Sample Category Title

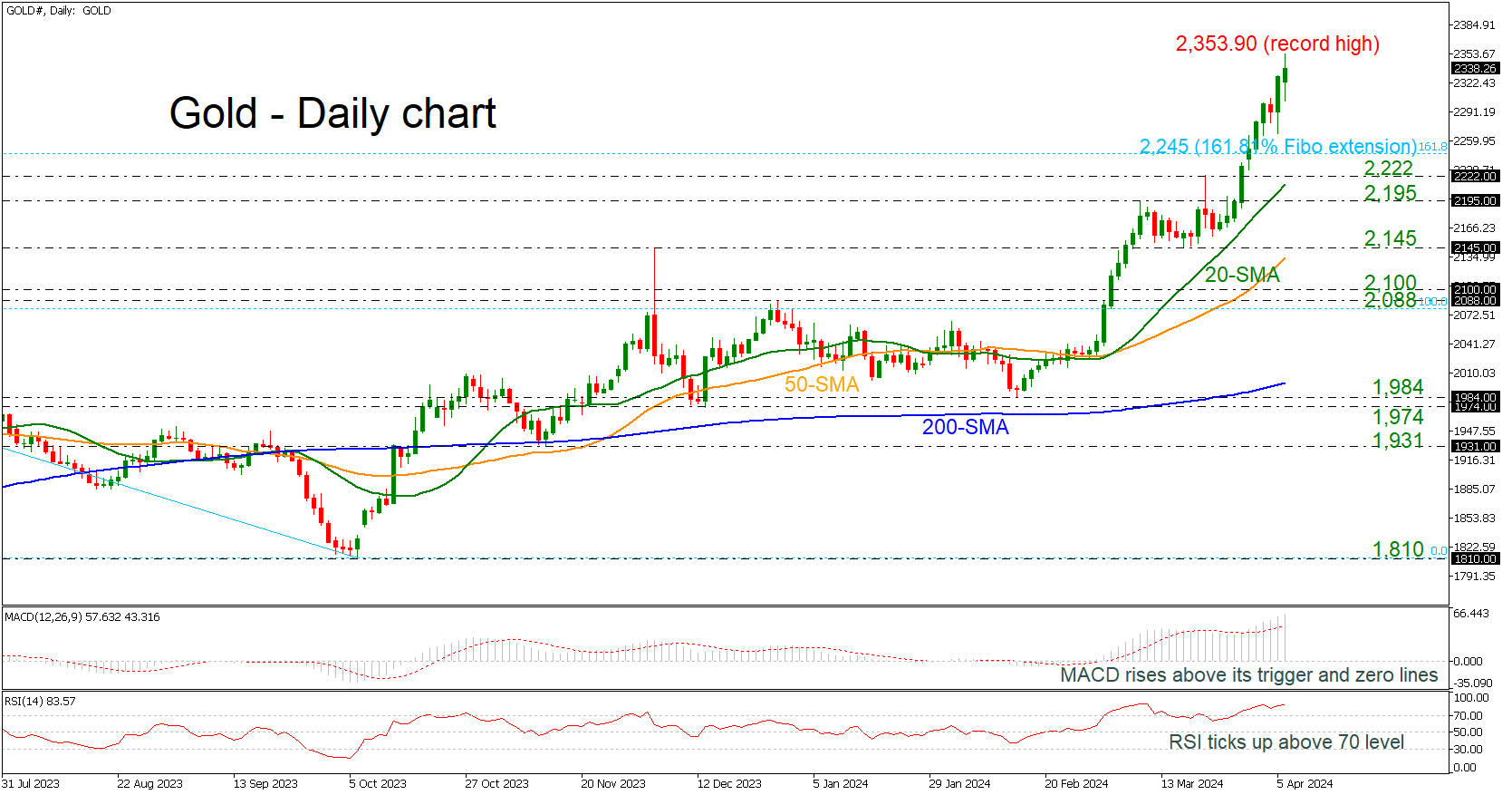

Gold Unlocks Fresh All-time High Again

- Gold reaches 2,353.90 above 161.8% Fibonacci extension

- MACD and RSI move higher in overbought regions

Gold prices are experiencing a fresh higher high today around the 2,353.90 level, successfully surpassing the 161.8% Fibonacci extension level of the downward move from 2,079 to 1,810 at 2,245.

