Sample Category Title

Sunset Market Commentary

Markets

ECB members came out “en masse” today, resembling the recent push by the US central bank. Hawkish Austrian ECB Holzmann immediately pulled an interesting string. He supports our “sequence” call, stressing that he didn’t see any circumstances for the ECB to cut policy rates before the Fed. We’re on the same line, arguing that the ECB won’t risk a weaker currency by moving ahead of the FOMC. Its credibility and especially inflation goal are at stake if the central bank risks taking the first leap while inflation is still running above the 2% inflation target. Given that Fed members are openly pushing back first rate cuts bets to the June meeting (at best), it implies that the window of opportunity for the ECB only opens at the July meeting, our preferred scenario. Holzmann continued by preferring a later but faster cycle compared to a rapid start with gentle moves lower. The main argument for erring on the hawkish side of expectations is the persistence of elevated wage pressure. Shorty after the Holzmann comments, the ECB published consumer survey inflation expectations for January. They slightly increased on the 1-yr horizon (3.3% from 3.2%) while keeping level on the 3-yr tenor (2.5%). ECB Schnabel lined up next, arguing that internal models suggest that the peak impact from interest increases may already be over. This again argues in favour of keeping policy rates higher for longer with inflation sticky above target and EMU growth set to recover from last year’s standstill. Bundesbank president Nagel added to the hawkish rhetoric by saying that officials mustn’t be tempted to cut rates earlier as the inflation outlook isn’t clear enough yet. He’s more comfortable with current market pricing (first move in June; max 100 bps of cuts this year) compared with say a month ago (start in April and cumulative 150 bps of cuts in 2024). Premature cuts could result in the worse outcome, reigniting inflation when it hasn’t actually been conquered. ECB President Lagarde underlined the importance of Q1 wage data which will only be at the central bank’s disposal by the June policy meeting. Lithuanian ECB Simkus is happy with Lagarde’s guidance of a first rate cut in “summer” while dovish Greek ECB member Stournaras is more precise, singling out the June meeting as his preferred kick-off point.

ECB rhetoric failed to inspire trading in an uneventful session. German Bund yields currently give up around 3 bps after setting YTD highs yesterday. Changes on the US yield curve are more modest, varying between +1 bp and -1 bp. EUR/USD treads water at 1.0830 with European stock markets slightly benefiting from yesterday’s WS momentum (EuroStoxx +0.4%;new cycle high).

News & Views

French finance minister Le Maire called for action in the creation of a Capital Markets Union (CMU). In his pitch before his European colleagues he noted the project has dragged on for a decade but that high financing needs for the green and digital overhaul underscore the need. France and Germany estimate these costs at some €500bn a year, which may be difficult to finance through public funds only. The many different financial systems and legal settings in the 27 EU countries make it very challenging to create the CMU. That’s why Le Maire suggests to kick off the project on a voluntary basis, beginning with three to four (unspecified) countries. His proposal would entail the submission to single EU supervision of banks, stock exchanges and asset management as well as the creation of a European savings product.

Belgian business confidence improved in February from -16.4 to -12.8. Doing so, the NBB’s company gauge reversed the setback from January with better readings across all sector. The smoothed series, indicating the underlying economic trend, increased only slightly but that does bring an end to the downward path in place since last May. Trade (from -17.8 to -11.9) posted the sharpest recovery on better forecasts for orders to be placed with suppliers, in response to growing demand expectations. Business-related services sector confidence (+9.1 from +4.6) was shored up by all sub indicators, from the assessment on current and expected activity to anticipated demand. Manufacturing (-18.5 vs. -22) also responded more favourably on all accounts with the biggest improvement seen in future demand. The upturn in confidence was the smallest in the building industry (-10.3 from -12.8).

