Sample Category Title

SNB’s Schlegel: Interventions contributes to price stability

SNB Vice Chairman Martin Schlegel defended the central bank's use of foreign exchange interventions, highlighting their effectiveness in maintaining price stability within Switzerland.

"Have foreign exchange interventions contributed to achieving price stability? Yes, they have," he said at an event in Geneva overnight.

He further elaborated that without utilizing foreign currency sales, SNB would have faced the necessity to escalate the policy rate significantly higher.

Schlegel also noted a modest average of 0.3% over the last fifteen years. He argued that, in the absence of foreign exchange purchases, inflation rates would have dipped considerably lower, potentially entering deflationary territory.

"Estimates suggest that it would have been significantly below zero without the purchases; we would thus not have fulfilled our mandate," Schlegel pointed out.

Will Friday’s Data Add to Hopes of UK Exit from Recession?

- Dovish BoE encourages more rate cut bets

- UK GDP for February expected to reveal slowdown

- The data comes out on Friday at 06:00 GMT

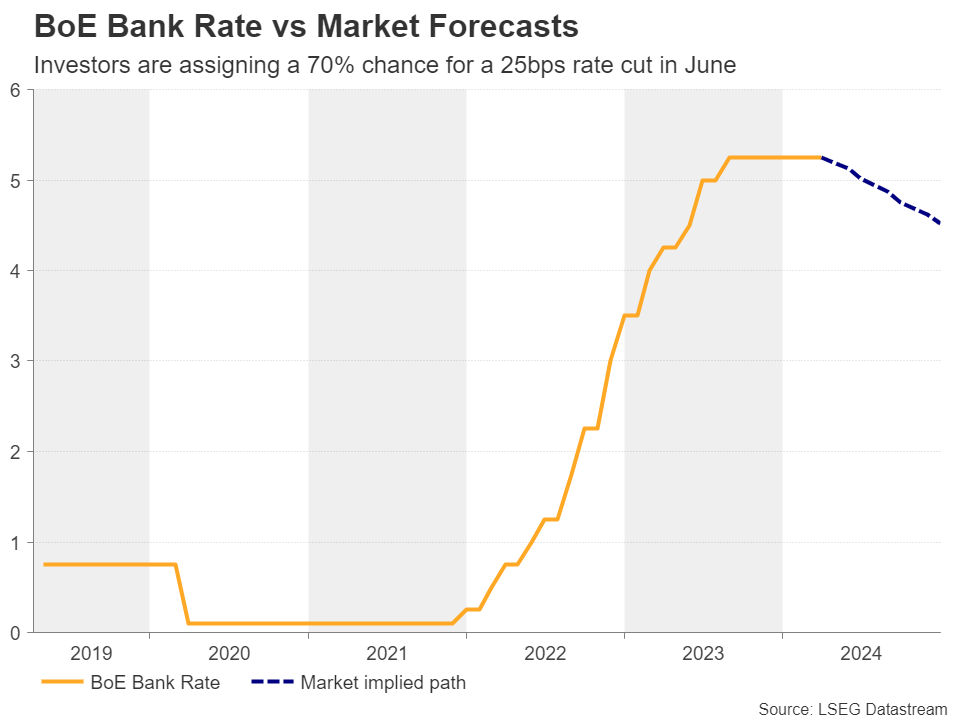

Investors add to June rate cut bets after BoE decision

With inflation in the UK coming down faster than previously expected, the Bank of England (BoE) appeared more dovish than expected at its latest gathering, on March 21. Once again, officials kept interest rates unchanged, but this time, there were no members voting for a hike. There was only one dissenting vote, and that was for a 25bps reduction.

On top of that, Governor Bailey reiterated that they are not yet at the point where they can cut interest rates, but he added that with inflation coming down, things are moving in the right direction.

This has led market participants to bring forward their BoE rate cut bets, with the overnight index swaps (OIS) market suggesting a 25% probability for a quarter point reduction at the Bank’s upcoming gathering in May, and chance for a cut in June rising to around 70%. The quick repricing has been weighing on the pound, with Cable tumbling from 1.2800 to near the 1.2600 area.

