Sample Category Title

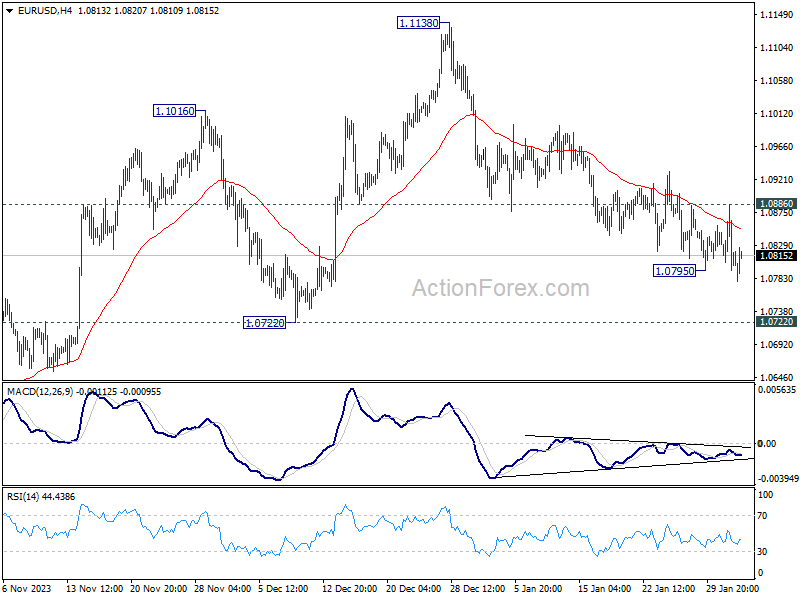

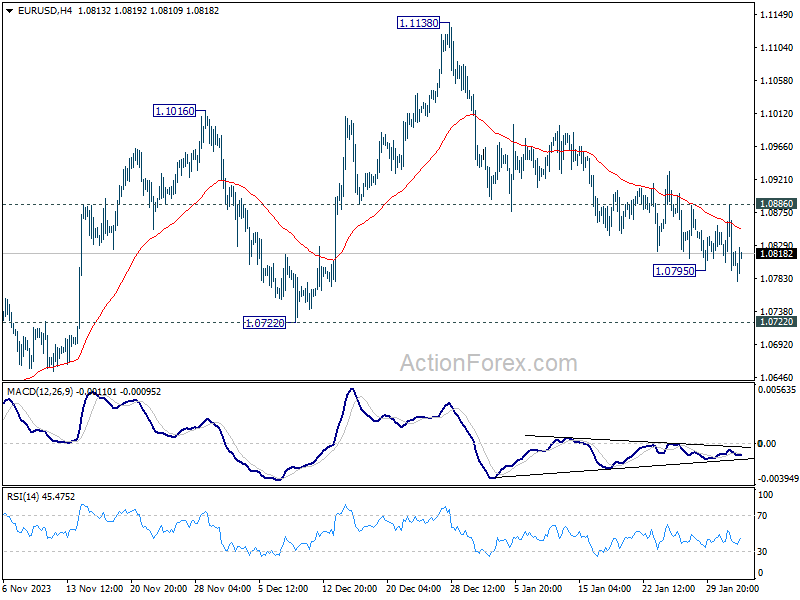

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0820; (P) 1.0838; (R1) 1.0865; More...

Intraday bias in EUR/USD is back on the downside with breach of 1.0795 temporary low. Fall from 1.1138 is trying to resume to 1.0722 structural support. Decisive break there will argue that whole rise from 1.0447 has completed, and target this low. On the upside, however, break of 1.0931 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

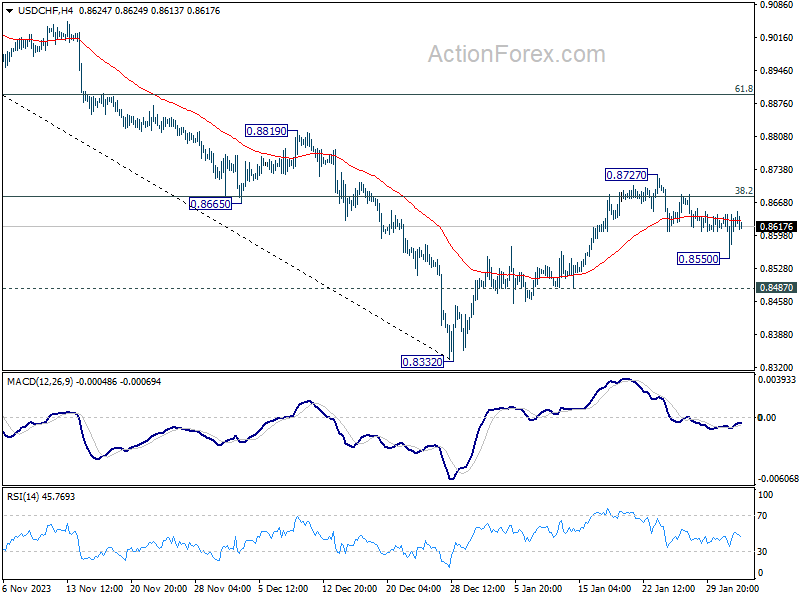

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8562; (P) 0.8603; (R1) 0.8655; More....

Intraday bias in USD/CHF remains neutral at this point. On the downside, below 0.8550 will resume the fall from 0.8727 for 0.8487 support. Break there will argue that rebound from 0.8332 has completed, and bring retest of this low. On the upside, firm break of 0.8727 will resume the rebound to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 instead.

