Sample Category Title

Japan’s household spending falls -6.3% yoy in Jan, deepening contraction

Japan reported significant decline in household spending in January, marking the 11th consecutive month of contraction. The decrease of -6.3% yoy was well below expectation of -4.3% yoy, representing the steepest annual drop since February 2021. Furthermore, on a seasonally adjusted month-on-month basis, spending fell by -2.1%, starkly contrasting with the expected 0.4% increase.

The Ministry of Internal Affairs and Communications highlighted several one-off factors contributing to this pronounced decrease. Notably, reduction in new car purchases, attributed to factory suspensions, played a significant role. Additionally, lower energy bills, a result of unusually warm weather, further depressed spending levels.

Moreover, the Ministry pointed out that the comparison with the same month last year is skewed due to a temporary boost in spending from post-pandemic travel subsidies.

The Slow Lane in the Tunnel

This week’s national accounts confirmed our view that the domestic economic is soft, especially the consumer. Pressures on households should start to ease in the period ahead.

The big-picture themes from the national accounts for the December quarter were largely as expected. The Australian economy is soft, expanding just 0.2% in the quarter and 1½% over 2023 as a whole. Domestic demand in the December quarter was weaker still, especially in the private sector. Almost all the 0.1% increase in domestic demand in the quarter came from the public sector.

Much of 2023’s weakness stemmed from the household sector. Consumption has been weak and this remained the case in the December quarter. Discretionary spending continues to decline, with overseas holidays especially weak. Part of this might be the result of shifting seasonal patterns in spending and holidaying. Even so, households are objectively limiting their spending in the face of income pressures. Consumption per person has been falling in Australia, unlike in most peer economies. It is no wonder that consumer sentiment has been so depressed.

We have been highlighting these income pressures for some time. The triple squeeze of a rising cost of living, increasing tax take and higher interest rates has required households to respond.

It has been less recognised that the squeeze from rising taxation as a share of income has been greater than from rising net interest payments. (Indeed, the ABS revised down the interest flow series this week, relative to previous releases.) This does not mean monetary policy has done little to slow the economy or combat inflation – there are other channels of monetary policy transmission beyond the immediate effect on household cash flows. But it does put the role of fiscal policy, and particularly bracket creep, in perspective.

There is light at the end of the tunnel for households. As inflation has declined, the squeeze on real household incomes from this source has diminished. The drag from taxation and net interest payments has also eased a little. Some of the former might reflect timing effects for tax return lodgements. Meanwhile the November increase in the cash rate would have taken effect in people’s debt repayments too late to have boosted the quarterly total for net payments by much.

As a result, real household disposable income increased in the quarter. It was only barely above the level a year previously, though. Once the growth in population over the same period is accounted for, real household disposable income is still going backwards.

Inflation’s grip on households’ spending power will continue to ease over the course of 2024. That is the desired outcome. With tax cuts – and, we believe, some reductions in the cash rate – coming in the second half of the year, that triple squeeze will truly begin to unwind.

It would not be appropriate to interpret the coming turnaround in real incomes as an upside risk that threatens an upsurge in demand-driven inflation. Rather, it represents an extraordinary phase in the household sector’s experience coming to a close. Two years of declining real incomes in the face of a tight labour market is not a combination that should be regarded as normal. And there are some potential offsets to this turnaround, especially from the labour market, which is expected to slow with a lag given current slow growth in activity. There are also some increases in net interest payments yet to come through.

Businesses have also adjusted to the slow demand. Some of them have run down their inventories, while investment in new equipment declined in the quarter. Consistent with our forecasts, the resilience that was believed to have prevailed in the first half of 2023 has not carried through into the second half. Activity in non-residential construction has held up, and opportunities in energy transition, resources and elsewhere remain. But with ongoing cost pressures and soft demand, many businesses would understandably seek to delay or rationalise their spending on new equipment.

The RBA would be comfortable with these outcomes. They have been seeking to slow demand because they want to bring the level of demand back into balance with supply. The December quarter outcome certainly helps achieve that objective. It also supports our house view that the RBA will reach the point of being prepared to reduce some of the contractionary stance of policy late in the year, most likely starting from September.

The RBA would also have been heartened by the ongoing turnaround in labour productivity, which increased as they – and we – expected. The second consecutive quarterly increase in this series does not make a trend. But it does lend weight to our view that much of the earlier slump was an artefact of the population surge. Over time, the capital stock will catch up – as long as investment does not decline precipitously.