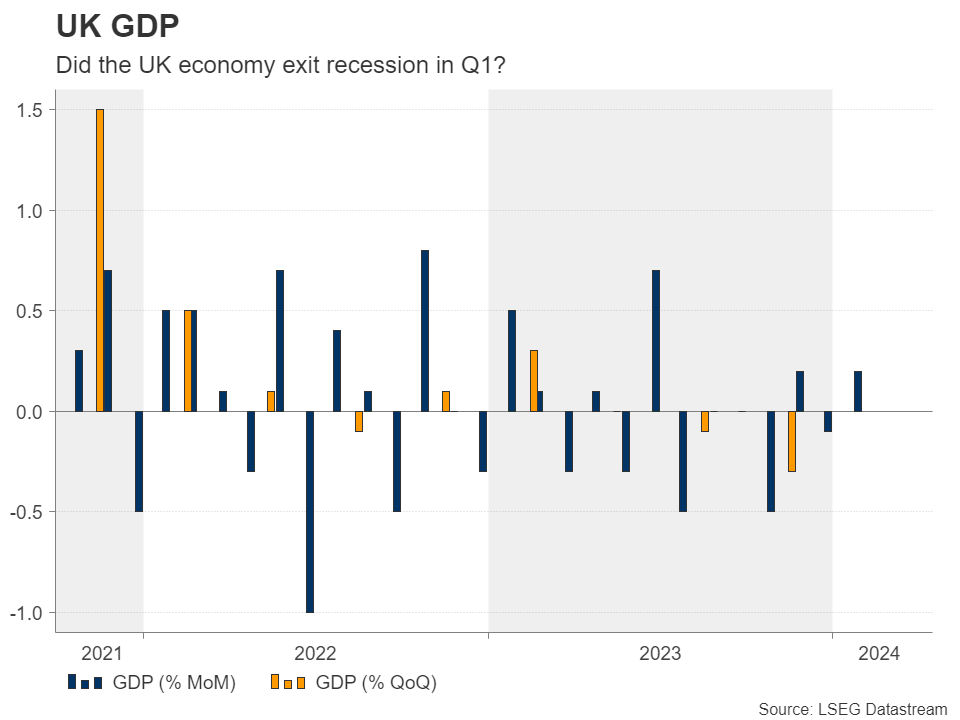

Did the UK economy exit recession in Q1?

For pound traders, this week may not be as busy as for dollar and euro traders, but they will still have the opportunity to reassess their view with regards to the BoE’s future course of action on Friday when the monthly GDP estimate for February is coming out, alongside the industrial and manufacturing production figures for the month.

Given that the UK economy slipped into recession in the second half of 2024, market participants may be eager to find out whether it entered growth mode again during the first quarter of the new year. The monthly GDP rate for January clocked in at 0.2% m/m, while the composite PMIs for both January and February pointed to improvement, although the March print pointed to a mild slowdown.

The aforementioned numbers suggest that the UK economy started the new year on a stronger footing, but that remains to be confirmed by Friday’s numbers. The forecast points to a slowdown to 0.1% m/m, which could revive some concerns regarding the performance of the UK economy, despite not entering contraction territory.

The NIESR GDP tracker points to a 0.3% q/q for the first quarter of 2024, but a soft monthly rate for February could bring that forecast into question, especially after the March PMIs pointed to a slowdown in business activity during the last month of the quarter.

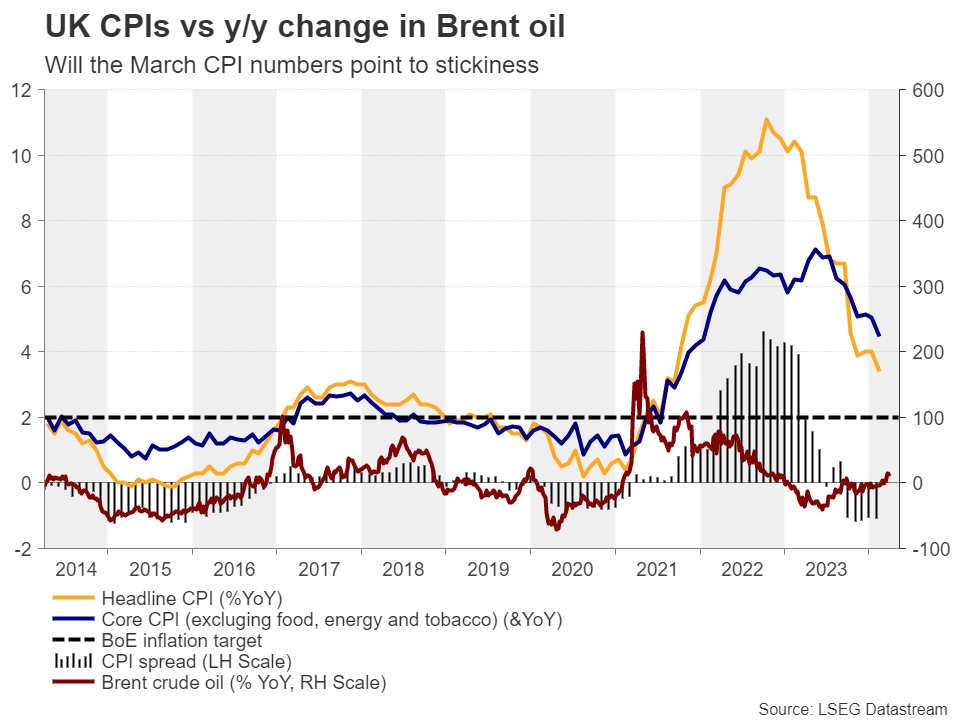

Too early for conclusions as CPI data loom next week

Therefore, investors may remain convinced that there is a strong chance for the BoE to begin cutting interest rates in June, which could weigh somewhat on the pound. However, calling for a bearish outlook may still be premature, especially ahead of next week’s CPI data for March.

Despite the slowdown, the March PMIs also revealed that output prices across the UK private sector rose at the fastest pace in eight months, which tilts the risks surrounding next week’s inflation data to the upside. Therefore, even if the pound slips somewhat this week, it could bounce back up next week.

