Sample Category Title

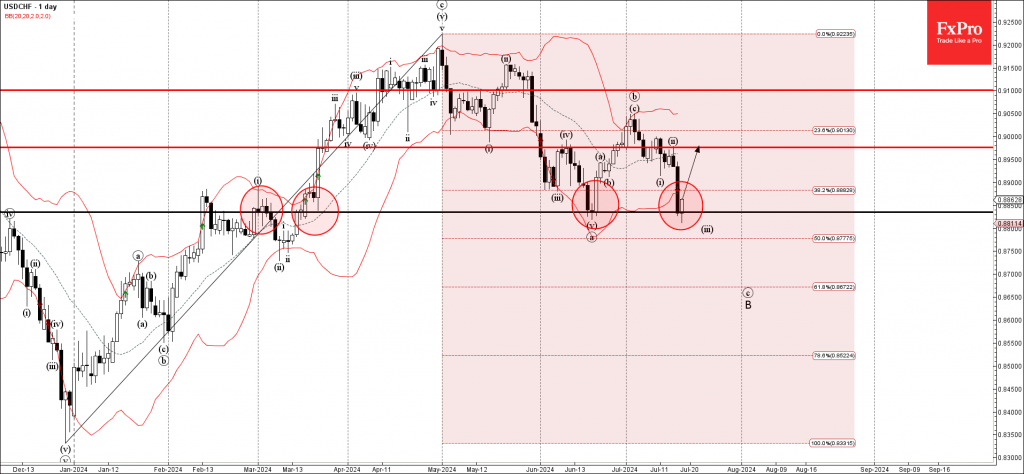

USDCHF Wave Analysis

- USDCHF reversed from support area

- Likely to rise to resistance level 0,9000

USDCHF currency pair today reversed up from the support area located between the key support level 0.8835 (which created the Morning Star in June), 38.2% Fibonacci correction of the upward impulse from December and the lower daily Bollinger Band.

The upward reversal from this support area stopped the previous waves c and B.

Given the strength of the support level 0.8835, USDCHF currency pair can be expected to rise further to the next resistance level 0,9000 (top of the previous correction ii).

ECB Review: A ‘Wide Open’ September Meeting

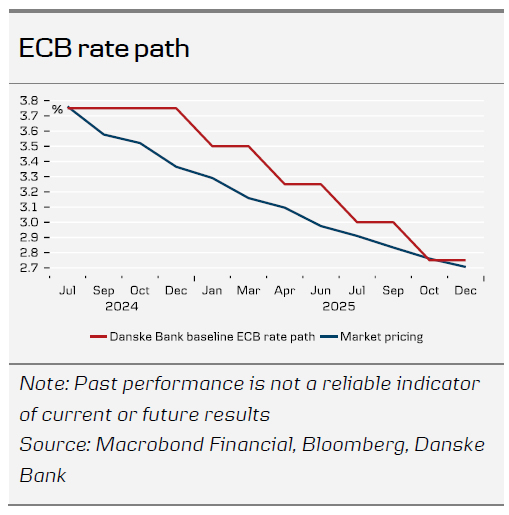

Today, the ECB held its policy rates unchanged, as unanimously expected by markets and analysts. The central bank did not send any signals for the September decision, where it repeated its call for a data-dependent and meeting-by-meeting approach. During the Q&A, Lagarde said that the "question of September and what we do in September is wide open", although markets do not share that view, pricing a 25% rate cut probability at 80%. We find the 2025 pricing of 84bp on the slightly dovish slide of expectations. We expect four more rate cuts by the ECB until end-2025.

