Sample Category Title

Apple Scraps EV, Joins AI Race

Apple abandoned its ambition to build an electric car. Yes, Apple car, which is in the making since the past decade, will never see the daylight. The company abandoned one of its biggest projects of the past decade in a surprise decision yesterday and said that the 2000 people working on it concentrate on the generative AI division instead. That’s exactly what Meta did last year; it decided to become more discrete on its metaverse development and go full blast into AI to increase its business value. This is what Apple is doing today. Having understood that missing the AI turn would be a severe hit to the company, they are getting – a bit later than the others – into the AI race. Better late than never.

Apple has been struggling to extend gains since last December. The latest earnings season hasn’t been a walk in the park given the difficult business in China. And while Apple’s tech peers saw their stock prices rise from the record to record, Apple’s only achievement – I am talking about stock price huh? – has been to keep its head above $180 per share. So yes, doubling down on AI is certainly a good decision, Apple rose 0.81% yesterday.

Elsewhere, Microsoft cut a deal with the European Mistral AI, and Alibaba led the largest single day financing round for a Chinese AI startup called Moonshot AI, hoping that it could help them smooth out supply chains and lead to more efficient automation. All this to say that the AI topic is here to stay. The more companies move toward AI developments, the more Nvidia investors see dollars in their eyes. Nvidia didn’t gain yesterday – not a usual day for the chip giant, but the developments confirm that investments pour in.

On the macro front

The S&P 500 had a slow session yesterday, as the US yields were little changed on the back of mixed economic data, the rising suspense regarding whether the US will default on March 1 and a 7-year US government bond auction that settled above 4.30%. The durable goods orders tanked more than 6% in January, the most in nearly 4 years. Richmond manufacturing index came in better-than-expected, except for shipments, while Atlanta Fed’s GDPNow index was revised up to 3.2% for this quarter from 2.9% printed earlier.

Today, the US will reveal its latest GDP numbers. The US economy is expected to have grown 3.3% in Q4. That’s lower than the 5% printed in the Q3, but it’s still a very strong growth for an economy that underwent the most aggressive tightening cycle of its modern history. And if Atlanta’s GDP prediction is an indication, the slowdown will slow in the first quarter of this year.

Robust growth is good, if it’s not accompanied by stronger inflation. Is it possible? Yes, it is possible, if supply grows faster than demand, but I think that’s not necessarily the case for the US right now. Demand remains strong despite the latest weakness in consumer spending and durable goods orders. And core PCE – which will be released tomorrow – is expected to print the biggest jump in a year on a monthly basis. Therefore, good news (on GPD data) has the potential to be bad news for market sentiment, provided that strong growth and higher inflation would push the Federal Reserve (Fed) rate cut expectations further down the road. Pricing today suggests that the market expects a 75bp cut from the Fed this year – matching what the Fed members plotted on their latest dot plot in December. The probability of a June rate cut slipped just below 60% yesterday. A U-turn in inflation won’t only delay the first rate cut but likely slow the pace of the future cuts as well. That’s not good news for risk appetite.

But hey, don’t ring the alarm bell yet. G20 chiefs said that soft landing is possible, as the post-pandemic inflation is gently fading. If there is no major surprise on the inflation front, the central banks should go ahead with their rate cut plans and avoid a recession. If not, high inflation would call for an extended period of high interest rates which could eventually push the world economy into recession. It’s all on inflation’s shoulder.

Good news: inflation in Japan fell to a 22-month low and inflation in British stores slowed to the lowest level since March 2022 thanks to easing supply-chain pressures, falling input costs for energy and fertilizers and a forceful competition between the British retailers.

In the FX, the US dollar index is stuck between its 100 and 200-DMA and should find a clear direction after tomorrow’s inflation print. US crude continues to test the $79pb offers to the upside. Inflation in Australia came in lower than expected, keeping the Reserve Bank of Australia (RBA) hawks away from the marketplace, and the Reserve Bank of New Zealand (RBNZ) kept its rate unchanged for the 5th straight meeting and said that risks to inflation became more balanced. The Kiwi-dollar fell to 0.61 as the latest RBNZ decision came as a disappointment to hawks who were betting that the RBNZ would hike rates at today’s meeting.

