Sample Category Title

Week Ahead – Hawkish Risk as Fed and NFP on Tap, Eurozone Data Eyed Too

- Fed meets on Wednesday as US inflation stays elevated

- Will Friday’s jobs report bring relief or more angst for the markets?

- Eurozone flash GDP and CPI numbers in focus for the euro

- Chinese PMIs and New Zealand employment to be watched too

Will the Fed put rate cut hopes in more peril?

The upcoming week looks sure to be an action-packed one for the US dollar, as besides an FOMC meeting and the April jobs report, there’s a flurry of other data on the US agenda that will give traders little time to rest.

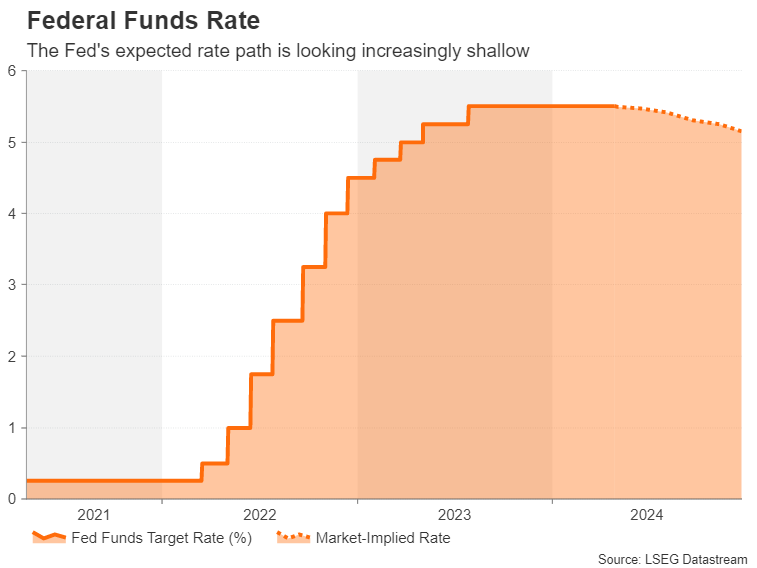

The main focal point during the first half of the week will be the Federal Reserve’s policy decision on Wednesday. It wasn’t that long ago that the May meeting was seen as the one where policymakers would set in stone the path to a June rate cut. However, following the string of hotter-than-expected inflation and employment data, the timing has moved further out into the future, with a cut seen unlikely before September.

With no updated FOMC projections to accompany the May decision, investors will be hanging on every word to come out of Chair Powell in his press briefing for any clues as to how soon the Fed will begin easing policy. Those clinging on to hopes that a summer rate cut is still possible will probably be disappointed.

The most recent commentary from Fed officials suggests committee members are more than comfortable staying on pause for a while longer, although the majority continue to foresee some amount of easing later in the year. Powell will likely reiterate the need for patience but still hint that rate cuts remain on the cards.

What investors will be trying to gauge, however, is how confident Powell is on inflation coming down substantially over the coming months that would allow policymakers to loosen their restrictive stance. If Powell strikes a somewhat more hawkish tone than his usual more balanced approach, the US dollar could resume its uptrend.

A labour market that won’t cool

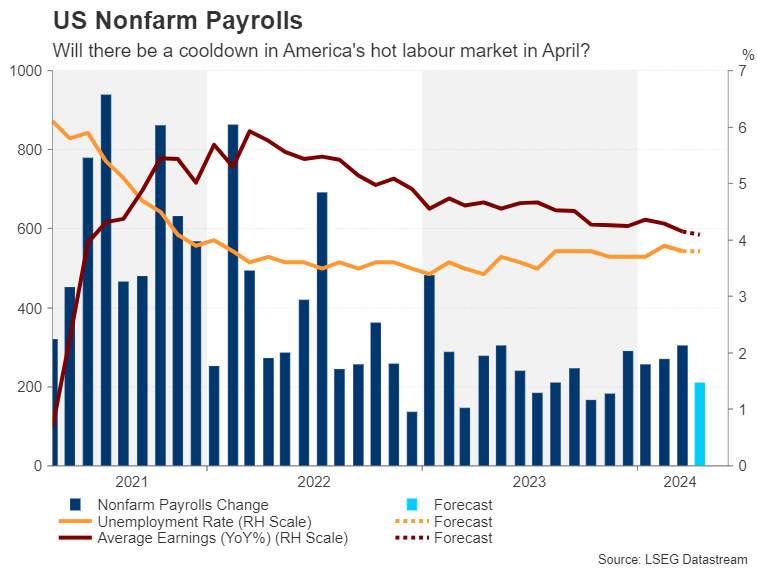

In the event there’s an absence of any fresh signals from the Fed, investors will turn their attention to Friday’s nonfarm payrolls report. Far from slowing, the US economy added an astonishing 303k jobs in March. Analysts expect a figure closer to 210k in April, while the jobless rate is forecast to have stayed at 3.8%.

