Sample Category Title

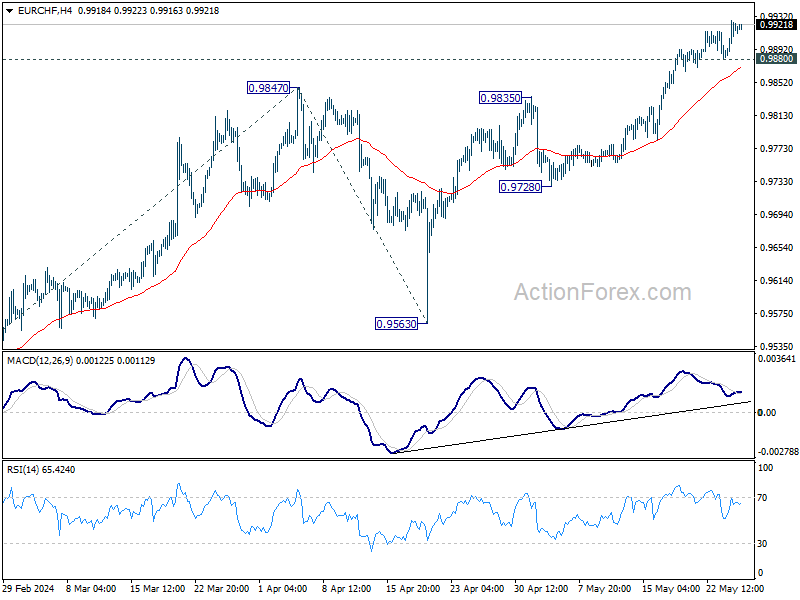

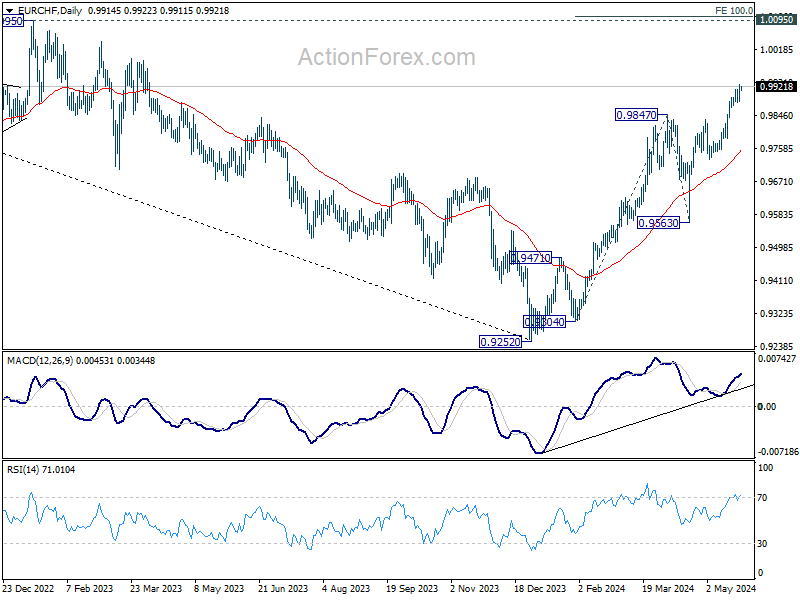

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9894; (P) 0.9911; (R1) 0.9939; More....

Intraday bias in EUR/CHF is now on the upside this week as recent rally continues. Current rise from 0.9252 should target 100% projection of 0.9304 to 0.9847 from 0.9563 at 1.0106, which is slightly above 1.0095 key structural resistance. On the downside, below 0.9880 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, as long as 0.9728 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004.

Subdued Holiday Trading Precedes Key Inflation Data Releases

Trading has been characteristically subdued in the Monday's Asian session. Japanese Yen is have a broad but weak recovery, with no clear indication of a reversal from its recent selloff. Australian and New Zealand Dollars are also mildly firmer, following rebound in Asian stocks. Meanwhile, Swiss Franc and Euro are among the softer currencies, while British Pound and Dollar are mixed.

Activity in the markets is likely to remain low, compounded by the holidays in both the UK and the US. However, traders are expected to return with heightened focus as significant inflation data from the US, Eurozone, Australia, and Japan are scheduled for release, alongside other important economic indicators from Canada, Swiss and China.