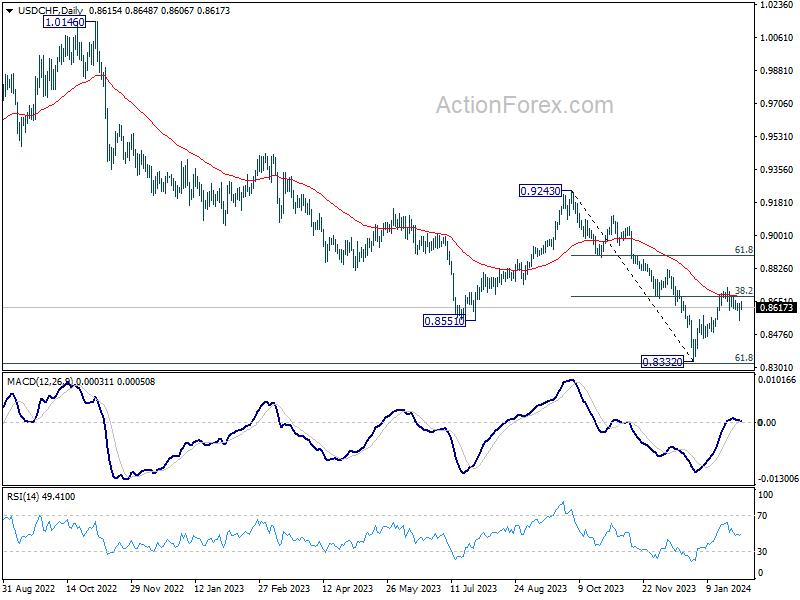

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

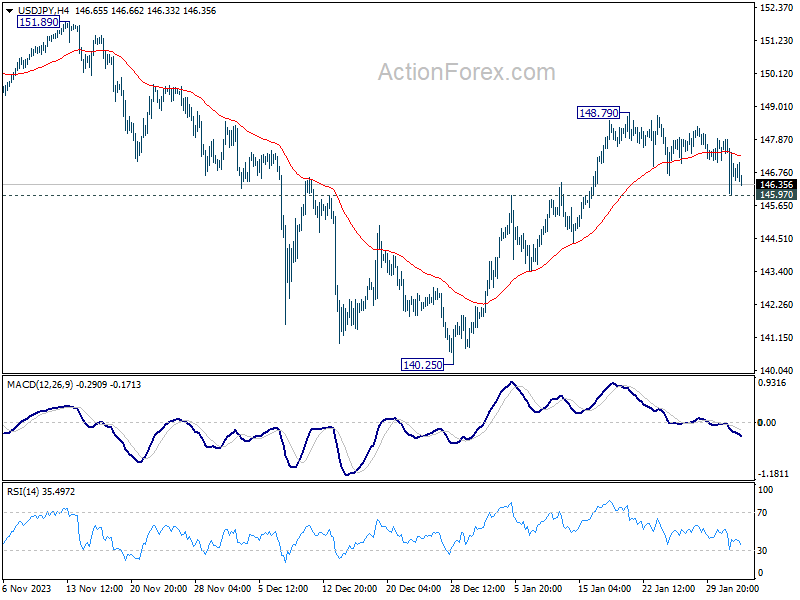

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.16; (P) 147.54; (R1) 147.99; More...

USD/JPY is still holding above 145.97 resistance turned support. Intraday bias stays neutral at this point, and further rally is still in favor. As noted before, corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone. However, firm break of 145.97 will dampen this view, and turn bias to the downside for deeper fall towards 140.25.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 142.49) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

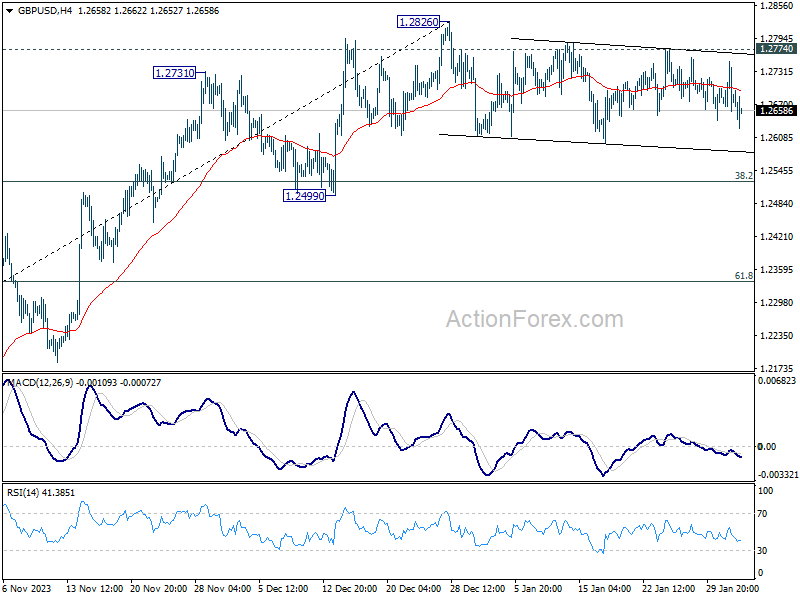

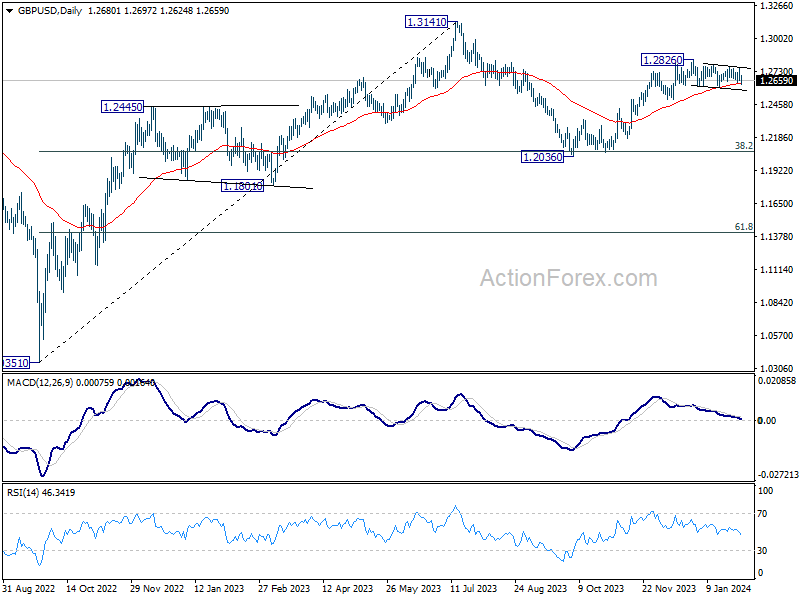

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2646; (P) 1.2699; (R1) 1.2739; More...

