Sample Category Title

USD/CAD Weekly Outlook

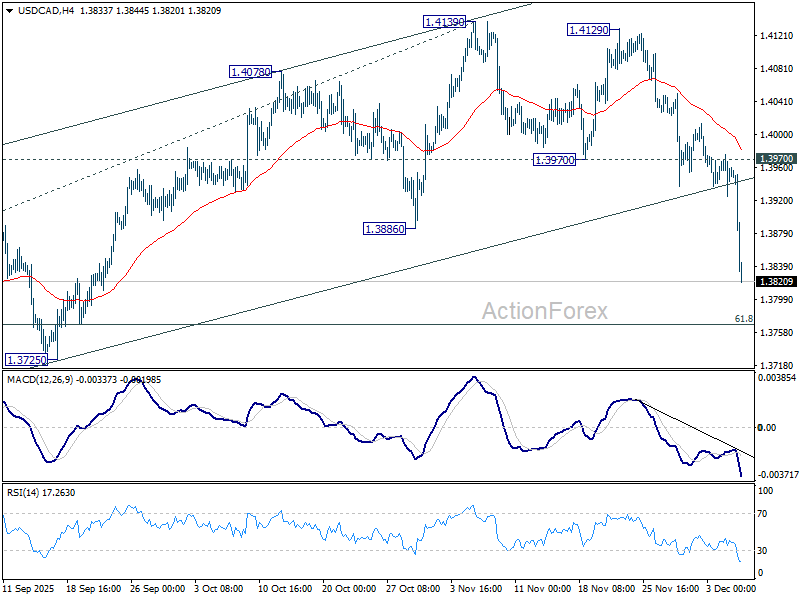

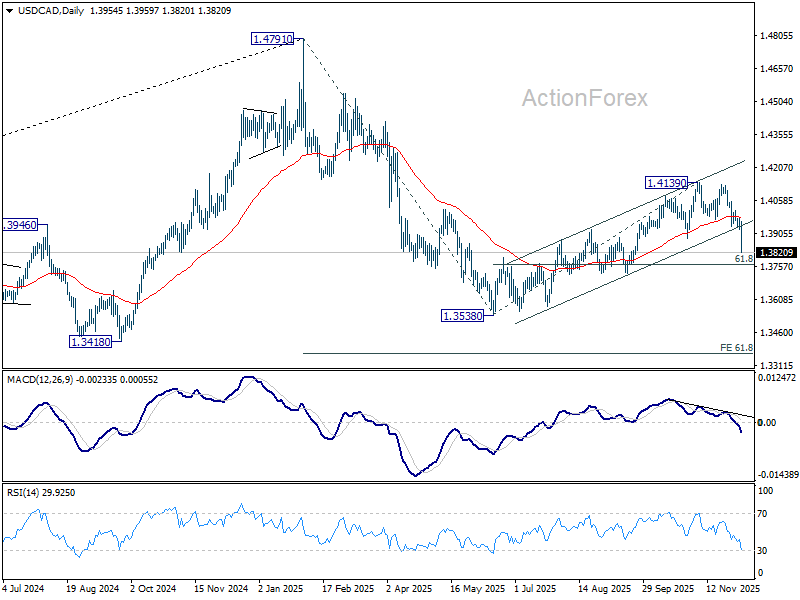

USD/CAD's steep decline last week suggests that rise from 1.3538 has already completed at 1.4139. Initial bias remains on the downside this week for 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low. For now, risk will stay on the downside as long as 1.3970 support turned resistance holds, in case of recovery.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

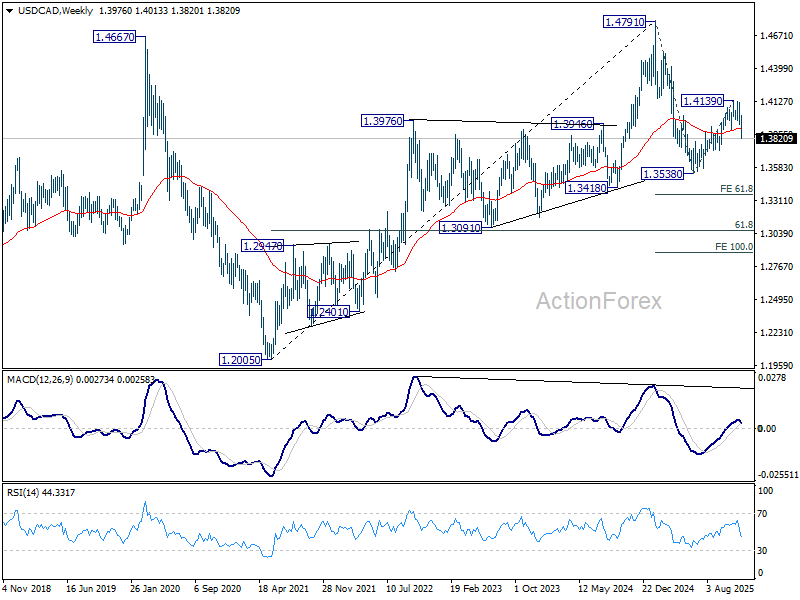

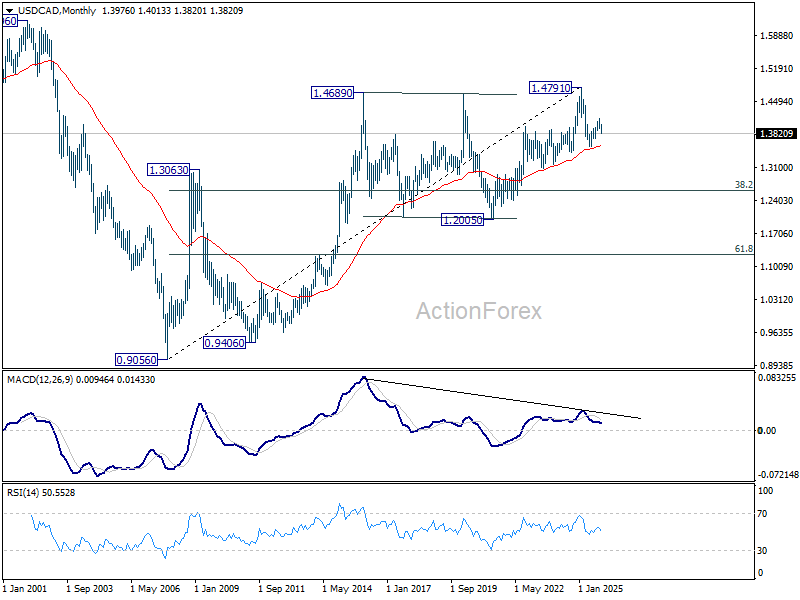

In the long term picture, rising 55 M EMA (now at 1.3567) remains intact. Thus, up trend from 0.9056 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction. to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