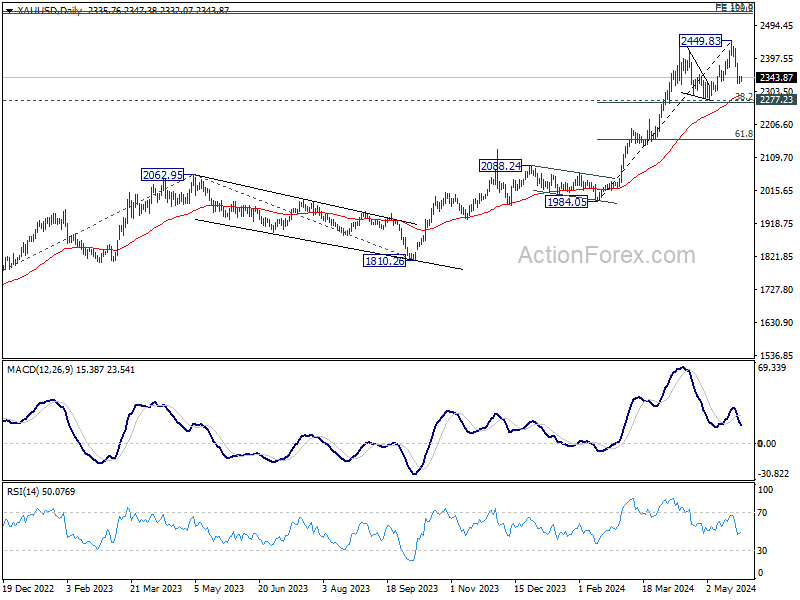

Technically, Gold's rally was cut short after hitting 2449.83 but there is no clear sign of trend reversal yet. As long as 2277.34 cluster support holds (38.2% retracement of 1984.05 to 2449.83 at 2271.90) further rally is still expected. The real test for Golds lies in 2500 psychological level, which is close to 161.8% projection of 1614.60 to 2062.95 from 1810.26 at 2535.69.

In Asia, Nikkei rose 0.66%. Hong Kong HSI is up 1.14%. China Shanghai SSE is up 0.75%. Singapore Strait times is up 0.11%. Japan 10-year JGB yield rose further by 0.0163 to 1.026.

ECB's Lane frames 2024 policy debate to determining degree of reduced restrictiveness

In an interview with the Financial Times, ECB Chief Economist Philip Lane indicated that, barring major surprises, there is sufficient evidence to "remove the top level of restriction" in June, suggesting an initial reduction in the 4.00% deposit rate. He noted that the forthcoming data over the next few months will guide ECB in determining the pace at which further restrictiveness can be eased.

Lane acknowledged that the path to disinflation will be "bumpy and gradual." He framed the debate for this year by stating that ECB still "needs to be restrictive all year long," but within this "zone of restrictiveness," there is potential to "move down somewhat."

He added, "We don't need the data to say normalization is a lock. What we do need the data to say is: is it proportional, is it safe, within the restrictive zone to move down."

Looking ahead to next year, Lane mentioned that discussions about the "normalization" of monetary policy will be more pertinent when wage growth has visibly decelerated and the inflationary impacts of current fiscal measures have diminished.

BoJ's Ueda: Neutral rate estimation a unique challenge for Japan

In a speech today, BoJ Governor Kazuo Ueda reiterated the central bank's commitment to achieving sustainable and stable 2% inflation. He acknowledged the progress made in "moving away from zero" and "lifting inflation expectations," but underscored the need to "re-anchor" them at 2%.

Ueda stressed the importance of a cautious approach, aligning with other central banks that employ inflation-targeting frameworks. However, he highlighted that some challenges are "uniquely difficult" for Japan.

A notable example is determining the "neutral interest rate," a task complicated by Japan's "prolonged period" of near-zero short-term interest rates over the past three decades. This historical context makes it particularly challenging to estimate the neutral rate accurately.

Despite some fluctuations in real interest rates, the lack of significant interest rate movements remains a "considerable obstacle" for BoJ. This impedes their ability to assess the economy's response to changes in interest rates effectively.

BoJ's Uchida: Deflation battle nears end, but anchoring inflation expectations remains a challenge

In a speech today, BoJ Deputy Governor Shinichi Uchida expressed optimism that the end of Japan's long battle against deflation is "in sight." However, he emphasized that there remains a "big challenge" in anchoring inflation expectations at 2% target.

Uchida pointed out that it is "not so clear" whether Japan has fully overcome the "deflationary norm." A critical question is whether companies will maintain their current price-setting behaviors once the global inflationary pressures subside. He highlighted the importance of the labor market in this context.

"If the structural changes in the labor market continue, companies will have to build business models that generate enough profits and wages to keep and attract employees," Uchida noted. Regarding price-setting strategies, he added that companies need to "rewrite their prices in their menus promptly," reflecting labor costs while considering the potential impact on product demand.

The week's spotlights on inflation data from US, Eurozone, Australia, and Japan

Inflation data from several major economies will be under intense scrutiny this week. Although these data points may not directly impact imminent monetary policy decisions, they will significantly influence interest rate outlook for the remainder of the year.

In the US, PCE data is anticipated to reflect the trends observed in recent CPI reports, which indicated resumed cooling in both headline and core inflation. Unless there are unexpectedly large deviations, it is likely that the probabilities of a Fed rate cut in September will remain broadly unchanged at 50/50.

Moving to Europe, preliminary CPI for Eurozone might register a modest increase in May, with the core CPI expected to remain stable. This shouldn't change ECB's plan to reduce interest rates in June. But prospects for a follow-up rate cut in July seem minimal unless economic conditions deteriorate significantly.

In Australia, slight moderation is forecasted in monthly CPI for April. Such a trend would support RBA decision to maintain the current interest rate well into late 2024. However, any unexpected increase in inflation could tilt the balance towards an interest rate hike in the latter half of the year.