Nothing (really) new…

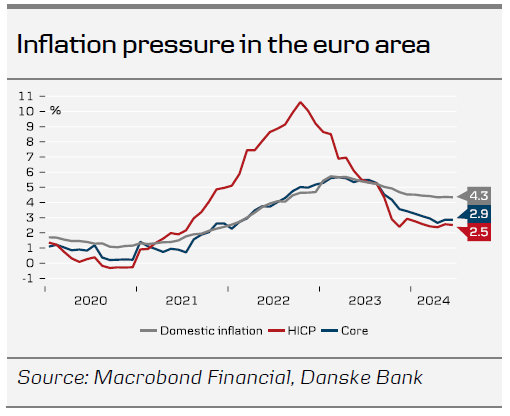

As widely expected, the ECB meeting did not carry new policy signals. We did not expect that either given the limited new information that the ECB has received since the June ECB meeting. The decision statement was balanced with a key paragraph to both the dovish and the hawkish camp of the ECB. The statement read; "While some measures of underlying inflation ticked up in May owing to one-off factors, most measures were either stable or edged down in June", as well as, "domestic price pressures are still high, services inflation is elevated and headline inflation is likely to remain above the target well into next year". The inflation assessment was largely unchanged, yet we took note of the slight adjustment in the risk picture for growth, which is now titled to the downside (in June it was balanced in the short-term and to the downside in the medium-term). During the press conference Lagarde said that arguments on the "one hand and on the other hand" were discussed, thus leading us to conclude that this will be remembered as a stock taking meeting. With no new policy signals, Lagarde ended the press conference with greetings for the "vacation and summer break".

… as key data is only coming ahead of the September meeting

The ECB's modus-operandi of taking a meeting-by-meeting and data-dependent approach on a three-tiered reaction function (inflation outlook, underlying inflation, and strength of transmission mechanism) means that incoming information ahead of September will be important. In particular the triangulation between wages, productivity, and profits will play a key role in whether the ECB will hold or cut in September, which Lagarde also highlighted today. The key dates to watch are 14 August for productivity, 22 August for negotiated wages, and 6 September for both compensation per employee and profits data. The meeting is scheduled for 12 September. In addition, we will have the flash inflation for July and August, and the final inflation for July. The latter in particular is key given that this allows to compute the domestic inflation pressure that features prominently in the ECB's underlying inflation discussion. We see this still printing in excess of 4% at the timing of the September meeting. In September, we will also get new staff projections.

Our median baseline of no September rate cut still holds, which is built on a combination of the strength of the labour market, sticky underlying inflation, and the recovery of the euro area growth. We repeat that a key risk to our ECB September rate call is whether the Fed will cut in September, and whether this adds 'political' pressure to cut rates as well, despite the sticky underlying inflation. We find the September rate cut case more compelling in the US (and in light of Powell's comments this week) than in the euro area.

Subdued market response following no new policy signals

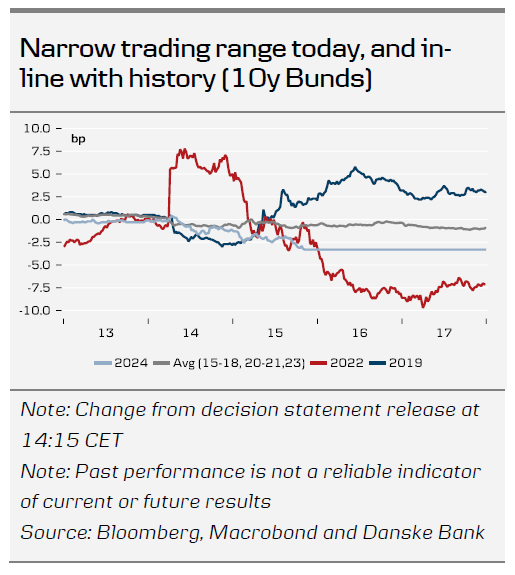

The ECB meeting did not notably affect the bond or the FX markets as expected. 10y Bunds traded in a narrow range of less than 1bp around 2.43%. The EUR/USD remained steady in the 1.0900-1.0950 range throughout the announcement and the press conference. With limited new information since the ECB's first rate cut in this round six weeks ago, the ECB hardly had any reason to send new monetary policy signals ahead of the September meeting.

The next catalysts for the markets are the July flash PMIs for both the US and the euro area, the FOMC meeting on 31 July, and the US jobs report at the beginning of August, alongside developments in US politics. Concerns about euro area debt, spurred by the French election, have largely subsided following the "hung parliament."

Overall, even though we disagree with the market and think the ECB will stay on hold at the September meeting and only deliver one more cut this year, we believe that fundamental factors indicate a lower EUR/USD in the second half of the year. Despite recent softer US data, persistent US inflation and/or US growth outperformance in the second half could support the USD for the remainder of the year. We forecast EUR/USD to reach 1.05/1.03 in 6/12M.

