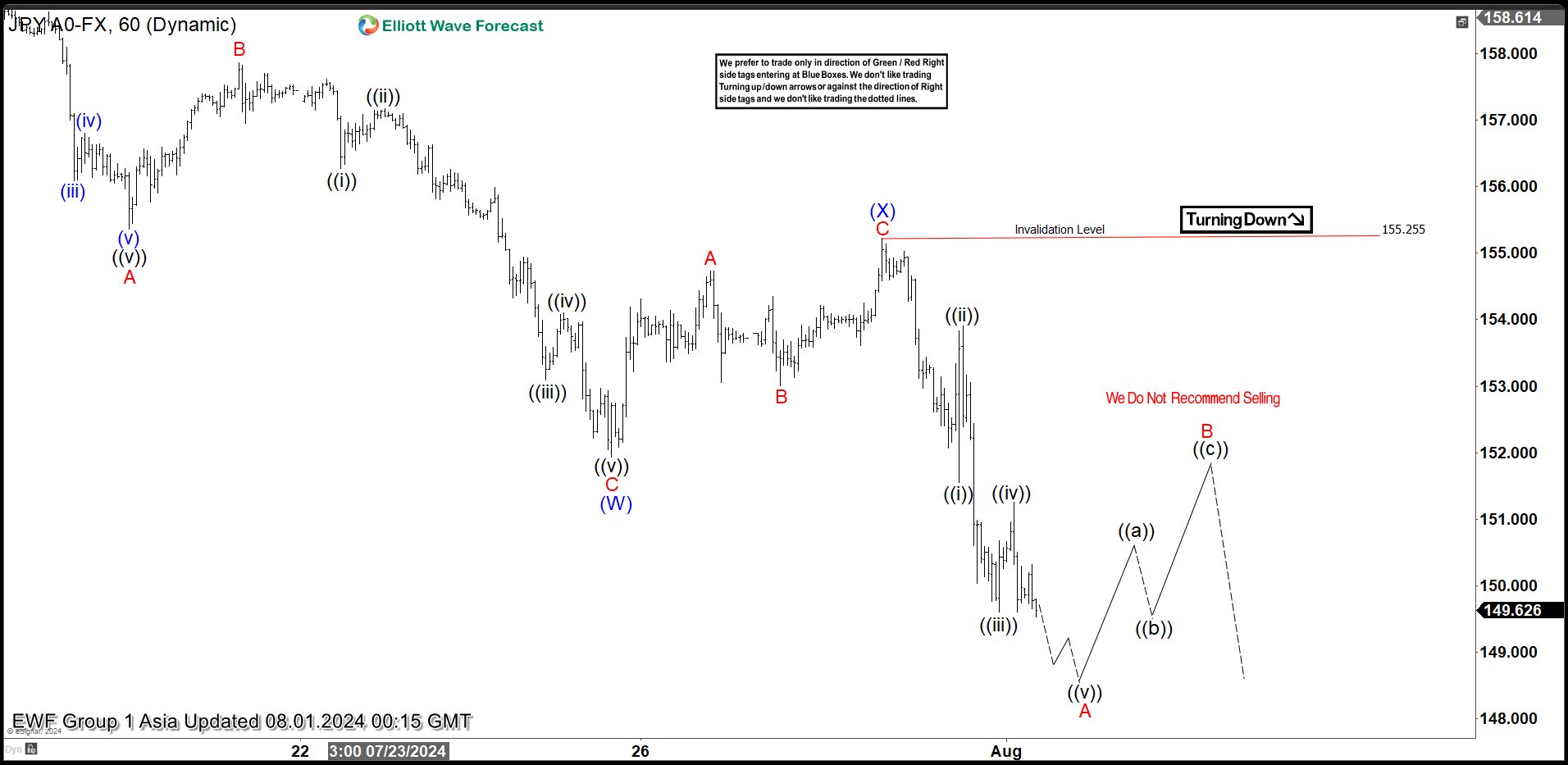

Short Term Elliott Wave in USDJPY suggests that cycle from 7.3.2024 high is in progress as a double three Elliott Wave structure. Down from 7.3.2024 high, wave A ended at 155.37 and rally in wave B ended at 157.86. Wave C lower ended at 151.94 which completed wave (W) in higher degree. Pair then rallied in wave (X) which ended at 155.25 as a zigzag structure. Up from wave (W), wave A ended at 154.73 and wave B ended at 153. Wave C higher ended at 155.25 which also completed wave (X) in higher degree. Pair has turned lower in wave (Y) which subdivides into a zigzag structure.

