Sample Category Title

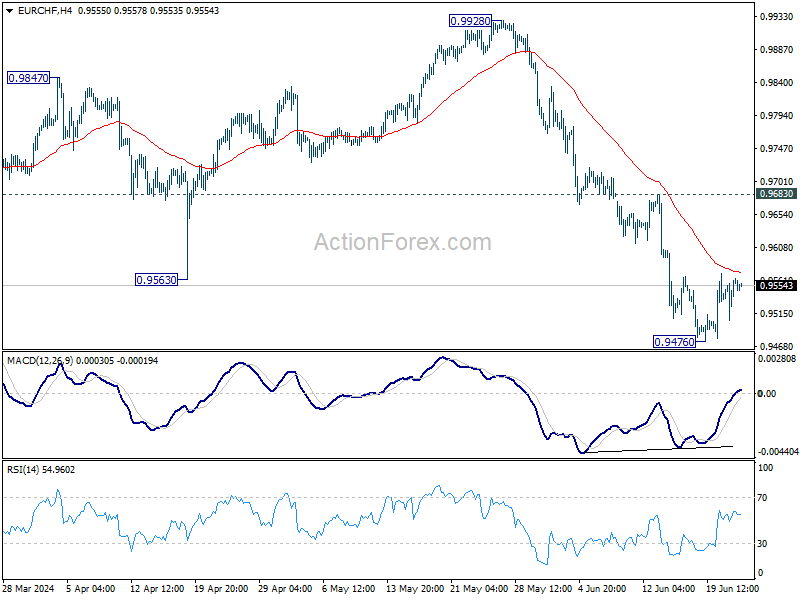

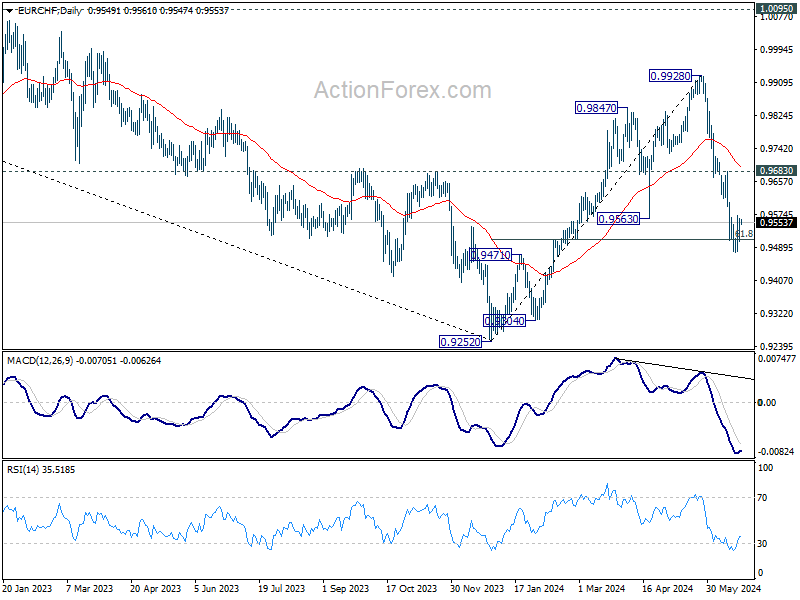

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9524; (P) 0.9545; (R1) 0.9583; More....

EUR/CHF is staying inc consolidation above 0.9476 and intraday bias remains neutral. While stronger recovery cannot be ruled out, outlook will remain bearish as long as 0.9683 resistance holds. On the downside, break of 0.9476, and sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will bring retest of 0.9252 low next.

In the bigger picture, rebound from 0.9252 should have completed at 0.9228. Medium term outlook remains bearish with 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

Nvidia Selloff Raises Worries

The week kicks off on a weak note following a moody trading session across Europe and the US on Friday. One of the most significant moves of last two trading days of the US was a 10% selloff in Nvidia sales for … no reason other than the fact that it was the end of the month, the end of the quarter and the end of H1, and investors preferred taking profits while they repositioned for the new half than buying more Nvidia shares at peak levels, and at a very high valuation with little certainty regarding how to value a stock that’s price-to-projected sales hit the highest of the S&P500. But still, Nvidia is expected to deliver around $28bn in the Q2, more than double the same time last year, while Microsoft is expected to announce 15% sales and Apple just 3%. It’s just that, no one really knows at this point, if Nvidia deserves a higher price tag.

And the problem with that is, because the US Big Tech stocks led by Nvidia were responsible for most of this year’s rally in major US indices – because the S&P500’s equal weight index remained far behind the normal weighted index since at least a month, any weakness in the US tech rally could mean the end of the party for the major US indices.

