Sample Category Title

CPI Back on Time – Markets Weekly Outlook

Week in review – Geopolitical Turmoil on the Menu

Traders have returned to their desks, and volumes are finally normalizing after a holiday period that was anything but boring.

Connecting back to the end-December trading, metals rode a rollercoaster that took many to fresh record highs, setting a bar of high expectations for the new year.

The weekly open did not disappoint. The capture of Venezuelan President Nicolas Maduro by the Trump Administration over the weekend sent shockwaves through the headlines and ignited a wave of excitement across markets.

This reaction is rooted in a clear shift: The revival of the Monroe Doctrine—now dubbed the "Donroe Doctrine"—sets a precedent unseen in decades.

When viewing this alongside recent administration moves, such as renaming the Department of Defense to the Department of War and shifting military assets to the Caribbean, the market's angst transforms into a realization of a new reality.

As the operation unfolded, markets opened a renewed hype: The Freedom Trade.

Newfound excitement surged through the US Stock Market, powering the Dow Jones and traditional sectors beyond year-end records.

Investors are betting that "America First" is no longer just an isolationist slogan, but a policy that places US strategic interests above all else—including international norms.

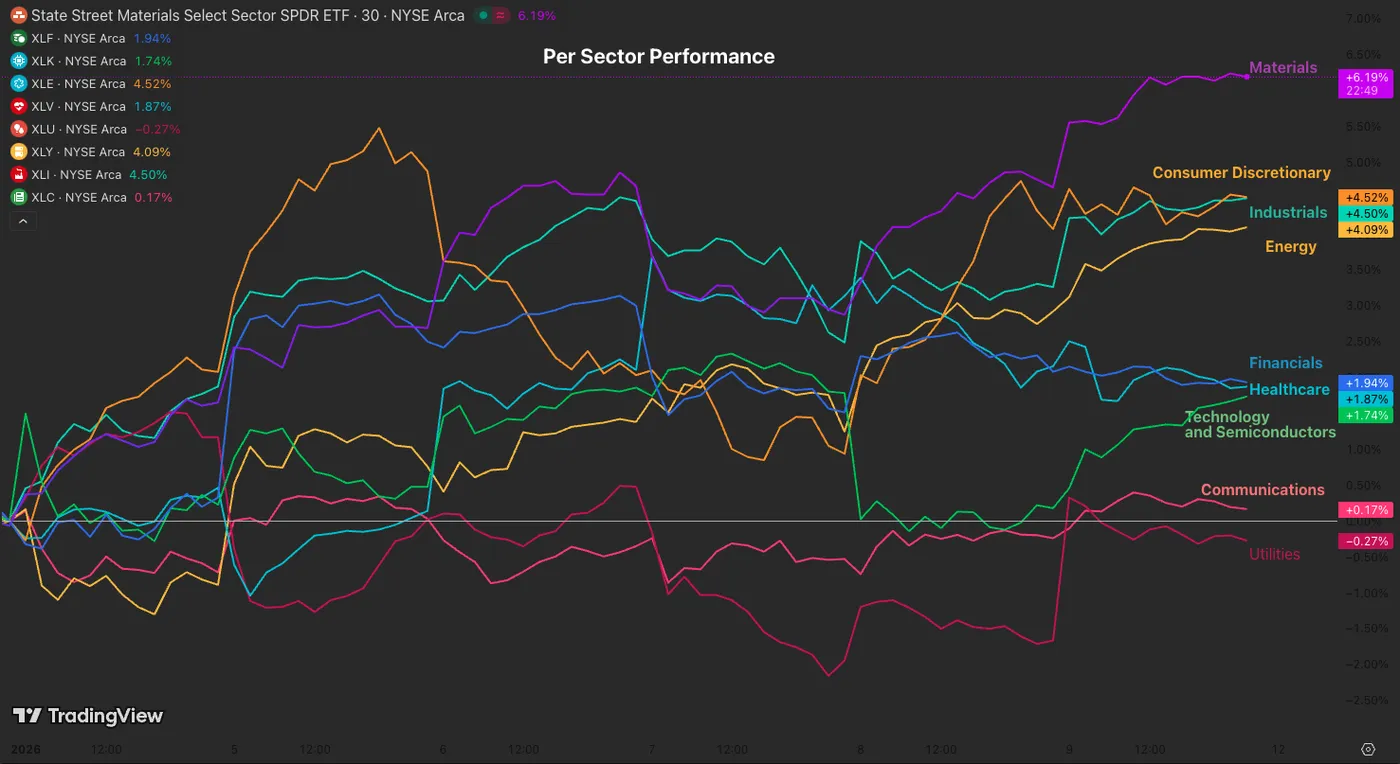

Stock Market per Sector Performance since beginning 2026 – Source: TradingView

The Market Consequence? Gigantic rallies in Industrials, Materials, Energy, and Consumer Discretionary sectors.

The translation is simple: if US External Policy returns to its past century way of operating—global military dominance and strategic shows of strength—traditional sectors stand to benefit the most. The administration is making it clear: the US is not to be reckoned with.

The Venezuela capture also extended elsewhere.

With threats of intervention now extending to Mexico, Cuba, Colombia, and even Greenland, global heads of state are waking up to defend their interests. The most significant tail risk for sentiment remains the standoff regarding Greenland, which directly challenges the NATO framework.

Amidst the geopolitical noise, markets also received crucial economic clues: the US labor picture is not worsening, and the global economy remains resilient, with Global PMIs staying firmly in expansion territory.

Weekly Performance across Asset Classes

Weekly Asset Performance – January 9, 2026 – Source: TradingView

Metals are once again standing on top of the latest geopolitical developments. Gold is up a sneaky 4% on the week, while Silver and Palladium are up above 11%.

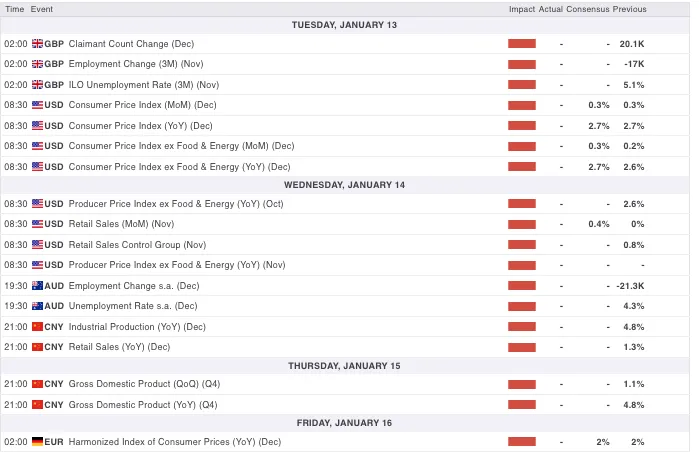

The Week Ahead – CPI and Elevated Tensions

Asia Pacific Markets – Chinese Trade Data and Australian Employment

This week wasn't only interesting for North America.

Japan saw renewed strength in wage growth data, which, combined with hawkish speeches from Bank of Japan members and strong approval ratings, led PM Takaichi to announce snap elections for mid-February. Her aim is to consolidate power; a victory would make her the first officially elected female Prime Minister in Japanese history.

