Sample Category Title

GBP and JPY Eyeballing Domestic Politics

Markets

A three-day slide in stock and crypto markets pulled dip-buyers from the sidelines going into the weekend. Equities bounced more than 2% in the US. Bitcoin hit the 60k mark, a 1.5 year low, before recovering to north of 70k again. Precious metals succumbed to overall asset selling on Thursday but staged a comeback at the end of the week. Intraday price swings varied between around +7% for gold and >21% for silver. Industrial commodities - oil, natural gas, aluminum, copper … strengthened too, offering support for currencies ranging from AUD over NZD to NOK. The US Dollar lost out against most peers, including the euro. EUR/USD recovered back north of 1.18. DXY came just shy of the 98 barrier before weakening to 97.63 in the close. GBP and JPY were eyeballing domestic politics. Starmer’s position as prime minister looks increasingly vulnerable after his chief of staff resigned on Sunday for his advice to hire Mandelson as ambassador. But being the man who actually appointed Mandelson, both allies and opponents are putting on the heat on Starmer. We’ve seen jittery gilt and GBP markets return last week, fearing for a potentially fiscally less strict successor to Starmer ever since the Mandelson crisis erupted. UK yields ended last week on a positive note but we’re keen to find out how they open after Sunday’s developments. The pound is losing ground in any case. EUR/GBP pushes to north of 0.87. The only currency worse off this morning is the US dollar. Renewed greenback weakness was sparked by reports of China urging banks to curb US Treasury exposure (see below). EUR/USD extends gains to 1.1850. The news also drives up (longer term) US yields by another 3 bps. That comes on top of Friday’s 1-4.8 bps bear flattening move. The yen is taking the election outcome positively. PM Takaichi’s LDP secured a landslide victory in snap elections yesterday with the largest (two-thirds) majority in the lower house since the party was created in 1955. Without compromises to be made with coalition partners and with an LDP now immune to (spending) pressure from the opposition given its strong mandate, JPY and JGBs assume a stable and a more cautious government fiscally speaking. USD/JPY eases to 156.5 after a strong February rally so far. Japanese yields rose 5 bps up to the 10-yr bucket. Ultra-long tenors, the ones most sensitive to the fiscal topic, quickly erased the few bps they gained at the open. The jury remains out on the strength of that narrative though. The long end of the curve remains vulnerable in core areas, from Japan over the UK to the US, each with their own trigger to pull.

News and views

Bloomberg, referring to people familiar with the matter, reported this morning that Chinese regulators advised financial institutions to reign in their holdings of US Treasuries. According to the report, officials urged banks to limited the purchases of US government bonds while instructing those with high exposure to reduce their positions. The directive was said not to apply to China’s state holdings of US Treasuries. The guidance is reportedly driven by concerns over concentration risk and market volatility and not directly linked to geopolitical maneuvering or a fundamental loss in creditworthiness of the US. US yields jumped 1-2 bps upon the release of the article. The dollar is losing (modest) ground.

The KMPG and REC report on UK jobs (compiled by S&P global) signaled a relative improvement in UK hiring conditions in January as recruiters signaled a softer drop in permanent staff appointments. At the same time, temporary billings are expanding slightly for the first time in three months. Candidate availability was reported to have increased at the softest pace in a year. The survey also points to stronger rises in starting salaries and temporary wages. The survey comes as the BoE last week indicated that might further reduce its policy rate (in a relatively near future) as disinflation is expected to bring inflation to the 2% target substantially faster than previously expected. At least for several MPC members, a weak labour market was a reason to frontload further easing, too.

Japan’s Takaichi Secures Historic Victory in Snap Election

In focus today

In Norway, we receive data on 2025Q4 mainland GDP growth. The current key figures point to underlying growth of around 0.1% q/q, but because the technical factors are partially reversing, we believe mainland-GDP growth was 0.3% in Q4.

