Sample Category Title

AUD/USD and NZD/USD Start Fresh Rally

AUD/USD is gaining pace and recently cleared 0.6600. NZD/USD is also rising and could extend its increase above the 0.6200 resistance zone.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar is moving higher from the 0.6480 zone against the US Dollar.

- A connecting bullish trend line is forming with support at 0.6615 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is gaining pace above the 0.6155 support.

- A key bullish trend line is forming with support at 0.6170 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair formed a base above 0.6480, as discussed in the previous analysis. The Aussie Dollar gained strong bids and started a decent increase above the 0.6540 resistance against the US Dollar.

The bulls pushed the pair above the 0.6580 resistance zone. There was a close above the 0.6600 resistance and the 50-hour simple moving average. Finally, the pair tested the 0.6635 zone. A high is formed at 0.6633 and the pair is now consolidating above 23.6% Fib retracement level of the upward move from the 0.6477 swing low to the 0.6633 high.

On the upside, the AUD/USD chart indicates that the pair is now facing resistance near 0.6635. The first major resistance might be 0.6650. An upside break above the 0.6650 resistance might send the pair further higher.

The next major resistance is near the 0.6720 level. Any more gains could clear the path for a move toward the 0.6800 resistance zone.

If not, the pair might correct lower. Immediate support is near a connecting bullish trend line at 0.6615. The next support could be 0.6595. If there is a downside break below the 0.6595 support, the pair could extend its decline toward the 0.6580 zone.

Any more losses might signal a move toward the 61.8% Fib retracement level of the upward move from the 0.6477 swing low to the 0.6633 high at 0.6540.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair followed AUD/USD. The New Zealand Dollar formed a base above the 0.6070 level and started a decent increase against the US Dollar.

The pair climbed above the 0.6125 resistance and the 50-hour simple moving average. The pair even spiked above 0.6180. A high is formed near 0.6183 and the pair is now consolidating gains.

On the upside, the pair is facing resistance near the 0.6185 zone. The NZD/USD chart suggests that the RSI is stable above 50. The next major resistance is near the 0.6200 level. A clear move above 0.6200 might even push the pair toward the 0.6250 level.

Any more gains might clear the path for a move toward the 0.6320 resistance zone in the coming days. On the downside, there is a support forming near 0.6170. There is also a bullish trend line forming with support at 0.6170.

The next major support is 0.6155 or the 23.6% Fib retracement level of the upward move from the 0.6068 swing low to the 0.6183 high. If there is a downside break below the 0.6155 support, the pair might slide towards 0.6125.

The 50% Fib retracement level of the upward move from the 0.6068 swing low to the 0.6183 high is also at 0.6125. Any more losses could lead NZD/USD in a bearish zone to 0.6070.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Focus Turns to the US and Nonfarm Payrolls

In focus today

In the US, we get the February jobs report today. We see downside risks to the non-farm payrolls and expect employment growth of +180k and see average wages to have risen 0.2% m/m seasonally adjusted. Whilst February data points received thus far have been mixed, we expect labour market conditions to gradually cool over the coming months.

In the euro area, focus turns to Q4 2023 wage growth, as the role of wages and their outlook have been dominating recent ECB communication. Data on compensation per employee will be released together with final national account data. Negotiated wages displayed a continued strong wage pressure in Q4, albeit at the same time showing the peak is behind us.

We also receive German industrial production data for January. Soft indicators such as the PMI and the Ifo index have continued to show troubles for the German industrial sector, although the worst period would appear to be behind us.

In China, we receive credit and money growth between 9 and 15 March. There is no fixed date or time for this data release. The recent trend in credit growth has been rather stable supported by government stimulus. It is however important to keep in mind that the numbers can be very volatile from month to month.

In Sweden we receive a triplet of data at 8.00 CET with the GDP figures, and production and consumption indicators for January. We expect them all to display positive m/m readings on the back of positive readings from hours worked and retail sales in January. We also get the Riksbank semi-annual business survey at 9.30 CET, and Riksbank governors Breman and Flodén are due to speak on economic outlook and monetary policy.

We wish you are happy Friday and good weekend!

Economic and market news

What happened overnight

In the US, President Biden gave his State of the Union speech in Congress. He used the speech to criticize his republican opponent in the November election, former President Donald Trump. As expected, President Biden also proposed a tax reform which included higher minimum taxes on all business, and people with wealth exceeding USD100m. The election takes place on 5 November.