XAUUSD: Bears Prepare To Takeover

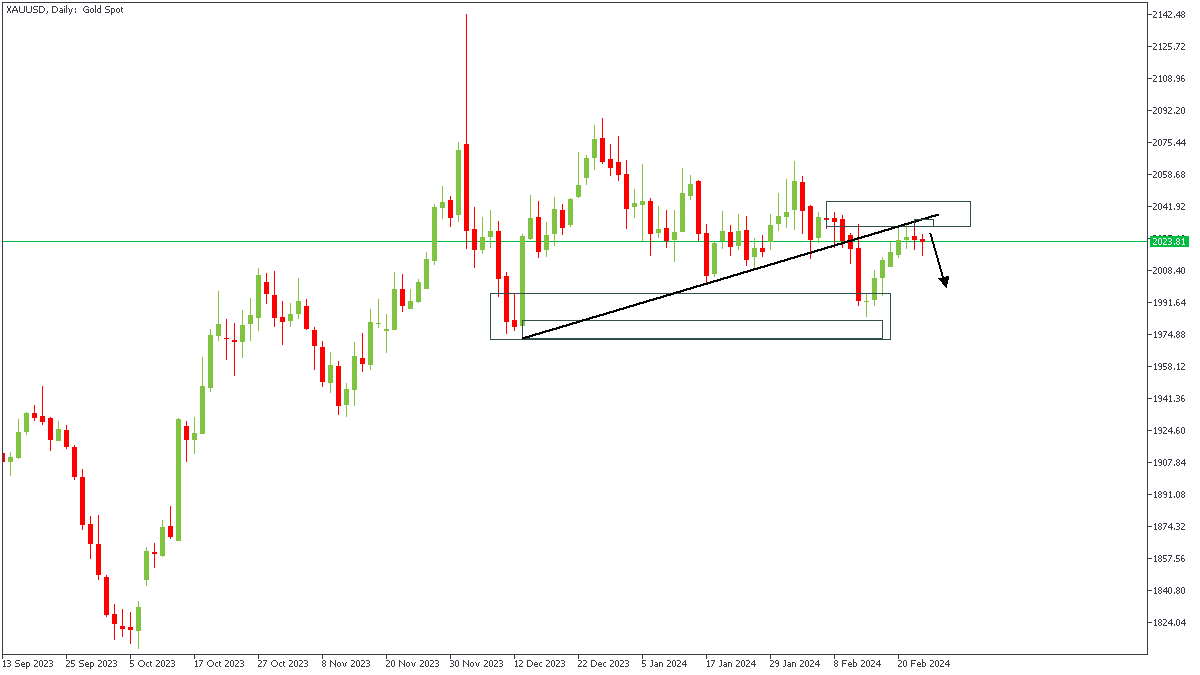

On Friday, the gold price (XAUUSD) retreated from a recent two-week high, facing selling pressure. This decline was driven by hawkish minutes from the FOMC meeting, indicating the Fed's reluctance to cut interest rates. Elevated US Treasury bond yields, supported by a "higher-for-longer" narrative, further weakened demand for gold, as investors favored yield-bearing assets. However, the US dollar struggled to gain momentum, staying near three-week lows, potentially supporting gold as a safe-haven asset amid geopolitical tensions in the Middle East. Moving forward, market attention will focus on US bond yields and USD dynamics, with short-term opportunities in XAUUSD influenced by broader risk sentiment.

XAUUSD - D1 Timeframe

Price action on the daily timeframe of XAUUSD shows price currently reacting from the rally-base-drop supply zone, albeit in a subtle manner. We also see that the previous low has been broken, which means that price can be said to have completed the retracement. The added confluence to this is the trendline resistance that price seems to also be reacting to at this time.

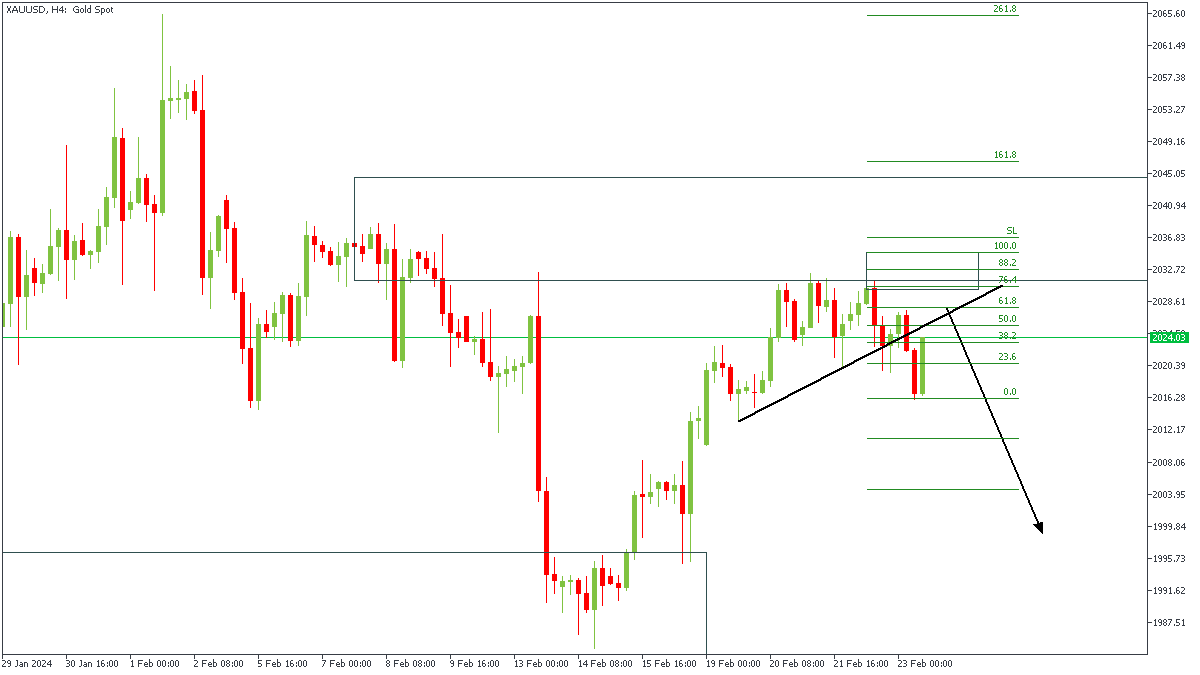

XAUUSD - H4 Timeframe

After reacting from the supply zone on the daily timeframe, here on the 4-hour chart of XAUUSD, we see that a change of character has already occurred from the recent break of structure. Following this, I expect to see a proper rejection from the trendline resistance and the Fibonacci retracement level. My target for this idea is the previous demand zone as shown on the chart.

Analyst’s Expectations:

- Direction: Bearish

- Target: $2,004.62

- Invalidation: $2,044.96

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

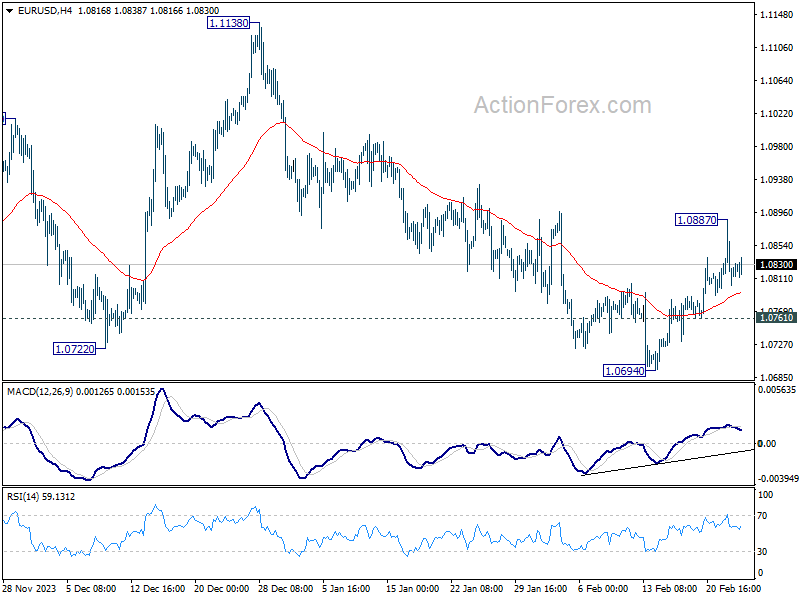

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0788; (P) 1.0838; (R1) 1.0872; More...

Outlook in EUR/USD is unchanged and intraday bias stays neutral. On the upside, break of 1.0887 will affirm the case that fall from 1.1138 has completed, and target this resistance. However, break of 1.0761 will turn bias back to the downside for retesting 1.0694 support.

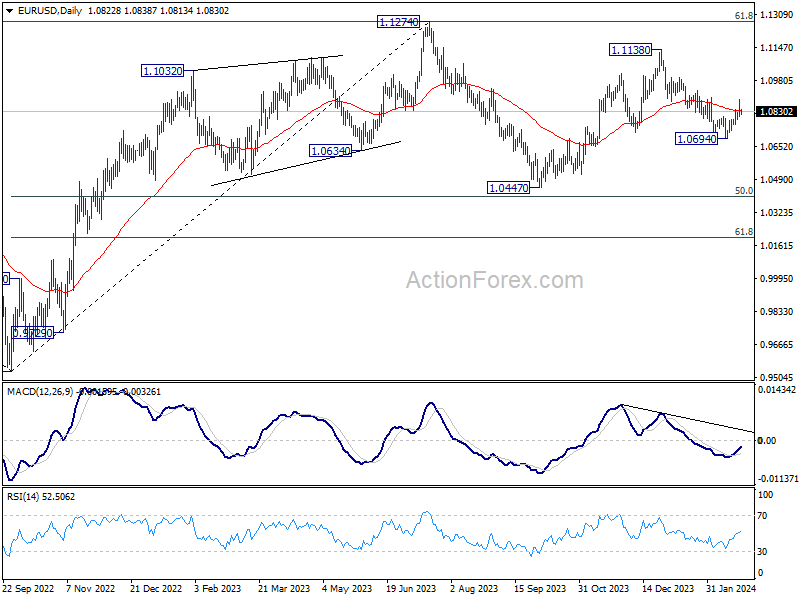

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

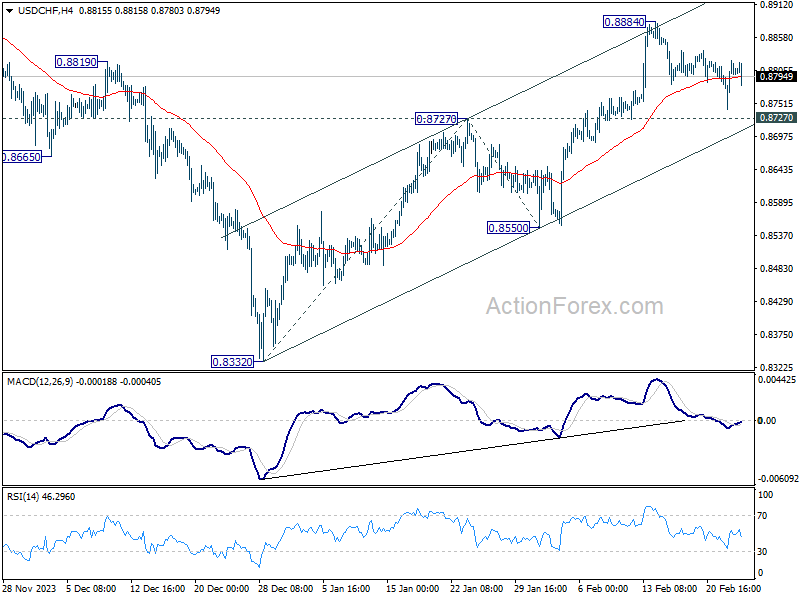

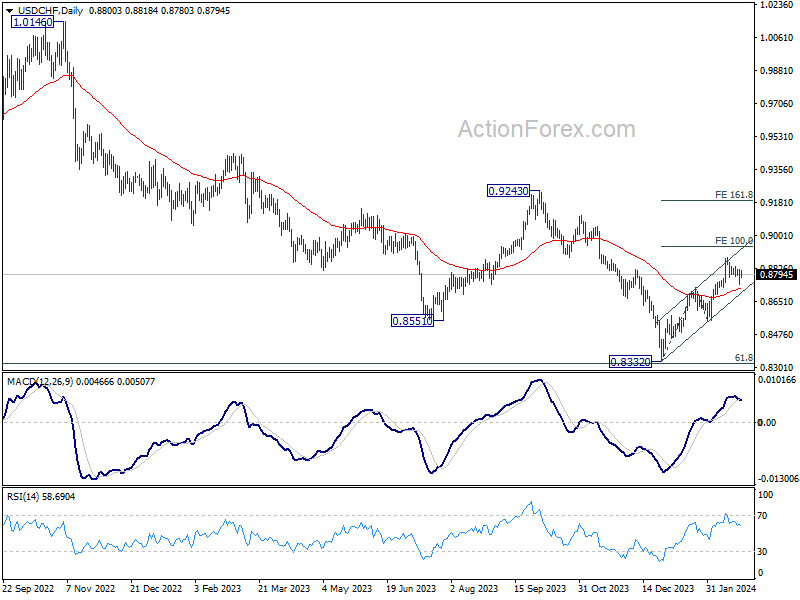

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8756; (P) 0.8789; (R1) 0.8835; More....

No change in USD/CHF's outlook as consolidation is extending. Intraday bias remains neutral. With 0.8727 resistance turned support intact, further rally is expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

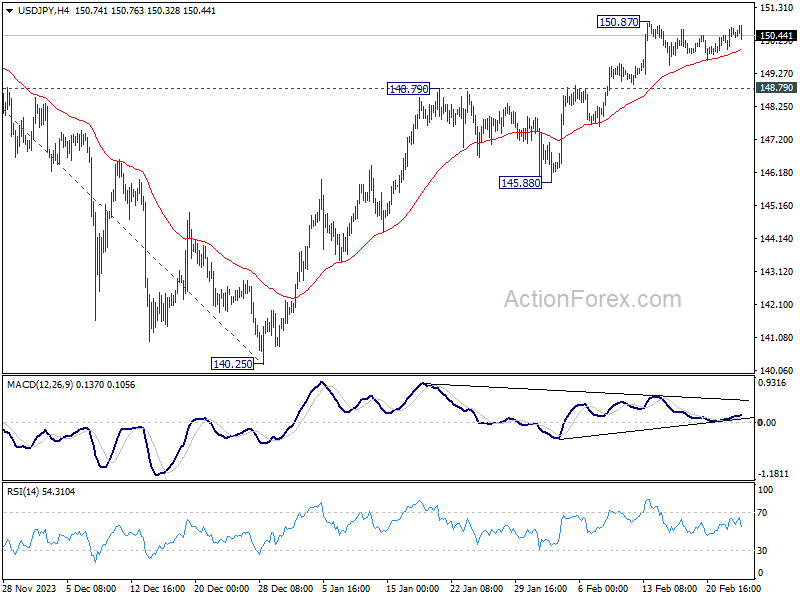

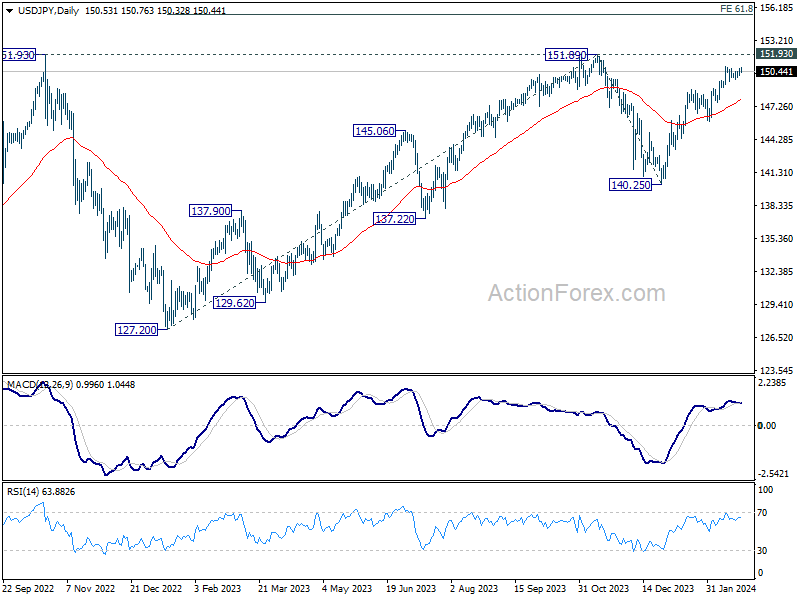

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.14; (P) 150.42; (R1) 150.81; More...

No change in USD/JPY's outlook as range trading continues. Another retreat cannot be ruled out, but downside should be contained by 148.79 resistance turned support to bring rise resumption. Above 150.87 will resume the rally from 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. However, firm break of 148.79 will turn bias to the downside for 145.88 support.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

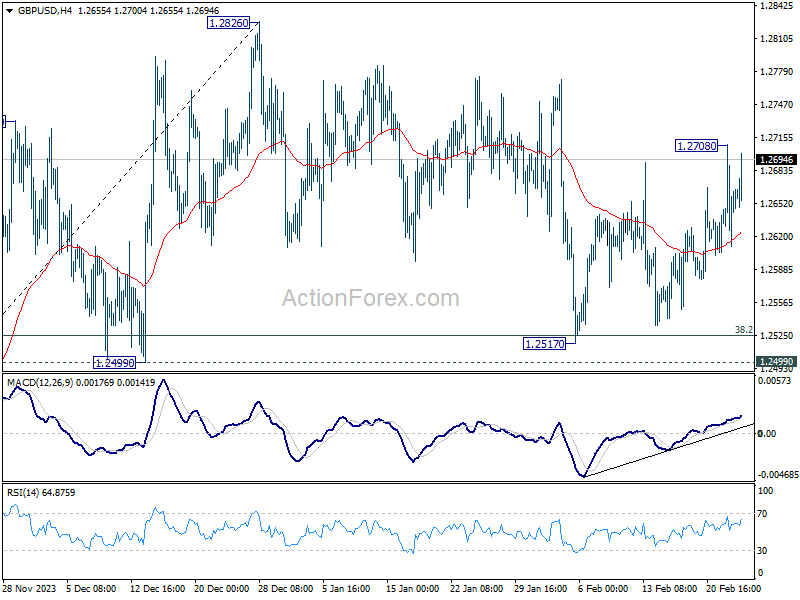

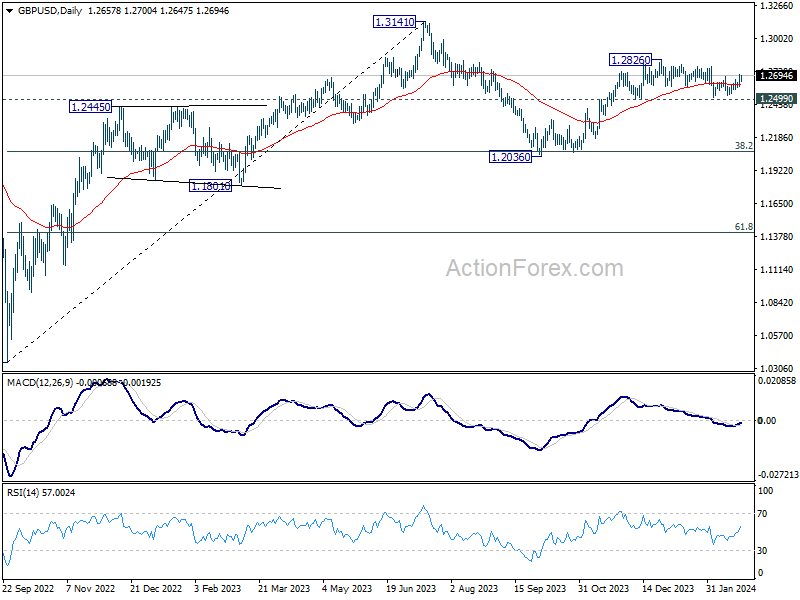

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2612; (P) 1.2661; (R1) 1.2710; More...

GBP/USD bounces notably today but stays below 1.2708. Intraday bias remains neutral first. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Yen and Dollar in Weak Positions as Traders Watch US Markets’ Record Rally

As US session gets underway, Yen and Dollar remain the weakest links in the currency markets, reflecting a broader trend of risk appetite among investors. All eyes are now on whether the US stock market can extend its record-setting run. In particular, there is anticipation that NASDAQ could catch up and achieve a new historical high. Meanwhile, there's prospect for Yen and Dollar to swap their positions before the week closes, contingent upon extended retreat US treasury yields.

Meanwhile, Euro presents a mixed picture following the latest German Ifo business survey, which underscored the persistent sluggish sentiment within Europe's largest economy. Despite stabilization, the economic outlook remains tepid at best. Additionally, a series of remarks from ECB officials aimed at tempering expectations for an early rate cut seems to have had limited impact on market sentiment, suggesting that investors may be looking beyond immediate policy signals.

Sterling, on the other hand, is finding some strength, especially against Euro, buoyed by overall positive risk sentiment. Australian dollar and New Zealand dollar are also benefiting from the prevailing risk-on environment, though Canadian dollar is noticeably trailing.

In Europe, at the time of writing, FTSE is up 0.06%. DAX is up 0.06%. CAC is up 0.63%. UK 10-year yield is down -0.028 at 4.087. Germany 10-year yield is down -0.034 at 2.407. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -0.10%. China Shanghai SSE rose 0.55%. Singapore Strait Times fell -1.18%.

ECB's Lagarde watches Q1 wage talks for clues on lasting disinflation

ECB President Christine Lagarde described Q4 wage figures as "obviously encouraging numbers". However, she underscored the importance of caution, stating that the Governing Council needs to gain "more confidence" in the sustainability of the disinflationary process currently underway.

Lagarde also pointed to ongoing wage negotiations across various sectors and employee groups, expected to conclude in Q1, with data becoming available in May. The outcomes of these negotiations are anticipated to be a critical factor in the ECB's assessment of the inflationary outlook.

"Those numbers will — especially if they continue to be encouraging — will be important for us to assess going forward in order to reach confidence," Lagarde remarked in a press conference today.

ECB's Nagel: Rate cut may be tempting, but it's not time yet

In the annual report from Bundesbank, ECB Governing Council member Joachim Nagel emphasized the importance of caution and patience. "Even though it may be very tempting, it is too early to cut interest rates. This is because the price outlook is not yet clear enough," Nagel stated.

Furthermore, Nagel's call for perseverance reflects an understanding of the challenges inherent in steering monetary policy towards achieving price stability. "We should not let ourselves stray away from the path we have embarked on," he advised, emphasizing the need for consistency and resilience in ECB's policy stance.

Holzmann: ECB's monetary policy often trails behind Fed's

In an interview with Bloomberg TV, ECB Governing Council member Robert Holzmann pointed out that historically, ECB tends to follow Fed's policy adjustments with a delay, typically around half a year.

"Typically the Fed always in the last few years has always gone first by about half a year so I would assume, ceteris paribus, as things are, that we would also follow with delay," he stated, indicating a likelihood that ECB would not preempt Fed in cutting its policy rates.

The Governing Council member also highlighted ongoing inflation risks, particularly from geopolitical tensions affecting shipping routes in the Red Sea. Holzmann cautioned that these factors could contribute to persistent inflationary pressures.

He specifically mentioned the possibility of an escalation in the Red Sea conflict affecting oil prices, a scenario that, while slim, poses a real risk to inflation and economic stability.

Holzmann also expressed skepticism towards market expectations for significant policy easing in Eurozone this year. He warned that market bets for 90 basis points of easing "may be much too high".

ECB Survey: Consumer inflation expectations for next tear rise to 3.3%

ECB's Consumer Expectations Survey for January showed that inflation expectations for the upcoming year have seen a slight uptick, increasing by 0.1% to 3.3%, while the forecast for three years ahead remains steady at 2.5%.

On a more optimistic note, the survey indicates a slight improvement in expectations for economic growth over the next year. The mean expectation for economic growth has become less negative, adjusting from -1.3% to -1.1%.

Furthermore, the expected mean unemployment rate for the next 12 months shows a slight decrease, moving from 10.8% to 10.6%.

German Ifo edges up to 85.5, stabilizing at a low level

German Ifo Business Climate ticked up from 85.2 to 85.5 in February, matched expectations. Current Assessment Index is unchanged at 86.9, a touch below expectation of 87.0. Expectations Index rose slightly from 83.5 to 84.1, above expectation of 83.8.

By sector, manufacturing fell from -15.8 to -17.4. Services rose from -4.8 to -4.1. Trade fell from -29.7 to -30.87. Construction rose from -35.8 to -35.4.

Ifo said that the German economy is "stabilizing at a low level".

New Zealand's retail woes deepen with eighth consecutive quarterly decline

New Zealand's retail sales volumes dropped by -1.9% qoq, a figure far below the expected decline of -0.2% qoq. This also marked the eighth consecutive quarter of contraction. Excluding auto sales, the decline was marginally less severe but still substantial at -1.7% qoq, again well below the anticipated -0.1% qoq decrease.

Melissa McKenzie, business financial statistics manager, highlighted the extent of the downturn, noting that "Ongoing falls in retail activity over the last two years were marked by a fall in most industries in the December quarter."

The contraction in retail sales was widespread, with 14 out of 15 retail industries reporting lower sales volumes compared to the previous quarter. The most significant downturns were observed in motor vehicle and parts retailing, which fell by -2.5%, food and beverage services, which saw a -2.4% decline, and fuel retailing, which dropped by -3.6%.

In terms of retail sales value, there was a qoq decrease of -1.5%, with ten of the sixteen regions experiencing lower seasonally adjusted sales values.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2612; (P) 1.2661; (R1) 1.2710; More...

GBP/USD bounces notably today but stays below 1.2708. Intraday bias remains neutral first. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q4 | -1.90% | -0.20% | 0.00% | -0.80% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | -1.70% | -0.10% | 1.00% | 0.40% |

| 00:01 | GBP | GfK Consumer Confidence Feb | -21 | -18 | -19 | |

| 07:00 | EUR | Germany GDP Q/Q Q4 F | -0.30% | -0.30% | -0.30% | |

| 09:00 | EUR | Germany IFO Business Climate Feb | 85.5 | 85.5 | 85.2 | |

| 09:00 | EUR | Germany IFO Current Assessment Feb | 86.9 | 87 | 87 | 86.9 |

| 09:00 | EUR | Germany IFO Expectations Feb | 84.1 | 83.8 | 83.5 |

ECB’s Lagarde watches Q1 wage talks for clues on lasting disinflation

ECB President Christine Lagarde described Q4 wage figures as "obviously encouraging numbers". However, she underscored the importance of caution, stating that the Governing Council needs to gain "more confidence" in the sustainability of the disinflationary process currently underway.