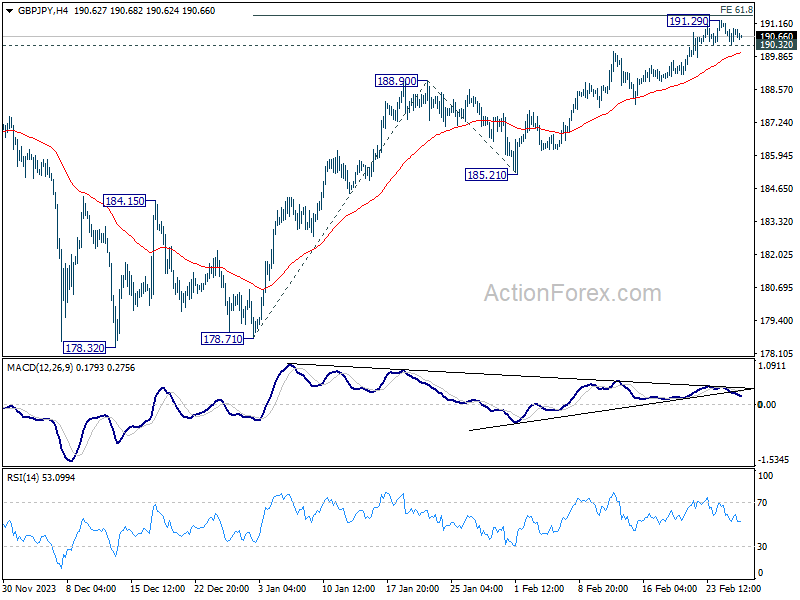

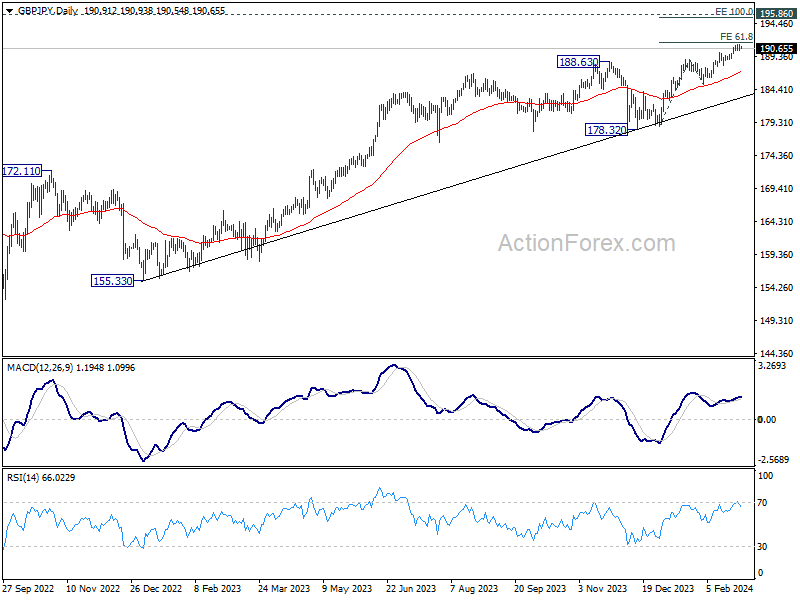

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.50; (P) 190.84; (R1) 191.31; More....

Intraday bias in GBP/JPY is turned neutral again with current retreat. On the upside, decisive break of 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50 will extend larger up trend to 100% projection at 195.40. On the downside, however, break of 190.32 minor support will turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

