Sample Category Title

Change of Heart from Fed Governor Waller Significant

Markets

We’ve given Fed governor Waller plenty of attention this year. He’s been the voice of the large minority inside the Fed who from the beginning of the year has been pushing to keep policy rates at their peak levels for longer. Markets had to gradually retrace from huge easing bets at the beginning of the year, guided by Waller’s “What’s the rush?” and “There’s still no rush” chorus. Backed by stubborn Q1 inflation figures and a strong labour market, this eventually resulted in a median FOMC forecast of just one 25 bps rate cut this year at the June policy meeting. Benign Q2 CPI prints and fear that we might reach a tipping point in the labour market - from pulling vacancies to effectively reducing headcount – tilted the market balance back in favour of more (at least two) and potentially even bigger (50 bps instead of 25 bps) policy rate cuts. Fed governors welcomed the data, but didn’t commit to a specific timing for pulling the trigger. Fed Waller yesterday joined this majority view. “Current data are consistent with achieving a soft landing, and I will be looking for data over the next couple months to buttress this view. While I don’t believe we have reached our final destination, I do believe we are getting closer to the time when a cut in the policy rate is warranted.” The change of heart from Fed governor Waller is significant and a confirmation towards recent market repricing. While the US 2-yr yield reversed intraday course on his comments (from +6 bps to eventually +2 bps), it’s telling that they didn’t trigger a test of the recent lows around 4.40%. We conclude that at least in the short run, sufficient (or even again too much) Fed policy easing has been discounting. Ceteris paribus, this 4.4% floor should be able to hold going into the July 31 FOMC meeting.

Dollar weakness was yesterday’s main trading theme, with technical breaks in USD/JPY (<157.19), GBP/USD (>1.30) and EUR/USD (>1.0916). These moves occurred despite a modest yield rebound and an ongoing equity market correction. US tech-heavy Nasdaq posted its worst result YTD, correcting 2.77% lower. Hawkish trade/foreign policy comments by president-candidate Trump against Taiwan and the semiconductor sector played a role. EUR/GBP attempted a move below 0.84 after June CPI data (slightly) reduced odds of an August BoE rate cut (40% from 50%). A bang-in-line UK labour market report offers no directional guidance this morning. The ECB meeting is today’s key event. We expect ECB President Lagarde to hint at a potential 25 bps rate cut at the next September meeting. We don’t think that the outcome today will alter market pricing of quarterly rate cuts over the year ahead (Sep24, Dec24, Mar25, Jun25).

News & Views

The Australian labour market remains strong even as the unemployment rate rose from 4% to 4.1% in June. The economy in June added net 50.2k (net) jobs, with the gain mostly due to a second consecutive strong rise of full-time employment (43k). The rise in the unemployment rate mainly was the result from a higher participation rate. At 66.9% (from 66.8% in May) it nears the all-time record high of 67% (Nov 2023). Seasonally adjusted monthly hours worked rose by 0.8%. The Australian Bureau of Statistics said that "The employment-to-population ratio and participation rate both continue to be near their 2023 highs. This, along with the continued high level of job vacancies, suggests the labour market remains relatively tight, despite the unemployment rate being above 4% since April’. The Australian 2-y bond yield rebounds 3.2 bps. Markets currently attach a > 25% probability to the RBA raising its policy rate at the August meeting. June CPI inflation data (July 31) will be important input. The Aussie dollar rebounds slightly after a recent (mild) setback, trading at AUD/USD 0.674.

Japan in June returned to a trade surplus of JPY 224bn compared to a JPY 1220bn deficit the previous month as (nominal) exports rose more than imports. Exports added 5.4% Y/Y while imports only rose 3.2%. Even so, growth in both cases slowed substantially from May and also missed market expectations both for exports (7.2%) and imports (9.6%). Both nominal data were for an important part due to a sharp weakening of the yen compared to last year. In volume terms, merchandise exports declined 6.2% Y/Y with imports where 8.9% lower, suggesting still mediocre domestic demand. Japan recorded a JPY 870bn trade surplus with the US while it had a deficit of JPY 335,49bn with China and a deficit of JPY 185.67bn with the EU.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed indicated that it needs more evidence to lower its policy rate. June dots suggested one move in 2024 and four next year. Disappointing ISM and back-to-back downward CPI surprises put the US money market back on (at least) two rate cuts this year (September/December). The US 10-yr yield tests the recent lows and the downside of the downward trend channel in the 4.2% area.