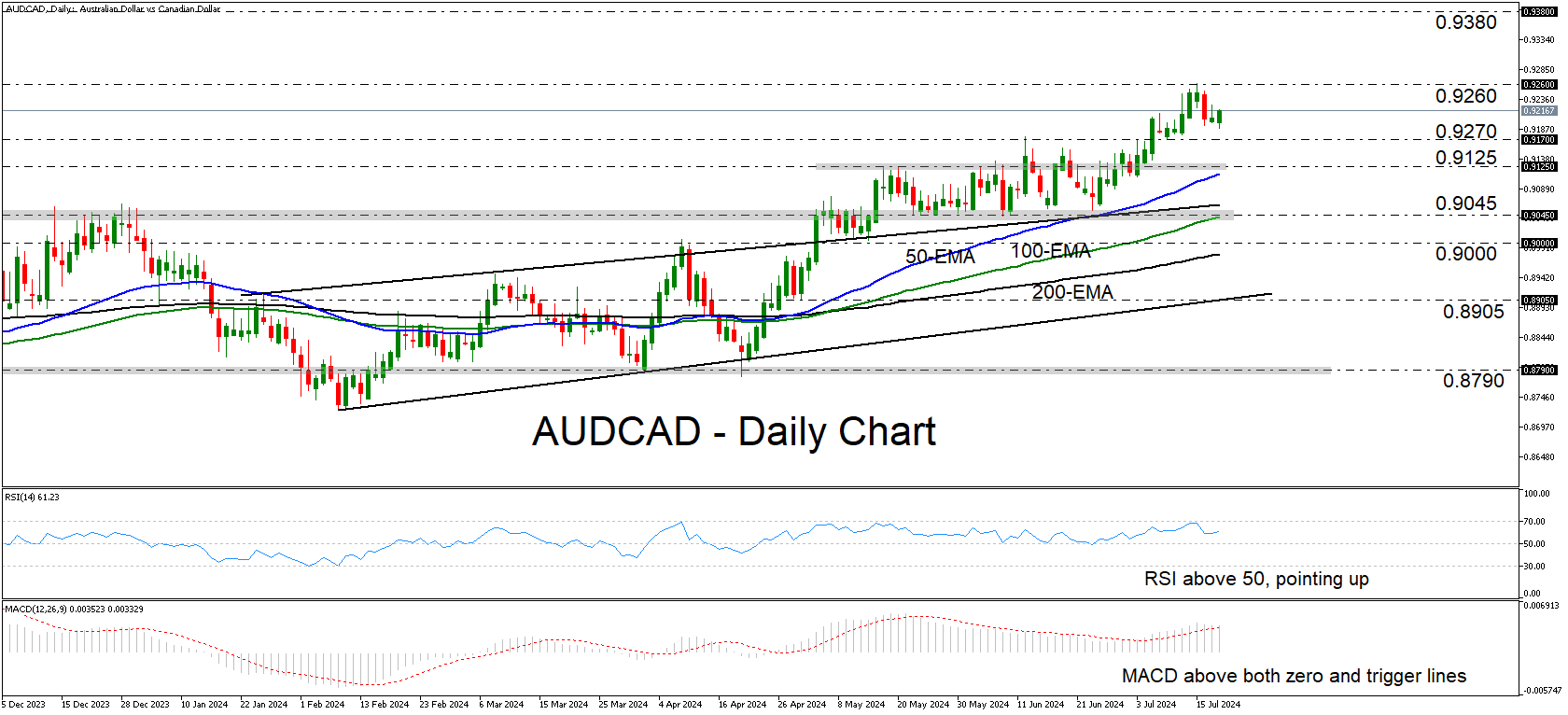

Is AUDCAD Ready to Extend Its Uptrend?

- AUDCAD prints higher highs and higher lows

- RSI and MACD detect positive momentum

- Break above 0.9260 could signal trend continuation

- Dip below 0.9125 may allow a decent correction

AUDCAD rebounded today from slightly above the support of 0.9270, marked by the low of July 9 and the inside swing high of June 12. Overall, the pair is printing higher highs and higher lows above all three of the plotted exponential moving averages (EMAs) on the daily chart, which paints a positive medium-term picture.

The RSI is lying above 50 and it is pointing up, while the MACD, although it shows some signs of slowing, it remains above both the zero and trigger lines. Both indicators are detecting positive momentum, which means that there is a decent chance for the uptrend to continue for a while longer.