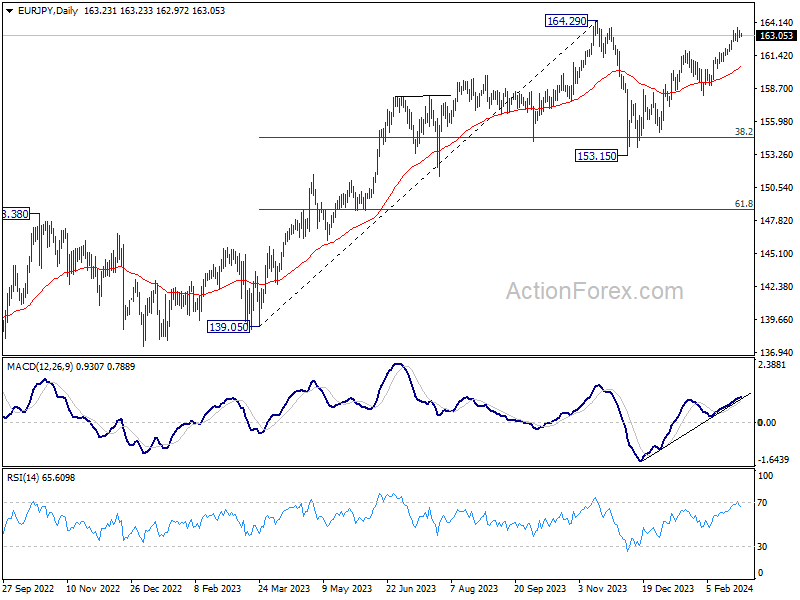

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.92; (P) 163.22; (R1) 163.55; More...

Intraday bias in EUR/JPY is turned neutral gain with current retreat. On the upside, above 163.70 will resume the rise from 153.15 to 164.29 high. However, considering loss of momentum as seen in 4H MACD, break of 162.55 minor support will turn bias back to the downside for deeper pullback first.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

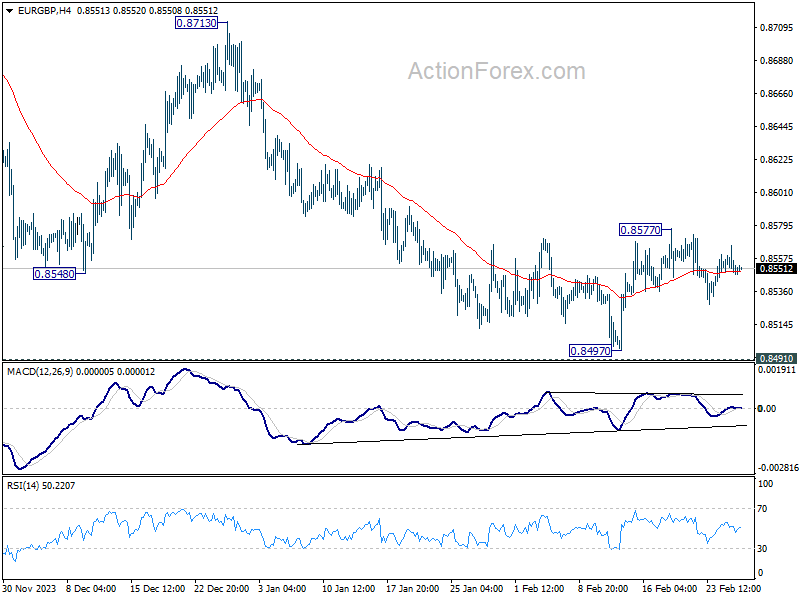

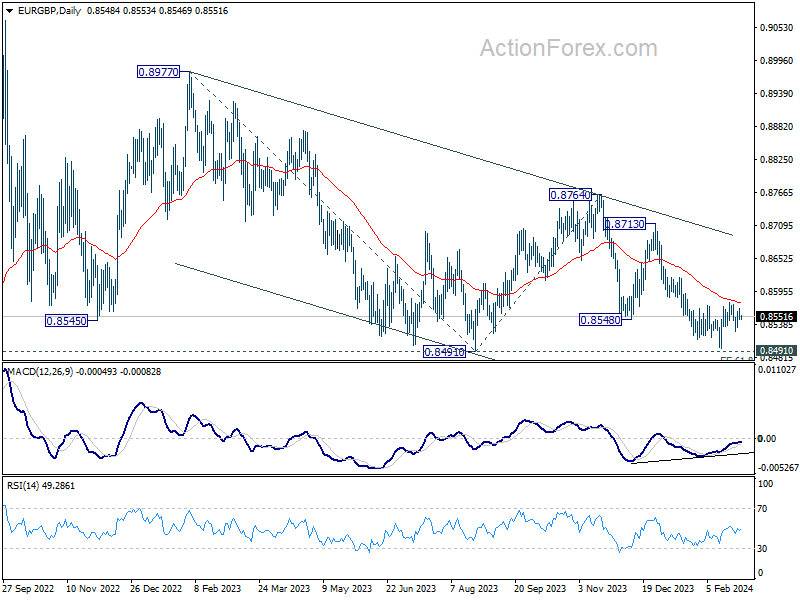

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8542; (P) 0.8555; (R1) 0.8561; More...

