Sample Category Title

FOMC Rate Decision – Potential Impact on EUR/USD, GBP/USD and Dollar Index

- The market anticipates a shift in the Fed’s stance, with three rate cuts now expected in 2024 due to softening economic data.

- A soft landing remains possible as the labor market cools and inflation shows signs of easing.

- Technical analysis suggests GBP/USD is consolidating, EUR/USD maintains a bullish structure, and the Dollar Index (DXY) is at risk of a sharp decline.

FOMC Preview: September Cut Most Likely

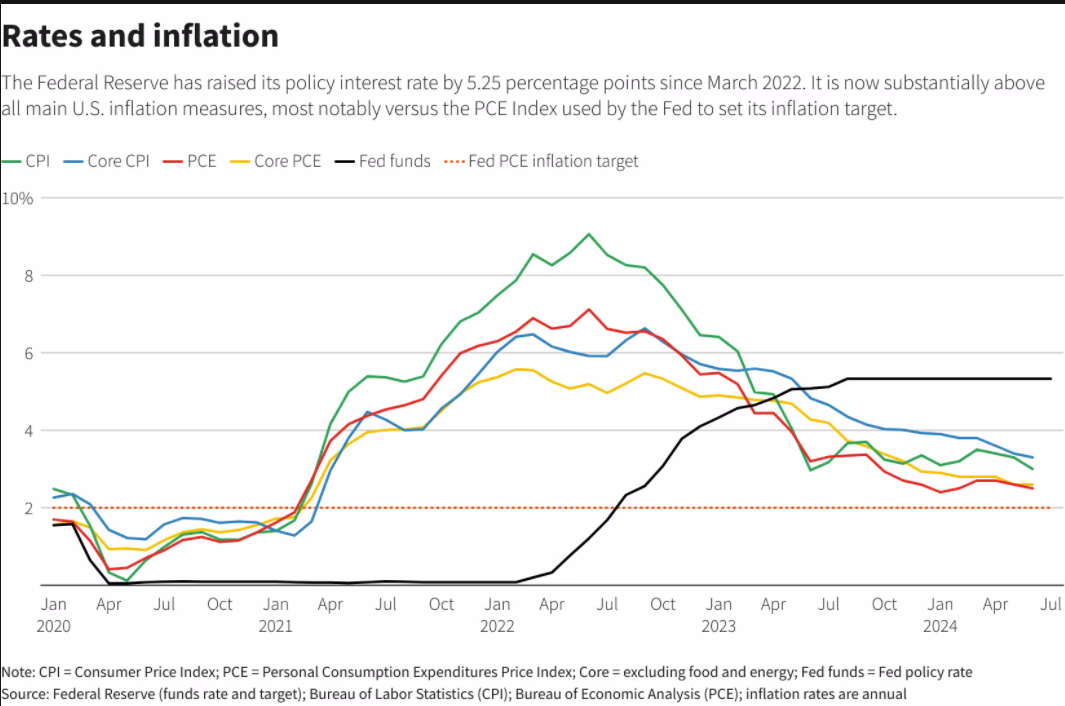

Market participants are approaching today’s FOMC meeting with numerous questions. The previous FOMC meeting was bullish for the US dollar as the Fed updated its projections to include one rate cut in 2024.

Since the June meeting, however, economic data has painted a very different picture. The recent changes and softening data in the US have significantly altered the landscape, with markets now pricing in three rate cuts for 2024.

A soft landing remains possible for the US as the labor market continues to cool. Unemployment has already reached 4.1% in June, exceeding the forecasted 4% predicted for the end of 2024.

Regarding inflation, both core CPI and the core PCE deflator were alarmingly high in the first quarter. However, the numbers for May and June appear more promising. Most notably, the “super-core services” excluding housing, food, and energy—that the Fed has heavily emphasized have slowed significantly. Additionally, the key housing components are now reflecting the moderation observed in third-party private rent series.

US Rates and Inflation Chart, July 31, 2024

Source: LSEG (click to enlarge)

This creates a slight dilemma for the Fed, as rising unemployment could heighten recession concerns. With income growth slowing and pandemic-era savings depleting, the Fed may be pushed to implement the three rate cuts currently anticipated before the year’s end.

Given this dilemma and the multitude of factors the Fed must consider, today’s forward guidance will be crucial. The rhetoric in June about one rate cut in 2024 is likely to change. If Fed Chair Powell maintains his outlook, it could lead to a short-term bounce for the US dollar.

Conversely, a pivot from Powell and a more bearish tone would theoretically lead to US dollar weakness. However, the recent selloff in the US dollar may indicate that much of the “pivot” is already priced in.

Technical Analysis

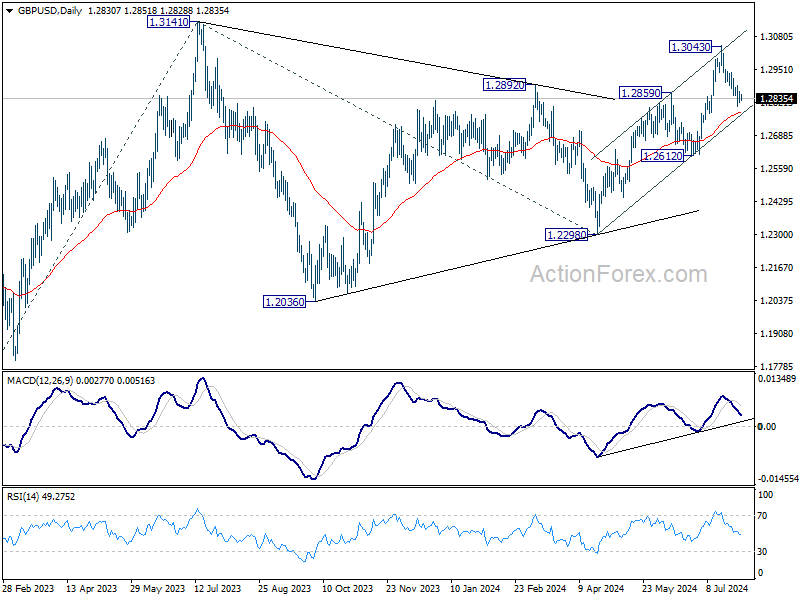

GBP/USD

From a technical perspective, GBP/USD has been consolidating over the past three days since hitting support at 1.2850. Both bulls and bears have attempted to move the price away from this level, but each effort has been countered by buying or selling pressure. This underscores the current uncertainty surrounding the upcoming Central Bank meetings.