This week, the US will reveal its latest GDP update on Thursday. US growth is expected to be revised slightly higher from 1.3% to 1.4% down, but that’s down from 3.4% printed a quarter earlier. And on Friday, investors will focus on core PCE data – the Federal Reserve’s (Fed) favourite gauge of inflation. The latter better be soft enough to prevent a broader selloff in US indices. On the individual front, FedEx and Micron Technology are due to release earnings.

Elsewhere, appetite is limited. The Stoxx 600 in Europe was toppish last week as the French political uncertainties occupied the headlines. The EURUSD sold off to 1.0670 on Friday and is trading a touch below 1.07 at the start of the week. Le Pen’s National Rally increased its lead in the polls for the upcoming legislative elections to 36%, while Emmanuel Macron’s centrists stand near 20% support. French risks will likely remain a shadow over the single currency at least until the election.

In Japan, the USDJPY is dangerously flirting with the 160 level – a level which had brought the Japanese policymakers to intervene to stop the bleeding back in April. The Japanese Vice Finance Minister Kanda told reporters that they are ready to intervene 24 hours a day if necessary. The net speculative short positions against the yen remain relatively high despite the rising risk of a currency intervention. The latter means that the USDJPY could post a rapid fall in case a BoJ-triggered price action clears a part of these short positions, but currency intervention alone will hardly send the USDJPY into a sustainable bearish trend; the Bank of Japan (BoJ) must change its rate policy that leads to such a strong yen selloff in the first place.

In energy, US crude is lower this Monday morning after having tested and failed to clear the $82pb resistance last Friday. Trend and momentum indicators remain in favour of a further rise while the RSI index is not yet pointing at extensively bought market conditions. Clearing the $82pb level, the major 61.8% Fibonacci retracement on April to May selloff, should act as a strong signal about the viability of the latest rebound and could throw the foundation of a further rise toward $85pb. But clearing the $82pb could be difficult with sputtering China.

Chinese equities begin the week on continued downside pressure. The CSI 300 fell to an almost 4-month low on the back of insufficient rebound in economic activity, copper futures remain also under the pressure of a slow Chinese rebound.