If the bulls are willing to stay in the driver’s seat, they may soon challenge once again the 0.9260 zone, the break of which would confirm a higher high and perhaps pave the way towards the 0.9380 zone, marked by the high of February 2.

On the other hand, a dip below 0.9125 could signal a decent negative correction, perhaps towards the key support area of 0.9045, which acted as a temporary floor between May 20 and 27. That said, the trend would remain positive as the pair would still be trading above the prior upward sloping resistance (now support line) drawn from the high of January 25.

To sum up, AUDCAD continues trading in an uptrend and a decisive break above 0.9260 may confirm a trend continuation.

JPY Technical Outlook: Price Action on USD/JPY, GBP/JPY

- Japanese authorities have not confirmed whether they have intervened in the market to support the Yen.

- USD/JPY broke a long-term descending trendline but found support near the 100-day MA and 155.00 level.

- Price Action outlook and potential setups on USD/JPY and GBP/JPY.

Fundamental Overview

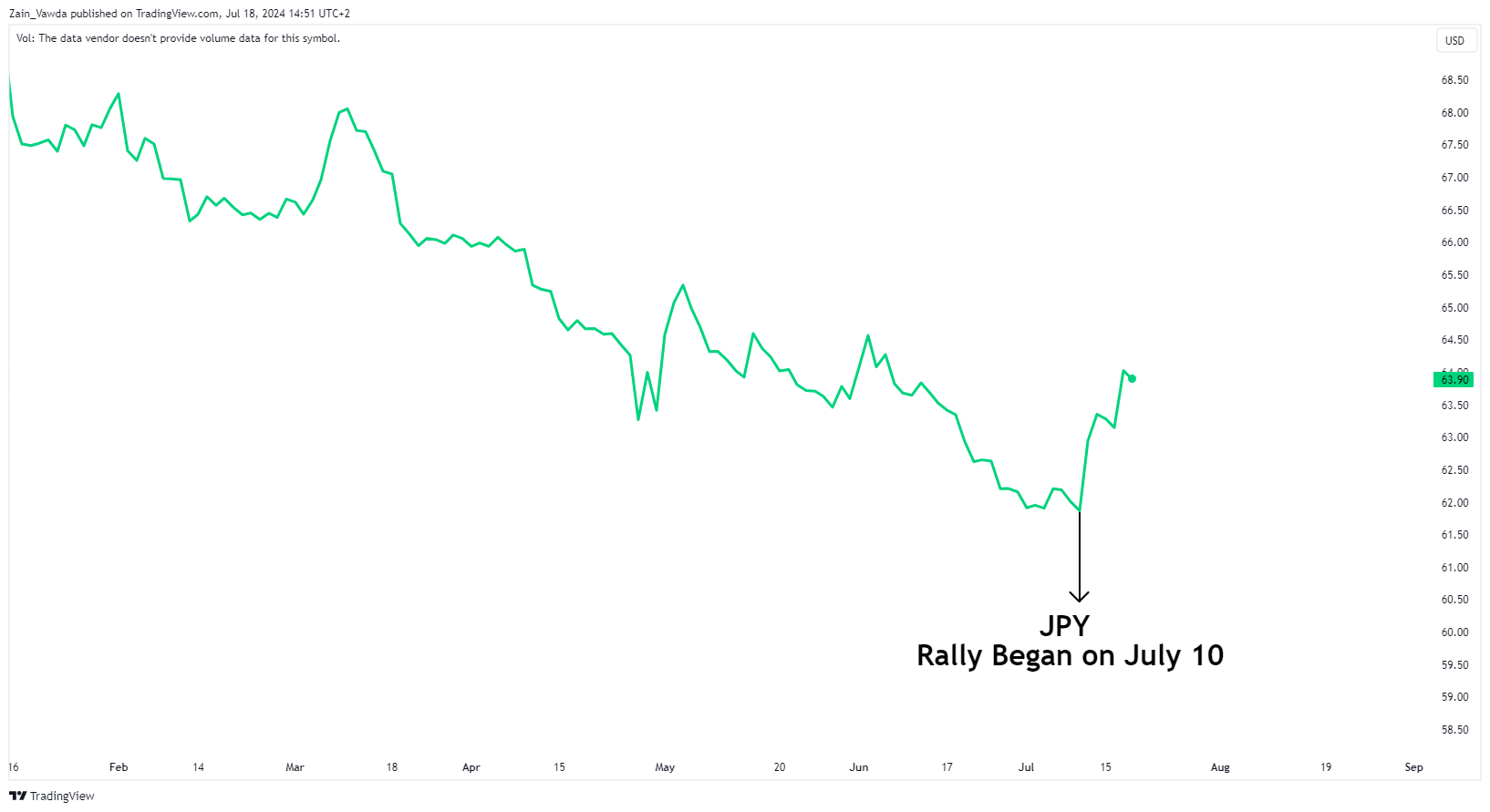

The Japanese Yen is enjoying a stellar week thanks in part to optimism around wage growth as well as rising rate cut optimism from the US Federal Reserve. The Yen rally has sparked talk of possible intervention for Japanese authorities who have refused to confirm whether intervention took place or not.

Earlier in the day, the release of the latest Bank of Japan (BoJ) did not show any immediate signs of intervention. According to Kazushige Kamiyama, a senior Bank of Japan (BoJ) official and the central bank’s Osaka branch manager, the BoJ would like to maintain an accommodative monetary environment as much as possible.

Money market data from last week did suggest that Authorities bought as much as 6 trillion Yen last week. This coupled with continued JPY strength has increased the belief of market participants that intervention has been ongoing during this week as well.

Japanese Yen Currency Index

Source:TradingView (click to enlarge)

Technical Analysis

USD/JPY