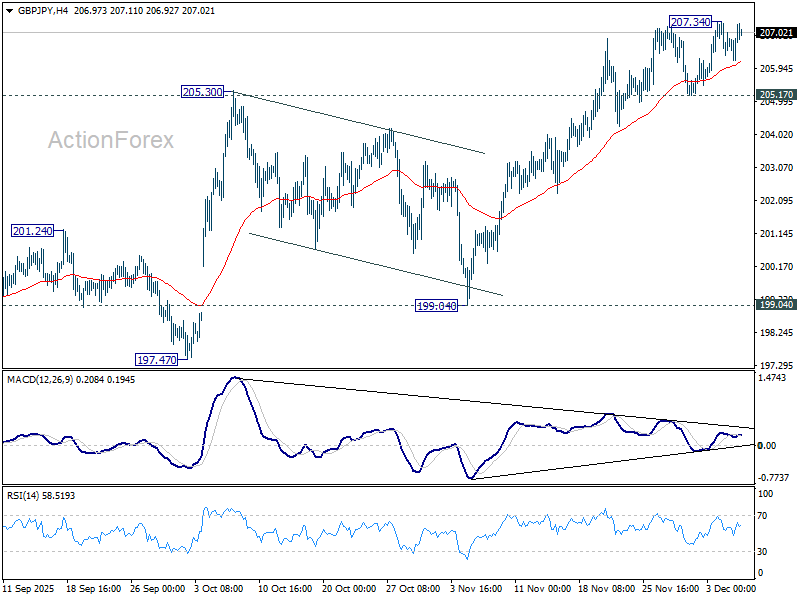

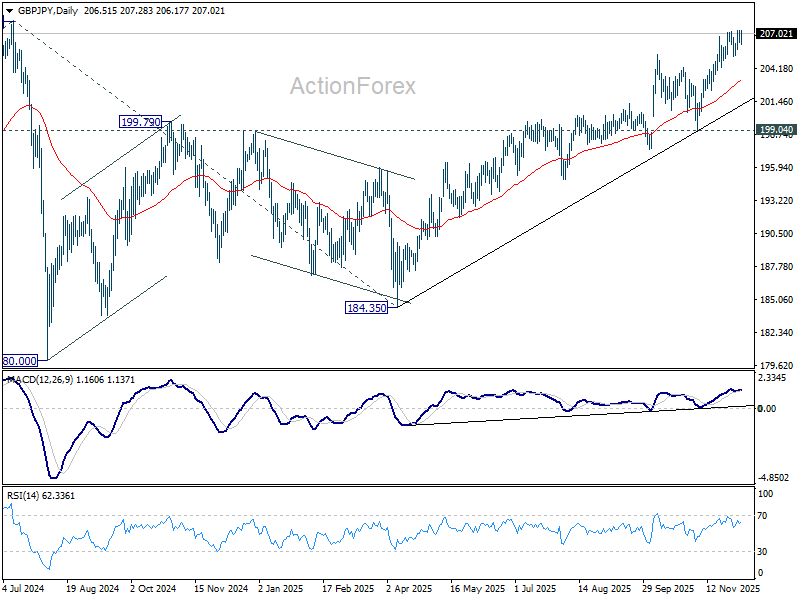

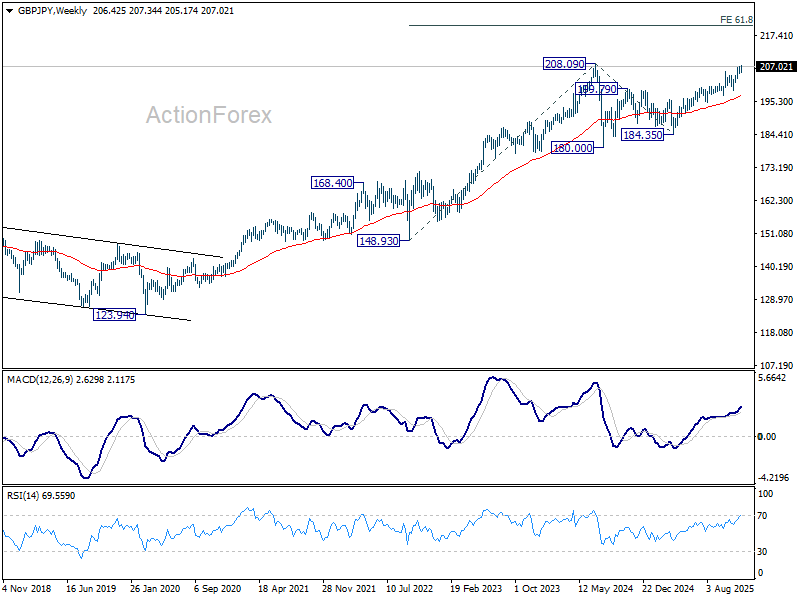

GBP/JPY Weekly Outlook

GBP/JPY edged higher to 207.34 but quickly retreated. Initial bias stays neutral this week first, but further rise is expected as long as 205.17 support holds. Break of 207.34 will resume the rally from 184.35 and target 208.09 high. However, break of 205.17 support will turn bias to the downside for deeper pullback, possibly to 55 D EMA (now at 203.25).

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

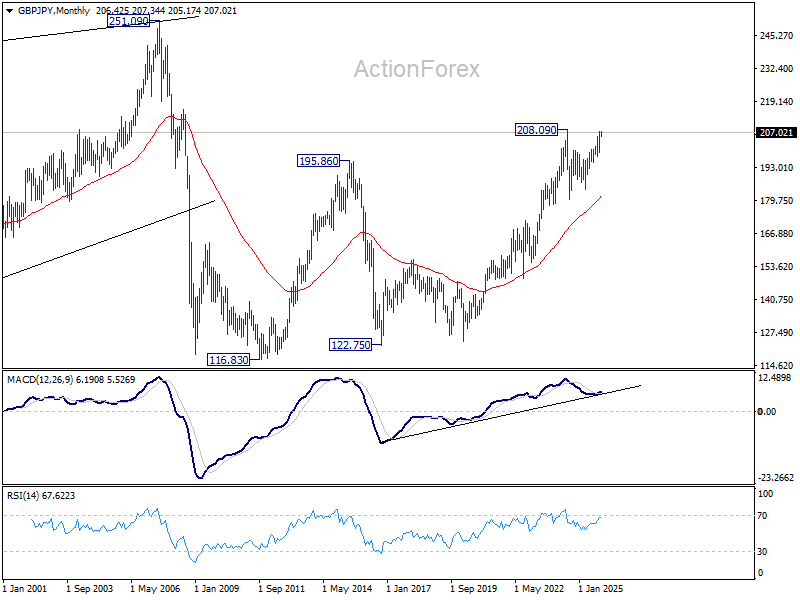

In the long term picture, there is no sign that the long term up trend from 122.75 (2016 low) has concluded. But firm break of 208.09 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

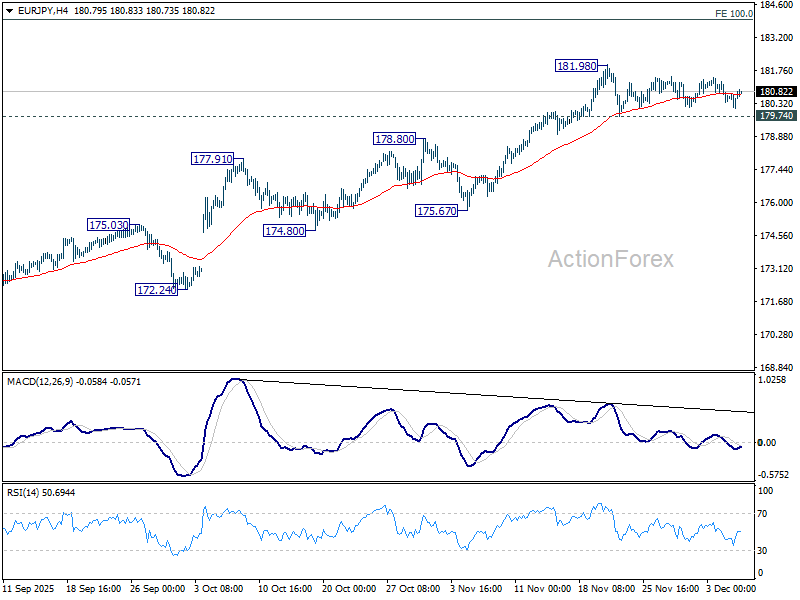

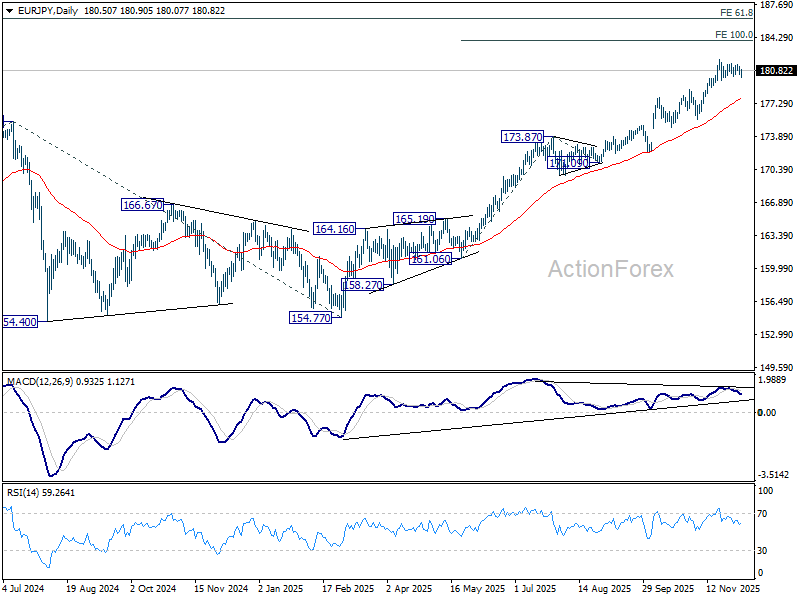

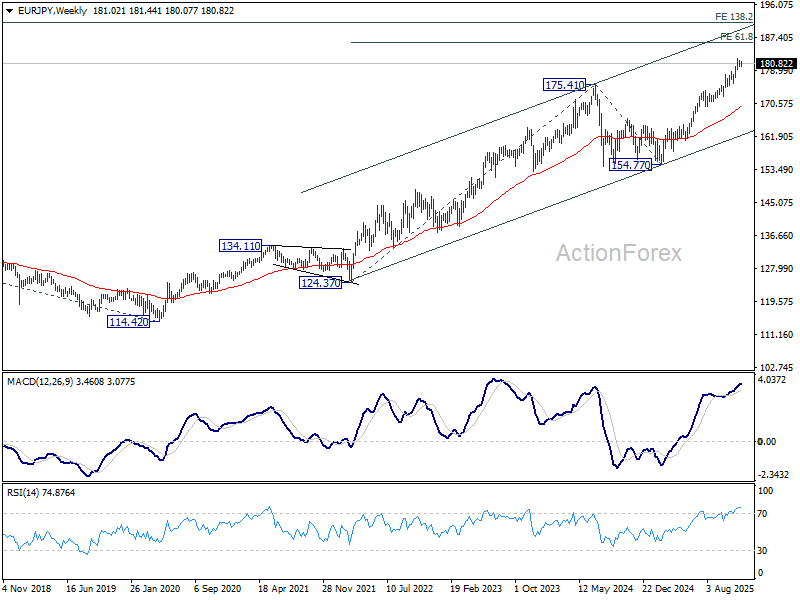

EUR/JPY Weekly Outlook

EUR/JPY stayed in established range below 181.98 last week and outlook is unchanged. Initial bias remains neutral this week first, and further rally is expected with 179.74 support intact. On the upside, break of 181.98 will resume larger up trend to 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 177.84).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, considering bearish divergence condition in D MACD, upside should be capped by 186.31 on first attempt. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.87) holds, even in case of deep pullback.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