Immediate support below the 1.2850 area lies at the 1.2800 and 1.2750 levels. A break below these support zones could shift focus back to the psychological 1.2500 mark. Conversely, an upward movement will face resistance at 1.2950 before the psychological 1.3000 level becomes crucial again.

Support

- 1.2800

- 1.2750

- 1.2680

Resistance

- 1.2950

- 1.3000

- 1.3040

GBP/USD Daily Chart, July 31, 2024

Source: TradingView (click to enlarge)

EUR/USD

From a technical perspective, EUR/USD has risen today following a slight uptick in the Euro Area’s inflation print.

On a broader scale and daily timeframe, EUR/USD maintains a bullish structure. A daily candle close below the 1.0680 level would be necessary to alter this structure. The 100-day moving average around the 1.0800 level is currently providing support, with immediate resistance at 1.0860 and 1.0900.

Conversely, a decline from the current price may find support at 1.0755 before the key swing low at 1.0680 comes into focus.

EUR/USD Daily Chart, July 31, 2024

Source: TradingView (click to enlarge)

Support

- 1.0800

- 1.0755

- 1.0680

Resistance

- 1.0860

- 1.0900

- 1.0948

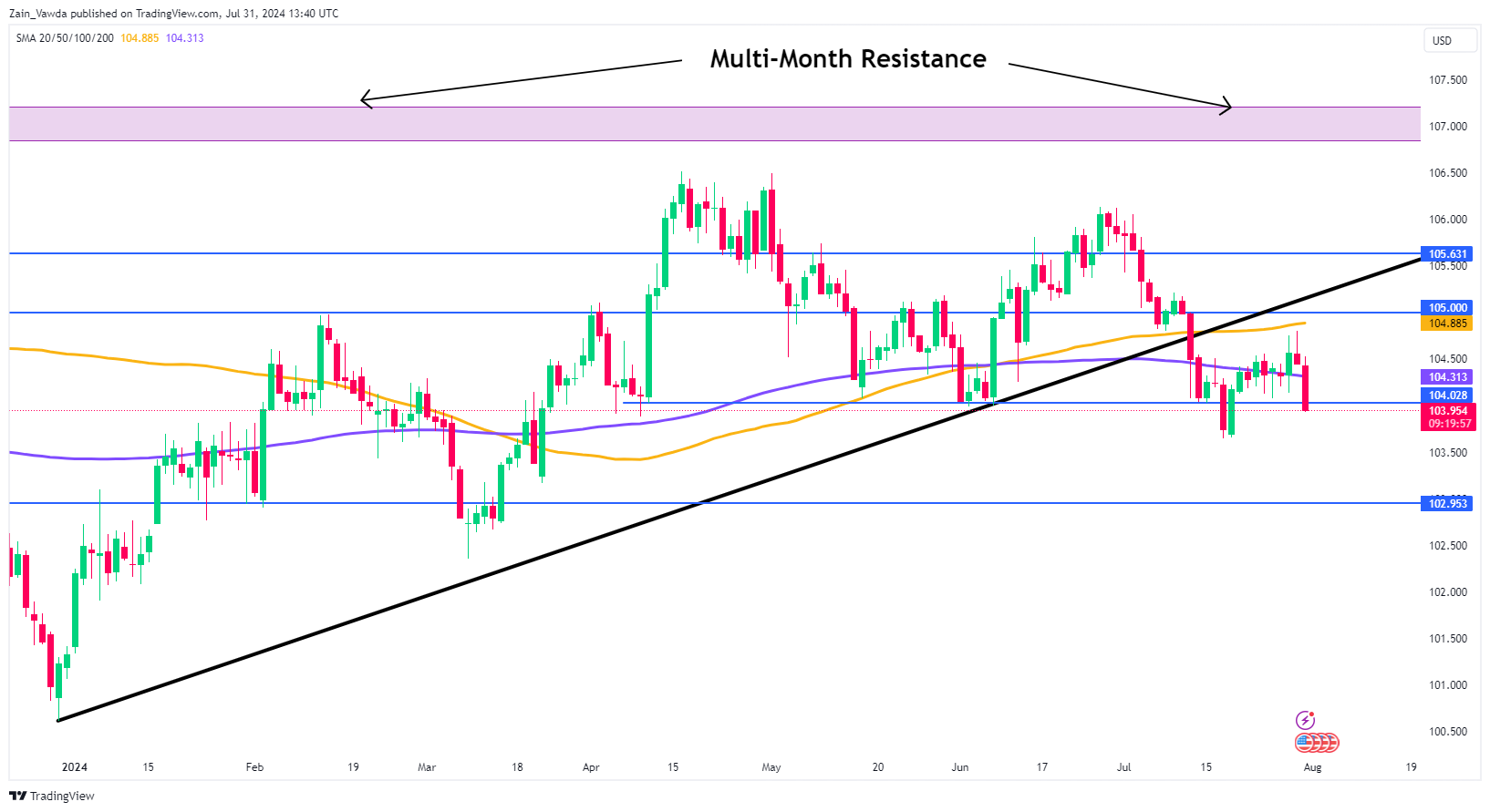

US Dollar Index

The Dollar Index (DXY) is at risk of a sharp decline following the FOMC meeting, with much depending on the Fed’s rhetoric. However, the technical outlook appears concerning.

