Sample Category Title

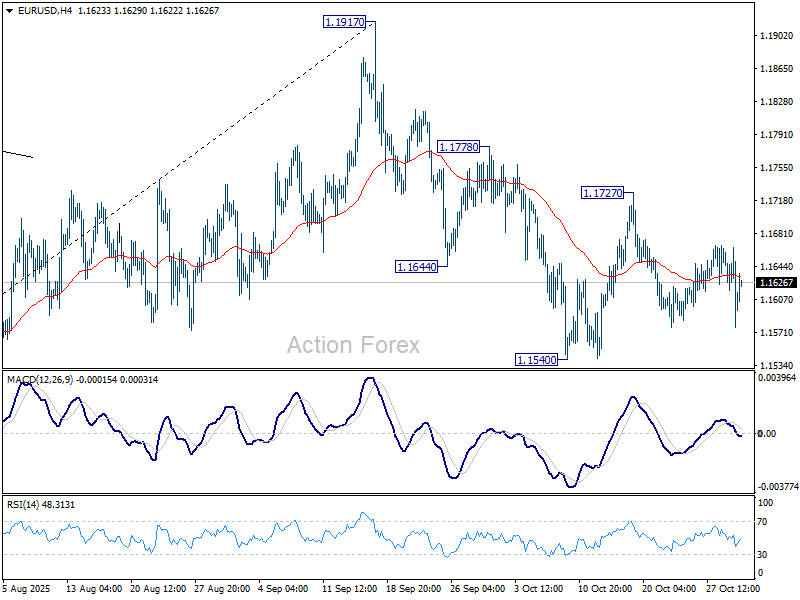

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1564; (P) 1.1615; (R1) 1.1652; More…

Intraday bias in EUR/USD remains neutral as sideway trading continues. On the downside, below 1.1540 will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

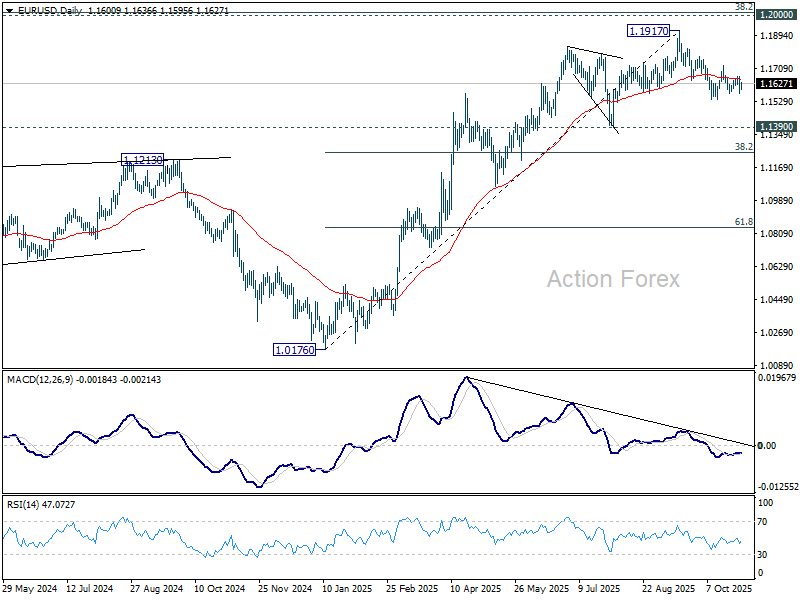

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

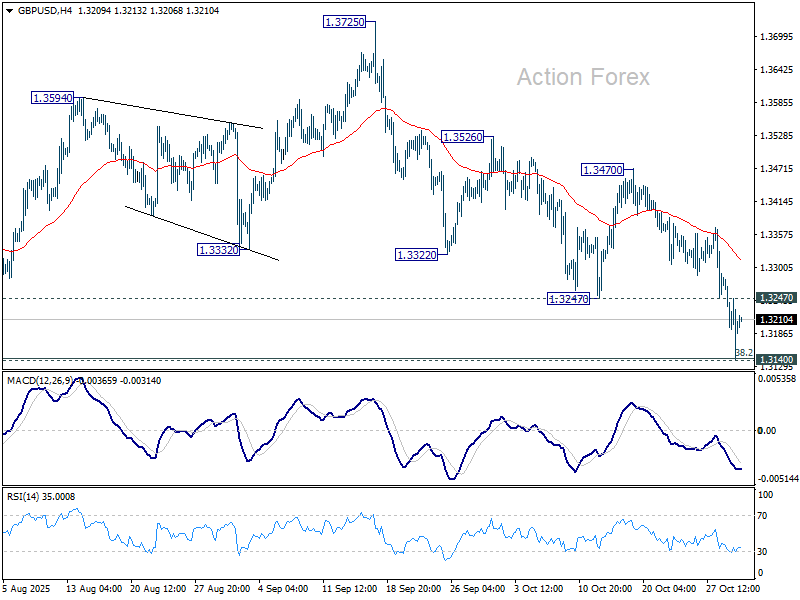

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3130; (P) 1.3206; (R1) 1.3270; More...