Where they might be less comfortable is on the housing front. The potential wealth effect of a renewed upsurge in housing prices is unlikely to be the main concern given any additional consumer demand needs to be set against the weak starting point.

Rather, the issue at present is the low rate of new production of housing in the context of high construction costs and ongoing (if more moderate) population growth. New housing construction is one of the most important channels of the transmission of monetary policy, here and overseas. The current low rate of dwelling investment is therefore an expected outcome of the RBA’s policy actions. To the extent that higher interest rates have dampened dwelling investment, however, they exacerbate Australia’s current housing affordability challenges in the medium term. These challenges also relate to some of the other headwinds affecting the industry, including the competing bid for resources from non-residential construction. The inflation–employment trade-off is therefore not the only short-term policy dilemma that policymakers must navigate.

Opposing Perspectives on China’s Path to Prosperity

China’s National People’s Congress for 2024 and the market response again highlighted how far apart the views of China’s authorities and global investors are on both the current health of the economy and the way to achieve long-term prosperity.

China’s 2024 National People’s Congress met expectations with respect to key policy actions, but disappointed in terms of sentiment – market participants clearly hopeful the new year would bring a more aggressive policy style. As was the case throughout 2023, the market and China’s authorities currently have very different perspectives on the economy’s immediate health and the long-term path to prosperity, with authorities confidence in the dividend from trade and investment ex-housing intact but the market of the belief that housing must again take a leading role in China’s growth story.

According to the 2024 government work report delivered at the NPC, GDP growth of “around 5%” is expected to again be achieved in 2024 after a 5.2% gain in 2023. Year-over-year, direct support from the central government is little changed, 2024’s deficit target of 3.0% the same as 2023.

October’s late revision of the 2023 deficit target to 3.8% will also support activity in 2024, as will an additional RMB1trn in sovereign special bonds – a stop-gap measure to sure-up infrastructure investment while local government funding through land sales is impaired. Still, there is no evidence of authorities believing their support for the economy must be dialled up.

Whereas the growth and fiscal targets are best considered hard targets, authorities 3.0% CPI projection is more a symbol of intent. What the target speaks to is a plan to bolster household employment and incomes through trade and investment and, in time, justify a sustained rebound in consumer perceptions of their family finances and wealth. In doing so, authorities will encourage the use of existing and new capacity and thereby create a supportive environment for profitability, wage growth and consequently domestic inflation.

For consumer views of family finances to fully heal however, further targeted support for housing construction is also necessary. While this began in 2023, 2024 must see a material expansion through additional funding and liquidity being made available for developers and local governments as well as clear direction from the Central Government that their reform process is complete.

A core focus of the housing reforms has been the re-shaping of the construction pipeline to focus on the development of housing for low and middle-income households to ‘live in’ as opposed to product for investors. With interest rates and deposit rates having been cut significantly, an end to uncertainty over developers’ finances should quickly see the investment pipeline refill and investment begin to grow on households’ terms not direct Government support.

The property sector’s healing is likely to take place over 2024 and 2025. In the meantime, there is cause to believe 2023’s consumption momentum can be sustained throughout 2024, with Lunar New Year anecdotes suggesting a growing number of Chinese consumers are increasing their discretionary spend. Highlighting the potential scale of pent-up demand for 2024 and beyond, retail sales have only increased 4% annually the past four years (2020-2023) having grown closer to 10% between 2015 and 2019.

In our view, the above consumer narratives are sustainable trends which can help support GDP growth “around 5%” in both 2024 and 2025. The other foundation is business investment, itself dependent on trade.

Throughout 2023, we detailed at length the strength anticipated then seen in high-tech manufacturing. For the year, fixed asset investment related to chemical products, automobiles and electrical machinery grew by 13%, 19% and 32% respectively. Utilities also grew 23%, and other infrastructure 6%. High-tech manufacturing is unlikely to grow as fast in 2024 and 2025; but now being of similar scale to housing, its contribution to growth will remain large. Importantly, as the new capacity investment is creating comes online, the trade position will benefit, drawing and accumulating income from exports while also reducing lost wealth and income through imports.