USD/JPY broke the long-term descending trendline which has been in play since December 2023. However, the pair does appear to have found support stopping just shy of the 100-day MA and key support area at the 155.00 handle.

Theoretically, breaking the trendline should result in further downside, especially with growing optimism around US rate cuts. However, historically, even when the Bank of Japan (BoJ) has intervened in the forex market, rapid gains by the Yen have often been quickly reversed.

Of course, past performance does not guarantee future results. Key resistance levels to watch include the 157.800 mark, which aligns closely with the trendline break. A retest and subsequent rejection of this level could signal further downside potential.

Alternatively a daily candle close above the 158.450 mark will see a shift in structure and likely put bulls back in the driving seat.

Support

- 155.00 (100-day MA)

- 153.59

- 152.00

Resistance

- 157.80

- 158.44

- 160.00

USD/JPY Daily Chart, July 18, 2024

Source: TradingView.com (click to enlarge)

GBP/JPY

Looking at GBP/JPY and the daily chart almost mirrors USD/JPY. Not surprising given the overarching narratives has been JPY weakness rather than appreciation of other currencies.

Dropping down to an H4 timeframe and we have a descending trendline that comes into focus which could cap further gains. A break above this trendline may face the 100-day MA resting at 204.945 with the next area of focus being the 206.00 handle.

Alternatively a rejection of the 100-day MA or trendline will first need to clear the 200-day MA which came to the support of GBP/JPY pair overnight. A break of this support could finally facilitate a move down toward the 200.00 psychological level.

GBP/JPY Daily Chart, July 18, 2024

Source: TradingView.com (click to enlarge)

Support

- 202.64

- 200.00

- 1.9750

Resistance

- 203.600

- 204.951

- 206.00

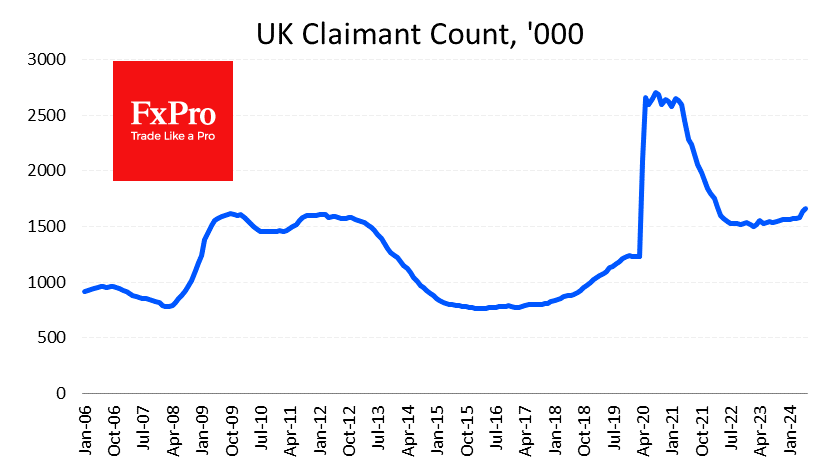

UK Jobs Data Cooled the Pound

The UK labour market is experiencing a cooling phase. The number of applications for unemployment benefits in June increased by 32.3K after a jump of 51.9K a month earlier. Prior to that, this indicator had been drifting for almost two years, adding an average of 2.5K per month.