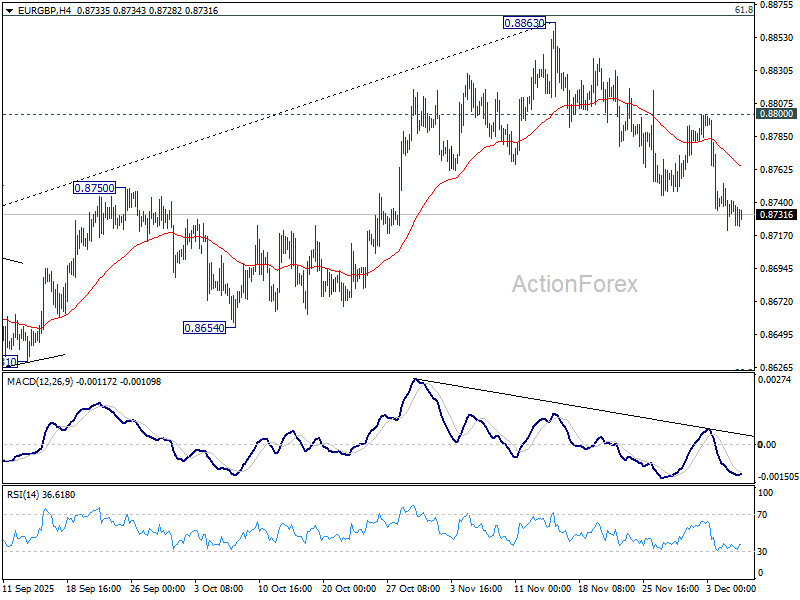

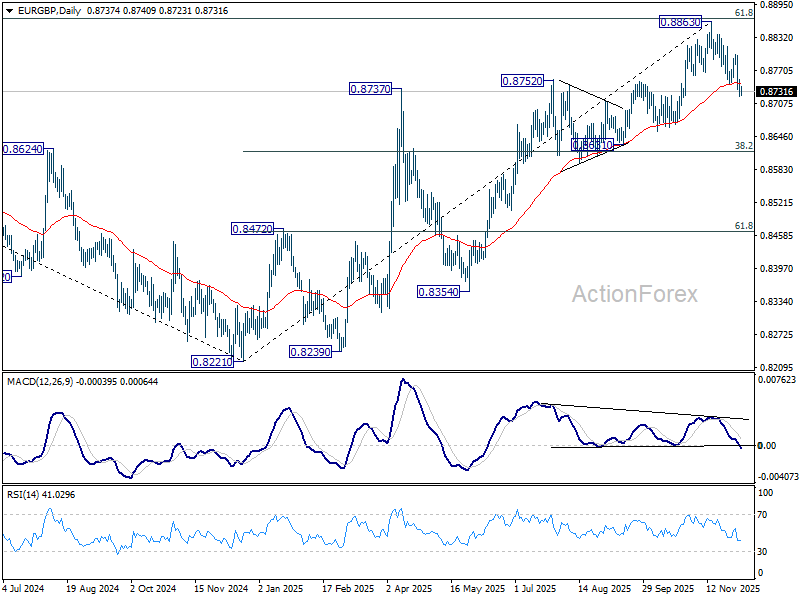

EUR/GBP Weekly Outlook

EUR/GBP's fall from 0.8863 extended last week and the break of 55 D EMA (now at 0.8745) should confirm rejection by 0.8867 key fibonacci level. Initial bias stays on the downside this week for 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). For now, risk will stay on the downside as long as 0.8800 resistance holds, in case of recovery.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

