Sample Category Title

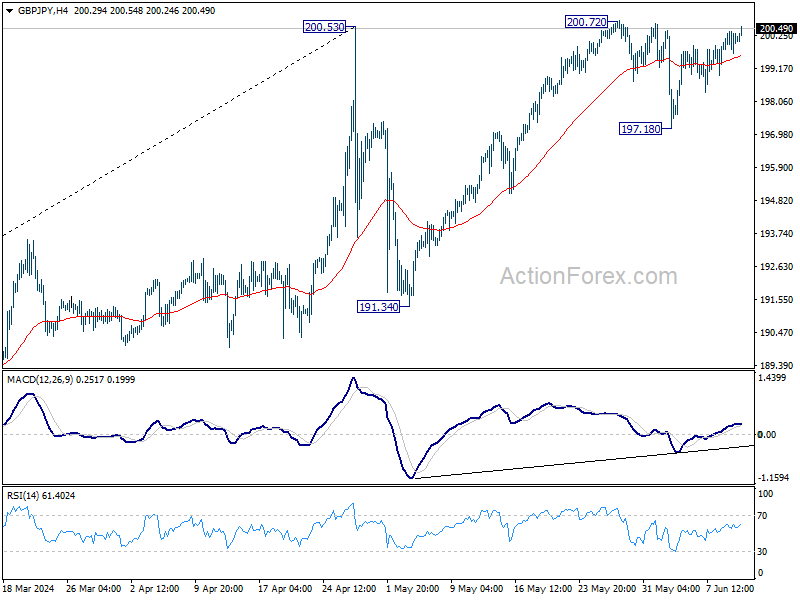

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.77; (P) 200.09; (R1) 200.49; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the upside, decisive break of 200.72 will resume larger up trend. Nevertheless, break of 197.18 will turn bias to the downside and extend the corrective pattern from 200.53 with another falling leg.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Sustained trading above 200.53 will pave the way to 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

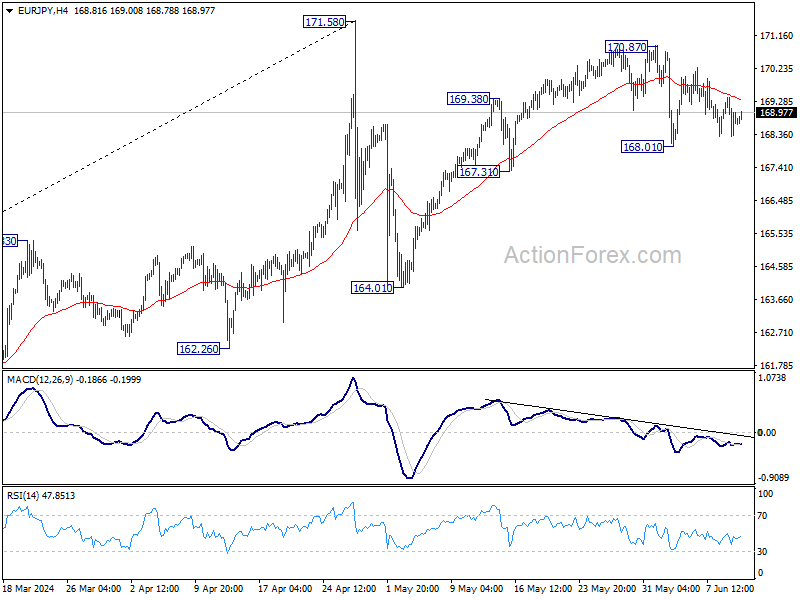

EUR/JPY Daily Outlook

Daily Pivots: (S1) 168.24; (P) 168.83; (R1) 169.37; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the downside, break of 168.01 support will strengthen the case that rise from 164.31 has completed at 170.78 already. Intraday bias will be back on the downside for 167.31 support, and then 164.01. Nevertheless, break of 170.87 will resume the rally to retest 171.58 high instead.

In the bigger picture, a medium top was formed at 171.58 after brief breach of 169.96 (2008 high). But as long as 55 W EMA (now at 159.51) holds, price actions from there is seen as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8440; (P) 0.8456; (R1) 0.8472; More...