No change in GBP/USD's outlook and intraday bias remains neutral. Consolidation from 1.2826 is extending and deeper fall cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2774 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

BoE’s Three-Way Split Vote Muddles Sterling’s Path, Yen Strength Continues

Sterling is currently trading with indecisiveness following BoE's rate decision, which has provoked mixed reactions in the markets. The decision, notable for its combination of hawkish and dovish signals, resulted in a rare three-way voting split—the first occurrence since 2008—with two members favoring a rate hike, one a cut, and the rest opting for no change. This split highlights the complexities and differing perspectives within the MPC.

BoE has notably relinquished its tightening bias, and significantly lowering the conditioned rate path, which now sees interest rate to fall to 3.9% by the onset of next year. Despite this dovish tilt, the bank simultaneously revised its inflation forecasts upward, suggesting that inflationary pressures will persist above target until 2026. Governor Andrew Bailey's remarks were also clear in that the central bank is not yet in a position to contemplate rate reductions.

Meanwhile, Japanese Yen continues to assert its strength, capitalizing on weakening global benchmark yields. US 10-year yield is teetering on the brink of falling below the 3.9% mark, while its UK counterpart exhibits a similar downward trajectory. German 10-year yield, is merely holding its ground, lacking the momentum for a significant recovery.

Euro, the second strongest for the day after Yen, finds itself buoyed slightly by higher than expected inflation readings in both the headline and core CPI in Eurozone. Dollar, trailing as the third strongest, faces challenges in making decisive progress. In contrast, Australian Dollar is positioned as the weakest, followed by New Zealand Dollar. Sterling and Canadian Dollar, though weaker, are not as severely impacted, while Swiss Franc displays mixed performance.

Technically, while EUR/USD dipped again earlier in the day, it quickly found its way back into familiar range. Downside momentum is clearly waning as seen in 4H MACD. It's now a crucial decision point for traders on whether to push EUR/USD through 1.0722 key structural support to confirm near term bearish reversal. Or, the bears will just give up and let EUR/USD bounce through 1.0886 minor resistance to confirm short term bottoming. This decision is likely to become clear shortly.

In Europe, at the time of writing, FTSE is up 0.18%. DAX is down -0.07%. CAC is down -0.54%. UK 10-year yield is down -0.0271 at 3.774. Germany 10-year yield is up 0.009 at 2.182. Earlier in Asia, Japan 10-year JGB yield fell -0.0412 to 0.695. Nikkei fell -0.76%. Hong Kong HSI rose 0.52%. China Shanghai SSE fell -0.64%. Singapore Strait Times fell -0.32%.

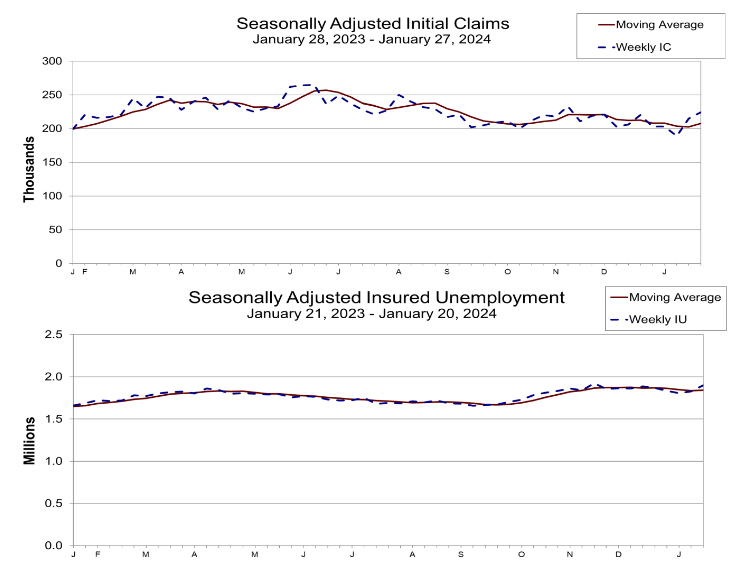

US initial jobless claims rises to 224k, abv exp 211k

US initial jobless claims rose 9k to 224k in the week ending January 27, above expectation of 211k. Four-week moving average of initial claims rose 5k to 208k.

Continuing claims rose 70k to 1898k in the week ending January 20. Four-week moving average of continuing claims rose 7.5k to 1841k.

BoE stands pat, two vote for hike, one for cut

BoE left the Bank Rate unchanged at 5.25% as widely expected. However, two MPC hawks (Jonathan Haskel and Catherine Mann) voted for another 25bps to 5.50%. Meanwhile, one dove (Swati Dhingra) voted for a 25bps cut to 5.00%. That resulted in a 6-3 vote for the decision.

Nevertheless, the central bank dropped tightening bias by omitting the language that "Further tightening in monetary policy would be required...." Instead, it's now "prepared to adjust monetary policy as warranted by economic data".