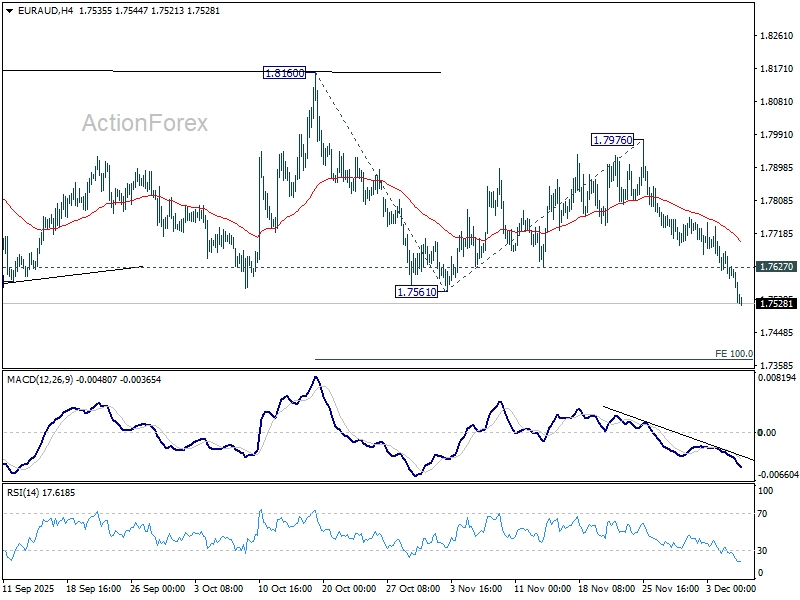

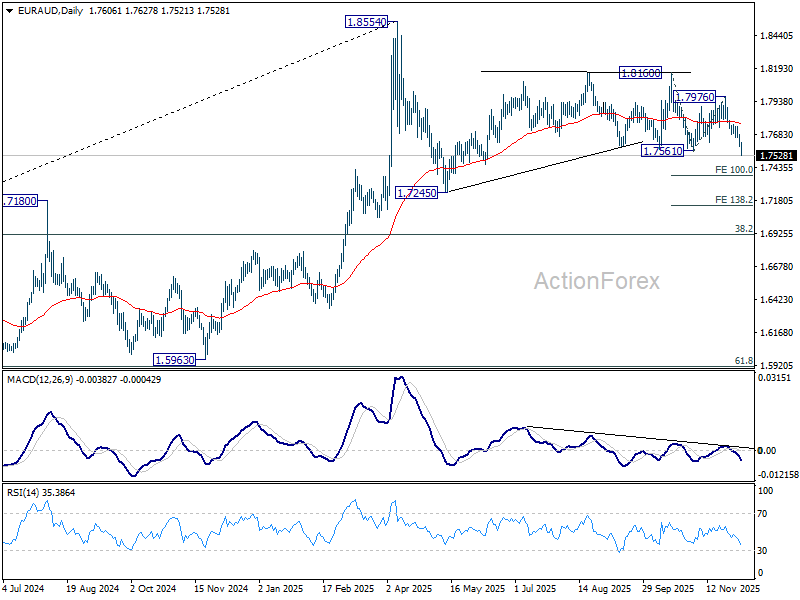

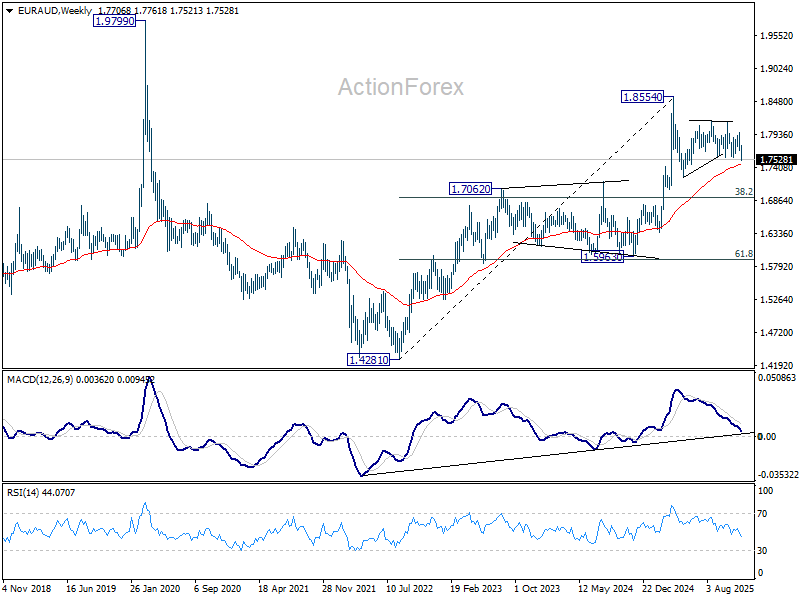

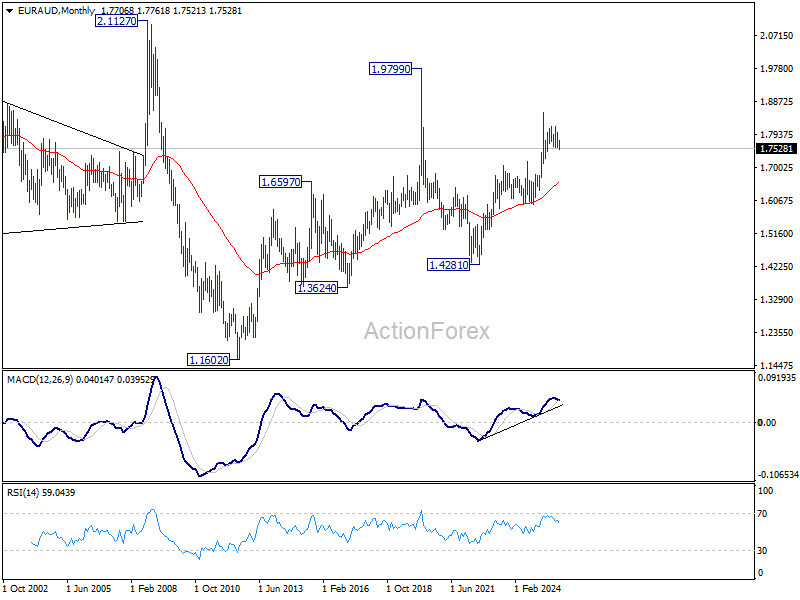

EUR/AUD Weekly Outlook

EUR/AUD's steep decline and solid break of 1.7561 support confirms resumption of fall from 1.8160. More importantly the whole pattern from 1.8554 should now be in its third leg. Initial bias stays on the downside this week for 100% projection of 1.8160 to 1.7561 from 1.7976 at 1.7377. Firm break there will pave the way to 138.2% projection at 17148. On the upside, above 1.7627 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, as long as 55 W EMA (now at 1.7449) holds, price actions from 1.8554 could still be a correction to rise from 1.5963 only. However, sustained break of the EMA will argue that it's already correcting the whole up trend from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6579) holds, this second leg could still extend higher.

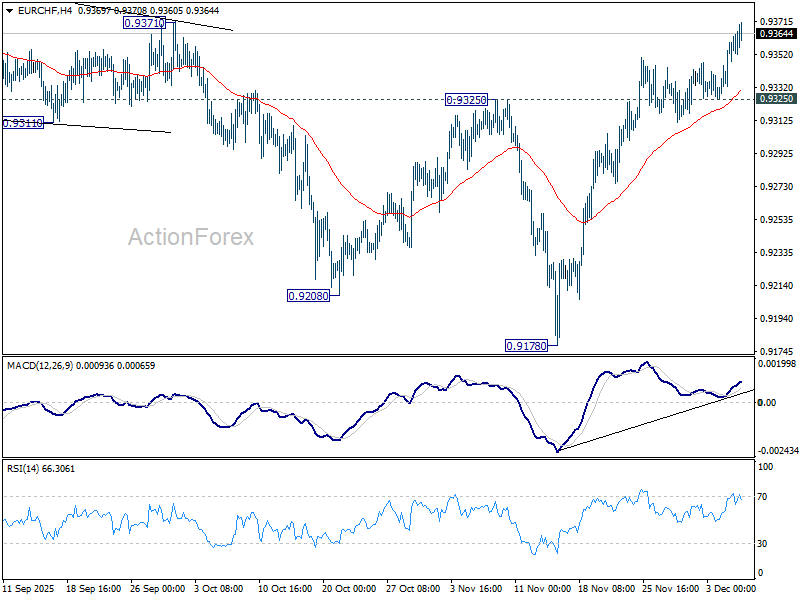

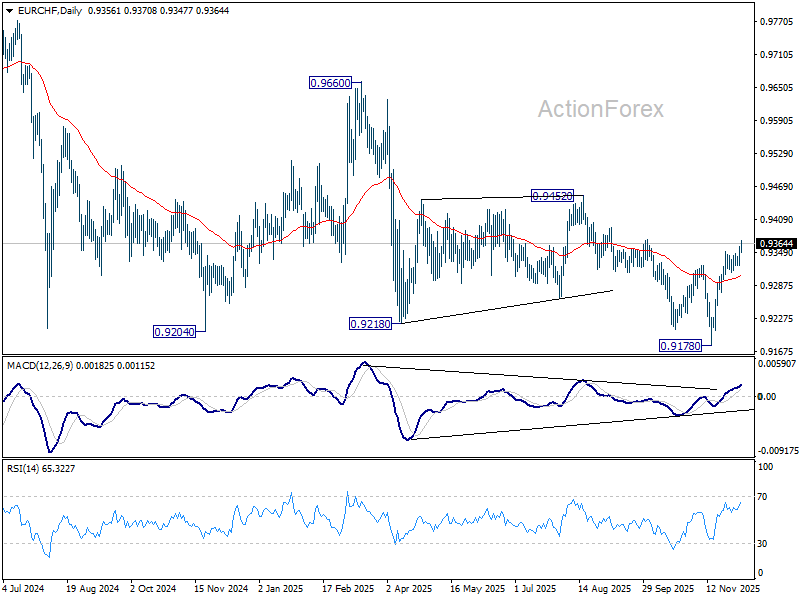

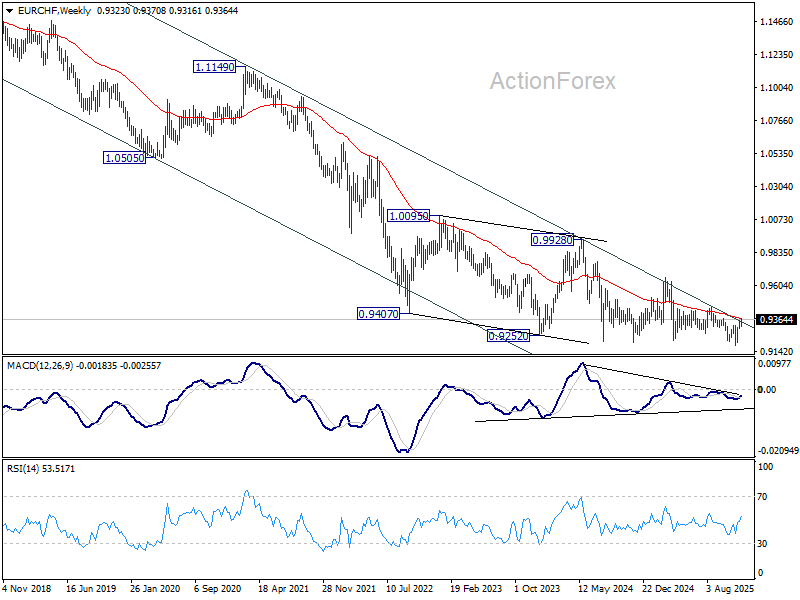

EUR/CHF Weekly Outlook

EUR/CHF's rally from 0.9278 short term bottom resumed last week and the development solidify that case that fall from 0.9660 has completed. Initial bias stays on the upside this week for 0.9452 key structural resistance. Decisive break there will carry larger bullish implications. For now, risk will stay on the upside as long as 0.9325 support holds, in case of retreat.

In the bigger picture, EUR/CHF has breached long term falling channel resistance as the rebound from 0.9278 extends. Considering bullish convergence condition in W MACD, sustained trading above 55 W EMA (now at 0.9316) will indicate medium term bottoming, and suggests that it's already in larger scale rebound. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9228 resistance next. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9278 at a later stage.

In the long term picture, overall long term down trend from 1.2004 (2018 high) is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as falling 55 M EMA (now at 0.9785) holds.

Summary 12/8 – 12/12

Monday, Dec 8, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 2.20% | 1.90% |

| 23:50 | JPY | GDP Deflator Y/Y Q3 | 2.80% | 2.80% |

| 23:50 | JPY | GDP Q/Q Q3 F | -0.50% | -0.40% |

| 23:50 | JPY | GDP Annualized Q3 F | -2.00% | -1.80% |

| 23:50 | JPY | Current Account (JPY) Oct | 3.00T | 4.35T |

| 03:00 | CNY | Trade Balance (USD) Nov | 105.0B | 90.1B |

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 49.5 | 49.1 |

| 07:00 | EUR | Germany Industrial Production M/M Oct | 0.50% | 1.30% |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | -6.3 | -7.4 |