The bullish rally started after the rebound off the 1,984 support with the technical oscillators suggesting even further upside structure. The MACD is standing above its trigger and zero lines, while the RSI is pointing up in the overbought territory.

As the price is moving higher, the next resistance levels to have in mind is the psychological number of 2,400 ahead of the 261.8% Fibonacci extension of 2,515.

On the flip side, a dive beneath the 161.8% Fibonacci of 2,245 could take the market towards the immediate support lines of 2,222 and 2,195, which encapsulates the 20-day simple moving average (SMA) at 2,213. Below that, the 2,145 barricade and the 50-day SMA at 2,134 may halt bearish actions.

Summarizing, the broader outlook in the precious metal is strongly positive and only a decline beneath the 200-day SMA, which is standing at 1,999 may switch the view to a bearish one.

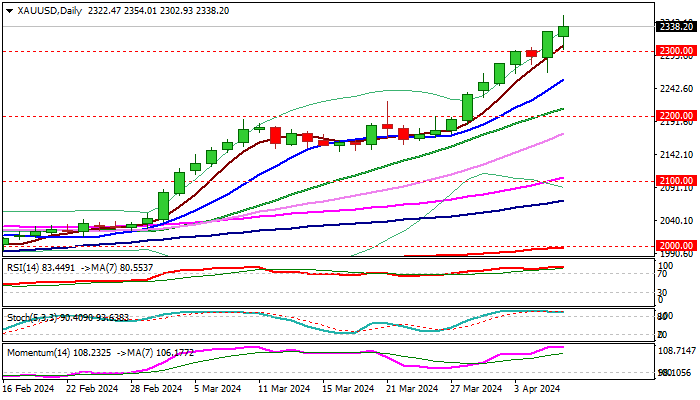

XAU/USD: Gold Hits New Record High Above $2,300

Gold continues to trend higher and posted new record high ($2354) in early Monday trading, in extension of last week’s 4% advance, which generated strong bullish signal on weekly close above psychological $2300 barrier.

The metal remains well supported by strong safe-haven demand, as well as expectations that the Fed will cut rates (as early as June) which deflates dollar.

Gold gained almost 14% since the start of the year, with the strongest acceleration higher seen in March, when the price rose nearly 10%, marking the biggest monthly gains since July 2020.

Bulls firmly hold grip despite strongly overbought technical studies (day/week/month) and eye next target at $2400, but some corrective action should be anticipated.

Broken $2300 barrier reverted to initial support, followed by rising 10DMA ($2256) and strong supports at 2200 zone (rising 20DMA / psychological) which should contain dips and mark a healthy correction of a larger uptrend.

Res: 2354; 2400; 2426; 2500.

Sup: 2300; 2256; 2222; 2200.

BTC/USD Analysis: Bitcoin Price Rises Ahead of Halving

The halving (reduction of block mining rewards) is expected to occur on April 19-20.

Theoretically, Bitcoin mining will become less profitable, leading to a reduction in coin supply. Given unchanged demand, this should drive up the BTC/USD price. Ripple CEO Brad Garlinghouse has forecasted that the cryptocurrency market cap will double by the end of 2024, reaching $5 trillion, with Bitcoin's halving contributing to this growth.

In practice, Bitcoin price is influenced by too many factors to conclusively prove the bullish impact of halving. For instance, looking at history, the last halving occurred on May 11, 2020, and the price increased by approximately 12% in the following week. On the other hand, today's Bitcoin price might already reflect the imminent halving.

Nevertheless, the market currently shows predominantly positive sentiment, as over the weekend, BTC/USD price rose by around 2.5%.

According to the technical analysis of the BTC/USD chart today:

→ From April 2-4, there was no downward pressure on the market to push the price below the lower boundary of the ascending channel (shown in blue), which remains relevant.

→ Conversely, a series of higher lows forming since April 2 indicates bullish intentions to break above the descending channel (shown in red).

Therefore, the approaching halving and associated positive expectations could lead to:

→ Breaking above the consolidating zone (shown with black lines).

→ Overcoming a significant resistance level near the psychological mark of $70,000 per coin.