Immediate focus is now on 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142) as GBP/USD's fall extended. Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, above 1.3247 support turned resistance will turn intraday bias neutral first. However, decisive break of 1.3140/2 will complete a double top pattern (1.3787/3725) and turn near term outlook bearish.

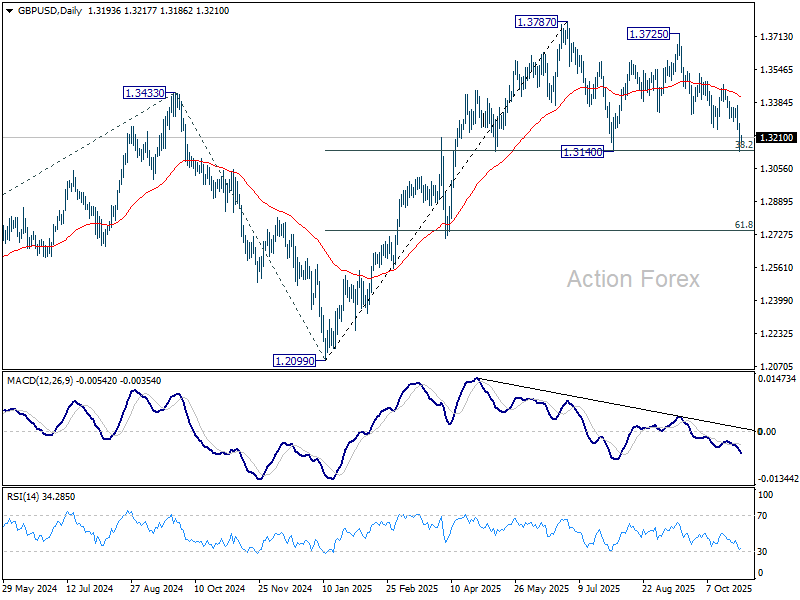

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

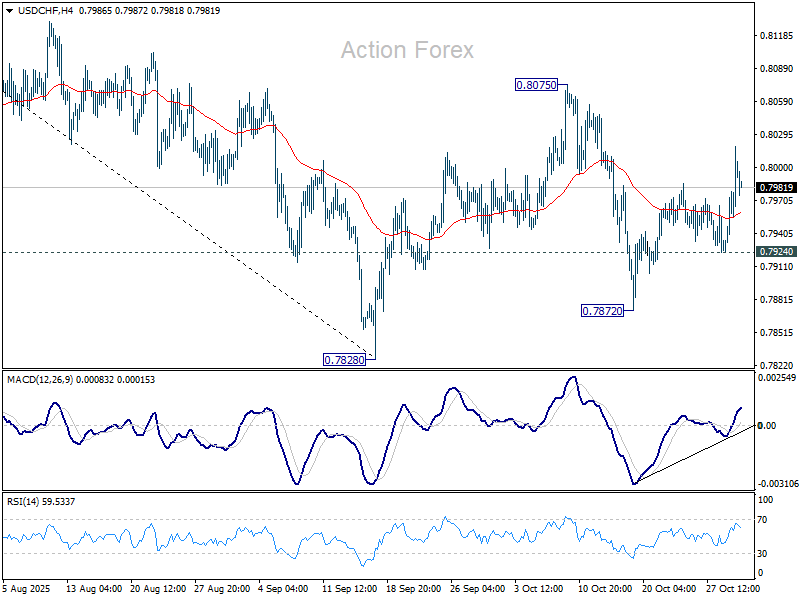

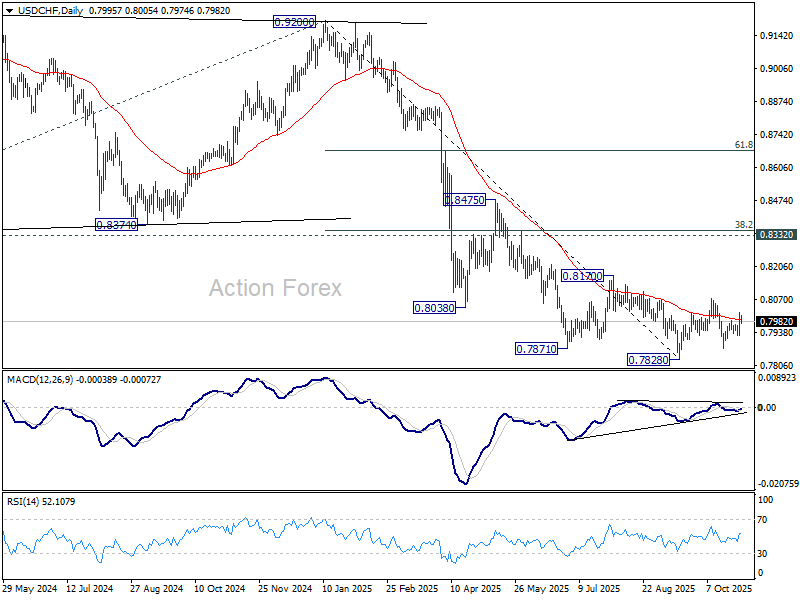

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7943; (P) 0.7981; (R1) 0.8037; More…

USD/CHF's rebound from 0.7872 resumed higher and the development suggests that corrective pattern from 0.7878 is extending with another rising leg. Intraday bias is back on the upside for 0.8075 resistance first. For now, risk will be mildly on the upside as long as 0.7924 support holds, in case of retreat.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