Down from wave (X), wave ((i)) ended at 151.54 and wave ((ii)) ended at 153.9. Wave ((iii)) lower ended at 149.6 and rally in wave ((iv)) ended at 151.26. Expect pair to extend lower in wave ((v)) which should complete wave A of (Y). Afterwards, it should rally in wave B to correct cycle from 7.30.2024 high before turning lower again. Near term, as far as pivot at 155.25 stays intact, expect rally to fail in 3, 7, or 11 swing for further downside.

USDJPY 60 Minutes Elliott Wave Chart

USDJPY Elliott Wave Video

https://www.youtube.com/watch?v=BA7V2F7gNh4

Confidence Grows Amongst FOMC Members

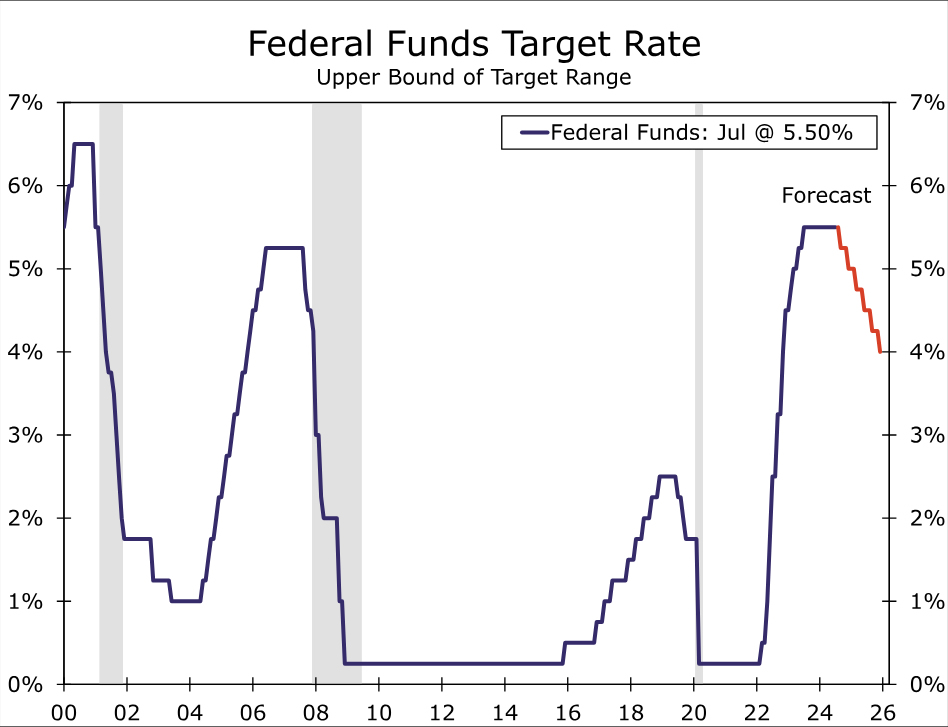

The scene is set for a September first cut by the FOMC. The underlying inflation trend warrants a series of cuts at a measured pace to a 3.375% terminal by mid-2026.

At the July meeting, the FOMC kept rates steady but stated that the economy is moving closer to the point at which it will be appropriate to lower the policy rate. In the press conference, Chair Powell subsequently asserted that the economy does not need to weaken further to justify an easing cycle. Instead, the catalyst will be confidence in the sustainability of the established downtrend in inflation.