In this scenario, the nearest target for bulls could be the median line of the blue ascending channel.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*At FXOpen UK and FXOpen AU, Cryptocurrency CFDs are only available for trading by those clients categorised as Professional clients under FCA Rules and Professional clients under ASIC Rules respectively. They are not available for trading by Retail clients.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

EUR/USD: Short-term bullish, till ECB

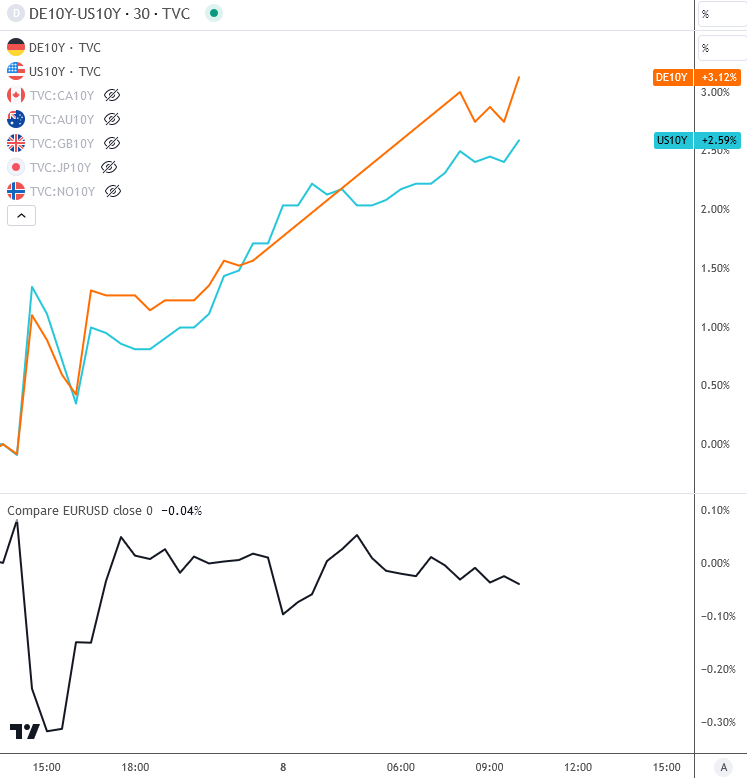

EURUSD stabilized last week, firstly with five five waves up from 10725 which marks an important short-term low, and then bounced after a wave set-back despite strong US jobs data. We see nice wave b correction that is now pointing to higher prices near-term only; possibly wave C up to 1.09-1.0940 area till ECB this Thursday. A slightly higher rates in Germany compared to one in US can be one of the reasons why EURUSD pair holds the support.

US Money Markets Increasingly Push a First Cut by Fed Further into Time

Markets

Friday’s March payrolls were strong across the board. Employment topped all estimates by growing 303k, wage growth was solid and the unemployment rate eased back to 3.8% despite an uptick in the participation rate. The first Fed governors commenting after the release erred to the hawkish side. Dallas president Logan said there’s no urgency in cutting rates, adding that the risk of cutting too soon is higher than being late. She’s worried about disinflation stalling. Fed governor Bowman continues to see upside inflation risks and isn’t comfortable with cutting until disinflation returns. Both Logan and Bowman stated the possibility of a higher neutral rate, which would limit the Fed’s overall cutting capacity. US yields across the maturity spectrum revisited the YtD highs. We expected the break higher would need confirmation from Wednesday’s US CPI (March). Yet, it’s already happening as we speak. Granted, Asian dealings usually just pick up where US financial markets left off but the technical breaks are there. Apart moving beyond the YtD high, the US 2-y yield also surpasses resistance from the 200dMA to trade around 4.78%. The 10-y tenor jumped above the 4.40% resistance (50% recovery on the 2023Q4 decline) this morning and eked out further gains to a new 2024 high. US money markets increasingly push a first cut by the Fed further into time and will look for additional evidence supporting their case in a reaccelerating (headline) CPI. The dollar neither on Friday neither this morning really stands to benefit from the yield support, despite being driven by the real component and concentrating at the front-end of the curve (>10 bps). EUR/USD rebounded from an intraday-low just south of 1.08 to close unchanged at 1.0837. It’s hanging around these levels this morning. Rising German yields offer only part of the explanation since the move higher was only a fraction of what happened in the US (1.2-3.9 bps). A surprisingly resilient risk environment (US stock markets rose up to 1.2%) is a second piece of the puzzle. Equally astounding is the ongoing rally in gold, with new record highs for the shiny metal (again) today. Oil prices retreated sub $90/barrel with a partial retreat by Israeli forces from southern Gaza easing some of the geopolitical/supply concerns. Other than inflation figures in the US, the eco calendar gives the stage to the ECB on Thursday. Frankfurt won’t have the desired wage negotiation data by then, giving Lagarde an easy way out of tricky questions. It does have input from the Bank Lending Survey (Tuesday). The central bank of Canada and New Zealand both meet on Wednesday and US banks kick off the Q1 earnings season on Friday. A slew of Fed speeches are scattered across the week.