This recursive loop between investment and trade and the consequent scaling up of national income is the foundation for Chinese authorities long-run prosperity ambitions. If these gains can be recycled into new jobs and wealth across the economy, not only will they deflate the significance of the nation’s existing debt, but also offer capital to fund sustainable growth in consumption and housing. Income, not debt, is set to remain the focus of China’s authorities, with risks related to the latter expected to resolve themselves as growth persists, and property investment to follow growth elsewhere in the economy.

NFP: USD Hungers For Revitalization

The USD Index (DXY) dipped below the 103.00 support level for the first time since early February, indicating a significant decline in the US dollar. The focus on March 8 will be on the release of Non-farm Payrolls, the Unemployment Rate, and a speech by the Fed’s J. Williams. EURUSD reached new multi-week highs near 1.0950 after the ECB decided to maintain monetary conditions unchanged. GBPUSD surged to fresh 2024 highs above 1.2800, driven by increased selling pressure on the US dollar. USDJPY fell to new five-week lows below the 148.00 support level, influenced by lower US yields and speculation about the BoJ’s potential actions.

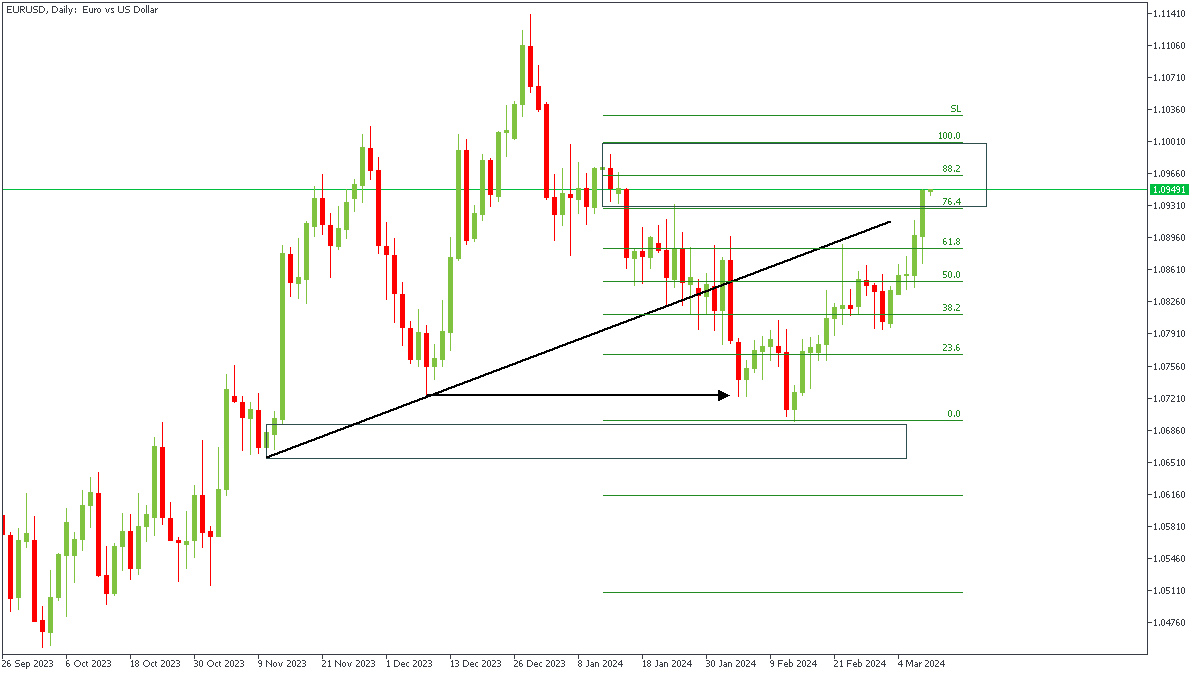

EURUSD - D1 Timeframe

Following the violation of the previous low as indicated by the horizontal arrow, we’ve seen price action on the Daily timeframe of EURUSD climb back up rather quickly to retest the recent supply zone that brought about the break of structure. There is also a resistance trendline, as well as the Fibonacci retracement levels which could be considered as confluences in favour of a bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.08568