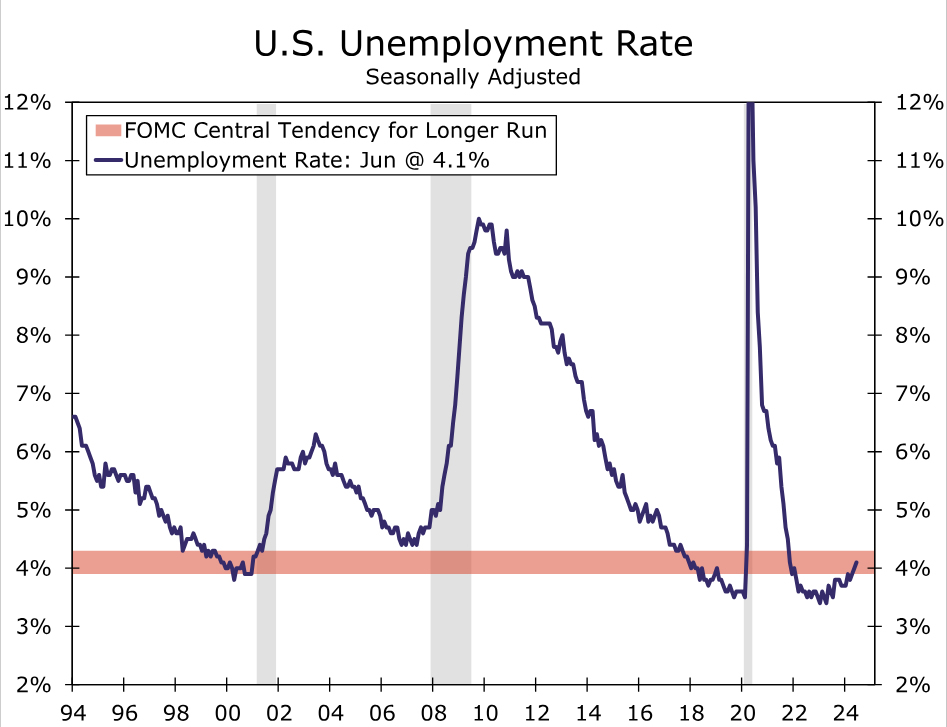

The Committee continue to believe they have time on their side to gauge inflation’s pace and risks. “The unemployment rate has moved up but remains low”, and current momentum is believed to be consistent with a re-balancing of labour demand and supply rather than an outright weakening. Labour market conditions are expected return to a state broadly consistent with that just ahead of the pandemic in 2019, which itself was robust. In the press conference, Chair Powell also highlighted that growth in domestic demand has, to date, remained healthy in 2024.

“Further progress toward the Committee's 2 percent inflation objective” is therefore desired in Q3 before beginning to ease policy. In thinking about the sustainability of the inflation downtrend and the probability of a September cut, it is noteworthy that annual CPI ex-shelter has, since June 2023, held within a 0.8%-2.3%yr range and averaged less than 2.0%yr. Inflation expectations are now also essentially in line with the decade average on a 1-year and 5-year view (University of Michigan Survey); and, as per the Employment Cost index overnight, wage growth is converging to a pace consistent with maintaining inflation at the 2.0%yr target into the medium-term.

The underlying strength of the economy notwithstanding, “the economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate”. This is a change from the language in the previous statement which highlighted only the risks to inflation. Chair Powell emphasised in the press conference that the FOMC have the capacity to adjust the pace of easing as necessary. Right now, the market is focusing on the downside risks for the labour market – which we have been highlighting throughout 2024 and will get an update on in Friday’s July employment report – and consequently a more rapid and/or deeper cutting cycle than we are forecasting (see below). But, a year ahead, if the underlying strength of the economy holds up, inflation risks will likely assert again – the US’ domestic capacity constraints are real and enduring, and trade policy a meaningful threat.

Westpac’s view of the FOMC outlook seeks to balance these risks. We continue to expect a first cut in September followed by a single cut per quarter from Q4 2024 to Q2 2026 to a 3.375% terminal rate. Against the FOMC’s 2.8% ‘longer run’ estimate (revised up in June from 2.6% at the March meeting) and our own slightly higher view of the likely trend in neutral rates, the end point for the cycle is best considered mildly restrictive. In our view, policy is only likely to return to a neutral or expansionary setting if consumption growth weakens materially below trend: fiscal policy, the green transition and capacity all warrant robust, if not strong, momentum in US investment into the medium term.