After breaking the long-term ascending trendline, the DXY experienced some consolidation and a brief retracement earlier in the week. As the FOMC meeting approaches, the selloff has resumed.

The DXY is currently breaking through support at the 104.00 level, with further support found at the recent lows of 103.65. Should it break lower, the 103.00 level comes into focus.

Conversely, a move higher from this point faces immediate resistance at 104.313, followed by the resistance level at 104.88 (100-day moving average), which is just below the psychological 105.00 mark.

US Dollar Index Daily Chart, July 31, 2024

Source: TradingView (click to enlarge)

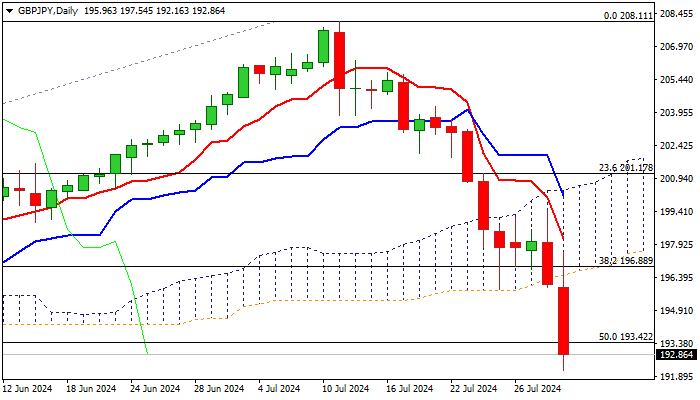

GBP/JPY Accelerates Lower After BoJ Rate Hike

GBPJPY extends steep downtrend by dropping 1.7% on Wednesday and on track for the biggest daily drop since 12 July 2023, after BOJ rate hike further boosted yen, while sterling remains deflated by growing expectations that BoE would deliver a 25 basis points rate cut tomorrow.

Markets also focus on today’s Fed rate decision at the end of two-day policy meeting, expecting Chair Powell to add to expectations for three rate cuts by the end of the year, with cycle likely to start in September.

Fresh acceleration lower brought the price well below ascending daily cloud (spanned between 196.50 and 200.39) and broke below 50% retracement of 178.73/208.11 (193.42) to hit the lowest since early May.

Bears pressure next significant support at 191.66 (200DMA), where stronger headwinds could be expected, as daily studies are oversold.

Upticks should be capped under daily cloud base (196.50) to keep bears intact for fresh push lower and possible probe below 190 mark, as BoJ’s fresh hawkishness and dovish BOE, would continue to weigh on the pair.

Res: 193.42; 195.04; 196.50; 197.37

Sup: 191.66; 191.35; 190.29; 189.95

Sunset Market Commentary

Markets

The biggest moves in markets ahead of tonight’s Fed policy meeting happened in the Japanese yen. A not completely expected rate hike to 0.25% by the Bank of Japan this morning, accompanied by a bond taper programme, took some investors off guard. In a hawkish presser afterwards, governor Ueda said that if the economy evolves according to the outlook, more rate hikes will follow, possibly beyond neutral (+/-0.5%). Ueda added that the weak currency was an argument to raise the rate today, along with increased confidence of a consumer-driven sustained return to the 2% inflation target. USD/JPY is testing the 150 barrier, the lowest level since mid-March on JPY strength (rather than USD-weakness that drove much of the recent USD/JPY decline). European markets eyeballed the EMU inflation print. Prices in July evolved in a not so comfortable way for the ECB. The headline figure was flat m/m, allowing the y/y figure to unexpectedly pick up from 2.5% to 2.6%. Core inflation stood at a June-matching 2.9%, defying expectations for a minor deceleration. And services inflation, lastly, barely eased from the 4.1% in June to 4% this month – a level deemed too high to reconcile with the ECB’s overall 2% target. An attempt of European/German yields to reverse earlier declines quickly faded to nothing and returned towards intraday lows. Net daily changes vary between 3.2-3.8 bps. The euro did hold on to some minor gains against the dollar (EUR/USD around 1.084) as the former was weighed down by a drop in US yields as well (2-4 bps)-. Q2 Employment Cost Index – the Fed’s preferred wage measure - came in a tad below consensus, ie 0.9% vs 1% (4.1% y/y, the slowest advance since 2021). Both wages & salaries (the base compensation component) as well as benefits eased compared to the previous quarter, suggesting moderating wage growth in a ditto labour market. The latter was also confirmed by the ADP job report printing at sub-par 122k.

We are now headed towards tonight’s FOMC meeting. The Fed’s status quo at 5.25-5.5% is widely anticipated. The central question is whether the recent string of beneficial CPI outcomes and mostly below-consensus economic outcomes will prompt clearer clues towards a first cut (in September) in either the statement or the presser. We think there’s a possibility of that to happen, be it subtle in order to prevent the recent sharp yield correction go much further against the background of thinner liquidity circumstances and technical support zones at the verge of breaking. Complementing the case for (short-term) yields not to drop much lower from current levels is the current pricing in money markets (almost three cuts priced in for 2024). The four cuts for 2025, as things currently stand, seem appropriate as well. First support for the dollar kicks in at EUR/USD 1.09. That should hold.