BoE will continue monitor a range of measures of "the underlying tightness of labour market conditions, wage growth and services price inflation."

CPI is projected to fall temporarily to 2% in Q2 2024, before rising again in Q3 and Q4. BoE sees CPI to be at to be at 2.8% in Q1 2025 (up from prior 2.5%), then 2.3% in Q1 2026 ( up from 1.9%), then 1.9% in Q1 2027 (new).

Four-quarter GDP growth is seen at 0.5% in Q1 2025 (up from 0.0%), the 0.8% in Q1 2026 (up from 0.6%), and 1.5% in Q1 2027 (new).

These are conditioned on a lowered market-implied path for Bank Rate that declines from 5.1% in Q1 2024 (prior 5.3%), then falls to 3.9% in Q1 2025 (down from 5.0%), and then 3.3% in Q1 2026 (down from 4.4%), and 3.2% in Q1 2027 (new).

UK PMI manufacturing finalized at 47.0, challenged by cost pressures and supply disruptions

UK PMI Manufacturing was finalized at 47.0 in January, up from December's 46.2. This modest improvement, however, did not signal an end to the sector's downturn, with continued contractions observed across key areas.

Rob Dobson, Director at S&P Global Market Intelligence, highlighted the pervasive nature of the contraction, noting declines in output, new orders, and employment across various manufacturing sub-industries. He pointed out that manufacturers are adopting a cost-cautious approach, focusing on cutting back on purchasing and stock holdings to improve efficiency, maintain cash flow, and protect margins in these challenging times.

The industry faces compounded difficulties due to the ongoing "Red Sea crisis", which is exacerbating supply chain disruptions. The rerouting of inputs from the Asia-Pacific region is leading to increased costs and longer supplier lead times, intensifying the strain on production schedules and amplifying inflationary pressures. This situation is particularly problematic as manufacturers grapple with weak domestic and international demand.

Eurozone CPI down to 2.8%, core falls to 3.3%, both above expectations

Eurozone CPI slowed from 2.9% yoy to 2.8% yoy in January, above expectation of 2.7% yoy. CPI core (excluding energy, food, alcohol & tobacco) slowed from 3.4% yoy to 3.3% yoy, above expectation of 3.2% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in January (5.7%, compared with 6.1% in December), followed by services (4.0%, stable compared with December), non-energy industrial goods (2.0%, compared with 2.5% in December) and energy (-6.3%, compared with -6.7% in December).

Eurozone's manufacturing PMI finalized at 46.6, persistent contraction with glimmers of hope in the south

Eurozone PMI Manufacturing was finalized at a 10-month high of 46.6 in January, up from December's 44.4. Despite this, caution is advised as the index still hovers below the critical expansion threshold. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlights that although there's been a consistent rise over the past three months, including in forward-looking indicators like new orders, the majority of the sub-indices, including the headline index, remain in the contraction zone.

This rebound in manufacturing is particularly evident in the "southern economies", with Greece leading at a 21-month high of 54.7 and both Spain (49.2) and Italy (48.5) showing encouraging trends. However, among the largest Eurozone economies, Germany, despite an 11-month high, remains in contraction at 45.5, and France's economic situation continues to be concerning, at 43.2.

The upward trend in sub-indicators such as stock of purchases, backlogs of work, and output, along with a growing optimism for higher output in the coming year, offers a glimmer of hope. This gradual recovery in the manufacturing sector, spearheaded by the southern economies, may serve as a crucial catalyst to pull the larger Eurozone economies out of the recessionary environment.

Japan's PMI manufacturing finalized at 48.0, depressed economy and escalating cost pressures

Japan's PMI Manufacturing was finalized at 48.0 in January, a minimal increase from December's 47.9, yet still indicative of ongoing challenges in the sector.

According to S&P Global, this figure represents a "modest deterioration" in the health of the manufacturing sector, marking a "sustained downturn" at the start of the year.

Usamah Bhatti of S&P Global Market Intelligence highlights the "depressed economic conditions" both domestically and globally as significant contributors to the sector's struggles. The data also shows notable declines in both output and new orders, with the latter experiencing a particularly sharp drop.

Manufacturers in Japan are also facing heightened pressures related to costs and supply. The cost burdens have been rising sharply, driven by increased prices of raw materials, labor, and fuel.

Additionally, supplier performance has deteriorated significantly, marked as the worst in three months. Issues such as delivery and logistical delays have been frequently mentioned, with some attributing these challenges to the ongoing disruption in the Red Sea.

China's Caixin PMI manufacturing unchanged at 50.8, economic challenges persist

China's Caixin PMI Manufacturing was unchanged at 50.8 in January, matched expectations. The sector showed modest production growth, although the overall sales expansion softened. Notably, this period marked the first rise in new export business in seven months, and business confidence reached a nine-month high. However, the employment sector continued to contract, and the market faced ongoing deflationary pressures.

Wang Zhe, Senior Economist at Caixin Insight Group, highlighted that despite the stability in manufacturing, the Chinese economy still grapples with "significant challenges", including weak demand, employment pressures, and subdued market expectations. He emphasized that these issues are yet to see a "fundamental shift reversal".

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2646; (P) 1.2699; (R1) 1.2739; More...