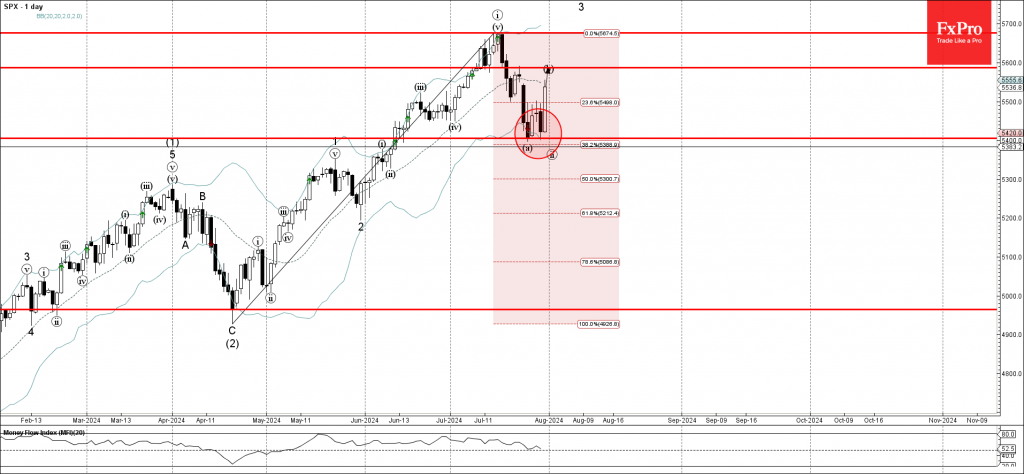

S&P 500 index Wave Analysis

- S&P 500 index reversed from support zone

- Likely to rise to resistance level 5585.00

S&P 500 index recently reversed up from the support zone located between the support level 5400.00, daily Bollinger Band and the 38.2% Fibonacci correction of the upward impulse from April.

The upward reversal from this support zone formed the second daily Japanese candlesticks reversal pattern Bullish Engulfing.

Given the overdoing daily uptrend, S&P 500 index can be expected to rise further toward the next resistance level 5585.00 – target price for the completion of the active wave (b).

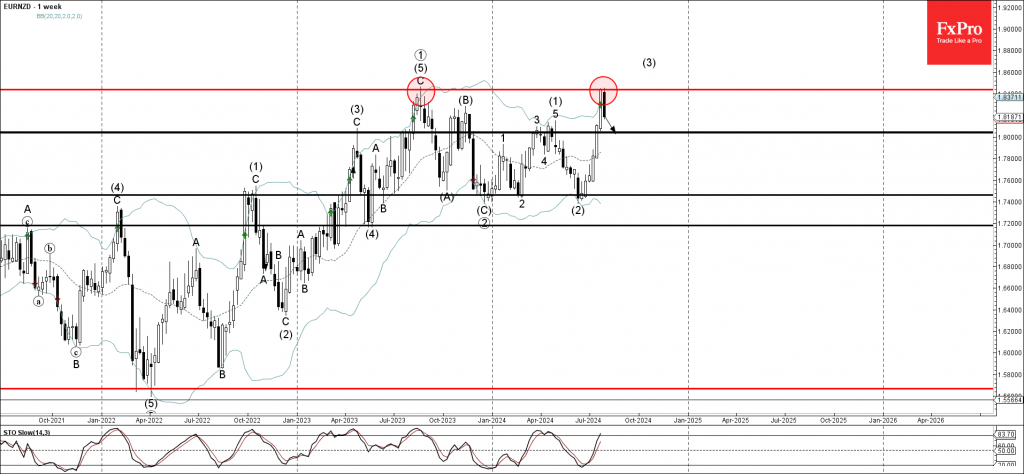

EURNZD Wave Analysis

- EURNZD under bearish pressure

- Likely to fall to support level 1.8045

EURNZD currency pair under the bearish pressure after the earlier downward reversal from the long-term resistance level 1.8435, which stopped the weekly uptrend in the middle of 2023.

The resistance level 1.8435 was strengthened by the upper weekly Bollinger Band.

Given the strength of the resistance level 1.8435 and the overbought weekly Stochastic, EURNZD currency pair can be expected to fall further to the next support level 1.8045.

FOMC: ‘Twas the Meeting Before Rate Cuts

Summary

As was widely anticipated, the FOMC left the fed funds rate unchanged at the conclusion of today's meeting, but it opened the door to potentially easing policy at its next meeting on September 18. While inflation remains above the FOMC's 2% target, it has fallen significantly since the Committee last raised rates a year ago. At the same time, the labor market has cooled sufficiently and now resembles its pre-pandemic state. In its post-meeting statement, the FOMC noted the improving balance between its employment and inflation goals and emphasized it is growing more mindful of the risks to the labor market by noting it is "attentive to the risks to both sides of its dual mandate", rather than previously only noting its attention to inflation risks.