News & Views

Polish inflation in July came in to the soft side of expectations. While the monthly reading quickened sharply from 0.1% to 1.4%, it fell short of a 1.6% consensus estimate. On a yearly basis, the number picked up from 2.6% to a 2024 high of 4.2%. That undershot expectations by 0.2 ppts but is nevertheless well above the central bank’s 2.5% +/- 1 ppt target. The few details made available by Poland Statistics showed that electricity, gas and other utilities drove the dramatic increase (+11.8% m/m). This was the result of the government’s decision to raise the energy cap for the second half of 2024. This will affect all upcoming readings on a similar basis and is one of the reasons for the hawkish monetary policy stance. The majority of the MPC council agrees that no cuts are appropriate this year with governor Glapinski at some point ruling out 2025 as well. Council member Wnorowski in a first reaction after the release said that inflation at the beginning of next year could pick up further but said he sees reasons for discussions about cuts to start in 2025Q2. The Polish zloty trades little chanced around EUR/PLN 4.29.

Following up on the US Treasury announcing the updated borrowing estimates for the running (and upcoming) quarter, the agency today released quarterly refunding statement detailing the borrowing strategy. The US Treasury expects that, based on current projected borrowing needs, it does not have to increase auction sizes for at least the next several quarters. With the exception of the August refinancing round (temporary $3 bn uptick in the 7-yr, 10-yr and 30-yr auction size), all other auction sizes were left unchanged at least through October 2024. That means the financing strategy remains tilted towards short(er) maturities with monthly sizes ranging from $58 to $70bn.

Graphs

US 2-yr yield reaches make or break moment

AUD/USD: Aussie dollar erases much of the CPI-driven weakness as US counterpart remains unconvincing

Brent ($/b) snaps losing streak as geopolitical concerns flare up (Israeli retaliatory attack in Lebanon)

Japanese 2-yr yield shoots to highest level in 15 years as central bank hiked and flags more to come, conditional on eco developments

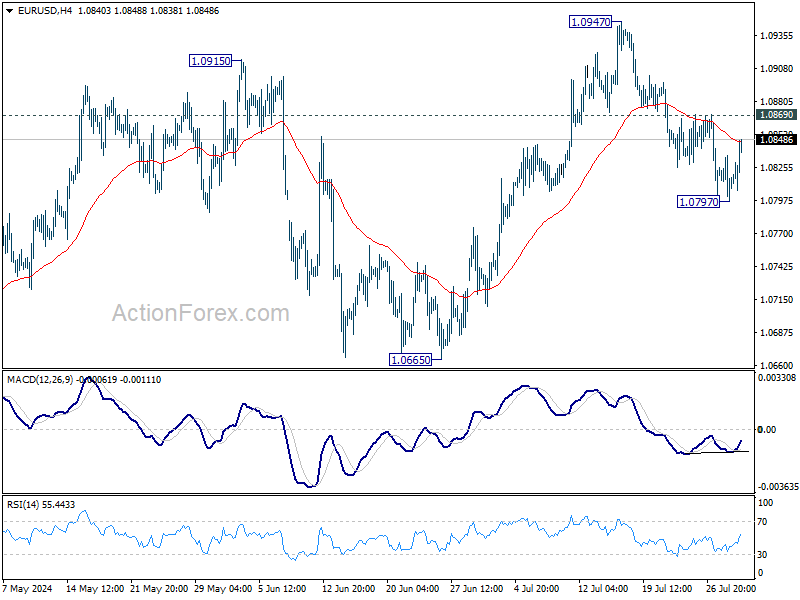

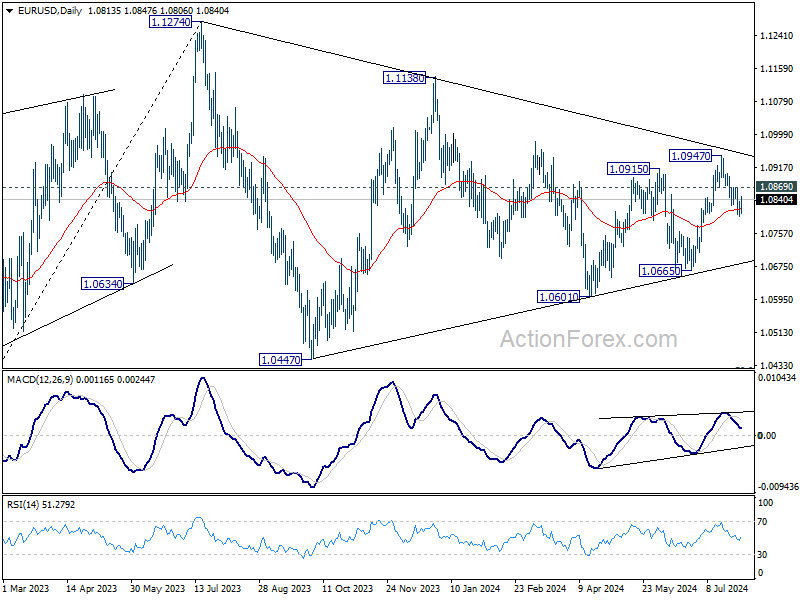

EUR/USD Outlook: Rises on EU CPI and US Labor Data, Bear-Trap Forming on Daily Chart

EURUSD bounced on Wednesday after a triple rejection at 1.0800 support zone (50% retracement of 1.0666/1.0948 rally/daily Kijun-sen) signals formation of a bear-trap.

Fresh gains were sparked by higher than expected EU inflation numbers in July which improved Euro’s sentiment and below expectations US ADP private sector payrolls signaling softening in US labor market and adding to Fed rate cut narrative.

Markets shift focus to the key event of the day – FOMC rate decision. The US central bank is expected to stay on hold in July policy meeting, but to provide more hints about their next steps at Chair Powell’s press conference.

The Fed is widely expected to start cutting interest rates from September, with more signals from the central bank, to deflate dollar and further boost the single currency.