News & Views

Peter Pellegrini has won the presidential elections in Slovakia this weekend as he defeated the pro-Western candidate Ivan Korcok. Pellegrini is an ally of Prime Minister Robert Fico and is seen as Russia-friendly. Pellegrini secured 53.1% of the votes. Even as the president in Slovakia has only limited executive powers, the victory of Pellegrini is seen as supporting a policy of the country further withdrawing its support for Ukraine. Pellegrini who, as a president, can veto laws and can nominate judges, also might support reforms of the government with respect to criminal law and media that might be contested by the EU. Despite his Pro-Russian, Ukraine sceptic stance, Pellegrini reiterated that Slovakia will remain a strong member of EU and Nato.

In a news conference on Friday, Governor of the National Bank of Poland (NBP) Glapinski said that the NBP didn’t discuss rate cuts at last week’s policy meeting. He even indicated that no one is talking about 2024 rate cuts altogether. The room for rate cuts in 2025 will depend on the inflation figures at the end of this year. Glapinski reiterated that there is still a high the degree of uncertainty. Polish CPI in Q4 is seen in a wide range between 3.9% (if anti-inflation measures are maintained) and 7.5% (if fully removed). Glapinski sees current decline in inflation as temporary (1.9% Y/Y in March) as higher VAT on food prices will filter through in coming months. Glapinski is also worried about the inflationary impact of real wages rising fast together with a reacceleration of the economy. Polish 2-y swap yields jumped 9 bps Friday afternoon (5.43%), even as this was partially due to the overall rise in core yields post strong US payrolls. The zloty remains well bid. At EUR/PLN 4.28, the Polish currency is holding within reach of the strongest levels against the euro since February 2020. (YTD low 4.2749).

Will German Industry Continue to Look Weak

In focus today

Today, we look out for German industrial production data for February, which will give more information on the state of the German industry that is still very weak.

The first round of the central wage settlement in Norway is now underway. The framework for the settlement in the manufacturing sector is stated by the parties to involve a wage increase of 5.2 % this year, given that the wage drift will be as expected. This settlement works as a blueprint for the settlements in other sectors as well, so we expect that this estimate will stand when all the settlements are finished. In that case, this will be a bit higher than Norges Bank assumed in its March monetary policy report of 4.9% and will probably add to the recent reprising of cut expectations even in Norway.

Riksbank Governor Erik Thedéen is giving three speeches today, which largely deal with the standard theme of the economic situation and current monetary policy and are therefore not expected to differ remarkably.

The main events this week are US March CPI on Wednesday, and policy rate decisions from both New Zealand (Tuesday night) and the ECB (Thursday). We expect both to keep rates unchanged. We have gotten strong hints from the ECB that it will deliver its first rate cut in June, so the primary insight from Thursday's meeting will be whether they confirm this stance.

Economic and market news

What happened over the weekend

After gaining 4% last week, oil prices declined overnight with the Brent price dropping 1.6% to 89.71 USD/bbl as of this morning. This is due to expectations of easing tensions in the Middle East after Israel and Hamas committed to new peace talks in Egypt.

What happened Friday

Markets scaled back US rate cut expectations after the March non-farm payrolls figure exceeded expectations at +303,000 (consensus: +200,000). The jobs report also showed that average hourly earnings increased 0.3% m/m. This suggests that wage sum growth accelerated which is a concern for the Fed from an inflation perspective. We also got hawkish comments from the Fed's Logan and Bowman, with the latter saying that "inflation progress has stalled". USD was initially stronger but reversed and ended the day broadly unchanged, while the 2Y treasury added 9bp.

