Sample Category Title

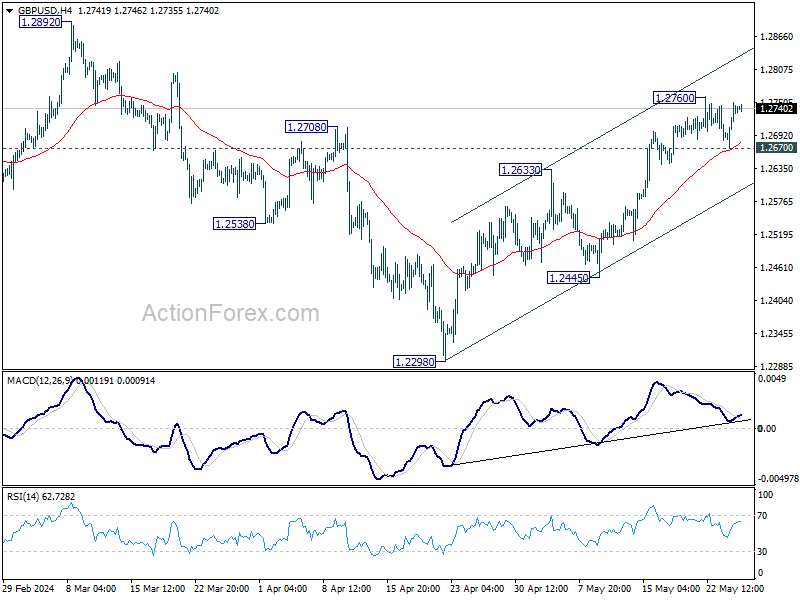

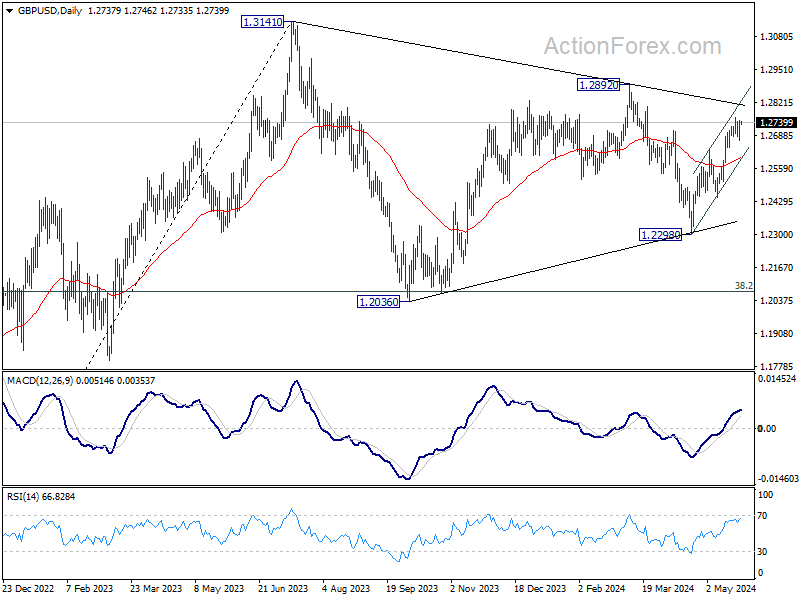

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2692; (P) 1.2721; (R1) 1.2767; More...

Intraday bias in GBP/USD stays neutral and further rise is in favor with 1.2670 support intact. Above 1.2760 will resume the rally from 1.2298 to 1.2892 resistance next. On the downside, below 1.2670 will turn bias to the downside for deeper pull back.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