What happened yesterday

The ECB held interest rates unchanged as was expected. At the press conference following the decision, President Lagarde was quite clear with guidance for a June rate cut, as she emphasised the need for more data ahead of the decision. Whilst April was not definitively ruled out, she said they will know a little more in April, and a lot more in June, hence highlighting the June meeting as key. We doubt that the incoming data ahead of the 11 April meeting will be sufficiently weak to change that view. It is therefore still our view that ECB will wait and deliver its first rate cut in June. The ECB also presented new staff projections which saw a downward revision of the 2024 projections across growth, headline and core inflation. Read more in our Flash: ECB Review - June cut is coming, 7 March.

In the Middle East, US president Biden announced he had directed US military to commence and build a temporary port in Gaza, so that it would be able to ramp up its delivery of humanitarian aid to the Palestinian people in Gaza. Meanwhile, Houthis' attack on a merchant ship in the Red Sea led to the first fatalities on a merchant vessel, as three people were killed.

In the commodity space, the IEA said it expects oil demand to grow by between 1.2 and 1.3 million barrels per day, down from around 2.3 million barrels per day last year. In its last projection OPEC+ had forecast growth at 2.25 million barrels per day this year.

Sweden officially became a NATO member state thus becoming the second new member to join the defensive alliance after Russia's invasion of Ukraine.

In Denmark, the pharmaceutical company Novo Nordisk delivered promising results in a Phase-1 trial of a new obesity drug. The subsequent market reaction meant the pharmaceutical giant overtook the electric vehicle maker Tesla in market value.

Equities: Global equities were higher yesterday with several indices setting new all-time highs. There was a lot of fuzz around the ECB meeting but at the end of the day with very little impact on equities. Instead, more classic late-cycle dynamics dominated with cyclical growth names outperforming and investor exuberance increasing. While still important, central banks should play a more secondary role for equities this year. The timing of rate cuts and the exact number of cuts does not matter so much if the soft-landing macro environment continues to unfold. In US yesterday, Dow +0.3%, S&P 500 +1.0%, Nasdaq +1.5% and Russell 2000 +0.8%. Asian markets are broadly higher this morning led by China while Japan is lagging as the currency keeps strengthening. US futures are mixed while European futures are broadly higher this morning.

FI: It was somewhat of a roller coaster ride yesterday in European rates around the ECB meeting. Initially market reacted with Bund yields lower by almost 10bp on the day. However, rates gradually drifted higher through the afternoon and 10y Bunds ended 3bp lower on the day. The move was a parallel shift in the 2y+ area. The strong initial market reaction was somewhat of a surprise since the ECB statement and the staff projections were broadly in line with expectations.

FX: The JPY, one of this week's outperformer within G10, maintains its gains, trading below 148 vs the USD and below 162 vs the EUR ahead of today's NFP. EUR/USD advanced further in the US session and starts the day at around 1.0950 as the USD is on the defensive across the board. GBP and the CAD are stronger vs the USD overnight, pushing Cable to fresh year highs at above 1.28. EUR/DKK rose yesterday above 7.4550. EUR/SEK and EUR/NOK are back to the lower end of the last week's 10-figure trading ranges, at 11.20 and 11.40, respectively. While both crosses are obviously susceptible to the NFP data, the former also eyes a batch of Swedish macro data at 08:00, the Riksbank's business survey at 09:30 alongside speeches by Anna Breman at 08:00 and Martin Flodén at 12:00.

US Payrolls Take Center Stage Today

Markets

The ECB left its policy rates and the APP run-down unchanged. In the quarterly forecasts, ECB staff downwardly revised 2024 growth and inflation. Growth this year is expected at 0.6% (vs 0.8% in December), but improvement is still expected in 2025 (1.5%) and 2026 (1.6%). Headline inflation is seen easing further (2.3% from 2.7% in 2024, 2% from 2.1% in 2025, 1.9% unchanged in 2026), with the 2024 decline mainly due to lower energy prices. Core inflation is expected to return to the 2% target at the end of the policy horizon (2.6% in 2024, 2.1% next year and 2% in 2026). Immediately after the release, EMU yields briefly dropped up to 8 bps. The euro fell from the 1.09 area to 1.087. However, those dips were easily reversed during the press conference as Lagarde repeated that the MPC needs more evidence on the disinflation process, especially on wages. Most of this information will only be available in June, making it the key reference in the ECB’s decision-making process. EMU yields reversed most of the decline. German yields ceded between 2.2 bps (2-y) and 1.2 bp (30-y). US Treasuries even outperformed Bunds. The text of Fed Chair’s Powell hearing before the Senate was unchanged from Wednesday before the House, but in the Q&A he indicated that the Fed is ‘not far from the confidence’ needed to start rate cuts. The comment is a bit strange (slip of the tongue?) as Fed governors recently almost unanimously held to the line that the MPC will take its time to assess whether inflation is sustainably returning to 2%. The US 2-y yield eased 5.2 bps while the 30-y yield gained marginally (+0.25 bps). The decline in US yields triggered renewed USD selling (EUR/USD close 1.0948, USD/JPY 148.05). US equities thrived (S&P +1.03%, new record close).