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 1.40% | 1.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | |

| Forecast: 2.20% | Previous: 1.90% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q3 | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 23:50 | JPY | GDP Q/Q Q3 F | |

| Forecast: -0.50% | Previous: -0.40% | ||

| 23:50 | JPY | GDP Annualized Q3 F | |

| Forecast: -2.00% | Previous: -1.80% | ||

| 23:50 | JPY | Current Account (JPY) Oct | |

| Forecast: 3.00T | Previous: 4.35T | ||

| 03:00 | CNY | Trade Balance (USD) Nov | |

| Forecast: 105.0B | Previous: 90.1B | ||

| 05:00 | JPY | Eco Watchers Survey: Current Nov | |

| Forecast: 49.5 | Previous: 49.1 | ||

| 07:00 | EUR | Germany Industrial Production M/M Oct | |

| Forecast: 0.50% | Previous: 1.30% | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | |

| Forecast: -6.3 | Previous: -7.4 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | |

| Forecast: 1.40% | Previous: 1.60% | ||

Tuesday, Dec 9, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Nov | 2.40% | 1.50% |

| 00:30 | AUD | NAB Business Confidence Nov | 6 | |

| 00:30 | AUD | NAB Business Conditions Nov | 9 | |

| 03:30 | AUD | RBA Interest Rate Decision | 3.60% | 3.60% |

| 04:30 | AUD | RBA Press Conference | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | 16.80% | |

| 07:00 | EUR | Germany Trade Balance (EUR) Oct | 15.8B | 15.3B |

| 11:00 | USD | NFIB Business Optimism Index Nov | 98.4 | 98.2 |

| 23:50 | JPY | PPI Y/Y Nov | 2.70% | 2.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Nov | |

| Forecast: 2.40% | Previous: 1.50% | ||

| 00:30 | AUD | NAB Business Confidence Nov | |

| Forecast: | Previous: 6 | ||

| 00:30 | AUD | NAB Business Conditions Nov | |

| Forecast: | Previous: 9 | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 04:30 | AUD | RBA Press Conference | |

| Forecast: | Previous: | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | |

| Forecast: | Previous: 16.80% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Oct | |

| Forecast: 15.8B | Previous: 15.3B | ||

| 11:00 | USD | NFIB Business Optimism Index Nov | |

| Forecast: 98.4 | Previous: 98.2 | ||

| 23:50 | JPY | PPI Y/Y Nov | |

| Forecast: 2.70% | Previous: 2.70% | ||

Wednesday, Dec 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Nov | 0.70% | 0.20% |

| 01:30 | CNY | PPI Y/Y Nov | -2.10% | -2.10% |

| 13:30 | USD | Employment Cost Index Q3 | 0.90% | 0.90% |

| 14:45 | CAD | BoC Interest Rate Decision | 2.25% | 2.25% |

| 15:30 | CAD | BoC Press Conference | ||

| 15:30 | USD | Crude Oil Inventories (Dec 5) | 0.6M | |

| 19:00 | USD | Fed Interest Rate Decision | 3.75% | 4.00% |

| 19:30 | USD | FOMC Press Conference | ||

| 21:45 | NZD | Manufacturingles Q3 | -2.90% | |

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | 4.2 | 3.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Nov | |

| Forecast: 0.70% | Previous: 0.20% | ||

| 01:30 | CNY | PPI Y/Y Nov | |

| Forecast: -2.10% | Previous: -2.10% | ||

| 13:30 | USD | Employment Cost Index Q3 | |

| Forecast: 0.90% | Previous: 0.90% | ||

| 14:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 2.25% | Previous: 2.25% | ||

| 15:30 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 15:30 | USD | Crude Oil Inventories (Dec 5) | |

| Forecast: | Previous: 0.6M | ||

| 19:00 | USD | Fed Interest Rate Decision | |

| Forecast: 3.75% | Previous: 4.00% | ||

| 19:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Manufacturingles Q3 | |

| Forecast: | Previous: -2.90% | ||

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | |

| Forecast: 4.2 | Previous: 3.8 | ||

Thursday, Dec 11, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Nov | -21% | -19% |

| 00:30 | AUD | Employment Change Nov | 20.0K | 42.2K |

| 00:30 | AUD | Unemployment Rate Nov | 4.40% | 4.30% |

| 08:30 | CHF | SNB Interest Rate Decision | 0.00% | 0.00% |

| 09:00 | CHF | SNB Press Conference | ||

| 13:30 | CAD | Trade Balance (CAD) Oct | -4.9B | -6.3B |

| 13:30 | USD | Initial Jobless Claims (Dec 5) | 205K | 191K |

| 13:30 | USD | Trade Balance (USD) Sep | -65.5B | -59.6B |

| 15:00 | USD | Wholele Inventories Sep F | 0.10% | 0.00% |

| 15:30 | USD | Natural Gas Storage (Dec 5) | -12B | |

| 21:30 | NZD | Business NZ PMI Nov | 51.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Nov | |

| Forecast: -21% | Previous: -19% | ||

| 00:30 | AUD | Employment Change Nov | |

| Forecast: 20.0K | Previous: 42.2K | ||

| 00:30 | AUD | Unemployment Rate Nov | |

| Forecast: 4.40% | Previous: 4.30% | ||

| 08:30 | CHF | SNB Interest Rate Decision | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 09:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 13:30 | CAD | Trade Balance (CAD) Oct | |

| Forecast: -4.9B | Previous: -6.3B | ||

| 13:30 | USD | Initial Jobless Claims (Dec 5) | |

| Forecast: 205K | Previous: 191K | ||

| 13:30 | USD | Trade Balance (USD) Sep | |

| Forecast: -65.5B | Previous: -59.6B | ||

| 15:00 | USD | Wholele Inventories Sep F | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 15:30 | USD | Natural Gas Storage (Dec 5) | |

| Forecast: | Previous: -12B | ||

| 21:30 | NZD | Business NZ PMI Nov | |

| Forecast: | Previous: 51.4 | ||

Friday, Dec 12, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Industrial Production M/M Oct F | 1.40% | 1.40% |

| 07:00 | EUR | Germany CPI M/M Nov F | -0.20% | -0.20% |

| 07:00 | EUR | Germany CPI Y/Y Nov F | 2.60% | 2.60% |

| 07:00 | GBP | GDP M/M Oct | 0.10% | -0.10% |

| 07:00 | GBP | Industrial Production M/M Oct | 1.10% | -2.00% |

| 07:00 | GBP | Industrial Production Y/Y Oct | -2.50% | |

| 07:00 | GBP | Manufacturing Production M/M Oct | 1.20% | -1.70% |

| 07:00 | GBP | Manufacturing Production Y/Y Oct | -2.20% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | -19.1B | -18.9B |

| 13:30 | CAD | Building Permits M/M Oct | -1.20% | 4.50% |

| 13:30 | CAD | Capacity Utilization Q3 | 79.30% | 79.30% |

| 13:30 | CAD | Wholeleles M/M Oct | -0.10% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Industrial Production M/M Oct F | |

| Forecast: 1.40% | Previous: 1.40% | ||

| 07:00 | EUR | Germany CPI M/M Nov F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 07:00 | EUR | Germany CPI Y/Y Nov F | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 07:00 | GBP | GDP M/M Oct | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 07:00 | GBP | Industrial Production M/M Oct | |

| Forecast: 1.10% | Previous: -2.00% | ||

| 07:00 | GBP | Industrial Production Y/Y Oct | |

| Forecast: | Previous: -2.50% | ||

| 07:00 | GBP | Manufacturing Production M/M Oct | |

| Forecast: 1.20% | Previous: -1.70% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Oct | |

| Forecast: | Previous: -2.20% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | |

| Forecast: -19.1B | Previous: -18.9B | ||

| 13:30 | CAD | Building Permits M/M Oct | |

| Forecast: -1.20% | Previous: 4.50% | ||

| 13:30 | CAD | Capacity Utilization Q3 | |

| Forecast: 79.30% | Previous: 79.30% | ||

| 13:30 | CAD | Wholeleles M/M Oct | |

| Forecast: -0.10% | Previous: 0.60% | ||

Markets Weekly Outlook – FOMC Rate Cut Countdown, Economic Projections May Hold the Key

Week in Review: Markets Buoyed Ahead of FOMC Meeting

The week draws to a close with risk assets largely buoyed by the prospect of an interest rate cut from the Federal Reserve.

On Friday, the main US stock market indexes all moved slightly higher. The Dow Jones gained 236.46 points (a 0.49% rise), the S&P 500 increased by 31.44 points (a 0.46% gain), and the Nasdaq rose by 131.27 points (a 0.56% increase).

Looking ahead to next week, Federal Reserve officials are scheduled to have a significant debate: should they lower interest rates, or keep them steady? The core issue is that while prices remain difficult to control (stubborn inflation) and the job market is still surprisingly strong (resilient), some Fed members are hesitant to cut rates.

Other employment-related data still does not suggest a quick slowdown in hiring, which gives those who prioritize fighting inflation (the "hawks") a stronger argument. Despite this internal debate, investors in the market still anticipate that the Fed will go ahead and cut rates by another quarter-point sometime by June 2026.

Source: CME FedWatch Tool

Heading into the decision, Wall Street indexes are all near all-time highs with the hope that the Federal Reserve meeting will serve as a catalyst for fresh all-time highs to be printed. Will such a move materialize?

How Did the US Dollar and FX Perform?

The US dollar was slightly weaker on Friday but generally stayed within its recent trading range against other major currencies.

The dollar's strength index (DXY) dipped 0.2%, landing at 98.906, which is close to its weakest point in the past five weeks.

Meanwhile, the euro gained slightly, reaching 1.1651 against the dollar.

The Japanese yen remained mostly unchanged on Friday at 155.15 per dollar, taking a pause after recent days of strength driven by speculation that the Bank of Japan (BOJ) might raise its interest rates later this month. Reports from both Bloomberg and Reuters suggested that BOJ officials are indeed prepared to raise rates on December 19th unless there is a significant unexpected economic event.

The Canadian dollar strengthened by the most in six months against its US counterpart on Friday and bond yields jumped, as stronger-than-expected domestic jobs data boosted bets the Bank of Canada would begin raising interest rates next year.

Finally, the British pound (Sterling) also rose 0.2%, trading at 1.335 and nearing its highest level in six weeks.