We suspect today's decision, post-meeting statement and Powell's press conference statements reflect a compromise among the Committee members. While some more dovish members were likely inclined to reduce the policy rate at today's meeting, more hawkish members are likely wanting to see more data. To thread the needle, we think Chair Powell arrived at a compromise: hold rates steady at this meeting, but send overt signals to the market and broader public that the base case is for rate cuts starting soon. We look for the FOMC to cut the fed funds rate by 25 bps at its next meeting, with a further 25 bps cut in December and an additional 100 bps of easing in 2025.

FOMC Sits Tight but Signals Rate Cuts Are Coming Soon

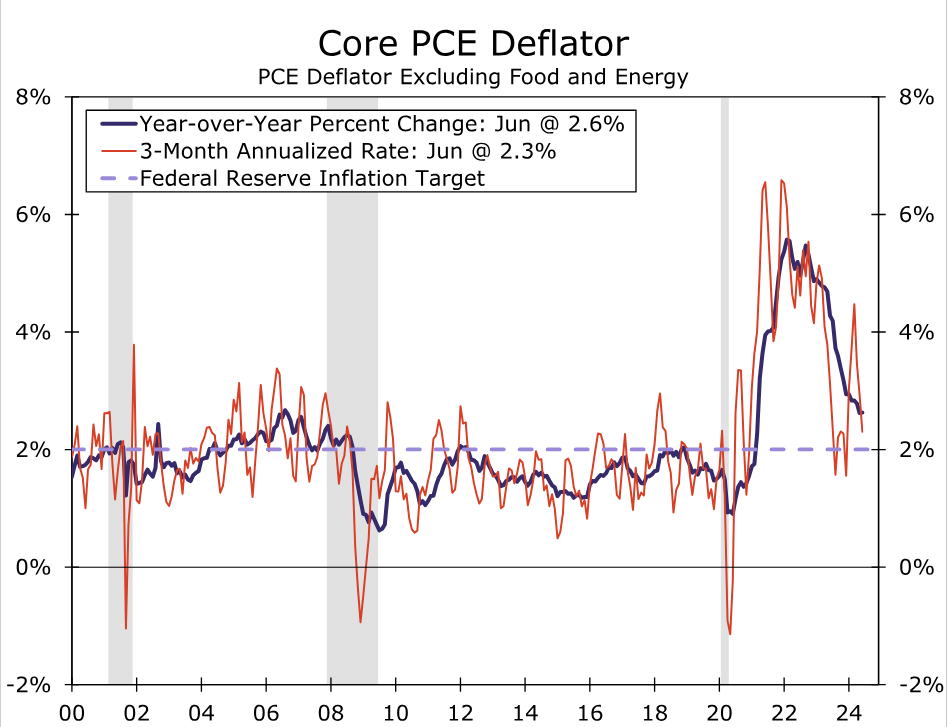

The FOMC made no policy changes at the conclusion of today's meeting, but opened the door to a rate reduction as soon as its next meeting on September 17-18. For a year now the FOMC has left the fed funds rate unchanged at a 23-year high of 5.25–5.50% to put downward pressure on inflation. While inflation is still not back to the Committee's 2% target, the core PCE deflator has fallen meaningfully from a year-over-year pace of 4.6% when the FOMC last hiked rates a year ago to 2.6% today. The result has been a passive tightening in policy with the real fed funds rate rising over the past year. At the same time, the jobs market has continued to cool and by most measures has returned to its pre-pandemic state. The unemployment rate has risen from its cycle-low, nonfarm payrolls gains over the past three months have been the slowest in more than three years and labor cost growth has cooled noticeably.

The post-meeting statement indicated that the FOMC now sees the risks of a too hot economy or a too cool one as more equally balanced. The statement now reads that the Committee "is attentive to risks to both sides of its dual mandate", rather than only emphasizing the risks to its inflation mandate as it had in the prior statement. The change of tone comes as the Committee noted softer conditions in the labor market, including job gains having "moderated" and the unemployment rate having "moved up" even if it "remains low." Meantime, the Committee acknowledged "some further progress" in lowering inflation back to 2%. While the changes marked a step toward eventual easing, they stopped short of fully committing to a rate cut in September to give the Committee flexibility to react to incoming data over the next seven weeks. That said, the implicit signals for looming rate cuts were there: Chair Powell stated in the press conference that "a rate cut could be on the table in September" and "the broad sense of the committee is that the economy is moving closer to the point at which it will be appropriate to reduce our policy rate."