US Payrolls take center stage today. Job growth is expected to ease to 200k (from an astonishing 353k in January). The unemployment rate is expected unchanged at 3.7%, but wage growth (AHE) is seen moderating (0.2% M/M and 4.3% Y/Y). Evidence from the ISM’s suggests downside risks for the job growth figure. On the other hand, the bar for AHE (0.2% M/M) is not high. Considering the market reaction to the ISM’s and yesterday’s ‘no far from confidence’ headline from Powell, the market might still be more sensitive to a downside surprise rather than to a modestly stronger or in-line report. US MM markets might ponder whether there is still a chance for a May cut (which we don’t see as a real option). In this scenario, the dollar might face further headwinds. EUR/USD 1.0969 is 61% retracement on the end December/mid-February correction, with even the December top (1.1139) on the radar.

News & Views

Egypt’s shock therapy already yielded some results. The central bank on Wednesday jacked up rates by 600 bps while authorities allowed a more than 35% devaluation of the currency as it tries to both combat inflation and stem a huge FX crisis. Mere hours later, the IMF unlocked a long-awaited loan that has also been increased in size from $3bn to $8bn. Combined with the large $35bn investment deal struck with the UAE, it prompted rating agency Moody’s to lift Egypt’s outlook to positive from negative. This creates possibilities for the current Caa1-rating (obligations judged to be of poor standing and subject to very high credit risk) to be raised as well in the future. It “reflects significant official and bilateral support announced and marked policy steps taken in the past week that will, if maintained, support macroeconomic rebalancing,” Moody’s explained, adding that the UAE investment is expected to cover Egypt’s external financing gap until June 2026. Egyptian dollar bonds extended a recent sharp rally while the country’s pound on the first day after the devaluation strengthened marginally from USD/EGP 50.09 to 49.38.

Czech central bank board member Prochazka said they won’t rush with monetary easing so that they don’t “scare investors”. Prochazka is explicitly referring to the weak Czech koruna. The currency has been top of mind at the central bank since the depreciation trend kicked in in April last year. The fall accelerated after the CNB raised the easing pace to 50 bps in February. Prochazka said rate cuts have been and will remain gradual, suggesting no change at that tempo for the time being. The policy rate currently stands at 6.25%. This compares to a neutral rate which the central bank, according to Prochazka, sees at about 3.5-4%. With this in mind, Czech money markets expect monetary policy to shift from restrictive to supportive around Q4 of this year. EUR/CZK meanwhile found a short-term equilibrium around recent highs of 25.36.