The crucial factor here is whether wage increases will remain moderate and continue growing at slightly more than 4.0%. Any acceleration in average hourly earnings could spark a bigger panic about fading rate cut bets than an upside surprise in the headline payrolls print.

Also on investors’ radar next week are the ISM manufacturing and non-manufacturing PMIs for April, due on Wednesday and Friday, respectively. Following the softer-than-expected services PMI by S&P Global, a similarly weak ISM services PMI could offset the effects from potentially stronger jobs data and a hawkish tilt by the Fed.

In other releases, quarterly employment costs will be watched on Tuesday along with the Chicago PMI and the consumer confidence index. On Wednesday, there will be more labour market indicators consisting of the JOLTS job openings and ADP employment survey.

Euro sets sights on GDP and CPI update as June cut nears

Barring surprisingly strong wage figures awaited by the ECB at the end of May, a June rate cut seems to be a done deal. What is less certain is the rate path thereafter. Market pricing for the year end has fallen below 75 basis points (~3 rate cuts) in recent weeks and Germany’s influential Bundesbank head Joachim Nagel has warned that a June cut does not necessarily have to be followed by a series of further reductions.

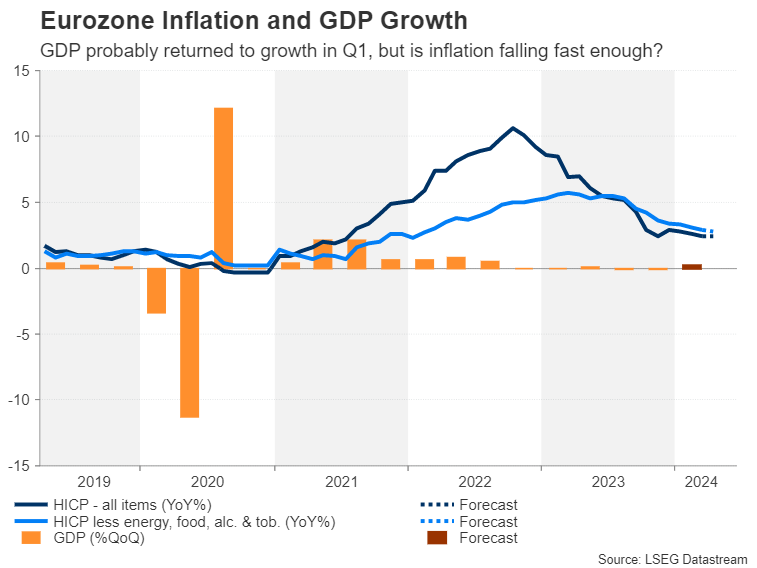

Preliminary readings on first quarter GDP and April CPI due on Tuesday will likely further shape expectations about the rest of 2024, though the probability for June is unlikely to budge much unless there’s a big deviation from the forecasts.

The euro area economy likely expanded by 0.2% quarter-on-quarter in the first three months of the year after flat growth in Q4. An improving economic outlook would lessen the urgency for the European Central Bank to cut rates aggressively so policymakers would have to see further declines in inflation to maintain a dovish stance. Headline inflation is projected to have stayed unchanged at 2.4% in March.

The euro is currently trying to establish a foothold above the $1.07 handle; whether it succeeds will depend on which way the incoming data turns.

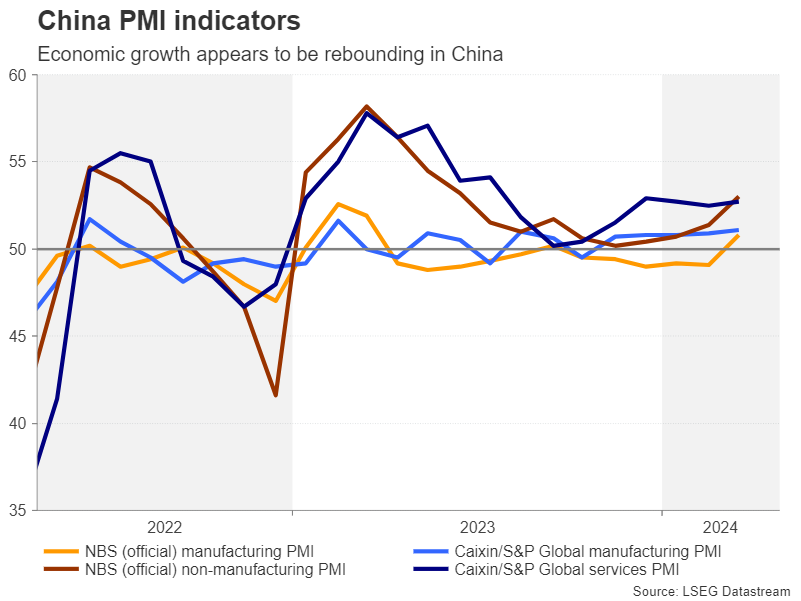

Chinese PMIs and New Zealand jobs on the way

Another region enjoying a bounce back in economic activity is China. The official composite PMI climbed to the highest since May 2023 in March, although much of it was driven by the services sector and the recovery in manufacturing remains tepid.