Intraday bias in EUR/GBP remains on the downside. Current down trend should target 0.8376 projection level next. On the upside, above 0.8446 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

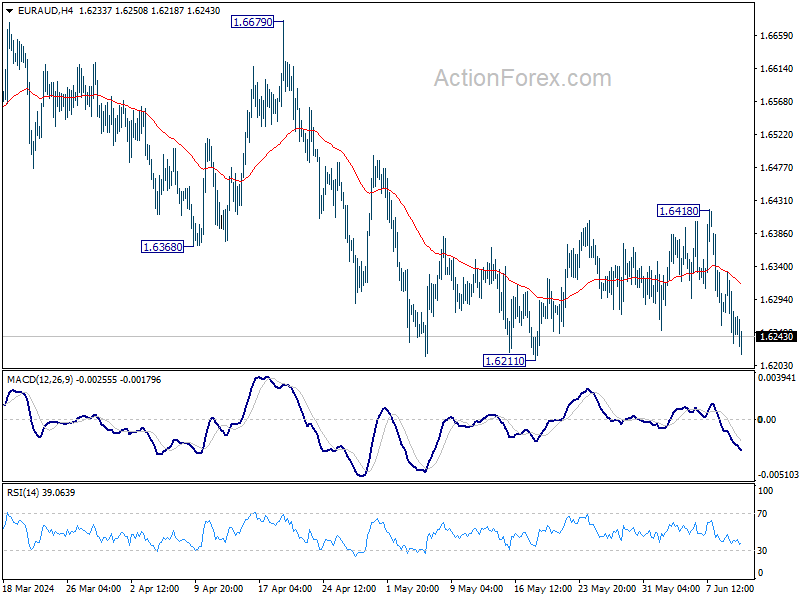

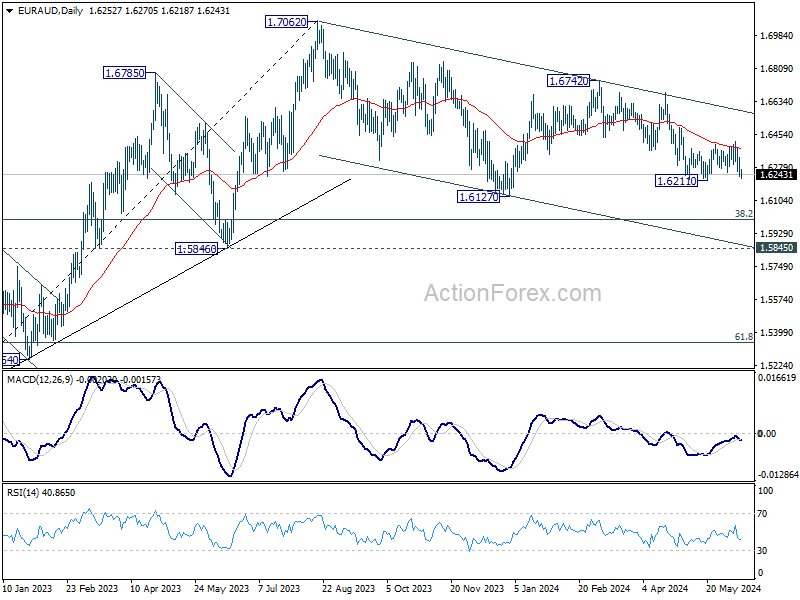

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6217; (P) 1.6277; (R1) 1.6318; More...

EUR/AUD is still bounded in range above 1.6211 and intraday bias stays neutral. On the downside, firm break of 1.6211 support will resume the whole decline from 1.6742, as the third leg of the correction from 1.7062. Further fall should be seen through 1.6127 support. On the upside, sustained break 1.6418 resistance will resume the rebound from 1.6211 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

