Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.06; (P) 151.41; (R1) 151.71; More...

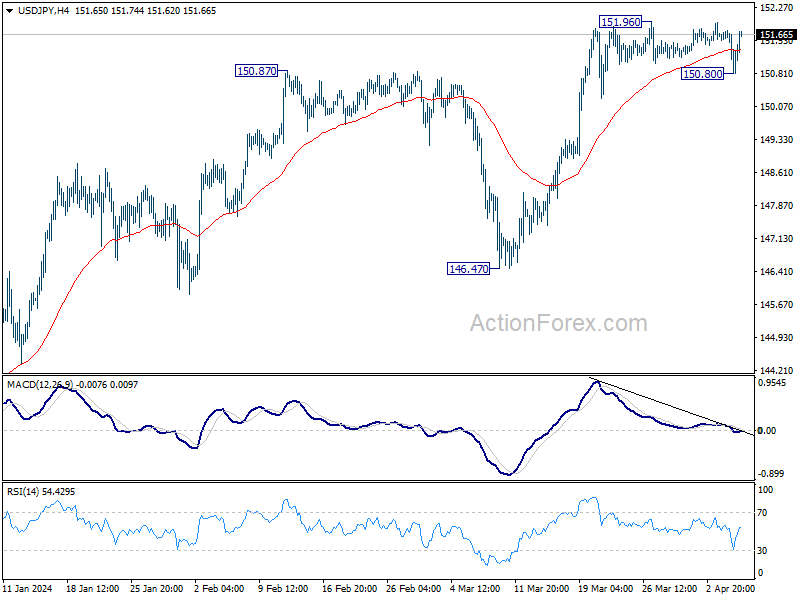

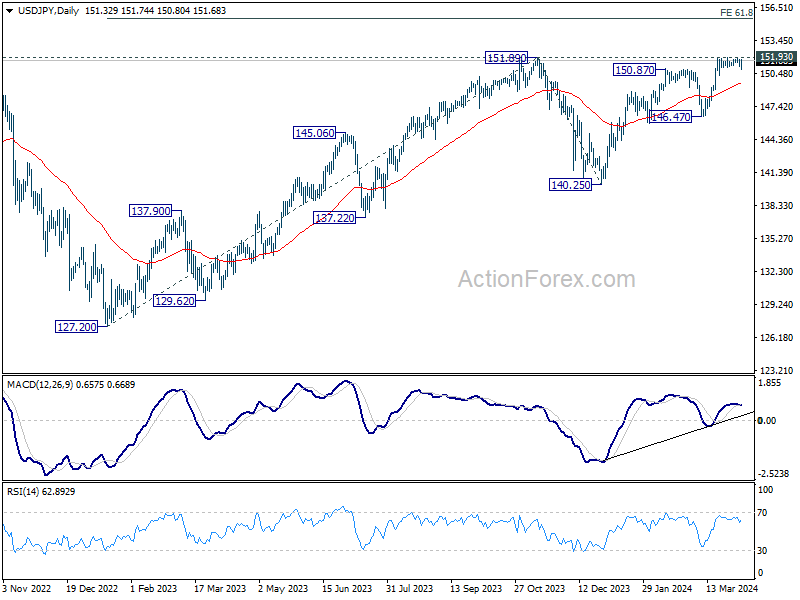

Intraday bias in USD/JPY is turned neutral as it recovered after dipping to 150.80. On the downside, break of 150.80 will resume the fall to 55 D EMA (now at 149.56). On the upside, however, sustained break of 151.93 key resistance will confirm long term up trend resumption.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

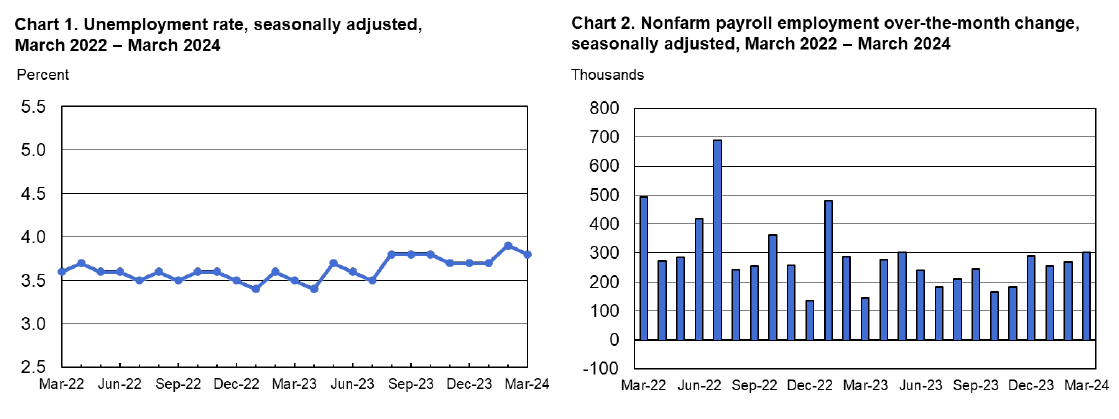

US: Payrolls Surprise to the Upside (Again), Unemployment Rate Ticks Down to 3.8%

Non-farm employment rose by 303k in March, considerably above the consensus forecast of 213k. Job gains in the two prior months were also revised higher by a combined 22k.

Private payrolls rose 232k, with the bulk of service sector gains (212k) concentrated in health care & social assistance (81.3k) and leisure & hospitality (49k). Hiring across the construction sector (+39k) rose by the fastest pace in nearly two-years. Government hiring remained robust in March, adding 71k jobs.

In the household survey, both the labor force (+469k) and civilian employment (+498k) recorded strong gains, with the latter more than offsetting February's pullback. The unemployment ticked down 0.1 percentage points to 3.8%, while the labor force participation rate rose 0.2 percentage points to 62.7%

Average hourly earnings (AHE) were up 0.3% month-on-month (m/m) – an acceleration from February's soft 0.1% m/m gain. On a twelve-month basis, AHE rose 4.1% – the slowest pace of wage growth since June 2021.

Key Implications

Another solid employment report, with payroll gains coming in well above consensus and revisions showing a bit stronger pace of job creation in months prior. Through the first quarter, the U.S. economy added an impressive 829k new jobs – nearly a 200k more than in the fourth quarter of last year. With job openings still elevated and stronger immigration flows helping to alleviate some of the constraints on labor supply, job growth has the potential to run in the 150k-200k range through the remainder of the year.

We heard from several voting FOMC members this week and the messaging was consistent: policymakers are in no rush to cut rates. With the labor market still strong and the economy humming, the FOMC can afford to be patient and wait for clearer signs that inflation is on a sustainable path back to 2% before dialing back the policy rate. Post-payrolls release, market pricing for a June cut has narrowed and bets are now more evenly split between June and July. Any upward surprise in next week's CPI release could fully push market expectations of the first rate cut to July, which would align to our forecast.

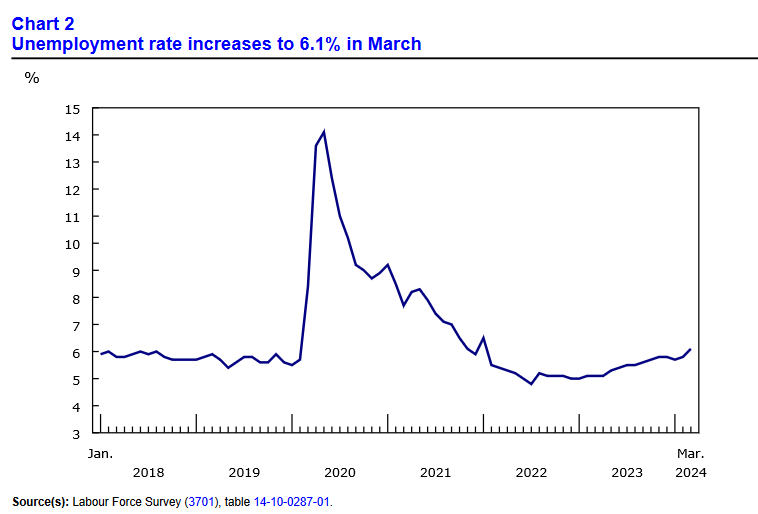

Canada’s Labour Market Sheds Jobs, Unemployment Rate Jumps

The Canadian labour market shed 2.2k positions in March, with full-time employment down -0.7k and part-time employment down -1.6k.

The unemployment rate rose 0.3 percentage points to 6.1%, the highest level in more than two years, and the participation rate was unchanged at 65.3%.

Employment by sector showed losses in accommodation and food services (-27k), wholesale and retail trade (-23k) and professional, scientific and technical services (-20k). A positive offset was seen in health care and social assistance (+40k).

Lastly, total hours worked fell 0.3% month-on-month, while wages were up 5.1% year-on-year (from 5.0% in February).

Key Implications

The Canadian labour market lost steam in March, with the unemployment rate rising significantly. This continues the trend over the last year, where Canadian firms have been unable to absorb strong population-driven labour force growth. While this has brought the labour market into balance, it also means that more Canadian workers are unemployed (280k more since the beginning of 2023). To make matters worse, hours worked fell for the first time in four months. This throws some cold water on expectations that the recent string of hot economic data prints to start 2024 will be sustained.

Today's report casts a cloud over the Canadian economy, but it is unlikely to change the Bank of Canada's (BoC's) thinking when it meets next week. As mentioned above, recent data outside of this weak employment report has been quite strong. This validated the Bank's decision to remain patient with the start of rate cuts. While it has afforded the central bank some extra time to wait to ensure inflation remains on its downward trajectory 2%, markets are increasingly betting that the BoC will pull the trigger on its first rate cut in June.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3495; (P) 1.3527; (R1) 1.3576; More...

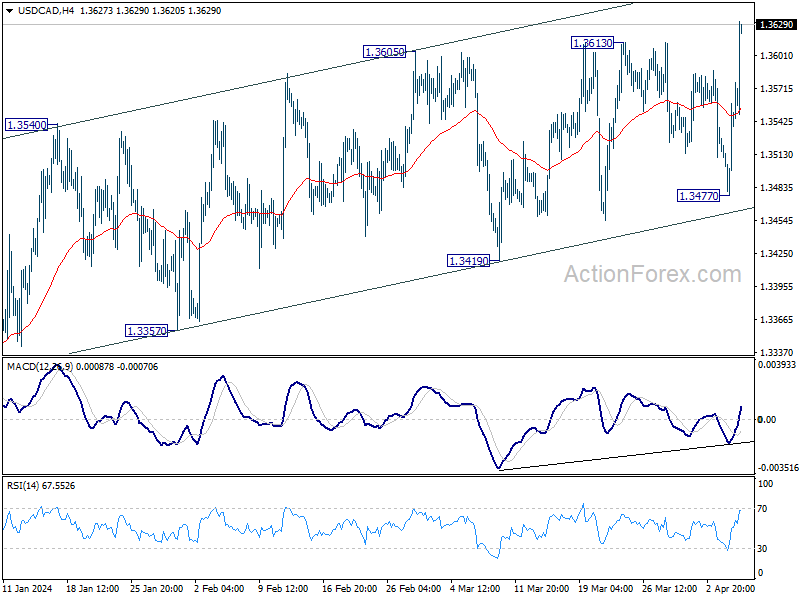

USD/CAD's rally from 1.3716 resumed by breaking through 1.3613 resistance and intraday bias is back on the upside. Current rise should target channel resistance at 1.3664 first. Sustained break there would prompt upside acceleration towards 1.3897 resistance next. For now, near term outlook will stay bullish as long as 1.3477 support holds, in case of retreat.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

NFP Fuels Dollar Surge, Canadian Jobs Drag Loonie

Dollar rises broadly in early US session in response to surprisingly strong non-farm payroll data. Dollar's ascent is notably pronounced the Canadian Dollar, which simultaneously grapples with its own disappointing employment figures. But against others, the overall strength of the greenback remains somewhat contained for now. The picture could shift dramatically as the NFP report catalyzes a significant surge in US treasury yields and exerts downward pressure on stock futures. Should the turmoil in stocks and bonds persist, Dollar may well gather substantial momentum later in the session.

As for the week at this point, Australian Dollar remains the standout performer, followed by New Zealand Dollar. Dollar's ascent post-NFP has positioned it as the third strongest currency for the now. Conversely, Canadian Dollar finds itself at the bottom of the performance ladder, with the Swiss Franc not far ahead. Euro and British Pound re mixed, positioned in the middle alongside Japanese Yen. But there is room for the picture to change drastically before weekly close.

In Europe, at the time of writing, FTSE is down -1.00%. DAX is down -1.57%. CAC is down -1.51%. UK 10-year yield is up 0.050 at 4.078. Germany 10-year yield is up 0.0321 at 2.399. Earlier in Asia, Nikkei fell -1.96%. Hong Kong HSI fell -0.01%. China was on holiday. Singapore Strait Times fell -0.52%. Japan 10-year JGB yield fell -0.0066 to 0.771.

US NFP grows 303k in Mar, unemployment rate ticks down to 3.8%

US non-farm payroll employment grew 303k in March, well above expectation of 205k. That's also much higher than the average monthly gains of 231k over the prior 12 months.

Unemployment rate ticked down from 3.9% to 3.8%, below expectation of 3.9%. Participation rate rose from 62.5% to 62.7%.

Average hourly earnings rose 0.3% mom, matched expectations. Over the past 12 months, average hourly earnings have increased by 4.1 yoy.

Canada's employment falls -2.2k, unemployment rate jumps to 6.1%

Canada's employment decreased -2.2k in March, much worse than expectation of 34.5k increase. Unemployment rate jumped from 5.8% to 6.1%, above expectation of 5.9%. Labor force participation rate was unchanged at 65.3%. Average hourly wages rose 5.1% yoy, up from prior month's 5.0% yoy.

Eurozone retail sales falls -0.5% mom in Feb, EU down -0.4% mom

Eurozone retail sales volume fell -0.5% mom in February, worse than expectation of -0.3% mom. Volume of retail trade decreased for food, drinks, tobacco by -0.4% mom, non-food products (except automotive fuel) by -0.2% mom, automotive fuel in specialised stores by -1.4% mom.

EU retail sales fell volume -0.4% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were recorded in Germany (-1.9%), Belgium (-1.8%) and Cyprus (-1.1%). The highest increases were observed in Poland (+1.4%), Croatia (+1.2%) and Estonia (+1.0%).

BoJ's Ueda: Excessive Yen weakness could prompt monetary policy response

In an interview with The Asahi Shimbun newspaper, BoJ Governor Kazuo Ueda highlighted extended Yen weakness could prompt further rate hikes by the central bank.

"If exchange rate trends have an effect on the cycle between wages and prices that cannot be ignored, that would become a reason for responding to the situation through monetary policy," he explained.

Ueda also outlined other conditions under which BoJ might consider additional rate hikes, after the landmark shift in March which exited negative interest rates.

The decision to end negative interest rates was made with a certain level of confidence, quantified by Ueda as "75 percent." He indicated that an increase in this confidence level to "80 percent or 85 percent" could prompt further adjustments

Governor also touched on factors likely to boost personal consumption, including the government's planned income tax cut in June, expected wage increases, and a slowdown in consumer price inflation. These developments, if they materialize as anticipated, could pave the way for a higher interest rate as early as between summer to autumn.

Moreover, Ueda acknowledged the impact of a "excessively weak yen" on Japan's economy and consumer prices, suggesting that significant currency weakness could influence future decisions regarding interest rate hikes.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3495; (P) 1.3527; (R1) 1.3576; More...

USD/CAD's rally from 1.3716 resumed by breaking through 1.3613 resistance and intraday bias is back on the upside. Current rise should target channel resistance at 1.3664 first. Sustained break there would prompt upside acceleration towards 1.3897 resistance next. For now, near term outlook will stay bullish as long as 1.3477 support holds, in case of retreat.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y Feb | -0.50% | -2.80% | -6.30% | |

| 00:30 | AUD | Trade Balance (AUD) Mar | 7.28B | 10.50B | 11.03B | 10.06B |

| 05:00 | JPY | Leading Economic Index Feb P | 111.8 | 111.6 | 109.9 | 109.5 |

| 06:00 | EUR | Germany Factory Orders M/M Feb | 0.20% | 0.60% | -11.30% | -11.40% |

| 06:00 | EUR | Germany Import Price Index M/M Feb | -0.20% | -0.10% | 0.00% | |

| 06:45 | EUR | France Industrial Output M/M Feb | 0.20% | 0.50% | -1.10% | -0.90% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | 715B | 678B | ||

| 08:30 | GBP | Construction PMI Mar | 50.2 | 49.8 | 49.7 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | -0.50% | -0.30% | 0.10% | 0.00% |

| 12:30 | USD | Nonfarm Payrolls Mar | 303K | 205K | 275K | 270K |

| 12:30 | USD | Unemployment Rate Mar | 3.80% | 3.90% | 3.90% | |

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.30% | 0.30% | 0.10% | 0.20% |

| 12:30 | CAD | Net Change in Employment Mar | -2.2K | 34.5K | 40.7K | |

| 12:30 | CAD | Unemployment Rate Mar | 6.10% | 5.90% | 5.80% | |

| 14:00 | CAD | Ivey PMI Mar | 54.2 | 53.9 |

Canada’s employment falls -2.2k, unemployment rate jumps to 6.1%

Canada's employment decreased -2.2k in March, much worse than expectation of 34.5k increase. Unemployment rate jumped from 5.8% to 6.1%, above expectation of 5.9%. Labor force participation rate was unchanged at 65.3%. Average hourly wages rose 5.1% yoy, up from prior month's 5.0% yoy.

US NFP grows 303k in Mar, unemployment rate ticks down to 3.8%

US non-farm payroll employment grew 303k in March, well above expectation of 205k. That's also much higher than the average monthly gains of 231k over the prior 12 months.

Unemployment rate ticked down from 3.9% to 3.8%, below expectation of 3.9%. Participation rate rose from 62.5% to 62.7%.

Average hourly earnings rose 0.3% mom, matched expectations. Over the past 12 months, average hourly earnings have increased by 4.1 yoy.

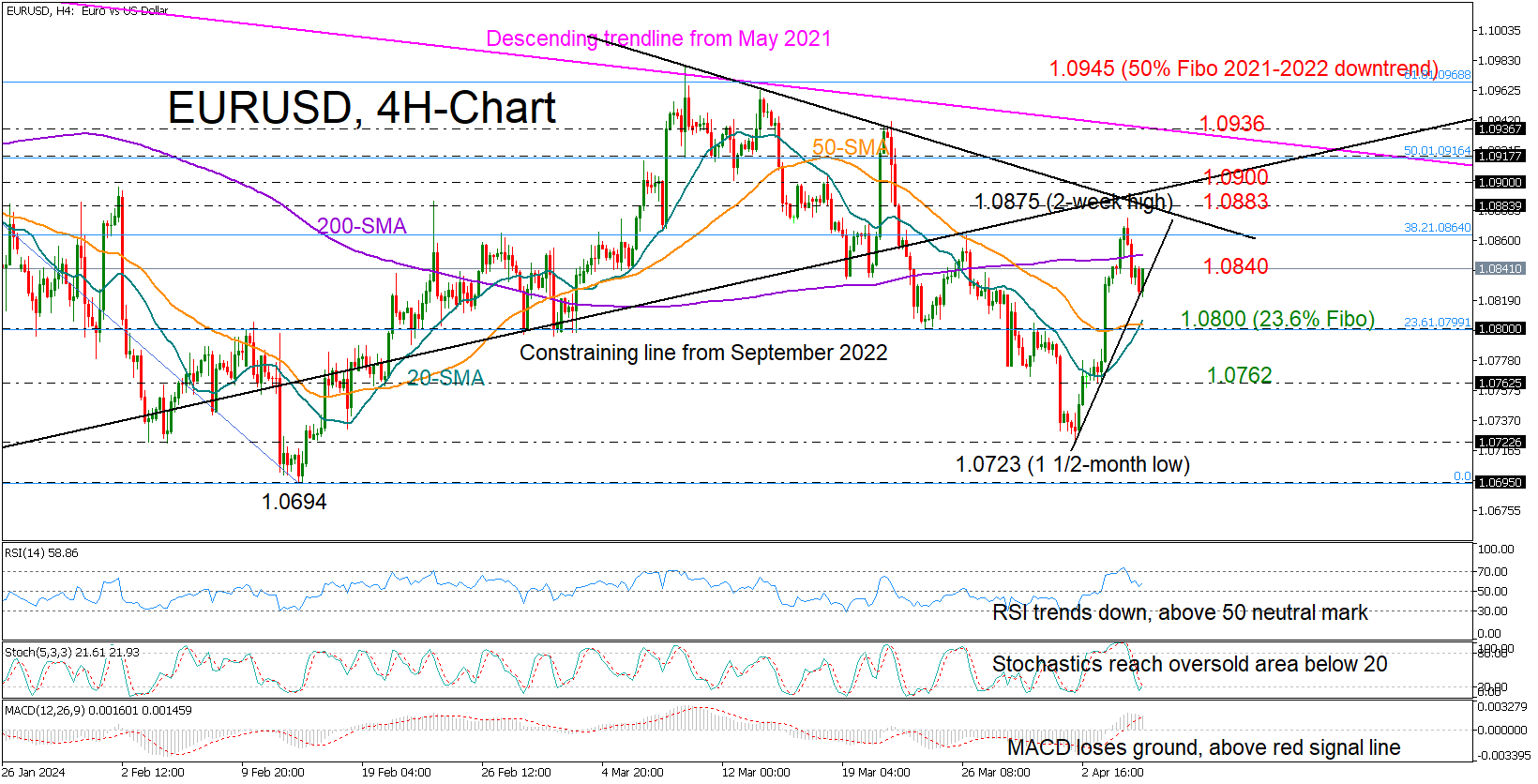

EURUSD Trims Earlier Gains as Clock Ticks Down to NFP

- EURUSD pulls back from two-week high

- Technical bias is not bearish yet

EURUSD gave up some ground on Thursday after a sharp rally from a one-and-a-half-month low of 1.0723 to a two-week high of 1.0875.

The US nonfarm payrolls report is on the agenda today and investors will look at whether jobs growth slowed down to 212k and wage growth eased to 4.1% y/y as forecasts suggest. The pair might receive some assistance if there are indications of a weakening US labor market, and the near-term technical outlook cannot exclude a shift to a recovery phase.

Both the RSI and the MACD are sloping to the downside, but the former is still above its 50 neutral mark and the latter has yet to cross below its red signal line. Moreover, the stochastic oscillator has already reached its 20 oversold level, suggesting that the bearish action in the price might halt soon.

Adding to the encouraging signals is the progressing bullish cross between the 20- and 50-period simple moving averages (SMAs). The completion could maintain investors’ confidence in the recent positive turnaround.

The support trendline drawn from the lows of this week is currently buffering downside forces around 1.0825, but traders are hoping for a close above the 1.0840 level, where the 20-SMA is placed in the daily chart, to refocus on the descending trendline from March at 1.0884. Breaking above the latter could result in an immediate pause near the psychological level of 1.0900. If not, the recovery could speed up to 1.0935, where the long-term resistance line from May 2021 is positioned.

Should the price drop below 1.0825, the 20- and 50-period SMAs may offer assistance around 1.0800. A continuation lower could initially pause around 1.0780 and then near 1.0760, while a deeper move could set the stage for another battle near the 1.0723 low.

Briefly, EURUSD has started a new negative cycle, but the short-term bias hasn't shifted to the bearish side yet. Nevertheless, a close above 1.0840 will be needed to restore buying interest.