In the euro area, the February Sentix Investor Confidence indicator will be released. As the first measure of investor confidence for February, consensus expects the reading to improve to 0, up from -1.8 in January.

For the rest of the week, we will keep an eye on US retail sales and the Q4 employment cost index on Tuesday, the US Jobs Report and Chinese CPI on Wednesday, and UK GDP growth on Thursday. The week concludes on Friday with US CPI taking centre stage.

Economic and market news

What happened over the weekend

In Japan, Prime Minister Sanae Takaichi's coalition secured a supermajority in the lower house, winning 328 out of 465 seats following a rare winter snap election. This provides her with a strong mandate to advance her legislative agenda, including plans for tax cuts and increased military spending aimed at countering China. The market reacted strongly to her victory, with Japanese stocks surging to record highs as the Nikkei 225 jumped 5.7%, reflecting investor optimism over her fiscal policies. However, bond yields climbed as concerns grew about the potential impact of her spending plans on fiscal stability, while the yen weakened initially before rebounding after verbal intervention from Japanese officials. Takaichi's nationalistic policies and economic agenda are expected to shape both domestic markets and geopolitical dynamics in the region.

In the US, San Francisco Fed President Mary Daly (non-voter) signalled on Friday that one or two rate cuts may be required in 2026 to address vulnerabilities in the labour market, particularly the challenges faced by new graduates and stagnant wages. While inflation remains above the 2% target, Daly views labour market risks as more pressing, highlighting the need for flexibility in monetary policy amid ongoing uncertainties.

In geopolitics, Iran's foreign minister warned that Tehran would target US bases in the region if attacked by US forces, clarifying that host countries would not be the target. This came after indirect nuclear talks between the two nations showed progress, with further discussions expected next week. Despite the diplomatic efforts, tensions remain high following President Trump's demands for Iran to halt uranium enrichment and missile development, alongside a recent US naval buildup in the region.

In Sweden, January CPI inflation increased slightly to 0.4% y/y from 0.3% in December, falling short of expectations. CPIF inflation was at 2.0% y/y, while core inflation (CPIF excluding energy) came in at 1.7% y/y, both lower than expected. The surprise lies in core inflation, which was significantly weaker, whereas energy and mortgage rates developed as anticipated.

In India, refiners are reducing Russian oil purchases for March-April deliveries, a move that could bolster New Delhi's efforts to finalise a trade pact with Washington by March. US President Trump has lifted 25% tariffs on Indian goods, citing India's commitment to halt Russian oil imports, although no formal announcement has been made. India's Russian oil intake has already dropped significantly, with refiners shifting to Middle Eastern, African and South American suppliers.

In Thailand, Prime Minister Anutin Charnvirakul's Bhumjaithai Party secured 193 out of 500 seats in the general election, surpassing expectations and consolidating the conservative vote. The result reduces risks of political instability and sent Thai stocks 3% higher to their strongest level in over a year. Coalition talks are expected to begin in the coming days, with Anutin pledging to form a strong government and advance nationalist policies, including building a Cambodia border wall and strengthening the military.

Equities: Global equities closed last week on a stronger footing, led by a sharp rebound in the US session on Friday that ultimately pushed equities higher for the week. This came despite continued weakness in consumer discretionary, led by Amazon, and lingering pressure on several of the mega-cap names. That said, the tone within tech shifted meaningfully, with semiconductors and broader hardware showing solid relative strength. Last week's rotation was nothing short of violent: US tech hardware rose approximately 7% for the week, while tech software fell roughly 7%.

Small caps also performed strongly versus large caps, with the Russell 2000 up 3.6% on Friday alone, underlining the breadth of the move away from crowded growth exposures. Asian equity markets are extending the risk-on tone this morning. Japanese equities are up more than 4% following Sunday's election, where Prime Minister Takaichi secured a definitive victory and a supermajority in the Lower House, effectively paving the way for what markets are already framing as Abenomics 2.0. South Korean equities are also up around 4%, reinforcing the regional risk rally. European and US futures are more subdued but remain modestly in the green.