No change in GBP/USD's outlook and intraday bias remains neutral. Consolidation from 1.2826 is extending and deeper fall cannot be ruled out. But downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2774 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | -6 | -1 | ||

| 00:30 | AUD | Building Permits M/M Dec | -9.50% | 0.10% | 1.60% | |

| 00:30 | AUD | Import Price Index Q/Q Q4 | 1.10% | 0.60% | 0.80% | |

| 00:30 | JPY | Manufacturing PMI Jan F | 48 | 48 | 48 | |

| 01:45 | CNY | Caixin Manufacturing PMI Jan | 50.8 | 50.8 | 50.8 | |

| 08:30 | CHF | Manufacturing PMI Jan | 43.1 | 44.5 | 43 | |

| 08:45 | EUR | Italy Manufacturing PMI Jan | 48.5 | 47.3 | 45.3 | |

| 08:50 | EUR | France Manufacturing PMI Jan F | 43.1 | 43.2 | 43.2 | |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 45.5 | 45.4 | 45.4 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 46.6 | 46.6 | 46.6 | |

| 09:30 | GBP | Manufacturing PMI Jan F | 47 | 46.9 | 47.3 | |

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 6.40% | 6.40% | 6.40% | |

| 10:00 | EUR | Eurozone CPI Y/Y P | 2.80% | 2.70% | 2.90% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y P | 3.30% | 3.20% | 3.40% | |

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.25% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--1--6 | 2--0--7 | 3--0--6 | |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -20.00% | -20.20% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 26) | 224K | 211K | 214K | 215K |

| 13:30 | USD | Nonfarm Productivity Q4 P | 3.20% | 2.40% | 5.20% | 4.90% |

| 13:30 | USD | Unit Labor Costs Q4 P | 0.50% | 2.10% | -1.20% | -1.10% |

| 14:30 | CAD | Manufacturing PMI Jan | 45.4 | |||

| 14:45 | USD | Manufacturing PMI Jan F | 50.3 | 50.3 | ||

| 15:00 | USD | ISM Manufacturing PMI Jan | 47.7 | 47.4 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 45.6 | 45.2 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 48.1 | |||

| 15:00 | USD | Construction Spending M/M Dec | 0.50% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -202B | -326B |

US initial jobless claims rises to 224k, abv exp 211k

US initial jobless claims rose 9k to 224k in the week ending January 27, above expectation of 211k. Four-week moving average of initial claims rose 5k to 208k.

Continuing claims rose 70k to 1898k in the week ending January 20. Four-week moving average of continuing claims rose 7.5k to 1841k.

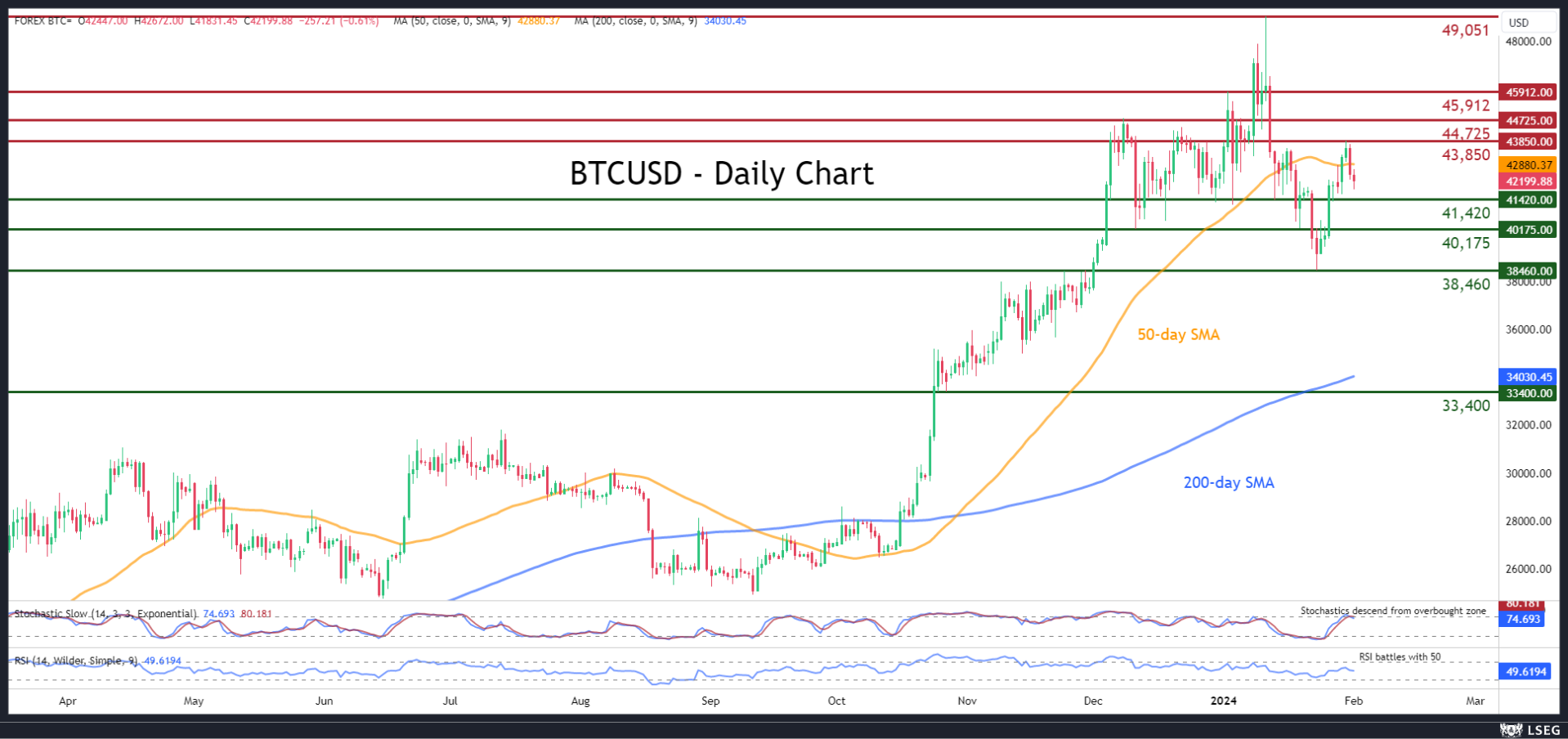

BTCUSD Drops Below 50-day SMA

- BTCUSD bounces off 2024 low and reclaims 40,000

- But price dips back below 50-day SMA after advance pauses

- Momentum indicators suggest weakening buying pressures

BTCUSD (Bitcoin) experienced a strong decline from its recent two-year peak of 49,051, dropping to as low as 38,460. Despite the price’s attempt for recovery, a new round of weakness has begun, with Bitcoin dropping below the 50-day simple moving average (SMA) following a rejection near 43,850.