- Invalidation: 1.10040

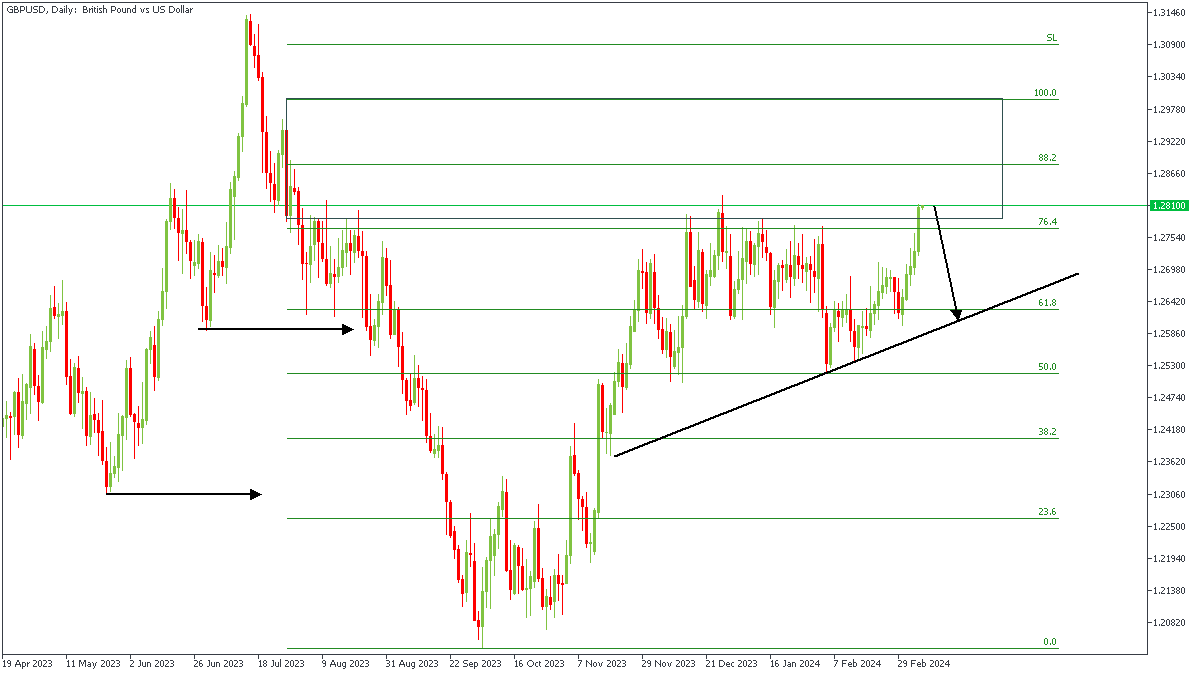

GBPUSD - D1 Timeframe

The daily timeframe of GBPUSD, following the break below the previous low, is currently trading within the supply zone formed right before the break of structure. As a result, I am considering the possibility of a bearish pressure on GBPUSD as a result of the NFP data; this is based off of the Fibonacci retracement levels and the supply zone purely - I’ll be cautious here though, since there aren’t several confluences to consider.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.26629

