Sample Category Title

CHFJPY Posts Perfect Rally from Elliott Wave Blue Box Area

In this technical blog, we analyze the historical performance of the CHFJPY 1-hour Elliott Wave charts, as presented to members of ElliottWave-Forecast. The analysis highlights an impulsive rally that began from the October 15 low and concluded at the October 27 high, which surpassed the prior peak from October 8—signaling a potential bullish extension. Based on this development, we recommended that members avoid short positions on the yen cross and instead consider buying the dips in 3, 7, or 11 swing sequences within the designated blue box areas. The following sections will detail the wave structure and provide our updated forecast.

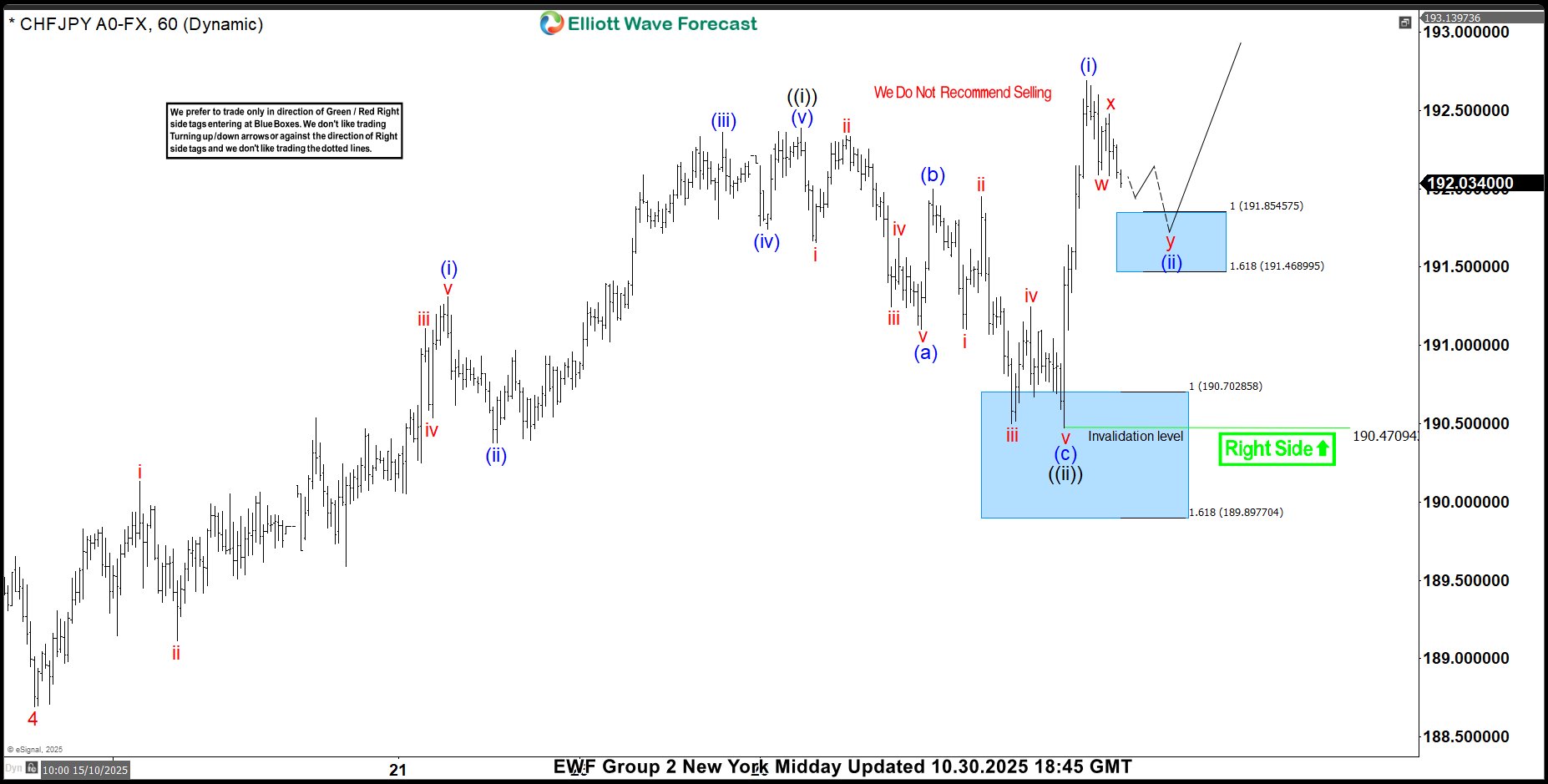

CHFJPY 1 Hour Elliott Wave Analysis [October 30 Asia Update]

Impulsive Rally from October 15 to October 27

The chart highlights a strong impulsive rally that began at the October 15 low and peaked on October 27. This upward move unfolded in a classic five-wave impulse, confirming bullish momentum. Notably, the October 27 high exceeded the previous October 8 peak, suggesting an extension to the upside.

Zigzag Correction in Progress

Following the rally, CHFJPY entered a corrective phase, forming a Zigzag Elliott Wave structure — a 5-3-5 pattern where waves (a) and (c) both consist of five sub-waves. In this case:

- Wave (a) developed as a standard impulse.

- Wave (c) shows overlapping characteristics, indicating it is likely unfolding as a diagonal.

Price has already reached the 100% Fibonacci extension of wave (a) measured from wave (b). However, the decline from the wave (b) high currently shows only three waves. This implies that a marginal new low may be needed to complete five swings within wave (c), thereby finalizing the three-wave pullback from the October 27 peak.

Blue Box Support Zone and Forecast

We expect buyers to emerge within the blue box support area between 190.70 and 189.89. As long as price holds above the 161.8% Fibonacci extension level at 189.89, the bullish outlook remains intact. From this zone, we anticipate either:

- A continuation of the rally toward a new high above the October 27 peak, or

- A minimum three-wave reaction higher.

CHFJPY 1 Hour Elliott Wave Analysis [October 30 Midday New York Update]

Following our previous analysis, the chart confirms that buyers did indeed step in at the blue box support zone between 190.70 and 189.89, triggering a strong rally that swiftly broke above the October 27 peak. The nature of this advance appears impulsive, reinforcing the bullish outlook.

Pullback Structure and Support Expectations

Given the impulsive character of the rally, we expect any pullbacks to remain corrective — ideally unfolding in 3, 7, or 11 swings — and supported for further upside extension. Traders who entered long positions from the initial blue box zone should now be in a risk-free position.

Next Area of Interest: 191.85 – 191.46

Looking ahead, the 191.85 – 191.46 zone marks the next potential support area, where we anticipate another blue box to form. This region is likely to attract fresh buying interest and could serve as the launchpad for the next leg higher. However, it’s important to note that a break below the October 30 low at 190.47 would invalidate this bullish scenario and suggest a deeper correction may be underway.

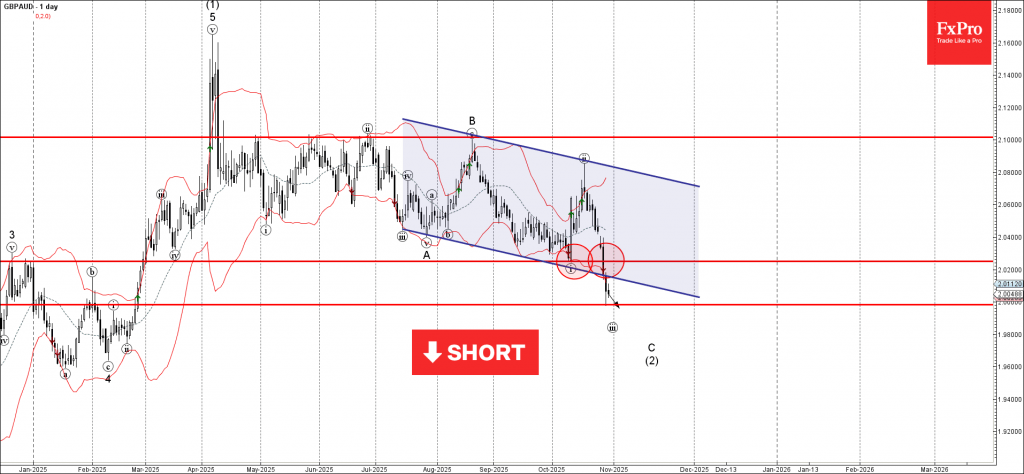

GBPAUD Wave Analysis

GBPAUD: ⬇️ Sell

- GBPAUD broke support zone

- Likely to fall to support level 2.0000

GBPAUD currency pair recently broke the support zone between the support level 2.0250 (which stopped the previous impulse wave i) and the support trendline of the daily down channel from July.

The breakout of this support zone accelerated the active impulse wave C of the intermediate ABC correction (2) from the start of April.

Given the clear downtrend, GBPAUD currency pair can be expected to fall toward the next round support level 2.0000.

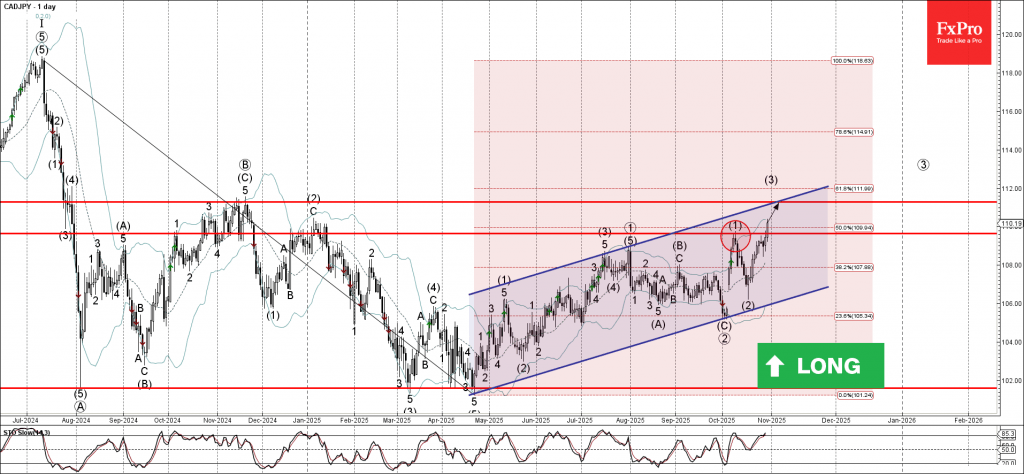

CADJPY Wave Analysis

CADJPY: ⬆️ Buy

- CADJPY broke resistance zone

- Likely to rise to resistance level 111.30

CADJPY currency pair recently broke the resistance zone between the resistance level 109.60 (which stopped wave (1) at the start of October) and the 50% Fibonacci correction of the downtrend from July of 2024.

The breakout of this resistance zone accelerated the active intermediate impulse sequence (3) from the middle of October.

Given the clear daily uptrend, CADJPY currency pair can be expected to rise further to the next resistance level 111.30 (former multi-month high from November).

Sunset Market Commentary

Markets

Some last-minute economic data including stronger-than-expected Q3 GDP and national inflation numbers (see below) ahead of the ECB policy meeting highlighted the logic of the outcome. The deposit rate was kept unchanged at 2% today. That unanimously decided status quo was based on the fact that inflation, including underlying gauges, remains close to the 2% medium-term target and developed in line with the September outlook. There was no risk balance offered. But based on the opposing arguments, including a return of supply chain bottlenecks (hello, 2020), spelled out, we assume the risks are considered being balanced. A robust labour market and earlier monetary easing amongst others keeps the economy growing against the backdrop of a challenging global environment. The ECB chair, citing today’s GDP release, added she wouldn’t worry too much about growth at this point in time. Some of the downside risks mitigated, she said, following the trade deal sealed with the US, the ceasefire in the middle east and the progress in China-US relations announced this morning. That assessment comes after Lagarde in September said risks to the economy “become more balanced”. ECB Lagarde singled out (digital) services a key engine for growth. Manufacturing was instead held back by higher tariffs and a stronger euro, denting external demand. The ECB expects this divergence with solid internal demand to persist. As usual, Lagarde kept the cards close to her chest in terms of what to expect from policy going forward. The ECB remains in a good place but it’s not a fixed good place. Decisions will be made on meeting-by-meeting basis and take into account incoming economic and financial data. Given that neither the risks to nor the outlook of inflation had changed and with the ECB becoming less negative on growth risks, a 2% deposit rate for the months ahead remains our base scenario. If anything, the bar for rate cuts after today shifted higher. The money market implied probability barely changed and remains well below 50%. European swap yields retain most of the earlier rise with net daily changes varying between +1 bp and +2 bps. Treasury yields stabilize after the Fed-driven 10 bps jump yesterday. The euro loses some ground against the dollar in a move more inspired by the risk-off mood than anything else. EUR/USD eases to below 1.16 but in technically irrelevant trading. A disappointing JPY in the wake of the Bank of Japan’s unchanged rates decision this morning underperforms global peers. USD/JPY surges to a 9-month high north of 154. Stock markets slip to around 1% in the US (Nasdaq) with investors taking some chips off the table after the 5-day 5% rally.

News & Views

Belgian inflation rose by 0.36% M/M in October after two monthly declines in August and September. The most significant price increases in October were registered for holiday villages, clothing, private rents, participation in recreational sporting services, plane tickets, restaurants and cafés and personal care. Hotel rooms, natural gas, electricity and package holidays had a downward effect. Annual inflation slowed from 2.1% Y/Y to 2% and is actually hovering sideways between 1.9% and 2.1% since May. Core inflation was unchanged at 2.6% Y/Y. Services inflation increased from 3.5% to 3.6% while rent inflation was unchanged at 4%. Food inflation slowed from 3.3% to 2.7% and energy dropped by 1.9% Y/Y from -1.5% Y/Y in September. Other European countries reporting inflation data today were Spain and Germany. Spanish inflation showed an unexpected acceleration in harmonized CPI from 0.2% M/M to 0.5% M/M (3.2% Y/Y from 3%; core 2.5% from 2.4%). German inflation also rose more than expected (0.3% M/M & 2.3% Y/Y) suggesting upside risks to tomorrow’s EMU print. Consensus expects 0.2% M/M and 2.1% Y/Y.

Czech GDP grew by 0.7% Q/Q in Q3 according to the preliminary estimate with year-on-year growth of 2.7% being mainly driven by final consumption expenditure of households and gross capital formation. External demand also helped quarterly growth. Both significantly beat consensus (0.3% Q/Q & 2.3% Y/Y). Full details will only be released by the end of the month (Nov 28). The Hungarian statistical office also published a first indication for Q3 growth. It disappointed with no-growth on a quarterly basis and GDP rising by 0.6% Y/Y.