Technical picture on daily chart is mixed (conflicting MA’s, negative momentum and north-heading RSI) and lacks clearer technical signal, although fresh gains point to development of reversal signal on daily chart.

However, such scenario will need confirmation, with lift and close above 1.0850 zone (falling 10DMA / Fibo 38.2% of 1.0948/1.0798 bear-leg) seen as minimum requirement to validate bullish signal and expose upper pivots at 1.0870 zone (lower platform / 50% retracement).

Only sustained break below 1.0800 pivot would neutralize fresh bulls and signal continuation of larger downtrend from 1.0948 (July 17 top).

Res: 1.0850; 1.0870; 1.0890; 1.0902.

Sup: 1.0807; 1.0800; 1.0773; 1.0732.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0797; (P) 1.0816; (R1) 1.0835; More.....

Intraday bias in EUR/USD is turned neutral with current recovery. But further decline is expected with 1.0869 resistance intact. Sustained break of 55 D EMA (now at 1.0815) will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947. Deeper decline should then be seen to 1.0601/0665 support zone next. Nevertheless, break of 1.0869 minor resistance will bring retest of 1.0947 instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

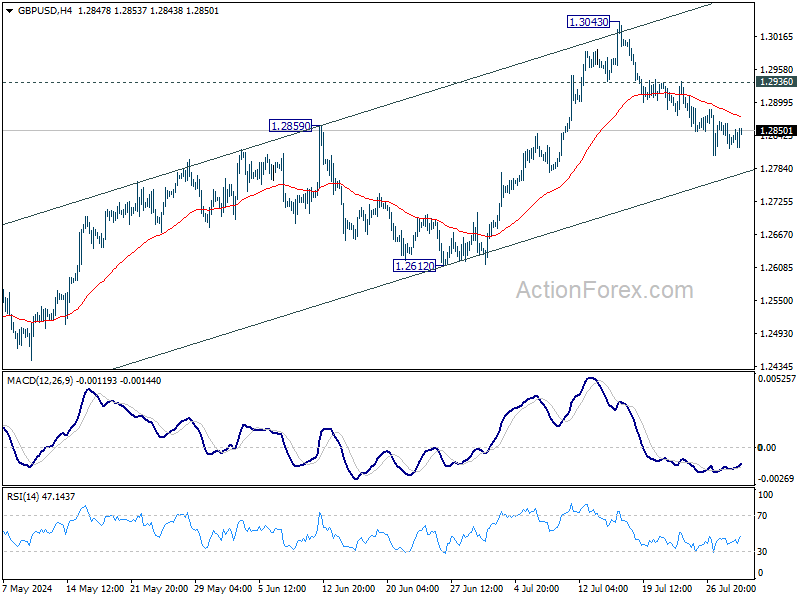

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2815; (P) 1.2841; (R1) 1.2863; More...

GBP/USD is losing downside momentum as seen in 4H MACD. But further decline is still expected with 1.2936 resistance intact. Decisive break of 55 D EMA (now at 1.2781) will suggest that rise from 1.2298 has completed with three waves up to 1.3043. Deeper fall would be seen to 1.2612 support and below. On the upside, above 1.2936 resistance will bring retest of 1.3043 resistance instead.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022. However, break of 1.2612 support argue that this corrective pattern is extending with another falling leg.