The rise in claimant count claims may be evidence of worsening economic conditions, strengthening the hand of inflation doves on the Bank of England’s Monetary Policy Committee. In this regard, weaker-than-expected data caused pressure on GBPUSD, forcing it to retreat to 1.2980 against the highs recorded at 1.3040 a day earlier.

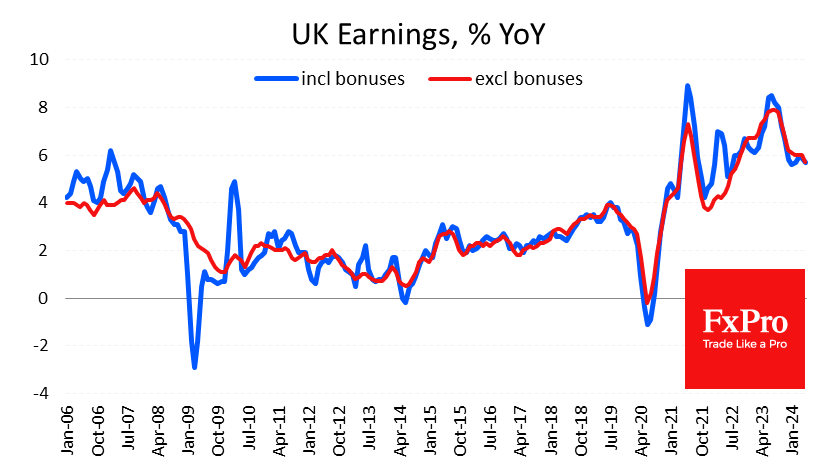

In parallel, data recorded a slowdown in wage growth, with the rate of growth decelerating to 5.7% 3m/y. In earnings excluding bonuses, this is a pullback to levels we last saw in September 2022, but it is still significantly above the norm, suggesting continued impressive domestic pressure on prices.

On balance, the published data noted that the economy is moving in the direction needed for the Bank of England to ease policy but is unlikely to force this as early as August. With the data in hand, it seems that the Central Bank may wait until mid-September or even early November.

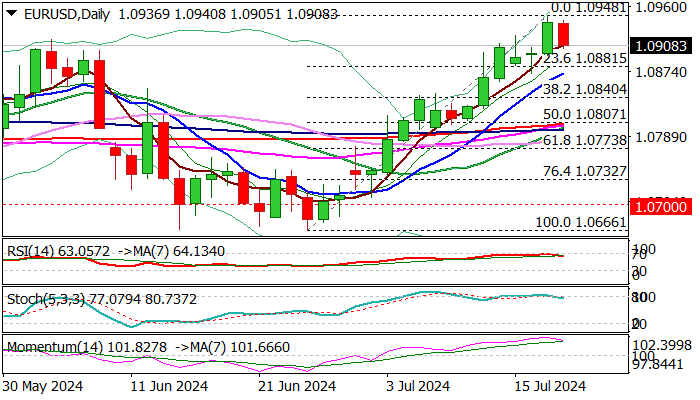

EUR/USD Outlook: Dips from New High Following ECB Decision

EURUSD eases further from new multi-week high (1.0948) as markets digested ECB’s decision to stay on hold and repeat its mantra that future action will be dependent on incoming economic data.

On the other hand, confidence that the ECB will deliver two more rate cuts by the end of the year continues to strengthen among market participants.

The EU policymakers are not happy with still high prices, which was the main argument for today’s decision, but remain on track for future rate cuts, as high borrowing costs are about to further hurt already damaged bloc’s economy.

From the technical point of view, current easing comes as a result of overbought conditions on daily chart, with limited dips to ideally find ground at 1.0870 (rising 10DMA) zone and not to exceed 1.0840 (Fibo 38.2% of 1.0666/1.0948) to mark a healthy correction.

Conversely, increased downside risk to be expected on loss of 1.0840/00 pivots (Fibo / psychological/converged DMA’s).

Res: 1.0948; 1.0981; 1.1000; 1.1017.