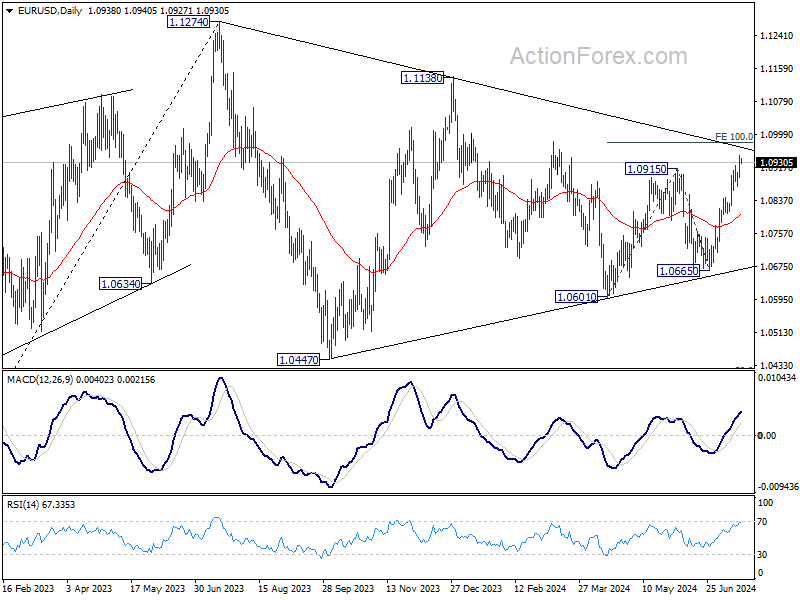

EUR/USD

EUR/USD is testing the topside of the 1.06-1.09 range as the dollar loses interest rate support at stealth pace. Markets consider a September rate cut a done deal and only need confirmation from high-ranked Fed officials. In the meantime, the euro got rid of the (French) political risk premium. Risks of a topside break are high, bringing the psychologic 1.10 and the December 2023 top at 1.1139 on the radar.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 is support is being tested.

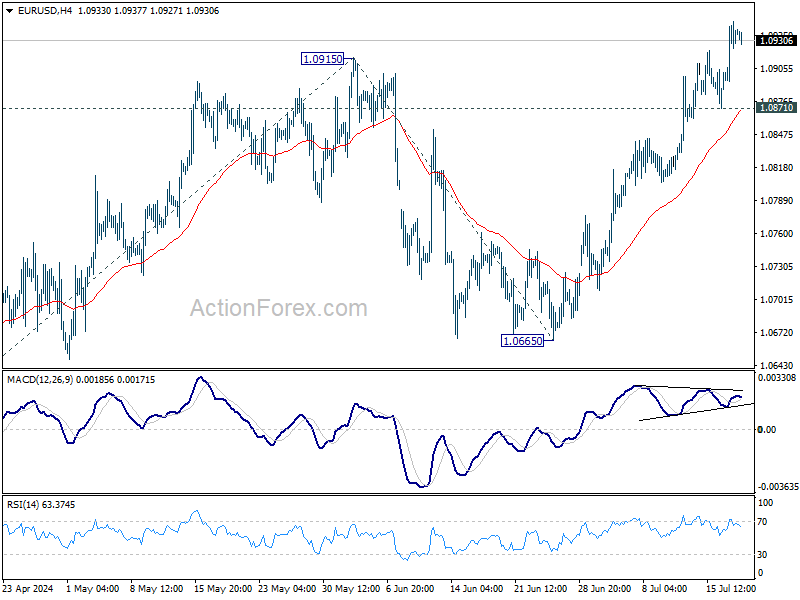

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0907; (P) 1.0928; (R1) 1.0960; More....