Japan's focus will be on Tokyo CPI, where a rebound in core inflation within the capital is anticipated. Yet, it remains premature for BoJ.

Additionally, other economic indicators such as US consumer confidence, Canadian GDP, Australian retail sales, Swiss GDP, and China's NBS PMIs.

Here are some highlights for the week:

- Monday: German Ifo business climate.

- Tuesday: Japan corporate service price; Australia retail sales; Canada IPPI and RMPI; US house price index, consumer confidence.

- Wednesday: New Zealand ANZ business confidence; Australia CPI; German Gfk consumer sentiment; Germany CPI flash; Swiss UBS economic expectations; Eurozone M3 money supply; Fed's Beige Book.

- Thursday: Australia building approvals, private capital expenditure; Swiss trade balance, GDP, KOF economic barometer; Eurozone unemployment rate; Canada current account; US GDP revision, jobless claims, goods trade balance, pending home sales.

- Friday: Japan Tokyo CPI, unemployment rate, industrial production, retail sales; China NBS PMIs; German import prices, retail sales; Swiss retail sales; UK M4 money supply, mortgage approvals; Eurozone CPI flash; Canada GDP; US personal income and spending, PCE inflation, Chicago PMI.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9894; (P) 0.9911; (R1) 0.9939; More....

Intraday bias in EUR/CHF is now on the upside this week as recent rally continues. Current rise from 0.9252 should target 100% projection of 0.9304 to 0.9847 from 0.9563 at 1.0106, which is slightly above 1.0095 key structural resistance. On the downside, below 0.9880 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, as long as 0.9728 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate May | 90.3 | 89.4 | ||

| 08:00 | EUR | Germany IFO Current Assessment May | 89.9 | 88.9 | ||

| 08:00 | EUR | Germany IFO Expectations May | 90.5 | 89.9 |

It’s Been a Roller-Coaster Month

We had a roller-coaster month of May in terms of central bank expectations. The month began with the Federal Reserve’s (Fed) decision to hold the interest rates steady, and Jerome Powell saying that the Fed’s next move will probably NOT be a rate cut. The latter had sent the markets rallying with enthusiasm. Then, the US jobs data came in softer-than-expected, and inflation didn’t surprise to the upside for the 4th straight month – but producer prices came in hotter-than-expected, and the Fed members kept giving hawkish speeches one after the other, repeating insistently that the rates are good where they are and that cutting them is not necessarily a good idea. Markets’ bull had an ear on the avalanche of Fed comments without necessarily putting too much focus on them, until last week’s Fed minutes revealed an inconvenient truth: that ‘many’ Fed members questioned whether keeping the rates high for longer is enough restrictive to continue the inflation battle, and if hiking rates wouldn’t be more effective. And the mood finally darkened. This is where we are right now.

While last week began on optimism that inflation could allow the Fed to cut rates as early as in September, this week begins on pessimism that the latter will probably not be possible. The US markets are closed today, but the US 2-year yield ended last week near 4.95% and the probability of a September cut fell to a coin flip. But regardless, the US stock markets continue to trade near record levels. The S&P500 and Nasdaq both closed last week a few points below their ATH levels, boosted by a fresh shot of energy after Nvidia reported another set of blowout results and a strong forecast – under these conditions, it will be hard for the tech rally to expand to the rest of the market.

In China and nearby, the CSI 300 and HSI index are better bid this Monday morning following a correction last week – which brought sellers back to the market before the HSI index got the opportunity to test the 20K psychological resistance. The Chinese stimulus measures are supportive of gains, but the rising tensions with the West are threatening the Chinese companies’ revenue expectations. In this beautiful context of rising trade tensions, G7 leaders took the opportunity to further escalate tensions with China at their weekend summit – after the US re-imposed tariffs on hundreds of goods (Biden’s only hope to improve his popularity for the November election). China’s EV makers are on the front line as China became the world’s biggest car exporter. The latest news are about to derail the BYD rally. The stock is preparing to test the 200 support to the downside.

Here in Europe, investors will also be focused on fresh inflation data for May. The headline inflation may have advanced from 2.4% to 2.5% while core inflation is seen steady near the 2.7% level. The European Central Bank (ECB) is expected to start cutting the rates next month. Therefore, if this week’s inflation data shows no surprise, the dovish divergence between the ECB and the Fed should prevent the EURUSD from clearing the 1.09 offers. Against sterling, the euro is sitting on a critical support, the 0.85 level. A hotter-than-expected inflation report from the UK brought the Bank of England (BoE) hawks to the battle field last week, but uncertainties surrounding an upcoming and a too-early general election in the UK will hardly let the pair gain momentum below this level. Elsewhere, the USDJPY is slightly better bid this morning as the Bank of Japan (BoJ) Governor Ueda said that he doesn’t have a ‘big problem’ after the Japan 10-year yield hit a 12-year high last week. If the BoJ leaves the yields to themselves, north is the only possible direction as the country’s debt-to-GDP is at least double the other G7 nations. But we know that they won’t do that – and we also know that the BoJ can’t sustainably counter the yen selloff. As such, buying the Japanese yen still doesn’t look convincing – even at the current levels.