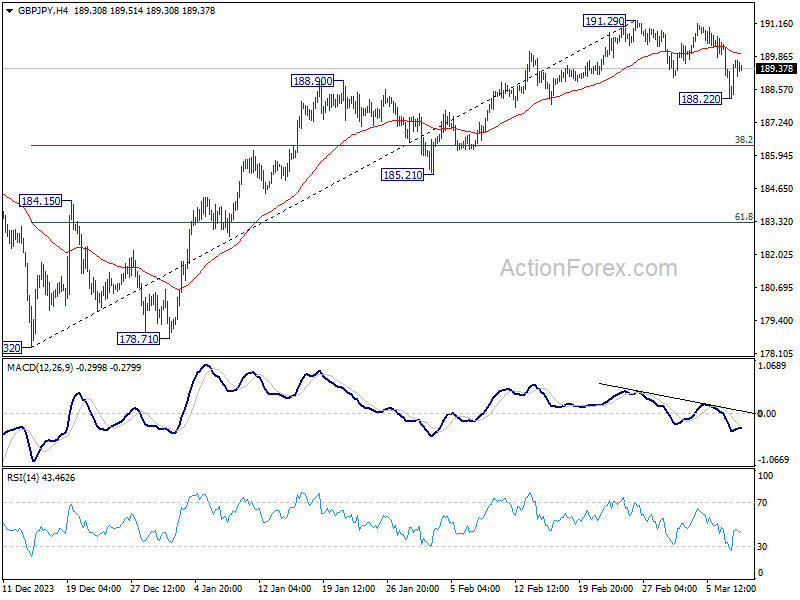

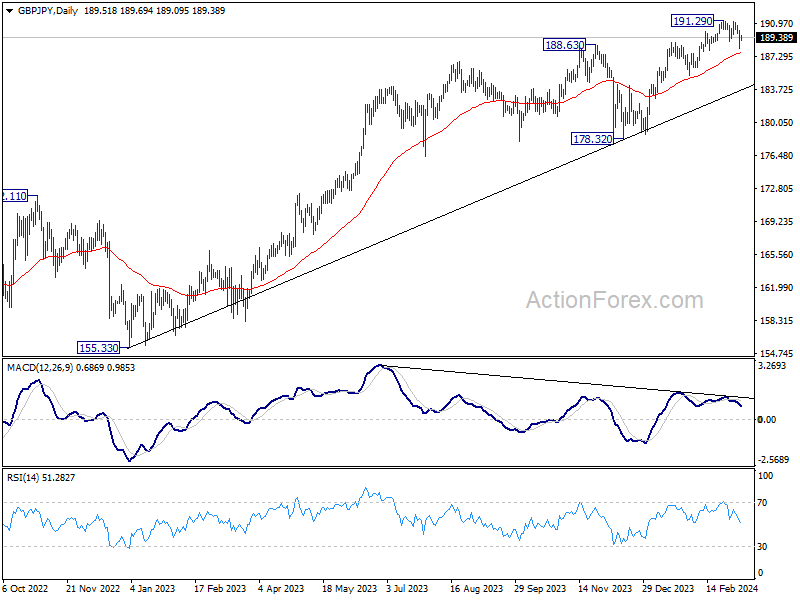

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.48; (P) 189.36; (R1) 190.49; More.....

GBP/JPY recovered after dipping to 188.22 and intraday bias is turned neutral first. On the downside, below 188.22 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger reversal and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.96) will retain near term bullishness and bring retest of 191.29 high.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

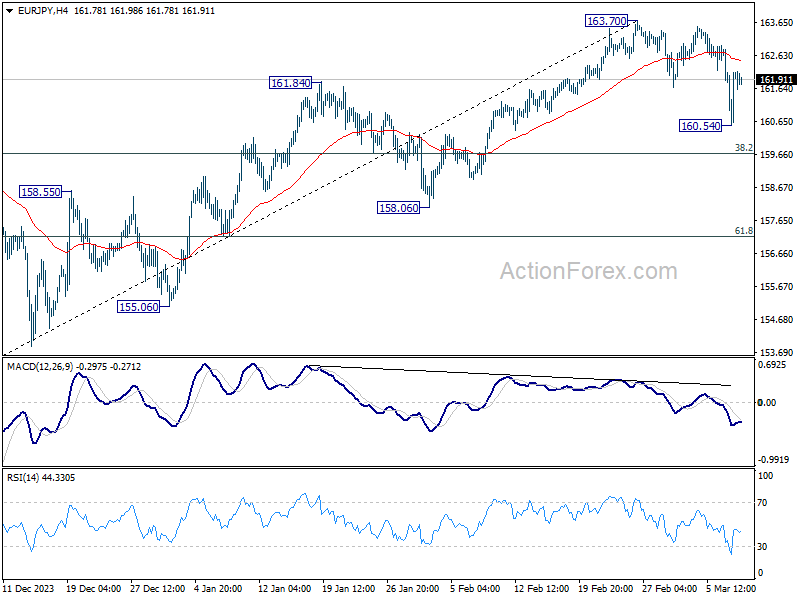

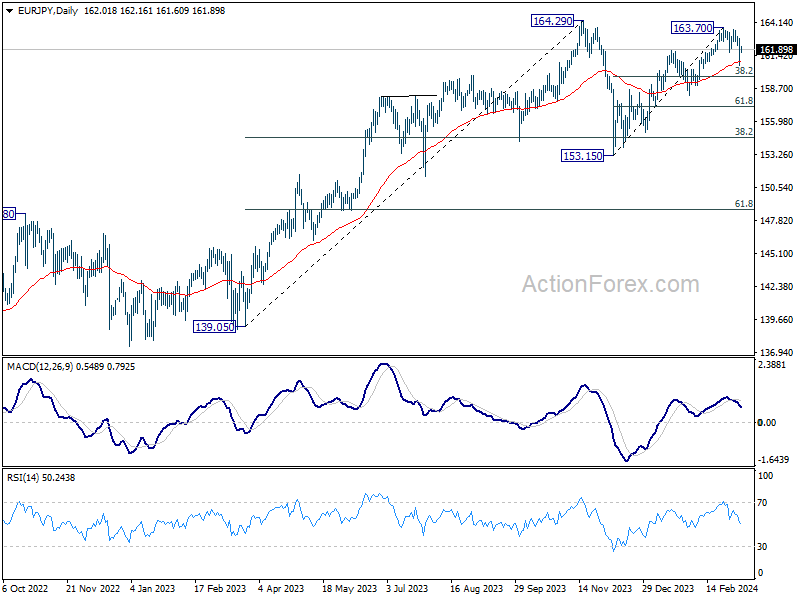

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.82; (P) 161.82; (R1) 163.07; More...