Intraday bias in EUR/USD remains on the upside for the moment. Rally from 1.0601 is in progress and should target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. On the downside, below 1.0871 minor support will turn intraday bias neutral gain first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

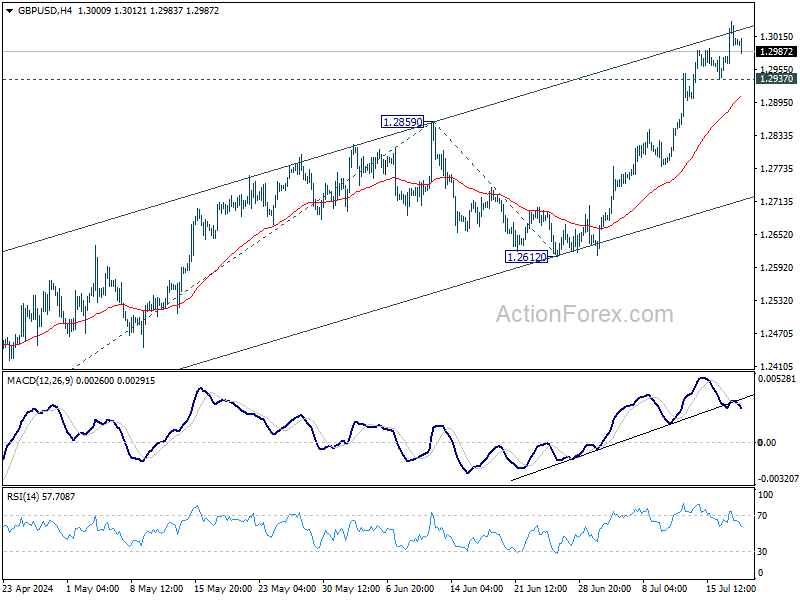

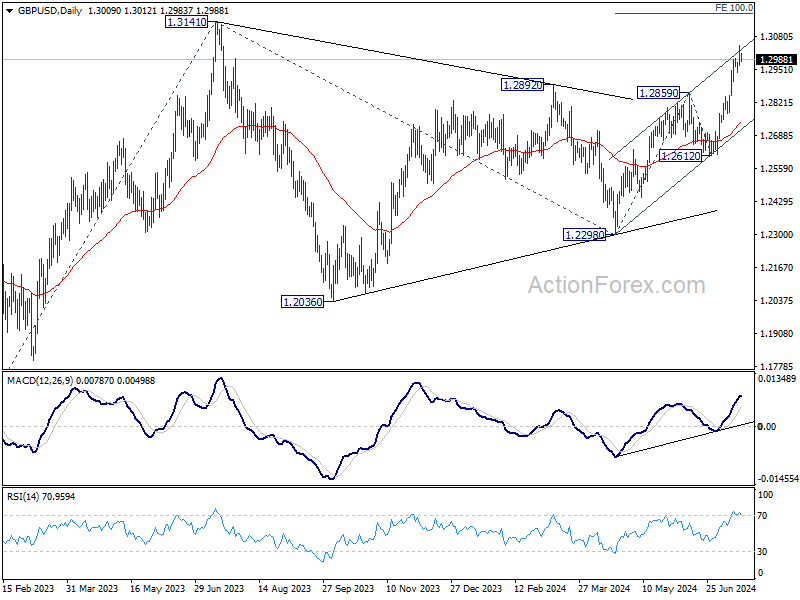

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2968; (P) 1.3006; (R1) 1.3048; More...

Further rally is expected in GBP/USD with 1.2937 minor support intact, despite some loss off upside momentum. Current t rise from 1.2298 should target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. On the downside, below 1.2937 minor support will turn intraday bias neutral again first.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