Elsewhere, US crude fell to and rebounded from $76.40pb on Friday on waning reflation trade (due to a significant retreat in Fed cut expectations). OPEC countries will meet this week and probably announce to extend supply cuts into the second half of the year in an attempt to set a floor under the actual selloff. But if the global central banks don’t play along, it will be hard for OPEC to keep oil prices sustained. US crude could extend losses toward the $75pb level if OPEC fails to boost appetite at this week’s announcement.

ECB’s Lane frames 2024 policy debate to determining degree of reduced restrictiveness

In an interview with the Financial Times, ECB Chief Economist Philip Lane indicated that, barring major surprises, there is sufficient evidence to "remove the top level of restriction" in June, suggesting an initial reduction in the 4.00% deposit rate. He noted that the forthcoming data over the next few months will guide ECB in determining the pace at which further restrictiveness can be eased.

Lane acknowledged that the path to disinflation will be "bumpy and gradual." He framed the debate for this year by stating that ECB still "needs to be restrictive all year long," but within this "zone of restrictiveness," there is potential to "move down somewhat."

He added, "We don't need the data to say normalization is a lock. What we do need the data to say is: is it proportional, is it safe, within the restrictive zone to move down."

Looking ahead to next year, Lane mentioned that discussions about the "normalization" of monetary policy will be more pertinent when wage growth has visibly decelerated and the inflationary impacts of current fiscal measures have diminished.

BoJ’s Uchida: Deflation battle nears end, but anchoring inflation expectations remains a challenge

In a speech today, BoJ Deputy Governor Shinichi Uchida expressed optimism that the end of Japan's long battle against deflation is "in sight." However, he emphasized that there remains a "big challenge" in anchoring inflation expectations at 2% target.

Uchida pointed out that it is "not so clear" whether Japan has fully overcome the "deflationary norm." A critical question is whether companies will maintain their current price-setting behaviors once the global inflationary pressures subside. He highlighted the importance of the labor market in this context.

"If the structural changes in the labor market continue, companies will have to build business models that generate enough profits and wages to keep and attract employees," Uchida noted. Regarding price-setting strategies, he added that companies need to "rewrite their prices in their menus promptly," reflecting labor costs while considering the potential impact on product demand.

BoJ’s Ueda: Neutral rate estimation a unique challenge for Japan

In a speech today, BoJ Governor Kazuo Ueda reiterated the central bank's commitment to achieving sustainable and stable 2% inflation. He acknowledged the progress made in "moving away from zero" and "lifting inflation expectations," but underscored the need to "re-anchor" them at 2%.

Ueda stressed the importance of a cautious approach, aligning with other central banks that employ inflation-targeting frameworks. However, he highlighted that some challenges are "uniquely difficult" for Japan.

A notable example is determining the "neutral interest rate," a task complicated by Japan's "prolonged period" of near-zero short-term interest rates over the past three decades. This historical context makes it particularly challenging to estimate the neutral rate accurately.

Despite some fluctuations in real interest rates, the lack of significant interest rate movements remains a "considerable obstacle" for BoJ. This impedes their ability to assess the economy's response to changes in interest rates effectively.