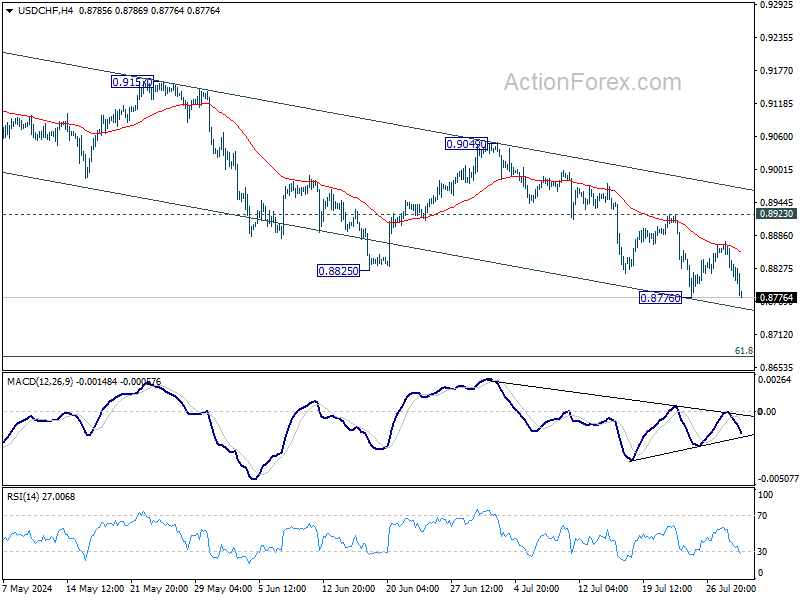

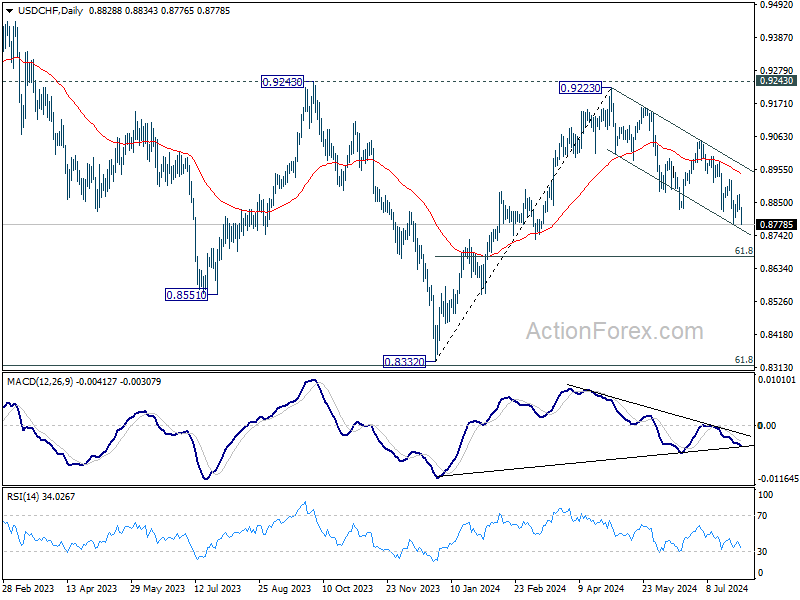

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8810; (P) 0.8843; (R1) 0.8860; More…

USD/CHF is holding above 0.8776 support despite today's dip and intraday bias remains neutral. More consolidations could still be seen but further decline is expected as long as 0.8923 resistance holds. On the downside, break of 0.8776 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. However, break of 0.8923 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

Canada’s Economy Advanced in May, Modest Growth Expected in June

The Canadian economy grew for a second consecutive month, up by 0.2% month-on-month (m/m). This print landed ahead of Statistics Canada's advanced guidance and market expectations of a 0.1% m/m gain. The flash estimate for June points to a 0.1% m/m gain.

May's reading was broad-based, with output expanding in 15 of 20 industries. Goods-producing industries (0.4% m/m) did most of the heavy lifting, meanwhile growth in services was up a more modest 0.1% m/m.

On a weighted basis, the manufacturing sector contributed most to the overall gain in May's GDP, and was up for a consecutive month (+1.0% m/m). The oil & gas sector (-0.6% m/m) was the only goods industry to contract on the month, pulled lower by declines in the oil and gas extraction subsector.

On the services side, education, health care, and public admin all grew between 0.3%–0.5% m/m. The startup of the Transmountain pipeline helped pull the transportation sector forward by 0.1% m/m in May. On the downside, retail trade fell by 0.9% on the month with most subsectors seeing declines.

The advanced reading of 0.1% m/m growth in June is being driven by gains in the construction, real estate and finance sectors, with manufacturing and wholesale trade acting as a headwind.

Key Implications

GDP data for May came in a bit stronger than expectations, which has put second quarter growth tracking around 2.2%, which if realized, would be the fastest quarter of growth since Q2-2022. The Canadian economy appears to be showing some resilience in the second quarter led by a strong showing in the goods sectors. Advanced guidance for June suggests that current strength may not be sustained.

GDP readings of late have been relatively stable, allowing the Bank of Canada to keep its focus more squarely on the evolution of inflation, especially with the start of its interest rate easing cycle well underway. With two interest rate cuts under its belt–and likely a couple more this year–we'd expect the growth backdrop to continue to be supported. The BoC is particularly upbeat about third quarter growth (2.8% q/q annualized), but we expect the weight of still-high interest rates to result in more trend-like growth next quarter.

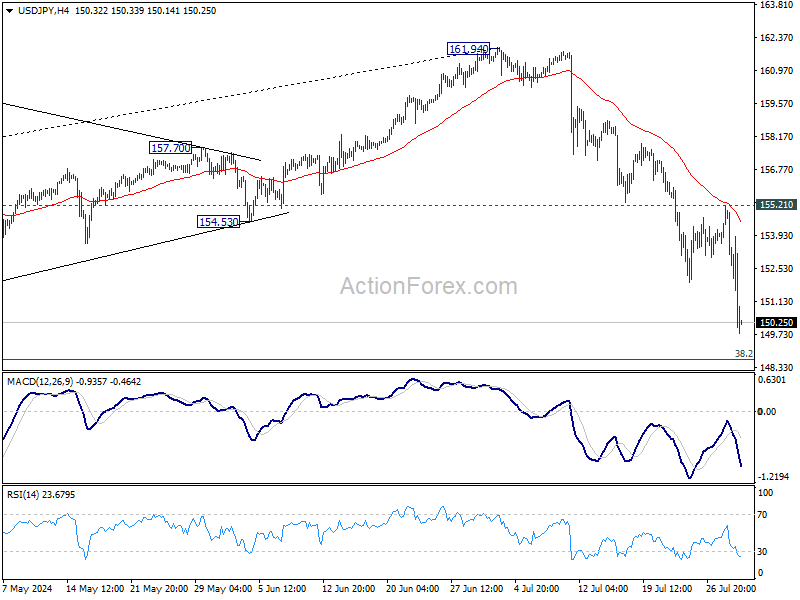

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.86; (P) 153.54; (R1) 154.43; More...

USD/JPY's fall from 161.94 accelerates lower again to as low as 149.77 so far. Intraday bias stays on the downside for 148.66 fibonacci level, which is close to medium term channel support (now at 148.22). Strong support could be seen there to bring rebound. But break of 155.21 resistance is needed to confirm short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Next target is 38.2% retracement of 127.20 to 161.94 at 148.66. Decisive break there will pave the way to 140.25 support next. Risk will now stay on the downside as long as 55 D EMA (now at 156.90) holds, in case of rebound.

Dollar Dips on Weak ADP While Yen Marches On, Market Awaits FOMC

Dollar dipped as weaker-than-expected ADP job data hit the market entering US session. However, the movement has been limited with traders bracing for FOMC rate decision. Fed is widely expected to keep its policy rate unchanged at 5.25-5.50% today. The main focus is whether Fed will signal enough "confidence" to start cutting interest rates in September, a move that markets have fully priced in. Nonetheless, there is a risk that Chair Jerome Powell might sound non-committal, emphasizing that future decisions will remain data-dependent. Recent economic data, including Q2 GDP, suggest that economic activities are just normalizing without a sharp slowdown, suggesting that Fed is not in a hurry for policy loosening.