We suspect today's decision, post-meeting statement and Powell's press conference statements reflect a compromise among the Committee members. We believe the more dovishly inclined FOMC participants probably made the case for cutting rates at today's meeting. As outlined above, inflation is nearly back to the central bank's target, and the economy has begun to show signs that restrictive monetary policy is taking its toll. Put more simply, if the overwhelming consensus is that a 25 bps cut is appropriate in seven weeks, why wait?

That said, we think the hawks on the Committee likely pressed Powell from the opposite direction. Inflation has been above target for more than three years (and counting), and while the economy appears to have decelerated this year, it has not fallen off a cliff. Given how tough the job has been bringing inflation down, what's another seven weeks of waiting in exchange for a few more inflation and employment readings? To thread the needle, we think Chair Powell arrived at a compromise: hold rates steady at this meeting, but send overt signals to the market and broader public that the base case is for rate cuts starting soon.

We believe economic conditions have softened sufficiently to drive inflation even closer to 2% in the months ahead, and that risks to the labor market are mounting. While thus far cooling in the labor market is consistent with conditions "normalizing", the increasingly restrictive stance of policy risks threatening the employment side of the FOMC's mandate. We look for the Committee to reduce the fed funds rate by 25 bps at its September meeting as a result, with a further 25 bps cut in December and an additional 100 bps of easing in 2025.

Fed Review: Mindful of Risks

- The Fed made no changes to its monetary policy in the July meeting, as widely anticipated. Powell avoided pre-committing but firmly opened the door for initiating rate cuts in September.

- The Fed sees plausible scenarios ranging from 'zero to several cuts this year'. Focus is on the risk of sharp deterioration in labour market conditions, but we see no reason for panic yet.

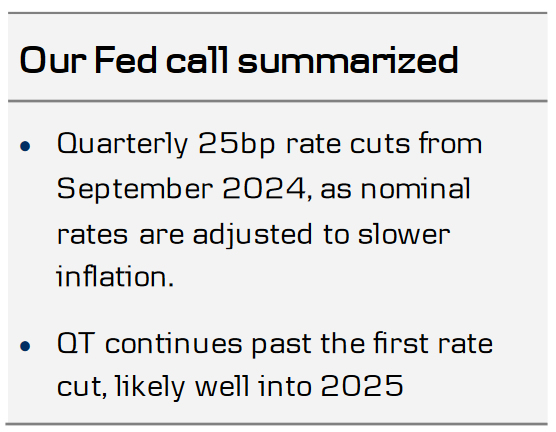

- Markets price in a 10-15% probability for a 50bp move in September and a cumulative 72bp of cuts by year-end. We still expect only quarterly 25bp reductions from September and forecast downside potential to EUR/USD.

Powell made it as clear as possible that the September cut is firmly on the table. Already the initial statement noted that 'job gains have moderated' (prev. 'remained strong') and that 'Committee is attentive to risks to both sides of its dual mandate' (prev. only 'inflation risks').

During the press conference, Powell noted several times that the Fed has become more mindful of downside risks with regards to the labour market, but also reaffirmed that the economy is 'actually in a good place' for now - and we would agree.

The Fed has reached a point where there is no longer uncertainty over whether or not the current policy is restrictive. Economic growth is slowing and labour market conditions have cooled notably. Upside risks to inflation prevail, but Q2 data has increased the policymakers' confidence on price pressures moderating further.

Powell emphasized that the outcome space for rates remains wide. He saw plausible scenarios ranging from 'zero to several cuts this year'. We have called for 25bp rate cuts in September and December, followed by four more in 2025, which is now already firmly on the hawkish side of current market pricing.