The latest PMI readings from both the government and Caixin/S&P Global are out on Tuesday.

If the economy gathers further momentum in April, that would bode well for risk-sensitive assets like stocks and oil, and commodity-linked currencies such as the Australian and New Zealand dollars.

In New Zealand, the local dollar will also be keeping an eye on domestic employment numbers scheduled for Wednesday. First quarter data on jobs growth, the unemployment rate and wages might offer clues as to how soon the RBNZ is likely to cut rates after the central bank recently gave its strongest indication yet that the next move will be down.

The kiwi could come under pressure if the labour market appears to be slowing.

Elsewhere, Canada publishes monthly GDP estimates on Tuesday and preliminary industrial production numbers for March are due out of Japan on the same day. Switzerland will release April CPI figures on Thursday and on Friday, Norway’s central bank announces its decision on interest rates.

Fed Preview – Cuts Still in the Horizon

- The Fed is widely expected to maintain the Fed Funds Rate unchanged next week by both markets and analyst consensus.

- The Fed could announce upcoming tapering of the QT pace already next week, but we would not expect it to have a significant impact on financial conditions.

- With no new projections, the market will have to rely on Powell for verbal guidance on rates outlook. We believe the Fed still sees cuts in the horizon in 2024, which could mean downside risks to yields and upside risks to EUR/USD.

The recent string of upside surprises in US inflation data has put rate cut speculation on the backfoot. We expect Powell to echo most of his colleagues in saying that some cuts are still expected for 2024, but that as long as the economy shows no significant signs of cooling, there is no sense of urgency for moving quickly.

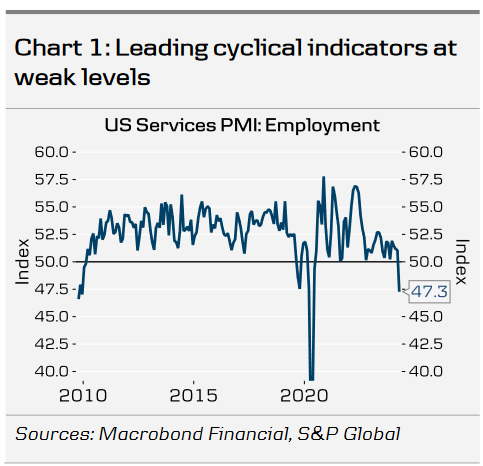

In our view, two factors suggest that the Fed is not yet ready to give up on signalling rate cuts for 2024. First, while rapid recovery in labour supply and improving productivity have given a sizable boost to the structural growth outlook, cyclical indicators still remain at subdued levels. April flash PMIs showed leading new orders components plunging across manufacturing and services. We have previously highlighted how fading support from inventory cycle is explaining the former and how early layoff indicators have flashed warning signals for the latter (see RtM USD, 16 April). Excluding the initial Covid-19 shock, services employment PMI fell to the lowest level since 2009 (Chart 1).

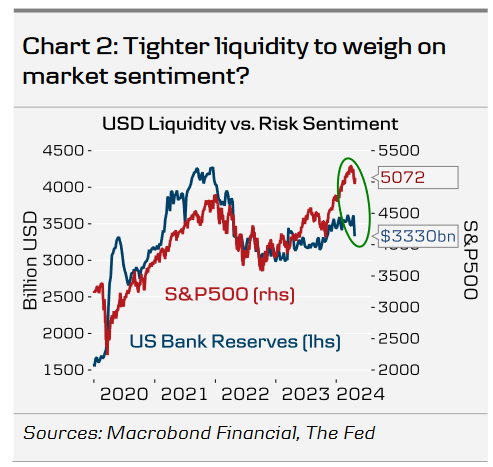

Second, after significant easing in late 2023, financial conditions have started to retighten. Bond yields have edged higher, broad USD has strengthened, commodity prices are rising and even equity markets gave up some of their gains in April. USD liquidity conditions are set to start tightening due to the Fed's QT in early summer as the liquidity boost from ON RRP has soon been depleted, which could signal further headwinds for the sentiment (Chart 2). Tighter financial conditions are a drag on the economy, and only around a year ago, the SVB's collapse illustrated how sudden the consequences can potentially be (markets were pricing in the Fed Funds Rate reaching as high as 5.7% just ahead of the crisis).

The Fed could also announce tapering the pace of QT already in this meeting. In our view, the Fed is not in a hurry to taper yet, but latest commentary has suggested that the participants prefer the 'slower but longer' approach to the QT's endgame to avoid 2019-esque sudden tightening in liquidity conditions. We discussed the implications for liquidity and the Fed's bond holdings in more detail in RtM USD, 23 April. In any case, the announcement should not have a significant impact on financial conditions.