China also released an improved inflation picture. Recent stimulus and a shift toward more business-friendly regulations have sparked a decent rebound from the preceding deflation. As a result, the CNY (Chinese Yuan) is strengthening aggressively and maintaining a higher path.

Looking ahead to next week, markets expect a slew of Chinese data. This includes Trade Reports on Tuesday—which will put hard numbers on the state of a fragmented global trade regime—followed by Retail Sales on Wednesday and GDP data on Thursday. Strong Chinese data tends to have a boosting effect on Antipodean currencies (AUD and NZD).

Speaking of the Antipodeans, traders will also welcome Australian Employment numbers. Following last week's better-looking but still very hot CPI data (3.4% y/y), expectations for this report are high.

A beat here would likely cement the case for a rate hike at the next RBA meeting on February 3.

Europe and UK Markets – UK Employment & GDP mixed with European CPIs

The UK moves to the forefront for the upcoming week.

Following last month's improved inflation data, traders will look to confirm a smoother rate cut cycle for the Bank of England in 2026, provided UK employment figures don't show unexpected strength. The release is scheduled for the Monday-Tuesday overnight session at 2:00 A.M.

Amidst appearances by several BoE members, market participants should also expect the UK monthly GDP numbers on Thursday.

For the Eurozone, ECB Vice President Luis de Guindos—one of the favorites to replace Christine Lagarde—is expected to speak twice. His comments should be tracked closely by EU traders as he looks to cement his standing.

On the data front, attention will turn to inflation, with the French and German CPI releases scheduled for Thursday and Friday, respectively.

North American Markets – US CPI and A LOT of Fed Speakers

The US will finally receive on-time Inflation data, with the CPI (Tuesday) and PPI (Wednesday) releases forming a critical wombo-combo which will be tracked closely by global traders.

Scrutiny is particularly high after the last report raised doubts regarding its accuracy; that print came in at 2.7% (vs. 3.4% expected), with the BLS reportedly taking some liberties to fill data gaps caused by the Shutdown.

The CPI is expected to land at 0.3% Month-over-Month, a sticky read that would almost certainly dash any hopes for a January rate cut (currently priced at just 10%).

Of course, don't forget the US Retail Sales at 8:30, also on Wednesday.

Elsewhere, a parade of Fed officials is scheduled to speak. NY Fed President Williams will headline the slate with appearances on Monday and Wednesday. We will also hear from the new 2026 rotation of regional voters, including Minneapolis Fed President Neel Kashkari, who is also set to speak on Wednesday.

To learn more about the 2026 voting rotation, check out our recent publication:

Who Are the Fed Speakers to Watch in 2026? A New Front-Runner for the Fed Chair

Finally, keep your notifications on for the geopolitical scene: The developing revolution in Iran could have profound implications for Oil markets and the broader global regime.

Next Week's High Tier Economic Events

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Safe Trades and enjoy your weekend!

The Weekly Bottom Line: Jobs, Trade, and Global Shifts

Canadian Highlights

- Canada’s unemployment rate jumped higher to 6.8% in December as rapid labour force growth outweighed tepid employment gains.

- Canada’s goods trade balance is back in deficit territory. But trade in gold continues to whipsaw both import and export readings, making discerning trends more challenging.

- Prime Minister Carney will visit China next week to discuss investment and trade; a timely meeting on the heels of the U.S./Venezuela situation.

U.S. Highlights

- The payrolls report for December came in weaker than expected, capping off the “low hire, low fire” 2025 jobs market.

- Global oil markets adjusted to the possible return of Venezuelan crude to global markets following U.S. actions in the country.

- Investors will have to stay tuned for the Supreme Court’s ruling on the IEEPA tariffs.