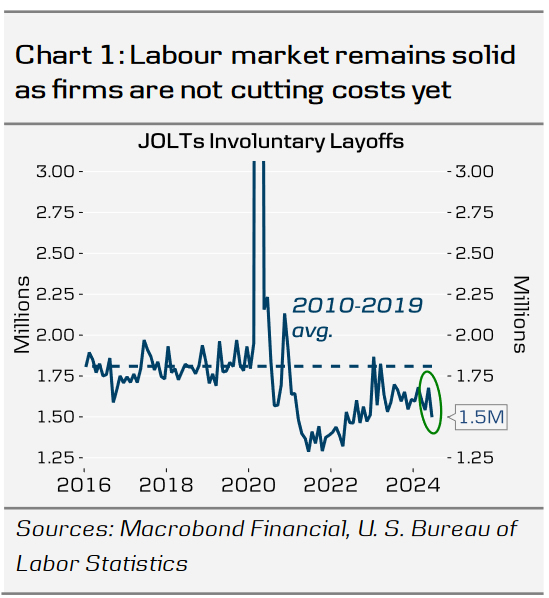

So why don't we believe in rapid cuts? Simply put, we still think the economy remains on a solid footing. In our Fed preview, 25 July, we discussed why firms are not yet under pressure to start cutting costs abruptly, and how fiscal policy helps to keep growth afloat. This week, the latest JOLTs data supported that view as firms' involuntary layoffs fell to the lowest level since November 2022.

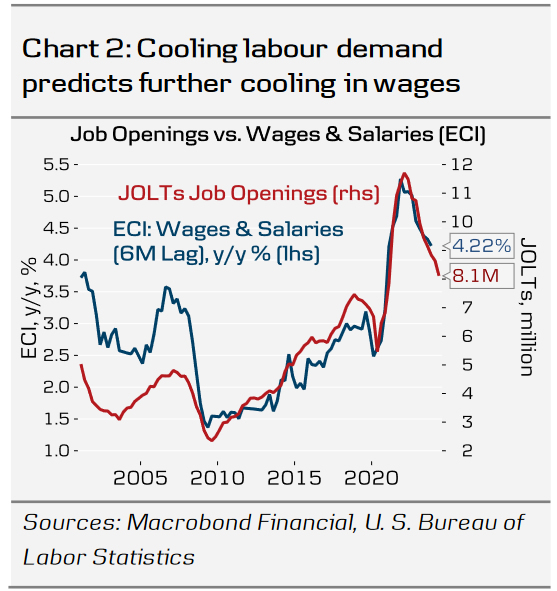

Is there a risk that the Fed is falling behind the curve? Yes, but for now the evidence is lacking. Powell humbly noted that gauging the perfect time for initiating cuts is inarguably tricky. We have for long argued that as real interest rates remain restrictive and as inflation continues to cool, the Fed will need to start lowering nominal policy rates to avoid overtightening its policy. Today's ECI data showed further moderation in underlying cost pressures and leading indicators point towards further slowdown over the coming 6M. For now, the speculation about looming cuts and the consequent easing in financial conditions have helped to ease some of the restrictive effect even when the actual cuts are still in the horizon. The Fed remains mindful of risks, but not in panic mode for now.

Markets: We think the current Fed cut pricing is excessive

The dovish signals from Powell at today’s conference added to the existing market narrative that Fed is set to ease aggressively. Money markets are now pricing 156bp worth of rate cuts over the next 12 months, up from 150bp prior to the statement release. EUR/USD moved lower during the press conference, but reversed part of the decline later on. The US Treasury curve bull-steepened, with the 10Y tenor declining by 6bp to a new 5-month low of 4.07. The current Fed pricing seems optimistic, and we believe that risks related to US rates are now strongly tilted to the upside (see Yield Outlook - Optimism has become excessive, 31 July).

Fed holds steady at 5.25-5.50%, keeps rate cut plans unclear

Fed kept interest rates unchanged at 5.25-5.50%, as widely anticipated, with a unanimous vote. The accompanying statement closely mirrored June's guidance for future decisions, maintaining that the Fed is "prepared to adjust the stance of monetary policy as appropriate."

Fed emphasized that its assessments will consider a "wide range of information," indicating that it is keeping its plans for potential rate cuts close to the chest for now.

On the economic front, Fed acknowledged that job gains have "moderated" and the unemployment rate has "moved up." Additionally, the statement noted "some further progress" in reducing inflation towards the target. Fed also mentioned that risks to inflation and employment are continuing to "move into better balance."