Intraday bias in EUR/GBP remains neutral for the moment. Risk stays mildly on the downside with 0.8577 resistance intact. Decisive break of t 0.8491/7 support zone will resume larger down trend. On the upside, however, break of 0.8577 will turn bias to the upside for resuming the rebound from 0.8497.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

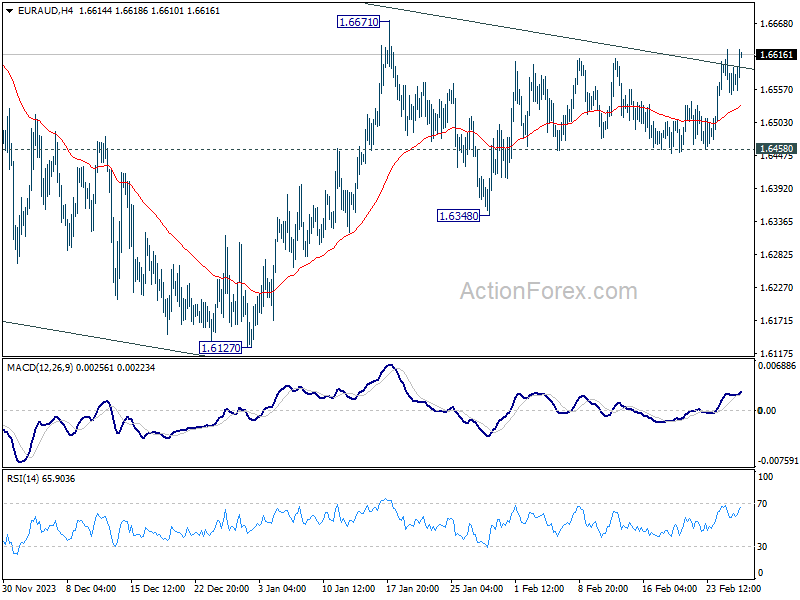

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6540; (P) 1.6584; (R1) 1.6616; More...

Intraday bias in EUR/AUD remains neutral at this point. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, below 1.6458 support will turn bias to the downside for 1.6348 and possibly below.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

