Sample Category Title

Week Ahead – US CPI in the Spotlight as Dovish Fed Bets Fade

- All eyes on US CPI on Tuesday after run of strong data

- Retail sales on the agenda too for the US dollar

- Pound on standby for UK data flurry, including CPI and GDP

- Japanese GDP and Australian employment coming up too

Will US CPI remain sticky?

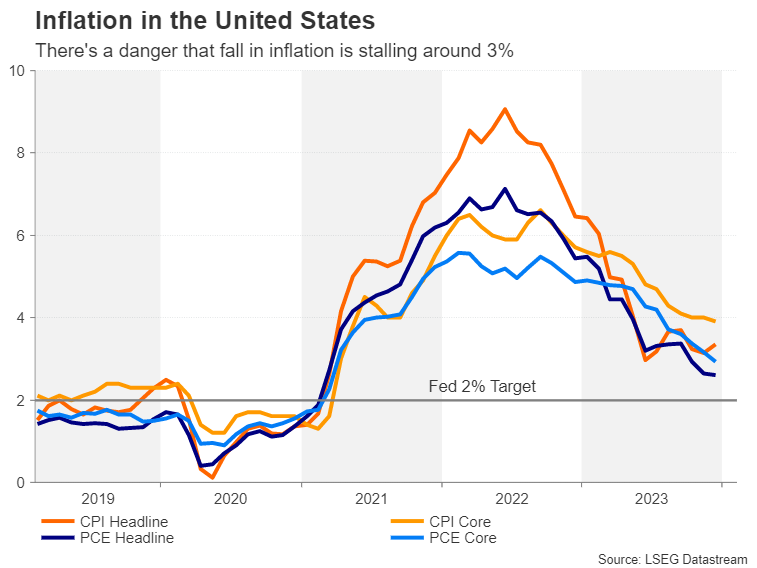

Inflation in the United States has generally been trending lower but the progress to get it all the way down to 2% has stalled in recent months, at least according to the CPI metric. Whilst Fed officials are optimistic that price measures will continue to head lower over the next few months, the resilience of the US economy is proving to be a thorn in the side of the Fed, as strong domestic demand increases the odds of inflationary pressures brewing again, particularly if there’s a significant re-acceleration in wage growth.

The consumer price index rose to 3.4% y/y in December, having been hovering above 3.0% since last July. There was somewhat better news for core CPI, which eased below 4.0% y/y for the first time since May 2021.

The picture for PCE inflation – the Fed’s preferred measure – is a little more encouraging, especially on an annualized basis. Headline PCE stood at 2.0% and core PCE at 1.9% on a six-month annualized basis in the last two months of 2023. This may have contributed to the markets’ exuberance in anticipating an imminent dovish pivot by the Fed.

However, Fed officials have overwhelmingly signalled that a rate cut may be some time away, giving the US dollar a leg up as investors priced out a March move.

Tuesday’s CPI print could be crucial in determining whether easing expectations will be pushed back further, as investors still see a strong likelihood of a rate cut in May. Forecasts suggest CPI stayed unchanged at 3.4% y/y in January.

US economy might be running hot again

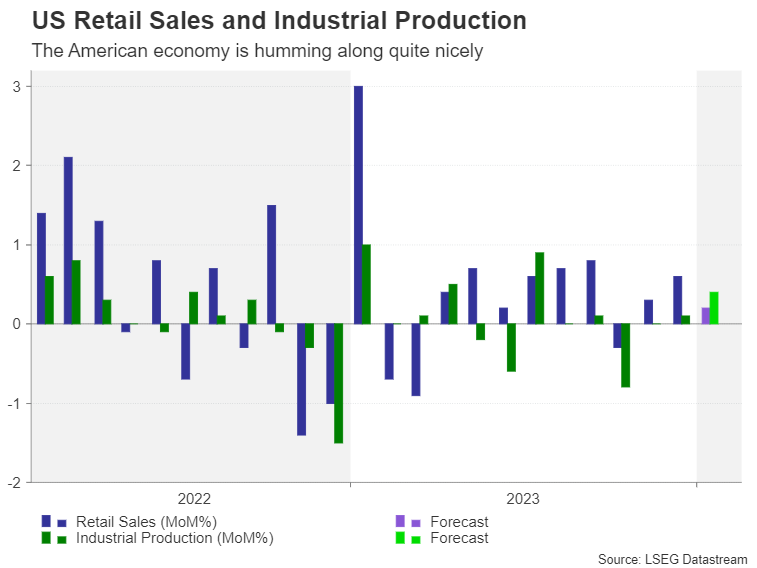

But the worry isn’t just inflation not coming down fast enough. The US economy appears to have enjoyed a pickup in activity in January so Thursday’s retail sales numbers will be vital too. The consensus estimate is for a 0.2% m/m increase, pointing to a cooldown from December.

In other data, the Philly Fed manufacturing index is also due on Thursday along with industrial production figures for January. Wrapping up the week on Friday are housing starts, building permits, producer prices and the University of Michigan’s preliminary consumer sentiment survey.