All together, we see risks tilted towards slightly dovish market reaction, if the Powell maintains clear verbal guidance for rate cuts in 2024, even when emphasizing that there is no urgent need to act for the time being. Our call for rate cuts starting already in June is inarguably under pressure, but we still like our view for three cuts in total in 2024.

Weekly Focus – Rate Cut Expectations Pushed Back Further

It has been a volatile week for risk markets, once again mostly driven by expectations regarding the first rate cuts by the big central banks. Euro area PMIs came out much stronger than expected, and service sector output prices increased, raising a question of whether the ECB was too complacent when they basically pre-committed to a rate cut in June. US Q1 GDP missed expectations but mostly because of a decline in exports, while PCE inflation on a quarterly basis ticked up more than expected. As a result, markets have yet again pushed back rate cut expectations and the first Fed rate cut is currently not fully priced in until November.

The pricing of 'higher for longer' in the US together with elevated energy prices remain a drag for the Japanese yen which continued to weaken this week. On Friday, USD/JPY broke a new high above 156.50 level after a dovish hold by the Bank of Japan and April inflation data surprising to the downside. Soon after the meeting the pair suddenly corrected sharply lower. The short-lived move was likely an intervention by Japanese authorities, yet a futile one as JPY quickly reversed the gains. The weakness in JPY is a reason we expect Bank of Japan to hike rates once more this year, most likely in July.

Geopolitical risks remain on the agenda. While the situation in the Middle East seems to have calmed for now, Russia's war in Ukraine is gathering renewed attention. The US finally approved a new USD 61 billion support package for Ukraine, which should bring almost immediate relief for Ukraine on the frontline. We do not expect the dynamics to change drastically, though. The US support will enable Ukraine to keep on fighting, but significant advances seem to be challenging for both sides at the moment. Also this week, Belarusian President Lukashenka claimed to have prevented a drone attack from Lithuania, raising concerns of some kind of a false flag operation by the Kremlin-Minsk axis.

Next week, focus on the US rates market is likely to remain as both the Fed meeting and a plethora of interesting macro releases are due. In line with market consensus, we do not expect any changes on monetary policy. Hence, focus will be on Powell's verbal guidance as well as on any hints on the Fed's plans to taper the pace of QT. Just ahead of the rate decision, ISM Manufacturing index and ADP private sector employment report will be released for April alongside JOLTs labour turnover data for March. On Thursday, we will get the Q1 preliminary productivity data, and on Friday, the April jobs report rounds up an interesting week.

In the euro area, focus will be on April flash inflation data. German and Spanish inflation prints will set direction on Monday, while the euro area data will follow on Tuesday. Inflation has declined in recent months but the underlying momentum in service inflation has picked up. We expect inflation to remain unchanged at 2.4% y/y due to food inflation and rising energy inflation while core inflation should decline to 2.6% y/y. The key thing to look out for is service inflation which has gained momentum recently and remains sticky on the back of recent wage increases. Euro area Q1 GDP data is out on Tuesday. We expect that the economy grew 0.2% q/q driven by the service sector while the manufacturing sector declined slightly as indicated by industrial production data and PMIs.

Sunset Market Commentary

Markets

The yen showed some huge intraday swings today. USD/JPY rose beyond 156 and was moving quickly towards 157 next. A violent countermove then pushed it back to the 155 figure only to trade back at the highest level of the day (and 34 years) just south of 157. It’s the kind of move you would expect on news the BoJ is “asking for quotes” in the market, typically the first step of an actual FX intervention. But in absence of confirming headlines, we assume it’s general market nervousness, amplified by the fact that Japanese markets are closed on Monday. That risks triggering more hefty price moves in liquidity-thinned trading. JPY investors are on high alert after this morning’s BoJ meeting disappointed once again. Inflation forecasts were revised higher but the policy-relevant gauge was seen just short of 2% over the policy horizon. This suggests the central bank is not yet fully convinced of prices moving towards target over the medium term. Governor Ueda at the press conference indeed noted that the trend is still below 2%. Said otherwise: there won’t be a follow-up rate hike to the March one just yet. Neither did the BoJ deliver on expectations here and there that it would tweak its bond buying programme. This puts Japanese monetary policy in ever stark contrast with the US. Solid economic growth and rusty, above-target inflation in combination with the upcoming November elections is closing the Fed’s window of opportunity to cut rates in no time. Today’s March PCE deflators coming in to the upside of expectations (2.7% headline, 2.8% core, both on a robust 0.3% m/m pace) with another batch of strong (real) personal spending and income data was testament. US money markets have pushed forward the timing of a first, fully priced in rate cut to December if we take November 7 – just days after the elections – out of the equation. The dollar is better bid against most G10 peers except for the commodity-linked ones (AUD, NZD, CAD). Note that the likes of Brent oil are returning stealth mode to their recent 7-month highs just shy of $90/b. Copper pierced through to a new 22-month high. EUR/USD called off an early attempt to rise to trade slightly lower in the 1.072 region. Nice equity gains (1%+ in Europe and 0.2-1.4% in the US) provide a cushion for the euro.