Sup: 1.0895; 1.0870; 1.0840; 1.0800.

Sunset Market Commentary

Markets

The ECB kept its key policy rates unchanged today in an unanimous decision. In its policy statement, the central bank repeats that it doesn’t pre-commit to a particular rate path. They follow a meeting-by-meeting and data-dependent approach to determining the appropriate level and duration of restriction. Unlike at the April meeting, there’s no clear hint that a new policy rate cut is granted for the September meeting. The April reference said: "if the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction." ECB President Lagarde kept her cards close to her chest during the Q&A session with the press as well. The ECB’s key concern is the strengthening of underlying core (and more specifically services) inflation. Also headline inflation is likely to remain above the target well into next year. The question of what the central bank does in September is wide open and will be based on all info they’ll receive in between. Also on this guidance, there seems to have been some kind of unanimity on the board. Recall that the ECB earlier this year announced that they would nonetheless close the gap between the deposit rate and the main refinancing rate from 50 bps currently to 15 bps. The spread between the MRO and the penalty lending rate will stay unchanged at 25 bps. The market reaction to the ECB meeting was muted. Daily changes on the German yield curve range between -1 bp (2-yr) and +2 bps (30-yr). The ECB not committing to the September meeting isn’t seen as skipping the opportunity for now. Money markets stick to their path of quarterly rate cuts in September, December, March and June. The euro trades a tad softer at EUR/USD 1.0919. EUR/GBP changes hands at 0.8410. This morning’s UK labour market data (just like yesterday inflation) don’t rule out one scenario or the other (hold or cut) at the August 1st Bank of England policy meeting. US eco data were mixed with weekly jobless claims rising more than forecast, from 222k to 243k, matching the highest level since August 2023. The Philly Fed business outlook beat consensus, rising from 1.3 to 13.9, the second best level since April 2022. Details showed a huge boost in new orders, shipments and employment with firms being more optimistic on these components six months ahead as well. Firms still have quite some pricing power with prices received accelerating to a YTD high while prices paid slightly decelerated.

News & Views

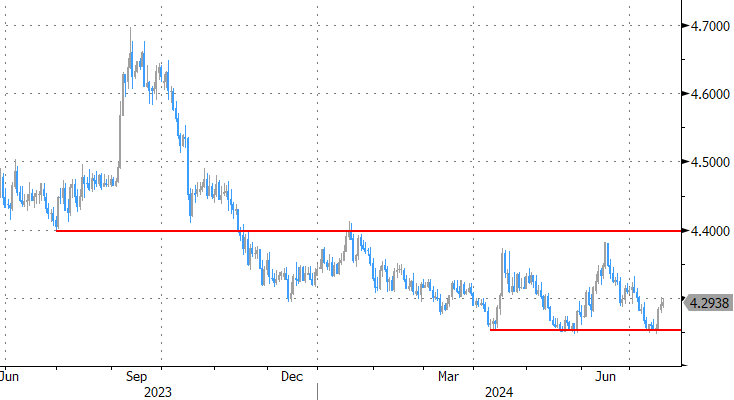

A series of June data published by Statistics Poland painted a mixed picture. Employment in the enterprise sector was unchanged from May but declined 0.4% Y/Y. Despite this consolidation in employment, wages and salaries growth in the enterprise sector remained elevated, increasing 1.8% M/M due to the payment of bonuses, awards and overtime pays. This put gross wages 11% higher compared to the same month last year. In this respect, Statistics Poland mentions that in January 2024, the statutory minimum salary for work was by 17.8% compared previous level set in July 2023, which also affected changes in gross wages and salaries in the enterprise sector. Producer price inflation remains very subdued at 0.1% M/M with prices 6.1% lower Y/Y. Yearly price declines in mining (-5.5%), manufacturing (-5.2%) and electricity and gas (-15.3%) were partially compensated by higher prices in water (2.5%) and construction (6.0%). Industrial production in June rebounded by 3.2% M/M after a 4.5% decline in May, bringing Y/Y growth back in positive territory (0.3%). YTD production growth is also marginally positive (0.1%). The data published today probably won’t change the assessment of the National Bank of Poland to leave its policy rate unchanged at least for this year and probably also going into 2025 as it focuses on the impact of ‘administered price hikes’ and on potential demand pressures due to strong (real) wage growth. After solid gains in June, the zloty (EUR/PLN 4.2975) recently fell prey to profit taking with EUR/PLN rebounding off the 4.25 support area.