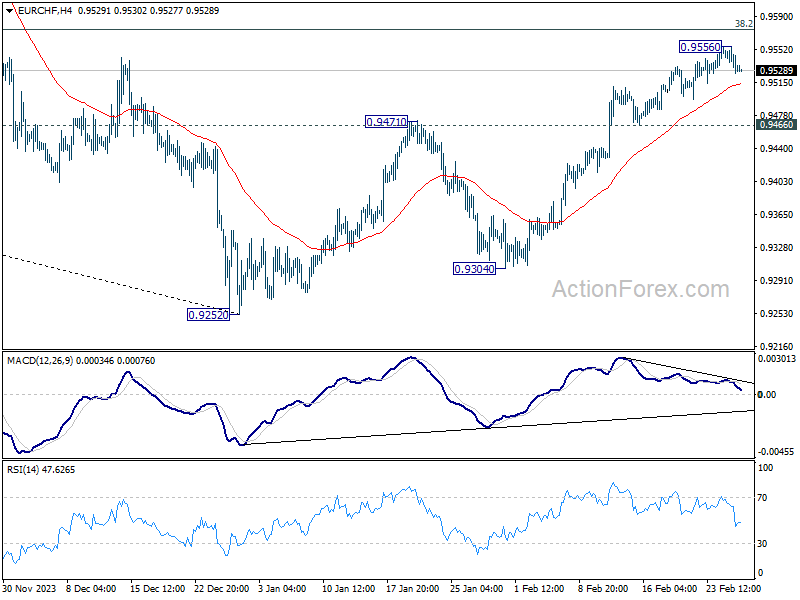

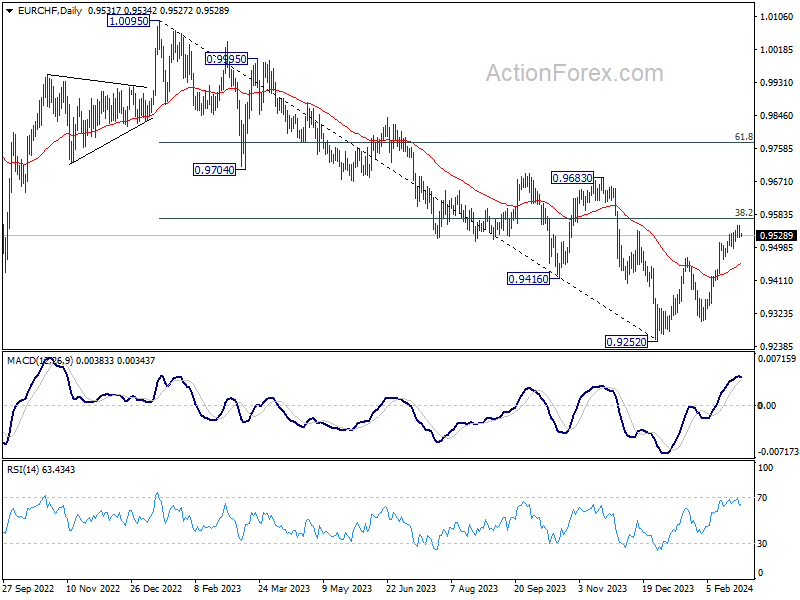

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9517; (P) 0.9538; (R1) 0.9548; More...

Intraday bias in EUR/CHF is turned neutral again with current retreat. Considering loss of momentum as seen in 4H MACD, in case of another rise, upside should be limited by 0.9574 fibonacci resistance. On the downside, break of 0.9466 support will argue that rebound from 0.9252 has completed as a three-wave correction. Outlook will be turned bearish for retesting 0.9252/9304 support zone.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574 and possibly above. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