- Invalidation:1.30024

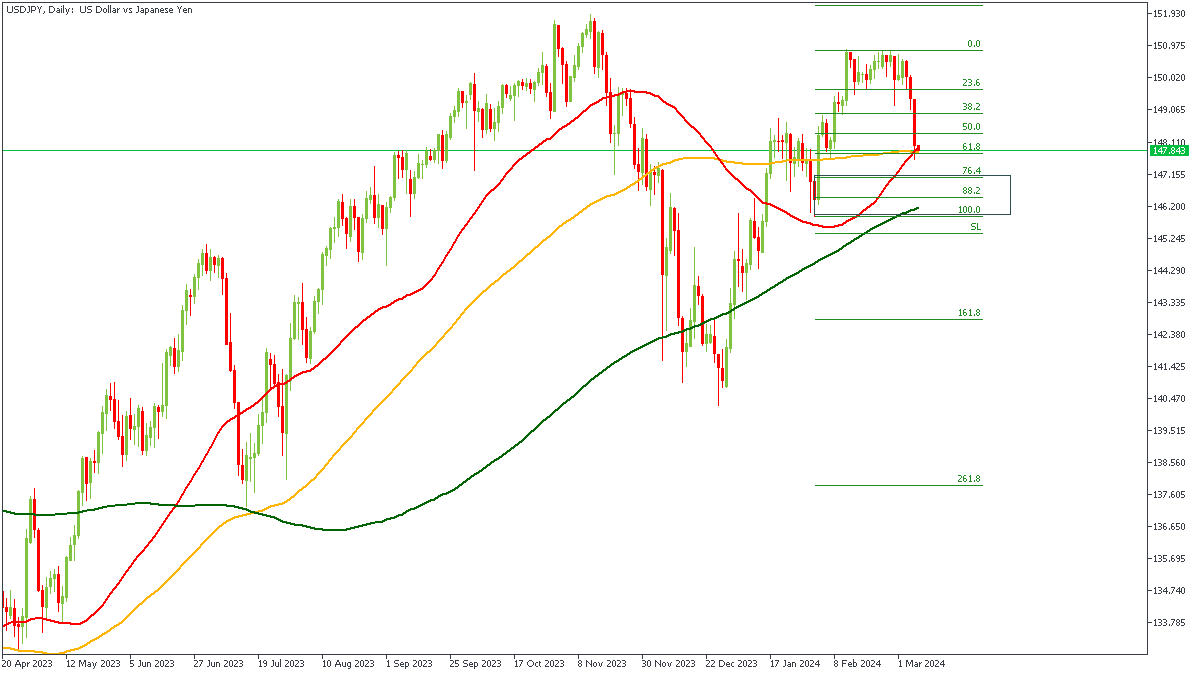

USDJPY - D1 Timeframe

Here on the daily timeframe of USDJPY we clearly see the uptrend as indicated by the moving averages, with the 50 and 100 period moving averages providing ample support for the price action at the moment. Combining this with the bullish array of the moving averages and the Fibonacci retracement levels, I presume the market could regain bullish momentum in a short while - possibly as a result of the NFP data.

Analyst’s Expectations:

- Direction: Bullish

- Target: 149.718

- Invalidation: 145.815

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

ECB Review: June Cut is Coming

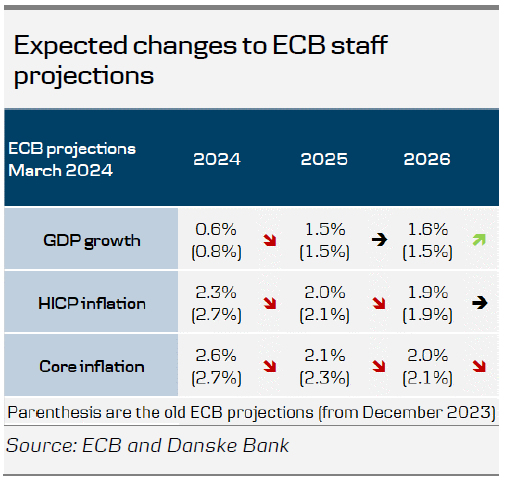

- Today, the ECB decided to keep policy rates unchanged, as unanimously expected by markets and analysts. The new staff projections saw a downward revision of the 2024 projection across growth, headline and core inflation. For 2025, the ECB revised down the projections for 2025 by 0.1pp and 0.2pp for headline and core respectively. Core inflation for 2026 was revised 0.1pp lower.

- Lagarde was quite clear with guidance for a June rate cut, and while April was not ruled out, she said they will know a little more in April, and a lot more in June. We doubt that the incoming data ahead of the 11 April meeting will be sufficiently weak to change that view.

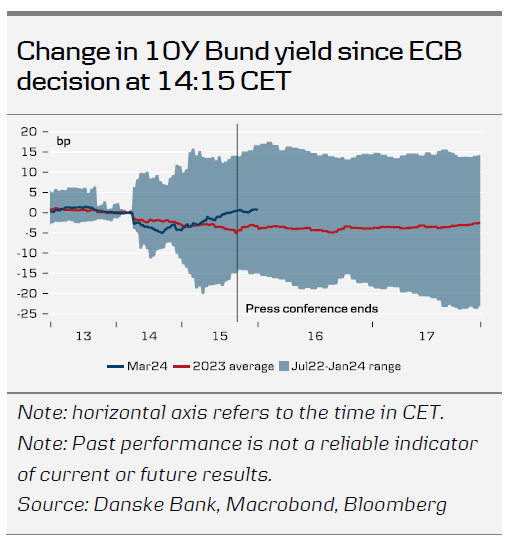

- Markets initially reacted with lower yields across the curve; however, they gradually drifted higher through the afternoon. The move was a parallel shift in the 2y+ area. For 2024, markets added 3bp to now have a 95bp cut priced in.