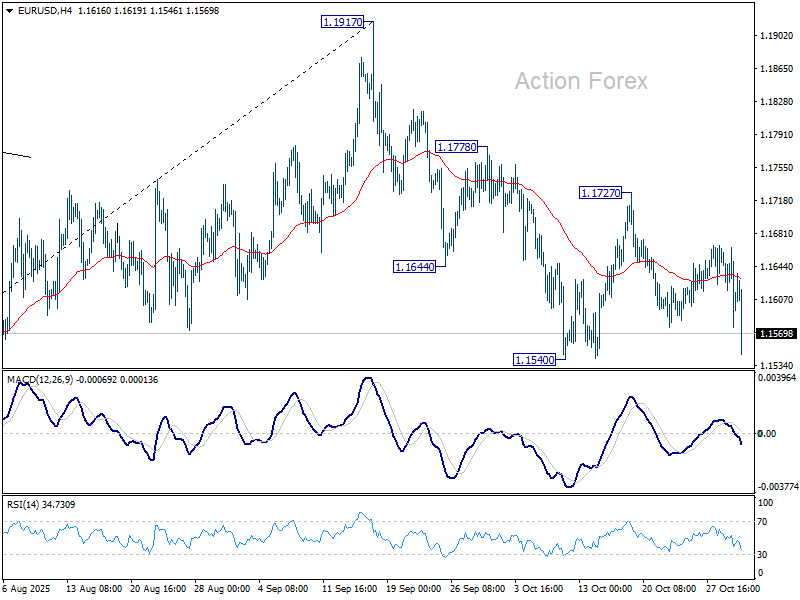

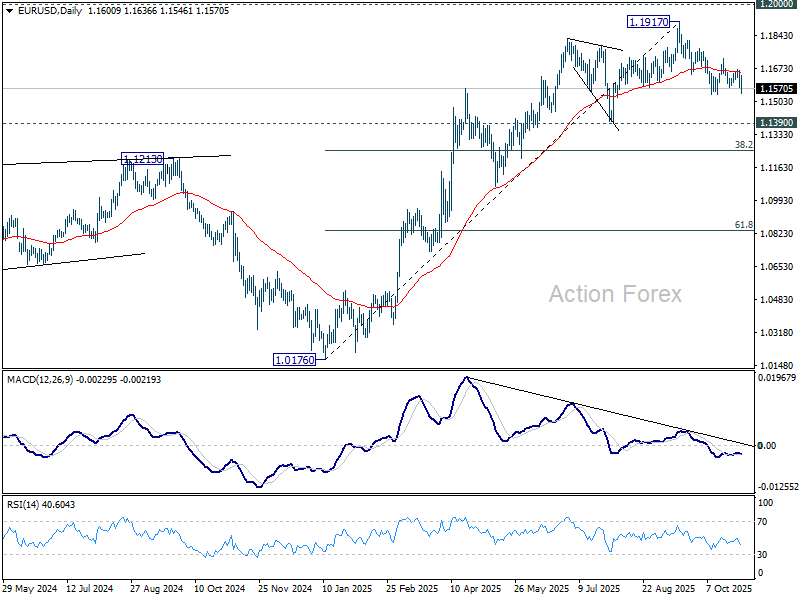

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1564; (P) 1.1615; (R1) 1.1652; More…

Focus is now on 1.1540 support as EUR/USD's decline continues today. Firm break there will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