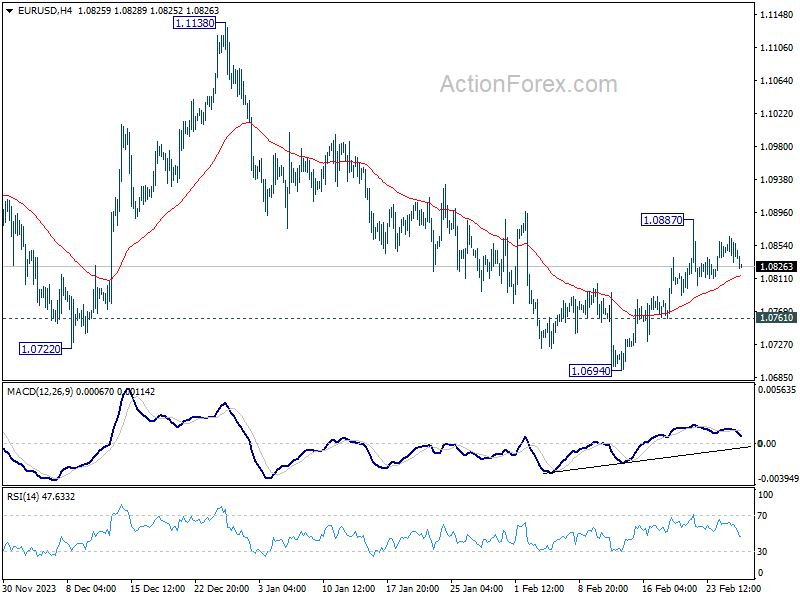

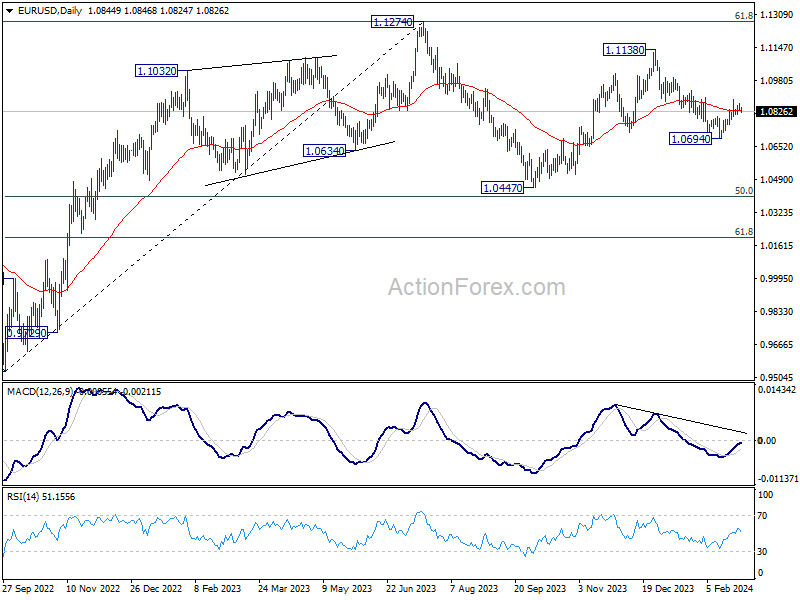

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0830; (P) 1.0848; (R1) 1.0863; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. On the upside, break of 1.0887 and sustained trading above 55 D EMA (now at 1.0832) will affirm the case that fall from 1.1138 has completed. Stronger rally would then be seen back to 1.1138. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