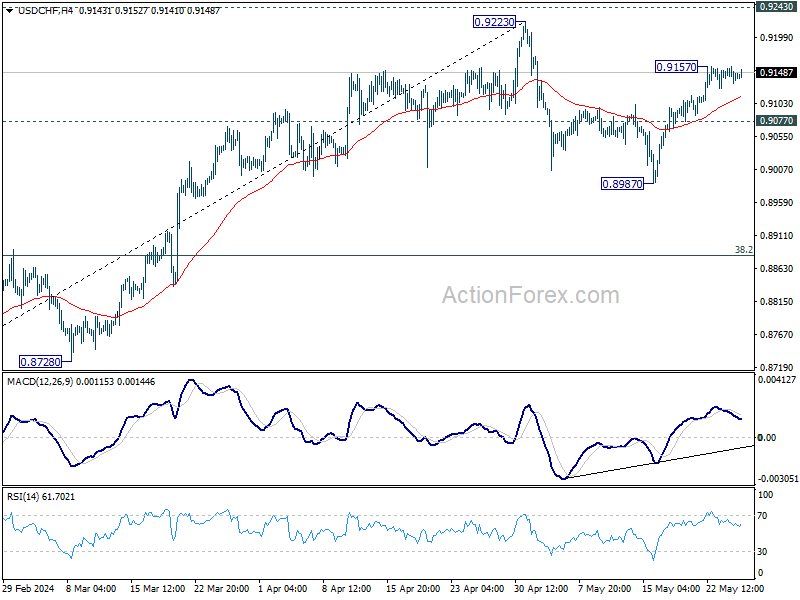

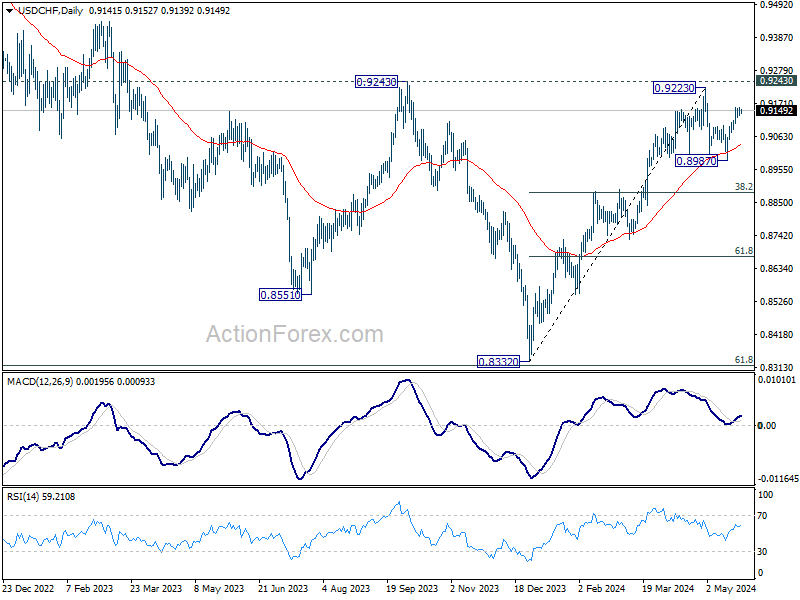

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9134; (P) 0.9146; (R1) 0.9160; More....

Intraday bias in USD/CHF remains neutral for the moment. Current development suggests that pull back from 0.9223 has completed already. Above 0.9157 will bring retest of 0.9223. However, break of 0.9077 support will bring retest of 0.8987. Break there will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Trading Probably Will Take a Slow Start

Markets

With investors looking ahead to a long weekend in the US and the UK; the upleg in core yields slowed on Friday. US and EMU yields closed with changes of less than 1.5 bps across the curve. US durable goods orders (+0.7% M/M) and core shipments (+0.4% M/M) printed stronger than expected, but coming after a downward revision of the March figures. Inflation expectations from the U. of Michigan consumer confidence survey faced a downward revision as well and helped to soften the yield rally. Fed’s Waller elaborated on the topic of a potentially higher neutral US interest rate. This topic will remain in focus as a further rise of the neutral estimate in the June dots is very much possible. Especially in a context where disinflation slows, this might fuel the debate whether Fed policy is tight enough to bring inflation back to target in a timely manner. The Minutes of the May meeting earlier last week showed that the FOMC wasn’t that sure that policy indeed shouldn’t be tightened any further. After last week’s repositioning, US markets now again scaled back the possibility of a September Fed rate cut to about 50%, with markets also seeing only one rate cut this year. The German 2-y yield and EMU 2-y swap rate finished the week at a YtD closing peak. An ECB June rate cut is not put into question anymore, but strong PMI’s and higher than expected Q1 negotiated wages published on Thursday, suggested that the room for follow-up easing might be limited in H2. Equities showed resilience despite the ‘hawkish repositioning’ in bond markets last week. A bearish engulfing pattern on US indices on Thursday didn’t trigger any further follow-through losses. The Nasdaq even rebounded 1.1%. The dollar gained ground last week, but momentum dwindled end last week. EUR/USD still finished the week at 1.0847. So the 1.0895 correction top still isn’t that far away.