- Lagarde said she has a strong expectation that the operational framework will be completed at the 13 March (non-monetary policy) meeting.

Acknowledging the progress

The ECB meeting today was a predictable one with no deviation from the prevailing ECB narrative on delivering a rate cut this summer. President Lagarde acknowledged that most measures of underlying inflation have eased further; however, it was nevertheless highlighted that domestic price pressure remains high, in part 'owing to strong growth in wages'. On the other hand, Lagarde also highlighted that growth in wages has started to moderate, and firm profits will absorb part of the increased labour costs. The ECB focused on its internal wage growth tracker and the job portal Indeed for timely wage indications. Both measures have the advantage of being more timely than the usual favourite gauge, namely the compensation per employee, which will be released tomorrow covering Q4 23. The staff projections – which saw a revision of the core projection for 2025 – don't rule out an April rate cut, but with the limited data by then (one PMI print, inflation, SPF and BLS) we do not think they will deliver a rate cut there.

The ECB didn't discuss cutting rates at 'this meeting', but Lagarde said they have 'just begun' discussing dialling back the restrictiveness of monetary policy. This tallies very well with her comment on little more information by April and a lot more by June. Lagarde said they do not commit to a specific pace, rhythm or magnitude of future rate moves.

Staff projections see inflation at 2% target in 2025, but the ECB is not yet sufficiently confident to start lowering rates

Lagarde characterised the current state of the economy as weak, especially since consumers are holding back spending and foreign demand is low. However, surveys point to a gradual recovery in growth this year as real income rises and global growth increases.

On the back of the economic assessment, new staff projections lowered the inflation projections for 2024 and 2025, while 2026 was unchanged. Headline inflation is now expected at 2.3% in 2024 (vs 2.7% in December), 2.0% in 2025 (vs 2.1 % in December) and 1.9% in 2026 (vs 1.9% in December). The downward revision for 2024 compared with the December projection mainly reflects a lower contribution from energy prices. Lagarde said the ECB is more confident in the expected decline in inflation, but not yet sufficiently confident to start lowering rates.

Lagarde stressed that wage growth is a key upside risk for inflation and that it is currently causing domestic inflation, which is mainly services, to remain high. This is also visible in the projections for core inflation. The ECB revised down projections for core inflation to 2.6% in 2024 (vs 2.7% in December), 2.1% in 2025 (vs 2.3% in December) and 2.0% in 2026 (vs 2.1% in December). Wage growth is expected at 4.5% in 2024, down from 4.6% in the December projections. The ECB expects wage growth at 3.6% and 3.0% in 2025 and 2026, respectively, down from 3.8% and 3.3% in December. Lagarde noted that they await more data, especially on wages, before they are sufficiently confident of inflation returning to the 2% target.

The near-term growth projections were revised down as financing conditions are restrictive and past interest rate increases continue to weigh on demand. The growth forecast for 2024 was revised down to 0.6% (from 0.8% in December), remained at 1.5% in 2025 and was revised up to 1.6% in 2026. Hence, growth is expected to remain subdued in the near term and then start to pick up, supported initially by consumption and later also by investments.

Limited FX market impact

As we expected, the FX market impact of the meeting was very limited. EUR/USD initially experienced a slight decline as the EUR weakened, broadly due to downward revisions in the ECB's inflation outlook, which in turn caused front-end European yields to decline and added to rate cuts for ECB pricing this year. However, we saw a reversal of these moves during Lagarde's press conference, as Lagarde guided that the first rate cut is more likely in June than April. We recently discussed the possibility of a short-term rise in EUR/USD due to USD weakness resulting from softer US data. This hypothesis has been supported by cooling signs in the US labour market, coupled with lower-than-expected ISM manufacturing and services. The biggest potential catalyst for the cross this week is the US February jobs report. If our expectation of a softer US labour market holds true, we could see EUR/USD rise further in the very near term.

However, over the course of the year, we still expect EUR/USD to trend lower. We believe the US economy is in a stronger position relative to the euro area, based on factors such as relative terms of trade, real rates, and relative unit labour costs. There are also signs that underlying inflation appears more persistent in the US compared with the euro area, which, all else being equal, should support the USD. A strong USD, coupled with tighter financial conditions, is a necessary condition for the Fed to sustainably achieve its inflation target of 2%. We forecast EUR/USD to reach 1.05/1.04 within a 6/12M horizon.