Euro saw a slight bounce following stronger-than-expected headline and core inflation readings. The headline CPI has reaccelerated slightly, and core CPI did not slow for the third straight month. There remains one more inflation report before ECB meets on September 11-12, making it premature to conclude that ECB won't consider another rate cut. However, today's data complicate the decision.

Meanwhile, Yen remains the strongest performer of the day. Yen surged after BoJ raised interest rates for the second time this year, extending gains after Governor Kazuo Ueda's press conference. Ueda emphasized that 0.50% interest rate won't be the ceiling, as the central bank will continue to hike if the economy and prices align with its projections. He did not rule out further tightening this year, stating it would depend on incoming data, such as services inflation, inflation expectations, and overall demand and output gap. Ueda also noted that while Yen's depreciation hasn't altered economic forecasts, there is a "significant risk" of a weak yen leading to an overshoot of inflation.

Australian Dollar is the worst performer today following Q2 inflation data, which showed slowdown in the core measure. This data should be welcomed by RBA, reducing the pressure to hike interest rates again. Indeed, markets are now pricing in a 65% chance of a rate cut by year-end, compared to 30% chance of a hike next week before the data.

Technically, a key level to watch today for the rest of the US session is 1.0869 minor resistance in EUR/USD. Firm break there will argue that fall from 1.0947 has completed as a corrective move, after drawing support from 55 D EMA. In this case, rise from 1.0601 would be ready to resume through 1.0947 towards 1.1138 resistance. Nevertheless, rejection by 1.0869 will set the stage for deeper fall back to 1.0665 support next.

In Europe, at the time of writing, FTSE is up 1.20%. DAX is up 0.56%. CAC is up 1.09%. UK 10-year yield is down -0.052 at 3.998, below 4% handle. Germany 10-year yield is down -0.033 at 2.311. Earlier in Asia, Nikkei rose 1.49%. Hong Kong HSI rose 2.01%. China Shanghai SSE rose 2.06%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield rose 0.0644 to 1.061.

Canadian GDP grows by 0.2% mom in May, exceeds expectations

Canada's GDP grew by 0.2% mom in May, surpassing the expected 0.1% mom growth. The primary driver of this growth was the goods-producing industries, which saw a 0.4% increase with four out of five sectors expanding. The services-producing industries also contributed, albeit modestly, with a 0.1% rise. Overall, 15 out of 20 sectors experienced growth.

Advance information suggests that real GDP increased by 0.1% mom in June. Gains in construction, real estate and rental and leasing, and finance and insurance were partially offset by declines in manufacturing and wholesale trade.

US ADP employment grows only 122k, wages growth slows further

In July, US ADP private employment grew by 122k, significantly below the expected 166k. Breaking it down by sector, goods-producing jobs increased by 37k, while service-providing jobs rose by 85k. By establishment size, small companies lost -7,000k, medium-sized companies added 70k jobs, and large companies added 62k jobs.

Annual pay gains for job-stayers slowed to 4.8% yoy, the lowest rate in three years. Annual pay growth for job-changers also dropped significantly from 7.7% yoy to 5.2% yoy.

Nela Richardson, chief economist at ADP, commented, "With wage growth abating, the labor market is playing along with the Federal Reserve's effort to slow inflation. If inflation goes back up, it won't be because of labor."

Eurozone CPI rises to 2.6% yoy in Jul, core CPI unchanged at 2.9% yoy

Eurozone CPI rose from 2.5% yoy to 2.6% yoy in July, above expectation of 2.4% yoy. Core CPI (ex-energy, food, alcohol & tobacco) was unchanged at 2.9% yoy, above expectation of 2.8% yoy.

Looking at the main components, services is expected to have the highest annual rate in July (4.0%, compared with 4.1% in June), followed by food, alcohol & tobacco (2.3%, compared with 2.4% in June), energy (1.3%, compared with 0.2% in June) and non-energy industrial goods (0.8%, compared with 0.7% in June).

BoJ hikes to 0.25%, signals more increases if outlook realizes

BoJ raised the uncollateralized overnight call rate from 0-0.10% to around 0.25% today. The decision was made by a 7-2 vote, with dissenting votes from Toyoaki Nakamura and Asahi Noguchi, who preferred to gather more information and conduct a careful assessment before adjusting the interest rate.

Regarding JGB purchases, there was a unanimous decision to reduce the amount of monthly outright purchases to about JPY 3T by Q1 2026. The amount will be cut by JPY 400B each calendar quarter.

BoJ stated that economic activity and prices have been "developing generally in line with the Bank's outlook." Moves to raise wages have been spreading, and the annual rate of import price growth has "turned positive again," with upside risks to prices requiring attention.

It also noted if the outlook presented in the July Outlook Report is realized, BoJ will continue to raise the policy interest rate and adjust the degree of monetary accommodation accordingly.

In the new economic projections, the BoJ made several adjustments:

- Fiscal 2024 growth forecast was lowered from 0.8% to 0.6%.

- Fiscal 2025 growth forecast remains unchanged at 1.0%.

- Fiscal 2026 growth forecast remains unchanged at 1.0%.

For inflation projections:

- Fiscal 2024 CPI core forecast was lowered from 2.8% to 2.5%.

- Fiscal 2025 CPI core forecast was raised from 1.9% to 2.1%.

- Fiscal 2026 CPI core forecast remains unchanged at 1.9%.

- Fiscal 2024 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2025 CPI core-core forecast remains unchanged at 1.9%.