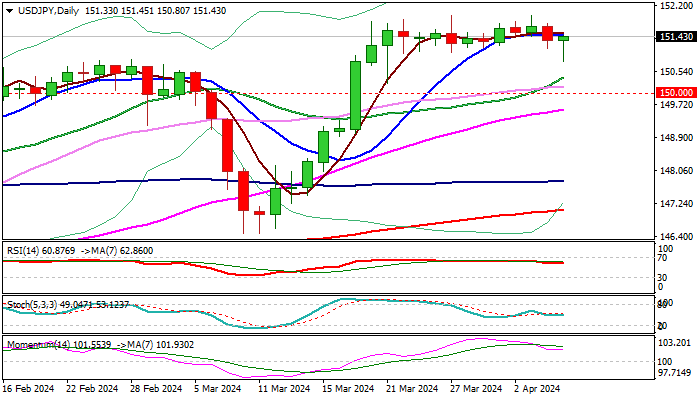

USD/JPY: Trades Within Extended Narrow Range Ahead of Key US Labor Data

USDJPY remains within a two-week range and consolidating just under multi-year peaks at 151.90/152.00 zone (tops of Oct 2022 / Nov 2023 / March 2024).

Extended sideways mode (the pair is on track to end the second consecutive week in a tight Doji candle) reflects strong indecision, as the dollar remains supported by a wide gap between Fed and BoJ interest rates, while fears of Japan’s intervention to support weak yen, continue to cap the action.

Technical studies remain bullish on all larger timeframes and strong bullish bias expected while the price stays above broken 150 level, reverted to solid support, however, fundamentals are likely to be pair’s key driver this time.

Markets await release of US March labor data for fresh signals, with US NFP forecasted to increase by 200K in March, compared to 275K increase previous month, with stronger than expected March numbers to be dollar supportive and vice versa.

Initial support lays at 150.40 (20DMA), guarding pivots at 150.00/149.87 (psychological / Fibo 38.2% of 146.48/151.97 upleg), loss of which would shift near-term focus to the downside and expose next strong support at 149.20 (top of thick daily cloud / Fibo 61.8%).

Key barriers lay at 152.00 zone and sustained break here to spark stronger bullish acceleration, though looming intervention is likely to remain a strong obstacle for bulls.

Res: 151.52; 151.97; 152.56; 153.00.

Sup: 150.67; 150.40; 150.00; 149.87.

Japanese Yen Jumpy Ahead of US Payrolls

The Japanese yen showed a bit of strength earlier but has pared these gains. In the European session, USD/JPY is trading at 15141, up 0.04%

All eyes on US nonfarm payrolls

The markets are bracing for a sharp drop in US nonfarm payrolls for March. Job growth hit 353,000 in January but then fell to 275,000 in February and the market estimate for March stands at 200,000. The labour market has stood up well in the face of elevated interest rates but another decline in the March data would indicate a clear downtrend in job growth, which would support the Federal Reserve deciding to lower interest rates sooner rather than later.

When can we expect the Fed to take the plunge and start lowering interest rates? That is a tough one to answer, especially because not all Fed members are on the same page, as evidenced by comments this week. Fed Chair Jerome Powell said that although inflation has been bumpy, he expected the Fed to lower rates “at some point this year”. Cleveland Fed President Loretta Mester echoed this position, saying that the Fed was becoming more confident that it could lower rates in the next few months.

Minneapolis Fed President Neel Kashkari sounded more hawkish, as he questioned if rate cuts were needed this year “if we continue to see inflation moving sideways”. Kashkari does not have a vote on monetary policy but his comments indicate that a rate cut is not a given and will depend on the data, in particular inflation.

In Japan, household spending rebounded in February with a gain of 1.4% y/y, compared to -2.1% in January. This beat the market estimate of 0.5%. On an annualized basis, household spending dropped 0.5%, following a 6.3% decline in January and beating the market estimate of -3%. The 0.5% decline marks a 12th straight drop in household spending but the rebound leaves room for optimism.

USD/JPY Technical

- USD/JPY is testing resistance at 151.41. Above, there is resistance at 151.71

There is support at 151.06 and 150.76