Core bonds licked their wounds ahead of the weekend. US and German yields roughly ease between 3 and 7 bps with the front end of the curve underperforming. Investors to some extend swooped in on the battered bonds after the PCE release today but it’s not very convincing so far. Especially with a heavy eco calendar next week, the risk is for getting burned. Brace yourselves for US ISMs, JOLTS job openings, the April labour market report, Treasury’s quarterly refunding scheme and the FOMC meeting. Europe is headed towards an avalanche of Q1 GDP (marking the low-point or even recovery in the cycle?!) and inflation numbers.

News & Views

The ECB’s March consumer expectations survey showed that median consumer inflation perceptions over the previous 12 months (5% from 5.5%) and inflation expectations for the next 12 months decreased (3% from 3.1%, the lowest level since December 2021). Inflation expectations three years ahead remain unchanged at 2.5%. This adds to the 25 bps rate cut case in June. Expectations for nominal income growth and nominal spending growth over the next 12 months decreased slightly, respectively to 1.3% and to 3.6%. The perception on economic growth over the next year is unchanged (-1.1%) while consumers turned less pessimistic on the labour market (expected unemployment rate of 10.7% from 10.9%). Finally, consumers expected housing prices to increase by 2.4% on a 1-yr horizon with mortgage rates forecast to fall slightly over the same time period (5% from 5.1%).

German Der Spiegel magazine reports that the federal government will have more borrowing leeway next year and is set to use it. Net new debt will be about €24bn in 2025 instead of the earlier flagged €16bn as the debt brake mechanism includes clauses in times of economic weakness. The figure compares to €70bn in 2023 and €40bn this year. All ministries except for defense (NATO goals of at least 2% of GDP spending on armed forces over the long term) have to do with less cash after the constitutional court ruled last year derailed the government’s finance planning with a ruling against the use of off-balance sheet funding to circumvent the debt brake.

Graphs

USD/JPY: how much longer can Japanese officials stand by and do nothing?

Commodities inlcuding Brent going towards their recent highs stealth mode.

EUR/GBP: sterling on track to erase last Friday’s slip-up with a nice weekly gain.

EuroStoxx50’s attempt to escape from a sell-on-upticks pattern needs further confirmation.

U.S. Consumer Spending and Income Rise in March, Inflation Holds Steady

Personal income grew 0.5% month-on-month (m/m) in March, an increase relative to February's 0.3% gain and in line with market expectations.

Accounting for inflation and taxes, real personal disposable income rose 0.2% in March, a recovery from the -0.1% decline in February.

Personal consumption expenditures rose by 0.8% m/m for a second consecutive month, above market expectations (0.6%). Spending in real terms rose by a solid 0.5% m/m – the same as in February. The increase in real spending reflected growth in both goods (1.1%) and services (0.2%) outlays.

On inflation, the Fed's preferred inflation metric, the core PCE price deflator, remained steady on both a monthly and annual basis. The measure came in at 0.3% month-over-month and 2.8% annually – the same pace as in February. While the monthly change was in line with market expectations, the annual number was higher (markets expected 2.6% y/y).

The personal savings rate fell in March to 3.2% from February's 3.6% reading.

Key Implications

Today's report fills in some of the details of the headline numbers reported yesterday in the Q1 GDP advance release. Despite mounting challenges and dwindling savings, the U.S. consumer powered ahead, closing out the first quarter on solid footing. As such, real personal consumption expenditure growth was 2.5% annualized in 2024 Q1 (down from 3.3% in 2023 Q4). Most of the quarterly strength came from spending on services, despite a solid showing from goods spending in the final month of the quarter. Ultimately, with a decent handoff to Q2, consumer spending is set to remain resilience.

While both annual and core PCE inflation did not decelerate, holding steady was the next best alternative. The outturn suggests that much less of the recent hot CPI inflation readings has filtered through to the Fed's preferred metric. Not so great however was the fact that while the 6-month annualized change held steady at 3%, the 3-month annualized measure continued to trek up (from 3.7% to 4.4%) pointing to some near-term stickiness. Core services excluding housing, or supercore inflation, also suggest that near-term price pressures persists. Taken together, these developments point to the Fed continuing to exercise patience with respect to rate cuts, with markets currently betting on a first cut in the fall.