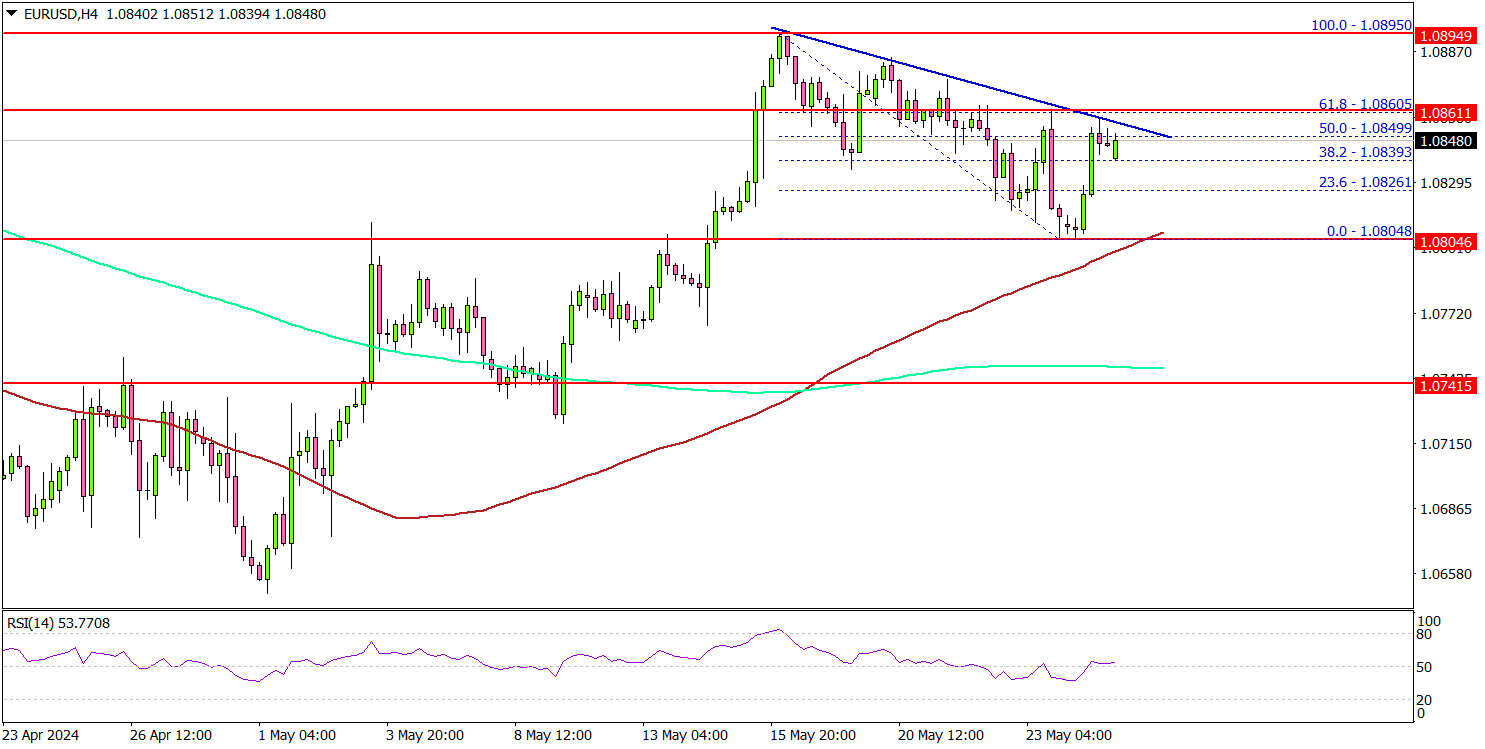

EUR/USD Targets Further Upside: Bullish Momentum Builds

Key Highlights

- EUR/USD is showing positive signs above the 1.0800 support.

- It is eyeing an upside break above the 1.0880 resistance on the 4-hour chart.

- Gold price took a hit and declined below $2,350.

- GBP/USD could gain bullish momentum if it clears the 1.2750 resistance.

EUR/USD Technical Analysis

The Euro remained well-bid above the 1.0800 level against the US Dollar. EUR/USD formed a base and started a fresh increase above the 1.0825 resistance.

Looking at the 4-hour chart, the pair even settled above the 200 simple moving average (green, 4-hour) and the 100 simple moving average (red, 4-hour). The pair spiked above the 50% Fib retracement level of the downside correction from the 1.0895 swing high to the 1.0804 low.

The pair is now attempting an upside break above a connecting bearish trend line with resistance at 1.0860. It is near the 61.8% Fib retracement level of the downside correction from the 1.0895 swing high to the 1.0804 low.

A clear move above the 1.0860 resistance might send it toward the 1.0900 level. Any more gains might call for a move toward the 1.0950 level in the near term.

If there is no move above the 1.0860 resistance, the pair might correct gains. Immediate support is near the 1.0820 level. The next major support is at 1.0800 and the 100 simple moving average (red, 4-hour).

If there is a downside break below the 1.0800 support, the pair might test the 200 simple moving average (green, 4-hour) at 1.0750. Any more losses might send the pair toward the 1.0720 level.

Looking at Gold, the bears pushed the price further lower and there was a move below the $2,350 support zone.

Economic Releases

- German IFO Business Climate Index for May 2024 – Forecast 90.3, versus 89.4 previous.

- German IFO Current Assessment Index for May 2024 - Forecast 89.9, versus 88.9 previous.

- German IFO Expectations Index for May 2024 – Forecast 90.5, versus 89.9 previous.

Brent Crude oil Wave Analysis

- Brent Crude oil reversed from strong support level 81.00

- Likely to rise to resistance level 84.3

Brent Crude oil recently reversed up from the support area located between the strong support level 81.00, which has been reversing the price from February, and the lower daily Bollinger Band.

The support level 81.00 was strengthened by the nearby lower daily Bollinger Band and by the 61.8% Fibonacci correction of the upward impulse 1 from December.

Given the bullish divergence on the daily Stochastic, Brent Crude oil can be expected to rise further to the next resistance level 84.30.

Forex and Cryptocurrency Forecast

EUR/USD: The Battle of Europe and US PMIs

Overall, the past week favoured the dollar, but the advantage over the European currency was minimal. If you look at where the EUR/USD pair was on 15 May, it returned to this zone on 24 May, regaining the losses of recent days. Recall that the report from the US Bureau of Labor Statistics (BLS) released on 15 May showed that the Consumer Price Index (CPI) decreased from 0.4% to 0.3% month-on-month (m/m), against a forecast of 0.4%. On an annual basis, inflation also fell from 3.5% to 3.4%. Retail sales volume demonstrated an even more significant decline, from 0.6% to 0.0% month-on-month (forecast 0.4%). These data indicated that inflation in the country, though resistant in certain areas, is still on the decline. At that moment, there were renewed discussions in the market about a possible rate cut by the Fed as early as this autumn. As a result, the Dollar Index (DXY) went down, and EUR/USD went up. Stock indices S&P 500 and Nasdaq reached record highs.