- Fiscal 2026 CPI core-core forecast remains unchanged at 2.1%.

Australia's trimmed mean CPI drops to 3.9%, continuing six-quarter downtrend

In Q2, Australia's CPI rose by 1.0% qoq, matching both expectations and the pace set in Q1. Annual rate increased from 3.6% to 3.8% , also in line with forecasts.

More notably, the core inflation measure marked its sixth consecutive quarter of cooling. Trimmed mean CPI, which is a key indicator of underlying inflation, rose by 0.8% qoq. This represents a slowdown from the prior quarter's 1.0% qoq increase and falls below the expected 0.9% qoq. Annually, trimmed mean CPI slowed from 4.0% yoy to 3.9% yoy, below the expected 4.0% and continuing its downward trend from the peak of 6.8% in the December 2022 quarter.

Additionally, the monthly CPI for June slowed from 4.0% yoy to 3.8% yoy, again matching expectations.

NZ ANZ business confidence jumps to 27.1, inflation expectations fall further

In July, New Zealand's ANZ Business Confidence saw a notable increase, jumping from 6.1 to 27.1. Own Activity Outlook also improved, rising from 12.2 to 16.3. Meanwhile, cost expectations fell slightly from 69.2 to 68.2, and wage expectations edged up from 73.5 to 74.6. Pricing intentions saw an increase from 35.3 to 37.6. Importantly, inflation expectations continued their steady decline, falling from 3.46% to 3.20%.

ANZ commented that the economic climate remains one where "bad news is good news" for RBNZ. With mounting evidence that monetary policy has been effective, perhaps overly so, there is now a broad expectation that RBNZ will start easing the Official Cash Rate this year.

ANZ noted that "evidence is mounting that the inflation dragon is on its last legs," which positions the New Zealand economy for a more robust recovery compared to a scenario where inflation control efforts were only partially successful.

China's NBS PMI manufacturing falls to 49.4 in amid weak demand and extreme weather

China's official NBS PMI Manufacturing index fell slightly from 49.5 to 49.4 in July, just above the expected 49.3. This index has remained below the 50-mark, which separates growth from contraction, for all but three months since April 2023.

NBS analyst Zhao Qinghe attributed the decline in manufacturing activity to the typical off-season for production in July, insufficient market demand, and extreme weather conditions such as high temperatures and floods in some areas.

PMI Non-Manufacturing index also fell, dropping from 50.5 to 50.2, in line with expectations, but still indicating expansion for the 19th consecutive month. Within this category, construction subindex decreased from 52.3 to 51.2, while services subindex slipped from 50.2 to 50e.

Overall, the official PMI Composite, which combines both manufacturing and non-manufacturing sectors, declined from 50.5 to 50.2.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.86; (P) 153.54; (R1) 154.43; More...

USD/JPY's fall from 161.94 accelerates lower again to as low as 149.77 so far. Intraday bias stays on the downside for 148.66 fibonacci level, which is close to medium term channel support (now at 148.22). Strong support could be seen there to bring rebound. But break of 155.21 resistance is needed to confirm short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Next target is 38.2% retracement of 127.20 to 161.94 at 148.66. Decisive break there will pave the way to 140.25 support next. Risk will now stay on the downside as long as 55 D EMA (now at 156.90) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | -13.80% | -1.70% | -1.90% | |

| 23:50 | JPY | Industrial Production M/M Jun P | -3.60% | -4.20% | 3.60% | |

| 23:50 | JPY | Retail Trade Y/Y Jun | 3.70% | 3.30% | 2.80% | |

| 01:00 | NZD | ANZ Business Confidence Jul | 27.1 | 6.1 | ||

| 01:30 | AUD | Monthly CPI Y/Y Jun | 3.80% | 3.80% | 4.00% | |

| 01:30 | AUD | CPI Q/Q Q2 | 1.00% | 1.00% | 1.00% | |

| 01:30 | AUD | CPI Y/Y Q2 | 3.80% | 3.80% | 3.60% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q2 | 0.80% | 0.90% | 1.00% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q2 | 3.90% | 4.00% | 4.00% | |

| 01:30 | AUD | Retail Sales M/M Jun | 0.50% | 0.30% | 0.60% | |

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.60% | 0.40% | ||

| 01:30 | CNY | NBS Manufacturing PMI Jul | 49.4 | 49.3 | 49.5 | |

| 01:30 | CNY | NBS Non-Manufacturing PMI Jul | 50.2 | 50.2 | 50.5 | |

| 03:57 | JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | 0.10% | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -6.70% | -2.00% | -5.30% | |

| 05:00 | JPY | Consumer Confidence Jul | 36.7 | 36.5 | 36.4 | |

| 06:00 | EUR | Germany Import Price Index M/M Jun | 0.40% | 0.10% | 0.00% | |

| 07:55 | EUR | Germany Unemployment Change Jul | 18K | 16K | 19K | |

| 07:55 | EUR | Germany Unemployment Rate Jul | 6.00% | 6.00% | 6.00% | |

| 08:00 | CHF | UBS Economic Expectations Jul | 9.4 | 17.5 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 2.60% | 2.40% | 2.50% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 2.90% | 2.80% | 2.90% | |

| 12:15 | USD | ADP Employment Change Jul | 122K | 166K | 150K | 155K |

| 12:30 | USD | Employment Cost Index Q2 | 0.90% | 1.00% | 1.20% | |

| 12:30 | CAD | GDP M/M May | 0.20% | 0.10% | 0.30% | |

| 13:45 | USD | Chicago PMI Jul | 44.1 | 47.4 | ||

| 14:00 | USD | Pending Home Sales M/M Jun | 1.60% | -2.10% | ||

| 14:30 | USD | Crude Oil Inventories | -1.6M | -3.7M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |