Sample Category Title

USD/CAD Weekly Outlook

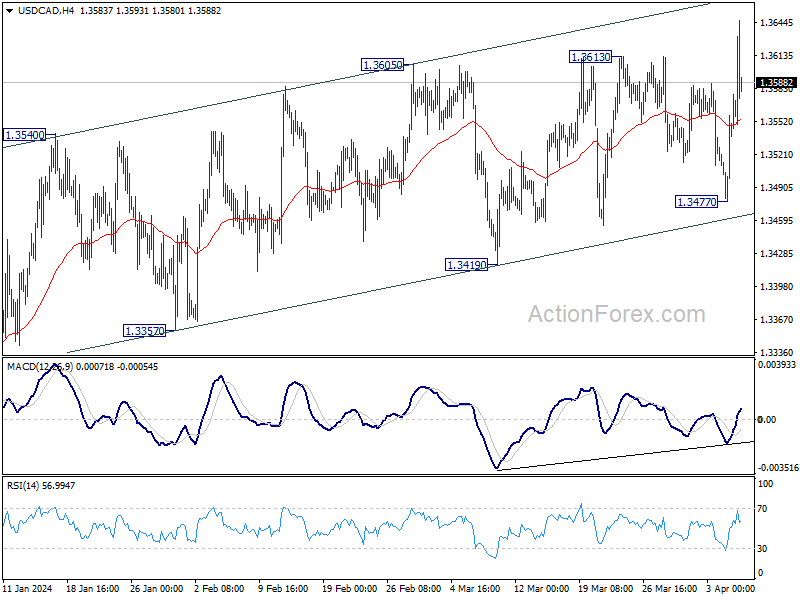

USD/CAD's rise from 1.3176 resumed by breaching 1.3613 resistance last week. Initial bias stays on the upside this week for channel resistance at 1.3665 first. Sustained break there would prompt upside acceleration towards 1.3897 resistance next. For now, near term outlook will stay bullish as long as 1.3477 support holds, in case of retreat.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

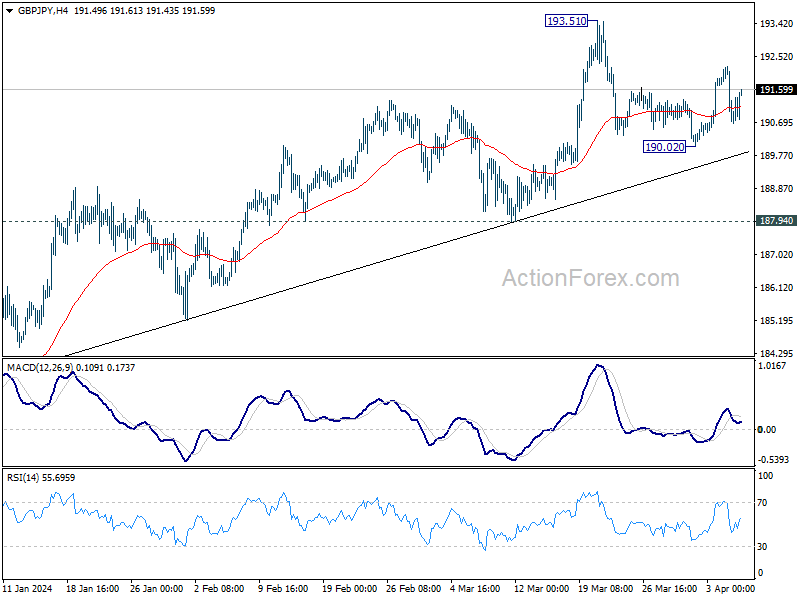

GBP/JPY Weekly Outlook

GBP/JPY rebounded after initial dip to 190.02 but failed to break through 193.51 resistance. Initial bias remains neutral this week for more consolidations. On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. On the downside, though, break of 190.02 will turn bias to the downside for 187.94 support instead.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

a href="https://www.actionforex.com/wp-content/uploads/2024/04/gbpjpy20240406w2.png">

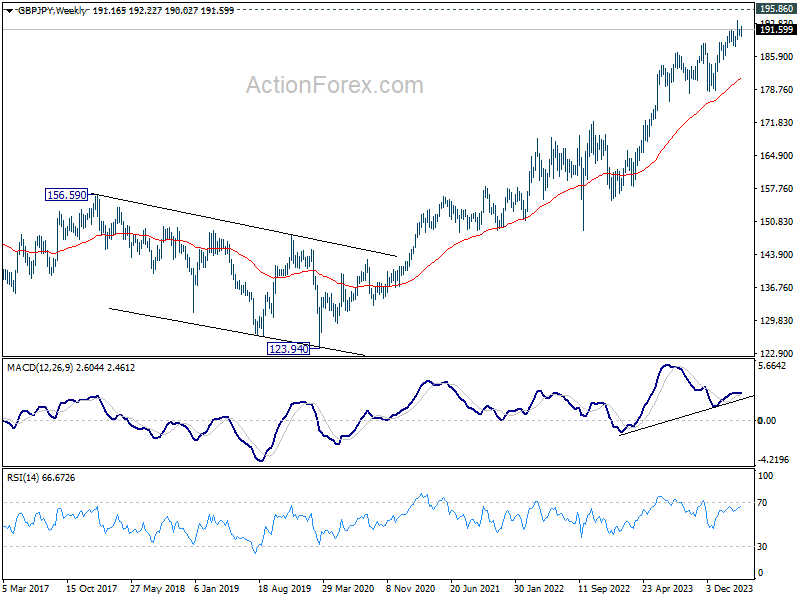

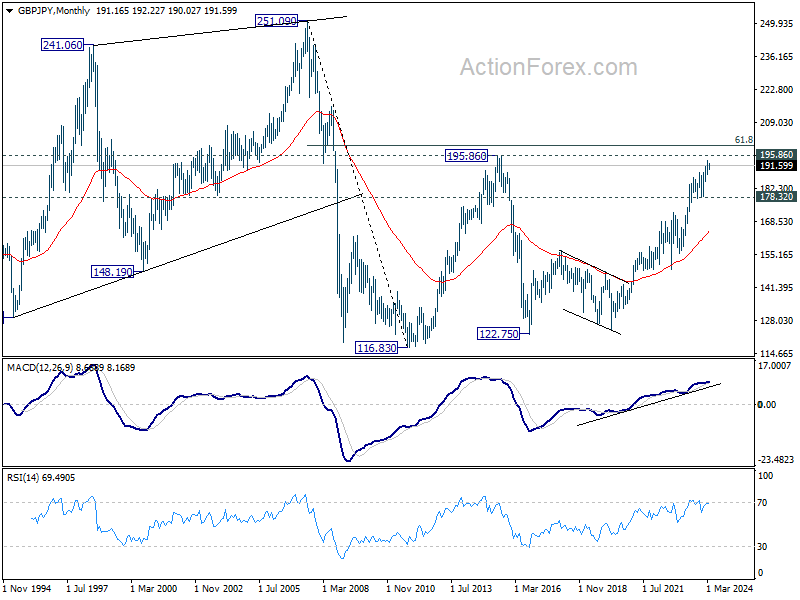

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Further rally will remain in favor as long as 178.32 support holds. Break of 195.86 (2015 high) is possible. But strong resistance could be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80 to limit upside, at least on first attempt.