The Week Ahead - Fed in Focus, RBA & BoC Rate Decisions Ahead

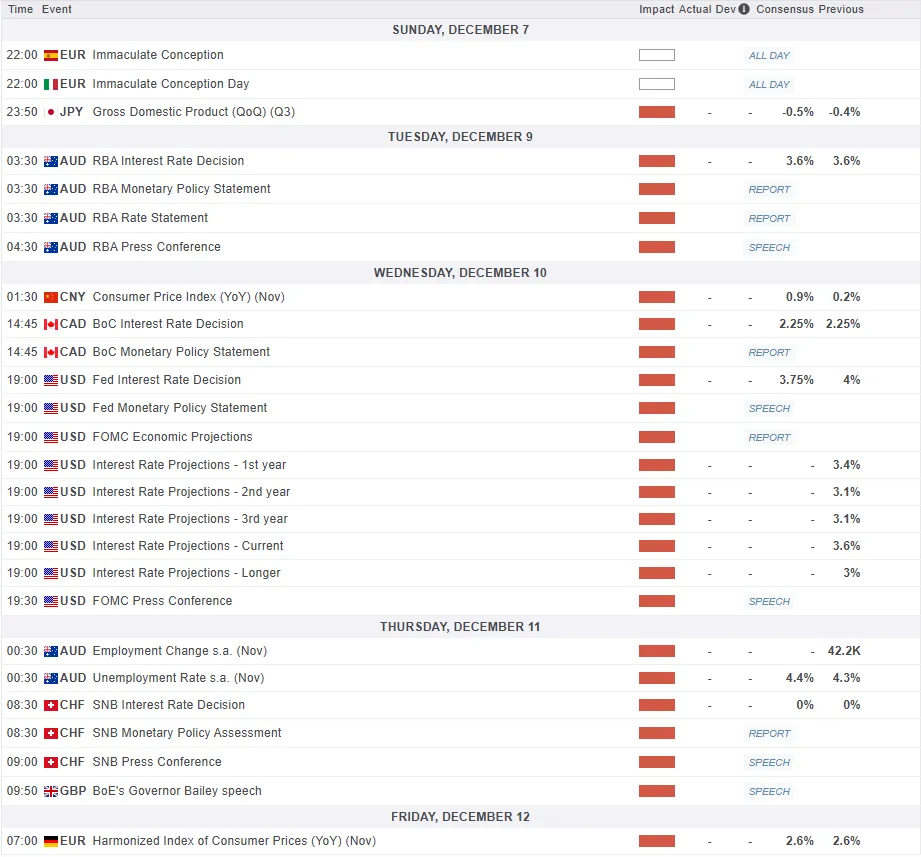

The week ahead will see market focus on the Federal Reserve rate decision. There is also rate decisions from Canada and Australia but given the stature of the US economy and its ability to affect overall market sentiment, the RBA and BoC decisions will likely be overshadowed.

Asia Pacific Markets

The Reserve Bank of Australia (RBA) is expected to keep its main interest rate unchanged at 3.6% next Tuesday. Since recent reports showed that both inflation and economic growth were stronger than expected, it's now much less likely that the RBA will cut interest rates again. This suggests that the central bank might be finished with its current cycle of lowering rates.

China's trade activity is expected to grow only moderately. Although the recent trade agreement and reduced tariffs from the U.S. should help Chinese exports, the way the numbers are calculated (base effects) will keep the growth rate low. For November, I forecast exports to grow by 3.3% and imports by 3.4%, resulting in a trade surplus of about $100.3 billion.

Separately, China’s inflation rate is predicted to continue its recovery, rising to 0.5% for the year, which is a positive sign after it recently moved back above zero. This is largely because the falling price of food is no longer dragging down the overall inflation number, and the prices of non-food items are starting to rise. While inflation remains quite low, it is important to prevent a sustained period of falling prices (deflation) to keep long-term spending and investment healthy. Since inflation is still low, it will likely not be a major factor in the People's Bank of China's interest rate decisions.

FOMC to Steal the Show

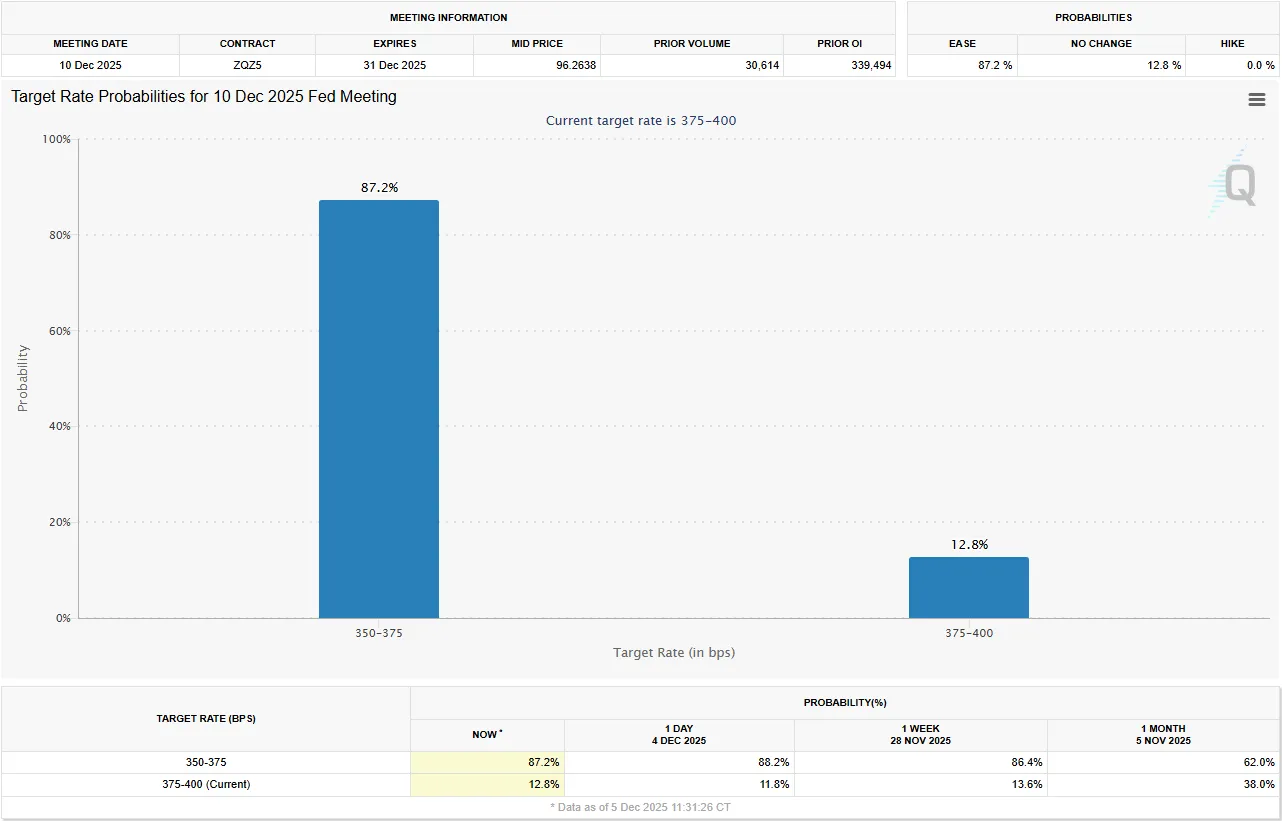

The Federal Reserve (US) is expected to cut its interest rate by $0.25\%$ this Wednesday. While some worry that new tariffs could keep prices high (inflation), the main reason for the cut is the growing concern about the weakness in the job market, which important Fed members have recently noted. Along with the decision, the Fed will release new predictions, which are likely to suggest only one more rate cut in 2026.

However, this long-term outlook might not significantly affect the market's expectations which currently price in two or three cuts for 2026 because the composition of the Fed's voting committee and leadership (including the Chair, Jerome Powell) could change drastically under the new administration.

Separately, Canada is likely to take a break from its recent series of interest rate cuts this Wednesday. Stronger-than-expected recent growth and employment figures support this pause, though we still anticipate one final cut early in 2026 due to ongoing trade risks with the US.

Finally, for the UK, I expect to see an improvement in the monthly Gross Domestic Product (GDP) data on Friday. The previous drop in September was mainly because a cyberattack stopped production at a major car company, but since that production has restarted, October's GDP numbers should bounce back.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. GMT time (click to enlarge)

Chart of the Week - US Dollar Index

This week's Chart of the week is the US Dollar Index (DXY)

From a technical perspective, the DXY has had a change in structure having taken out the November 14 swing low around the 99.00 handle.

Thursdays daily candle closed as a hammer offering bulls some hope. However, as has been the case of late any attempt at a bullish move has been met by swift selling pressure.

The period-14 RSI remains below the 50 mark which is a sign of bearish momentum.

Immediate support is provided by the 100-day MA which rests at the 98.58 before the 98.00 and 97.70 handles come into focus.

Upside resistance may be found at the 200-day MA around 99.51 before the 100.00 psychological level and the 100.61 level come into focus.

The Dollar Index trajectory may depend on the economic projections for 2026. Any sign that the Fed see more than one rate cut in 2026 could send the DXY sliding with a test of the YTD low a possibility depending on how dovish the Fed outlook is.

Alternatively, a hawkish stance could have the opposite impact. This would be similar to what we witnessed after the previous Fed meeting in October.