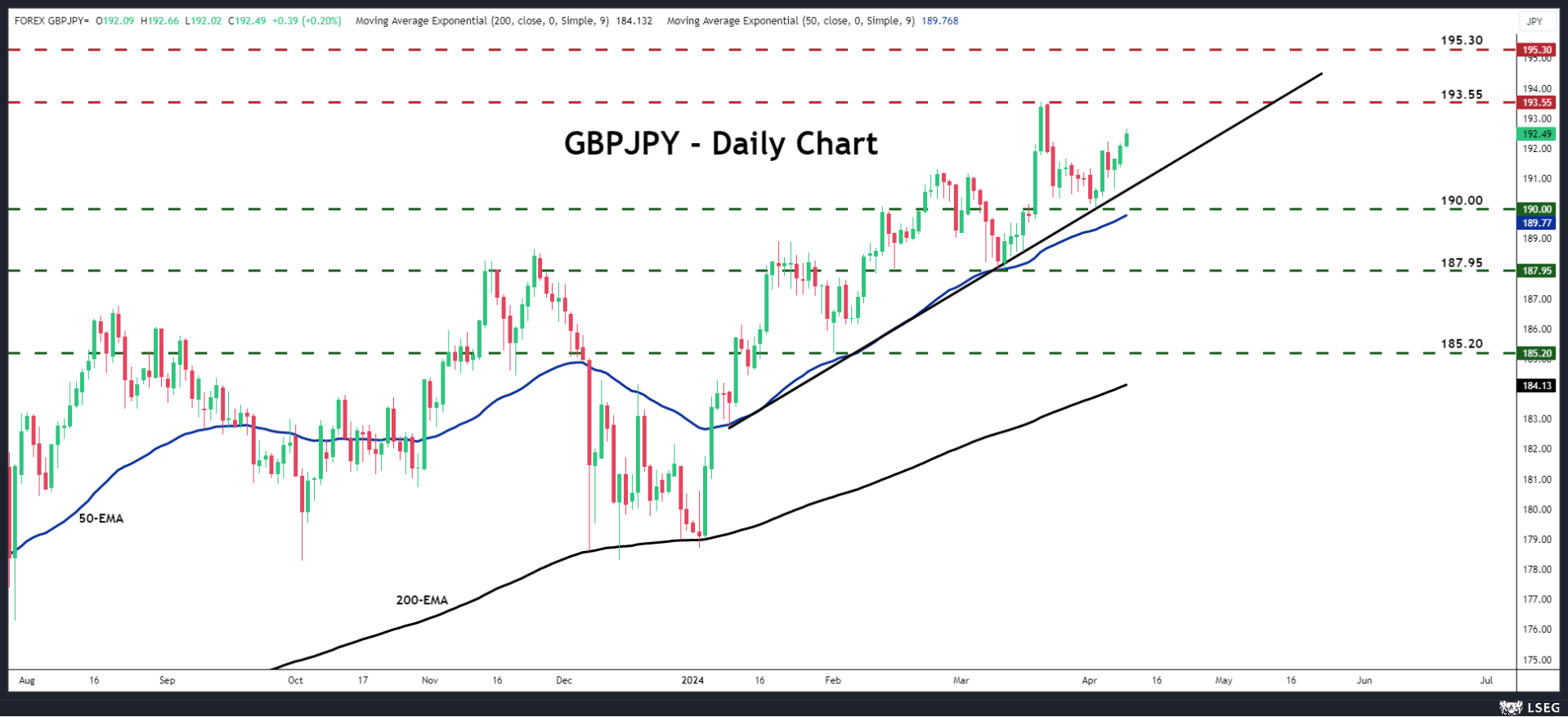

Pound/yen remains in uptrend mode

Pound/yen has been marching north since April 2, when it hit support at the crossroads of the 190.00 barrier and the short-term upward sloping support line drawn from the low of January 9. Even if the pair pulls back this week, as long as the retreat stays in check above 190.00, the bulls could remain willing to jump back into the action and aim for the high of March 20 at around 193.55.

On the downside, a slide below 190.00 could signal a larger bearish correction, but for a major trend reversal to start being examined, the pair may need to fall all the way below the 187.95 zone.

BoC to Put June Rate-Cut on the Map-Tentatively

- BoC monetary report due on Wednesday 13:45 GMT, press conference at 14:30 GMT

- Interest rates to remain steady this time, but policymakers might support a June rate cut