If the slide resumes, the inside swing low of 41,420 could act as the first line of defence. In case of a downside violation, the price may face the December support of 40,175. Further declines might encounter strong support at the 2024 bottom of 38,460.

Alternatively, should bearish pressures abate, Bitcoin could surge towards the recent rejection region of 43,850. Conquering this barricade, the bulls might attack the December high of 44,725. A jump above the latter could shift the spotlight to 45,912.

In brief, BTCUSD has been losing ground in the near-term after its rebound met strong resistance. Nevertheless, a break above the 50-day SMA could revive the bulls’ hopes for a sustained recovery.

Australian Dollar Falls to 10-Week Low after Fed Decision

The Australian dollar is sharply lower on Thursday after the Fed policy meeting a day earlier. In the European session, AUD/USD is trading at 0.6514, down 0.78%. Earlier, the Australian dollar dropped as low as 0.6508, its lowest level since November 20.

Powell says March rate cut unlikely

The Federal Reserve met on Wednesday and there was no surprise as the Fed left interest rates unchanged for a fourth straight month. The rate-tightening cycle has largely achieved its aim of lowering inflation and there’s little doubt that the Fed is done with tightening. Fed Chair Jerome Powell pivoted at the December meeting and signalled that rate cuts were coming in 2024. The markets proceeded to price in a March cut but the Fed has been pushing back on these expectations, even though some US economic releases were stronger than expected.

The Fed’s pushback has forced the markets to pare expectations of a March cut, from over 80% in December to 48% prior to the Fed meeting. In the aftermath of the meeting, the odds of a March cut have fallen even further, to 35% according to the CME FedWatch tool. The markets are now eyeing the May meeting and have widely priced in an initial rate cut at that time.

The rate statement from yesterday’s meeting noted that it “does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward two per cent.” This was a strong signal to the markets not to expect a rate cut in March.

This stance was reiterated by Powell in his press conference. Powell said it was unlikely that the Fed would lower rates in March, although he did not rule out the possibility completely. The Fed Chair noted that inflation had declined without dragging down the economy or causing high unemployment, a message to the markets that he was not in any rush to start chopping rates.

Australian data is pointing to a weakening economy, just ahead of the Reserve Bank of Australia’s meeting on February 6. Inflation eased to 4.1% y/y in the fourth quarter, down from 5.4% in Q3, while retail sales sunk in December with a decline of 2.7% m/m. The RBA is virtually certain to pause next week and is expected to start to trim rates later this year.

AUD/USD Technical

- AUD/USD is testing support at 0.6538. Next, there is support at 0.6510

- There is resistance at 0.6581 and 0.6609

BoE stands pat, two vote for hike, one for cut

BoE left the Bank Rate unchanged at 5.25% as widely expected. However, two MPC hawks (Jonathan Haskel and Catherine Mann) voted for another 25bps to 5.50%. Meanwhile, one dove (Swati Dhingra) voted for a 25bps cut to 5.00%. That resulted in a 6-3 vote for the decision.

Nevertheless, the central bank dropped tightening bias by omitting the language that "Further tightening in monetary policy would be required...." Instead, it's now "prepared to adjust monetary policy as warranted by economic data".

BoE will continue monitor a range of measures of "the underlying tightness of labour market conditions, wage growth and services price inflation."

CPI is projected to fall temporarily to 2% in Q2 2024, before rising again in Q3 and Q4. BoE sees CPI to be at to be at 2.8% in Q1 2025 (up from prior 2.5%), then 2.3% in Q1 2026 ( up from 1.9%), then 1.9% in Q1 2027 (new).

Four-quarter GDP growth is seen at 0.5% in Q1 2025 (up from 0.0%), the 0.8% in Q1 2026 (up from 0.6%), and 1.5% in Q1 2027 (new).

These are conditioned on a lowered market-implied path for Bank Rate that declines from 5.1% in Q1 2024 (prior 5.3%), then falls to 3.9% in Q1 2025 (down from 5.0%), and then 3.3% in Q1 2026 (down from 4.4%), and 3.2% in Q1 2027 (new).

(BOE) Bank rate maintained at 5.25%

Monetary Policy Summary, February 2024

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 31 January 2024, the MPC voted by a majority of 6–3 to maintain Bank Rate at 5.25%. Two members preferred to increase Bank Rate by 0.25 percentage points, to 5.5%. One member preferred to reduce Bank Rate by 0.25 percentage points, to 5%.

The Committee's updated projections for activity and inflation are set out in the accompanying February Monetary Policy Report. These are conditioned on a market-implied path for Bank Rate that declines from 5¼% to around 3¼% by the end of the forecast period, almost 1 percentage point lower on average than in the November Report.

Since the MPC's previous meeting, global GDP growth has remained subdued, although activity continues to be stronger in the United States. Inflationary pressures are abating across the euro area and United States. Wholesale energy prices have fallen significantly. Material risks remain from developments in the Middle East and from disruption to shipping through the Red Sea.

Following recent weakness, GDP growth is expected to pick up gradually during the forecast period, in large part reflecting a waning drag on the rate of growth from past increases in Bank Rate. Business surveys are consistent with an improving outlook for activity in the near term.

The labour market has continued to ease, but remains tight by historical standards. In the February Report projections, the continuing relative weakness of demand, despite subdued supply growth by historical standards, leads a margin of economic slack to emerge during the first half of the forecast period. Unemployment is expected to rise somewhat further.

Twelve-month CPI inflation fell to 4.0% in December 2023, below expectations in the November Report. This downside news has been broad-based, reflecting lower fuel, core goods and services price inflation. Although still elevated, wage growth has eased across a number of measures and is projected to decline further in coming quarters.

CPI inflation is projected to fall temporarily to the 2% target in 2024 Q2 before increasing again in Q3 and Q4. This profile of inflation over the second half of the year is accounted for by developments in the direct energy price contribution to 12-month inflation, which becomes less negative. In the MPC's latest most likely, or modal, projection conditioned on the lower market-implied path for Bank Rate, CPI inflation is around 2¾% by the end of this year. It then remains above target over nearly all of the remainder of the forecast period. This reflects the persistence of domestic inflationary pressures, despite an increasing degree of slack in the economy. CPI inflation is projected to be 2.3% in two years' time and 1.9% in three years.

The Committee judges that the risks around its modal CPI inflation projection are skewed to the upside over the first half of the forecast period, stemming from geopolitical factors. It now judges that the risks from domestic price and wage pressures are more evenly balanced, meaning that, unlike in previous forecasts, there is no difference between the MPC's modal and mean projections at the two and three-year horizons.

Conditioned on the alternative assumption of constant interest rates at 5.25%, the path for CPI inflation is significantly lower than in the Committee's modal projection conditioned on the declining path of market rates, falling below the 2% target from 2025 Q4 onwards.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

At this meeting, the Committee voted to maintain Bank Rate at 5.25%. Headline CPI inflation has fallen back relatively sharply. The restrictive stance of monetary policy is weighing on activity in the real economy and is leading to a looser labour market. In the Committee's February forecast, the risks to inflation are more balanced. Although services price inflation and wage growth have fallen by somewhat more than expected, key indicators of inflation persistence remain elevated.

As a result, monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term in line with the MPC's remit. The Committee has judged since last autumn that monetary policy needs to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipates.

The MPC remains prepared to adjust monetary policy as warranted by economic data to return inflation to the 2% target sustainably. It will therefore continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. On that basis, the Committee will keep under review for how long Bank Rate should be maintained at its current level.

Minutes of the Monetary Policy Committee meeting ending on 31 January 2024

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying February 2024 Monetary Policy Report.

2: Consumer price inflation across major advanced economies had declined by more than had been expected in the November Report, with continued easing of both goods and services price inflation. The Committee compared features of the disinflation seen across the United States, the euro area and the United Kingdom, and the risks around the inflation outlook. The Committee judged that the divergence seen across economies reflected differences in energy price dynamics and variation in the impact and timing of recent global shocks and their subsequent dissipation, alongside distinct profiles for spare capacity. Disinflation in core goods prices had been comparatively more pronounced so far in the United States because in the euro area and the United Kingdom the lag between falls in producer output price inflation and core consumer goods inflation had shown signs that it might have been longer than in previous cycles.

3: There had also been some differences, as well as commonalities, in the development of services price inflation and wage growth across these economies. Bank staff analysis suggested that the recent falls in services inflation across the three economies had been accounted for largely by declining non-labour input costs, including energy. Labour costs, by contrast, had remained elevated across countries, although there were some signs of easing emerging, particularly in the United States. To the extent that they were broadly comparable, measures of wage inflation had remained considerably higher in the United Kingdom than elsewhere.

4: In the United Kingdom, all of the respondents to the Bank's latest Market Participants Survey (MaPS) expected Bank Rate to be left unchanged at this MPC meeting. They also all expected the next move in the Bank Rate to be downward. The median expected profile for Bank Rate from the MaPS implied a cumulative 100 basis point reduction in Bank Rate this year starting from June 2024, broadly in line with market pricing. Market contacts had suggested that disinflationary news in recent economic data outturns both in other jurisdictions and in the United Kingdom had been a significant factor in the downward moves in UK short-term rates in recent months. Similar downward moves in short-term rates had also occurred in other advanced economies over this period.

5: UK GDP growth had weakened in 2023, with this weakness particularly pronounced in market sector output. This reflected the significant tightening of monetary policy implemented since the end of 2021 to contain the persistence of second-round effects on inflation as well as continued weakness in potential supply growth. Cumulative GDP growth over 2023 as a whole had been materially weaker than expected at the time of the November Report, with the path for household consumption notably below expectations. Timelier indicators suggested that activity would edge up in 2024 Q1.

6: The Committee had completed its annual supply stocktake, as set out in Section 3 of the February Report, and judged that potential supply growth remained weak by historical standards. The MPC also now judged that the degree of excess demand had been a little higher over the recent past than had been assumed in the November Report, implying weaker supply growth in the past. At the same time, it had revised up slightly its view of potential supply growth in the future, although this was still expected to be weaker than the rates seen pre-Covid.

7: The Committee discussed the degree of persistence in wage growth and domestic price inflation. There had been downside news in headline CPI inflation relative to the November Report, accounted for by a combination of fuel, core goods and services prices. In absolute terms, services price inflation remained significantly elevated. There had been a common signal from a range of indicators that wage growth had eased somewhat recently, although it had remained significantly elevated overall. This downward trend had been most pronounced in the annual rate of growth of private sector regular average weekly earnings (AWE), although that had brought the AWE series more into line with other indicators.