Trading probably will take a slow start as US (Memorial Day) and UK markets (Spring Bank Holiday) are closed. German Ifo Business climate should confirm last week’s positive PMI’s and might provide further downside protection for EMU yields and the euro, admittedly in thin market conditions. Later this week, markets will keep a close eye at the April US PCE deflators and the first estimate of the EMU May inflation. US PCE deflators (headline and core) are expected to stabilize at 0.3%, confirming the message from the CPI published earlier this month. EMU (headline) inflation is expected at a modest 0.2% M/M, but unfavourable base effects still might lift the Y/Y measures (2.5% headline, 2.8% core). For now, we don’t see much of a trigger for markets to reverse the recent higher-for longer repositioning. Better EMU eco data also keep EUR/USD near the topside of the 1.0725/1.09 ST trading range.

News & Views

BoJ governor Ueda in an opening speech to a BoJ-hosted conference in Tokyo said Japan has progressed in lifting inflation expectations after a long period of deflation and ultra-easy monetary policy. He said the central bank will proceed cautiously to achieve 2% inflation, a target which is now being overshot for about two years in the wake of the pandemic and supply-side shocks. Ueda explained a gradual approach is necessary because "The absence of significant interest rate movements poses a considerable obstacle in assessing the economy's response to changes in interest rates,” referring to the extreme difficulty of estimating the country’s level of the neutral rate. The BoJ ended negative rates back in March and is seen hiking modestly further later this year. Japan’s 10-yr yield also topped 1% last Friday amid rising speculation the central bank will soon begin to taper its bond-buying programme. The BoJ is also under pressure from the historically weak yen. Despite the prospect of further monetary normalization, the spread with the likes of the US remains huge. USD/JPY currently trades just south of 157.

France’s PM Attal released a plan to reduce French jobless benefits as he tries to bring traction to president Macron’s economic reforms. The main goal of cutting the maximum duration of welfare to 15 months from 18 months and lengthen the period of work required to qualify for benefits is to get more people into jobs. It also comes with gradual lower government spending over the next few years. France’s high debt burden and budget deficits are in the spotlights recently with the IMF last week issuing a stark warning to bring things under control. Rating agencies have been highlighting the issue as well. France dodged two bullets end April with Moody’s and Fitch keeping the rating unchanged and the outlook stable. But S&P makes an assessment May 31 and holds a negative outlook.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target.. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell indicated that further tightening was unlikely. Soft US early month data triggering a correction off YTD peak levels. However, the Fed minutes still showed internal debate whether policy is restrictive enough. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already proved strong support for the US 10-y yield.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view but slower than expected April disinflation and a surprise general election on July 4 complicated matters. A June cut in line with the ECB looks improbable. Sterling extends a recent bull rally. A test of EUR/GBP’s 2024 YtD low (0.8489) is possible. We expect this important support level to hold.

Quiet Start to a Week Where Inflation Will Be in Focus

In focus today

The week kicks off with a very light schedule.

We receive the Germany Ifo indicator for May at 10.00 CET. The past two months have seen an increase in the assessment of the business situation, and it will be interesting to see if this continued in May.

The US is out today for Memorial Day, and the UK is out for the Spring bank holiday. Trading resumes Tuesday in both markets.