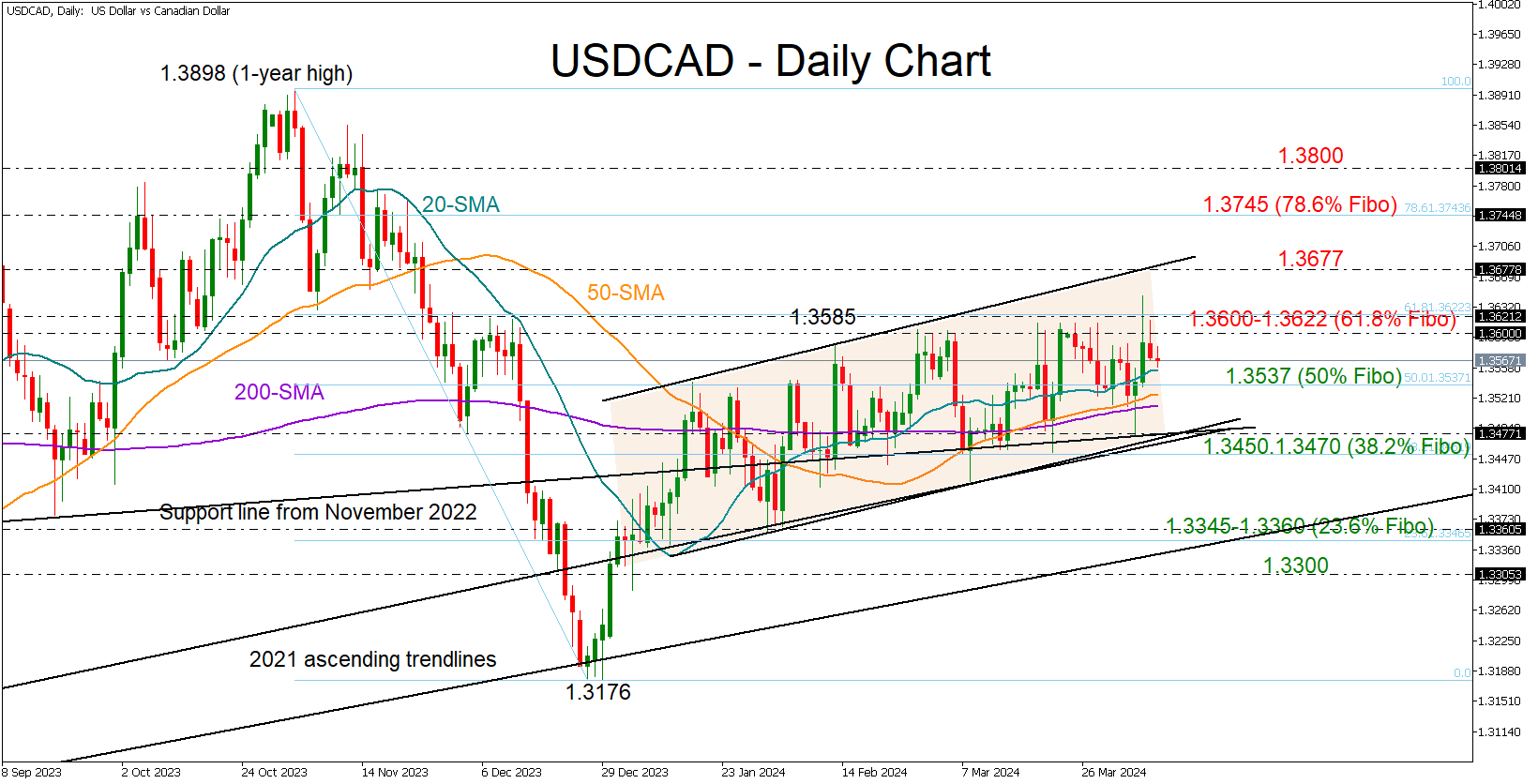

- USDCAD maintains soft uptrend, needs a clear close above 1.3600 to rally

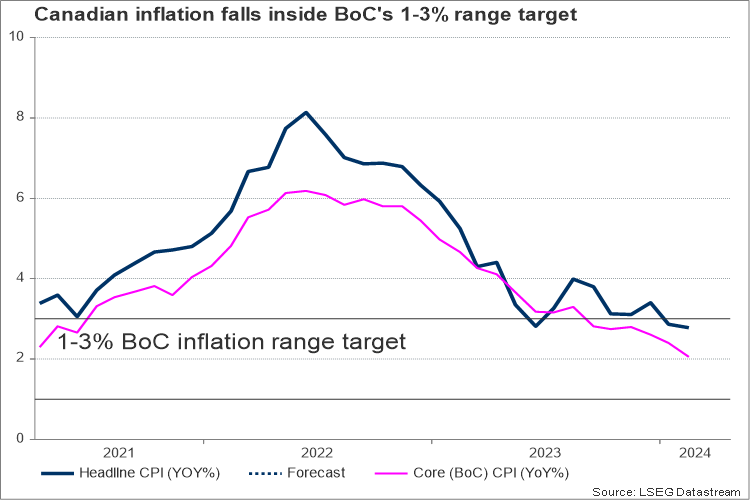

BoC closer to its inflation goal than its major peers

The Bank of Canada (BoC) will probably stick to the sidelines during its coming policy meeting on April 10, leaving interest rates unchanged at 5.0%. Like its peers, the central bank believes that it will be able to slash borrowing costs later this year, but policymakers still have different opinions on the timing. Nevertheless, the base scenario is for major central banks to start the easing cycle in June and there is reason to believe that the BoC is less likely to diverge from that path compared to its US counterpart.

First of all, inflation data has been more favorable since the March meeting. Headline inflation slowed down to a 2.8% year-on-year; faster than analysts expected, further easing within the BoC target zone of 1-3%. Remarkably, the core measure, which excludes volatile items like energy and food, declined to 2.1%, almost reaching the central bank’s 2.0% target, while the eurozone and US equivalents remain consistently higher. The monthly CPI readings have been subdued so far in 2024, reflecting weak price dynamics in the first quarter of the year too. Due to this, the monetary policy report released with the rate decision might contain lower inflation projections.

Labor market shows cracks, but real wages still high

As regards the labor market, conditions have returned to pre-pandemic levels. The economy lost 2.2k jobs in March, while on average, jobs growth was below 40k over the past year. What is more striking is that the unemployment rate continued to ascend in March, hitting a 26-month high of 6.1% from 5.8%. There are arguments that if the US methodology was applied to the Canadian labor data, the unemployment rate could still be elevated at 5.2%, reflecting the increased slack in the Canadian employment conditions.

Growth in population backed by rising migration has been the tailwind behind the rising jobless rate and the resilient wage growth. Canadian average hourly earnings are running hot and faster than the US ones at 5.0% despite changing trajectory to the downside in 2024. Policymakers argue that this level does not align with the central bank’s price stability objective, particularly when combined with low labor productivity, as is currently the case. In other words, if companies cannot increase the value of produced goods per worker, they will increase consumer prices to compensate for higher wages.