8: The majority of this year's wage setting processes would conclude in the next few months. A survey of firms conducted by the Bank's Agents suggested that the average pay settlement in 2024 would be for a rise only slightly lower than in 2023, at 5.4%. It remained to be seen to what degree the falls in CPI inflation and short-term inflation expectations would influence this year's wage setting, although this could also be influenced by a catch-up effect following the high rates of CPI inflation seen over the past couple of years. Evidence from the Agents suggested some possible upward pressures on wages from indirect effects of the increase in the National Living Wage. Intelligence from the Agents, however, also suggested that companies would not be able to pass on increased costs into prices as much as they had done in 2023.

The immediate policy decision

9: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

10: In the MPC's February Monetary Policy Report projections, UK GDP was expected to have been flat in 2023 Q4. Growth was expected to pick up gradually during the forecast period, in large part reflecting a waning drag from past increases in Bank Rate. In the medium term, the lower market-implied interest rate path, on which the forecast was conditioned, pushed up on GDP materially compared with the November projection.

11: The labour market had continued to ease, but had remained tight. In the February Report projections, the continuing relative weakness of demand, despite subdued supply growth by historical standards, led to a margin of economic slack emerging during the first half of the forecast period. Relative to November, the output gap projection had been pushed up by the boost to demand from the lower market path of interest rates. Equivalently, this implied that, if monetary policy were to follow the yield curve, then the stance of policy would be less restrictive than at the time of the November Report.

12: Twelve-month CPI inflation had remained above the 2% target. Inflation had fallen to 4.0% in December, below expectations in the November Report. The downside news had been broad-based, reflecting lower fuel, core goods and services price inflation. Although still elevated, wage growth had eased across a number of measures and was projected to decline further in coming quarters.

13: In the MPC's latest most likely, or modal, projections, CPI inflation was expected to fall temporarily to the 2% target in 2024 Q2 before increasing again in Q3 and Q4. This profile of inflation over the second half of the year was accounted for by developments in the direct energy price contribution to 12-month inflation, which becomes less negative. Conditioned on a lower market-implied path for Bank Rate than had underpinned the November Report, CPI inflation was then projected to remain above the 2% target over nearly all of the remainder of the forecast period, owing to persistence in domestic inflationary pressures.

14: The Committee judged that the risks around the modal inflation projection were skewed to the upside over the first half of the forecast period, stemming from geopolitical factors. Risks from domestic price and wage pressures were now more evenly balanced, however. Taken together, this meant there was no difference between the MPC's modal and mean projections at the two and three-year horizons.

15: The MPC judged that monetary policy would need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the MPC's remit. The Committee had judged since last autumn that monetary policy needed to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipated.

16: Six members judged that maintaining Bank Rate at 5.25% was warranted at this meeting. Headline CPI inflation had fallen back relatively sharply. The restrictive stance of monetary policy was weighing on activity and was leading to a looser labour market. In the Committee's February forecast, the risks to inflation were more balanced. Although services price inflation and wage growth had fallen by somewhat more than had been expected, key indicators of inflation persistence remained elevated. There were questions, on which further evidence would be required, about how entrenched this persistence would be, and therefore about how long the current level of Bank Rate would need to be maintained.

17: Two members preferred a 0.25 percentage point increase in Bank Rate, to 5.5%, at this meeting. Although headline inflation had fallen by more than had been expected, this was not necessarily informative about inflation persistence. Current indicators of economic activity had remained subdued, but real household incomes had continued to edge up, and forward-looking indicators of output had remained positive. The labour market was still relatively tight, consistent with a rise in the medium-term equilibrium rate of unemployment, and a range of indicators suggested that the pace of loosening had been slow. Measures of wage growth had moderated further but remained at rates above those consistent with the inflation target. Underlying services price inflation had slowed but remained elevated. These members continued to judge that there was evidence of more persistent inflationary pressures than included within the forecast. Financial conditions had eased since the MPC's December meeting. An increase in Bank Rate at this meeting was necessary to address the risks of more deeply embedded inflation persistence and to return inflation to target sustainably in the medium term.

18: One member preferred a 0.25 percentage point reduction in Bank Rate at this meeting. For this member, the increments applied on the way up, together with lags in transmission, meant that Bank Rate needed to become less restrictive now. Waiting for lagging indicators of domestic relative price growth to fall sharply before reducing rates would come with a risk of overtightening. There might be potential upside risks from geopolitics. That said, consumer price inflation was already, and had been for some time, on a firm downward trajectory. Moreover, leading indicators, such as those from granular producer prices data, pointed to an easing in consumer prices. The outlook for demand remained weak, and less resilient than previously assumed, with vacancies falling more sharply than in some other advanced economies and consumption not having recovered to pre-pandemic levels. This further reduced the prospects of embedded persistence, shown in forward-looking indicators of domestic relative prices, such as monthly annualised rates of nominal pay growth and the Bank's Agents' surveys, and suggested lower pass-through of costs to prices.

19: The MPC remained prepared to adjust monetary policy as warranted by economic data to return inflation to the 2% target sustainably. It would, therefore, continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. On that basis, the Committee would keep under review for how long Bank Rate should be maintained at its current level.

20: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 5.25%.

21: Six members (Andrew Bailey, Sarah Breeden, Ben Broadbent, Megan Greene, Huw Pill and Dave Ramsden) voted in favour of the proposition. Three members voted against the proposition. Two members (Jonathan Haskel and Catherine L Mann) preferred to increase Bank Rate by 0.25 percentage points, to 5.5%. One member (Swati Dhingra) preferred to reduce Bank Rate by 0.25 percentage points, to 5%.

Operational considerations

22: On 31 January, the total stock of assets held for monetary policy purposes was £738.0 billion, comprising £737.6 billion of UK government bond purchases and £0.4 billion of sterling non‐financial investment‐grade corporate bond purchases.

23: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Ben Broadbent

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

Sam Beckett was present as the Treasury representative.

David Roberts was also present on 24 and 26 January, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank's Court of Directors.