The most volatile day of the past week was Thursday, 23 May. Preliminary business activity data in the Eurozone exceeded expectations, strengthening the euro and lifting the pair to 1.0860. In Germany, the main locomotive of the European economy, the Manufacturing PMI rose from 42.5 to 45.4 points (forecast 43.2). This is still below the 50.0-point threshold separating decline from growth, but the trend is clearly positive. The Services PMI reached its highest level since June last year, hitting 53.9 against a forecast of 53.5 and a previous value of 53.2.

Germany's Composite PMI increased from 50.6 to 52.2 (market expectations were 51.0). Overall, business activity statistics in the Eurozone were also positive. The Composite PMI updated multi-month highs and, with a forecast of 52.0, actually reached 52.3 points (previous value 51.7).

However, the euro bulls' joy was short-lived. Later on Thursday, similar preliminary data on the US economy were released. They showed that business activity in the country's private sector grew at the highest rate in the past two years. The Manufacturing PMI rose from 50.0 to 50.9 points, and the Composite PMI jumped from 51.3 to 54.8 in a month. Market expectations were much lower, at the previous level of 51.3, so such a sharp rise signalled a surge in the DXY to 105.05 and a fall in the EUR/USD pair to 1.0804, as the likelihood of a rate cut in September decreased.

But the bears' joy was also short-lived. The GDP data released on Friday, 24 May, for Q1 2024 in Germany showed that the country's economy is saying goodbye to recession and moving into the growth zone. After a decline of -0.3%, GDP increased by 0.5%, resulting in a net growth of +0.2%.

In the end, after all these fluctuations, EUR/USD returned to the Pivot Point of the past one and a half weeks, closing at 1.0845. As for analysts' forecasts for the near future, as of the evening of 24 May, most (65%) expect the dollar to strengthen, 20% expect it to weaken, and the remaining 15% are neutral. All trend indicators on D1 are green, while 60% of oscillators are also green. Another 15% are red, and 25% are neutral grey. The nearest support for the pair is in the zones of 1.0830-1.0840, 1.0800-1.0810, then 1.0765, 1.0710-1.0725, 1.0665-1.0680, and 1.0600-1.0620. Resistance zones are located at 1.0880-1.0895, 1.0925-1.0940, 1.0980-1.1010, 1.1050, and 1.1100-1.1140.

The following week's calendar highlights Tuesday, 28 May, when the US Consumer Confidence Index will be announced. On the next day, 29 May, data on consumer inflation (CPI) in Germany will be released. On Thursday, 30 May, preliminary US GDP data for Q1 2024 will be published. The last working day of the week and the month might be quite eventful. On Friday, 31 May, Germany's retail sales volumes, preliminary inflation indicators (CPI) in the Eurozone, and the US Core Personal Consumption Expenditure Price Index will be announced. Traders should also note that Monday, 27 May, is a public holiday in the US, as the country observes Memorial Day.

GBP/USD: Uncertain Times for the Pound

The prospects for the British currency, as well as the national economy as a whole, are ambiguous. Additional uncertainty is brought by the fact that early parliamentary elections are scheduled for 4 July. As Prime Minister Rishi Sunak stated, "economic instability is just the beginning. [...] The time has come for Britain to make a choice. [...] Uncertain times require a clear plan and bold actions." However, what these "bold actions" will be remains unknown.

The macro statistics released last week did not add clarity. The preliminary Services PMI in the UK decreased from 55.0 to 52.9 points in May, against expectations of 54.7. And although in the manufacturing sector, this figure increased from 49.1 to 51.3, the Composite PMI stood at 52.8, below both the previous value of 54.1 and market expectations of 54.0.

As the latest data from the Office for National Statistics (ONS) showed, published on Friday, 24 May, retail sales in the country fell by -2.3% (m/m) in April, against a forecast of -0.4% and a result of -0.2% in March. The annual retail sales volume decreased by -2.7% compared to the previous result of -0.4%, and core retail sales fell by -3.0% (y/y) against 0% a month earlier, with all figures significantly below forecasts.

In such a situation, experts' opinions regarding the timing of the Bank of England's (BoE) rate cut also do not provide clear guidance. Analysts at JP Morgan (JPM) stick to their previous forecast of a rate cut in August but are cautious, citing still high consumer price inflation (CPI). "We adhere to our forecast [...] but believe that the risks have clearly shifted towards a later cut. Now it is a question of whether the Bank of England will be able to ease its policy at all this year." Strategists at Goldman Sachs, Deutsche Bank, and HSBC have also shifted their rate cut forecasts, moving the date from June to August for now. But this is only "for now"...

The maximum of the past week for GBP/USD was recorded at 1.2760. According to economists from Singapore's United Overseas Bank (UOB), the pair's upward momentum has slowed, and the likelihood of the pound rising to 1.2800 is decreasing. UOB believes that in the next 1-3 weeks, the British currency will trade in the range of 1.2685 to 1.2755.