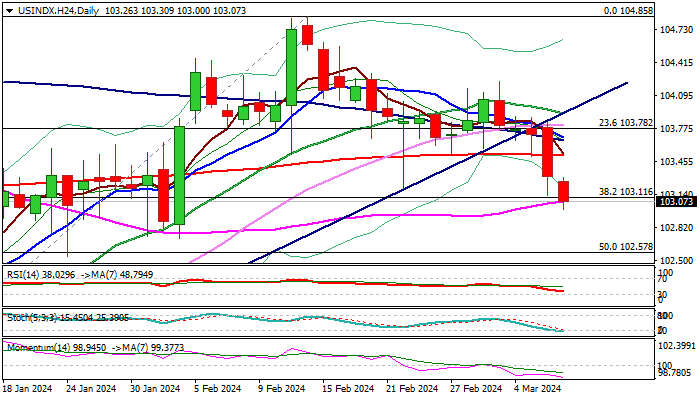

Dollar Index outlook: Dollar Falls Further on Rising Bets for Fed Rate Cut

The dollar index falls to five-week low on Thursday, remaining under increased pressure from growing expectations for June rate cuts.

Fed Chair Powell added to expectations by relatively dovish remarks in his testimony on Wednesday, saying that rate cuts will likely be appropriate later this year if economy evolves broadly as expected.

Markets shift focus on Friday’s release of US labor report, with weaker than expected February numbers to further sour the sentiment and increase pressure on greenback.

Fresh extension lower on Thursday broke through pivotal Fibo support at 103..11 (38.2% of 100.29/104.85 rally, reinforced by 55DMA) which contained Wednesday’s drop, with close below this level to generate fresh bearish signal and open way for extension towards supports at 102.57 and 102.04 (Fibo 50% and 61.8% respectively).

Technical studies on daily chart turn to full bearish setup, adding to negative outlook.

Oversold conditions, on the other hand, warn of price adjustment, with broken 200DMA (103.51) offering solid resistance and expected to cap upticks and keep bears in play for fresh push lower.

Res: 103.30; 103.51; 103.68; 103.91.

Sup: 102.71; 102.57; 102.04; 101.74.

Research China – A Long and Painful Transition

China continues to struggle with a housing crisis that shows no signs of turning three years into the crisis. We expect it to weigh on the economy again this year. However, the overall economy continues to muddle through with the help of stimulus and industrial policy.

In 2024 we look for growth to moderate from 5.2% to 4.5% but the decline is mostly due to less favorable base effects compared to 2023. Monetary and fiscal easing is expected to continue. The government growth target for 2024 is expected to be 5%.

Exports should perform better this year and we also look for more decent growth in manufacturing investments as well as infrastructure supported by a strong focus on green investments. Consumption growth, however, is set to slow and together with the housing crisis provides the main downside risk to the outlook.

In 2025 we look for growth to stay soft around 4.5%. China is in the middle of a long painful transition from a growth model highly dependent on housing to a new model where China aims at growth drivers to be hightech investments, upgrade of manufacturing, green investments and consumer demand.

Intense US-China geopolitical rivalry is here to stay despite the recent improved dialogue. We expect EU to at least double tariffs on Chinese EVs from 10% to 20-25% this year.

ETHUSD Storms to a Fresh 26-month Peak

- ETHUSD ascends sharply, touching 4,000 psychological mark

- Momentum indicators are deep within overbought zones

- Risk of a pullback is high given the overstretched rally

ETHUSD (Ethereum) has been in a steep uptrend, surging to consecutive multi-month highs. However, traders should not rule out an impending downside correction as the short-term oscillators are flagging extremely overbought conditions.

Should bullish pressures persist, the price might revisit its recent 26-month peak of 3,902. Breaking above that zone, Ethereum could advance towards the December 2021 resistance of 4,150. A violation of that zone may pave the way for the December 2021 hurdle of 4,490.

On the flipside, bearish actions could send the price to challenge the April 2022 resistance of 3,580, which could serve as support in the future. Further declines might then cease around the March 2024 support of 3,260. Sliding beneath that floor, the price could test the February support of 2,900, which also held strong in April 2022.