FI and FX: USD/JPY initially pushed higher toward 158 following the landslide election result in Japan but later retreated below 157 after Japanese officials signalled heightened vigilance in monitoring the FX market. EUR/USD remains anchored just above the 1.18 mark in a week where attention shifts to the January US jobs report and CPI release. US yields ended higher on Friday, particularly in the front end, with the 2-year rising 8bp as market sentiment improved. After a very poor mid-week the NOK FX still ended last week on a strong footing amid improving risk appetite, higher energy prices and an outperforming domestic equity market.

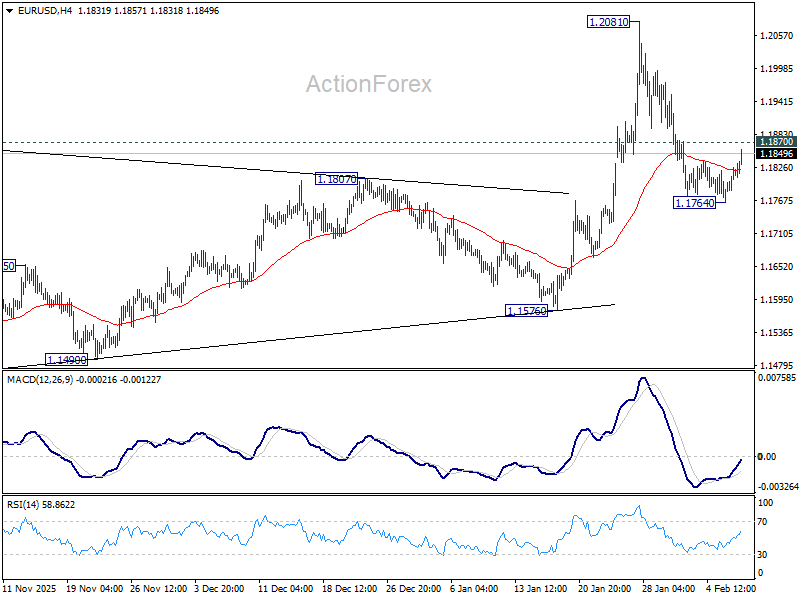

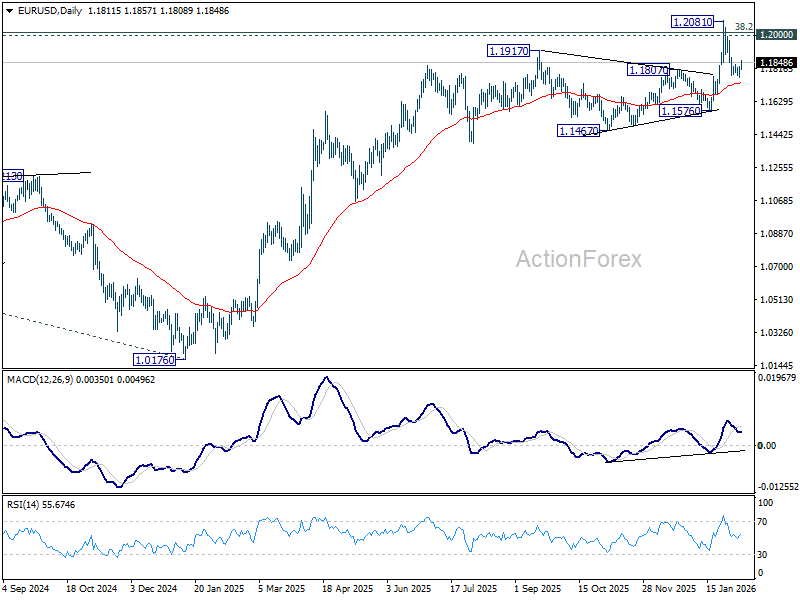

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1780; (P) 1.1803; (R1) 1.1840; More….