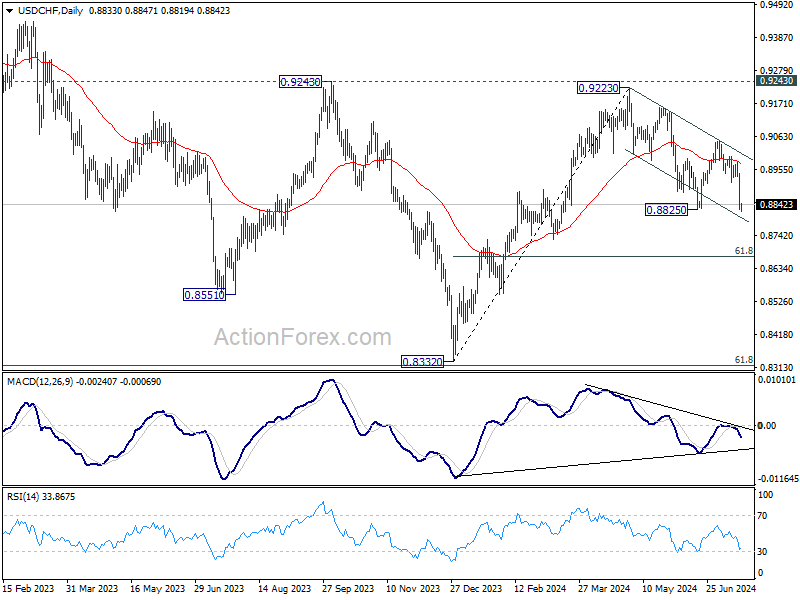

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8790; (P) 0.8871; (R1) 0.8915; More…

Intraday bias in USD/CHF stays on the downside as this point. Breach of 0.8825 support indicates that whole fall from 0.9223 is resuming. Deeper decline would be seen to 60% retracement of 0.8332 to 0.9223 at 0.8672 next. On the upside, above 0.8914 support turned resistance will turn intraday bias neutral first.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

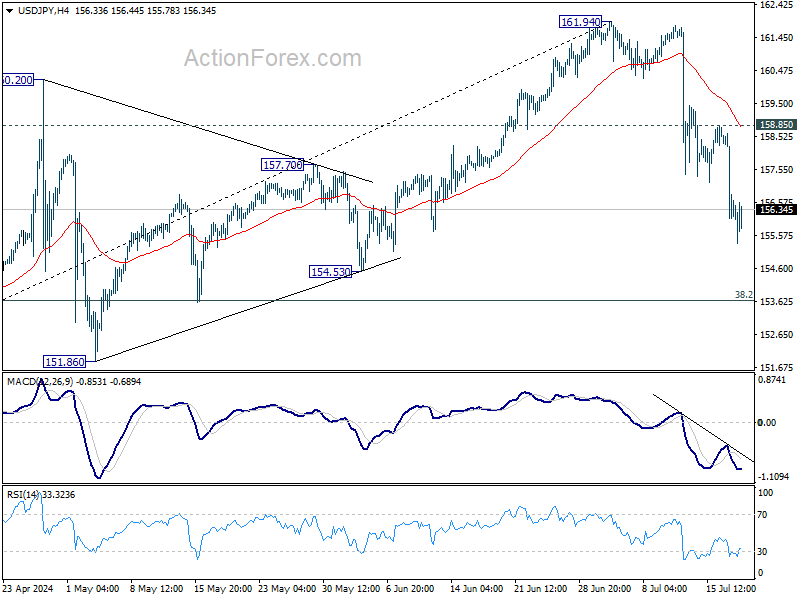

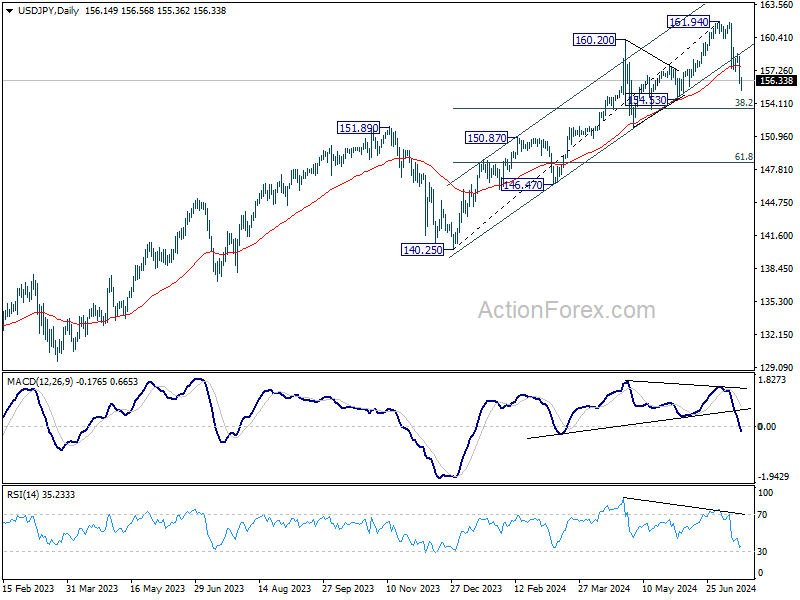

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.29; (P) 156.95; (R1) 157.84; More...