<

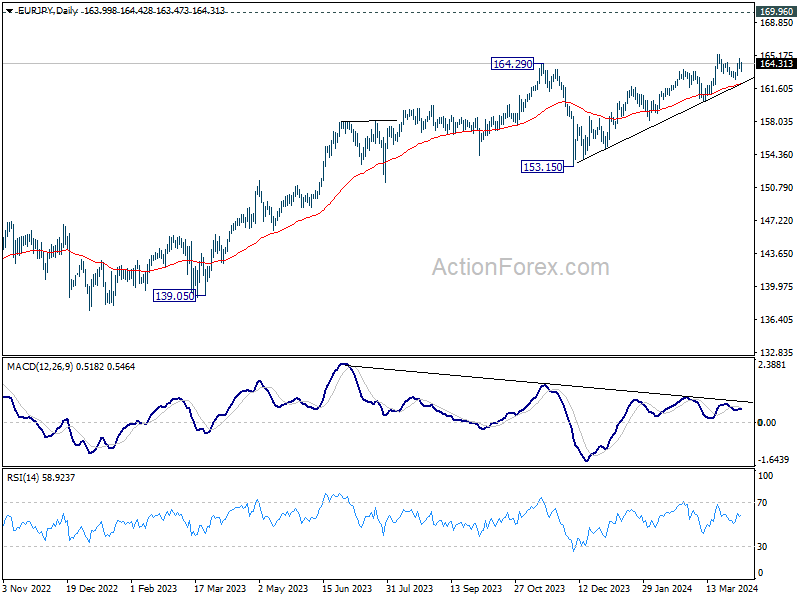

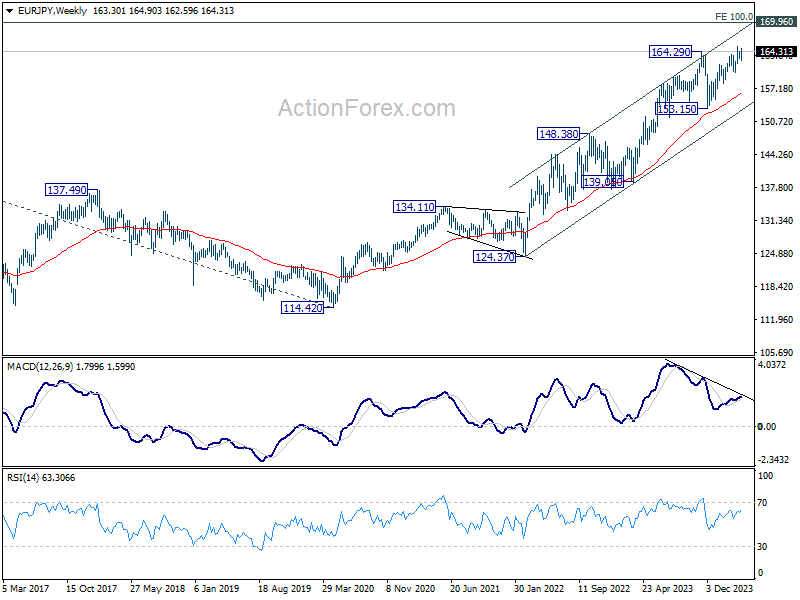

EUR/JPY Weekly Outlook

EUR/JPY rebounded after initial dip to 162.59 but failed to break through 165.33 resistance. Initial bias remains neutral this week first and more range trading could be seen. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. On the downside, though, break of 162.59 will turn bias to the downside for 160.20 support next.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 153.15 support holds.

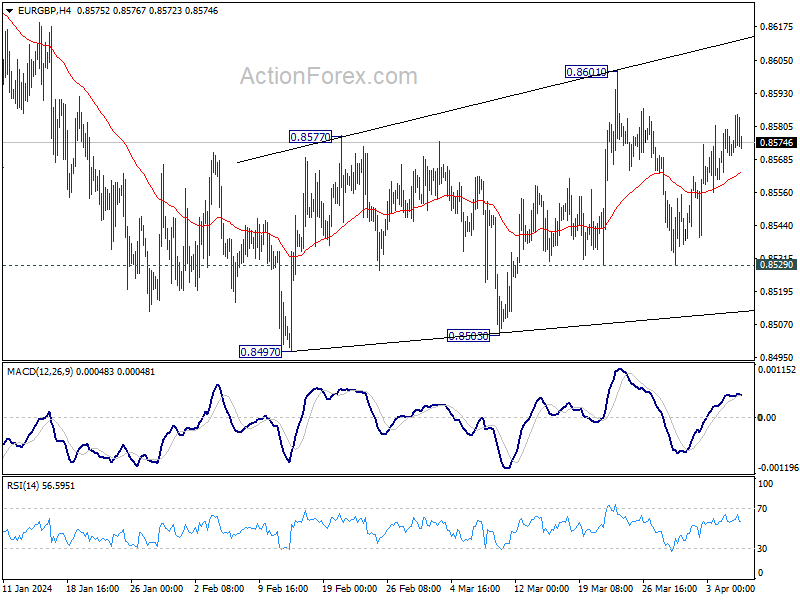

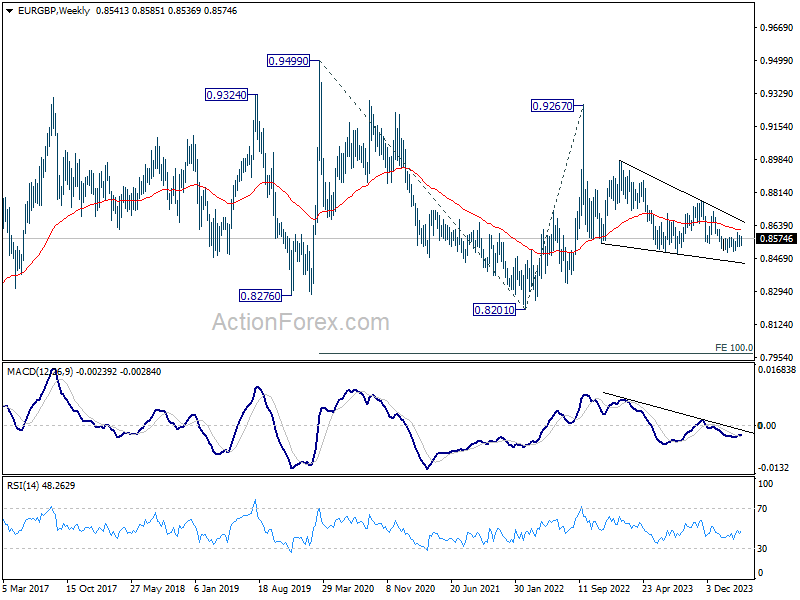

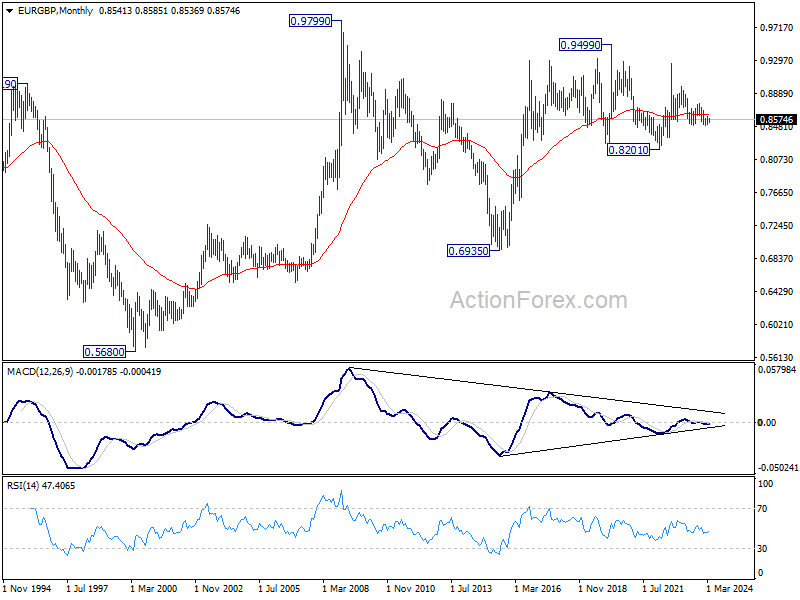

EUR/GBP Weekly Outlook

EUR/GBP remains bounded in range last week and outlook is unchanged. Initial bias stays neutral this week first. On the downside, firm break of 0.8529 support will argue that the corrective recovery from 0.8497 has completed at 0.8601. Intraday bias will be back on the downside for retesting 0.8497 low next. On the upside, break of 0.8601 will resume the rebound instead.

In the bigger picture, there is no clear sign that down trend from 0.9267 has completed, despite loss of downside momentum as seen in D MACD. As long as 0.8713 resistance holds, the down trend will remain in favor to resume through 0.8491 low at la later stage.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

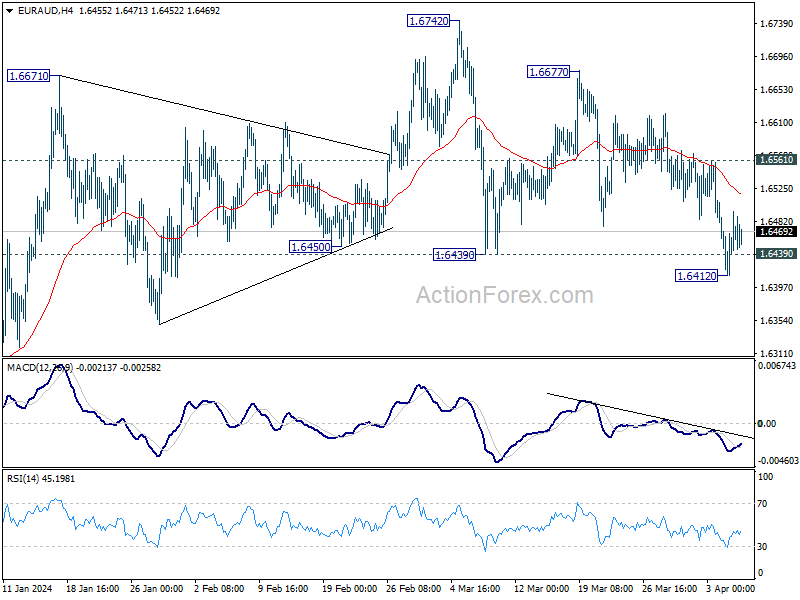

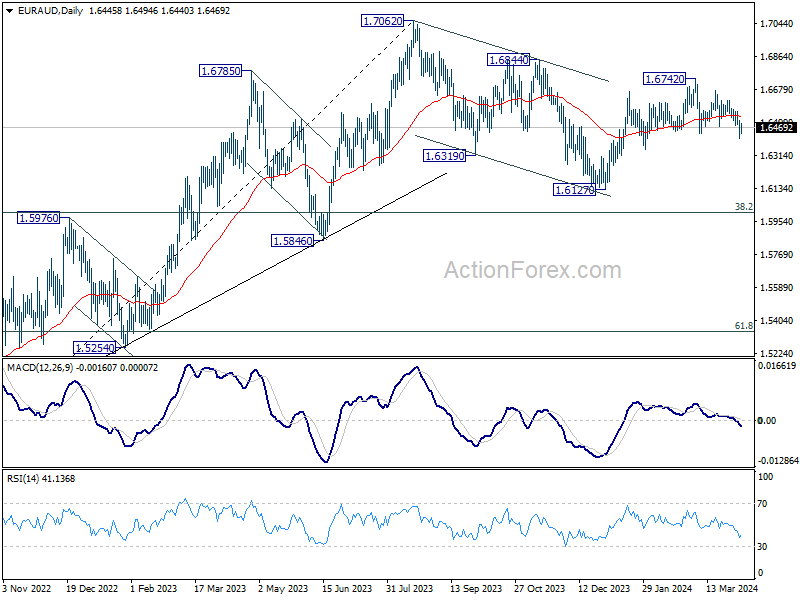

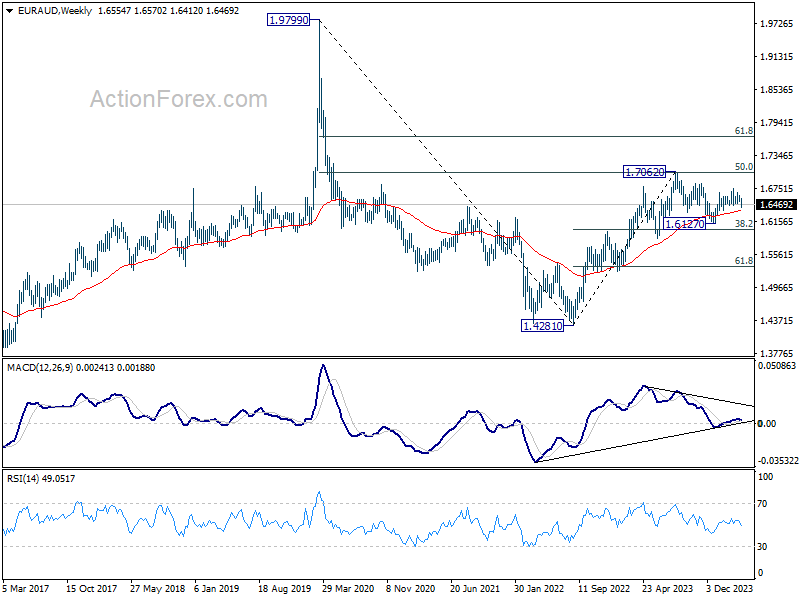

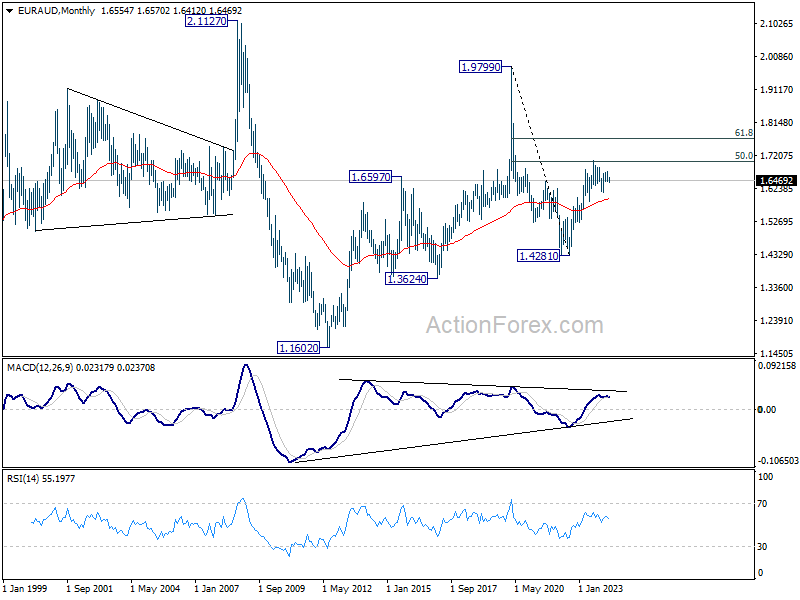

EUR/AUD Weekly Outlook

EUR/AUD dipped to 1.6412 last week but recovered since then. Initial bias remains neutral this week first. On the downside, break of 1.6412 and sustained trading below 1.6439 support will argue that whole rebound from 1.6127 has completed, and turn near term outlook bearish for this support again. Nevertheless, strong rebound from current level, followed by break of 1.6561 minor resistance, will turn bias back to the upside for retesting 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5950) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

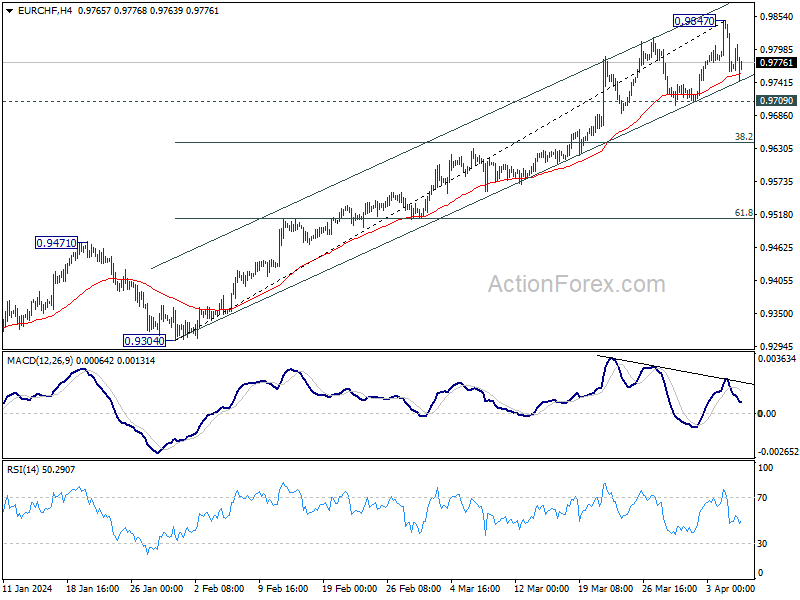

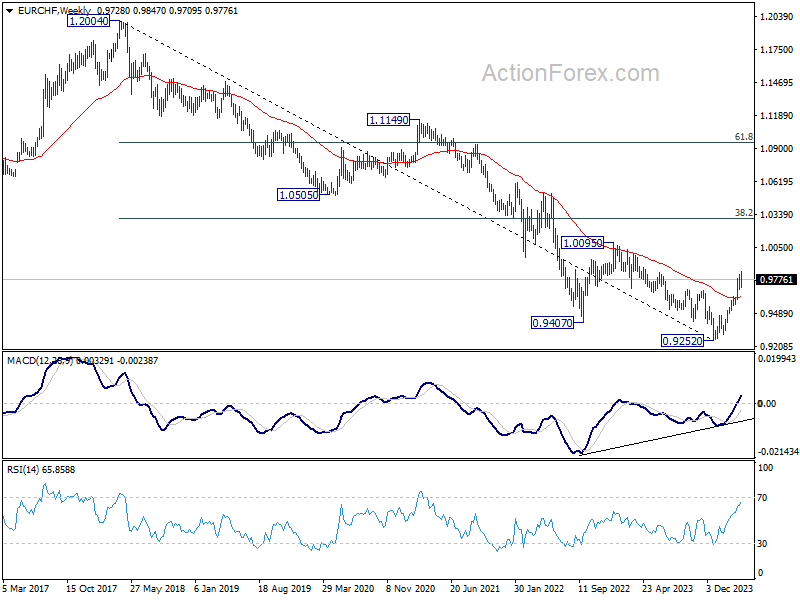

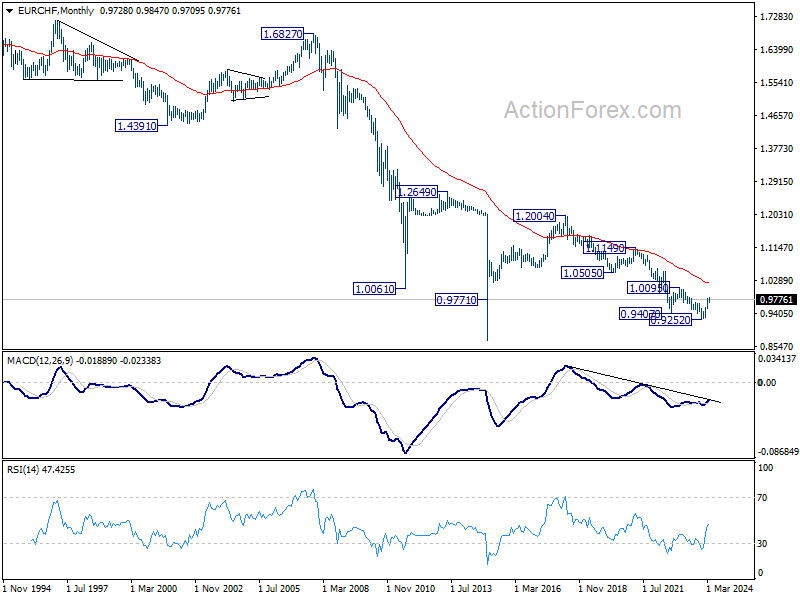

EUR/CHF Weekly Outlook

EUR/CHF's up trend extended to 0.9847 last week but retreated since then. Initial bias is turned neutral this week for consolidation first. But near term outlook will stay bullish as long as 0.9709 support holds. However, considering bearish divergence condition in 4H MACD, break of 0.9709 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9603) holds.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 4/8 – 4/12

Monday, Apr 8, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Feb | 1.80% | 2.00% |

| 23:50 | JPY | Current Account (JPY) Feb | 1.99T | 2.73T |

| 05:00 | JPY | Eco Watchers Survey: Current Mar | 51.6 | 51.3 |

| 05:45 | CHF | Unemployment Rate Mar | 2.20% | 2.20% |

| 06:00 | EUR | Germany Industrial Production M/M Feb | 0.60% | 1.00% |

| 06:00 | EUR | Germany Trade Balance (EUR) Feb | 25.1B | 27.5B |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Apr | -8.3 | -10.5 |

| 22:00 | NZD | NZIER Business Confidence Q1 | -2 | |

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Mar | 1.80% | 1.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Feb | |

| Forecast: 1.80% | Previous: 2.00% | ||

| 23:50 | JPY | Current Account (JPY) Feb | |

| Forecast: 1.99T | Previous: 2.73T | ||

| 05:00 | JPY | Eco Watchers Survey: Current Mar | |

| Forecast: 51.6 | Previous: 51.3 | ||

| 05:45 | CHF | Unemployment Rate Mar | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 06:00 | EUR | Germany Industrial Production M/M Feb | |

| Forecast: 0.60% | Previous: 1.00% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Feb | |

| Forecast: 25.1B | Previous: 27.5B | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Apr | |

| Forecast: -8.3 | Previous: -10.5 | ||

| 22:00 | NZD | NZIER Business Confidence Q1 | |

| Forecast: | Previous: -2 | ||

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Mar | |

| Forecast: 1.80% | Previous: 1.00% | ||

Tuesday, Apr 9, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Apr | -1.80% | |

| 01:30 | AUD | NAB Business Confidence Mar | 0 | |

| 01:30 | AUD | NAB Business Conditions Mar | 10 | |

| 05:00 | JPY | Consumer Confidence Mar | 39.7 | 39.1 |

| 06:00 | JPY | Machine Tool Orders Y/Y Mar P | -8.00% | |

| 06:45 | EUR | France Trade Balance (EUR) Feb | -7.0B | -7.4B |

| 10:00 | USD | NFIB Business Optimism Index Mar | 90.2 | 89.4 |

| 23:50 | JPY | Bank Lending Y/Y Mar | 3.10% | 3.00% |

| 23:50 | JPY | PPI Y/Y Mar | 0.80% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Apr | |

| Forecast: | Previous: -1.80% | ||

| 01:30 | AUD | NAB Business Confidence Mar | |

| Forecast: | Previous: 0 | ||

| 01:30 | AUD | NAB Business Conditions Mar | |

| Forecast: | Previous: 10 | ||

| 05:00 | JPY | Consumer Confidence Mar | |

| Forecast: 39.7 | Previous: 39.1 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Mar P | |

| Forecast: | Previous: -8.00% | ||

| 06:45 | EUR | France Trade Balance (EUR) Feb | |

| Forecast: -7.0B | Previous: -7.4B | ||

| 10:00 | USD | NFIB Business Optimism Index Mar | |

| Forecast: 90.2 | Previous: 89.4 | ||

| 23:50 | JPY | Bank Lending Y/Y Mar | |

| Forecast: 3.10% | Previous: 3.00% | ||

| 23:50 | JPY | PPI Y/Y Mar | |

| Forecast: 0.80% | Previous: 0.60% | ||

Wednesday, Apr 10, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% |

| 08:00 | EUR | Italy Retail Sales M/M Feb | 0.20% | -0.10% |

| 12:30 | CAD | Building Permits M/M Feb | -3.50% | 13.50% |

| 12:30 | USD | CPI M/M Mar | 0.30% | 0.40% |

| 12:30 | USD | CPI Y/Y Mar | 3.40% | 3.20% |

| 12:30 | USD | CPI Core M/M Mar | 0.30% | 0.40% |

| 12:30 | USD | CPI Core Y/Y Mar | 3.70% | 3.80% |

| 13:45 | CAD | BoC Rate Decision | 5.00% | 5.00% |

| 14:00 | USD | Wholesale Inventories Feb F | 0.50% | 0.50% |

| 14:30 | USD | Crude Oil Inventories | 3.2M | |

| 15:30 | CAD | BoC Press Conference | ||

| 18:00 | USD | FOMC Minutes | ||

| 23:01 | GBP | RICS Housing Price Balance Mar | -6% | -10% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Mar | 2.40% | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | NZD | RBNZ Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 08:00 | EUR | Italy Retail Sales M/M Feb | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 12:30 | CAD | Building Permits M/M Feb | |