Intraday bias in EUR/USD remains neutral for the moment. On the downside, sustained trading below 55 D EMA (now at 1.1730) will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support for confirmation. On the upside, above 1.1870 minor resistance will bring stronger rebound to retest 1.2081. Decisive break above 1.2 will carry larger bullish implications.

In the bigger picture, as long as 55 W EMA (now at 1.1470) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

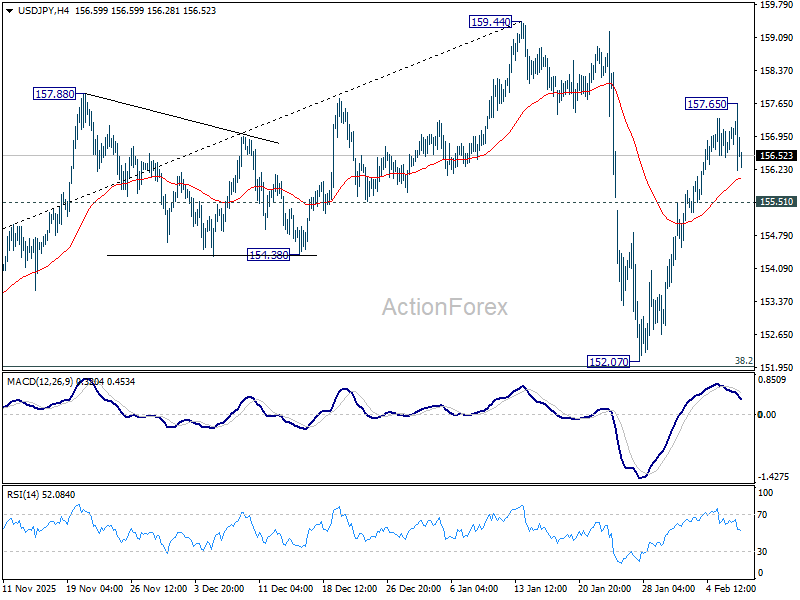

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.75; (P) 157.01; (R1) 157.51; More...

USD/JPY retreated quickly after brief spike to 157.65 and intraday bias remains neutral. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Above 157.65 will target a retest on 159.44 high. On the downside, below 155.51 minor support will bring deeper fall as another falling leg. But downside should be contained by 38.2% retracement of 139.87 to 159.44 at 151.96.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.68) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

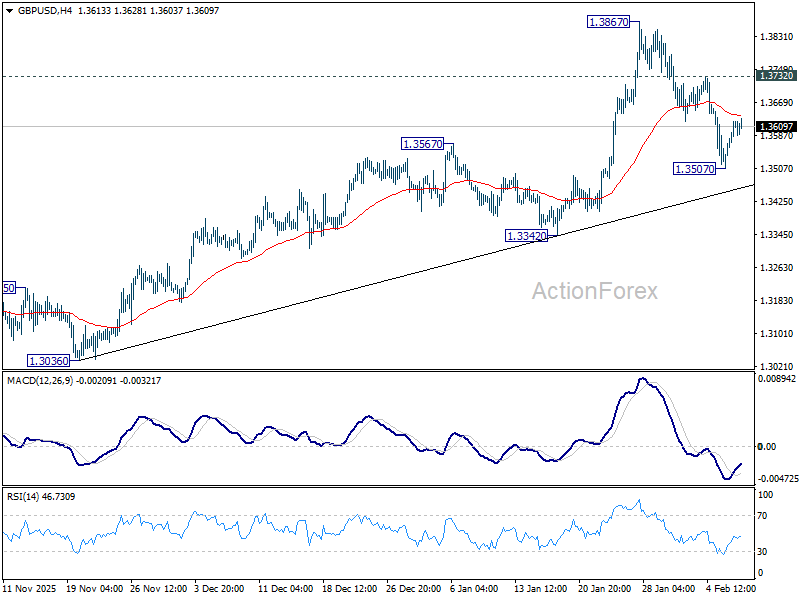

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3540; (P) 1.3581; (R1) 1.3654; More...