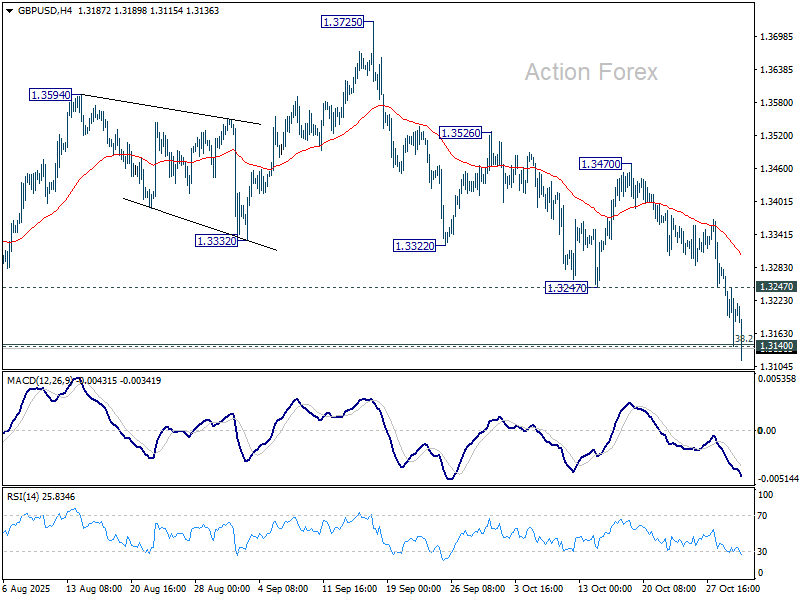

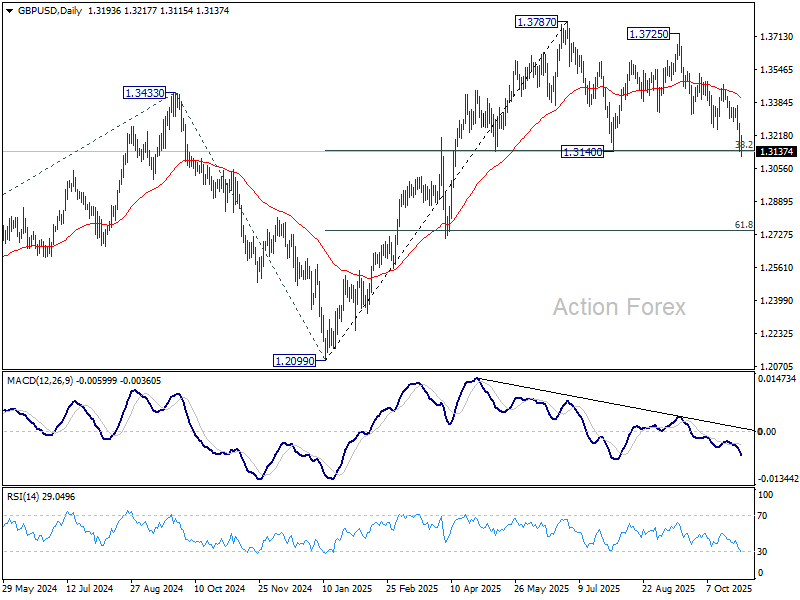

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3130; (P) 1.3206; (R1) 1.3270; More...

Focus stays on 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Decisive break there will complete a double top pattern (1.3787/3725) and turn near term outlook bearish. Deeper decline should then be seen to 61.8% retracement at 1.2744 next. On the upside, above 1.3247 support turned resistance will turn intraday bias neutral first.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