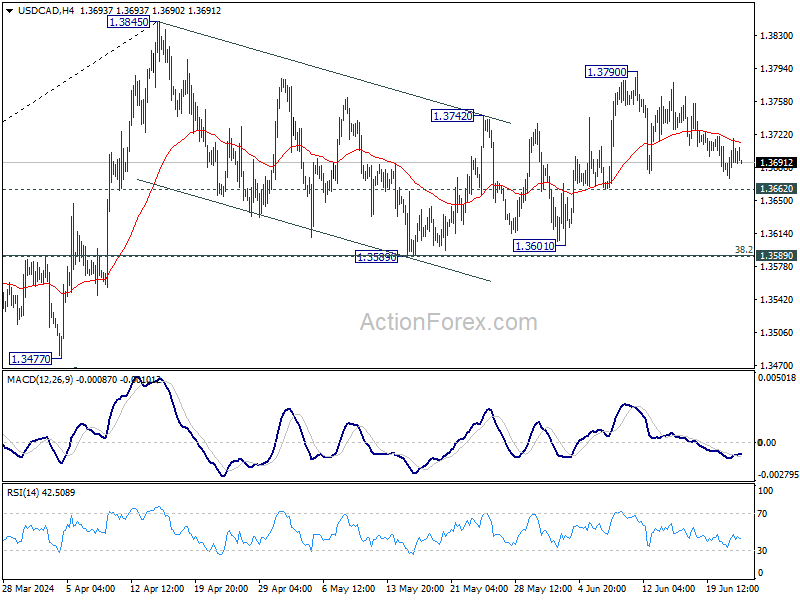

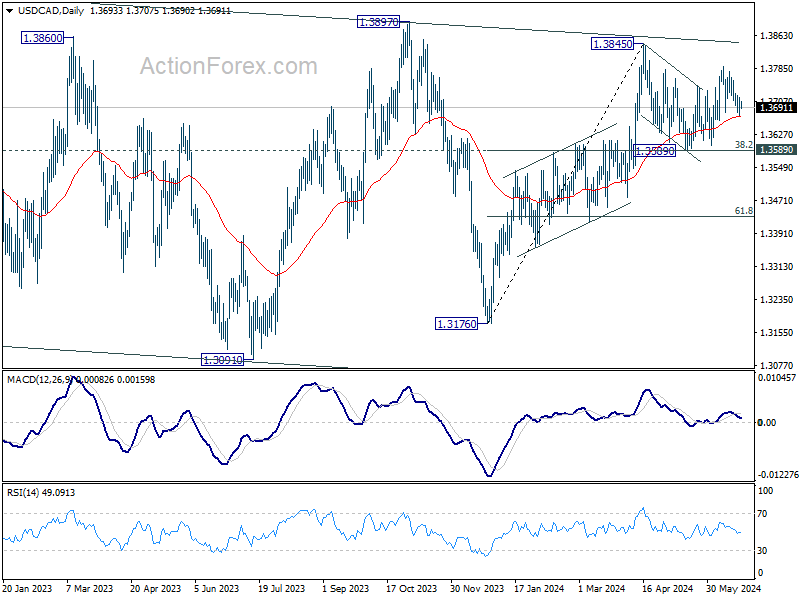

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3671; (P) 1.3698; (R1) 1.3721; More...

Intraday bias in USD/CAD remains neutral and outlook is unchanged. Further rally is expected as long as 1.3662 support holds. Above 1.3790 will bring retest of 1.3845 high first. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

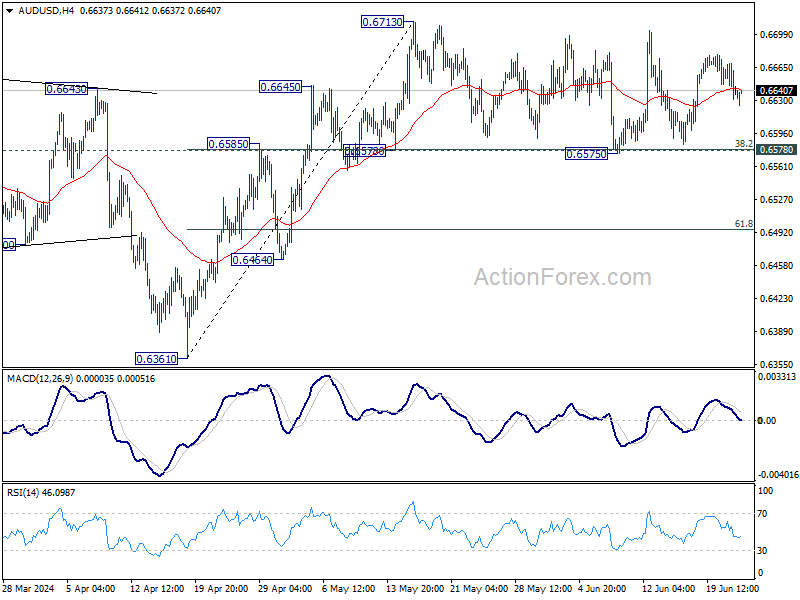

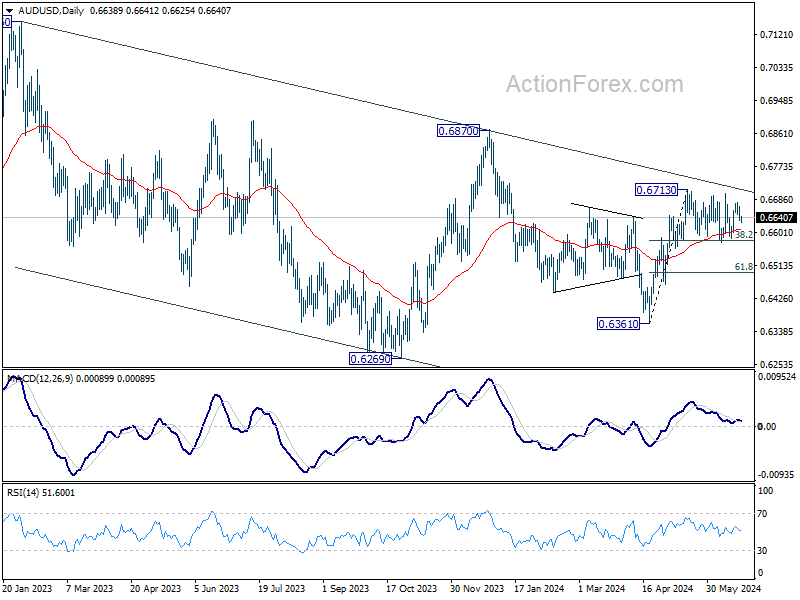

AUD/USD Daily Report

Daily Pivots: (S1) 0.6625; (P) 0.6648; (R1) 0.6663; More...