Intraday bias in GBP/USD remains neutral for the moment. On the downside, below 1.3507 will resume the fall from 1.3867 to 55 D EMA (now at 1.3483). Sustained break there will raise the chance of larger scale correction, and target 1.3342 support for confirmation. On the upside, above 1.3732 minor resistance will bring retest of 1.3867. Firm break there will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

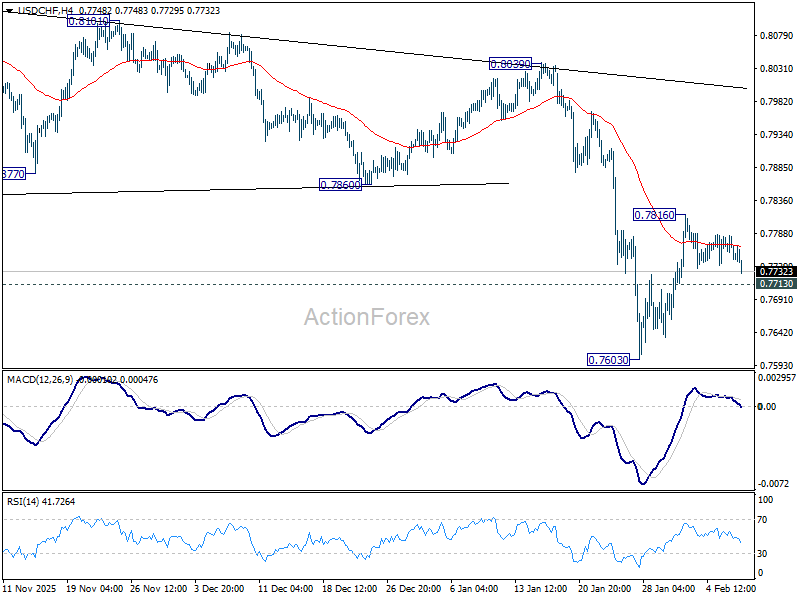

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7746; (P) 0.7767; (R1) 0.7782; More….

Intraday bias in USD/CHF remains neutral for the moment. Initial bias stays neutral this week first. Another rise might be seen but upside should be capped by 55 D EMA (now at 0.7890) to complete the corrective bounce fro 0.7603. On the downside, below 0.7713 minor support will bring retest of 0.7603. Firm break there will resume larger down trend to 0.7382 projection level next. However, sustained break of 55 D EMA will suggest near term reversal and target 0.8039 resistance for confirmation.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8152) holds.