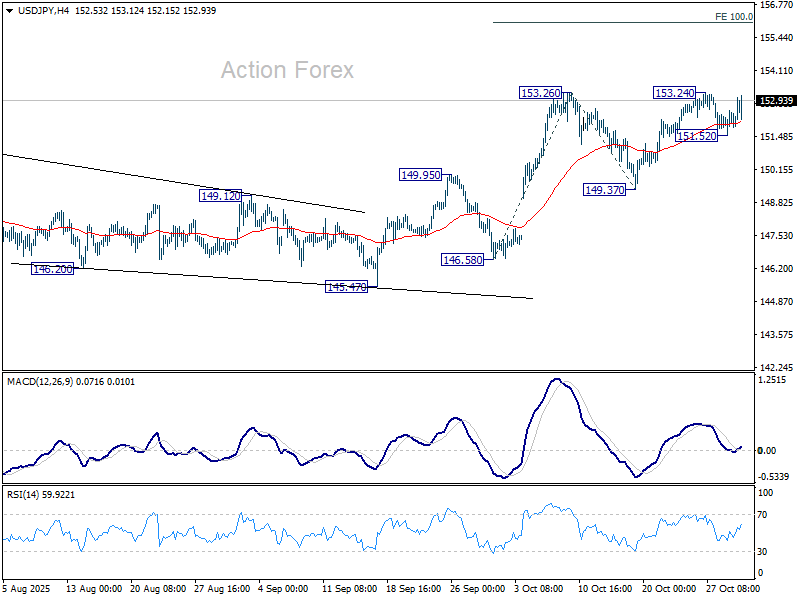

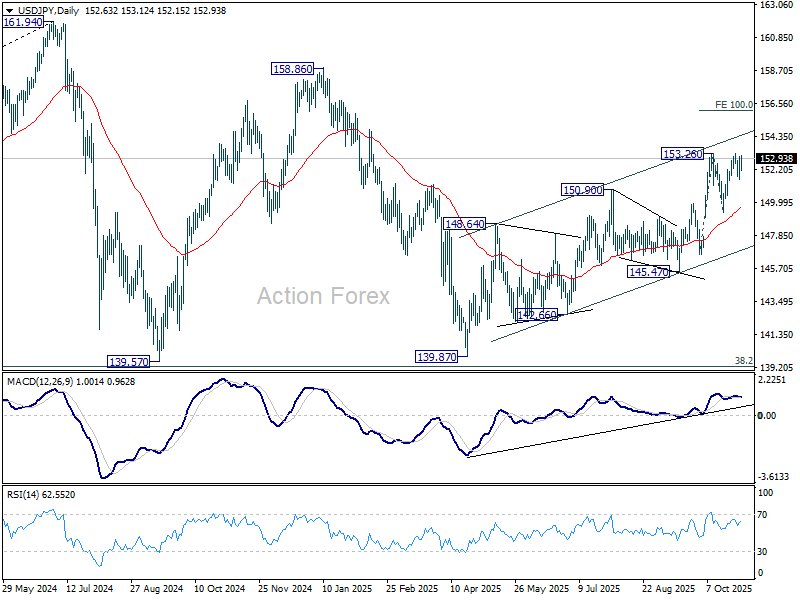

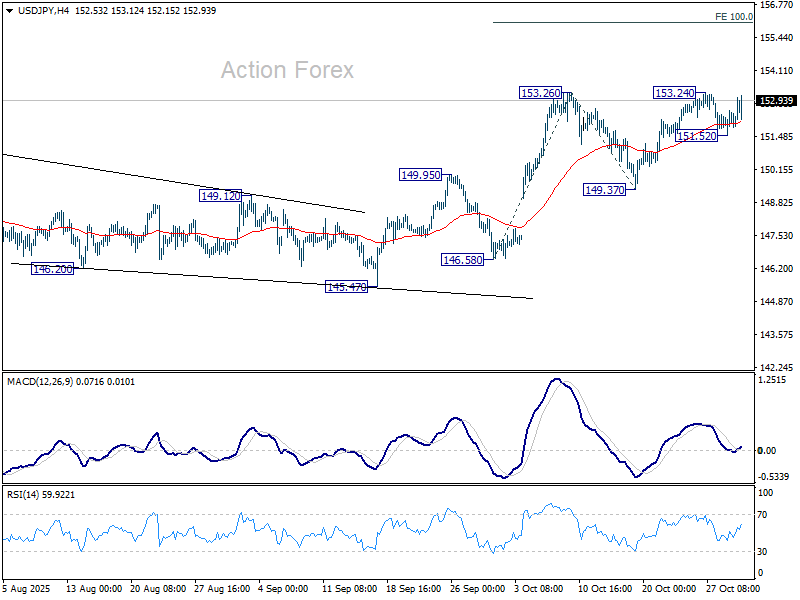

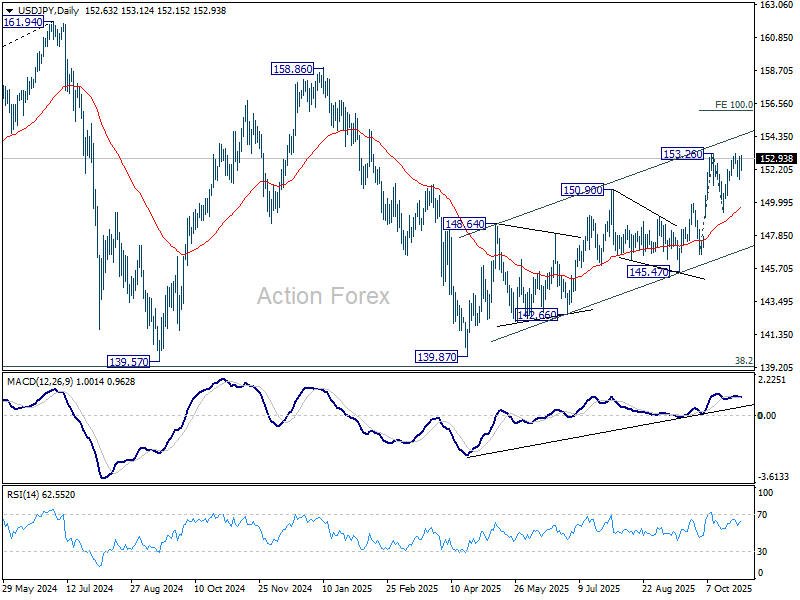

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.83; (P) 152.45; (R1) 153.35; More...

USD/JPY's rebound from 151.52 is still capped below 153.26 resistance and intraday bias remains neutral for now. On the upside, firm break of 153.26 will resume larger rally from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. However, break of 151.52 will extend the corrective pattern from 153.26 with another falling leg, and target 149.37 support instead.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Dollar Rebounds on Hawkish Fed Cut, Momentum Capped by Trade Optimism

Dollar tried to rebound overnight after markets pared back expectations for a December Fed rate cut, but momentum faded quickly in Asia. Optimism over a thaw in U.S.–China relations quickly reversed the rally attempt.

Fed’s three-way split decision to cut the federal funds rate by 25bps to 3.75–4.00% was interpreted as slightly more hawkish than expected. While Governor Stephen Miran again voted for a deeper 50bps move—consistent with his persistent dovish stance—the surprise came from Kansas City Fed President Jeffrey Schmid, who dissented in favor of holding steady.

More importantly, Fed Chair Jerome Powell emphasized during his press conference that another rate cut in December is “not a foregone conclusion.” He added that there were “strongly differing views” among policymakers on how to proceed, reinforcing the notion that the policy debate is far from settled.

Following Powell’s remarks, Fed funds futures repriced swiftly, now implying roughly a 70% chance of another 25bps cut in December, down from 90% before the meeting. The adjustment suggests investors are reassessing the pace and extent of policy easing heading into 2026 amid ongoing inflation and employment concerns.