BoC might cut rates in June but under certain conditions

Consequently, even though a rate reduction could have positive effects on business motivations and alleviate growth restrictions, the central bank may need to take some time to ensure a sustainable return to its inflation target, considering the recent increase in oil prices and elevated real wage growth. Besides, cutting rates to see inflation turning up again in the coming months could harm its credibility.

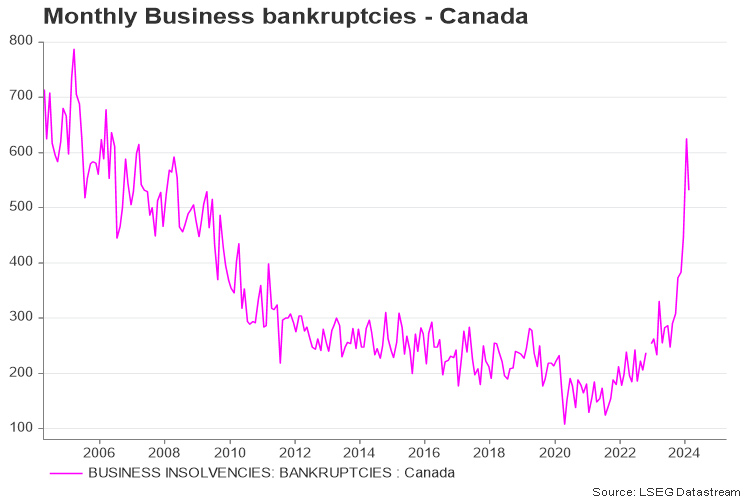

Moreover, while business bankruptcies have surged to the highest level since 2006, household debt relative to disposable income has gradually reverted to pre-pandemic levels, offering some relief for a potential delay. Hence, an immediate rate cut this week will be avoided, but clearer communication on the next policy steps is possible since there is no other meeting before June, although the BoC provides no guidance on its future policy decisions. Overall, policymakers could avoid any confusion by saying that a June rate cut could take place if the next inflation prints stay favorable.

How USDCAD might react?

According to futures markets, there is a 65% probability of a quarter percentage rate cut in June. If policymakers play down the odds, the loonie could gain fresh positive momentum, driving USDCAD down to the lower band of the two-month-old bullish channel at 1.3470-1.3450. A close lower would motivate a sharper decline to 1.3345-1.3360, unless the March low of 1.3418 adds a strong footing under the price.

Otherwise, if the central bank opens the door to a June rate cut, the pair could break the wall at 1.3600-1.3622 and climb to 1.3677. Above the latter, the recovery could continue towards the 1.3745-1.3800 region.

Sunset Market Commentary

Markets

Core bounds found some reprieve in this week’s second transitory trading session bridging Friday’s payrolls and tomorrow’s US CPI data. German Bunds outperforms US Treasuries after the ECB’s quarterly Bank and Lending Survey provided some more backing for the flagged June policy rate cut. Demand for loans from firms declined substantially, contrary to banks’ expectations of a recovery. A small net decline was reported for housing loans. Credit standards for loans to firms tightened slightly and that trend is set to continue in Q2. Standards eased moderately for housing loans with no profound changes expected in the next quarter. German yields currently cede 2.2 bps (2-yr) to 6.5 bps (30-yr). Changes on the US yield curve vary between -3 bps (30-yr) and -4.5 bps (7-yr). The dollar continues to struggle even as oil prices (Brent) steady above $90/b and risk sentiment is also clueless (Europe -0.5%; WS +0.5%). DXY moves back below 104 for the first time since the March FOMC meeting. EUR/USD similarly eyes 1.09 for the first time since then. Sterling is today’s (odd) outperformer with EUR/GBP a tad softer at 0.8565 and cable moving above 1.27.

The Japanese yen still hovers dangerously close to the USD/JPY 152 level considered line in the sand for officials. People familiar with the matter today suggested that the Bank of Japan will likely consider raising its inflation forecast later this month (Apr 26). The outcome of the annual Shunto wage negotiations (5.24% average; most in over 30 years) is the key driver. Rising energy prices and JPY weakness are other compelling factors. Compared with January, sources suggest that the current fiscal year’s 2.4% (CPI ex fresh food) might be upwardly revised with the first FY 2026 forecast to be around the 2% inflation target. Question remains whether such higher inflation prognosis will speed up the BoJ’s normalization plans after last month’s inaugural dovish rate hike. Markets rightly so didn’t interpret it as being the start of a genuine hiking cycle, putting JPY immediately with the back against the wall. Failure to give clear backing at the April policy meeting risks bringing the currency rapidly into tailspin with possible FX interventions in such scenario likely in vain.

News & Views

The Italian government expects the country to grow 1% this year. That would mark a slight acceleration from the 0.9% in 2023 but a slight downward revision from the 1.2% projected last year. PM Meloni’s cabinet pencilled in 1.2% for 2025. The budget deficit isn’t anticipated to drop below the 3% EU limit until 2026. Last year’s whopping 7.2% shortfall as a result of the so-called “superbonus” for home renovations has heavily impacted the budget update, a government official explained. Because of the large deficits in coming years, the debt-to-GDP ratio would now rise through 2026 and hit a peak at 139.8%. This marks a change in direction from the October projections, which forecasted a decline.