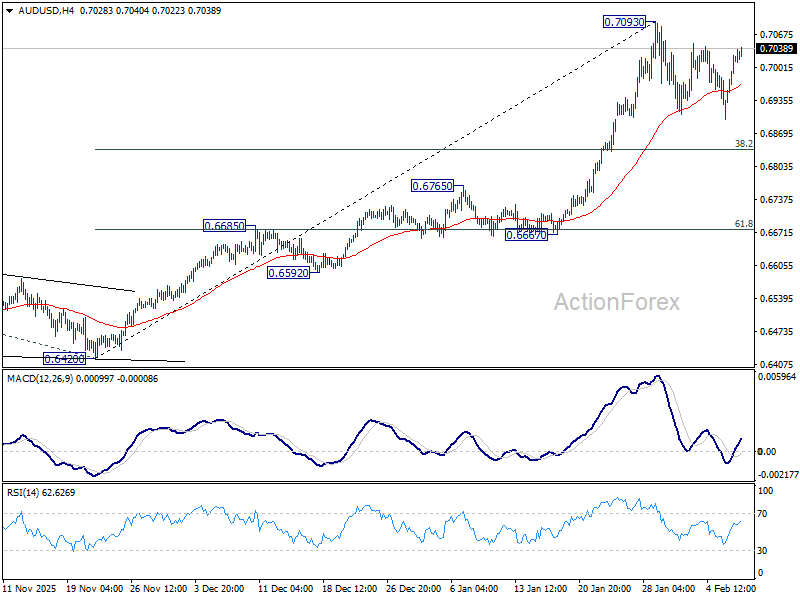

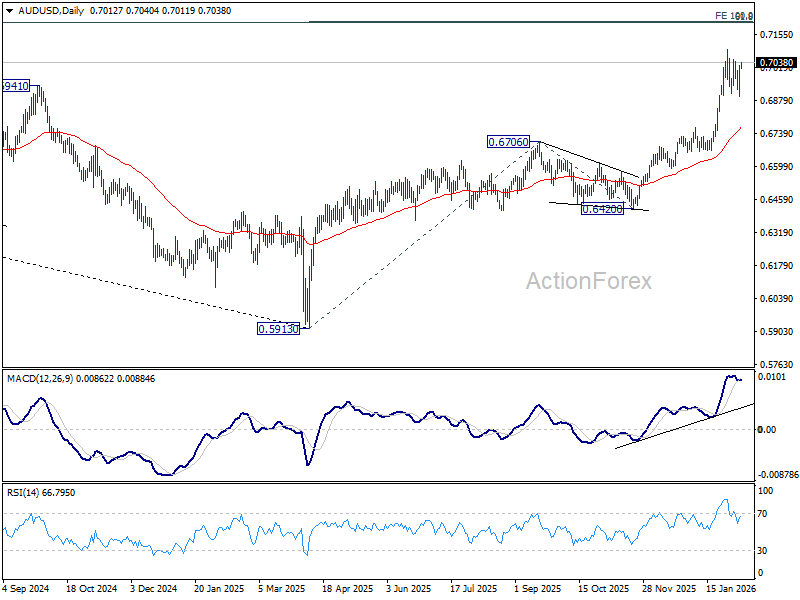

AUD/USD Daily Report

Daily Pivots: (S1) 0.6933; (P) 0.6979; (R1) 0.7061; More...

Intraday bias in AUD/USD remains neutral at this point, and consolidations could continue below 0.7093. In case of another fall, downside should be contained by 38.2% retracement of 0.6420 to 0.7093 at 0.6836. On the upside, break of 0.7093 will extend larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