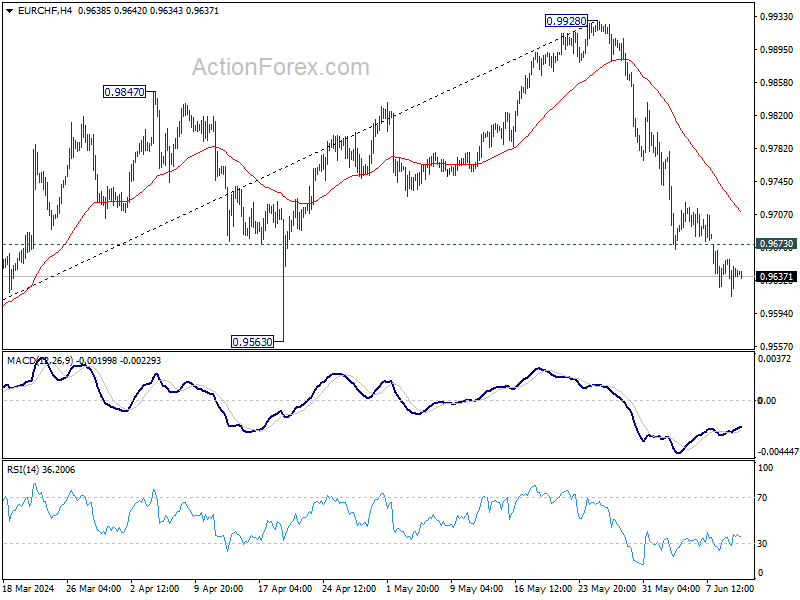

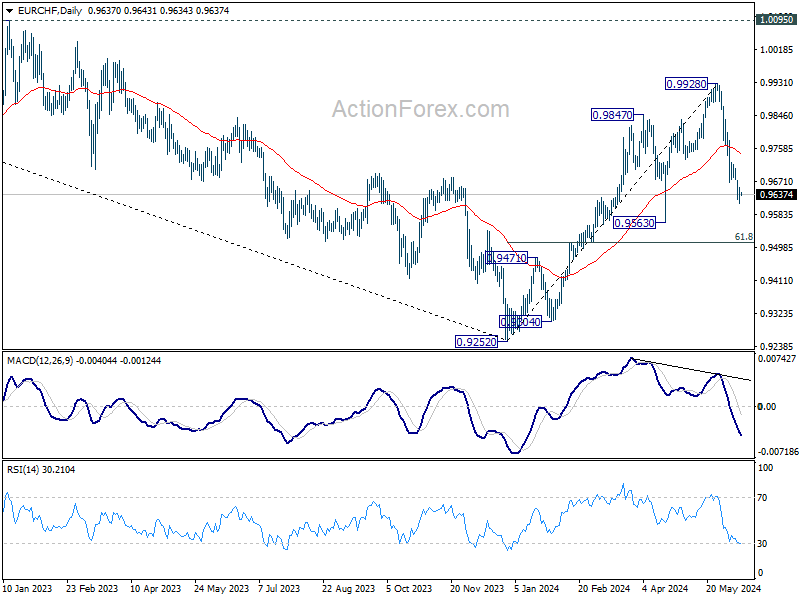

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9618; (P) 0.9639; (R1) 0.9661; More....

No change in EUR/CHF's outlook and intraday stays on the downside. Deeper fall would be seen to 0.9563 support. Decisive break there will argue that whole rise from 0.9252 has completed, and bring deeper fall to 61.8% retracement of 0.9252 to 0.9928 at 0.9510. On the upside, above 0.9673 minor resistance will turn intraday bias neutral first.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004. However, firm break of 0.9563 will suggest that the rally has completed and retain medium term bearishness.