Meanwhile, the Trump–Xi summit produced tangible progress. US President Donald Trump declared that “we have a deal,” announcing a one-year agreement on rare earths and critical minerals and halving fentanyl-related tariffs on Chinese imports. Trump also confirmed that total tariffs on Chinese exports will be reduced from 57% to 47%. He added that he would visit China in April, while Xi is expected to visit the U.S. "sometime after that".

Markets welcomed the outcome as a sign of easing trade tensions. Risk-sensitive currencies such as New Zealand and Australian Dollars leading gains. Kiwi was the day’s top performer so far, followed by Aussie and Swiss Franc.

Yen, meanwhile, weakened after the BoJ stood pat. Forecasts and language were largely steady. From a policy perspective, a December rate hike remains a 50/50 call, contingent on both incoming data and Prime Minister Sanae Takaichi’s approach to monetary normalization. Dollar was the second weakest major on the day, with Loonie rounding out the bottom three. Meanwhile, Sterling steadied after a bruising week and traded mid-pack with Euro.

Focus to the ECB later today, and it's meeting later today, and it's expected to deliver no change in rates and little new guidance. Policymakers are likely to reiterate that current policy settings are appropriate. The implications would be that the bar for any policy move—up or down—remains high.

In Asia, at the time of writing, Nikkei is down -0.43%. Hong Kong HSI is down -0.32%. China Shanghai SSE is down -0.32%. Singapore Strait Times is down -0.47%. Overnight, DOW fell -0.16%. S&P 500 fell -0.00%. NASDAQ rose 0.55%. 10-year yield rose 0.075 to 4.058.

BoJ holds at 0.50%, keeps gradual tightening bias intact

The BoJ left its overnight call rate unchanged at 0.50% as widely expected. The decision came by a 7–2 vote, with Hajime Takata and Naoki Tamura again dissenting in favor of a 25bps rate hike to move policy a little closer to neutral. The repeat split highlights the growing divergence within the board as policymakers debate how quickly to normalize monetary conditions.

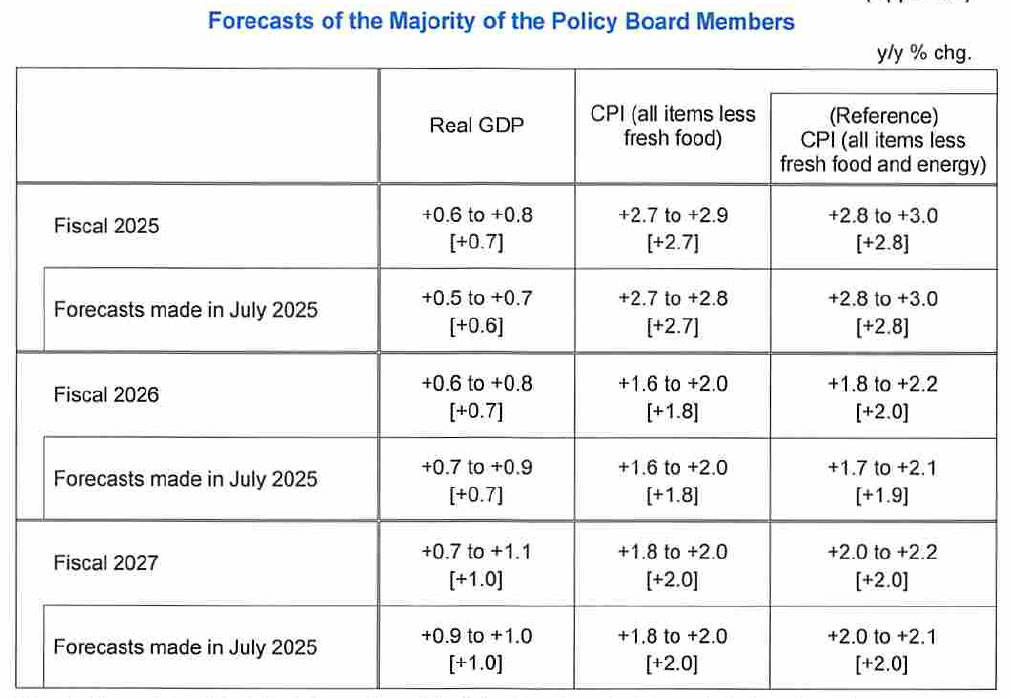

In its quarterly Outlook Report, the BoJ made only marginal revisions to its forecasts, signaling that the economic and inflation outlook remains broadly stable. The bank raised its fiscal 2025 GDP forecast slightly from 0.6% to 0.7%, while projections for 2026 and 2027 were left unchanged at 0.7% and 1.0%, respectively.