US Dollar Index (DXY) Daily Chart - October 17, 2025

Source:TradingView.Com (click to enlarge)

Be Nimble and Trade Safe.

The Weekly Bottom Line: Fed to Play Santa, Cut Policy Rate

Canadian Highlights

- Canada’s job market defied expectations again in November, pushing the unemployment rate down to a 16-month low.

- The labour market is demonstrating some resiliency, but slack still exists, and the short-term trajectory is marked by significant uncertainty.

- The Bank of Canada will make their final rate announcement of the year next week. We expect the Bank to hold rates steady at 2.25%.

U.S. Highlights

- Real consumer spending was flat in September, ending the third quarter on a soft note. Consumption for the third quarter was up 2.7% (q/q annualized).

- The Fed’s preferred inflation gauge – the core PCE deflator – rose by 0.2% month-on-month in September, as expected. That is still above the Fed’s target at 2.8% year-on-year, but down slightly from 2.9% in August.

- Combined with somewhat soft employment data in November’s ADP report, the Fed looks set to check off markets’ wish list for a rate cut next week.

Canada – Jobs Bringing on the Winter Heat

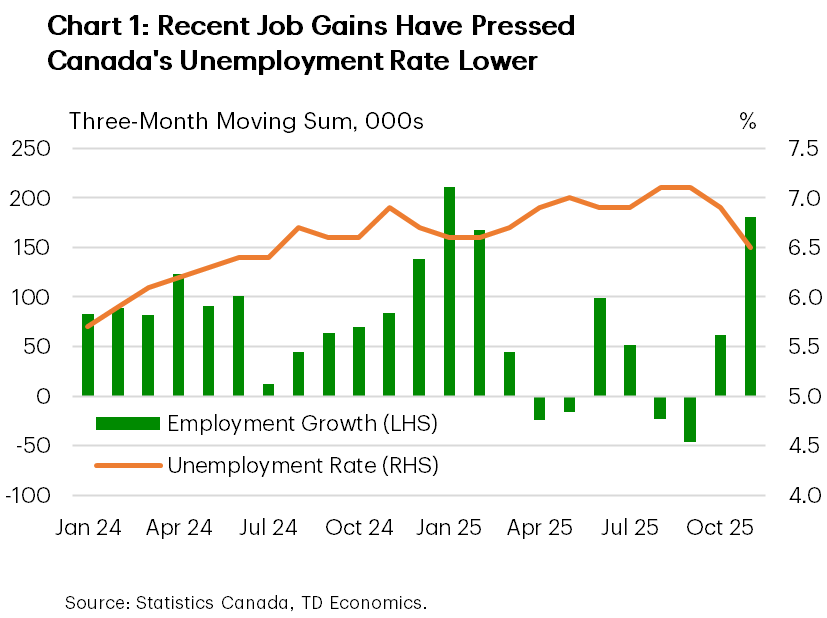

An update to Canada’s labour market was the sole event in an otherwise quiet start to December. And unlike the recent weather, the data brought some heat. Forecasters were caught flat-footed as Canada’s economy generated 54k jobs, against expectations for modest employment losses. Alongside a contraction in labour force growth, the national unemployment rate legged down to 6.5%, putting it back in line with mid-2024 levels. Other details were more mixed but upbeat on the margin. Part-time jobs drove the entirety of the gain, while job growth was concentrated in the private sector. To add, wage growth and hours worked both ticked higher on the month. In the wake of the news, the Loonie gained to 72 cents/USD, while yields are up a few basis points (bps), continuing their march higher on the week.

So, what do we make of all this, especially given the Labour Force Survey (LFS) has been particularly noisy in recent months? On one hand, Canada’s labour market is certainly displaying some resiliency. Job creation since tariffs took effect in March has averaged around 16k, roughly in line with historical average steady-state employment gains. That’s a great outcome considering the economy is facing one of the largest external trade shocks on record. What’s more, the Canadian economy gained a staggering 180k jobs over the last three months, which has helped put the unemployment rate on a downward trend (Chart 1).

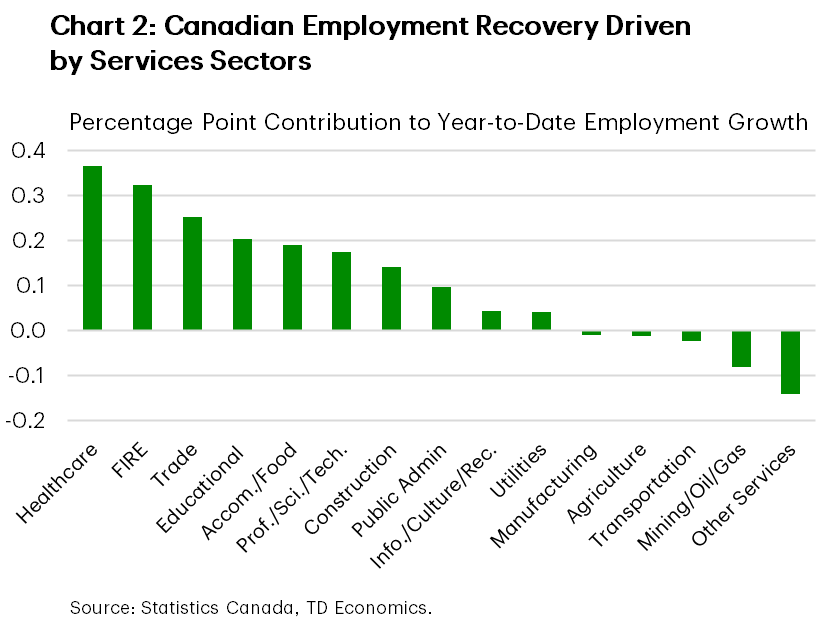

On the other hand, we are cautious to declare this a victory. Job conditions are showing signs of improvement, but the jobless rate is still elevated, and Canada’s payroll survey (SEPH) is painting a much weaker picture of labour conditions, albeit in data only up to September. The composition of employment gains this year has also been skewed, with almost 90% of job creation coming from the services sector (Chart 2). This result is unsurprising as the goods side of the economy is facing more of a disproportional hit from trade-related headwinds, but it still creates a wedge in the employment recovery narrative.

The Bank of Canada’s (BoC) will hold its final policy decision of the year next week. Prior to November’s employment report, it was already expected that interest rates would stay unchanged, and today’s update confirms this view. More important is how Governing Council guides the outlook. They are likely to recognize progress in employment while highlighting ongoing slack in the labour market and considerable uncertainty, especially as Canada and the U.S. enter complex USMCA renegotiation talks. We also expect the BoC will reaffirm that inflation will continue moderating. All told, we expect the Bank to maintain its current stance through 2026 and continue to look for signs that a sustained economic recovery is in the works.

We will finally get an update on how Canada’s exports are faring in the face of U.S. tariffs, as Statistics Canada will publish September’s international trade data on December 11th. Trade data was delayed due to the U.S. government shutdown, with October and November’s data to be released in January.

U.S. – Fed to Play Santa, Cut Policy Rate

Markets are convinced that the Fed will deliver an early holiday gift – a rate cut – next week. Odds of a December cut have hung near 90% ever since shifting up in late November, following support for more easing from Fed Presidents Williams (NY) and Daly (San Fran.). Economic data out this week, while mixed, did not perturb that balance. Equities managed to trek modestly higher, with S&P 500 up 1.1% from last week’s close.

September’s personal income and spending report provided a snapshot of spending and inflation trends before the government shutdown. Spending was flat in real terms in September, ending the third quarter on a soft note. Consumption for the quarter was up 2.7% (q/q annualized) – below expectations but still an improvement from 2.5% in the second quarter. September provides a soft handoff to the fourth quarter, which coupled with the government shutdown, slowing job growth, and weak consumer confidence, suggests spending will slow further at the end of the year. Early data from Thanksgiving weekend suggests holiday shopping was healthy but likely grew at a pace slightly below that of last year. Online sales continued to lead the way, with Cyber Week spending up nearly 8% year-over-year (y/y) according to Adobe. In-store gains were softer, with closely watched indicators pointing to growth in the low single-digits. AI tools helped boost retail site traffic, while a growing Buy-Now-Pay-Later (BNPL) trend also played an important role in propping up spending.

Core PCE inflation rose 0.2% month-over-month (m/m) in September, and 2.8% in y/y terms – a modest easing from 2.9% in the prior two months. The ISM services price index recorded a notable pullback in November – marking a modest positive post-shutdown signal with respect to inflationary pressures. Nonetheless, Cleveland Fed Inflation Nowcasting puts core PCE at 0.23% (m/m) for both October and November, 2.8% and 2.9% in y/y terms respectively – still well above target.