No change in AUD/USD's outlook as consolidation from 0.6713 is still extending. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

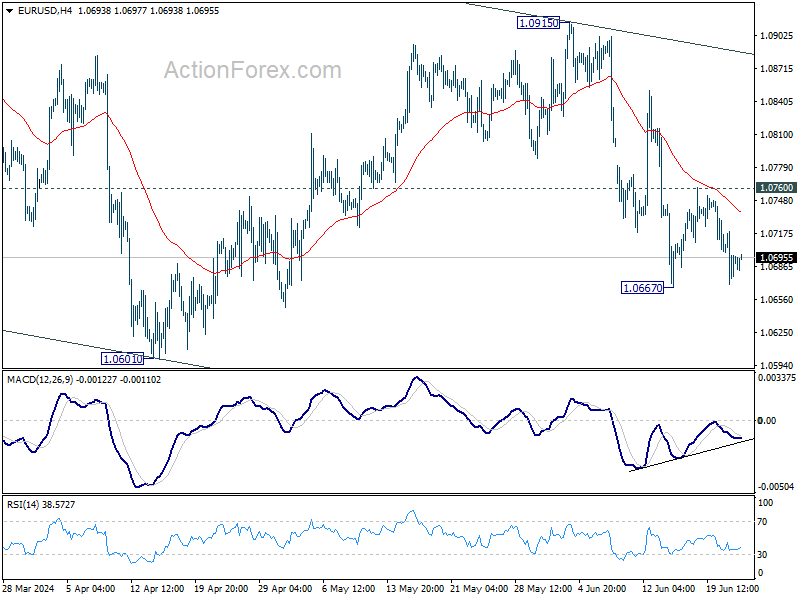

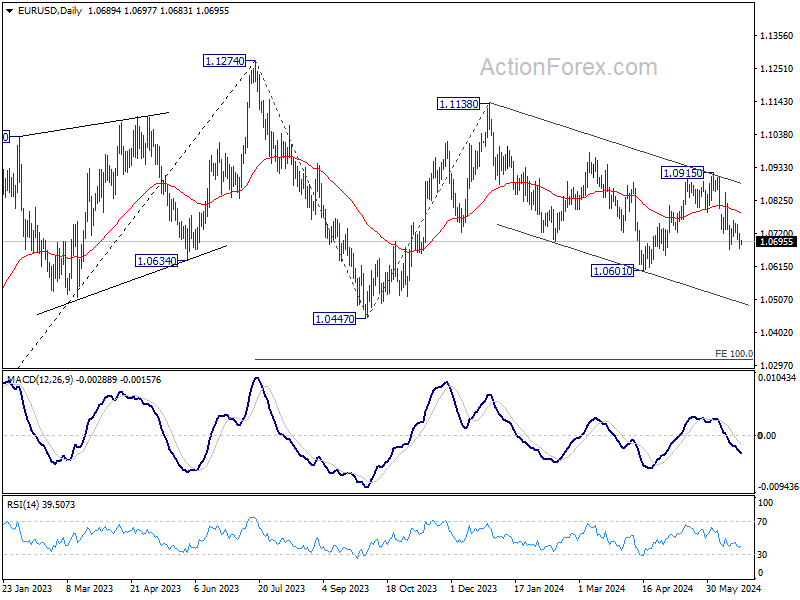

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0669; (P) 1.0695; (R1) 1.0719; More....

Intraday bias in EUR/USD remains neutral first and consolidation from 1.0667 could extend. But further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

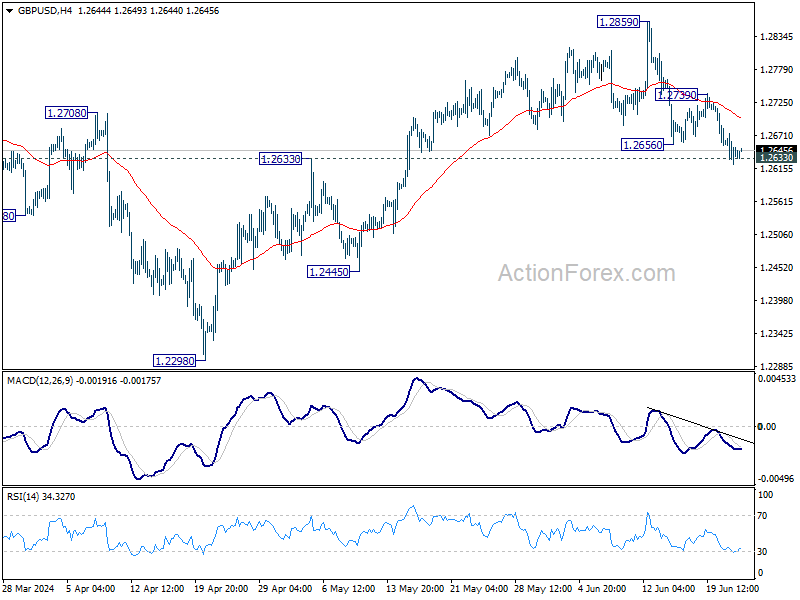

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2619; (P) 1.2646; (R1) 1.2671; More...