On prices, the BoJ kept its core CPI forecast at 2.7% for 2025, 1.8% for 2026, and 2.0% for 2027. Core-core CPI (excluding both fresh food and energy) was nudged higher to 2.0% in 2026 from 1.9%, with other years unchanged (2026 at 2.8% and 2027 at 2.0%). The bank reiterated that underlying inflation is expected to reach 2% in the latter half of the projection period through March 2027, retaining language from July that risks to the inflation outlook remain “roughly balanced.”

The BoJ also reiterated that it would continue to raise its policy rate and adjust the degree of monetary support “in accordance with improvements in the economy and prices.”

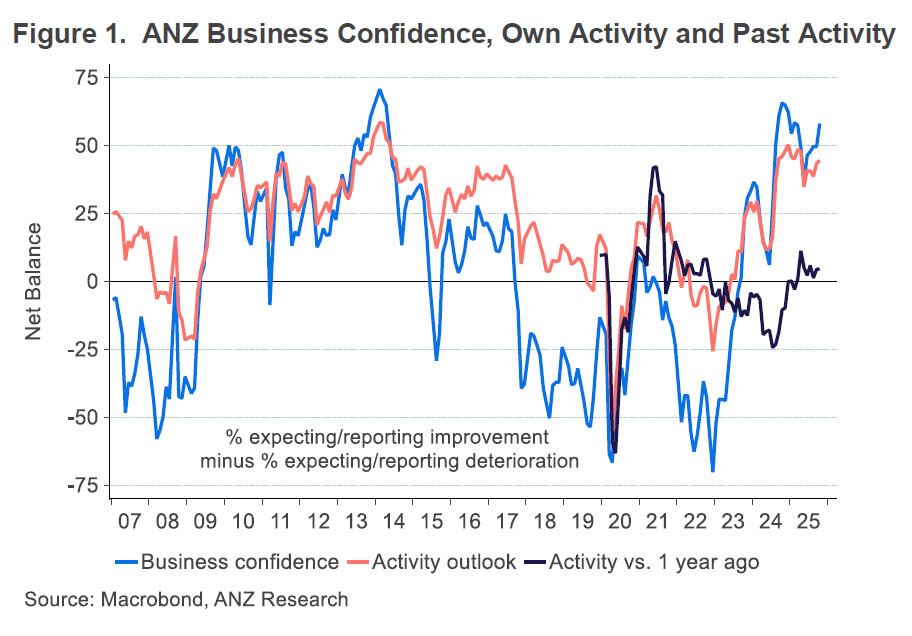

New Zealand ANZ business confidence surges to seven-month high, green shoots emerging

New Zealand’s ANZ Business Confidence Index surged sharply in September, rising from 49.6 to 58.1, the highest level since February. Own Activity Outlook also improved modestly, up from 43.4 to 44.6, marking its strongest reading since April.

Inflation expectations, meanwhile, remained broadly steady. The share of firms expecting to raise prices over the next three months eased slightly from 46% to 44%. Those anticipating cost increases ticked up from 75% to 76%. One-year-ahead inflation expectations edged higher from 2.71% to 2.75%.

ANZ noted that “green shoots are emerging, particularly for interest-rate-sensitive sectors.” The bank highlighted stronger retail sentiment as evidence that the economy is beginning to warm alongside the spring season, with monetary easing and high rural incomes supporting regional confidence and broader recovery momentum.

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.83; (P) 152.45; (R1) 153.35; More...

USD/JPY's rebound from 151.52 is still capped below 153.26 resistance and intraday bias remains neutral for now. On the upside, firm break of 153.26 will resume larger rally from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. However, break of 151.52 will extend the corrective pattern from 153.26 with another falling leg, and target 149.37 support instead.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

BoJ holds at 0.50%, keeps gradual tightening bias intact

The BoJ left its overnight call rate unchanged at 0.50% as widely expected. The decision came by a 7–2 vote, with Hajime Takata and Naoki Tamura again dissenting in favor of a 25bps rate hike to move policy a little closer to neutral. The repeat split highlights the growing divergence within the board as policymakers debate how quickly to normalize monetary conditions.

In its quarterly Outlook Report, the BoJ made only marginal revisions to its forecasts, signaling that the economic and inflation outlook remains broadly stable. The bank raised its fiscal 2025 GDP forecast slightly from 0.6% to 0.7%, while projections for 2026 and 2027 were left unchanged at 0.7% and 1.0%, respectively.