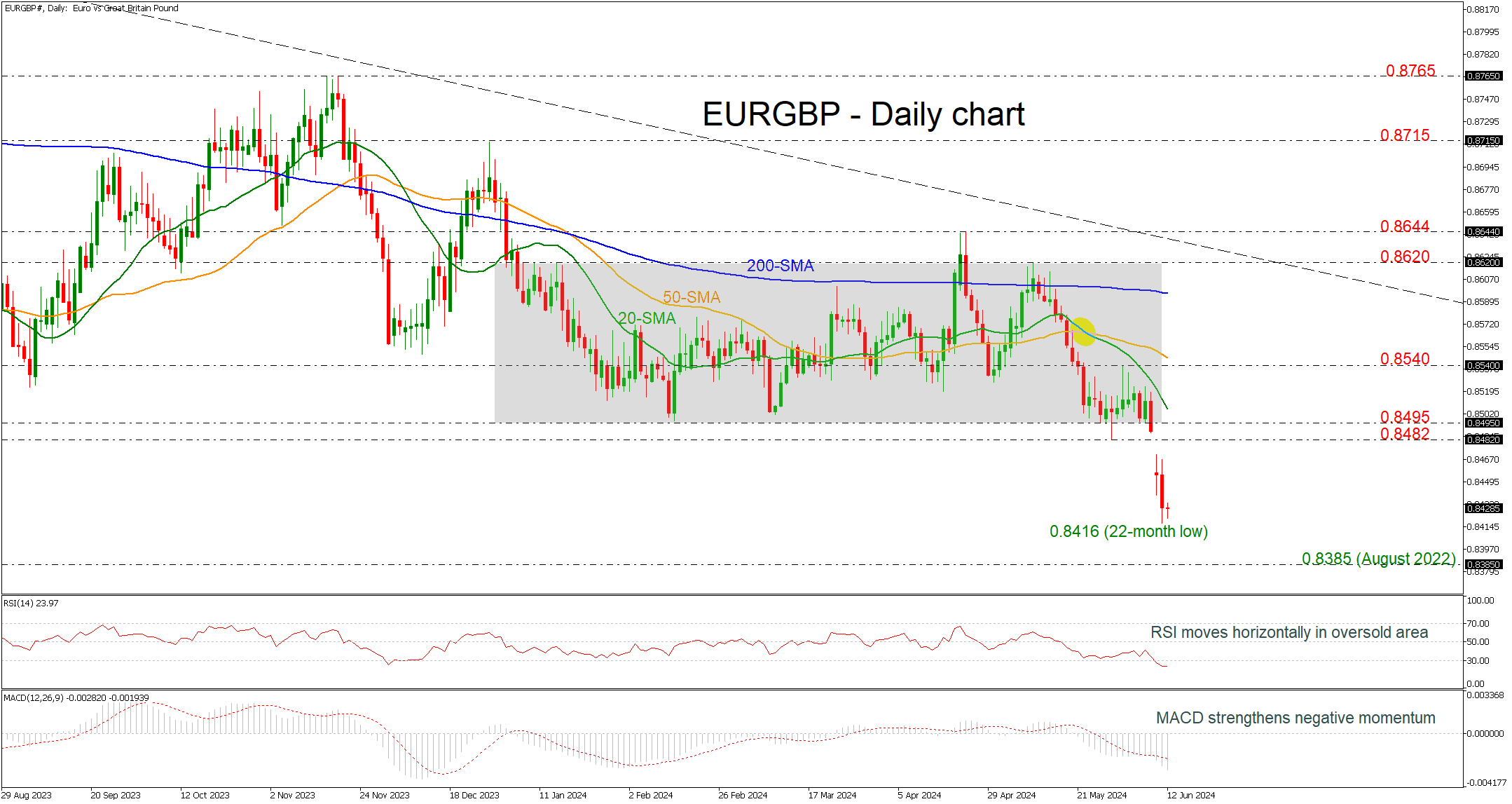

EURGBP Prints New 22-Month Low

- EURGBP continues to fall after bearish gap

- Price shifts neutral outlook to negative

- MACD and RSI hold in oversold regions

EURGBP opened with a significant bearish gap on Monday after the European elections on Sunday, sending the pair towards a fresh 22-month low of 0.8416. The pair is holding well below the medium-term trading range of 0.8495-0.8620, switching the outlook to negative.

Technically, the RSI is standing in the oversold region, while the MACD is looking extremely bearish as it is strengthening its downside momentum beneath its trigger and zero lines. The 20- and the 50-day simple moving averages (SMAs) are also pointing south.

In case of a tumble beneath the multi-month low of 0.8416, this could send the pair until the August 2022 bottom at 0.8385. Even lower, the 0.8340 support level, taken from the lows in July 2022 may halt bearish actions.

On the flip side, a potential rebound near the latest low could take traders to recoup the negative gap and meet the 0.8482-0.8495 resistance region. Above these obstacles, the 20- and the 50-day SMAs at 0.8500 and 0.8545 could be the next targets for the bulls to look for.

To sum up, EURGBP plunged beneath the consolidation area and changed the bias to a more negative one. A climb back above 0.8495 could endorse the view for a possible upside correction.

Market Analysis: EUR/USD Dives While USD/JPY Continues To Rise

EUR/USD gained bearish momentum below the 1.0810 support. USD/JPY is rising and might take out the 157.40 resistance.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline below the 1.0810 support zone.

- There is a connecting bearish trend line forming with resistance at 1.0760 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 155.25 and 156.25 levels.