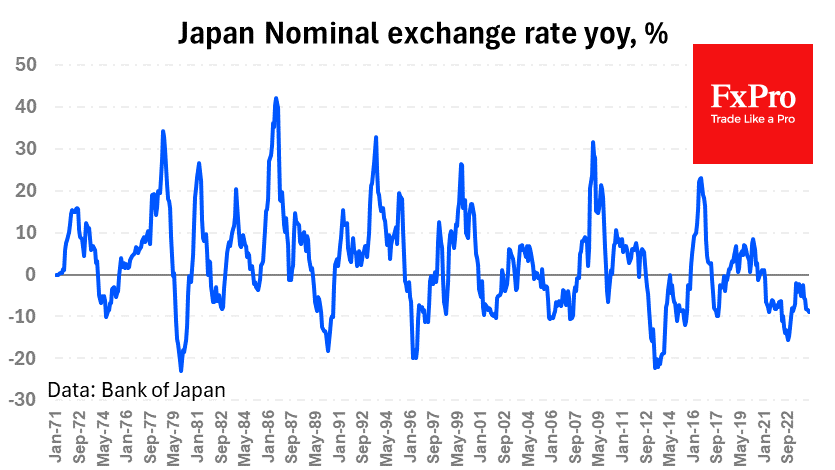

False Alert with Yen Interventions?

Even though the Bank of Japan left the key rate and parameters of the QE programme unchanged, the central bank’s inaction increased the pressure on the national currency. This resulted in USDJPY reaching 156.80 and EURJPY reaching 2007–2008 levels, which started a sharp decline due to the global financial crisis and related deleveraging.

USDJPY has already surpassed the levels where the October 2022 intervention took place and where the market reversal occurred about a year later. This begs the question of ‘when’, although the question of ‘will they’ is still relevant.

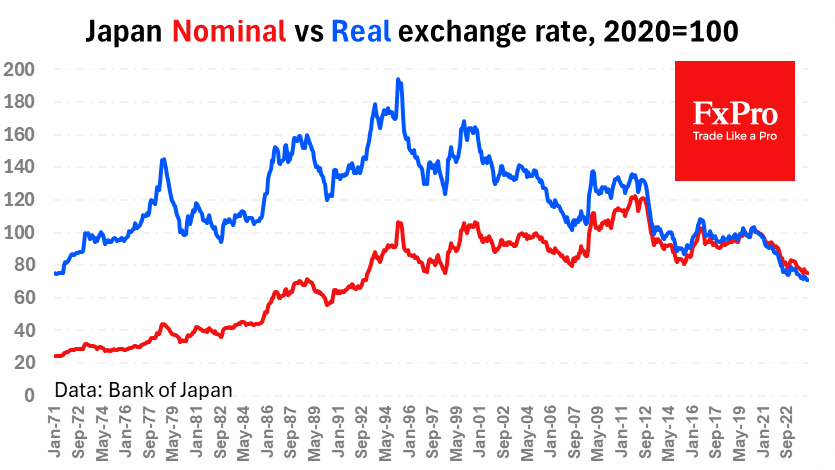

Central banks and governments do not focus on the nominal levels of individual currency pairs. They care about dynamics, as abrupt changes can cause inflation and economic shock. Therefore, it is more useful to look at the dynamics to a basket of currencies.

The nominal effective exchange rate of the yen has retreated to its lowest levels since the 1990s. The yen reversal to growth in 1997 on the back of crises in developing countries was at about the same level. The pressures of the global financial crisis in 2007 turned the yen up 5% higher. Thus, the current levels are not an anomaly, and the yen has fluctuated near these levels many times in the last 34 years.

A weakening yen potentially poses risks of inflating inflation. We have noticed that the government and CB intervene in the market when year-to-year changes approach 20%. USDJPY is adding 17% y/y, EURJPY is up 13% y/y. This is quite a lot but allows the authorities not to share the passions of the financial media and traders.

Yen weakening is measured by historical standards, not allowing to talk about a currency shock for the economy.

As the nearest turning points, we can consider the area of 160 on USDJPY – the point of market reversal in April 1990. EURJPY has a similar point near 170. At these levels, intervention cannot be certain. The chance of intervention in free forex pricing will clearly increase if the yen collapses rather than slowly creeping there.

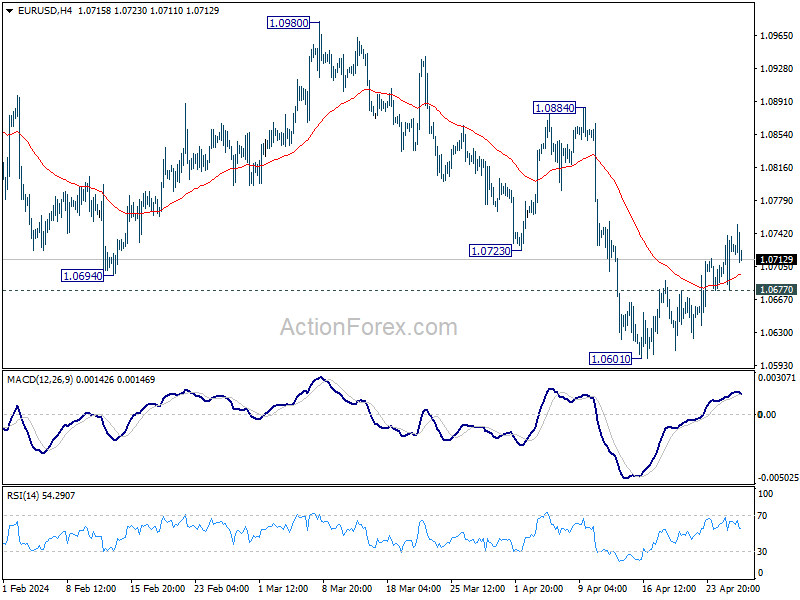

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0692; (P) 1.0716; (R1) 1.0754; More...