Intraday bias in GBP/USD remains mildly on the downside for the moment. Sustained break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. For now, risk will stay on the downside as long as 1.2739 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

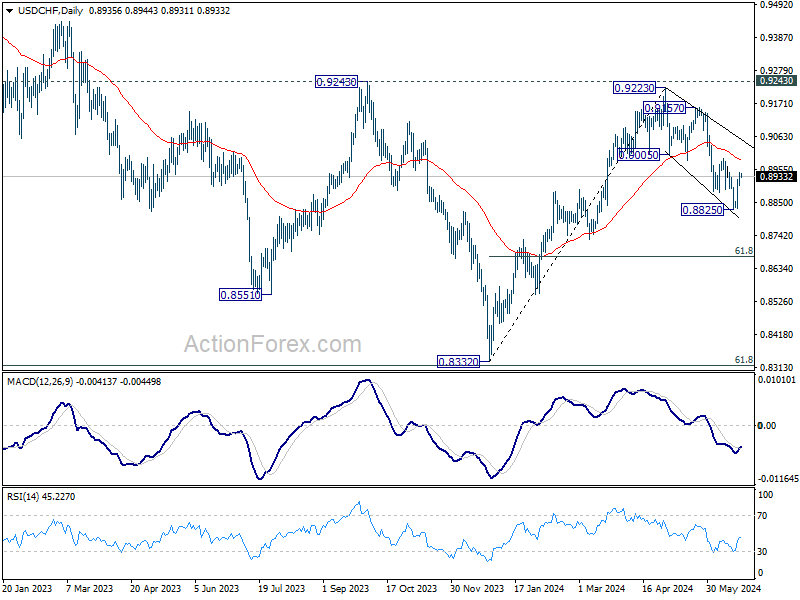

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8917; (P) 0.8931; (R1) 0.8958; More….

Intraday bias in USD/CHF stays neutral and more consolidations could be seen above 0.8825. Still, near term outlook remains bearish with 0.8992 resistance intact. Break of 0.8825 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