- There is a connecting bullish trend line forming with support at 156.85 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair struggled to clear the 1.0900 resistance zone. The Euro started a fresh decline and traded below the 1.0810 support zone against the US Dollar, as mentioned in the previous analysis.

The pair even declined below 1.0760 and tested the 1.0720 zone. A low was formed near 1.0719 and the pair is now consolidating losses. On the upside, the pair is now facing resistance near the 23.6% Fib retracement level of the recent decline from the 1.0901 swing high to the 1.0719 low at 1.0760.

There is also a connecting bearish trend line forming with resistance at 1.0760 and the 50-hour simple moving average. The next key resistance is near the 1.0780 level.

The main resistance is 1.0810 or the 50% Fib retracement level of the recent decline from the 1.0901 swing high to the 1.0719 low. A clear move above the 1.0810 level could send the pair toward the 1.0860 resistance.

An upside break above 1.0860 could set the pace for another increase. In the stated case, the pair might rise toward 1.0900. If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.0720.

The next key support is at 1.0680. If there is a downside break below 1.0680, the pair could drop toward 1.0650. The next support is near 1.0620, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a strong increase from the 155.25 zone. The US Dollar gained bullish momentum above 156.25 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 157.00. The current price action above the 157.00 level is positive. A high is formed at 157.40 and the pair might continue to rise. Immediate resistance on the USD/JPY chart is near 157.40.

The first major resistance is near 157.80. If there is a close above the 157.80 level and the RSI moves above 60, the pair could rise toward 158.50. The next major resistance is near 159.20, above which the pair could test 160.00 in the coming days.

On the downside, the first major support is near the 23.6% Fib retracement level of the upward move from the 155.11 swing low to the 157.40 high at 156.85. There is also a connecting bullish trend line forming with support at 156.85.

The next major support is visible near the 50% Fib retracement level of the upward move from the 155.11 swing low to the 157.40 high at 156.25. If there is a close below 156.25, the pair could decline steadily.

In the stated case, the pair might drop toward the 155.25 support zone. The next stop for the bears may perhaps be near the 154.60 region.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Inflation Data and Fed Verdict Could Set Dollar’s Summer Trend

The US currency is gearing up for the most important trading session of the current week, and possibly even the month. Today, the US Consumer Price Index (CPI) data for May will be released. Additionally, the Federal Reserve (Fed) has a meeting scheduled today where the base interest rate will be announced, along with the regulator's dot plot forecast for the rest of the year. Considering that last Friday's employment data exceeded forecasts, many investors and experts (according to an FT-Chicago Booth survey) believe that:

- The Fed will reduce rates by only a quarter of a percentage point this year;

- Instead of three cuts, economists and traders are pricing in up to two rate cuts by the end of the year.

Naturally, such hawkish market expectations are likely to support the strengthening of the US currency. However, it should be noted that the dollar is currently at medium- and long-term highs, and the likelihood of a pullback and the formation of reversal patterns is quite high.

USD/JPY

Following the technical analysis of the USD/JPY pair:

- There is a high probability of testing the May high of this year at 157.70;

- Consolidation above 157.70 could contribute to a renewed rise towards the psychological level of 160.00;

- A rebound or a false breakout at 157.70 could contribute to a return to 155.60-154.80.

EUR/USD

The EUR/USD currency pair is under double pressure. On the one hand, the dollar is strengthening after good labour market data in the US, and on the other hand, there is political uncertainty following the European Parliament elections, the results of which were published at the beginning of the week. Where might the pair head in the upcoming trading sessions?

- In case of weak data for the dollar, the price could attempt to close the "price gap" of Monday at 1.0800;

- A break of the important support level at 1.0710 could contribute to a resumption of the downward movement towards 1.0600.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US in the Spotlights Today