Pound to seek direction from UK CPI and GDP data

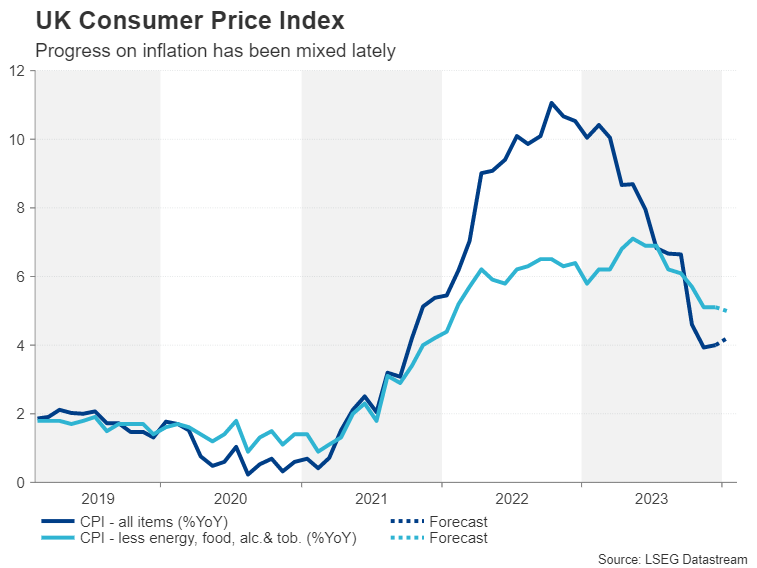

Inflation in the UK fell rapidly at the end of 2023 before edging up slightly. If both headline and core CPI resume their decline in January, this would come as a relief for the Bank of England but probably not for the pound. However, only the core measure is forecast to tick lower and headline CPI is expected to climb again to 4.2% y/y.

Although BoE policymakers have been pushing back on market expectations of an early rate cut, investors could ratchet up their bets if there’s a surprise drop in inflation.

But like in the US, it’s not just about the inflation picture as the economy has also been performing somewhat better than anticipated. UK GDP contracted by 0.1% in the three months to September, raising fears about a recession. But Q4 data due on Thursday is expected to show that the UK economy avoided a recession and recorded flat growth during the period.

Meanwhile, retail sales numbers will be watched on Friday for signs that consumer spending is recovering following an upbeat services PMI.

Not to forget about the labour market where wage growth has only just started to moderate. The employment report for December is out on Tuesday and any unexpected strength in the jobs market could dampen rate cut bets, lifting the pound.

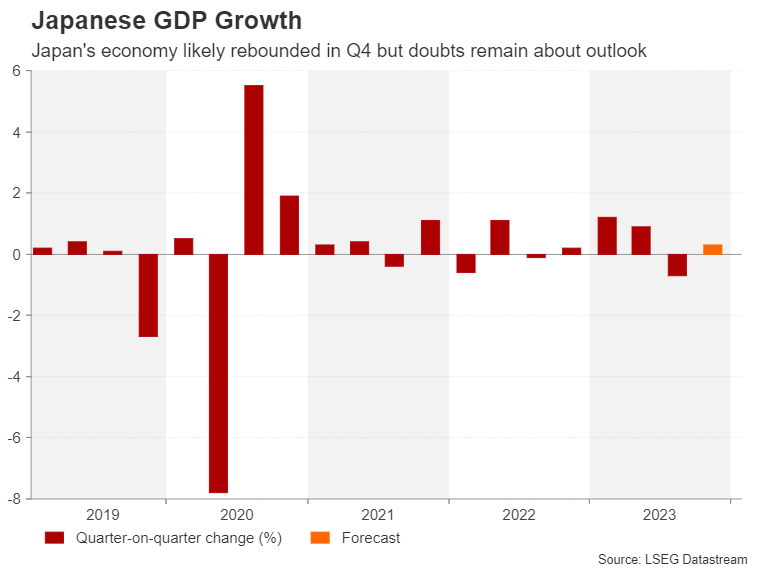

Japanese economy probably returned to growth in Q4

In Japan, the focus will be on the nation’s Q4 GDP readings on Thursday. After suffering a steeper-than-expected contraction in the third quarter of last year, economic growth is forecast to have rebounded by 0.3% q/q in the final three months of 2023.

If Thursday’s figures disappoint, doubts about the strength of the recovery are likely to persist as recent data has been rather mixed amid subdued consumption, although higher exports probably boosted GDP in Q4.

The Bank of Japan is hoping that this year’s ‘Shunto’ wage negotiations will spur pay growth and generate more sustainable inflation. But this could be a hard target to achieve even if the BoJ is confident enough to project it, so a sound economic backdrop is essential in adding credibility to its forecasts.

The yen could come under pressure on the back of a softer-than-expected bounce back, but an upside surprise cannot be ruled out either as most businesses have been positive in the BoJ’s most recent Tankan surveys.

Aussie and kiwi on a slippery slope

The Australian dollar hasn’t had a very good start to 2024 even though the Reserve Bank of Australia is expected to be one of the last to cut rates this year. China’s economic woes and the resurgent US dollar have offset the RBA’s relatively more hawkish stance.

An improvement in the labour market might lessen the aussie’s pain. Employment fell in December, taking markets by surprise. But Thursday’s jobs numbers are expected to provide some relief as the Australian economy likely added 30k jobs in January. This could pull the aussie away from multi-month lows versus the greenback as investors would pare back their bets of how many times the RBA would cut rates this year.

Chinese markets will be shut for the entire week for the Lunar New Year celebrations so the aussie could be more sensitive than usual to domestic data.

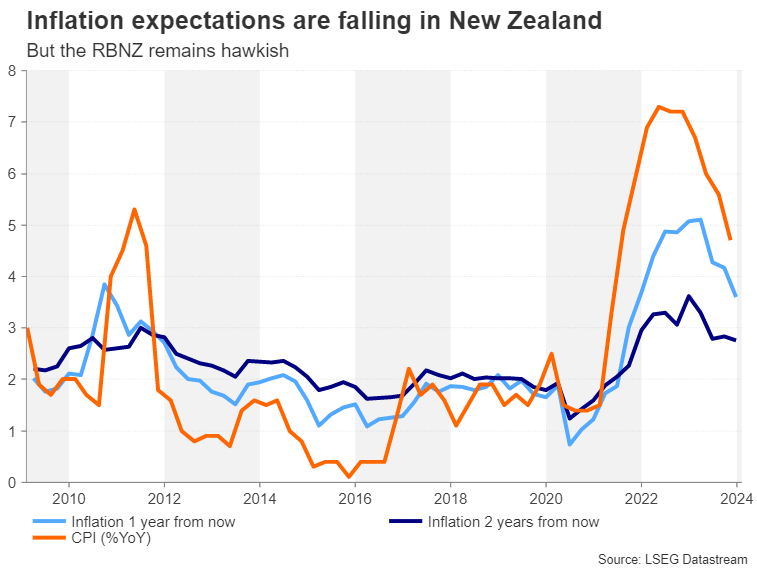

Across the Tasman Sea, the New Zealand dollar will be keeping an eye on the latest inflation expectations survey on Tuesday that the Reserve Bank of New Zealand publishes quarterly.

In the last report, one-year inflation expectations had fallen to 3.6% and two-year ones to 2.8%. Should expectations about future inflation maintain their downward path, this could undermine any fresh hawkish rhetoric from RBNZ Governor Adrian Orr when he speaks on Thursday.

Nevertheless, any downside reaction in the kiwi would likely be short lived as the RBNZ would need to see more evidence of abating inflation before turning dovish.

Weekly Focus – Higher Rates and Central Bank Pricing

Focus this week has been on the increase in interest rates and the decline in market expectations for central bank rate cuts that were initiated by the strong US job market report late Friday last week. While the headline numbers were very strong, we stress that the underlying details were softer. Average weekly hours worked declined to the lowest level since 2010 (when excluding March 2020) in a sign that the labour market is not as tight as one could fear. Also, average weekly earnings growth was negative month-on-month. Yet, markets have scaled back interest rate cut expectations for 2024 for the Fed and ECB from almost six 25bp cuts to four and a half cuts since Friday last week. These moves were also supported by speeches from Powell and ECB's Schnabel. Powell reiterated that the Fed would most likely not cut rates in March and backed the December dot plots of three cuts this year. Schnabel warned against the still present upside risks to euro area inflation that could cause inflation to flare up again.

The US ISM services index rose more than expected in January to 53.4 (cons: 52.0, prior: 50.6) and the prices paid subindex rose to the highest level since February 2023. The ISM services index has been very volatile and the rise in the price index contrasts the signal from PMI services. Hence, one should not put too much emphasis on a single print. However, in the big picture it is still nearly all recent US data releases that have surprised to the upside.

Chinese inflation fell more than expected in January with CPI at -0.8% y/y vs expectations of -0.5% y/y (previous was -0.3% y/y). Inflation was especially pulled lower by food prices. However, core CPI also declined to 0.4% y/y from 0.6% y/y in December. While deflation is still not widespread in core measures, the falling core inflation is clearly a symptom of a weak economy with too soft demand relative to supply.

In the euro area, retail sales fell 1.1% m/m in December in a sign that euro area consumers were still cautious about spending in December like the entire year. Given the low current consumption share, strong savings, high employment, and rising real wages there is room for private consumption to pick up in 2024. Yet, we likely still need to see a more pronounced increase in consumer confidence before private consumption picks up.

In Japan, the average wage growth for December came in at 1.0% y/y, which was stronger than in November, albeit lower than the 1.3% expected by consensus. Wage growth is key to the outlook for the Bank of Japan's (BoJ) monetary policy and possible tightening. We expect that we will probably have to wait until spring wage negotiations for wages to start moving much higher, and thereby for BoJ tightening to start tightening monetary policy. In the UK, wage growth eased in January in a comforting sign for the BoE although the wage pressure is still strong, and the labour market remains tight.

Focus next week is on US Inflation. The January US CPI print will be key in determining whether the recent upside surprises in US macro translates into higher price pressures. Also in the US, we look out for retail sales and the University of Michigan survey. From the UK we receive the job market report and January CPI. In the euro area, focus is on industrial production and German ZEW. Finally, in Japan we look out for 2023Q4 GDP.

Sunset Market Commentary

Markets

The US Bureau of Labor Statistics published its annual CPI revisions today. The same event last year showed some deviations from the initial outcomes large enough that they casted doubt on the speed of the disinflationary process. This time around, however, the hyped-up release lived up to its reputation as a non-event. Both the headline and core measure saw some adjustments but they were minor and two-sided. Having last year’s unpleasant surprise in mind, financial markets breathed a sigh of relief. US Treasury yields dropped from their intraday day highs in a kneejerk reaction before reversing course and resume today’s ride higher. They currently add between 2.4-3.7 bps across the curve. German Bunds underperform in an inversion move. Yields rise 6 bps at the front with the 2-y feeling ready for a test of the YtD high. Central bank speech was limited to ECB’s Kazaks nothing that inflation has fallen strongly, making 2024 the year of rate cuts. While the precise timing depends on the data, Kazaks said he isn’t as optimistic as markets on an inaugural cut in spring (euro area money markets price in about 35 bps of cuts by June). Speaking of data, market attention is gradually shifting towards Tuesday’s US CPI reading (January). Analysts expect the headline figure to ease from 3.4% to 2.9% and see a more gradual decline in core CPI from 3.9% to 3.7%. With all but every Fed member basically ruling out a March cut, all eyes are turned to the May policy meeting. A rate cut then (not our preferred scenario) is for about 80% discounted and could in theory gain further traction in case of a number in line or below consensus. Other important US data include January retail sales on Thursday and University of Michigan consumer confidence on Friday. The UK, however, is taking center stage with an extended economic update, spanning the labour market, retail sales and especially January CPI & Q4 GDP numbers. This may well be the trigger needed to unlock EUR/GBP from its current impasse. The pair is unable to escape from the laws of gravity, keeping it in an extremely tight trading range since mid-January. EUR/GBP looks especially vulnerable for a break to the downside with the key technical reference at 0.8492 the only thing standing in the way for a return to 0.834 (August 2022 correction low).

News & Views

Inflation in Hungary for the first time since March 2021 returned within the 3.0% +/- 1.0% target band of the MNB. Prices rose 0.7% M/M but this still reduced the Y/Y measure from 5.9% to 3.8% (consensus 4.3%), lower than the mean value in the December inflation report. According to the MNB, the positive surprise was primarily due to lower than expected fuel and processed food prices. In a separate assessment the National Bank of Hungary reckoned that measures of core inflation also declined. Core inflation ex indirect taxes eased from 7.6% to 6.1%. CPI ex processed food slow from 9.6% to 8.1%. Core inflation was also slightly below the MNB expectations while the rises in prices of demand-sensitive items was in line with the projection. On a more general level, the MNB sees a general slowdown in inflation, fuelled by the combined effect of tight monetary policy, the government’s measures to strengthen competition, subdued demand, base effects and a significantly lower external cost environment. The MNB sees the continued slowdown in underlying inflation illustrated by the fact that three-month annualised core inflation and inflation were both below 3 percent. The 2-y Hungarian swap yield dropped 11 bps after. The data again raise the case for the MNB to step up the pace of rate cuts from 75 bps to 100 bps. However, this argument is in balance with the forint weakening close to the EUR/HUF 390 barrier Admittedly, the forint didn’t decline any further today (EUR/HUF 388.5).

According to data published by the Swedish Riksbank today, the Bank reached the targeted amounts aimed at reducing the currency risk on its foreign exchange reserves. In September last year, it started the process of hedging the countervalue of USD 8 bln and euro EUR 2 bln of reserves. The procedure was expected to take between 4 and 6 months. The amounts of hedged funds were reached in the week of January 26, completing the program. The procedure officially wasn’t intended to serve as a currency intervention to support the krone. At the same time, it was seen as a tool to limit losses in reserves if the krone, which was seen as trading at a weak level, would appreciate. EUR/SEK currently trades at 11.28, compared to levels close to EUR/SEK 12 at the end of September.

USD/CAD Dips as Canadian Employment Shines

- Canadian employment jumps, wage growth falls

- USD/CAD edges lower

The Canadian dollar has climbed higher in the North American session after the release of Canada’s December employment report. In the North American session, USD/CAD is trading at 1.3432, down 0.20%.

Canada’s job growth beats forecast

Canada usually posts employment reports on the same Friday as the US, but had the stage all to itself today, as the US posted its job report last week. The news was good as employment jumped by 37,300 in January, smashing the market estimate of 15,000. The December reading was revised upwards to 12,300 from the initial estimate of just 0.1 thousand. The unemployment rate ticked lower to 5.7%, down from 5.8% in December and below the market estimate of 5.7%. As well, average hourly earnings eased to 5.3% y/y in January, compared to 5.7% a month earlier.

The Bank of Canada will be carefully monitoring the jobs data. Employment growth jumped, which points to a stronger labour market, but at the same time wage growth dropped. Wages are a key driver of inflation and today’s decline will support the BoC continuing to pause and not cut rates until the middle of the year or later. The BoC is content to continue its “higher for longer” stance and let high rates continue pushing inflation lower. The central bank’s top priority remains bringing down inflation to the 2% target, but businesses and consumers, especially homeowners, are groaning under the weight of elevated rates and are looking for some relief from the BoC.

The Federal Reserve continues to push back against rate cut expectations in March. This week, a host of Fed members delivered the message that inflation is heading lower but the Fed remains cautious and isn’t yet ready to lower rates, as the battle against inflation is not yet won. The markets have taken note of the Fed’s pushback and have pared expectations of a rate cut in March to 17%, down from over 70% in December, according to the CME’s Fed Watch tool.

USD/CAD Technical

- USD/CAD tested support at 1.3434 earlier. Below, there is support at 1.3392

- 1.3509 and 1.3551 are the next resistance lines

Canada’s Labour Market Strengthens in January, But Details Less Constructive

The Canadian labour market added 37.3k positions in January, with full-time employment down 11.6k and part-time employment up 48.9k.

The unemployment rate declined 0.1 percentage point to 5.7%, helped by a 0.1 percentage point to decline in the labour force participation rate to 65.3%. Despite a massive 126k increase in the population in January, only 18k net-new people entered the labour force, taking participation lower.

Employment by sector showed gains in wholesale/retail trade (+31k) and finance, insurance, real estate, rental and leasing (+28k). There was a notable decline in accommodation and food services (-30k).

Lastly, total hours worked rose 0.6% month-on-month and wages were down 5.3% year-on-year (from 5.7% on December).

Key Implications

The headlines for today's job report suggested surprising strength from the Canadian labour market. However, while falling unemployment is a good sign for the strength of the job market, the underlying details were weak. All the job gains were part-time, with the vast majority coming from cyclically insensitive public sector hiring. This along with the regular seasonality issue with January job reports (remember the head fake we got last January?), we'd argue that it is not the type of report the makes us think the Canadian labour market is in for a renewed upturn. Case in point, the lower unemployment rate was helped by weaker participation – not a typical sign of a strong labour market.

The Bank of Canada won't change course after today's report. The data are simply too volatile and don't paint a clear picture of the state of the Canadian economy. This leaves the BoC to continue fixating on the state of inflation. With headline and core inflation rates stuck around the mid-3% level, the Bank needs to see improvement before it can be convinced that it will reach its goal of price stability. This has markets pushing back on the timing of rate cuts, with June or July as the most likely start date.

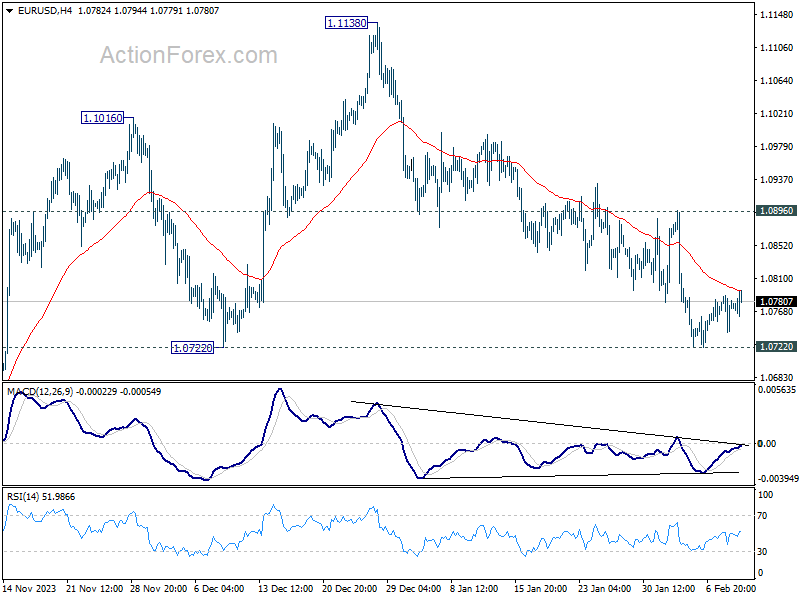

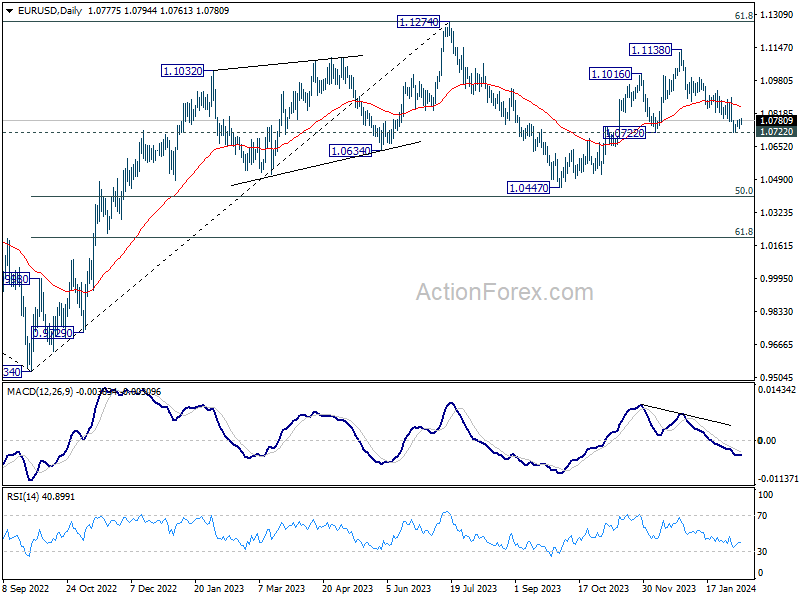

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0750; (P) 1.0770; (R1) 1.0797; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. On the downside, decisive break of 1.0722 will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low. On the upside, break of 1.0896 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

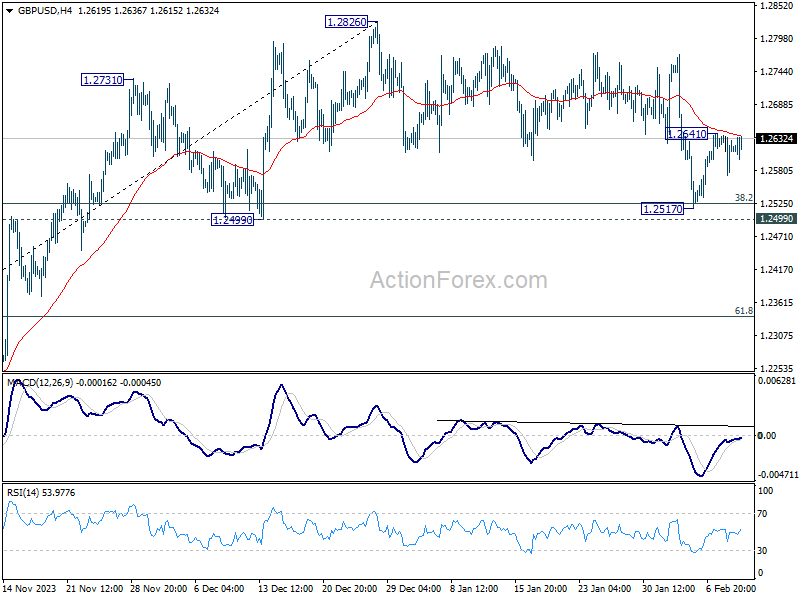

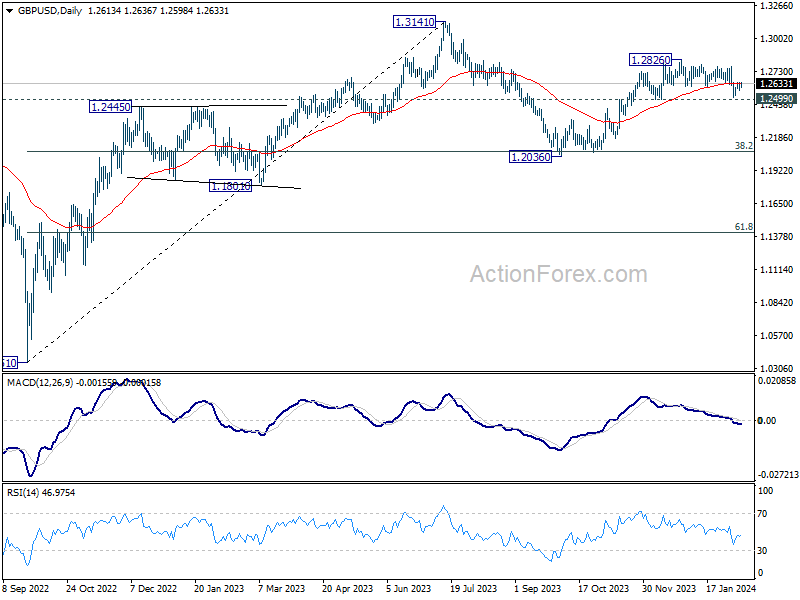

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2580; (P) 1.2609; (R1) 1.2647; More...

Intraday bias in GBP/USD stays neutral at this point. On the upside, above 1.2641 will resume the rebound from 1.2517 to retest 1.2826 high. On the downside, however, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's still in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

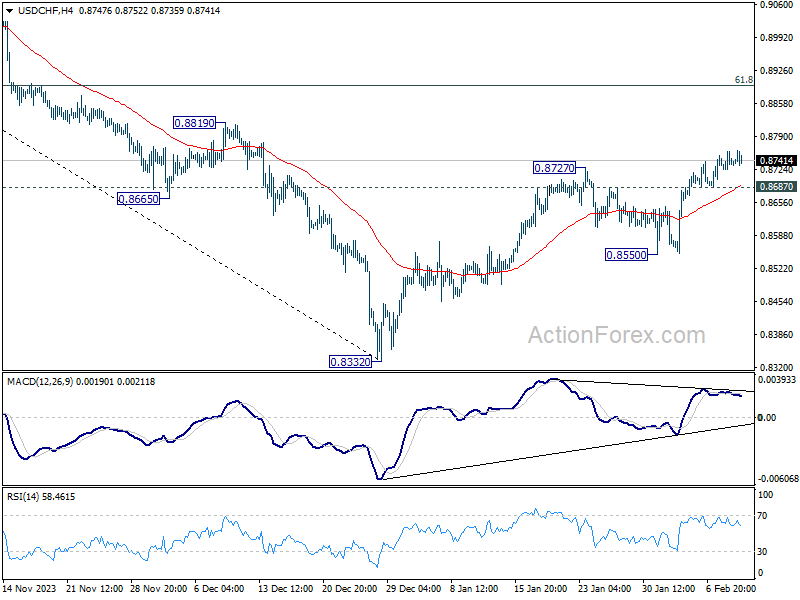

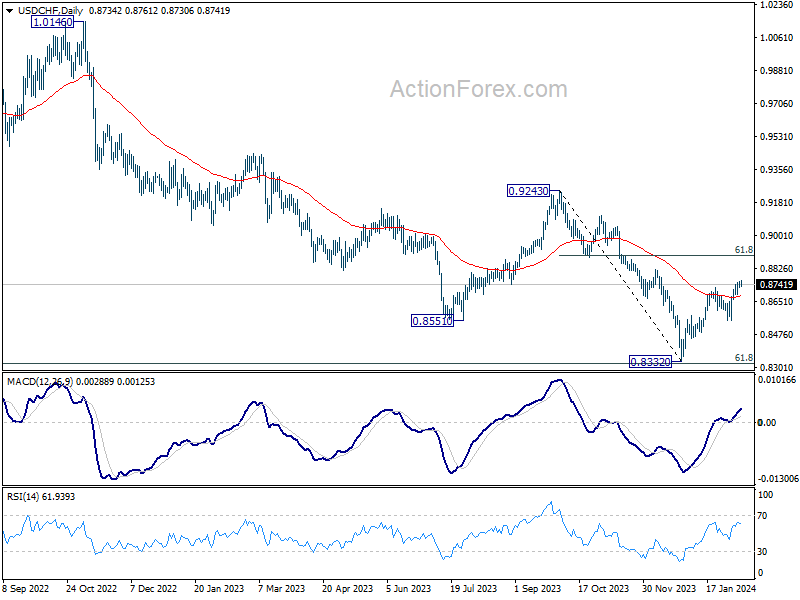

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8741; (R1) 0.8757; More....

Intraday bias in USD/CHF remains on the upside at this point. Current rise from 0.8332 would target 61.8% retracement of 0.9243 to 0.8332 at 0.8995 next. On the downside, below 0.8687 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.8550 support holds.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8677) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.

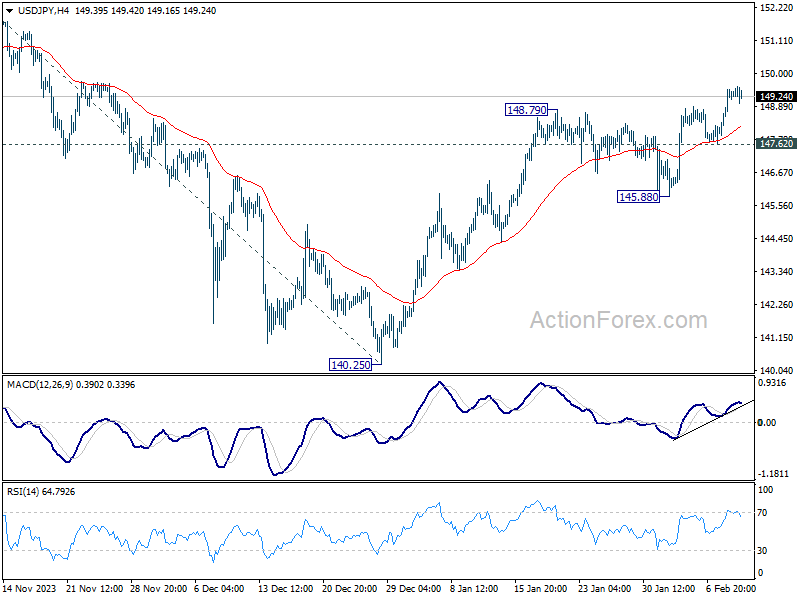

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.35; (P) 148.91; (R1) 149.89; More...

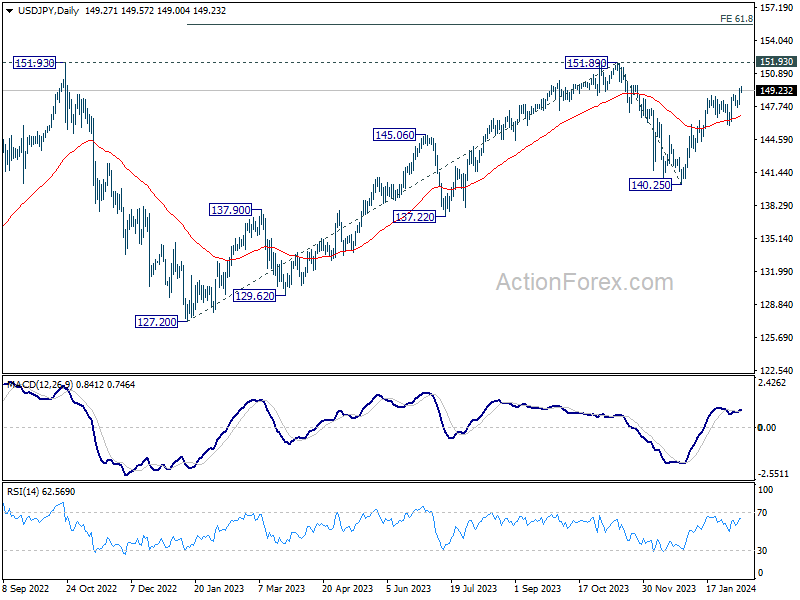

USD/JPY's rally from 140.25 is still in progress and intraday bias stays on the upside. Further rally would be seen to retest 151.89/93 key resistance zone. Decisive break there will confirm resumption of larger up trend. On the downside, below 147.62 minor support will turn intraday bias neutral first. But near term outlook will remain cautiously bullish as long as 145.88 support holds.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

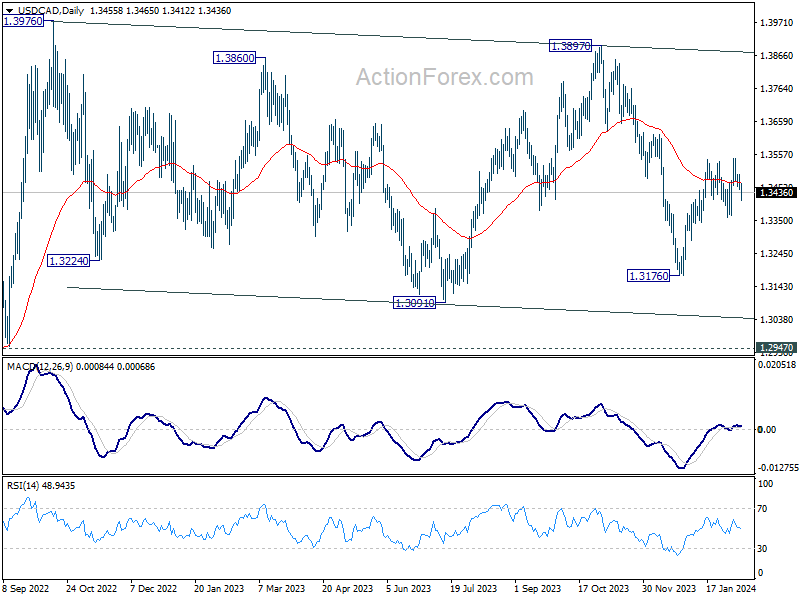

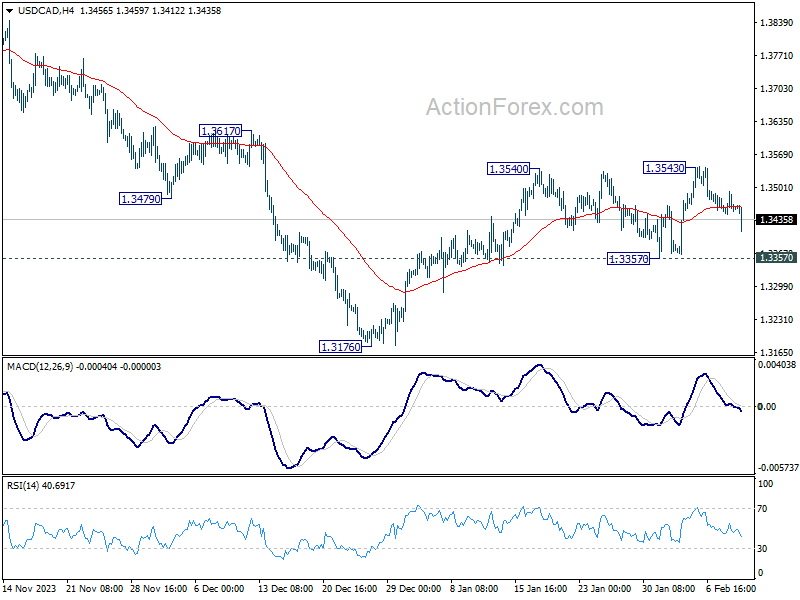

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3440; (P) 1.3467; (R1) 1.3485; More...

USD/CAD dips notably in early US session but stays well above 1.3357 support. Intraday bias remains neutral first and further rally is in favor. On the upside, decisive break of 1.3540/3 will resume the rise from 1.3176. That will also revive that case that whole fall from 1.3897 has completed, and target this resistance. Nevertheless, firm break of 1.3357 support will argue that rebound from 1.3176 has completed, and target this low for resuming whole fall from 1.3897.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.