The week ended at 1.2737. The median forecast of analysts for the near future is as follows: 60% voted for the pair's movement to the south, 20% for the northern direction, and 20% preferred neutrality. As for technical analysis, all trend indicators and oscillators on D1 point north, but a third of the latter signal overbought conditions. In case of further decline, the pair will encounter support levels and zones at 1.2695, 1.2635, 1.2575-1.2600, 1.2540, 1.2445-1.2465, 1.2405, 1.2300-1.2330. In case of growth, the pair will meet resistance at levels 1.2760, 1.2800-1.2820, 1.2885-1.2900.

No significant economic data releases for the United Kingdom are scheduled for the coming week. However, it should be noted that Monday, 27 May, is a bank holiday in the UK.

USD/JPY: Calmness, Ladies and Gentlemen, Just Calmness!

For such a super-volatile pair as USD/JPY, the past week was surprisingly calm. There were no currency interventions, and verbal interventions were as usual – lots of words, little action. Thus, Japan's Finance Minister Shunichi Suzuki once again expressed concern about rising prices caused by the weak national currency. According to Suzuki, one of the main goals of monetary authorities is to achieve wage growth exceeding inflation. "On the other hand," the minister added, "if prices remain high, achieving this goal will be difficult." In general, as usual, the government is closely monitoring the situation, understanding that everything is complicated, and therefore ... will continue to monitor.

Based on this contemplative policy, despite the GDP decline in Q1, on Thursday, 23 May, the Bank of Japan (BoJ) announced that it left the issuance volumes of Japanese government bonds (JGB) at the previous level. According to BoJ Governor Kazuo Ueda, "the economic outlook has not changed." The BoJ's view of the global economy has also not changed significantly. In general, calmness, ladies and gentlemen, just calmness!

Against this positive background, USD/JPY pair reacted only to the yield of US Treasury bonds and the dynamics of the Dollar Index (DXY). As a result, starting the five-day period around 155.70, it gradually moved up and ended it at 156.96. Analysts at United Overseas Bank (UOB) believe that given the weak upward pressure, the pair's growth in the next 1-3 weeks will be slow, and the barrier at 157.50 may prove to be a tough nut to crack. In their opinion, a price breakthrough above 157.00 is possible, but the pair is unlikely to consolidate above this level. The next resistance at 157.50 is unlikely to be threatened. UOB estimates that support is at 156.40, followed by 156.10. If USD/JPY falls below 155.60, it will indicate that the slight upward pressure has weakened, write the bank's economists.

Speaking of the average forecast, only 20% of analysts point south, 40% north, and another 40% east. Technical analysis tools are clearly devoid of such disagreements. Therefore, all 100% of trend indicators and oscillators on D1 point north, with 20% of the latter already in the overbought zone. It should be noted that while the green/north color of indicators regarding the British pound indicates its strengthening, in relation to the yen, it signals its weakening. Therefore, we advise paying attention to the GBP/JPY pair, whose dynamics have been very impressive lately.

The nearest support level is around 156.25, followed by zones and levels of 155.25-155.45, 154.60, 153.60-153.90, 153.00-153.15, 151.85-152.35, 150.80-151.00, 149.70-150.00, 148.40, 147.30-147.60, and 146.50. The nearest resistance is in the zone of 157.20, followed by 157.80-158.00, 158.45, 159.40, and 160.20-160.30.

From the events of the upcoming week, we recommend noting the speech of the Bank of Japan Governor Kazuo Ueda on Monday, 27 May, as well as the publication of consumer inflation (CPI) data in the Tokyo region on Friday, 31 May.

CRYPTOCURRENCIES: A Week Under the Ethereum Flag

In 2024, the crypto community began gradually forgetting the term "crypto winter." However, there was no talk of a "crypto spring" either. After the halving on 12 April, in the absence of a bull rally, small traders and speculators began selling off their coin reserves. According to The Block Research, the rate of opening new BTC wallets fell to a six-year low. However, the whales buying digital gold for the future prevented a complete collapse in prices.

And finally, at the end of the calendar spring, it seems spring has come to the crypto market. And it was awakened by the Federal Reserve System (Fed) of the USA with its monetary policy. According to analysts, the surge in investments in digital assets was a response to the May consumer inflation (CPI) report in the US, which positively impacted the risk appetites of institutional investors.

According to CoinShares, investments in crypto funds increased by $932 million from 13 to 17 May, after an inflow of $130 million the previous week. For the first time, there was an inflow of $18 million into Grayscale's ETF. This sharp increase in BTC-ETF investments, the highest in the last nine weeks, triggered a sharp rise in bitcoin on 20-21 May, approaching $72,000 for the first time since 09 April.

After bitcoin rose above $71,000, its price updated historical highs in the local currencies of several Asian and South American countries. According to CoinMarketCap, in Japan, BTC reached a record level of 11.2 million yen at the start of trading on 21 May. This is the first case where the flagship asset's price exceeded 11 million yen. Digital gold prices also peaked in Argentina, where the leading cryptocurrency reached 63.8 million Argentine pesos, slightly above the maximum on 14 March.