Intraday bias in USD/JPY stays on the downside for the moment. Current decline is seen as correcting whole rally from 140.25. Deeper fall should be seen to 38.2% retracement of 140.25 to 161.94 at 163.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

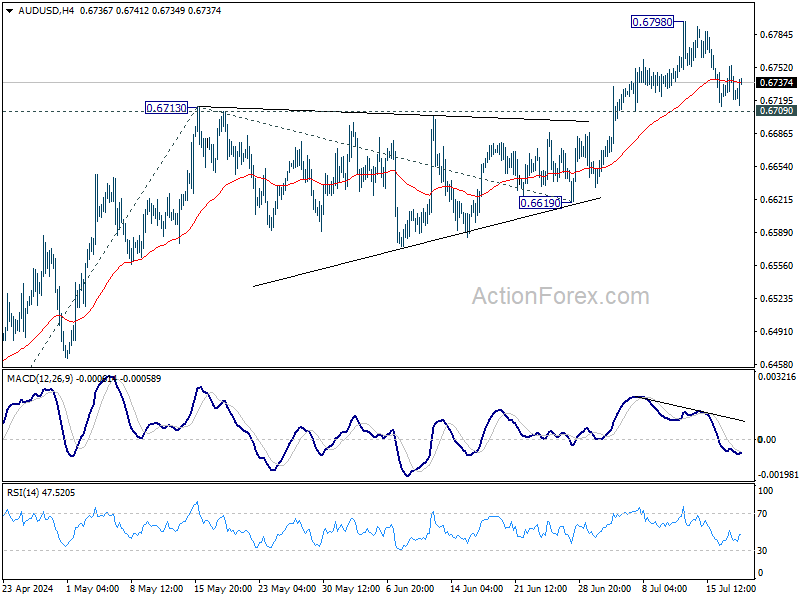

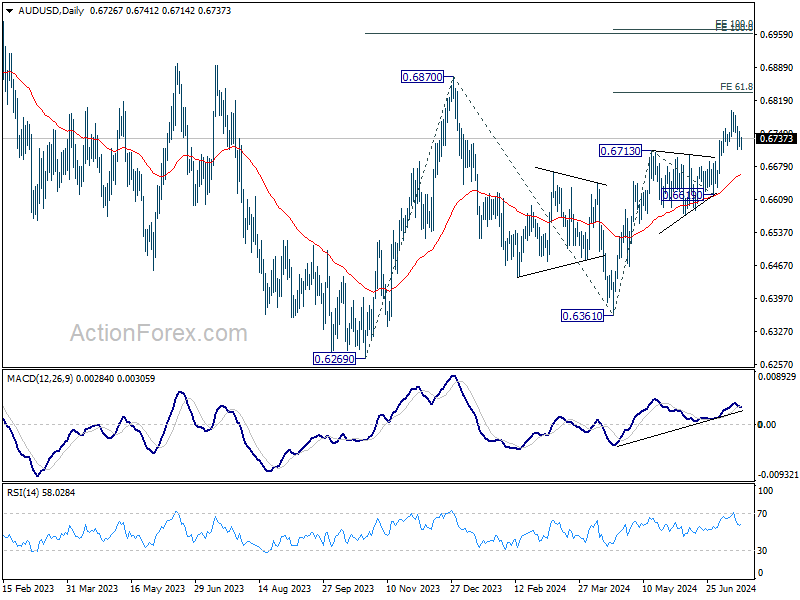

AUD/USD Daily Report

Daily Pivots: (S1) 0.6715; (P) 0.6735; (R1) 0.6749; More...

Intraday bias in AUD/USD remains neutral for the moment. Further rally is expected as long as 0.6709 minor support holds. On the upside, above 0.6798 will resume the rally from 0.6361 and target 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837. Decisive break there could prompt upside acceleration through 0.6870 resistance to 100% projection at 0.6971. On the downside, however, firm break of 0.6709 support will turn intraday bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