Elsewise, ECB's Schnabel, SNB's Jordan, Fed's Mester and Bowman, and BoJ's Himino (all voting members of their central banks) will participate in a panel discussion in Tokyo on monetary policy tomorrow morning (06.55 CET).

For the remainder of the week, we will especially be looking out for consumer confidence, GDP and PCE inflation data out of the US, unemployment, and CPI numbers out of the euro area, as well as PMIs out of China and Tokyo CPI out of Japan.

Economic and market news

What happened over night

In Asia, Chinese premier met with colleagues from Japan and South Korea for the first time in four years in three-way talks. Chinese premier Li Qiang heralded the meeting a new start to their relationship, as Japanese media reported the three nations might restart free-trade negotiations that had been on hold since 2019.

In China, industrial profits came out showing monthly growth again in April at 4% up from the -3.5% slide seen in March. The growth for the first four months of the year stood at 4.3% y/y.

Asian equity markets are trading in the green this morning, and oil is up slightly with Brent trading at around USD 82.3/bbl this morning.

What happened Friday and over the weekend

In Japan, inflation declined further as CPI excluding fresh food stood at 2.2% in April down from 2.6% in March. The declining inflation constitutes an obstacle to the Bank of Japan (BoJ) to hike rates further, albeit we are still waiting to see the solid spring wage increases take effect. Regained purchasing power and stronger private spending is what the BoJ is hoping for to pull the economy back into growth mode.

In the US, University of Michigan surveys of consumer expectations of inflation 1 and 5 years ahead showed downwards revisions to the initial releases of both April and May numbers. For May the final figures stood at 3.3% and 3.0% respectively for the 1 and 5 years ahead expectations. Yields were more or less flat by the end of Friday's session, whereas equity markets ended in the green with especially the Nasdaq and S&P500 rising, gaining 1.1% and 0.7% respectively.

In the euro area, we revised our expectations for the ECB policy rate path following a stronger economic start to the year coupled with sticky inflation. We removed our expectation for a September cut, yet still expect a cut during next week's meeting. The following one is projected to follow in December, see more in ECB preview - A political rate cut in June, and no cut in September, 24 May.

In the world of shipping, the cost of shipping containers continues to climb as complications in the Red Sea persist, the Financial Times reported. Prices have soared as businesses have begun preparing for the festive season earlier than usual in an attempt to avoid issues related to the disruption of supply chains caused by the attacks in the Red Sea by the Houthis in Yemen. Latest price data from last week show short-term contracts on routes from the Far East to North Europe and the US West Coast costing USD 4,677 and USD 4,760. Both indices are thus within striking distance of their peaks from earlier in the year when western nations led by the US and UK first began attacks on the Houthis, and shipping companies started swithdrawing from the Red Sea in response to the increased threat level.