EUR/JPY recovered after dipping to 160.54 and intraday bias is turned neutral first. On the downside, below 160.54 will resume the fall from 163.70 to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, sustained break of 55 4H MACD (now at 162.46) will retain near term bullishness, and bring retest of 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

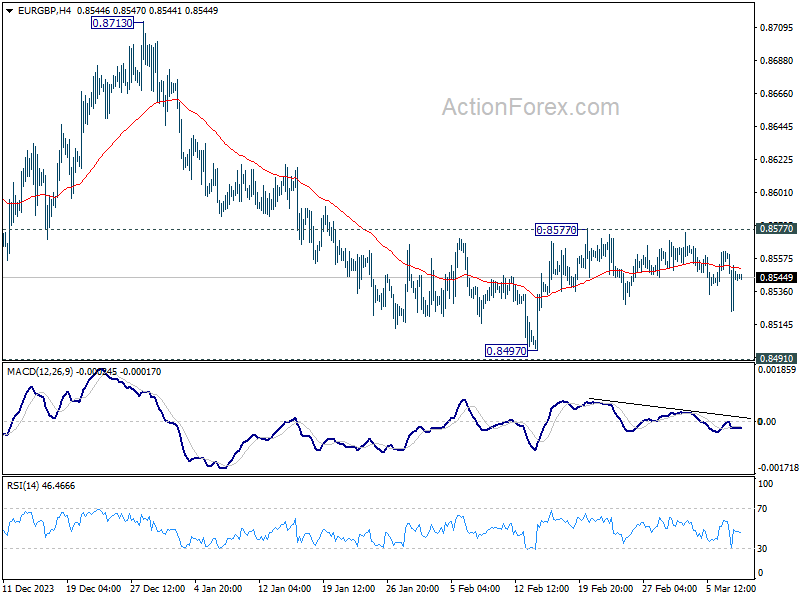

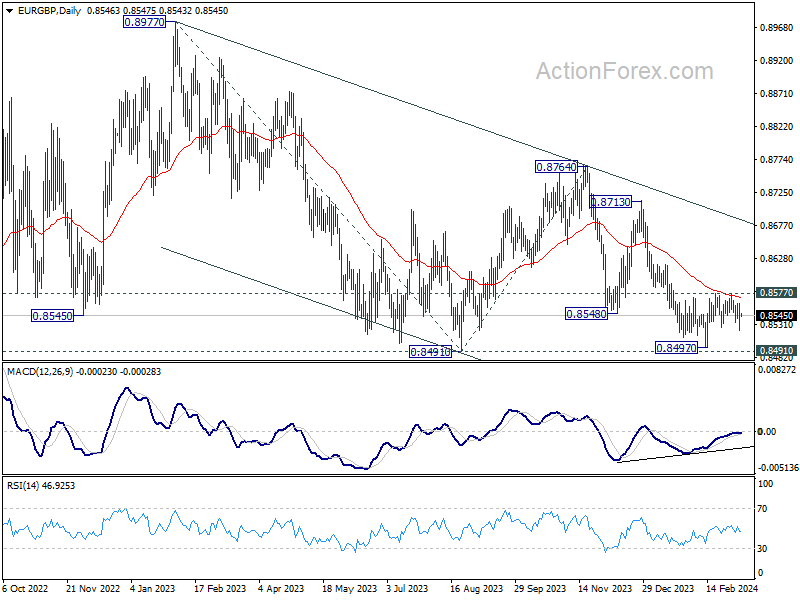

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8527; (P) 0.8545; (R1) 0.8567; More...

Range trading continues in EUR/GBP and intraday bias stays neutral. On the upside, decisive break of 0.8577 resistance and 55 D EMA (now at 0.8572) will argue that fall from 0.8764 has completed. Intraday bias will be back on the upside for rebound towards 0.8713 resistance. Nevertheless, firm break of 0.8491/7 support zone will confirm larger down trend resumption.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

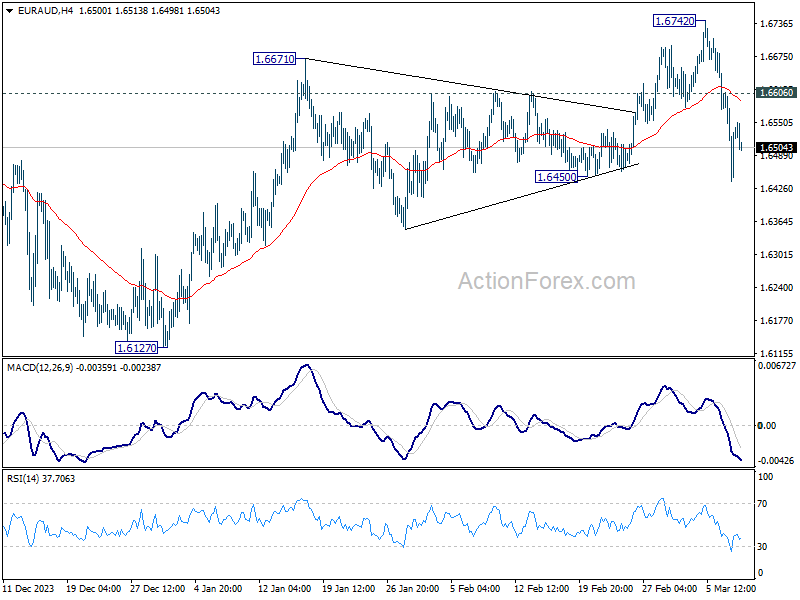

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6449; (P) 1.6530; (R1) 1.6619; More...

Intraday bias in EUR/AUD remains on the downside at this point. Decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742, and turn near term outlook bearish. On the upside, above 1.6606 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

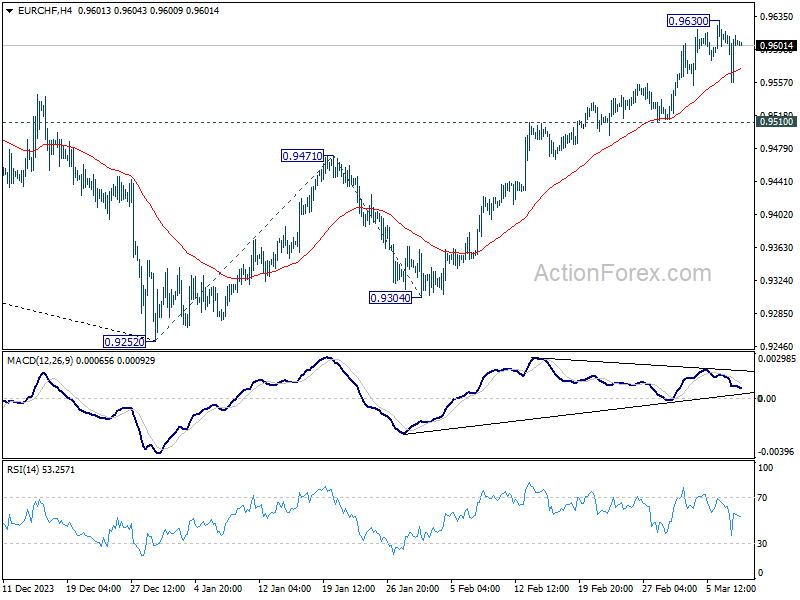

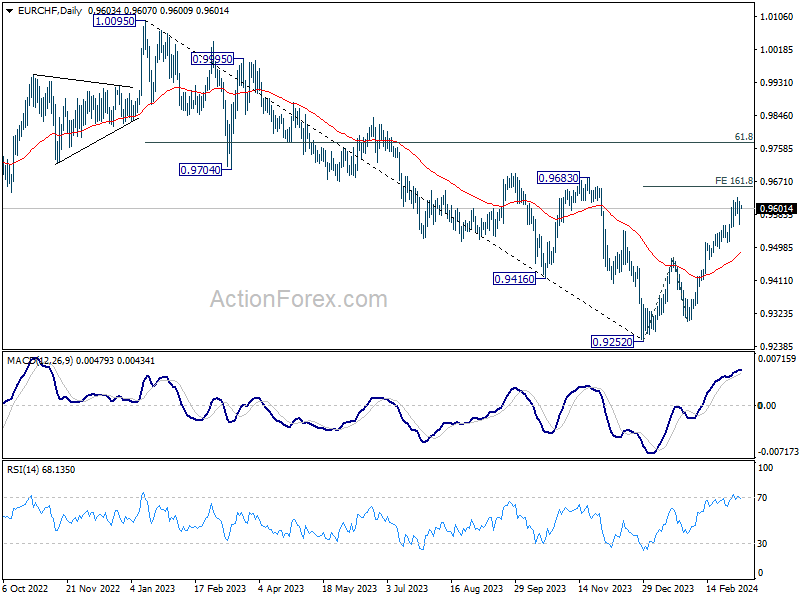

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9573; (P) 0.9596; (R1) 0.9634; More...