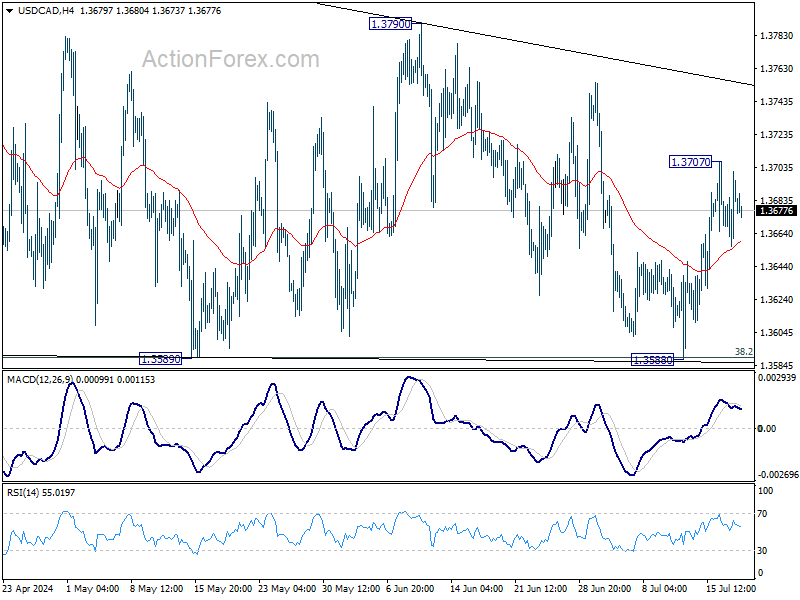

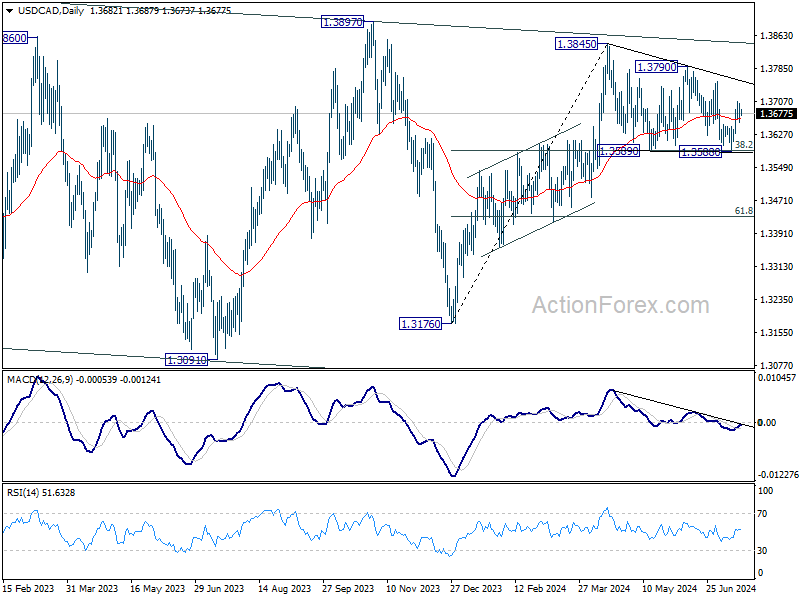

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3659; (P) 1.3681; (R1) 1.3704; More...

Intraday bias in USD/CAD remains neutral for the moment. Outlook is unchanged that corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589 twice. Above 1.3707 will target 1.3790 resistance first. Break of 1.3790 will argue that larger rise from 1.3716 is ready to resume through 1.3845.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

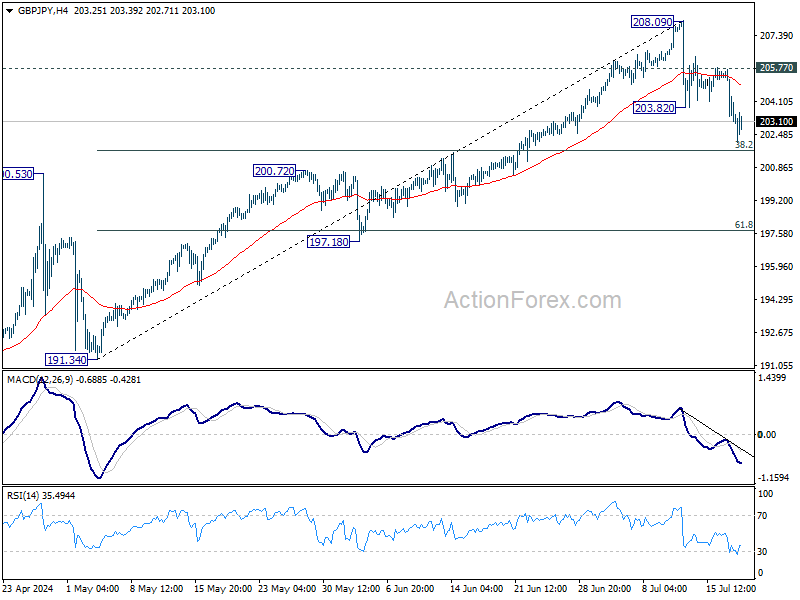

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.23; (P) 203.96; (R1) 204.91; More...