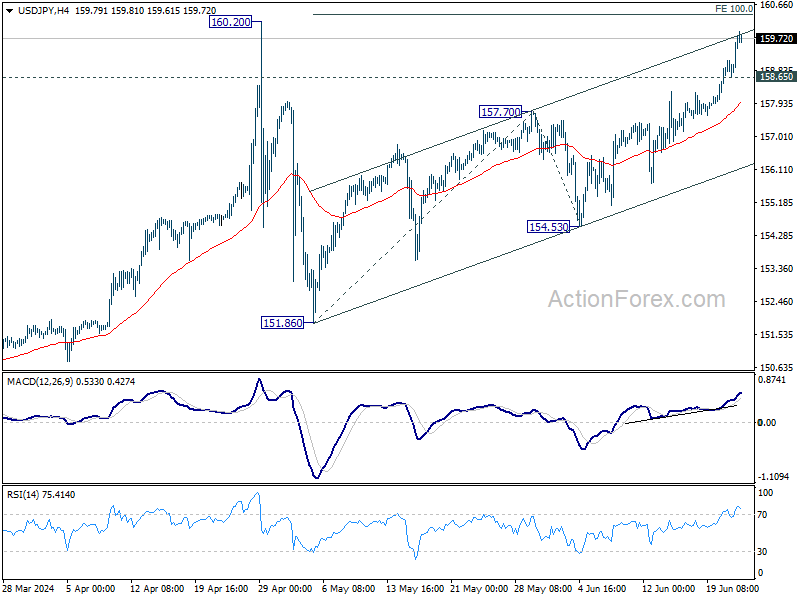

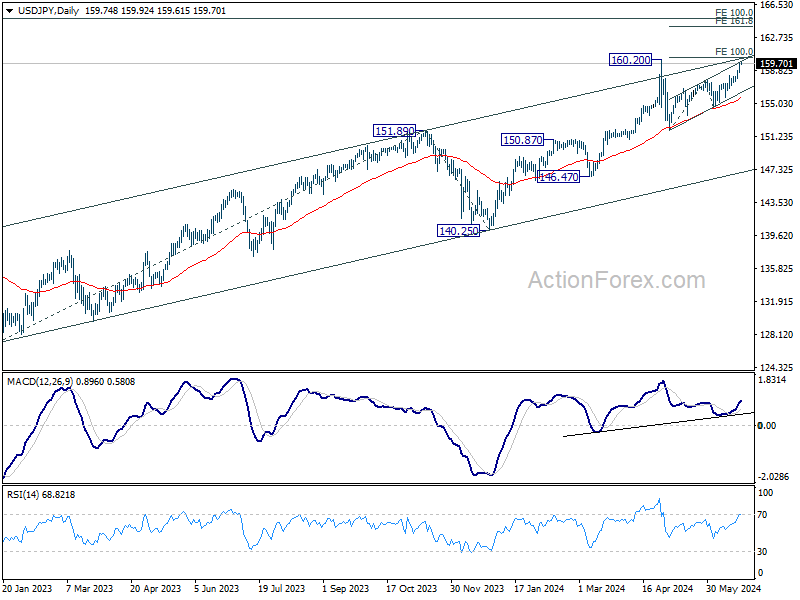

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.02; (P) 159.44; (R1) 160.22; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rally should target 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. Upside could be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first. However, decisive break of 160.37 will pave the way to 161.8% projection at 163.97.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Japan’s Inaction and Refrained Rhetoric Lead to Speculation on New Intervention Threshold

Yen recovered mildly in quiet Asian session along with the Swiss Franc, driven by mild risk aversion in the region. Despite this uptick, there is no strong indication of a significant rebound for the Japanese currency following its sharp decline last week. Notably, Japan did not utilize the thin liquidity at the beginning of the week to intervene in the currency markets. While some traders remain vigilant for possible intervention should USD/JPY surpass 160 level, we believe that the intervention threshold may have already been adjusted higher.

Japan's verbal intervention has been relatively restrained too. Finance Minister Shunichi Suzuki warned against excessive speculative movements in the current market, pledging to respond appropriately if necessary. However, stronger language, such as monitoring the markets with a "high sense of urgency," was notably absent. Meanwhile, top currency diplomat Masato Kanda only reiterated that "we are always ready to take appropriate action when there are excessive moves," and emphasized that Japan is prepared to intervene 24 hours a day if needed.

In the broader currency market, Sterling and US Dollar followed Yen and Swiss Franc as the stronger performers of the session. Meanwhile, New Zealand Dollar, Australian Dollar, and Canadian Dollar lagged, with Euro positioned in the middle. As the first half of the year draws to a close, upcoming inflation data from Canada, Australia, Tokyo, and the US are expected to inject more volatility into the markets.

Technically, AUD/JPY's long term up trend resumed last week and surged to the highest level since 2007, passing through 2013 high at 105.42. Further rally is expected as long as 104.91 resistance turned support holds. Next target is 61.8% projection of 95.48 to 104.91 from 102.59 at 108.41 which is above 2007 high at 107.88. This advance will depend on Japan's intervention stance and Australia's monthly CPI data scheduled for release on Wednesday.

In Asia, at the time of writing, Nikkei is up 0.60%. Hong Kong HSI is down -1.02%. China Shanghai SSE is down -0.70%. Singapore Strait Times is down -0.04%. Japan 10-year JGB yield is up 0.0212 at 0.999.

BoJ deliberates on rate hikes, Yen depreciation, and JGB purchase adjustments

During Monetary Policy Meeting on June 13-14, BoJ board discussed the need for adjustments in response to rising inflation risks. One key opinion indicated that if April Outlook Report's economic and inflation forecasts are realized, BoJ will raise the policy interest rate and adjust monetary accommodation.

Another member warned that prices could "deviate upward" from the baseline scenario if recent cost increases are passed on to consumers, suggesting a need for further policy adjustments from a "risk management" perspective. It's also highlighted the growing "upside risks" to prices, with one member stating these risks have affected consumer sentiment and that the policy interest rate should be raised "not too late" if appropriate.

The impact of Yen's depreciation was also discussed, with an opinion suggesting an "upward revision" to the inflation outlook, warranting a higher risk-neutral policy interest rate. Some members emphasized the importance of basing monetary policy on the "overall picture of developments in economic activity and prices," rather than short-term foreign exchange fluctuations. They stressed that policy should be informed by trends in prices and wage developments.

Regarding asset purchases, one opinion recommended reducing the purchase amount of Japanese government bonds to allow long-term interest rates to form more freely in financial markets. This reduction should be "sizeable" and "predictable," while ensuring flexibility to maintain stability in JGB market.