The Kingdom of Belgium successfully launched a €7bn 5y bond (OLO102, October 22, 2029), priced at MS-1 bp compared to initial guidance of MS+1 bp. Books totaled more than €46bn. Based on the 2024 budget plan this was the third and final syndicated sale of the year with the other two carrying a 10-year and 30-year tenor. Today’s syndication included, the Belgium Debt Agency completed just over 60% of its €41bn OLO funding need.

The European Round Table for Industry, a lobby group consisting of around 60 of Europe’s largest companies in the industrial and technology sector, in a new report said there’s a need for €800bn of investments in energy infrastructure alone to meet the 2030 climate targets. Looking further into time and considering Europe’s net zero ambitions by 2050, the price tag rises to a massive €2.5tn, to be channeled to the power grid, energy storage and carbon capture facilities. The Financial Times citing leading industry bodies reported that the private sector alone cannot carry such large investments alone. Government finances, however, are also under strain following the pandemic, energy crisis and a shift in spending priorities towards defense and other industries deemed too critical to be outsourced.

U.S. Small Business Optimism Index Edges Lower in March, Falling to the Lowest Level Since 2012

NFIB's Small Business Optimism Index fell 0.9 points to 88.5 in March, disappointing market expectations for a modest increase to 89.7. This marked the lowest level in the headline index since 2012.

Six of the ten subcomponents deteriorated on the month, two improved and two remained unchanged. Leading the decline was an 8-point drop in the share of firms expecting higher real sales to -18%. Expected credit conditions (-2 points to -8%), capital outlay plans (-1 point to 20%) and the belief that now is a good time to expand (-1 point to 4%) all edged lower, but earnings trends managed to tick higher (+2 points to -29%).

The net share of businesses planning to increase employment fell for the fourth month in a row, ticking down 1 point to 11% – almost half the level in the pre-pandemic period. The share of firms with unfilled job openings held steady at 37%, a level that's in line with the pre-pandemic average. Quality of labor concerns rose by 2 points to 18%, marking only a partial recovery after falling 5 points in the month prior. However, inflation was the top concern, with 25% of business owners identifying it as their top business problem.

The share of firms increasing compensation increased 3 points to 38%, while the share of firms planning to raise compensation over the next three months rose 2 points to 21%, recovering only a small portion of the 7-point drop in the month prior. The share of businesses 'raising' average selling prices rose 7 points to 28% in March, while the share of those 'planning’ to raise average selling prices rose 3 points to 33%.

Key Implications

Sales expectations deteriorated in March and small business confidence ended the first quarter on a sour note, with the index falling to 2012 lows. Looking underneath, while the U.S. labor market is showing continuous signs of resilience, today's survey results point to a cooling in conditions among smaller firms, with job openings and quality of labor concerns trending lower, and plans to increase employment falling to late-2016 levels.

Inflation remains a top concern for small business owners, a sentiment that was echoed in the pricing metrics. The sharp back-up in the share of firms raising average selling prices and a moderate increase in the share of those that plan raise prices in the next three months reinforce the notion that we're not out of the woods yet with respect to inflation. This latest data works in favor of a more patient Federal Reserve when it comes to lowering the policy rate.

NZ Dollar Climbs Ahead of RBNZ Rate Decision

The New Zealand dollar has posted considerable gains on Tuesday. In the North American session, NZD/USD is trading at 0.6065, up 0.54% and its highest level since March 21.

RBNZ widely expected to hold cash rate

The Reserve Bank of New Zealand meets early on Wednesday and it’s practically a given that it will hold the cash rate at 5.5%. This would mark the sixth straight time that the RBNZ maintains rates and prolongs its “higher for longer stance”.

Investors will be interested in whether the RBNZ pushes back against market expectations of rate cuts – investors have priced in two cuts with a 70% probability of a third this year. The decision will not include updated economic forecasts or a news conference with Governor Orr, which could limit New Zealand dollar volatility around the meeting.

The markets are being aggressive in their pricing of rate cuts, mainly due to a weak economy, as GDP has contracted in four of the past five quarters. However, high inflation is a key reason why the RBNZ is hesitant to signal rate cuts are coming. In the fourth quarter, the inflation rate was 4.7%, well above the upper limit of the 1-3% target band. New Zealand releases first-quarter CPI next week, and the release will be a key factor in the central bank’s rate policy.

The RBNZ would prefer to have the Federal Reserve cut rates first, as this would boost the New Zealand dollar and weigh on inflation. The Fed has signaled rate cuts are coming but stronger than expected data, such as last week’s nonfarm payrolls, may lead the Fed to delay lowering rates.