| Forecast: -3.50% | Previous: 13.50% | ||

| 12:30 | USD | CPI M/M Mar | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | CPI Y/Y Mar | |

| Forecast: 3.40% | Previous: 3.20% | ||

| 12:30 | USD | CPI Core M/M Mar | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | CPI Core Y/Y Mar | |

| Forecast: 3.70% | Previous: 3.80% | ||

| 13:45 | CAD | BoC Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 14:00 | USD | Wholesale Inventories Feb F | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 3.2M | ||

| 15:30 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 18:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

| 23:01 | GBP | RICS Housing Price Balance Mar | |

| Forecast: -6% | Previous: -10% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Mar | |

| Forecast: 2.40% | Previous: 2.50% | ||

Thursday, Apr 11, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Apr | 4.30% | |

| 01:30 | CNY | CPI Y/Y Mar | 0.40% | 0.70% |

| 01:30 | CNY | PPI Y/Y Mar | -2.80% | -2.70% |

| 08:00 | EUR | Italy Industrial Output M/M Feb | 0.50% | -1.20% |

| 12:15 | EUR | ECB Main Refinancing Operations Rate | 4.50% | 4.50% |

| 12:15 | EUR | ECB Rate On Deposit Facility | 4.00% | 4.00% |

| 12:30 | USD | PPI M/M Mar | 0.30% | 0.60% |

| 12:30 | USD | PPI Y/Y Mar | 2.30% | 1.60% |

| 12:30 | USD | PPI Core M/M Mar | 0.20% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Mar | 2.30% | 2.00% |

| 12:30 | USD | Initial Jobless Claims (Apr 5) | 215K | 221K |

| 12:45 | EUR | ECB Press Conference | ||

| 14:30 | USD | Natural Gas Storage | -37B | |

| 22:30 | NZD | Business NZ PMI Mar | 49.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Apr | |

| Forecast: | Previous: 4.30% | ||

| 01:30 | CNY | CPI Y/Y Mar | |

| Forecast: 0.40% | Previous: 0.70% | ||

| 01:30 | CNY | PPI Y/Y Mar | |

| Forecast: -2.80% | Previous: -2.70% | ||

| 08:00 | EUR | Italy Industrial Output M/M Feb | |

| Forecast: 0.50% | Previous: -1.20% | ||

| 12:15 | EUR | ECB Main Refinancing Operations Rate | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 12:15 | EUR | ECB Rate On Deposit Facility | |

| Forecast: 4.00% | Previous: 4.00% | ||

| 12:30 | USD | PPI M/M Mar | |

| Forecast: 0.30% | Previous: 0.60% | ||

| 12:30 | USD | PPI Y/Y Mar | |

| Forecast: 2.30% | Previous: 1.60% | ||

| 12:30 | USD | PPI Core M/M Mar | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 12:30 | USD | PPI Core Y/Y Mar | |

| Forecast: 2.30% | Previous: 2.00% | ||

| 12:30 | USD | Initial Jobless Claims (Apr 5) | |

| Forecast: 215K | Previous: 221K | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -37B | ||

| 22:30 | NZD | Business NZ PMI Mar | |

| Forecast: | Previous: 49.3 | ||

Friday, Apr 12, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 03:00 | CNY | Trade Balance (USD) Mar | 70.2B | 125.2B |

| 04:30 | JPY | Industrial Production M/M Feb F | -0.10% | -0.10% |

| 06:00 | EUR | Germany CPI M/M Mar F | 0.40% | 0.40% |

| 06:00 | EUR | Germany CPI Y/Y Mar F | 2.20% | 2.20% |

| 06:00 | GBP | GDP M/M Feb | 0.10% | 0.20% |

| 06:00 | GBP | Manufacturing Production M/M Feb | 0.20% | 0.00% |

| 06:00 | GBP | Manufacturing Production Y/Y Feb | 2% | |

| 06:00 | GBP | Industrial Production M/M Feb | 0.00% | -0.20% |

| 06:00 | GBP | Industrial Production Y/Y Feb | 0.50% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Feb | -14.5B | -14.5B |

| 11:00 | GBP | NIESR GDP Estimate Mar | 0.00% | |

| 12:30 | USD | Import Price Index M/M Mar | 0.40% | 0.30% |

| 14:00 | USD | Michigan Consumer Sentiment Index Apr P | 79.0 | 79.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 03:00 | CNY | Trade Balance (USD) Mar | |

| Forecast: 70.2B | Previous: 125.2B | ||

| 04:30 | JPY | Industrial Production M/M Feb F | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 06:00 | EUR | Germany CPI M/M Mar F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 06:00 | EUR | Germany CPI Y/Y Mar F | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 06:00 | GBP | GDP M/M Feb | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 06:00 | GBP | Manufacturing Production M/M Feb | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Feb | |

| Forecast: | Previous: 2% | ||

| 06:00 | GBP | Industrial Production M/M Feb | |

| Forecast: 0.00% | Previous: -0.20% | ||

| 06:00 | GBP | Industrial Production Y/Y Feb | |

| Forecast: | Previous: 0.50% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Feb | |

| Forecast: -14.5B | Previous: -14.5B | ||

| 11:00 | GBP | NIESR GDP Estimate Mar | |

| Forecast: | Previous: 0.00% | ||

| 12:30 | USD | Import Price Index M/M Mar | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr P | |

| Forecast: 79.0 | Previous: 79.4 | ||

The Weekly Bottom Line: Don’t Bet on June

U.S. Highlights

- Treasury yields shot higher this week, as expectations for a June rate cut fell.

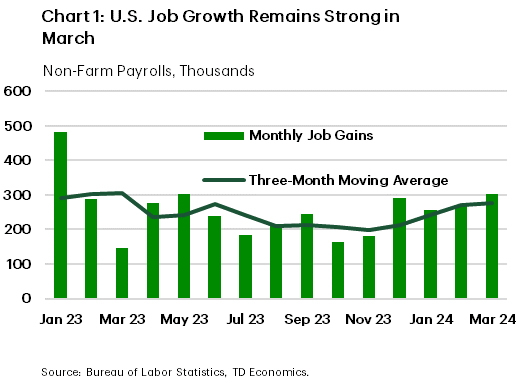

- The U.S. economy had another strong month of hiring in March – adding 303k jobs – while the unemployment rate ticked down to 3.8%.

- Seven voting FOMC members were out speaking this week and the messaging was consistent: policymakers are in no rush to cut rates.