EUR/CHF is extending the consolidation from 0.9630 and intraday bias remains neutral. Further rally is expected as long as 0.9510 support holds. Above 0.9630 will resume the rebound from 0.9252 to 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9622) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

Jobs Friday

Yesterday’s European Central Bank (ECB) meeting and Lagarde’s press conference went according to the plan. The ECB left its rates unchanged for the fourth straight meeting, lowered its inflation forecasts, predicted that inflation will reach the 2% target by next year and suppressed its growth forecast for this year. Still, Lagarde said that they aren’t ‘sufficiently confident’ in inflation to lower rates but that they ‘will know a little bit more in April and that they will know a lot more in June’. It was heard as ‘we will start cutting the rates in June if inflation continues to ease as predicted’. The dovish message was well received from the market: the Eurozone bond yields fell, the Stoxx 600 hit a fresh record, but the EURUSD extended gains above the 1.0955 as the US dollar fell more than the euro did as the Federal Reserve (Fed) Chair Jerome Powell reiterated that rate reduction in the US ‘can and will begin’ this year.

Who will cut first?

Mr. Powell sounded more confidently dovish Madame Lagarde. While Lagarde said they are not confident enough to lower rates, the Fed head said that he and his colleagues are ‘waiting to become more confident that inflation is moving sustainably at 2%’, that ‘when they get that confidence, they will begin dial back the level of restriction’ and that they are ‘not far from it’!

You don’t need to repeat such a confident message twice. The US dollar index tumbled to the lowest levels since January, and the dollar bears now target the 100 mark on expectation that the Fed is done cooking the idea of a rate cut, they are just waiting for it to cool before bringing it on the table. The smell of that dovish cake sent the S&P500 to a fresh record, of course. Nvidia gained another 4.5% - really I am not kidding – the company added another 4.5% yesterday just like that, whereas Broadcom – which also jumped more than 4% yesterday – fell 3% in the afterhours trading after announcing disappointing sales last quarter. Happily, the company highlighted that their AI demand is growing and that’s all that matters.

A different game is played in Asia

Japanese stocks fell below 40’000 level as the USDJPY tumbled below the 148 level on rising speculation that the Bank of Japan (BoJ) could be closer to exiting the negative rates than many think. The most aggressive hawks bet that the BoJ will already hike rates at their March meeting. I think that they will – in the best case scenario – hint that there could be a hike in April. But you never know with the BoJ.

The growing divergence between more hawkish BoJ expectations and more dovish Fed expectations should back a USDJPY decline to at least 140. Then, depending on how hawkish the BoJ sounds, we shall see the USDJPY ease to 125/130 level. But be careful because the BoJ will unlikely to raise its rates at the same speed than the ECB or the Fed did. The chances are that the BoJ will move slowly. Hence, the road below the 140 could be choppy.

Beyond Japan, the rebound in Chinese stocks began losing steam this week, as the government’s 5% growth and 3% inflation target looked overstretched and yesterday’s jump in trade numbers were ignored, as investors realized that the boost was due to the fact that the January and February data is announced together to avoid the Chinese New Year fall in activity. The iShares MSCI China ETF saw the biggest one-day outflows on Wednesday since last December.

Jobs Friday

Due today, the US jobs numbers could further boost the dovish enthusiasm… or not. Note that the last two readings were abnormally strong with NFP reads above 300K mark. The latter interrupted the downtrend in US payrolls – a downtrend that was in play following the post-pandemic peak.

But on the other hand, other metrics – like lower job openings and lower quit rates – hint that there is a normalization and a certain loosening in the US jobs market. The quit rates for example fell below the pre-pandemic average hinting that the Great Resignation era is leaving its place to Great Stay and that means a possible downward pressure on wages growth.

The US economy is expected to have added around 200K jobs last month, and the monthly average pay may have increased at a slower speed. Unemployment rate is seen steady at 3.7%. If the data is sufficiently soft – or ideally softer than expected, the Fed doves will finish the week on a dominant note. But if we see another month of blowout jobs report, confusion will reign.

But in all cases, what matters the most is inflation. Even if the US jobs data comes in hot, if next week’s US CPI read is soft enough, investors will continue to daydream about that first rate cut. Oh that first rate cut…