Lagarde also pointed to ongoing wage negotiations across various sectors and employee groups, expected to conclude in Q1, with data becoming available in May. The outcomes of these negotiations are anticipated to be a critical factor in the ECB's assessment of the inflationary outlook.

"Those numbers will — especially if they continue to be encouraging — will be important for us to assess going forward in order to reach confidence," Lagarde remarked in a press conference today.

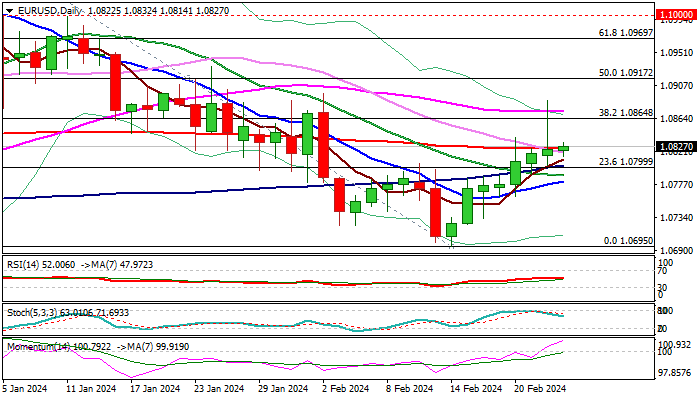

EUR/USD: Final Close Above 200DMA to Strengthen Near Term Structure

The Euro is holding within a narrow range on Friday but keeps slight bullish bias on strong positive momentum and the pair being on track for the first bullish weekly close in five weeks.

On the other hand, multiple failure to clear 200DMA barrier (1.0824) and Thursday’s strong upside rejection which left daily candle with long upper shadow, weighs on near-term action.

Improved German business climate in February (Ifo report) and Q4 GDP in line with expectations, contribute to supportive factors for the single currency.

Markets will focus on today’s close with fresh bullish signal expected on eventual close above 200DMA which will open way for retest of barriers at 1.0864/74 (Fibo 38.2% of 1.1139/1.0695 / 55DMA) and possibly spark stronger bullish acceleration on clear break higher.

Caution on repeated failure at 200DMA which will initially signal prolonged sideways mode while the price action stays above daily Tenkan-sen (1.0791).

Res: 1.0864; 1.0874; 1.0897; 1.0917.

Sup: 1.0814; 1.0791; 1.0768; 1.0740.

New Zealand Dollar Edges Lower After Soft Retail Sales

The New Zealand dollar has been on a roll but is in danger of snapping a seven-day rally during which it gained over 2% against the US dollar. NZD/USD is trading in the European session at 0.6185, down 0.16%.

New Zealand retail sales decline by 1.9%

Another retail sales report, another decline. New Zealand retail sales fell by 1.9% q/q in the fourth quarter of 2023, marking the eighth straight quarter of decline in retail spending. This was much lower than the revised 0.8% decline in Q3 and the market estimate of -0.4%.

The downswing was felt across the economy, as 14 of 15 retail industries recorded a fall in retail activity. On an annualized basis, retail sales slid 4.1%, down from -3.4% in Q3 and below the forecast of -3.6%, the fifth straight quarter of decline.

The weak data indicates that consumer spending is sputtering and that could mean New Zealand’s economy is in a recession. GDP growth contracted in the third quarter by 0.3% and if Q4 also records negative growth would meet the definition of a technical recession.

The retail sales release is doubly significant as it is the final key release before the Reserve Bank of New Zealand meets on February 28th. Governor Orr has not ruled out further rate hikes as part of a pushback against market expectations for a rate cut in mid-2024. Still, a rate hike doesn’t seem likely, especially after the weak retail sales report. The RBNZ has maintained the cash rate at 5.50% since April 2023 and it would be a major surprise if it does not hold rates next week.

NZD/USD Technical

- NZD/USD is putting pressure on resistance at 0.6211. Above, there is resistance at 0.6270

- 0.6168 and 0.6109 are providing support