Canada – Jobs, Trade, and Global Shifts

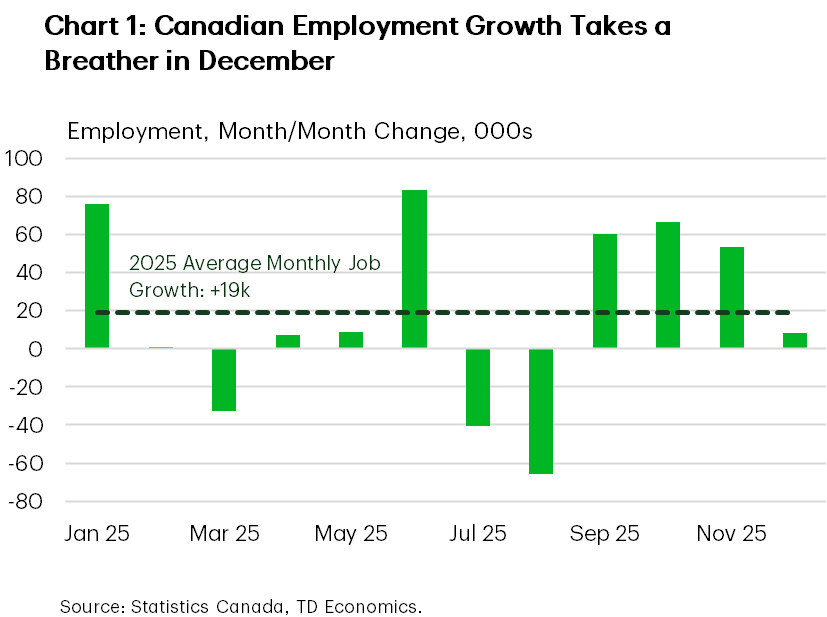

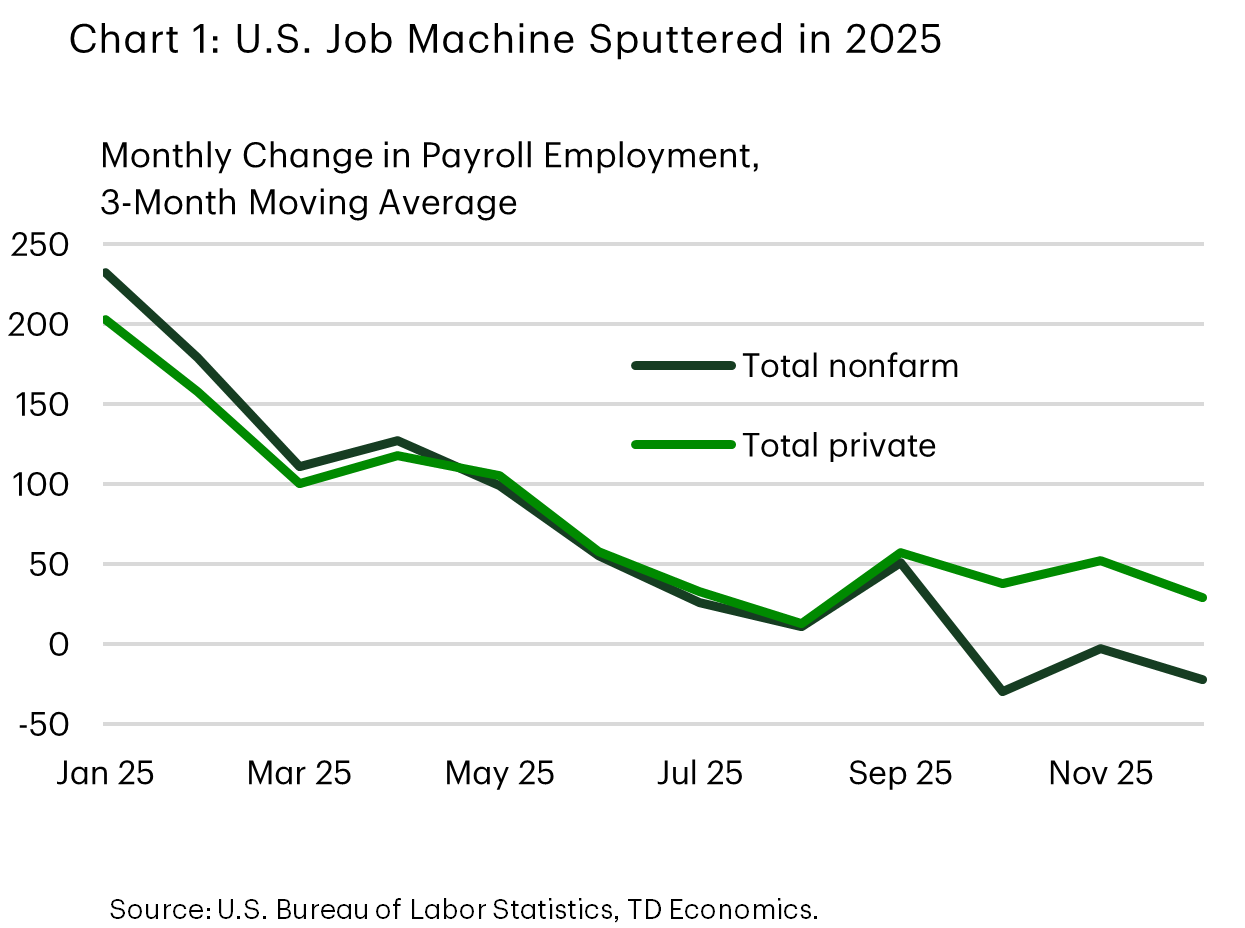

Data flow this week showed the Canadian economy entered the tail end of the year on a slightly positive note. An update to Canada’s job market was the headliner, with job creation totaling a modest 8k for the month of December. While this edged out market expectations, it represents a deceleration from the blistering 60k average gain over the prior three months (Chart 1). The unemployment rate also moved three ticks higher to 6.8%, completely unwinding the sharp drop in November, as the labour force grew at its fastest pace in over a year.

For all the headwinds and headaches, the labour market has put in a not-too-bad showing this year. In fact, the current unemployment rate is only 0.1 percentage points (ppts) above year-ago levels, a much better outcome than forecast in early 2025. Looking ahead, we’re expecting the jobless rate to peak this quarter before drifting lower thereafter as new labour force growth stalls. This report won’t change the Bank of Canada’s (BoC) policy stance, with several important data points due out before their January 28th meeting.

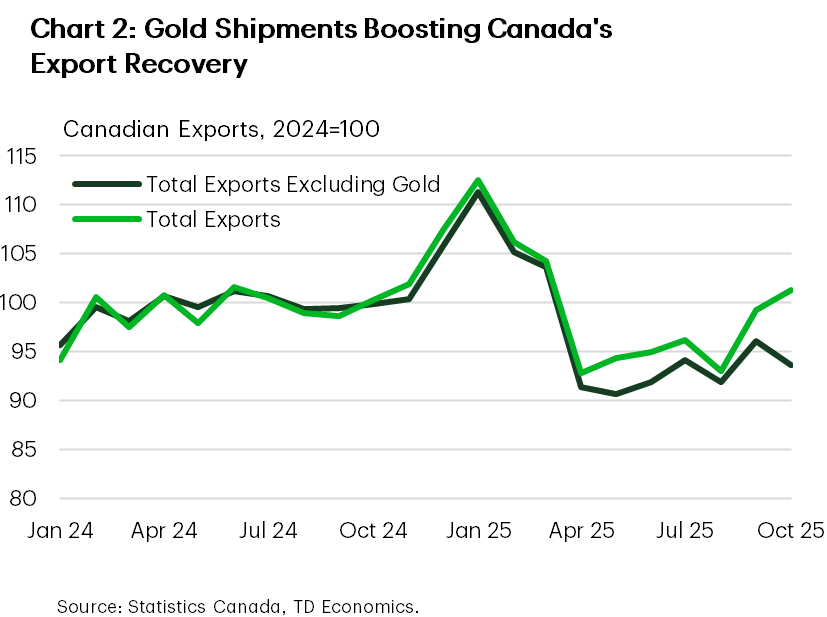

The improvement theme was also seen in the October trade data even though the nation’s trade balance flipped back to into the red. Chart 2 shows that total exports (including gold) have increased by 9% since bottoming in April 2025 and are approximately in line with average export levels for 2024, though those numbers have been lifted by high gold prices. Strip gold out of the equation and exports are up a more modest 2.5% since April 2025 and remain 6% below the 2024 average. Gold now accounts for almost 14% of Canada’s nominal exports, over three times above than its historical average.

There is also some improvement in export diversification. One third of Canadian exports are now being shipped to non-U.S. markets, a level never achieved outside of trade distortions seen during the early days of the pandemic. But again, gold is a big part of the picture. A multi-month surge in unwrought gold exports to the UK has made a sizeable contribution to the rise. Also of note, China has quickly become the main overseas buyer of Canadian crude, which has also helped Canada orient toward East-West trade.

Cultivating this relationship will be important, especially in the wake of the recent U.S./Venezuela situation. We wrote here about the potential near-term risks to Canada’s oil industry, and while minimal, it still strengthens the case for Canada to expedite a new oil pipeline that builds out capacity for Asian shipments. Chinese demand for Canadian crude is set to increase as the U.S. pressures Venezuela to cut ties with China. Canadian oil also has shorter shipping times and flexible tanker options, buoying the case for China to buy more Canadian crude. We are likely to see this discussed next week when Prime Minister Mark Carney visits China to engage in talks around boosting trade and investment.

U.S. – Hiring Slows, Affordability Worries Grow

The world was on tenterhooks this morning as all waited to see if the Supreme Court would rule on the administration’s use of the International Emergency Economic Powers Act (IEEPA) to implement some of its tariffs in 2025. The much-anticipated IEEPA ruling did not come, so the big news of the day is the weaker than expected December jobs report. Private sector hiring slowed, prior months were revised lower, and the number of jobseekers declined, allowing the unemployment rate to fall even as jobs growth slowed. The data reinforce the view that 2025 was a “low hire, low fire” year, characterized by a pronounced deceleration in job growth and a modest rise in the unemployment rate (Chart 1).

Survey data this week were mixed. The ISM Manufacturing Index contracted for a tenth consecutive month, with respondents citing “tariff related pricing pressures” and notable reductions in 2026 capital expenditure plans. By contrast, the ISM Services surprised to the upside, highlighting continued resilience in consumer demand for travel, healthcare, and professional services. The divergence between manufacturing and services has persisted throughout the year, as manufacturing remains more exposed to tariff related uncertainty. Both surveys indicated easing price pressures and softening labour demand, consistent with today’s payrolls release.