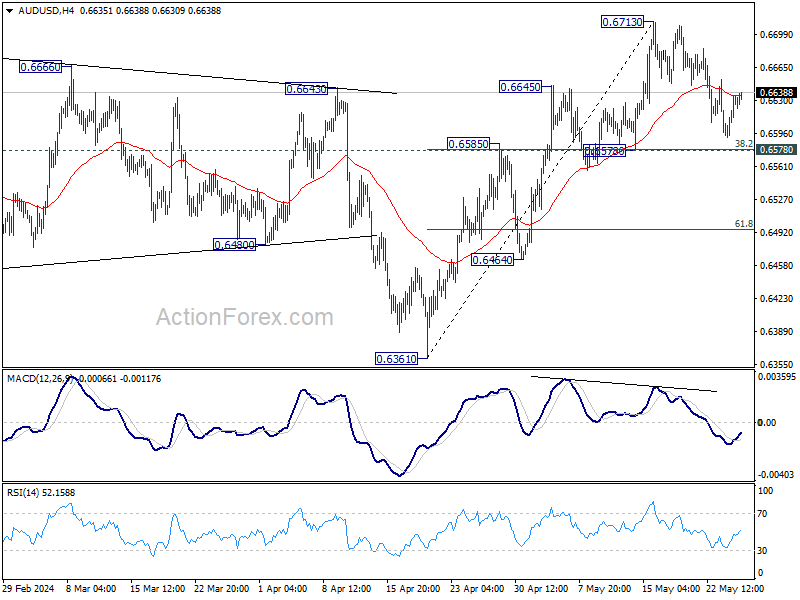

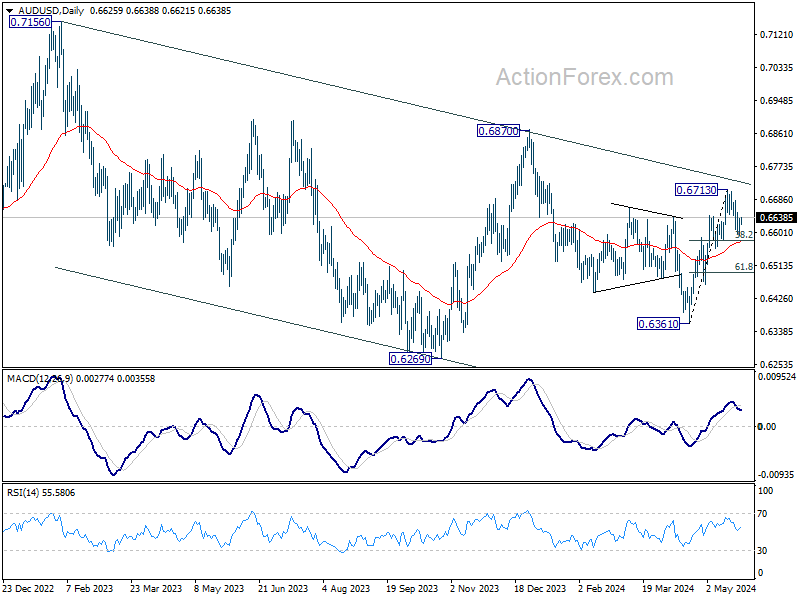

AUD/USD Daily Report

Daily Pivots: (S1) 0.6602; (P) 0.6619; (R1) 0.6647; More...

Intraday bias in AUD/USD remains neutral for the moment. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579 intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, firm break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

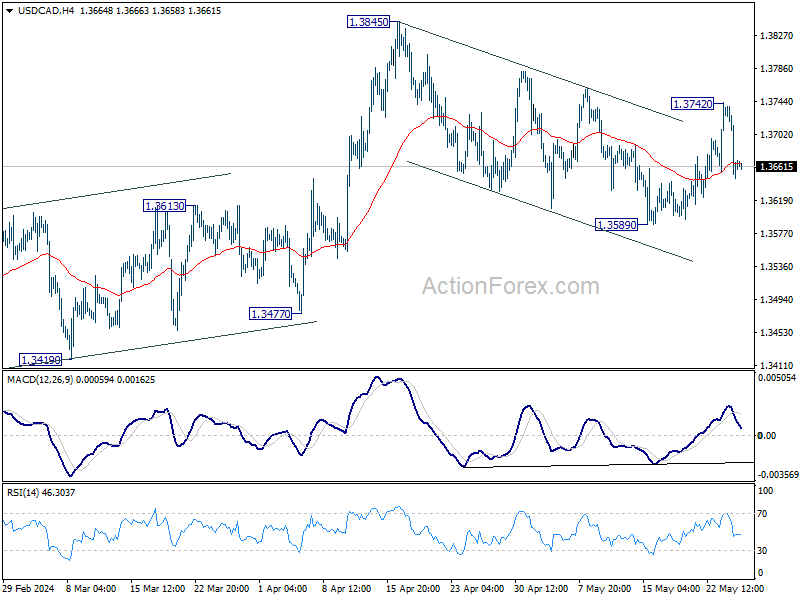

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3628; (P) 1.3684; (R1) 1.3721; More...