Canadian Highlights

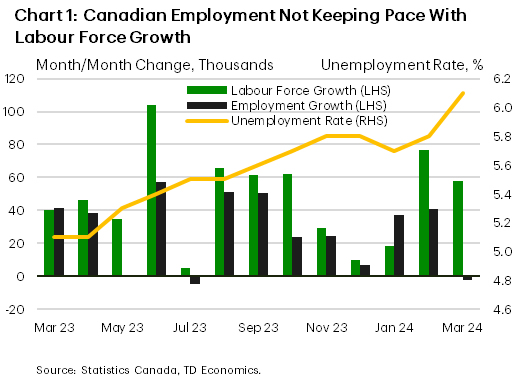

- Canada’s labour market lost some more steam in March, with the unemployment rate on the rise again. However, wages continue to show signs of stickiness.

- In contrast, international trade data as well as business and consumer sentiment are pointing to an improved economic backdrop after months of stall-speed growth.

- Interest rate relief is on the horizon, but the Bank of Canada is unlikely to move off its current policy stance at next week’s meeting.

U.S. – Don’t Bet on June

The first trading week of the second quarter saw Treasury yields push higher as market participants continued to dial back expectations on the timing of the first-rate cut. According to CME Fed futures, a June cut is only 53% priced, and expectations are now for a total of 60 basis points (bps) of cuts by year-end – a far cry from the 150-bps priced at the beginning of the year. Higher readings on inflation, a resilient economy, and a cautious FOMC have all been factors reinforcing the recent recalibration of expectations. At the time of writing, the 10-year Treasury yield is up 15 bps for the week (to 4.35%) and has risen nearly 50 bps since the beginning of the year.

It was a very busy week on the economic data calendar, but the headline release was Friday’s employment report. The U.S. economy added 303k jobs in March, well ahead of the consensus forecast. Meanwhile, the household survey showed strong gains in both the labor force and civilian employment, with the net effect being the unemployment rate ticking down to 3.8%.

On aggregate, the labor market remains healthy and has yet to show any meaningful signs of cooling. Over the past three months, job gains have averaged 276k – slightly stronger than the 251k averaged in 2023 (Chart 1). With job openings still elevated, and increased immigration alleviating some of the pressure on labor supply, job growth could conceivably run in the 150k-200k range for the rest of the year. This would go a long way in rebalancing the labor market, without necessitating any meaningful increase in the unemployment rate.

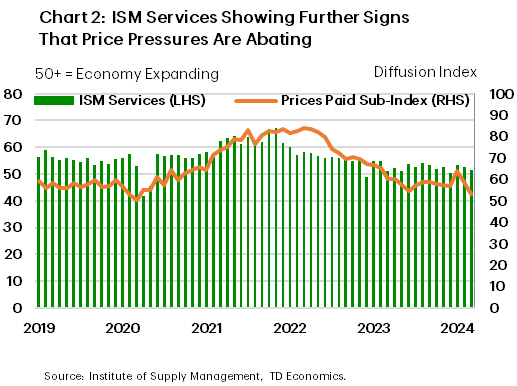

Other economic data out this week also brought encouraging news on the state of the economy. The ISM manufacturing index unexpectedly broke above the 50 mark – the threshold of expansion territory – for the first time in sixteen months. The release showed manufacturing activity is finding a firmer footing alongside an uptick in current production and a rebound in new orders. Meanwhile, the ISM services index slipped to a three-month low. The pullback reflected some softening in new-orders and a sharp decline in the prices paid sub-index, which fell to the lowest level since March 2020 (Chart 2). On the surface, this is an encouraging development for Fed officials who are struggling to rein in still elevated service inflation. However, the fact that 13 industries are still reporting an increase in prices suggests that even with some recent stabilization in the rate of price growth, elevated price pressures remain a concern.

This is why all seven voting FOMC officials out speaking this week maintained a cautious tone on the timing of rate cuts. In a speech delivered on Wednesday, Chair Powell stuck to the script, reiterating that he still believes, ‘rate cuts are likely to be appropriate at some point this year’ though decisions will be made on a ‘meeting by meeting’ basis. With the Fed waiting for further evidence of cooling inflationary pressures, next week’s CPI release will offer further insight on whether the recent uptick in inflation a speed bump, or perhaps something more meaningful.

Canada – Gearing Up For The Bank of Canada Decision

The Bank of Canada (BoC) had no shortage of new developments to digest this week. Labour market updates for the month of March highlighted the string of releases, though a pulse check on business and consumer sentiment as well as international trade data were also on watch. As the dust settles on the week’s data, markets have increased their bets that the BoC will pull the trigger in June. However, we think a July cut is more likely, which will allow the Bank a bit more time to compile evidence that inflation is moving durably back to 2%.

The Canadian economy lost a few jobs in March (-2.2k) against expectations for a trend-like gain. The details of the report were weak and consistent with a continued cooling in the labour market. The unemployment rate moved up sharply to 6.1% as employment struggles to keep pace with population-driven labour force growth (Chart 1). Meanwhile, hours worked fell slightly, suggesting economic activity for March moderated after a hot start to the year. However, wage growth remains a thorn in the BoC’s side, having been stuck above 5% y/y for the past year. More progress on this front is likely desired by the BoC, but there is clear evidence that current policy is doing its part in lowering the temperature on Canada’s job market.

However, on the growth side, February’s international trade data supported an acceleration in economic activity in the first quarter. Export and import volumes both surged after a weak prior month with current tracking suggesting trade will be another tailwind for Q1 growth. We do expect some give back in trade activity in March, especially in imports, as spending patterns weaken over the coming quarters.

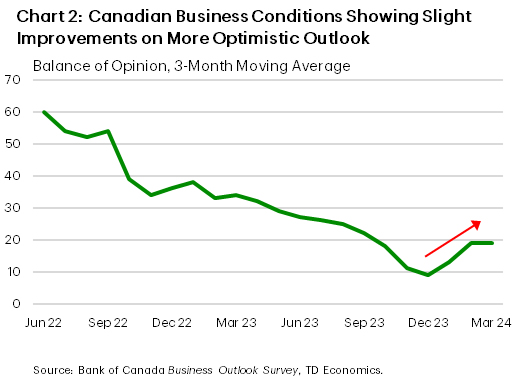

Meanwhile, business and consumer sentiment of the economy has improved slightly per the BoC’s Business Outlook Survey (BOS) and the parallel Canadian Survey of Consumer Expectations (CSCE). While demand remains under pressure due to high inflation and interest rates, expectations for lower interest rates provide more confidence about the future economic outlook (Chart 2).