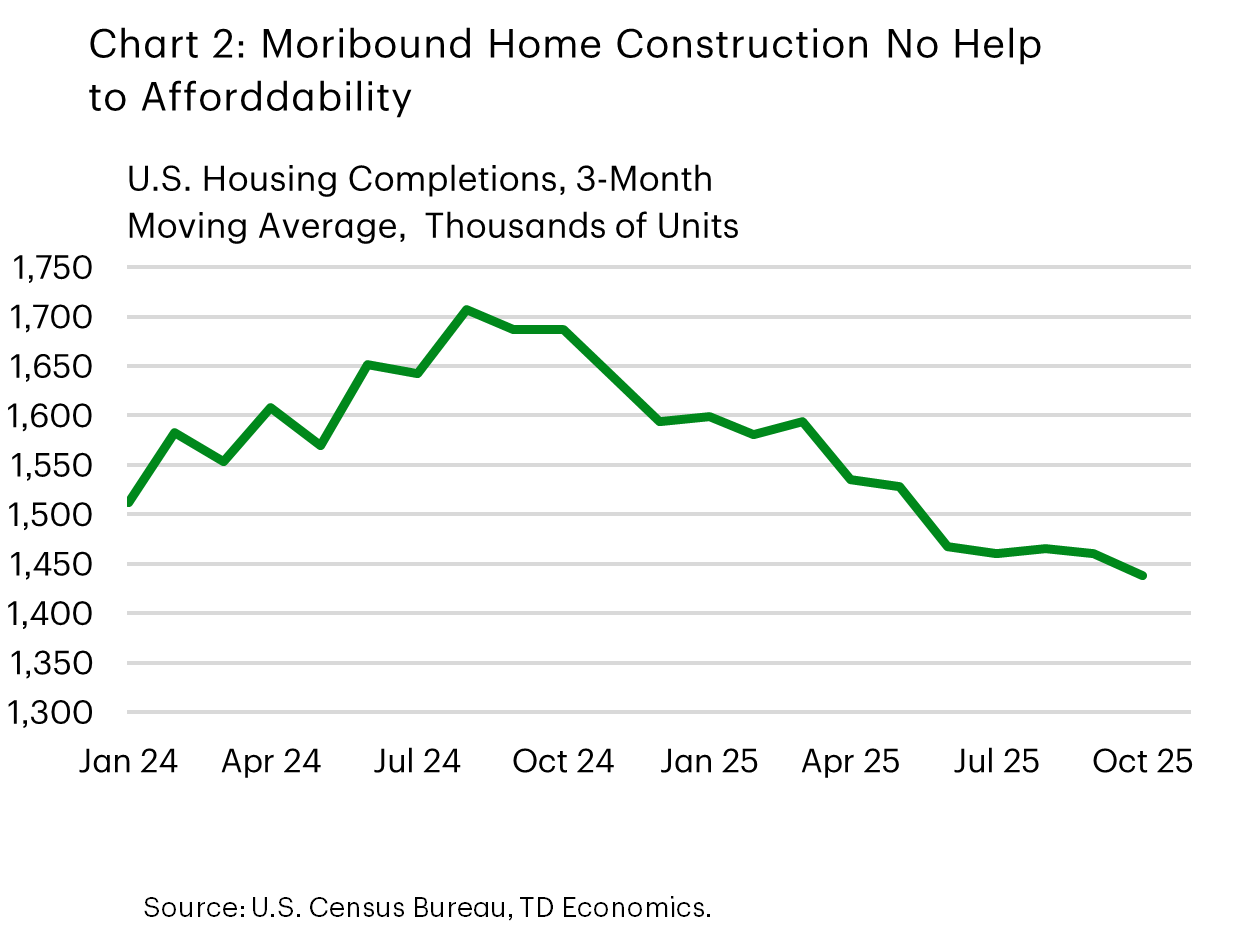

Developments in Venezuela added complexity to the oil market backdrop. Markets are assessing the administration’s commitment to the “Donroe Doctrine” and its implications for global oil supply. Despite Washington’s efforts to restore Venezuelan output, significant logistical and political hurdles remain. WTI moved down toward US$57 following the announcement that up to 50 million barrels of seized Venezuelan crude will be released to help address household affordability concerns. Adding to the affordability theme, housing data showed that homebuilding remains subdued, which doesn’t help the cost of housing (Chart 2). The administration has a clear desire to act on this front, promising a ban on institutional investor purchases and demanding government purchase mortgage-backed securities to help lower mortgage rates, though we await details on actual policy actions.

Prior to Friday’s jobs numbers, Federal Reserve officials suggested risks around employment and inflation were broadly balanced. Minneapolis President Kashkari indicated the labour market may be approaching equilibrium, while Richmond President Barkin characterized the economy as “finely tuned,” implying the FOMC would need to give equal weight to prices and employment. This reinforces our view and the view of the market that the FOMC is not in a hurry to cut rates further now, though we do expect to see interest rates come down later this year. We look ahead next week to the release of CPI inflation data, and after being let down by the Supreme Court this week, we are not going to be alone in being eager for news about when they may release decisions next.

Weekly Economic & Financial Commentary: Lukewarm Jobs Report Keeps March Rate Cut in Play

Summary

United States: Lukewarm Jobs Report Keeps March Rate Cut in Play

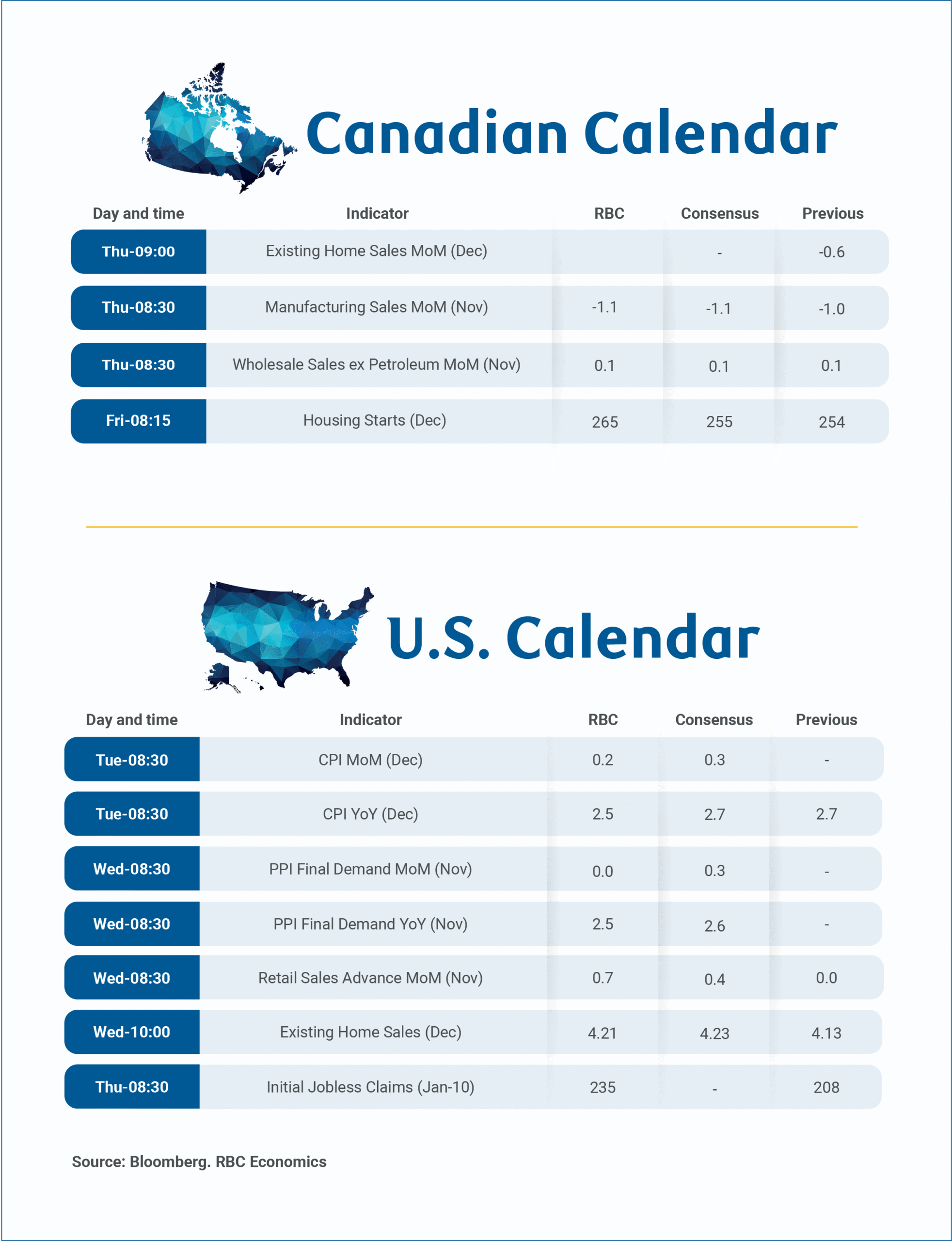

- The December labor data continued to signal a gradual and orderly cooling in the jobs market. We still view that the FOMC will be on hold at its upcoming Jan. 28 meeting and that a couple more rate cuts this year look likely amid the continued moderation in hiring. The Supreme Court did not rule on IEEPA tariffs Friday, but a decision could come as early as next week.

- Next week: CPI (Tue.), New Home Sales (Tue.), Retail Sales (Wed.)

International: Cooling Prices Dominate Global Data

- Global inflation data this week largely signaled easing, with declines in the Eurozone, Sweden, Australia and Mexico. Switzerland, Norway and China saw modest, likely temporary increases. Meanwhile, Japan’s wage growth came in softer than expected.

- Next week: India CPI (Mon.), U.K. Monthly GDP (Thu.)

Topic of the Week: Implications of U.S. Intervention in Venezuela

- Events in Venezuela this past weekend are top of mind for market participants, especially those with exposure to Latin America and oil. While the situation is very much riddled with uncertainty, we do not envisage material or long-lasting financial market disruptions on the basis that markets may have been prepared for political turnover in Venezuela.

Canada’s Manufacturing and Wholesale Reports to Point to Subdued Growth

Canadian manufacturing and wholesale reports for November should reinforce that heavily trade exposed sectors are still being negatively impacted by U.S. tariffs, even as we continue to expect increases in household spending to keep overall gross domestic product growth positive.

Statistics Canada's preliminary estimates showed a 1.1% decline in manufacturing sales in November, and a 0.1% increase in wholesales. The reported drop in manufacturing sales was despite a 1% rise in output prices, implying a larger decline in sale volumes.

Much of the weakness appears to have been concentrated in the auto sector— the number of vehicles produced was down 22% from a year ago in November in separately reported data, coinciding with the imposition of new U.S. tariffs on medium and heavy-duty trucks on Nov 1. StatsCan also flagged food manufacturing as a soft spot.

December home resale data on Thursday is expected to show a lackluster finish to 2025 as activity and prices moderated particularly in key markets like southern Ontario and B.C., where inventory is keeping buyers in a stronger negotiating position. Still, we continue to expect improvement in the Canadian economy, and the lagged impact of lower interest rates will support a gradual pick up in housing markets in 2026.

We look for housing starts on Friday to tick higher following a jump in permit issuance into October, and expect overall GDP growth to remain modestly positive in Q4 with continued growth in consumer spending. The advance estimate of retail sales showed a 1.2% increase in November.

In the U.S., we look for consumer price growth to slow on Tuesday and retail spending to remain firm on Wednesday.

2026 kicked off with a significant increase in geopolitical uncertainty, and headlines/fallout from U.S. military action in Venezuela will continue to be closely watched. The view that any significant shift in Venezuelan oil production would take many many years and would be unlikely in volume terms to meaningfully impact Canadian heavy oil production or sales to the United States. We have made no adjustments at this point to our Canadian or U.S. economic outlooks as a result.

Week ahead data watch:

December U.S. inflation data is expected to show soft core consumer price index (ex-food and energy) growth at 0.2% month-over-month, driven by persistent weakness in shelter costs, particularly rent and owners' equivalent rent. A sharp slowing in growth in the rent components between September and November was in part due to methodology issues resulting from the government shutdown that prevented collection/release of October CPI data, but we expect underlying rent price growth has also been slowing. Food prices likely ticked higher after surprising on the downside in November but gasoline prices declined, leaving headline CPI up a similar 0.2% month-over-month and 2.5% year-over-year.

We expect U.S. retail spending remained firm in November, driven in part by a rise in prices at gasoline stations, but also higher auto sales (unit vehicles sales rose 1.7% in November). Further growth in control (ex-auto, gas, and building material) store sales also build on the 0.9% jump in October.

Week Ahead – US CPI Might Challenge Geopolitics-Boosted Dollar

- Geopolitics may try to steal the limelight from US data.

- A possible US Supreme Court ruling on tariffs could dictate market movements.

- Dollar strength might be tested if investors refocus on Fed expectations.

- A crammed data calendar next week, US CPI comes on Tuesday; Fedspeak to intensify.

- Euro weakness persists, lingering risk of deterioration in US-EU relations.

Not the start most investors expected

At the tail end of 2025, most investors focused on Fed rate cut expectations and AI developments further reshaping the global economy. The nonexistent Santa Rally disappointed equity investors, but with most investment banks remaining quite optimistic about the 2026 performance, the mood could not be characterized as negative.

However, these expectations have been put aside, as US President Trump has other priorities. The transfer of Venezuelan President Maduro to the US to face heavy criminal charges and the control of Venezuela’s vast oil reserves, with US firms ready to invest heavily in the aging infrastructure, have changed the market narrative.

With every win, Trump becomes bolder in his strategy. Following the Maduro operation, his focus quickly shifted to Colombia, Cuba and Greenland, bolstering the USA’s foothold in the region after a period of relative inactivity. Greenland is the most intriguing case, as the US is trying to grab land from an ally and NATO member. Few expect this effort to fail, particularly as the US President has not excluded the military option to achieve his target.

Adding Iran to the mix, which was the main topic of discussion at the late-December meeting between Trump and Israel’s Netanyahu, means then 2025, with its tariff shenanigans and the April market rout, might end up being a walk in the park for investors compared to 2026.

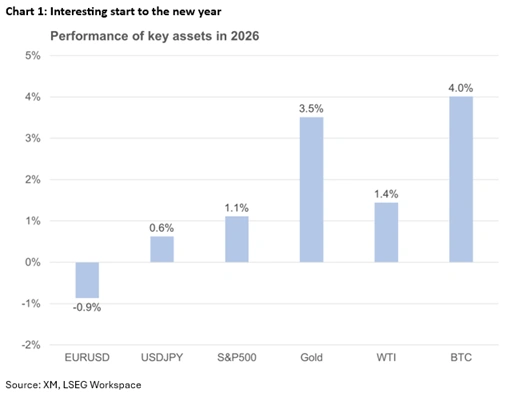

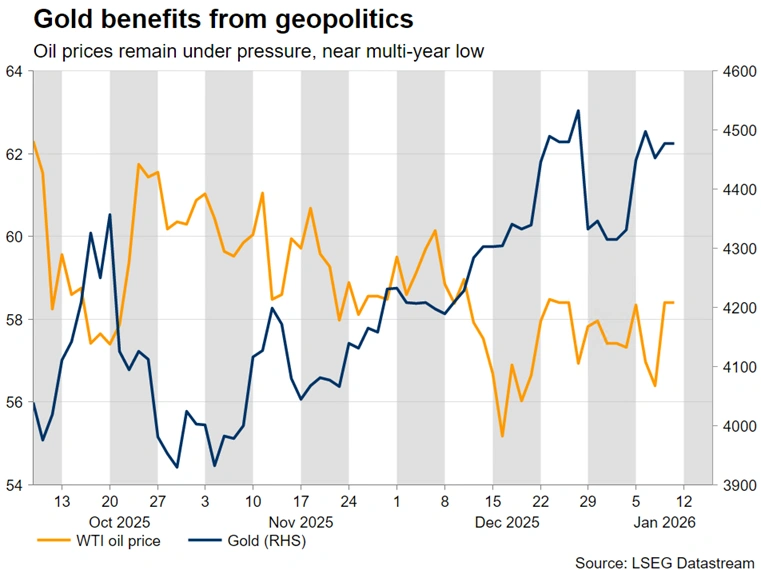

Gold remains bid, Oil near multi-year low

Both gold and oil have been quite responsive to the geopolitical developments, moving in opposite directions. Gold rallied towards the $4,500 level before correcting lower, partly dragged by silver’s erratic behaviour, while oil has been drifting lower as the excess supply story for 2026 could get even worse if US firms gradually restore the flow of Venezuelan oil. Coupled with decent chances of a Ukraine-Russia ceasefire, the outlook remains bleak for the oil market, with the five-year low of $55.19 around the corner.

Notably, Secretary of State Rubio is scheduled to visit Denmark next week, carrying Trump’s Greenland offer to Denmark, while the US President is expected to maintain his bold rhetoric on this issue. Gold stands ready to benefit from a likely deterioration of the EU-US relations and the previously unthinkable threat of military use in Greenland.

US tariffs in the spotlight

Amidst this volatile environment, there is growing speculation that on Friday, January 9, the US Supreme Court might announce its ruling on the legality of tariffs, after 10 am EST (3 pm GMT).

Should the ruling be positive, essentially confirming Trump’s ability to impose tariffs without Congress’s consent, Trump could restart his tariff rhetoric, targeting China and particularly Europe. He might feel compelled to threaten the EU with aggressive tariffs as a means to “acquire” Greenland.

If the ruling is negative, branding tariffs imposed using a 1977 law as illegal, Trump’s reaction could prompt an acute market reaction, although his administration has already drawn up a plan B to reimpose the existing tariffs under different legislation.

Gold stands ready to benefit under both aforementioned scenarios, particularly if the ruling deems current tariffs illegal. On the flip side, investors tend to shun the dollar during trade flare-ups, boosting other currencies like the euro and the Swiss franc.

What would be extremely interesting is if the Supreme Court sets boundaries to the President’s power, essentially limiting his ability to authorize tariffs or greenlight military operations without approval from Congress. Such a development could make Trump even more unpredictable going forward.

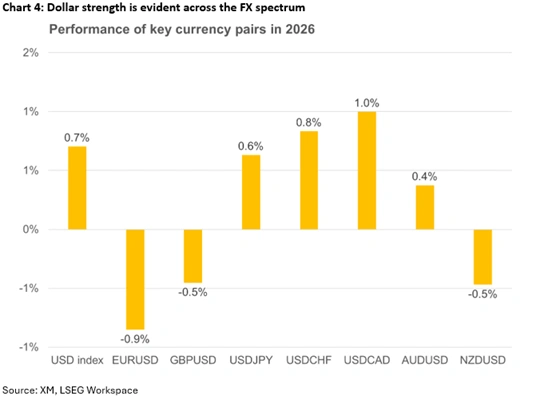

Normalcy might not suit the Dollar

The US dollar has started the new year on the right foot, outperforming both the euro and the pound, as developments regarding Venezuela have prompted an odd risk-off reaction in markets, with US equities also faring relatively well. The pound performance has been a surprise, with the focus now shifting to Thursday’s monthly GDP print for November.

On the other hand, the lack of new bullish catalysts is contributing to the euro’s current weakness. More importantly, considering Rubio’s visit to Denmark, the euro’s appeal might be dented by the possibility of an aggressive deterioration in US-EU relations, damaging the momentum built in the Eurozone economy due to the much-discussed aggressive fiscal spending. The ECB remains on the sidelines, but a severe economic downturn, mostly driven by a protracted trade flare-up, might be forced to reassess its current balanced policy stance.

US inflation data in the spotlight next week

Putting geopolitics aside, a return to normal newsflow might dent the dollar’s current appeal, as investors refocus on Fed rate cut expectations.

Stronger data releases, like Wednesday’s impressive ISM Services PMI survey, might keep the dollar bid, but investors are still convinced that the one rate cut pencilled in by policymakers in the December 2025 dot plot is too cautious. On the flip side, with around 60bps of easing currently priced in for 2026, investors are currently more comfortable with weaker data prints and appear ready to sell the dollar.

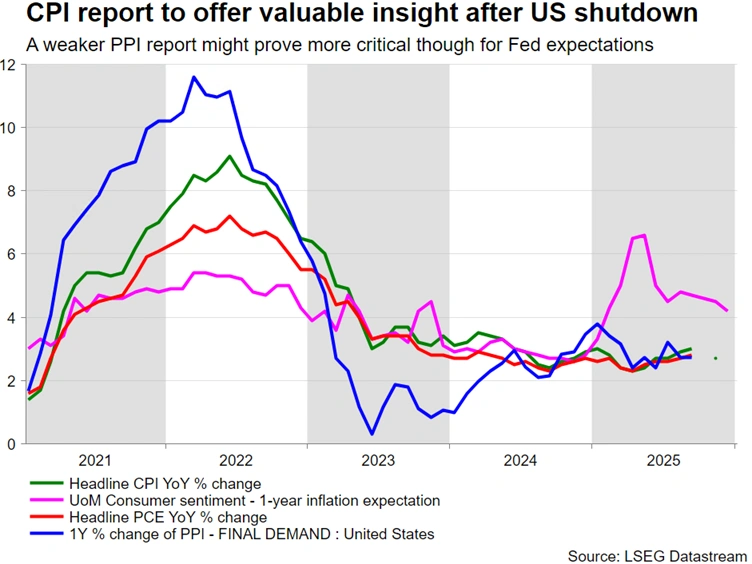

Next week, the calendar is crammed with pivotal data, mostly focusing on inflation and the consumer side of the US economy. On Tuesday, the December CPI report will be in the spotlight, the first inflation print potentially not affected by the US government shutdown.