Markets

Market conditions remained sour yesterday. Macron’s political gamble got another layer of uncertainty on rumours that the French president would resign in case of a defeat in the snap elections. While denied later, the genie was out of the bottle. Stocks in Europe remained under pressure. It wasn’t France’s CAC40 (-1.33%) that underperformed this time around, but Borsa Italiana (-1.93%), suggesting spreading market concerns. Both countries as well as Greece saw credit risk premia rising again (both against swap and Germany’s 10-yr) yield). The French spread vs swaps built on Monday’s break above the 2020 high. German bunds attracted a safe haven bid with yields easing between 2 (30-yr) and 6.6 bps (2-yr). US yields traded only a tad lower going into a strong $39bn 10-yr auction which stopped through (4.438% vs 4.458% WI). Bidding metrics were strong with the highest bid-to-cover in more than two years and investors snapping up about 75% of the sale, the most for a 10-yr auction since February 2023. The results contrasted sharply with those for the 3-yr auction on Monday and pushed rates in the US 4.5 to 6.4 bps lower across the curve. Euro weakness prevailed in currency markets. EUR/USD dropped for a third day straight to the lowest since early May (1.074). Some dollar strength was at play too. DXY moved further north of the 105 barrier. EUR/GBP quickly reversed a kneejerk move higher in the wake of the British labour market report to finish at a new YtD low of 0.8418.

The US is in the spotlights today. Tonight’s FOMC meeting is preceded by important CPI numbers. We see upside risks for the headline number (0.1% m/m, 3.4% y/y) and are more neutral on the core reading (0.3%, 3.5%). It serves as some last-minute input for the Fed even though it probably won’t have been factored in into the new projections. The policy rate will remain at an unchanged 5.25-5.5%, directing market’s focus towards the median rate forecasts. The March dot plot projected three rate cuts but that was a close call. We expect that balance to have shifted to two while holding on to the three forecasted for 2025. Markets currently already discount such a combined five cuts and differ only on the timing. In any case, the market reaction may stay muted. Projecting only one cut for 2024 without moving the second to 2025 is a tail risk that may trigger a UST sell-off. It does, however, require a large shift in individual views. We’ll keep a close eye at the long-term projection for the neutral rate, which is likely to have shifted further north. The statement in May adjust to the hawkish side, citing lack of progress towards the 2% inflation target. Eco data since offer few reasons to turn outright dovish with the latest services ISM and payrolls report case in point. But a more balanced tone from chair Powell (e.g. stressing the downturn in manufacturing or the uptick in the unemployment rate) at the presser should even things out a bit. Still, combined with the CPI release we’re more biased towards higher core/US yields. The dollar’s fortunes are at least, if not more, determined by the euro.

News & Views

Bloomberg reports that the US government is considering further restrictions on China’s access to chip technology used for AI, according to people close to the matter. Topic of debate is limiting the ability to use “gate all-around”, a new chip architecture which will be part of the next generation semiconductors to be manufactured withing the next year. There are also early-stage talks about limiting exports of high-bandwidth memory chips, used to train AI software. US Commerce Secretary Raimondo at several occasions stressed that the US will add to existing restrictions as much as needed to keep the most advanced AI technology out of Chinese hands.

Chinese inflation fell by 0.1% M/M on a headline level and by 0.2% M/M for the underlying core series. Both reversed similar increases in April. Consumer goods prices fell for a third month straight with services prices falling into deflation as well in May. Weak consumer demand remains the key reason. In Y/Y-terms, headline and core inflation respectively remained unchanged at 0.3% and slowed from 0.7% to 0.6%. Producer prices recorded a 20th consecutive Y/Y-decline, with the pace slowing though from -2.5% in April to -1.4% in May.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. The German 10y yield set a new YtD top at 2.7%.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed Chair Powell indicated that further tightening was unlikely. However, the FOMC Minutes still showed internal debate on whether policy is restrictive enough. Sticky inflation suggests any rate cut will be a tough balancing act while several policy makers hint at a higher neutral rate. The US 10-y yield is stuck in the 4.3/4.7% trading range.

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. Focus turns to the US side of the story with May CPI inflation numbers and a more hawkish Fed looming on the horizon.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.

US CPI and FOMC Rate Decision Today

In focus today

Today's main events will be the US May CPI at 14.30 CET followed by the FOMC rate decision at 20.00 CET. We expect the Fed to maintain monetary policy unchanged in line with broad consensus and market pricing. The median rate projection on the updated 'dot plot' is likely to signal only two rate cuts this year (prev. three) while economic projections will likely remain little changed, see Research US - Fed preview: No urgency, 7 June. We forecast headline CPI inflation at 0.19% m/m SA (Prior: 0.3%; Cons: 0.3%) and Core CPI at 0.25% m/m SA (Prior: 0.29%; Cons: 0.3%). We see risks tilted towards a dovish market reaction over the course of the day.