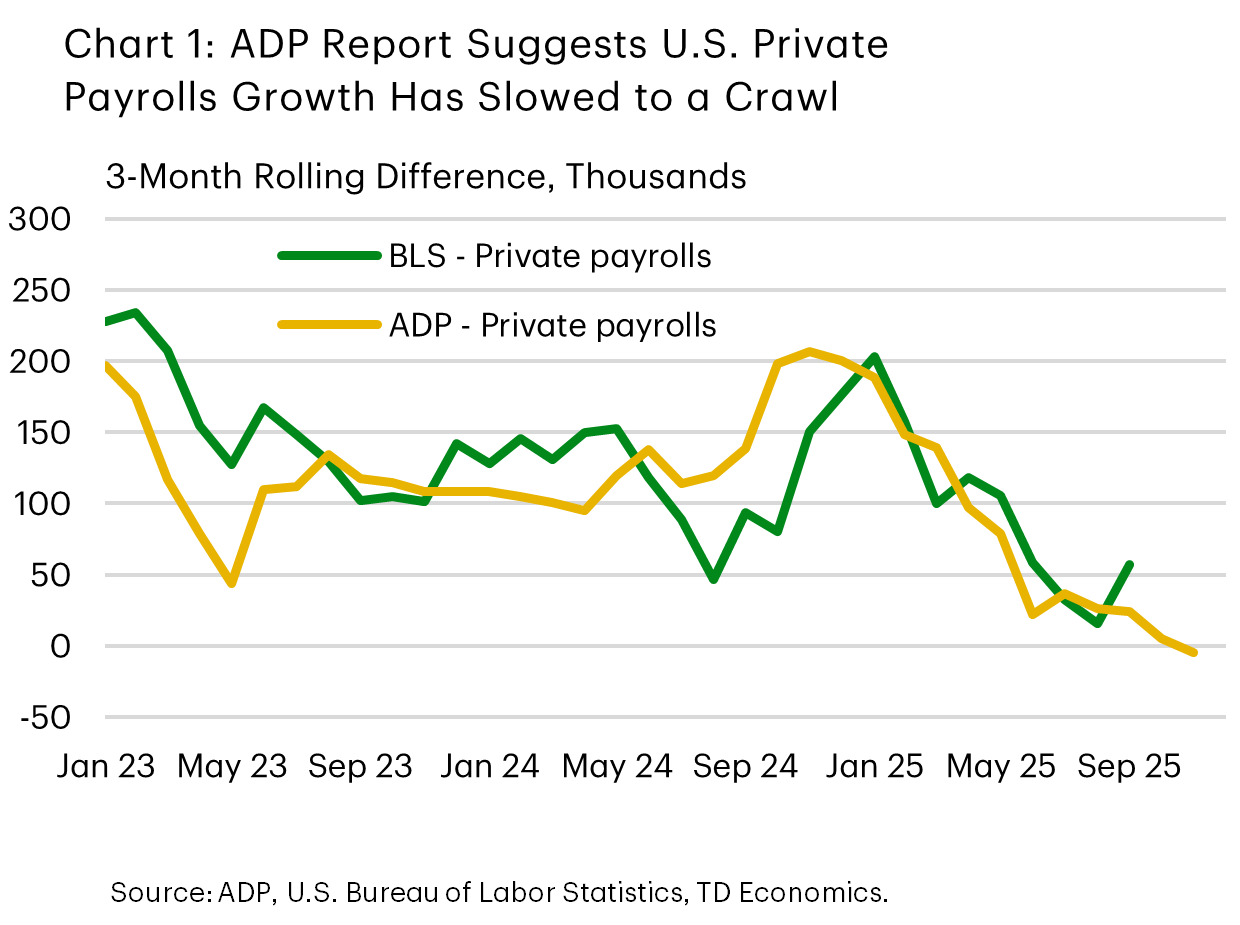

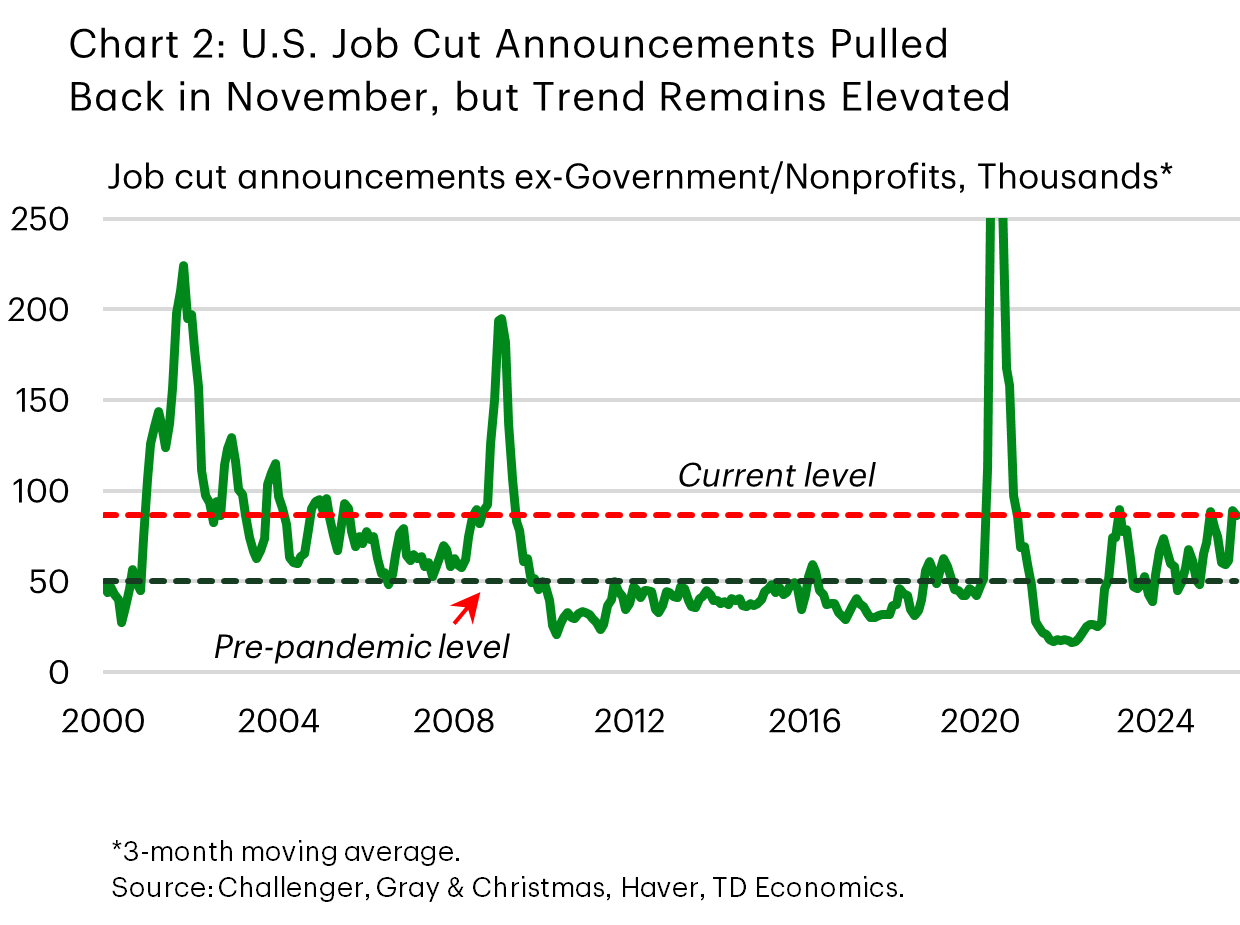

Employment data was mixed. Initial jobless claims dropped to a three-year low of 191k at November’s end. The Thanksgiving holiday may have distorted the data. But even prior to that last week, initial claims were still trending lower. Conversely, the ADP report showed private payrolls fell by 32k in November. Its three-month average, which is more closely aligned with the BLS equivalent, turned slightly negative too (Chart 1). Job cut announcements, meanwhile, also pointed to continued challenges. Layoff announcements in November were cut in half from their October tally, coming in at 71k. But even when looking past the weakness in the government sector, the trend in layoff announcements remains elevated (Chart 2). Overall, markets seemingly expect the Fed to focus on signs of labor market softness and maintain a cautious policy stance.

Our reading is that the Fed won’t disappoint market expectations next week. But in the New Year, the bar for additional cuts may be higher. Having delivered some insurance cuts, the Fed will likely take time to digest delayed economic reports and carefully assess post-shutdown data to form a clearer picture of the economy’s health.

Weekly Economic & Financial Commentary: A Split Committee and Steady Dots

Summary

United States: Consumers Still Carry the Torch, but the Glow Is Fading

- As Powell heads into one of his four remaining meetings as Fed Chair, strength in services and lingering consumer resilience contrast with manufacturing weakness, reinforcing expectations for a December rate cut.

- Next week: JOLTS (Tue.), ECI (Wed.), FOMC Meeting (Wed.)

International: Global Crosswinds: Sticky Prices and Softer Signals

- Eurozone inflation rose more than expected in November, reinforcing the case for the European Central Bank to keep rates on hold. Australia’s Q3 GDP came in below consensus with underlying details showing modest resilience. And in emerging markets, the Reserve Bank of India cut its policy rate and signaled a dovish bias while maintaining a neutral stance.

- Next week: Japan Labor Cash Earnings (Mon.), Bank of Canada Policy Rate (Wed.)

Topic of the Week: A Split Committee and Steady Dots

- The FOMC heads into its December meeting with a rare degree of internal division. Regional presidents—particularly those with a vote—have signaled greater skepticism toward further easing, setting the stage for opposition in both directions of the policy decision, though the more dovish governors are likely to provide the critical mass of support needed for another 25 bps rate cut.