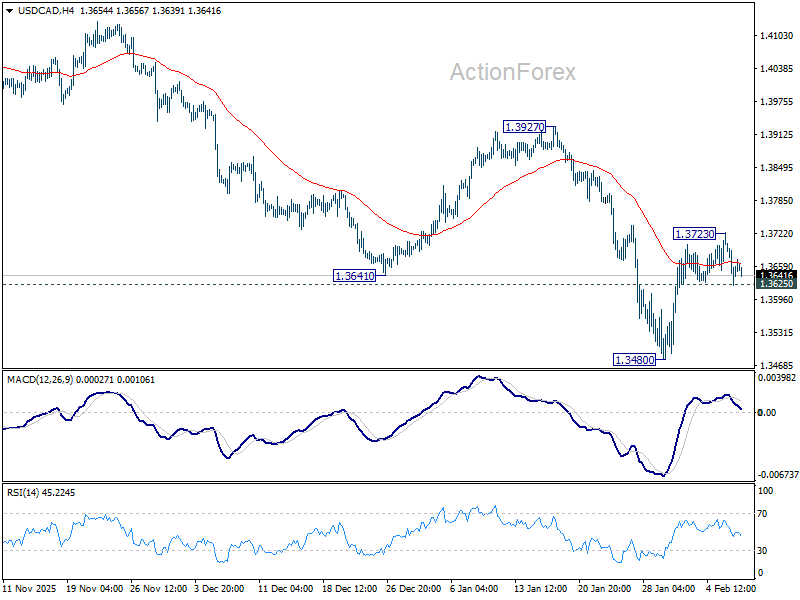

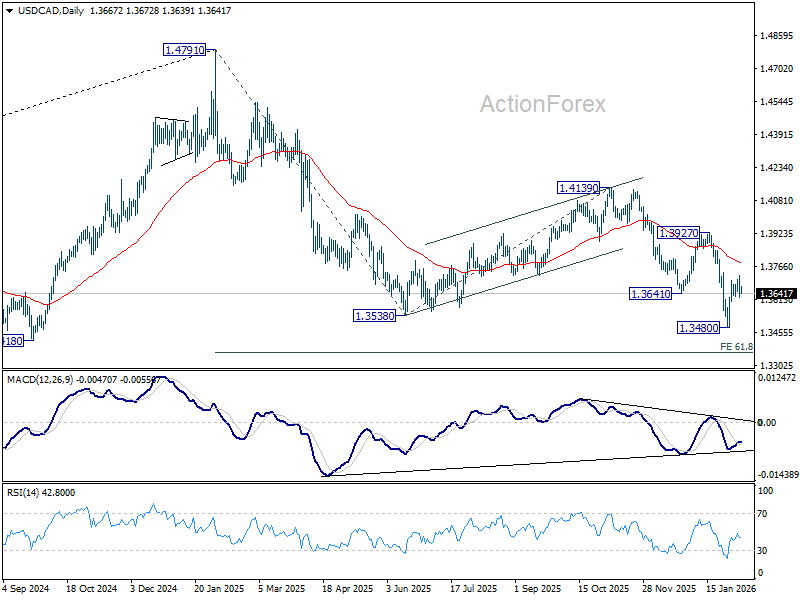

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3624; (P) 1.3675; (R1) 1.3725; More...

Intraday bias in USD/CAD stays neutral at this point. In case of another rise, upside should be limited by 55 D EMA (now at 1.3781) to complete the corrective bounce from 1.3480. On the downside, break of 1.3625 will bring retest of 1.3480. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