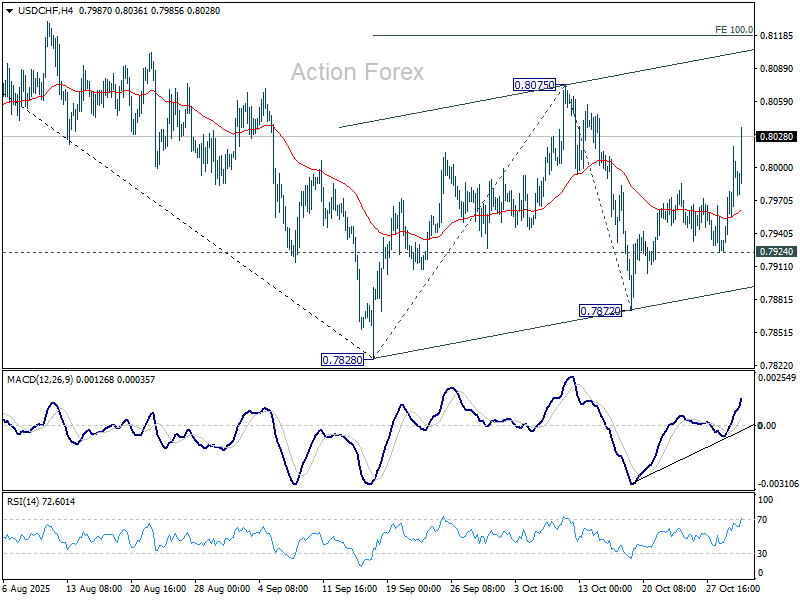

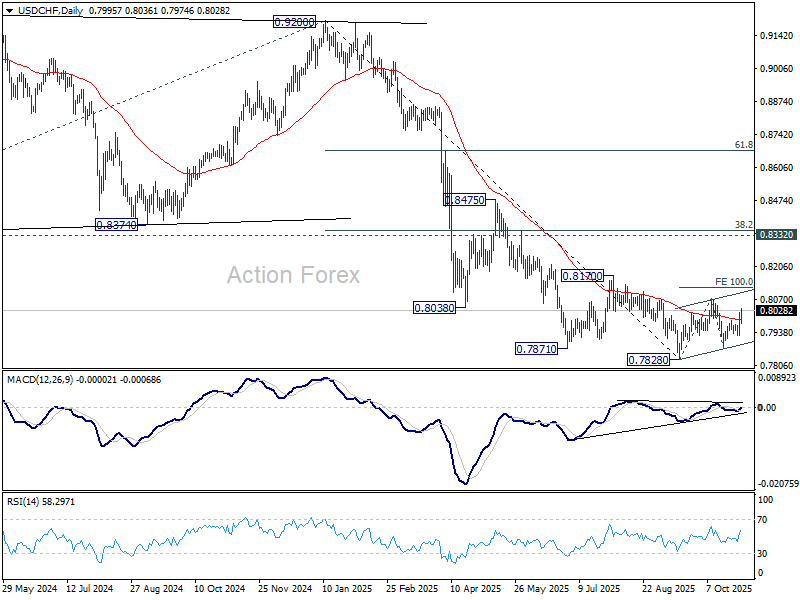

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7943; (P) 0.7981; (R1) 0.8037; More…

Intraday bias in USD/CHF remains on the upside at this point. Current development suggest that corrective pattern from 0.7878 is extending with another rising leg. Further rise should be seen to 0.8075 resistance. Firm break there will target 100% projection of 0.7828 to 0.8075 from 0.7872 at 0.8119. For now, risk will be mildly on the upside as long as 0.7924 support holds, in case of retreat.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

ECB holds at 2.00%, not pre-committing to any rate path

The ECB kept its deposit rate unchanged at 2.00%, in line with expectations, and signaled no change in its cautious, data-dependent approach. Policymakers reaffirmed that inflation remains close to the 2% medium-term target, with the Governing Council’s assessment of the outlook “broadly unchanged.”

In its statement, the ECB noted that the Eurozone economy continues to grow despite a difficult global backdrop. It cited the robust labor market, solid private sector balance sheets, and the supportive effects of past rate cuts as key "sources of resilience". However, the Bank acknowledged that the outlook remains uncertain, highlighting persistent global trade disputes and geopolitical risks as ongoing headwinds.

The Governing Council reiterated that future policy decisions will be made on a meeting-by-meeting basis and guided strictly by incoming data. ECB emphasized that it is "not pre-committing to a particular rate path."

(ECB) Monetary policy decisions

30 October 2025

The Governing Council today decided to keep the three key ECB interest rates unchanged. Inflation remains close to the 2% medium-term target and the Governing Council’s assessment of the inflation outlook is broadly unchanged. The economy has continued to grow despite the challenging global environment. The robust labour market, solid private sector balance sheets and the Governing Council’s past interest rate cuts remain important sources of resilience. However, the outlook is still uncertain, owing particularly to ongoing global trade disputes and geopolitical tensions.

The Governing Council is determined to ensure that inflation stabilises at its 2% target in the medium term. It will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance. In particular, the Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook and the risks surrounding it, in light of the incoming economic and financial data, as well as the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Key ECB interest rates

The interest rates on the deposit facility, the main refinancing operations and the marginal lending facility will remain unchanged at 2.00%, 2.15% and 2.40% respectively.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP and PEPP portfolios are declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises at its 2% target in the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.