The focus now shifts to the April 10th interest rate announcement where the BoC will release a fresh set of forecasts in their Monetary Policy Report (MPR). These updates may start to lay the foundation for interest rate cuts. Notably, since the last MPR released in January, inflation for Q1-2024 is coming in a touch lower than projected (3.1% vs 3.2% y/y), while growth should see a significant upgrade from the current flat-GDP projection. The BoC has held the policy rate at 5.00% for the last nine months, which has helped inflation on its path back to 2%. Indeed, headline inflation has now been in the high-end of the Bank’s 1–3 percent inflation target range for two consecutive months. However, we expect that the Bank will need to see a few more constructive inflation prints to ensure their mandate is being met.

Weekly Economic & Financial Commentary: Strong Jobs Numbers Diminish Urgency for Rate Cuts

Summary

United States: Strong Jobs Numbers Diminish Urgency for Rate Cuts

- Nonfarm payrolls expanded 303K in March, surpassing all estimates submitted to Bloomberg. The continued strength in hiring suggests less urgency for policymakers at the Federal Reserve to lower the target range of the fed funds rate. Recent comments from FOMC members have homed in on the jobs market's underlying momentum as justification to wait and allow for more inflation data.

- Next week: Small Business Optimism (Tue.), Consumer Price Index (Wed.)

International: Springtime Sentiment Data in Asian Economies Show Buds of Optimism

- This week saw the release of important economic sentiment data from both G10 and emerging economies. In Japan, the Bank of Japan's Q1 Tankan survey—a closely watched measure of business sentiment—showed signs that Japan’s economy may be able to gradually recover this year. In China, official March PMIs for the manufacturing and non-manufacturing sectors surprised to the upside, suggesting the economy started 2024 on a fairly solid note.

- Next week: Mexico CPI (Tue.), Bank of Canada Policy Rate (Wed.), European Central Bank Policy Rate (Thu.)

Credit Market Insights: Nothing But Net: Household Net Worth Climbed in the Fourth Quarter

- Household net worth climbed in the fourth quarter across all wealth cohorts. When indexed to 2000, household net worth is now at a fresh all-time high, sitting above its initial post-COVID peak from Q1-22. The biggest driver of the increase was a rise in corporate equities and mutual fund shares.

Topic of the Week: FY 2024 Budget Complete, but Fiscal Fights Still Loom

- On March 23, President Biden signed into law the last remaining appropriations bill for fiscal year 2024, completing a budget process that dragged on for nearly a year and included four short-term continuing resolutions to keep the government open and operating. That said, federal fiscal fights are anything but over.

BoC to Hold the Line on Interest Rates on Mixed Economic Data

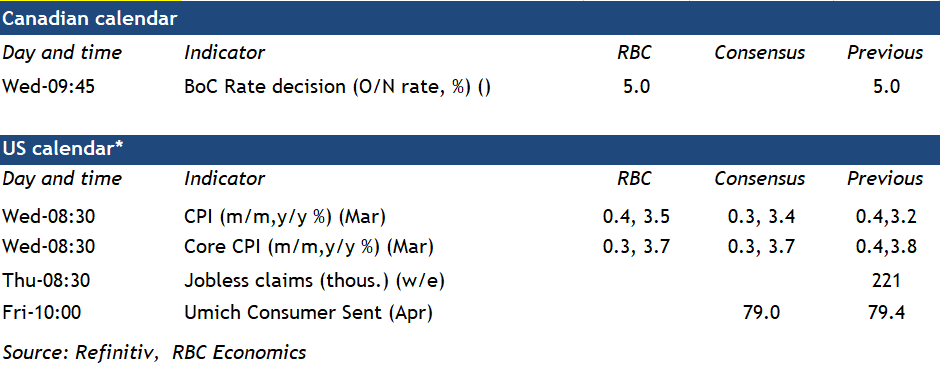

The Bank of Canada is widely expected to leave interest rates unchanged for a sixth consecutive policy decision on Wednesday. We expect the wording of the policy statement to leave options open for how long it plans to leave interest rates at current levels before pivoting to cuts.

Economic data since the last interest rate decision have been mixed. Gross domestic product growth in early 2024 is tracking substantially above the central bank’s forecast in January for a 0.5% Q1 increase. But that follows a string of softer readings by our count. GDP per person declined for six straight quarters to Q4 in 2023. Labour markets have continued to soften with the unemployment rate rising to 6.1% in March and job openings declining. Business bankruptcies have spiked higher, mounting debt service costs are cutting into household purchasing power, and wage growth has shown further signs of slowing.

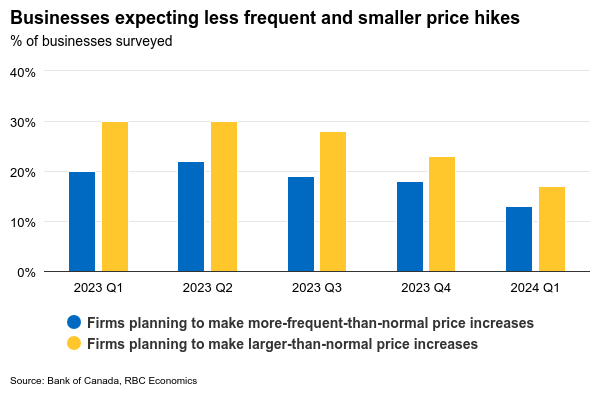

Most importantly for the BoC, inflation numbers have looked significantly better. Price growth year-over-year held below the top end of the 1% to 3% target range for a second straight month in February. The closely watched three-month rolling average of the central bank’s preferred core median and trim measures slowed to an annualized 2.2%. The Q1 Business Outlook Survey showed businesses expected inflation to continue to edge lower with further signs that business pricing strategies (planned frequency and magnitude of price changes) are normalizing. Resilience in early-2024 GDP data gives the BoC time to hold the line on interest rates for a little longer, but with most other economic data showing signs of softening, our base case assumption is that the BoC will be in a position to shift to cuts around mid-year.

Week ahead data watch

The U.S. Federal Reserve will be watching Wednesday’s March inflation print closely for signs that a resilient U.S. economy is reigniting inflation pressures following upside surprises in February and January. We expect a tick higher in year-over-year price growth to 3.5% (from 3.2% in February) but driven largely by an increase in gasoline prices. We expect core (excluding food and energy) price growth to edge down to 3.7% from 3.8% on a 0.3% month-over-month (seasonally adjusted) increase.