In the UK we get the monthly GDP figures for April. After a strong start to the year Q1 growth at 0.6% q/q, consensus expects a more muted print at 0.0% m/m for April.

In Germany, we receive the final inflation figures for May. The monthly increase in services inflation was very strong and the details will show much of this was due to the one-off increase in airfare taxes that increased by 19% on May 1 and how much was broad-based pressures.

Economic and market news

What happened overnight

In China the CPI print came in at 0.3% y/y (Cons: 0.4%, Prior: 0.3%) while the PPI came in at -1.4% (Cons: -1.5%, prior: -2.5%). Overall, the print still shows deflationary pressures in China with m/m change at -0.1%. Weak consumption is still supporting low prices and consumer confidence, despite several rounds of support measures.

What happened yesterday

ECB's Lane said Yesterday that ECB should wait with its next rate cut until uncertainty recedes. Lane argued that the key unknown is wage growth, saying that the bank will need to maintain a restrictive monetary stance. The comment seems in line with President Lagarde's interview on Monday, when she said that ECB could wait more than one meeting between cuts. On the other hand, Villeroy sounded way more dovish saying that there is 'significant leeway' to cut rates and still stay restrictive and that further cuts should be made without haste or procrastination. We expect the ECB to cut interest rates once more in 2024 at the December meeting.

10y French government bond yields widened further vs. 10y German bunds to 60bp, up from 55bp on Monday and 47bp on Friday. The French Cac 40 stock index fell to its lowest point since February. The changes show that markets still worry about future economic policy after President Macron called a snap parliament election. His party gained only around half the votes of primary presidential opponent Le Pen's party Rassemblement National (RN) at Sunday's European Parliament (EP) election. Macron has announced policies to strengthen public finances and reduce government debt. If RN gains majority markets see a risk that the French government will withdraw these actions and increase the budget deficit even more. Often the EP elections have been protest elections in France, not necessarily meaning that the same result will show in national elections. From here we look out for the two elections dates on 30 June and especially second round 7 July, where the final election result is determined.

In the US we got mixed signals from the May edition of NFIB's small business survey. The general optimism and future outlooks edged cautiously higher (albeit from a low level). At the same time, uncertainty rose to the highest level since the previous election month of November 2020. Price plans rose slightly from April but remain below Q1 levels. All-in-all, nothing that should move the markets here.

In the UK, the labour market report for April/May was to the weak side. Wage growth excl. bonus remains at 6.0% 3M/YoY (cons: 6.1%, prior: 6.0%) with the increase in the National Living Wage taking effect in April underpinning wage growth. While the report acts as input, the BoE has highlighted that it looks at a range of indicators to assess the tightness of the labour market noting the poor data quality of the survey.

Market movements

Equities: Global equities ended marginally lower yesterday, with the US pushing higher and ending close to the day's highs, while Europe, led by the peripherals, trended lower. We must admit i'’s surprising for us to see the European Parliament election, the subsequent announcement by Macron, the cut of Frenc credit rating having such a significant market impact. The bond spread between Germany and the peripherals, including France, widened considerably again yesterday, with banks underperforming. It is worth noting that banks were also a notable underperformer in the US yesterday. The politically driven markets are not behaving as we have been advocating for, and both sector and regional rotations are not going in our favour. In the US yesterday, the Dow was down by 0.3%, the S&P 500 was up by 0.3%, the Nasdaq increased by 0.9%, and Russell 2000 decreased by 0.4%. Asian markets are mixed this morning, while both European and US futures are trending higher.

FI: European rates were bid through most of the day driven by dovish comments from Villeroy where he said that there is'‘significant leewa'’ to cut rates and still stay restrictive and that further cuts should be made without haste or procrastination. Earlier in the morning Lagarde said that the'‘appropriate decisio'’ last week'‘does'’t mean interest rates are on a linear declining path. There might be periods where we hold rates agai'’. Bunds ended 5bp lower on the day at 2.62%.

FX: EUR sold off further yesterday against most of G10 amid French political uncertainty with EUR/USD trading close to the 1.07 mark. In this regard, we also note that EUR/CHF and EUR/DKK has dropped in recent days-– an early sign of rising safe-haven demand in currency markets.