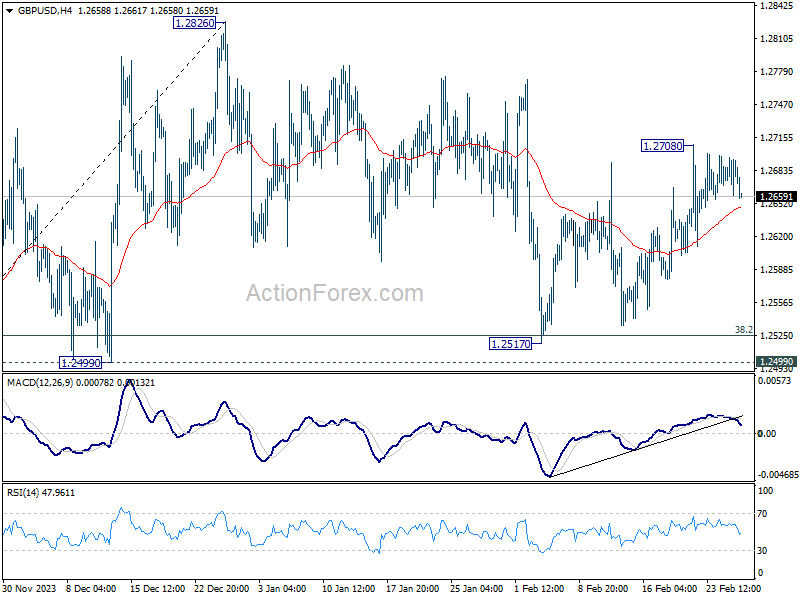

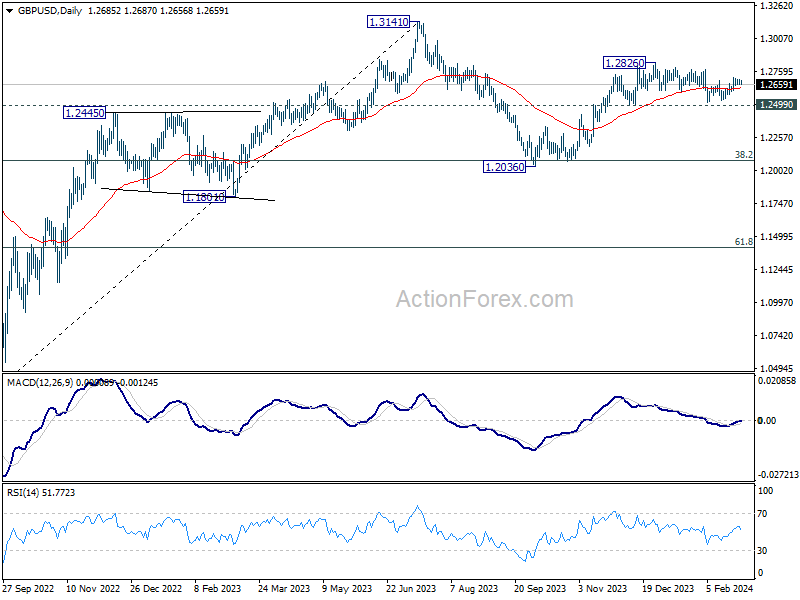

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2665; (P) 1.2681; (R1) 1.2702; More...

Intraday bias in GBP/USD stays neutral at this point and outlook is unchanged. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

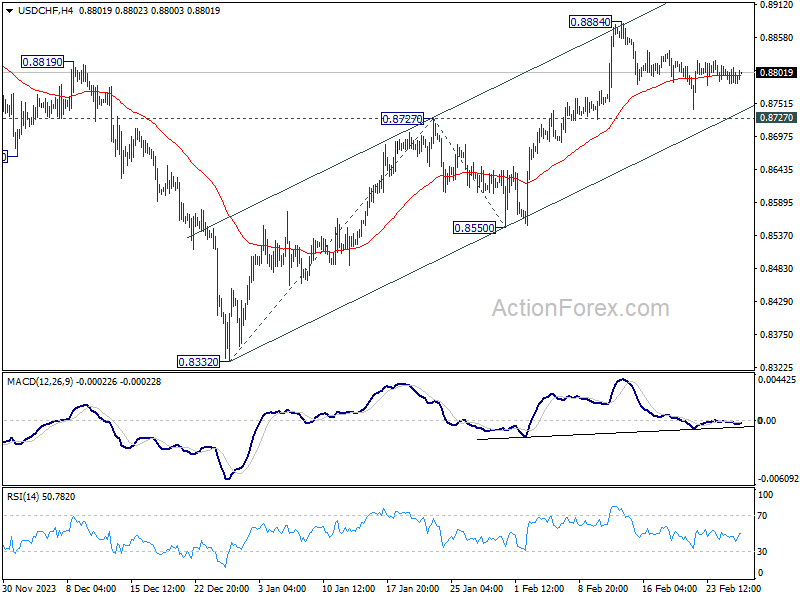

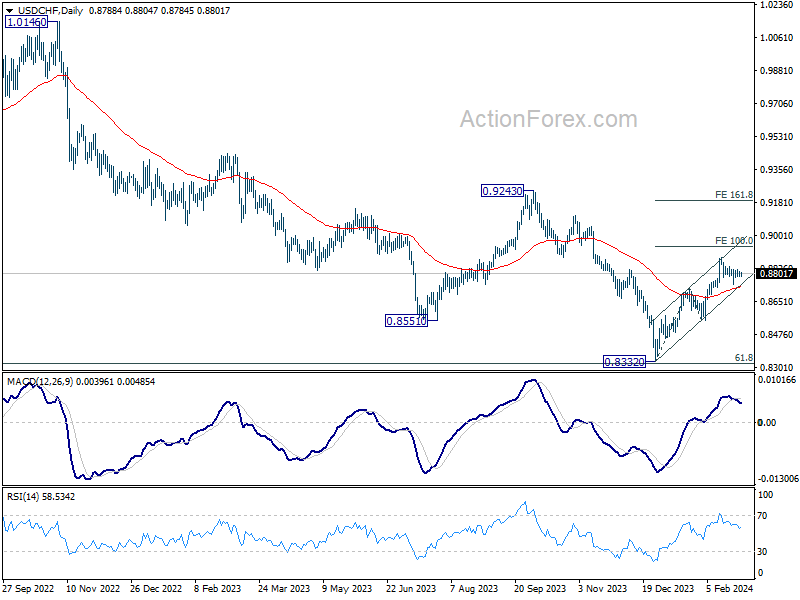

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8776; (P) 0.8794; (R1) 0.8803; More....