Bank of Japan governor Ueda said he expected inflation to accelerate from "summer towards autumn" due to the large wage increases agreed to during union negotiations in March. He reiterated that another rate hike would be data dependent but that it is on the table if the 2% inflation target is sustainably achieved.

Equities: Global equities ended higher on Friday, but lower for the week. Interesting on Friday was the reaction to the jobs report. At first glance, the very strong report sent yields higher while equity investors saw it as "too strong" and reacted negatively. However, later into the US cash session, equities turned around and ended sharply higher led by cyclical growth stocks. This is more or less how we see the coming period where strong macro data should continue to support risky assets while higher yields should be a temporary challenge. Asian markets are mostly higher this morning led by Japan. European futures are higher as well while US futures are lower.

FI: The main event this week is the ECB meeting on Thursday, where we look for a "confirmation" of a rate cut in June as discussed in our ECB preview as well as RTM Euroland, where we also discuss the outlook and market impact for a downgrade of France. The other main event is the US CPI data released on Wednesday together with the minutes of the latest FOMC meeting. If the data continues to surprise on the upside the market is expected to price out more rate cuts in 2024. This should put upwards pressure on US Treasury yields as seen last week, where 10Y Treasury yields rose some 20bp.

FX: EUR/USD ended the week slightly higher above the 1.08 mark after the stronger-than-expected US jobs report on Friday. Intervention talks sent USD/JPY a bit lower on Friday, but the move reversed, and the cross is trading just below 152 again. The Scandies had a good week, with both the NOK and the SEK appreciating against the EUR and the USD. EUR/NOK declined to around 11.60, while EUR/SEK fell to around 11.50. EUR/GBP trended higher for most of last week and ended around 0.8580.