Intraday bias in EUR/USD remains mildly on the upside at this point. Rebound from 1.0601 could extend to 55 D EMA (now at 1.0784). On the downside, break of 1.0677 minor support will turn intraday bias to the downside for retesting 1.0601 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

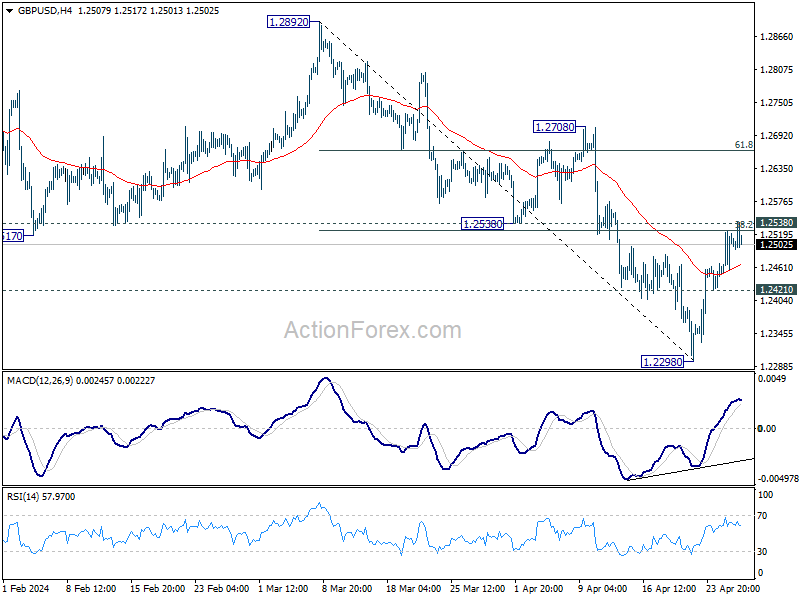

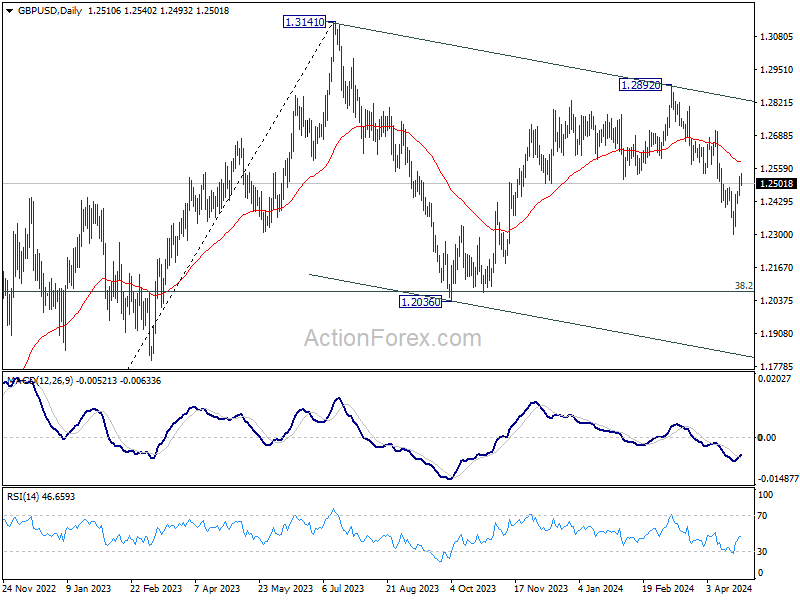

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2464; (P) 1.2495; (R1) 1.2543; More...

No change in GBP/USD's outlook and intraday bias stays neutral. Near term outlook stays bearish as long as 1.2538 support turned resistance holds. Break of 1.2421 minor support will argue that rebound from 1.2298 has completed and bring retest of this low. However, decisive break of 1.2538 will bring stronger rally to 55 D EMA (now at 1.2583) and above.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