Another deceleration in price pressures, partly contradicting Fed members’ expectations for near-term inflation to remain elevated, as seen in the December 10 Fed meeting minutes, would potentially play into the hands of the new Fed Chair, potentially bringing forward the first 25bps rate cut currently priced in for mid-June. Notably, Trump has been mum on the name of Powell’s replacement.

On Wednesday, retail sales and producer price index data for November will be released, with the former giving significant insight into consumer spending appetite. A strong set of figures could beef up the current 2.7% growth forecast by the Atlanta Fed GDPNow model.

Meanwhile, after a relatively quiet period, Fedspeak is expected to intensify. The next Fed meeting is just 20 days away, which means that Fed members have to put their arguments across ahead of the usual blackout period. The focus will be on the more hawkish voting members, like Cleveland’s Hammack and Dallas’ Logan. Interestingly, the doves clearly have the upper hand this year in terms of the votes, adding to expectations for a persistently dovish Fed stance in 2026.

Most FX pairs are at the Dollar’s mercy

It has been a difficult start to the new year for peripheral currencies. Central bank rate expectations should be at the forefront, but, for now, dollar strength is dominating the moves. Apart from the Aussie, which is marginally gaining against the greenback, the remaining currencies are on the back foot at this stage versus the dollar, despite their respective central banks completing their easing cycles.

Specifically, developments with Venezuela could turn into a serious headache for Canada. A good part of Canada’s production is heavy oil, which is also the dominant product of Venezuela, further denting PM Carney’s bargaining power with President Trump, who is not the biggest fan of Canada.

Similarly, Australia is closely monitoring China’s newsflow. There is a renewed attempt by Chinese authorities to improve the situation on the ground by expediting investment plans and further allowing banks to address bad loans, in order to beef up their financial health and profitability. Notably, on Wednesday, Chinese trade balance data for December will be published, with investor attention on whether exports maintain their recent robust annual pace of increase and imports continue to grow, validating China’s efforts to prop up domestic demand.

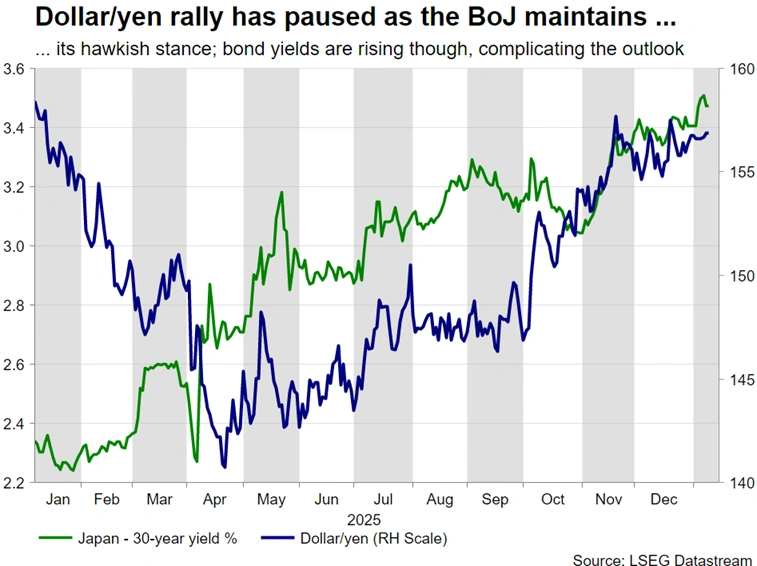

Finally, the yen has been resisting the dollar’s strength, courtesy of the hawkish BoJ. Investors are trying to bring forward the next rate hike, currently priced in for September, but mixed data have been muddling the outlook. The BoJ will probably have to wait until the Shunto round, which realistically means that the April meeting is the key one for the next move. Until then, Japanese government officials will probably continue to verbally intervene to keep dollar/yen well below the ¥160, unless of course, the Fed surprises with a Q1 rate cut.

Weekly Focus – Focus Remains on Geopolitics

The year 2026 started eventful - but less so in economics, and more so in geopolitics. In our Geopolitical Radar: What's next after US assault on Venezuela? 9 January, we write how President Trump has already verbally attacked other countries in its neighbourhood, namely Mexico and Colombia. Furthermore, over the past week, the US administration has repeated its interest in making Greenland part of the US instead of it being a largely independent part of the Danish realm. Politically, that is of course a very important issue for Denmark, but not for economic reasons. Read more in our Flash Comment Denmark - Greenland has only limited impact of the Danish economy, 7 January.

As we write in our Geopolitical Radar, we think that the most likely next target of the US administration could be Iran's Islamic regime. The bombardment in June that targeted Iran's nuclear facilities resulted in only a temporary setback for Iran's nuclear program. As the US now has access to Venezuelan oil reserves, it might be less concerned with a potential Iranian retaliation that might disrupt oil trade in the Persian Gulf, and importantly, current anti-government protests in Iran could give the US-Israeli alliance a pretext to intervene.

Come what may, thus far markets have completely shrugged off events in Venezuela. Brent oil price is up only two dollars since the US attack, and futures curve is little changed as well. The limited reaction in the oil market is understandable. Despite of having the world's largest proved oil reserves, Venezuela's share of world oil supply is a mere 1%. Furthermore, Venezuelan oil is heavy and sour, making it more expensive to process. American refineries on the Gulf Coast are equipped to process such qualities, but the more relevant question is whether it makes economic sense to invest in Venezuela. According to estimates, the breakeven oil price for new projects in Venezuela is USD 80, and as there is already excess supply in the world market, prices are expected to stay much lower in the near future.

In the first weeks of 2026 it seems focus will most likely remain on geopolitics. Large economies remain on track and have been largely immune to geopolitical turbulence. Chinese and European exports have been robust despite facing higher tariffs in the US, and American businesses and consumers are only gradually starting to pay the price. In the coming two years, we expect economic growth close to trend levels in both the US and the euro area. We expect two more rate cuts from the Fed, while for the ECB, we foresee no rate changes in the forecast horizon.

Next week's economic calendar is almost empty. In Europe, we get the euro area Sentix indicator on Monday, showing the first estimate of investor confidence in 2026. On Thursday, the German statistics agency published the first full-year 2025 GDP estimate, thereby giving the first indication of Q4 GDP growth. In the UK, November GDP data is due on Thursday. In the US, the key data release of the week will be the December CPI. The previous November release was potentially distorted by data collection delays after the government shutdown, which might have caused Black Friday discounts to have an outsized negative impact on the data. Reversal of these effects is likely to lift December CPI, and we forecast above consensus prints.

US UoM consumer sentiment rises to four-month high, inflation expectations steady

US consumer sentiment improved modestly in January, with the University of Michigan index rising from 52.9 to 54.0, its highest level since September. Current Economic Conditions Index climbed from 50.4 to 52.4, while the Expectations Index ticked up from 54.6 to 55.0.

The survey noted that concerns about tariffs are gradually easing, though respondents remain guarded about the broader strength of business conditions and the labor market.

On inflation, year-ahead expectations held steady at 4.2%, the lowest reading since January 2025. Longer-run expectations edged up slightly from 3.2% to 3.4%, but remain well below last year’s peaks.