New Zealand's goods exports reach record high in may, trade surplus exceeds expectations

New Zealand's goods exports rose by 2.9% yoy to NZD 7.2B in May, marking the first time that monthly exports have surpassed the NZD 7B mark. Goods imports also saw a slight increase, rising by 0.6% yoy to NZD 7.0B. This resulted in a trade surplus of NZD 204m, exceeding the expected NZD 155m.

Breaking down the top monthly export movements by country, New Zealand saw mixed results. Exports to China fell by -12% yoy, and exports to Australia dropped by -3.8% yoy. In contrast, exports to the US surged by 33% yoy, while exports to the EU and Japan rose by 2.8% yoy and 12% yoy, respectively.

On the import side, imports from China increased by 2.6% yoy, while imports from the EU decreased by -1.8% yoy. Imports from Australia -4.7% yoy, whereas imports from the US and South Korea rose by 1.6% yoy and 5.8% yoy, respectively.

Inflation reports from Canada, Australia, Japan, and US to drive currencies

Inflation data will once again be the focus this week, with critical reports coming from Canada, Australia, and Tokyo in Japan. The United States will also release its PCE inflation data.

The minutes of BoC's June meeting revealed that governing council had considered delaying a rate cut until July but decided to act earlier this month, citing significant progress in reducing inflation. Thus, it is unlikely for BoC to deliver a back-to-back rate cut in July, although this will depend on how inflation evolves. Canada's CPI common has steadily declined from 3.9% in December to 2.6% in April. However, a stalling of progress in May could keep BoC cautious.

Australia's monthly CPI data for May might show a slight tick down in inflation. Yet, the readings have been stuck between 3.4% and 3.6% since last December, a situation that does not instill confidence in RBA to close the door on further tightening. While RBA will wait for Q2 CPI for a more comprehensive assessment, the monthly CPI could still provide valuable insight into inflation trends.

In Japan, Tokyo's core CPI is expected to tick up slightly in June, continuing to hover around the 2% level due to fluctuations in energy prices. BoJ has repeatedly indicated that a rate hike in July is a possibility, but the situation remains complex. Fading demand-led price pressures would likely keep the BoJ cautious about tightening further. However, cost-push inflation resulting from a weakening Yen could prompt a monetary policy response.

In the US, PCE core price index is expected to rise by only 0.1% mom in May, the smallest increase since last November. This would be a positive development for Fed, suggesting that inflationary pressures are easing. But it is way too early for Fed to decide on whether to start cutting interest rates in September, considering that it is only June. More data will be needed to make an informed decision.

Here are some highlights for the week:

- Monday: New Zealand trade balance; BoJ summary of opinions; Germany Ifo business climate.

- Tuesday: Japan corporate service price index; Australia Westpac consumer sentiment; Canada CPI; US house price index, consumer confidence.

- Wednesday: Australia monthly CPI; Germany Gfk consumer sentiment; Swiss UBS economic expectations; US new home sales.

- Thursday: Japan retail sales; New Zealand ANZ business confidence; Eurozone M3 money supply; US Q1 GDP final, jobless claims, durable goods orders, goods trade balance, pending home sales.

- Friday: Japan Tokyo CPI, unemployment rate, industrial production, housing starts; Germany import price: UK Q1 GDP final; Swiss KOF economic barometer; Germany unemployment; Canada GDP; US personal income and spending, PCE inflation, Chicago PMI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.02; (P) 159.44; (R1) 160.22; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rally should target 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. Upside could be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first. However, decisive break of 160.37 will pave the way to 161.8% projection at 163.97.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | 204M | 155M | 91M | -3M |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 08:00 | EUR | Germany IFO Business Climate Jun | 89.7 | 89.3 | ||