NZD/USD Technical

- NZD/USD is testing resistance at 0.6060. Above, there is resistance at 0.6107

- 0.6000 and 0.5953 are providing support

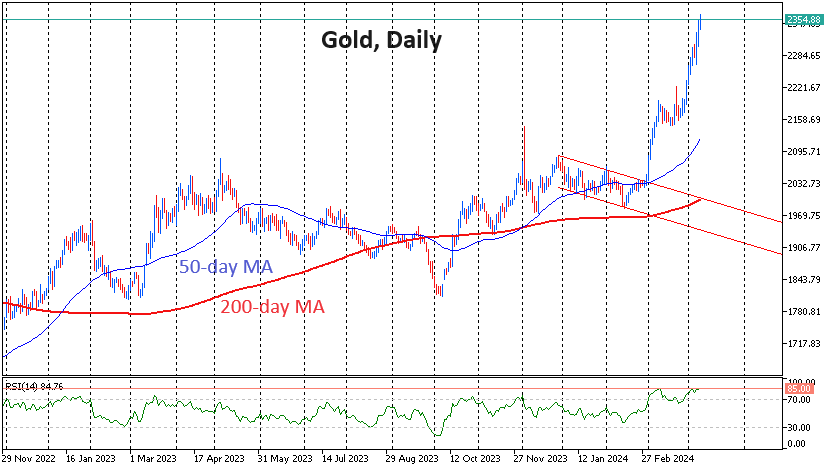

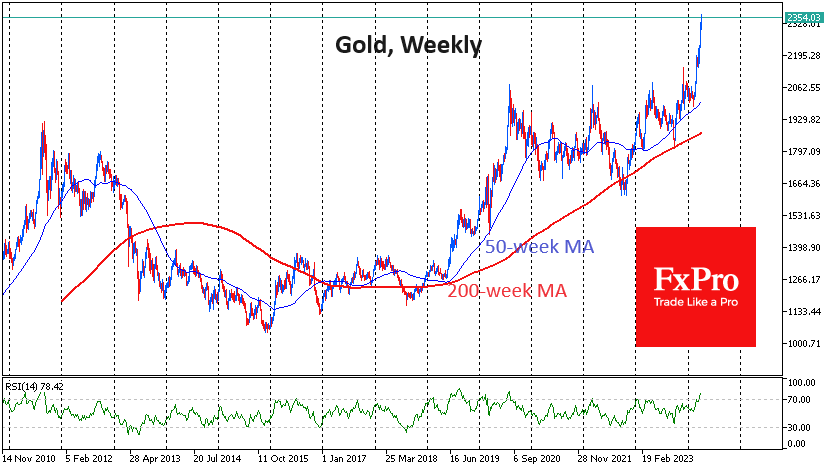

Gold Temporarily Ignores Negative News

Gold has been hitting all-time highs almost daily for the past two weeks, reaching $2365 in the spot market on Tuesday before the start of US trading. The ability to rise above $2070 per ounce, which gold found in late February, has signalled a break of resistance that has kept gold above since August 2020.

Gold is now rising more actively than it did in the previous long-term bull cycle. In 2011, years of gains were followed by a two-year consolidation, which was replaced by a three-year bear market.

Gold has been increasing, reacting to positive news and mostly ignoring the negative. The price reversed sharply to the upside in the final quarter of last year on signals from the Fed that the next step would be a rate cut, not a rate hike. At the same time, the revision of expectations from six or seven to two rate cuts in 2024 did not hinder the rise at all.

It seems that any news on the US is a reason to buy. Signals of a strong economy and inflation – highlight gold’s property of retaining value. Weakness in inflation – fuels expectations that the Fed will be cutting rates soon, which favours demand for risk assets.

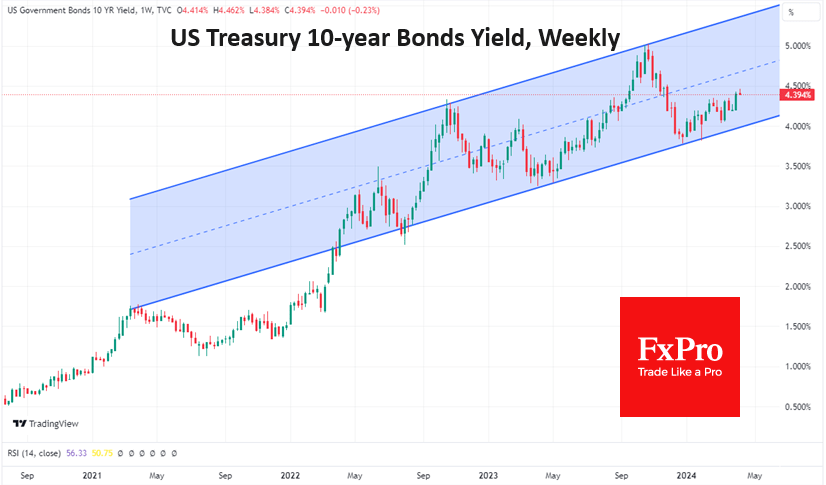

There are risks that bulls are now ignoring the commodity mix looming over them in the form of US bond yields. 10-year treasuries have seen yields rise from 3.8% at the end of January to 4.45% on Monday. The reversal came from the lower boundary of the long-term rising channel, indicating that the smart money is wagering on a high rate scenario for the long haul.

Other markets can’t ignore what’s going on in the government debt market for long. Stock indices are already starting to notice it, forming a smooth downtrend in early April and repeatedly testing previous trading channels.

Meanwhile, gold has been overbought, according to RSI, in daily and weekly timeframes to the maximum since early August 2020. Back then, an eight-week rise was followed by a multi-month pullback.

The US inflation report scheduled for Wednesday has a chance to hurt gold soon. If the outcome for the markets is a further rise in government bond yields, global markets could become more synchronised, triggering a more active sell-off in equity markets and affecting gold and other commodities. In this case, it could take months before we see further price retracement of historical highs.