Intraday bias in USD/CAD remains neutral this week first. On the upside, break of 1.3742 will affirm the case that correction from 1.3845 has completed at 1.3589. Further rally would then be seen to retest 1.3845 high. However, sustained trading below 55 D EMA (now at 1.3637) will argue that whole rise from 1.3176 has completed already.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

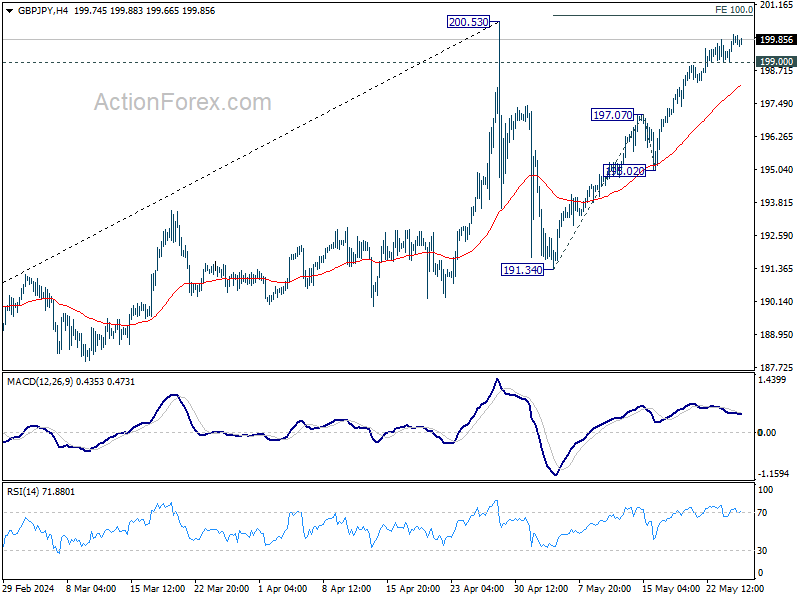

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.24; (P) 199.66; (R1) 200.37; More...

Intraday bias in GBP/JPY remains on the upside for 100% projection of 191.34 to 180.07 from 195.02 at 200.75. But upside should be limited there. On the downside, below 198.25 minor support will turn intraday bias neutral first. Further break of 197.07 will argue that the third leg of the corrective pattern from 200.53 has started, and target 191.34 support and possibly below.

In the bigger picture, a medium term top could be in place at 200.53 after breaching 199.80 long term fibonacci level. As long as 55 W EMA (now at 183.92) holds, price actions from there is seen as correcting the rise from 178.32 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 178.32 support.