In the Philippines, one bitcoin briefly rose to 4.18 million pesos, the highest since mid-March 2024. In several other countries, BTC prices also equalled or were very close to mid-March's maximum prices: in the UK, Australia, Canada, Chile, Colombia, Egypt, Israel, Norway, India, South Korea, Taiwan, and Turkey.

However, the Fed and American macro statistics, having awakened the markets, also calmed them. After strong business activity data in the US, BTC/USD returned to the support zone of $67,000. Another (and probably the main) reason why bitcoin could not update its historical high was its main competitor, ethereum, which drew investors' attention. (More on this below).

QCP Capital expects bitcoin to reach $74,000 and update its ATH (All-Time High) in the coming months. According to the company's economists, institutional acceptance of cryptocurrency is accelerating, and improving conditions in the global economy create conditions for capital inflows into risky assets. The US presidential election, scheduled for 5 November 2024, is also starting to have a strong positive impact on the cryptocurrency market.

Cryptocurrency themes continue to strengthen in the pre-election rhetoric of candidates seeking to gain the votes of the crypto community, which, according to NYDIG, numbers more than 46 million citizens in the US, or 22% of the adult population. Haseeb Qureshi, Managing Partner of Dragonfly Capital, believes that in such a situation, the administration of President Joseph Biden will soon be forced to ease its policy regarding the digital asset industry. A complete turnaround is not to be expected, but a softening of the position will still occur, Qureshi said.

CNN has recently reported on upcoming debates between Biden and his competitor, Donald Trump. The incumbent president will have to answer a number of uncomfortable questions about the harsh policy towards the crypto industry, which led to the outflow of cryptocurrency capital, the closure of large companies, and high-profile lawsuits. From Donald Trump, who turned the topic of cryptocurrency into a weapon against his opponent, in addition to attacks for the current state of affairs, loud pre-election promises can be expected, which could lead to significant volatility in the crypto market. Possible participation of Elon Musk, who expressed willingness to become a moderator, and independent candidate Robert Kennedy Jr., should enliven the debates, the first round of which is scheduled for 27 June, and the second for 10 September.

The main beneficiary of the past week was not bitcoin but ethereum. On Monday, 20 May, news reached the media that the US Securities and Exchange Commission (SEC) asked companies to update Form 19b-4 in applications for launching spot Ethereum ETFs in an accelerated manner. After these news, the financial agency Bloomberg immediately raised the chances of such funds being approved from 25% to 75%. Against this background, the leading altcoin quickly outpaced the flagship cryptocurrency in terms of growth rates.

The deadline for the first two applications from VanEck and Grayscale was Thursday, 23 May. Shortly before the X hour, ETH/USD reached $3,947, showing a growth of almost 30% in three days. According to Coinglass, the amount of liquidations and forced closures of short positions on crypto exchanges amounted to $340 million. A total of 78.8 thousand positions were liquidated, and the largest individual liquidation occurred on the HTX exchange for the ETH/USDT pair for $3.1 million.

The SEC did not disappoint expectations and on 23 May approved not two but a total of eight applications for the issuance of spot ETFs based on Ethereum and gave the go-ahead for trading and listing these funds on exchanges. According to Variant Investments Chief Legal Officer Jake Chervinsky, this step signals a "significant shift in US crypto policy, possibly more important than the ETFs themselves." This may also mean that recognizing ethereum as a commodity, the regulator will not categorize many other altcoins as securities. According to Rekt Capital, the market is already on the verge of an altcoin rally, the peak of which is expected in July.

Experts expect significant capital inflows after the listing of ETH-ETFs and believe that billions of dollars will be invested in derivatives in the first week after trading starts. Analysts from QCP Capital believe that the altcoin rate in the short term can rise to $4,000 and exceed $5,000 by the end of the year.

An even bolder forecast is given by Standard Chartered Bank economists. They expect capital inflows into such funds in the first year to range from $15 to $45 billion (2-9 million ETH). In this case, the fund's demand will lead to the asset's rate rising to $8,000 at a bitcoin rate of $150,000. Moreover, if market dynamics are positive, by 2025, the price of Ethereum will reach $14,000, and bitcoin's rate will increase to $200,000.

As of the evening of Friday, 24 May, BTC/USD is trading at $69,900, and ETH/USD at $3,735. The absence of an immediate pump and some drawdown of this pair on 23-24 May can be explained by the fact that everyone who wanted to has already managed to buy ethereums ahead of the SEC's historic decision. The total cryptocurrency market capitalization is $2.55 trillion ($2.42 trillion a week ago). The Bitcoin Fear & Greed Index (Crypto Fear & Greed Index) has not changed and remains in the Greed zone at 74 points.

And in conclusion of the review, forecasts from Artificial Intelligence. The latest version of GPT-4o from OpenAI believes that the price of bitcoin on 1 August 2024 will be in the range of $76,348 to $89,108 "considering current market factors and historical trends." GPT-4o's competitor, the anthropic AI model Claude 3 Opus, has formed an even more optimistic vision, designating the range between $105,072 and $167,808 by the indicated date.