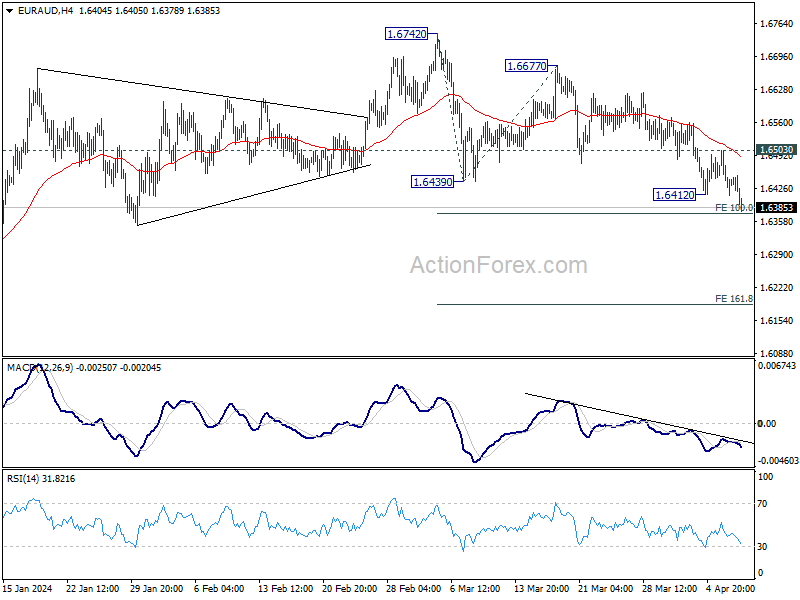

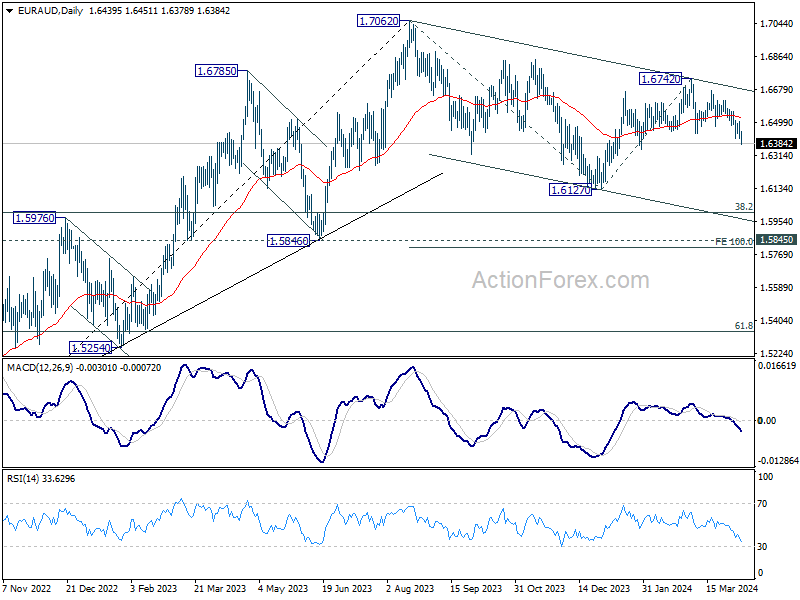

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.6398; (P) 1.6456; (R1) 1.6500; More..

EUR/AUD's decline from 1.6742 resumed by breaking through 1.6412 support and intraday bias is back on the downside. Current development suggests that rebound from 1.6127 has completed. Break of 100% projection of 1.6742 to 1.6439 from 1.6677 at 1.6374 will pave the way to 161.8% projection at 1.6187 next. For now, risk will stay on the downside as long as 1.6503 resistance holds, in case of recovery.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). The correction is still in progress with fall from 1.6742 as the third leg. Strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

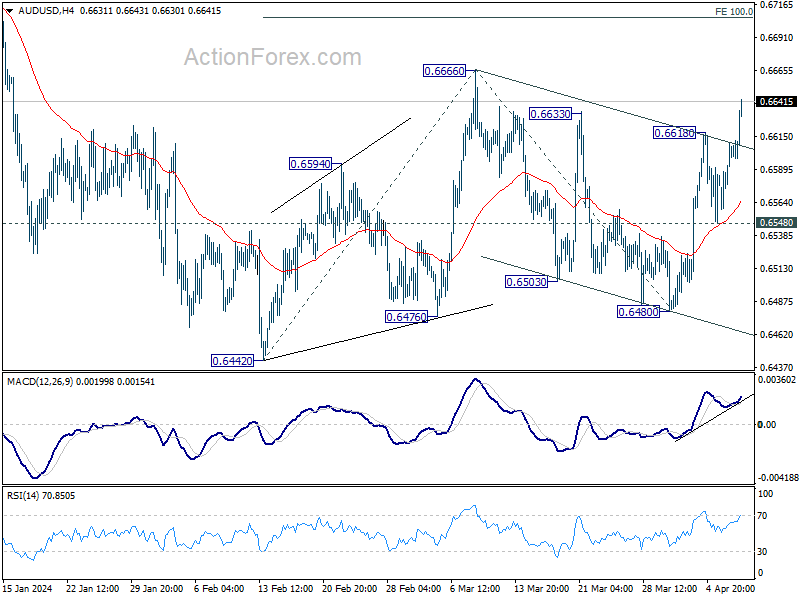

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6573; (P) 0.6592; (R1) 0.6623; More...

AUD/USD's rise from 0.6480 resumed by breaking through 0.6618 resistance and intraday bias is back on the upside. Current development affirms that case pattern from 0.6442 is now in is third leg. Further rise would be seen to 0.6666 and then 100% projection of 0.6442 to 0.6666 from 0.6480 at 0.6704. Nevertheless, break of 0.6548 support will turn bias back to the downside instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.