On prices, the BoJ kept its core CPI forecast at 2.7% for 2025, 1.8% for 2026, and 2.0% for 2027. Core-core CPI (excluding both fresh food and energy) was nudged higher to 2.0% in 2026 from 1.9%, with other years unchanged (2026 at 2.8% and 2027 at 2.0%). The bank reiterated that underlying inflation is expected to reach 2% in the latter half of the projection period through March 2027, retaining language from July that risks to the inflation outlook remain “roughly balanced.”

The BoJ also reiterated that it would continue to raise its policy rate and adjust the degree of monetary support “in accordance with improvements in the economy and prices.”

New Zealand ANZ business confidence surges to seven-month high, green shoots emerging

New Zealand’s ANZ Business Confidence Index surged sharply in September, rising from 49.6 to 58.1, the highest level since February. Own Activity Outlook also improved modestly, up from 43.4 to 44.6, marking its strongest reading since April.

Inflation expectations, meanwhile, remained broadly steady. The share of firms expecting to raise prices over the next three months eased slightly from 46% to 44%. Those anticipating cost increases ticked up from 75% to 76%. One-year-ahead inflation expectations edged higher from 2.71% to 2.75%.

ANZ noted that “green shoots are emerging, particularly for interest-rate-sensitive sectors.” The bank highlighted stronger retail sentiment as evidence that the economy is beginning to warm alongside the spring season, with monetary easing and high rural incomes supporting regional confidence and broader recovery momentum.

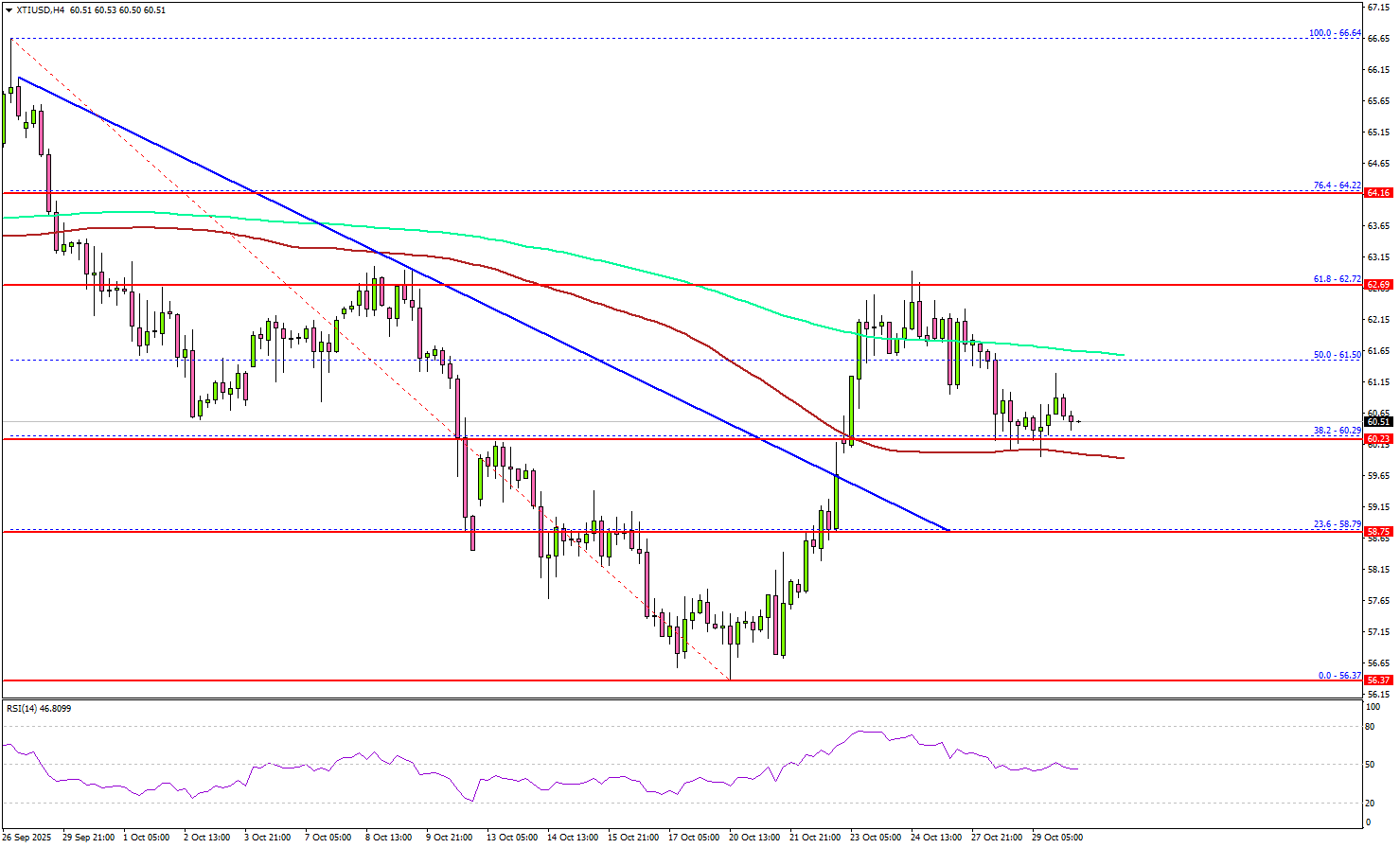

WTI Crude Oil Steadies — Traders Eye GDP Release For Next Cue

Key Highlights

- WTI Crude Oil prices started a recovery wave above $60.00.