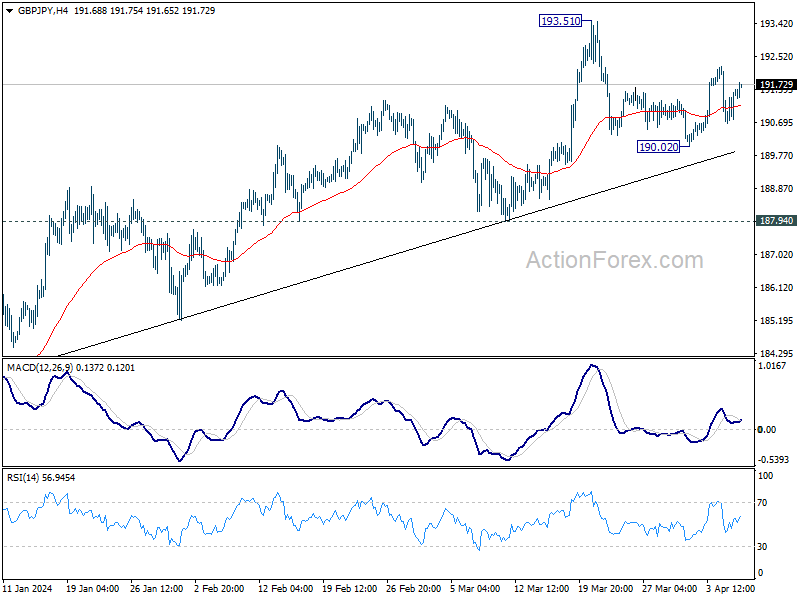

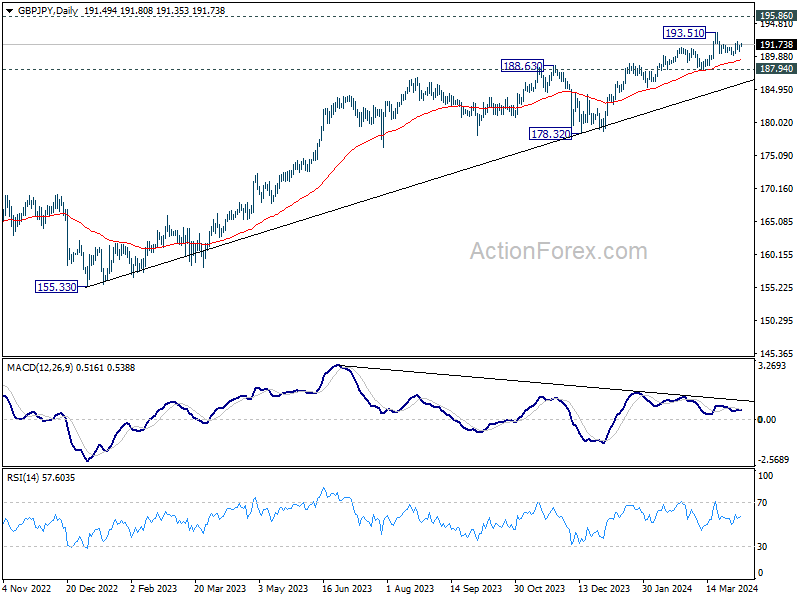

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.00; (P) 191.31; (R1) 191.95; More.....

Intraday bias in GBP/JPY remains neutral and more consolidations could be seen below 193.51./ On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. On the downside, though, break of 190.02 will turn bias to the downside for 187.94 support instead.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

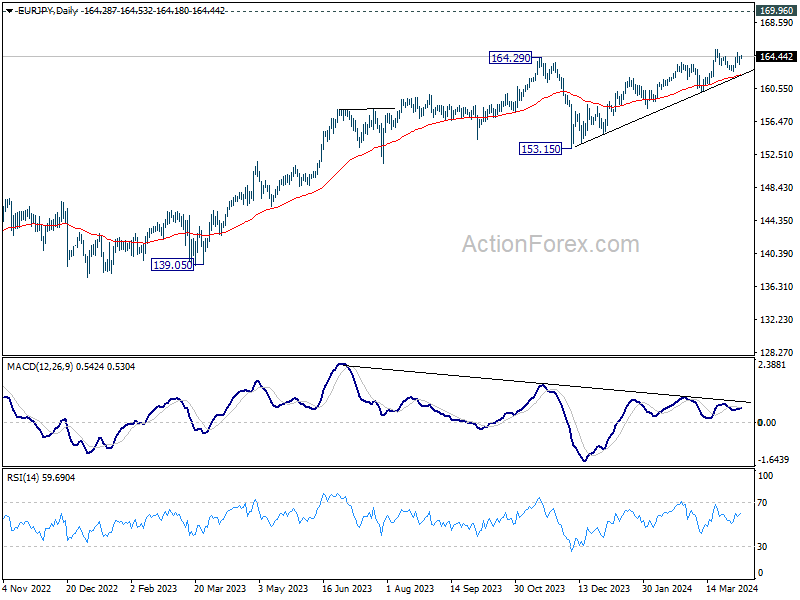

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.77; (P) 164.10; (R1) 164.72; More...

Intraday bias in EUR/JPY remains neutral and more consolidations could be seen below 65.33. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. On the downside, though, break of 162.59 will turn bias to the downside for 160.20 support next.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

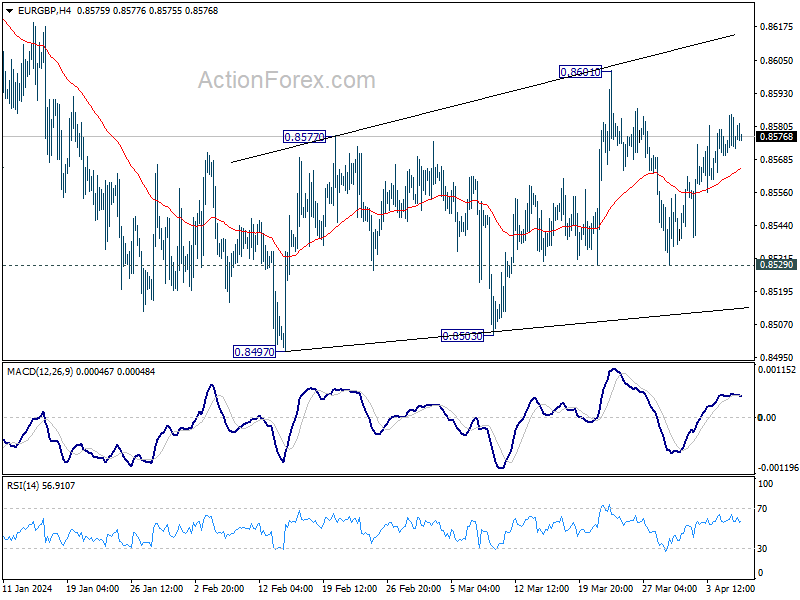

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8569; (P) 0.8577; (R1) 0.8584; More...