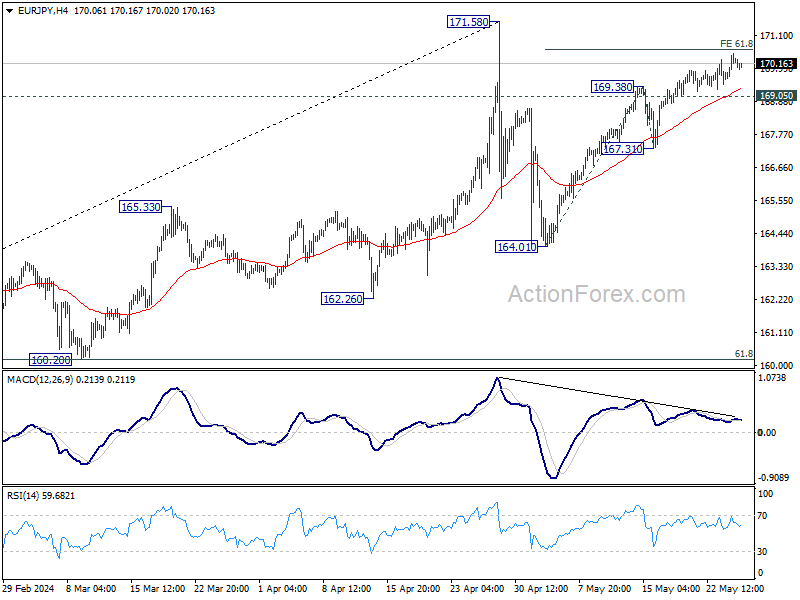

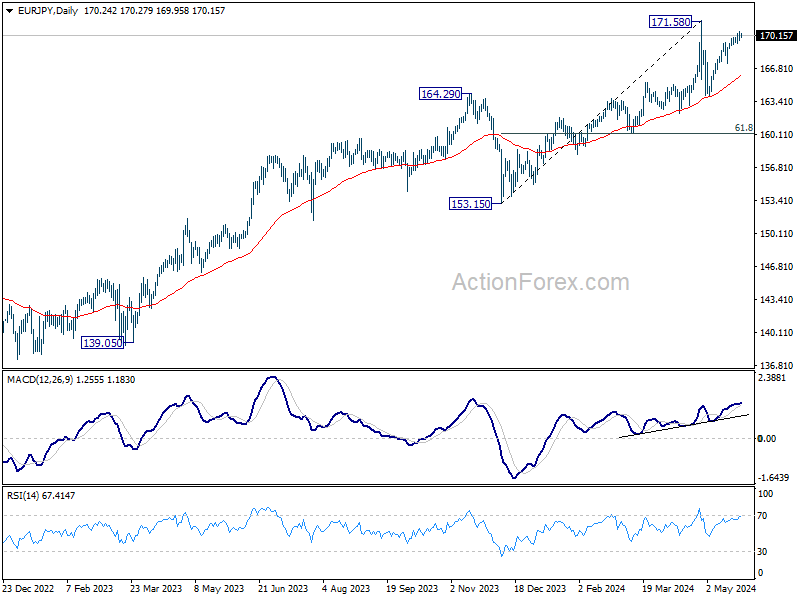

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.72; (P) 170.11; (R1) 170.64; More...

Intraday bias in EUR/JPY remains on the upside for 61.8% projection of 164.01 to 169.38 from 167.31 at 170.62, and then 171.58 high. On the downside, break of 169.05 minor support will intraday bias neutral first. Further break of 167.31 should turn bias back to the downside to start the third leg of the corrective pattern from 171.58 towards 164.01.

In the bigger picture, a medium top could be formed at 171.58 after brief breach of 169.96 (2008 high). As long as 55 W EMA (now at 158.72) holds, price actions from there is seen as correcting the rise from 153.15 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

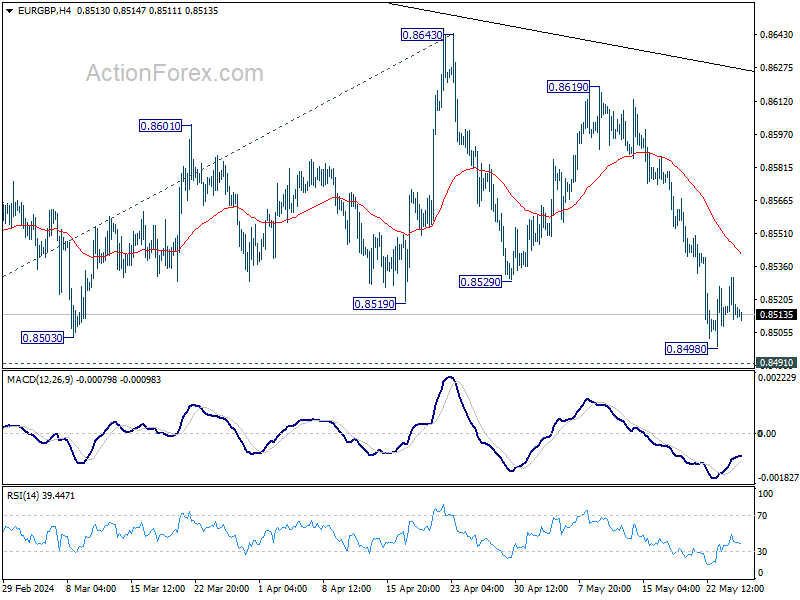

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8508; (P) 0.8520; (R1) 0.8528; More...