Intraday bias in GBP/JPY is back on the downside as fall from 208.09 resumed. Deeper decline would be seen to 38.2% retracement of 191.34 to 208.09 at 201.69. Strong support is expected there to bring rebound. On the upside, above 205.77 minor resistance will turn intraday bias will turn bias back to the upside for retesting 208.09. However, sustained break of 201.69 will argue that larger correction is already underway.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 200.72 resistance turned support holds, even in case of deep pullback.

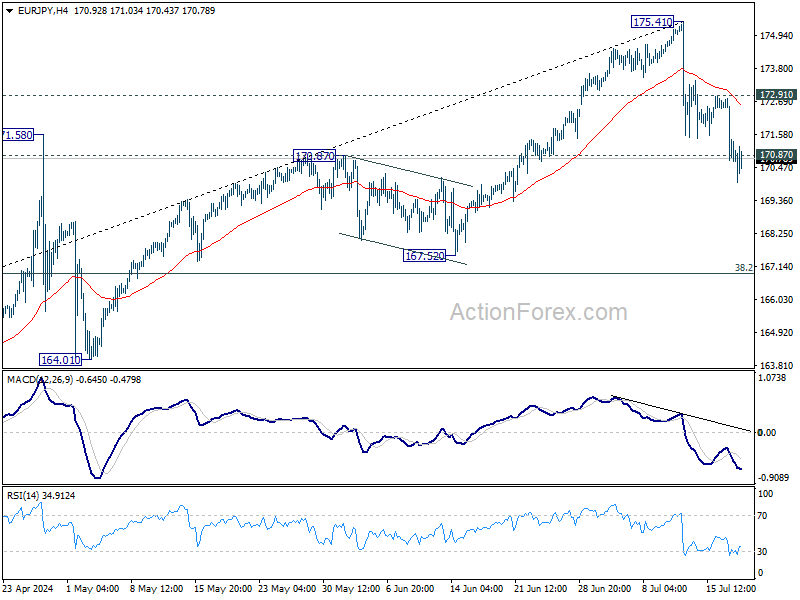

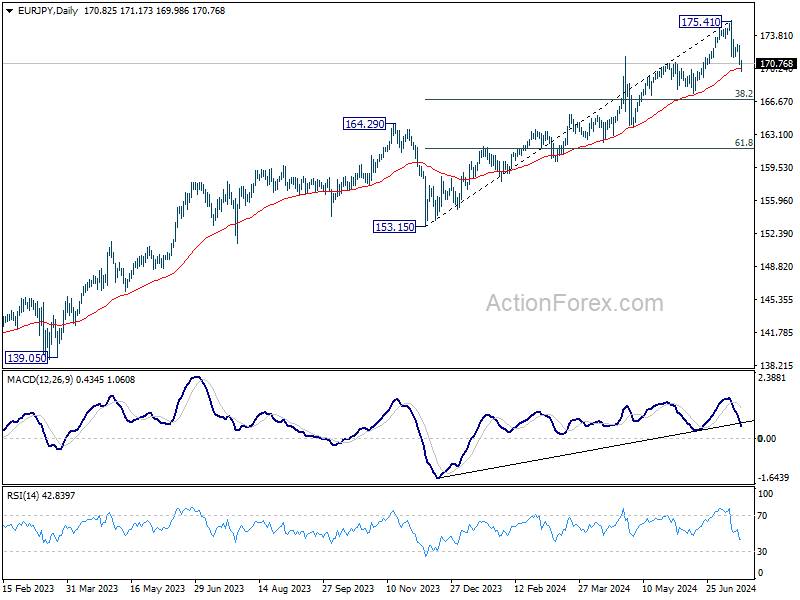

EUR/JPY Daily Outlook

Daily Pivots: (S1) 170.11; (P) 171.47; (R1) 172.23; More...