Sunset Market Commentary

Markets

The Fed is off the hook for January. December payrolls downwardly surprised, but from a market (and a Fed) point of view the situation on the labour market didn’t deteriorate. The economy added 50k jobs (vs 70k consensus) with a 76k downward revision to October/November numbers. Details showed a modest rebound in government payrolls (+13k) following heavy job cuts in October (-174k; delayed DOGE-effect). Job cuts were mainly centered in the goods-producing sector (-21k) while private services added 58k jobs. Within those broad services, retail trade remains an underperformer with three consecutive months of job losses. A lot of attention went to the unemployment rate which, partly because of seasonality and annual revisions for the household survey, dipped from a downwardly revised 4.5% in November to 4.4%. Household employment rose by 232k according to that survey with total household employment hitting an all-time high at just shy of 164mn. Average hourly earning rose by 0.3% M/M and accelerated from 3.6% Y/Y to 3.8% Y/Y, matching the fastest pace since July 2025. US money markets reduced remaining 25 bps rate cut bets for the January 28 FOMC meeting from 15% to only 5%. The next move is only fully discounted by the June FOMC meeting, suggesting the Fed is done cutting policy rates under Chair Powell. The US yield curve bear flattens slightly with yields adding 1.5 bps (30-yr) to 2.7 bps (2-yr). The dollar traded volatile after the release but EUR/USD 1.1650 remains name of the game. US equity markets opened with 0.2%-0.4% gains. A potentially big event risk is concentrated at the Supreme Court later today. It could issue an opinion on Trump’s reciprocal tariffs that may or may not result in actual rulings to either keep them in place or strike them down. The latter would undoubtedly introduce new uncertainty: What will happen to the current trade deals? What other tariff routes are there for the US government? How quickly can these get implemented and how different are the tariff rates going to be? Rising risk premia would probably lift long-term US bond rates but the jury remains out whether and how it’ll affect other US asset classes (equities, the dollar).

News & Views

The UN’s Food and Agricultural Organization (FOA) food index eased further by 0.8% m/m in December of last year as declines in the prices for dairy products, meat and vegetable oils more than offset (modest) increases in cereals and sugar. Overall, the index showed rather mild swings during 2025, but with divergent trends in the major subcategories. The index closed 2.3% below the level at the end of 2024. Still, despite the gradual decline in H2 2025, the index average over 2025 was 4.3% higher compared to the 2024 average. The end-2025 level was 22.4% below the peak reached in March 2022. Cereal prices added 1.7% m/m in December. For the whole of 2025, the cereal price Index was 4.9% below the 2024 level, marking the lowest annual average since 2020. Especially prices of rice declined sharply (-35.2% average). The vegetable oil price index decreased marginally (0.4% m/m). For the year 2025, vegetable oil prices rose 17.1% y/y marking a three-year high amid tight global supplies. The sugar price index rose 2.4% m/m after three consecutive monthly declines, but it remained 24% below its level a year ago. The average index over 2025 also marked the lowest level since 2020.

After three consecutive months of unexpected sharp rises in Canadian job growth (totaling 181k), the Canadian economy added a modest 8.2k jobs in December (vs -2.5k consensus). The unemployment rate rose from 6.5% to 6.8%, but Statistics Cananda indicated that this was due to a rise in the participation rate (65.4%) as more people were looking for work. The rise in the unemployment rate also is seen as partially reversing a cumulative decline of 0.6% over the previous two months. Overall, 1.6mn people were unemployed in December (+73k compared to November). Average hourly earnings eased slightly from 3.6% Y/Y to 3.4%. The market reaction was limited as it probably won’t change the policy assessment of the Bank of Canada. The BoC likely finished its easing cycle end October (2.25%). This level should be adequate to hold inflation near 2% while helping the economy through current period of structural adjustment. Markets err on the side of a first rate hike by the end of the year (50%), but this remains a highly conditional call. The loonie cedes marginal to trade near USD/CAD 1.388.

US: Payrolls Rise by 50k in December, While Unemployment Rate Ticks Down to 4.4%

Non-farm payrolls rose by 50k in December, slightly below the consensus forecast of 70k. Job gains for the two prior months were revised lower by a total of 76k. The bulk of the downward revisions were concentrated in October (-68k), coinciding with the government shutdown.

- For 2025, the economy added 584k jobs, well below the 2.0 million added the year prior.

Private payrolls added 37k new positions last month, down slightly from the 50k reported in November. Jobs gains were concentrated in leisure & hospitality (+47k) and health care & social assistance (+38.5k). Meanwhile, retail trade (-25k), construction (-11k), professional & business services (-9k), and manufacturing (-8k) all recorded jobs losses. Government added 11k.

In the household survey, the unemployment rate ticked down to 4.4% (previously 4.5%) as civilian employment (+232k) rose while the labor force (-42k) was slightly lower. The labor force participation rate ticked down to 62.4% (from 62.5% in November).

- The Bureau of Labor Statistics also revised its seasonal adjustment factors for 2025, which were small on balance, but did lower November's unemployment rate to 4.5% (previously reported at 4.6%).

Average hourly earnings rose 0.3% month-on-month (m/m), following an upwardly revised 0.2% m/m gain (previously 0.1% m/m) in November. Relative to December 2024, wages are up 3.8% (from 3.6% in November).

Key Implications

The labor market appears to have stabilized at the end of last year. Smoothing through volatility, private payrolls have largely steadied in recent months while the unemployment rate ticked down from its cycle high reached in November. But make no mistake, the combination of big policy changes and a significant ramp-up in AI investments resulted in a measurable softening in the job market last year, with the economy adding only a third of the jobs was created in 2024.

This morning's report should provide policymakers with further reassurance that the labor market is stabilizing, supporting the case for a "pause" on rate cuts. Market pricing on Fed futures were little changed following the release, with the next rate cut not fully priced until June.

Canada’s Unemployment Rate Jumps as Labour Force Expands to Close 2025

Canada's economy added 8k jobs in December (+0.0% month/month), 10k more than consensus expectations for a 2.5k decline. The details were healthier, with full-time positions rising 50k, while part time decline 42k. In the twelve months to December part-time work advanced 2.6% (+99k) while full-time work rose 0.7% (+128k).

The unemployment rate rose to 6.8% from 6.5% in November (consensus expectations were for a rise to 6.7%) and is 0.1 percentage points (ppts) above the 6.7% last December. The unemployment rate was lifted by 81k entrants into the labour force. This boosted the labour force participation rate by 0.3 ppts – its highest level since July and in line with December 2024.

Job gains were once again concentrated in health care and social assistance (+21k), with other services (+15k) and construction (+11k) also being notable contributors. The biggest losses were in professional, scientific and technical services (-18k), and accommodation and food services (-12k).

Wage growth slowed in December, with average hourly wages up 3.4% versus a year ago (3.6% in November).

Key Implications

After a string of upside surprises, the Canadian labour market gave back some of its gains in December, with job growth effectively petering out, and the unemployment rate ticking higher as more people started looking for work. In a noisy data series, this is not all that surprising and remains in line with our view that the labour market is not yet out of the woods.

This report is unlikely to move the needle for the Bank of Canada. There is still slack in the labour market, but uncertainty about the supply side of the economy and the risk to inflation means they are unlikely to tip the policy rate into accommodative territory.