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have moderated, and the unemployment rate has moved up but remains low. Inflation has eased over the past year but remains somewhat elevated. In recent months, there has been some further progress toward the Committee's 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals continue to move into better balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Austan D. Goolsbee; Philip N. Jefferson; Adriana D. Kugler; and Christopher J. Waller. Austan D. Goolsbee voted as an alternate member at this meeting.

Bank of Japan Hikes Rates Further, Slows Bond Buying

Summary

- The Bank of Japan (BoJ) sprung a mild surprise at today's announcement, raising its policy rate to around 0.25%, from around 0% to 0.1% previously. The BoJ also said it would reduce the pace of its bond purchases to around ¥3T per month by early 2026. The BoJ's accompanying comments leaned hawkish in tone, and suggested further tightening would likely be forthcoming.

- Given the central bank's apparent willingness to look through subdued activity data, and apparent desire to front load policy normalization, we now forecast faster BoJ rate hikes than previously. We see another 25 bps rate hike to 0.50% in October, while we also now forecast a further 25 bps rate hike to 0.75% in January 2025.

Bank of Japan Delivers Monetary Tightening, Signals More To Come

The Bank of Japan (BoJ) sprung a mild surprise on markets, delivering an earlier than expected rate increase. The central bank also announced a reduction to its monthly bond purchases, though perhaps a slightly more gradual pace of bond purchases than anticipated. Specifically, the BoJ:

- Raised the target for the uncollateralized overnight call rate to around 0.25%, from around 0% to 0.1% previously.

- Signaled it would reduce the pace of its monthly bond purchases by around ¥400B every quarter, to just under ¥3T per month by early 2026.

For August-September 2024, the BoJ said bond purchases would be ¥5.3T per month, and with regular ¥400B reductions each quarter, fall to ¥2.9T per month by Q1 2026. The central bank said it would conduct an interim review of its bond buying plan in June 2025, and in the case of a rapid rise in long term bond yields, respond nimbly, including for example, increasing its purchases.

In addition to the surprise rate hike, the BoJ's announcement and Governor Ueda's post-meeting press conference were notable for several hawkish leaning comments:

- Real interest rates are expected to remain significantly negative after the change in the policy interest rate, and accommodative financial conditions will continue to firmly support economic activity.

- If the outlook for economic activity and prices evolves broadly as expected, the central bank will accordingly continue to raise the policy interest rate and adjust the degree of monetary accommodation.

- Import price inflation has turned positive and upside risks to prices require attention.

- Wage increases have been significantly higher than last year, and have been spreading across regions, industries and firm sizes.

- FX developments are more likely to affect prices than in the past.

- Governor Ueda said another rate hike before year-end was data dependent. Asked about the terminal level of the BoJ's policy rate, Ueda said 0.50% was not considered a particular limit.

With respect to its outlook on price pressures, the Bank of Japan lowered its core inflation forecast for fiscal year 2024 to 2.5% (from 2.8% previously) and increased its forecast for fiscal year 2025 to 2.1% (from 1.9%). The BoJ kept its forecast for core inflation for fiscal year 2026 unchanged at 1.9%.

We see a couple of important takeaways from today's announcement. First, the BoJ appears to be willing to discount subdued economic activity to some extent, given recent weakness in GDP and some other activity data. That suggests that wage and inflation data will remain particularly important for the timing and magnitude of further rate increases. Second, it also appears possible the BoJ is to some extent trying to front load rate increases, such that the Bank of Japan makes progress in normalizing monetary policy ahead of the significant and sustained monetary easing that is anticipated from the Federal Reserve.

Against this backdrop, we now expect earlier and more pronounced rates hikes from the Bank of Japan than previously. We forecast the next 25 bps policy rate hike to 0.50% at the October monetary announcement, a rate hike that will likely be supported by continued firmness in wages and inflation. We also forecast another 25 bps rate increase to 0.75% at the January 2025 announcement. We acknowledge, however, that this 2025 rate increase is less certain, depending on how price trends evolve and whether the BoJ's cumulative rate increases have a more meaningful impact in restraining the economy. Beyond that, we expect the BoJ to hold its policy rate steady through the rest of 2025. Given our outlook for faster Bank of Japan tightening, and ongoing easing from the Federal Reserve over time, we believe conditions remain in place for the yen to strengthen through much of 2025.