EUR/JPY's break of 170.87 resistance turned support argues that fall from 175.41 might be correcting whole rise from 153.15 already. Intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 170.30) will target 38.2% retracement of 153.15 to 175.41 at 166.90. On the upside, though, break of 172.91 resistance will revive near term bullishness and bring retest of 175.41 high.

In the bigger picture, medium term outlook will stay bullish as long as 164.29 resistance turned support holds. Long term up trend is still in favor to continue through 175.41 at a later stage. However, firm break of 164.29 will be a strong sign of bearish trend reversal.

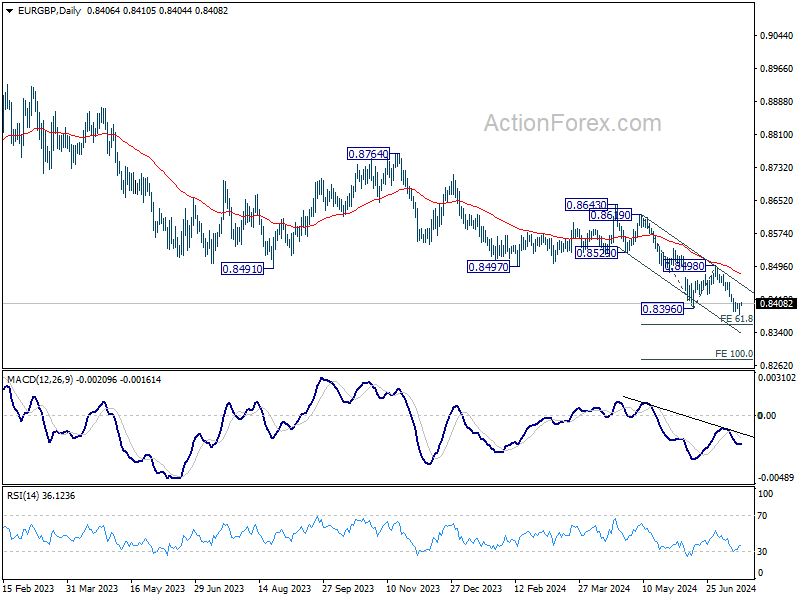

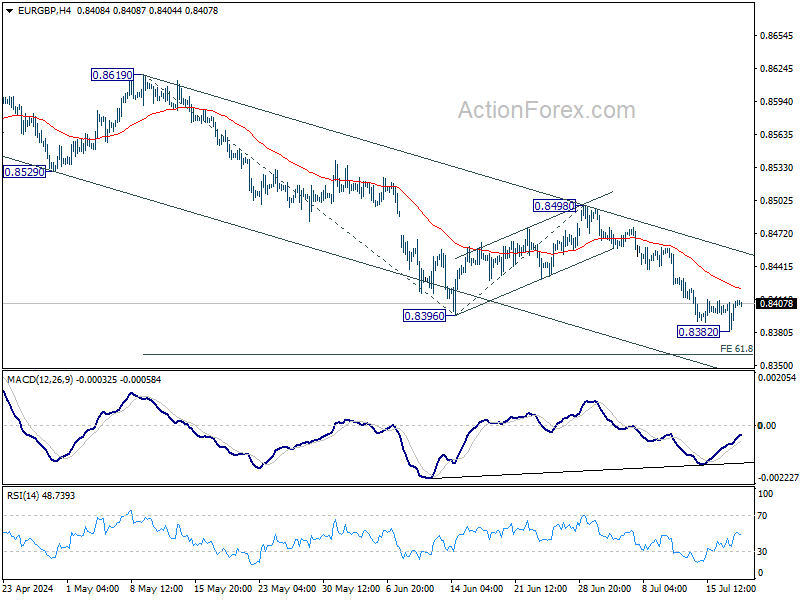

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8391; (P) 0.8401; (R1) 0.8419; More....

EUR/GBP recovered quickly after dipping to 0.8392 and intraday bias remains neutral. Further decline is in favor. But considering bullish convergence condition in 4H MACD, downside could be contained by 61.8% projection of 0.8619 to 0.8396 from 0.8498 at 0.8360 on first attempt. On the upside, break of 55 4H EMA (now at 0.8421) will turn bias back to the upside for stronger rebound.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.