Overall, ETHUSD has been posting a series of consecutive multi-month highs, but the advance is starting to look overdone from a technical perspective.

Sunset Market Commentary

Markets

Some of the most remarkable moves ahead of the ECB policy decision were seen in JPY and UK gilts. The former outperformed global peers on increased Bank of Japan policy normalization bets. Events supporting the case succeeded each other quickly. Bloomberg yesterday reported that some government officials have moved to endorse a BoJ rate hike. Officially, the Japanese government still declares the country in a state of deflation but something’s moving. Within the BoJ a consensus is forming as well, with board member Nakagawa this morning being the latest one expressing growing confidence in reaching the 2% target. Finally, this morning’s data showed wages growing at the fastest and consensus-topping clip since June. That came on top of news that the Japanese Trade Union Confederation (Rengo) said its affiliated unions demand a 5.85% wage increase at this year’s spring pay talks (Shunto). That’s the highest in 30 years and is hard evidence of the virtuous wage-price spiral the BoJ is looking for. USD/JPY cascaded since Tuesday from 150.55 to 147.85 today. Strong (expected) wage growth and stubbornly high CPI expectations by firms (see below) drove the gilt underperformance. UK yields rose more than 5 bps at the front at some point, helping sterling to appreciate against the likes of EUR and USD.

The ECB delivered no surprises by holding rates constant and sticking to a natural APP rundown, to be followed by PEPP from 2024H2 at €7.5bn/month with this cap removed by year-end. Growth remains sluggish this year (0.6%, from 0.8%) with downside risks but should pick up further out (1.5% in 2025 and 1.6% in 2026). Lagarde did note the recent improvement in some indicators (eg. PMIs). Inflation continues to ease. Lower energy prices pushed the 2024 forecast down from 2.7% to 2.3%. HICP should hover around the 2% target in 2025 and slightly below that in 2026. Core gauges improved more moderately and from still-elevated levels as high wage growth tempers the process. Forecasts show 2.6%-2.1%-2% over the policy horizon. The downward tweaks mean the ECB will officially hit its target in the medium term. It triggered fresh euro day lows and a drop in European yields (-6 to -7 bps, with knock-on effects in the US and UK) going into the press conference. The audience mostly tried to retrieve guidance for a first rate cut. Confidence in reaching the goal increased but more evidence about disinflation’s durability is needed: “We will know more in April, but we will know a lot more in June.” Data on the outcome of wage negotiations remains key. That comment supported the euro and yields somewhat (EUR/USD around the 1.09 levels prior to the policy decision, yields pare losses to 3-4 bps). It makes the June meeting an increasingly live one from a market point of view. They counted on that one to be the kick-off gathering for quite some time and that hasn’t changed today. It would mean the ECB is pioneering the easing cycle instead of the Fed. About this unusual sequence Lagarde said the ECB takes into account the international environment but that decisions are taken independently.

News & Views

The monthly Decision Maker Panel survey published by the Bank of England slowed that firms’ expectations on price developments are slowing at only a moderate pace. Firms reported that their output prices rose by an average rate of 5.4% in the three months to February down 5.6% in January. Businesses expect their output price to rise by 4.3% over the next year (3m MA). Firms see one-year ahead CPI inflation to decline to 3.3% vs 3.4% in January. The three-year ahead inflation expectations eased from 2.9% to 2.8%, well above the BoE’s 2% target. Firms see a slowdown in employment growth. Growth job growth in the three months to February slowed to 2.3% from 2.4%. Employment for the next 12 months is now expected at 1.6% down from 1.7% (3m MA). Realized wage growth was reported at 6.7%. Wages still are expected to rise 5.2% over the next 12 months. The survey suggests that firms remain cautious to see inflation sustainably return to the BoE’s target short-term, but also in a somewhat longer horizon.

The Central Bank of Turkey (CBRT) introduced a temporary reserve requirement for banks if their monthly loan growth exceeds 2.0%, according to regulation published in the official gazette. The additional reserve requirement follows tightening measures announced yesterday to reinforce the monetary policy stance via non-interest rate measures. The CBRT yesterday reduced the monthly growth limit for LT commercial loans from 2.5% to 2.0%. The limit for monthly growth for general purpose loans was reduced from 3.0% to 2.0%. At least for now, the new measures didn’t halt de decline of the lira. EUR/TRY is setting record at 34.85.