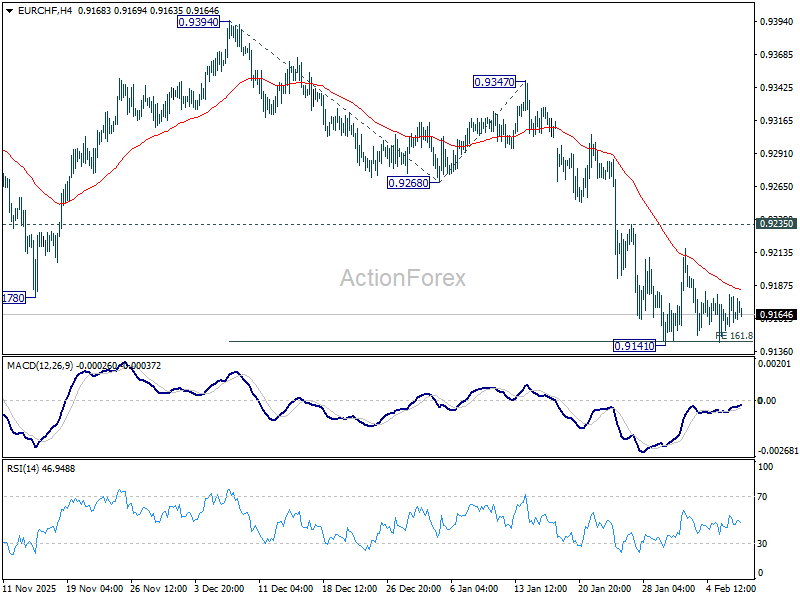

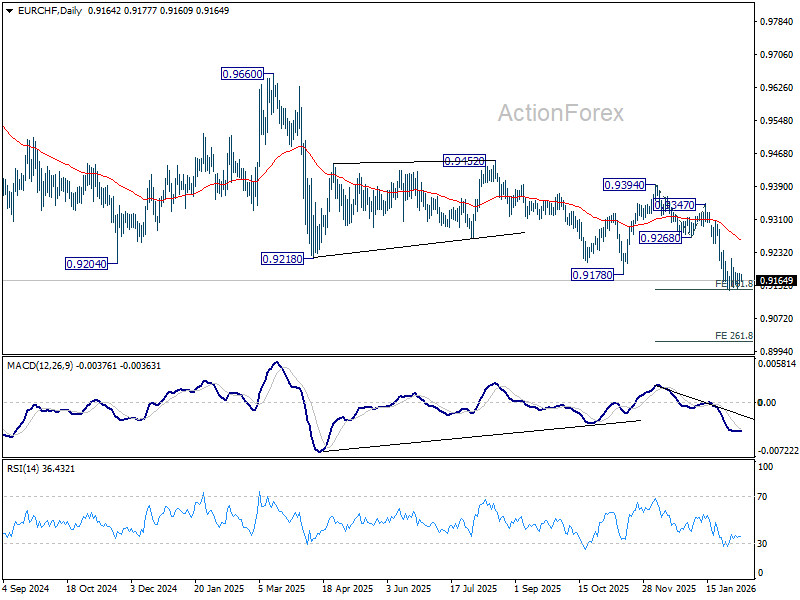

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9153; (P) 0.9167; (R1) 0.9181; More....

Intraday bias in EUR/CHF remains neutral and more consolidations could be seen above 0.9141. Another recovery cannot be ruled out, but upside should be limited below 0.9235 resistance. On the downside, firm break of 0.9141 will extend larger down trend to 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9341) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

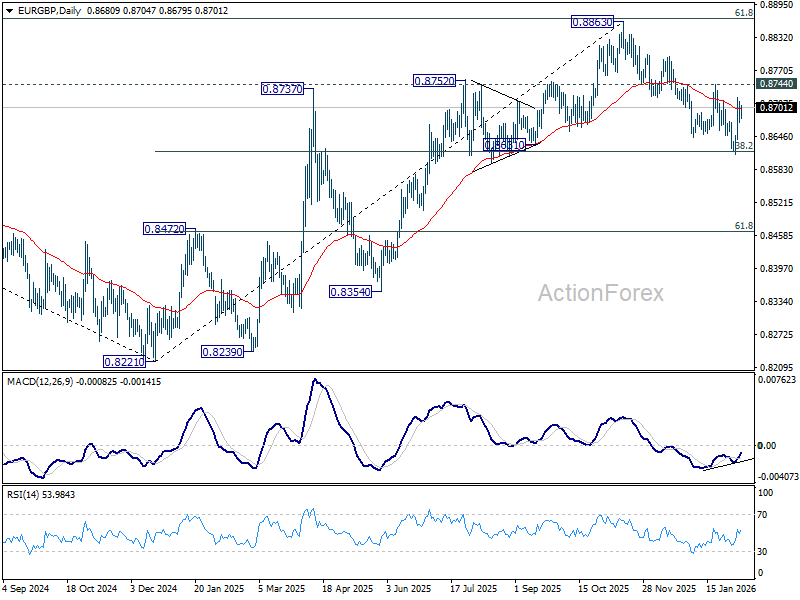

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8665; (P) 0.8690; (R1) 0.8706; More…

Intraday bias in EUR/GBP remains neutral for the moment. On the upside, firm break of 0.8744 resistance will argue that fall from 0.8863 has completed at 0.8611 as a correction. Further rally should be seen back to retest 0.8863 high. On the downside, sustained break of 38.2% retracement of 0.8221 to 0.8663 at 0.8618 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8629) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.