Intraday bias in EUR/GBP remains neutral for the moment, and further decline is expected as long as 55 D EMA (now at 0.8561) holds. Decisive break of 0.8491/7 will resume larger down trend to 0.8376 projection level next.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

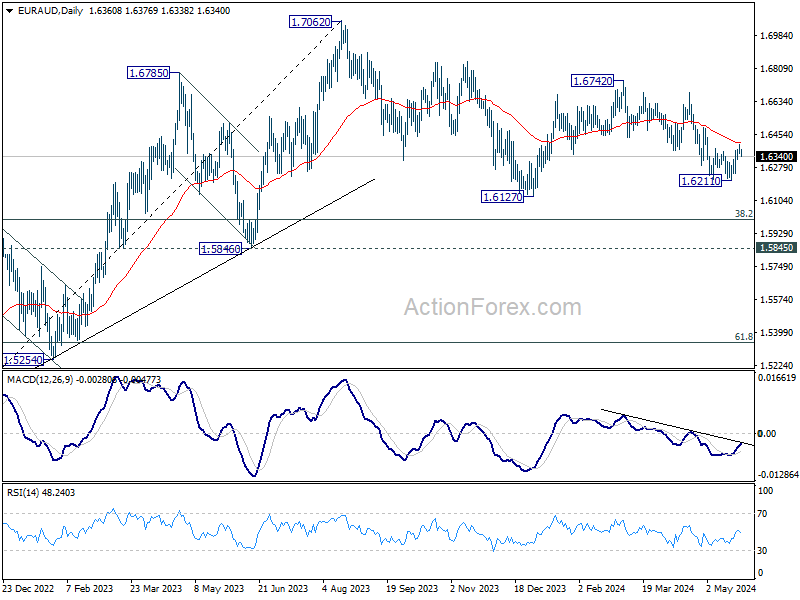

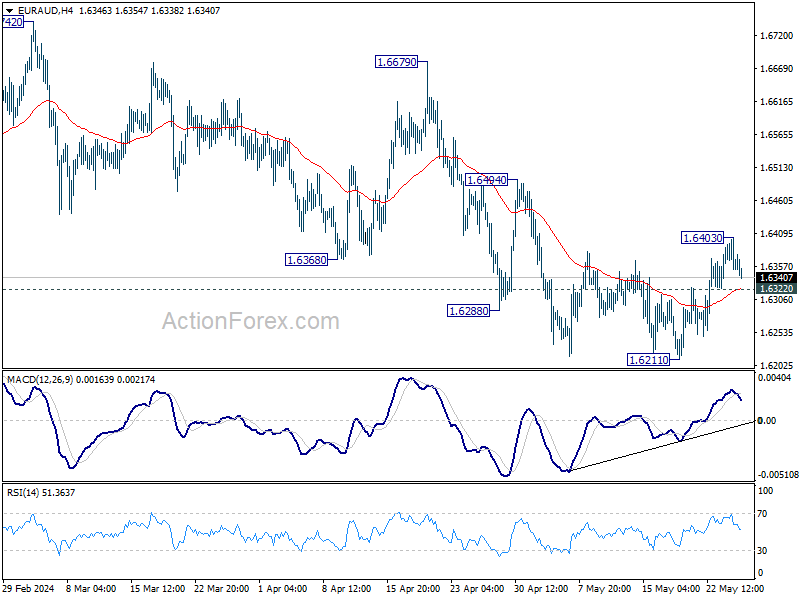

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6343; (P) 1.6374; (R1) 1.6394; More...

Intraday bias in EUR/AUD is turned neutral first with current retreat. On the downside, break of 1.6322 minor support will indicate rejection by 55 D EMA (now at 1.6408). Deeper fall would be seen to retest 1.6211. Firm break there will resume the whole decline from 1.6742, as the third leg of the correction from 1.7062. On the upside, above 1.6403 will resume the rebound from 1.6211 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.