Intraday bias in EUR/GBP stays neutral for the moment. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8713 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

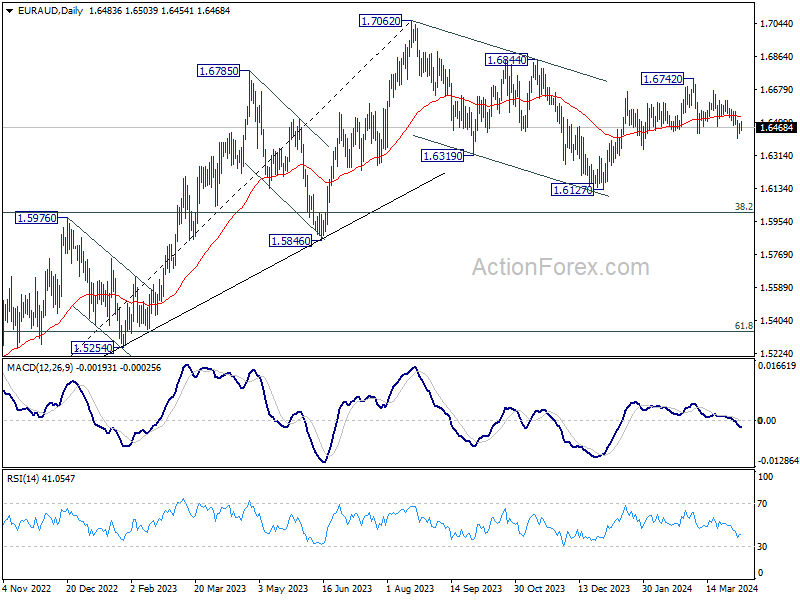

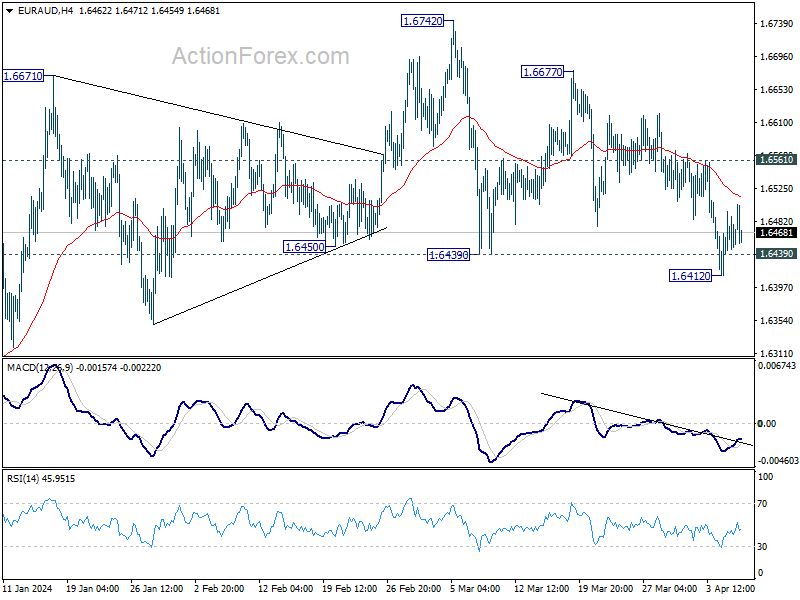

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6427; (P) 1.6462; (R1) 1.6506; More..

Intraday bias in EUR/AUD remains neutral at this point. On the downside, break of 1.6412 and sustained trading below 1.6439 support will argue that whole rebound from 1.6127 has completed, and turn near term outlook bearish for this support again. Nevertheless, strong rebound from current level, followed by break of 1.6561 minor resistance, will turn bias back to the upside for retesting 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.