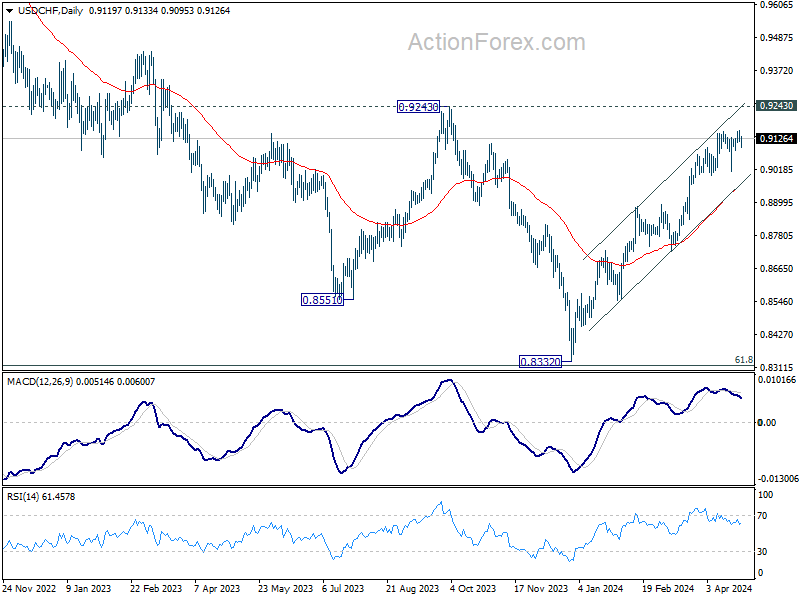

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9104; (P) 0.9137; (R1) 0.9155; More....

Intraday bias in USD/CHF remains neutral for the moment. On the upside, firm break of 0.9151 will resume the rally from 0.8332 and should target 0.9243 key resistance next. On the downside, break of 0.9085 will turn bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

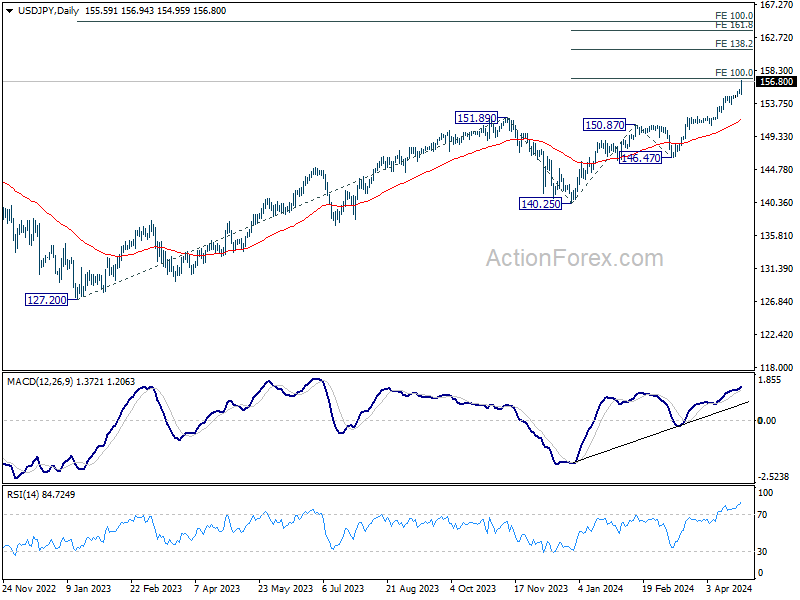

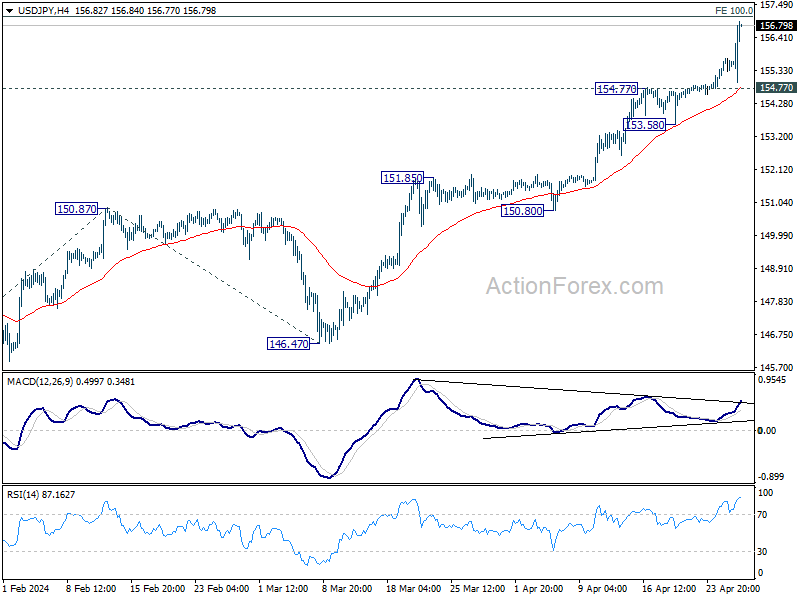

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.32; (P) 155.53; (R1) 155.87; More...

Intraday bias in USD/JPY remains on the upside for 100% projection of 140.25 to 150.87 from 146.47 at 157.09. Some resistance could be seen there to bring retreat. But further rally is expected as long as 154.77 resistance turned support holds. Sustained break of 157.09 will target 138.2% projection at 161.14 next.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.