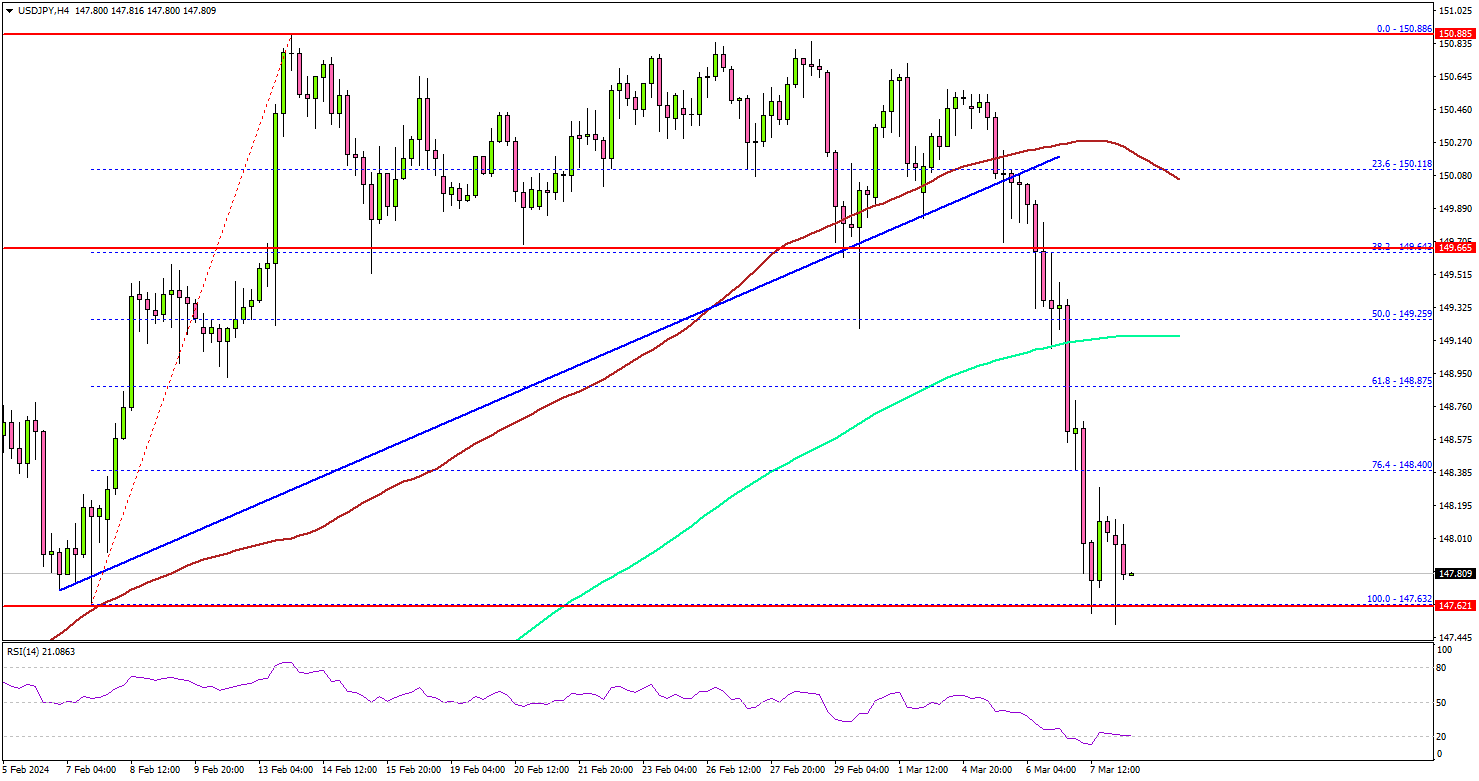

USD/JPY Nosedives After Rejection, Gold Extends Rally

Key Highlights

- USD/JPY started a major decline from the 150.80 resistance zone.

- It traded below a key bullish trend line with support at 150.00 on the 4-hour chart.

- Gold prices surged above the $2,120 resistance zone.

- The nonfarm payrolls could change by 200K, down from 353K.

USD/JPY Technical Analysis

The US Dollar struggled to clear the 150.80 resistance zone against the Japanese Yen. USD/JPY started a major decline after it settled below 150.00.

Looking at the 4-hour chart, the pair settled below the 150.00 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). It also traded below a key bullish trend line with support at 150.00.

The bears took control and dumped the pair below the 148.80 support zone. There was a clear move below the 76.4% Fib retracement level of the upward move from the 147.63 swing low to the 150.88 high.

Immediate support is near the 147.60 level. The next major support is at 147.20. If there is a downside break below the 147.20 support, the pair could decline toward the 146.00 support.

If there is a recovery wave, the pair could face resistance near the 148.20 level. The first major resistance is now forming near the 148.80 level and the 200 simple moving average (green, 4-hour). The main resistance is near 149.20. A close above the 149.20 zone could open the doors for more upsides. The next stop for the bulls might be 150.00.

Looking at Gold, there was a strong increase above the $2,120 resistance and the bulls might aim for a move toward $2,180.

Economic Releases

- US nonfarm payrolls for Feb 2024 – Forecast 200K, versus 353K previous.

- US Unemployment Rate April 2024 - Forecast 3.7%, versus 3.7% previous.