| 08:00 | EUR | Germany IFO Current Assessment Jun | 88.4 | 88.3 | ||

| 08:00 | EUR | Germany IFO Expectations Jun | 91 | 90.4 |

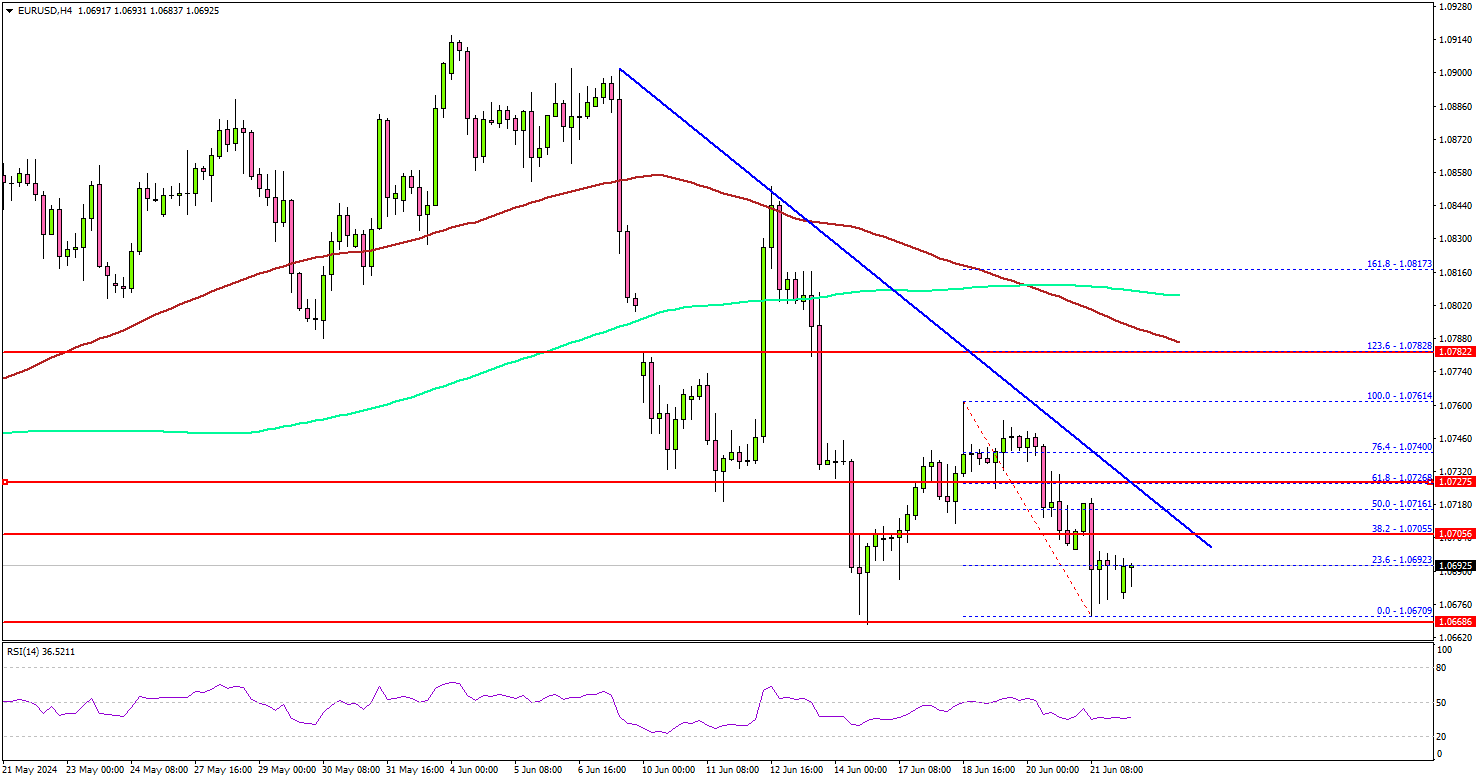

EUR/USD Remains At The Edge, Can It Recover?

Key Highlights

- EUR/USD failed to surpass 1.0765 and declined once again.

- A major bearish trend line is forming with resistance at 1.0710 on the 4-hour chart.

- GBP/USD declined heavily and traded below the 1.2680 support.

- Bitcoin price extended losses and traded below the $64,200 support.

EUR/USD Technical Analysis

The Euro failed to recover above the 1.0765 resistance against the US Dollar. EUR/USD started another decline and traded below the 1.0720 support.

Looking at the 4-hour chart, the pair settled below the 1.0720 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). It is now consolidating near the 1.0670 support zone.

On the upside, the pair is facing resistance near the 1.0710 level. There is also a major bearish trend line forming with resistance at 1.0710 on the same chart.

The first major resistance is near the 1.0720 level. A clear move above the 1.0720 resistance might send it toward the 1.0750 level. The main resistance is still near 1.0765. Any more gains might call for a move toward the 1.0820 level in the near term.

If not, the pair might dip again. Immediate support is near the 1.0670 level. The next major support is near the 1.0650 zone. A downside break and close below the 1.0650 support zone could open the doors for a larger decline. In the stated case, the pair could decline toward the 1.0550 level.

Looking at GBP/USD, the pair trimmed most gains and there was a bearish reaction below the 1.2680 support zone.

Economic Releases

- German IFO Business Climate Index for June 2024 – Forecast 89.7, versus 89.3 previous.

- German IFO Current Assessment Index for June 2024 - Forecast 88.4, versus 88.3 previous.