USD/CHF's consolidation from 0.8884 continues and intraday bias stays neutral for the moment. With 0.8727 resistance turned support intact, further rally is expected. On the upside, above 0.8884 will resume the rally from 0.8332 to 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

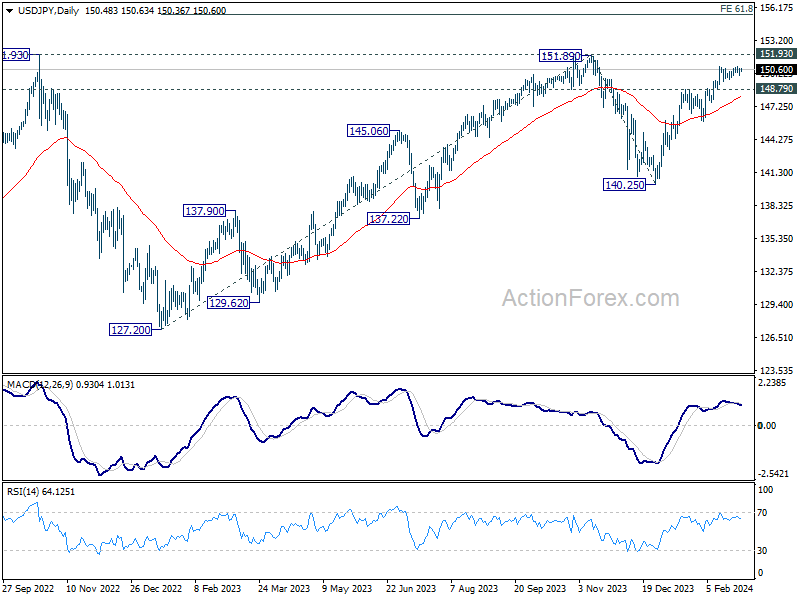

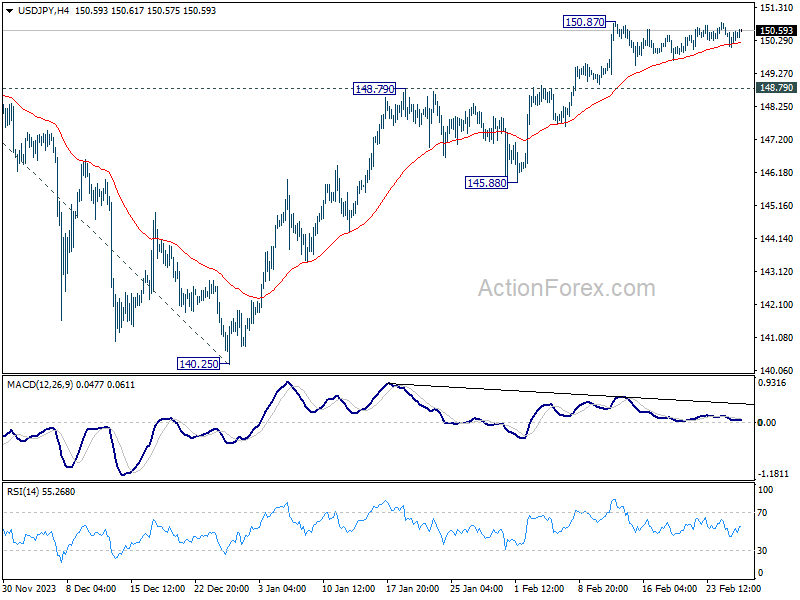

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.17; (P) 150.44; (R1) 150.81; More...

Intraday bias in USD/JPY stays neutral as sideway trading continues. In case of deeper retreat, downside should be contained by 148.79 resistance turned support to bring rebound. On the upside, break of 150.87 will resume 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next.

In the bigger picture, rise from 140.25 is seen as resuming the trend from 127.20 (2023 low). Decisive break of 151.89/.93 resistance zone will confirm this bullish case and target 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. However, break of 148.79 resistance turned support will delay this bullish case, and extend the corrective pattern from 151.89 with another falling leg.