The Chinese Communist Party today published a statement at the end of the ‘Third plenum’ meeting. The statement is seen as advocating continuity rather than a big U-turn even as the country tries to implement fundamental changes. Amongst others, the communiqué reiterated policy aims to support new productive forces, to put in place a policy of expanding domestic demand, to prevent and resolve risks in the real estate sector and to reform taxation and the financial system. A more detailed plan is expected to be published in the coming days.

Graphs

DXY (trade-weighted dollar): trying to avoid a drop below neckline of double top formation into this week’s close

USD/CNY: no change of heart at Chinese Communist Party after Third Plenum meeting

EUR/PLN: zloty bounced off strongest levels YTD even as the NBP sticks to forward guidance

Vix volatility index: correction on stock markets just the beginning?

EUR/USD – Slightly Lower as ECB Holds Interest Rates

The euro has edged lower on Thursday. Early in the North American session, EUR/USD is trading at 1.0919, down 0.18% on the day. The euro hasn’t posted a losing day since July 9, gaining 1% during that period.

ECB maintains rates at 3.75%

The European Central Bank maintained its key lending rate at 3.75% at today’s meeting, after cutting rates by a quarter-point in June. The decision to hold rates was widely expected, especially after the June cut, and the euro has had a calm day. The markets are following ECB President Lagarde’s press conference, hoping for clues about future rate policy.

The rate statement noted that “services inflation is elevated and headline inflation is likely to remain above the target well into next year”. The markets weren’t perturbed by this hawkish comment as the ECB has demonstrated that it is willing to lower rates even when inflation is above the 2% level, as it did in June.

The markets have priced in two more quarter-point cuts in September and December. ECB policy makers have been cautious and the rate statement reiterated that the ECB was “not pre-committing to a particular rate path”. ECB officials have stressed that inflation remains high and wage growth, which is feeding services inflation, needs to come down in order for the ECB to feel confident in lowering rates further.

In the US, Fedspeak will be in focus, with five public appearances from FOMC members before the week is over. Investors will be hoping to get some insights on Fed rate policy, with the markets widely expecting a rate cut in September.

.

EUR/USD Technical

- EUR/USD is testing support at 1.0928. Below, there is support at 1.0907

- 1.0960 and 1.0981 are the next resistance lines

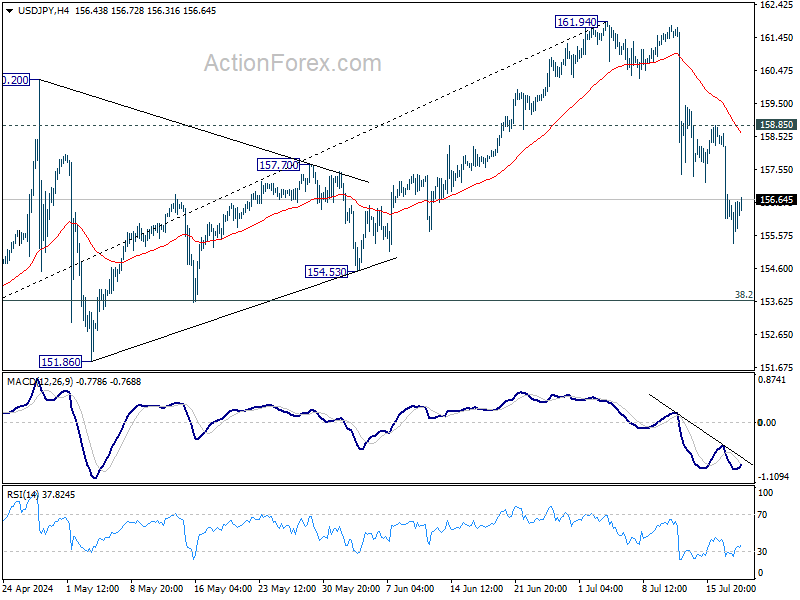

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.29; (P) 156.95; (R1) 157.84; More...

USD/JPY's fall from 161.94 is seen as correcting whole rally from 140.25. Deeper decline is expected as long as 158.85 resistance holds, to 38.2% retracement of 140.25 to 161.94 at 163.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.