- It broke a major bearish trend line with resistance at $59.50 on the 4-hour chart.

- Gold corrected gains and started a consolidation phase near $4,000.

- The US GDP for Q3 2025 could increase 3% (preliminary).

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price found support near $56.50 against the US Dollar. A base was formed, and the price started a recovery wave above $58.00 and $58.80.

Looking at the 4-hour chart of XTI/USD, the price broke a major bearish trend line with resistance at $59.50. There was a move above the 50% Fib retracement level of the downward move from the $66.64 swing high to the $56.37 low.

The price cleared the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour). On the upside, immediate resistance is near the $62.00 level.

The first key hurdle for the bulls could be $62.75 and the 61.8% Fib retracement level of the downward move from the $66.64 swing high to the $56.37 low. The main hurdle sits at $64.00.

A close above $64.00 might send Oil prices toward $65.00. Any more gains might call for a test of $66.50 in the near term. On the downside, the first major support sits near the $60.00 zone.

The next support could be $58.80. A daily close below $58.80 could open the doors for a larger decline. In the stated case, the bears might aim for a drop toward $56.50. Any more losses could open the doors for a test of the $55.00 zone.

Looking at Gold, there was a downside correction, and the price could soon attempt to clear the $4,250 resistance.

Economic Releases to Watch Today

- US Gross Domestic Product for Q3 2025 (Preliminary) – Forecast 3% versus previous 3.8%.

- US Initial Jobless Claims - Forecast 223K, versus 218K previous.

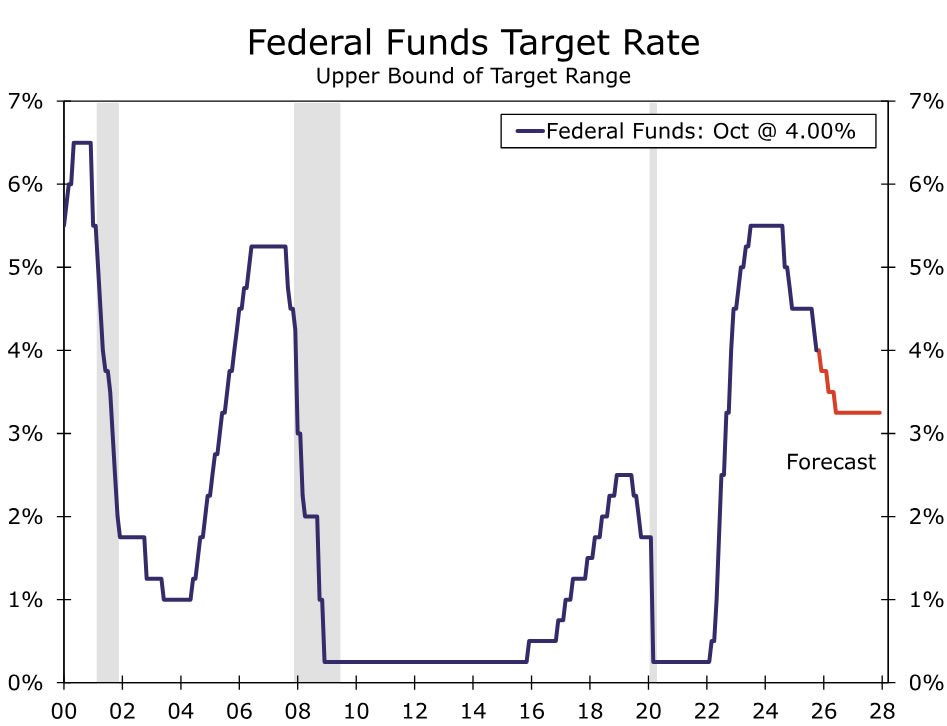

FOMC: Another Risk-Management Cut, but December Looms Large

Summary

- As was widely expected, the FOMC lowered the fed funds target range by 25 bps to 3.75%-4.00% at the conclusion of its October meeting. Yet, Chair Powell made clear that additional easing in December was far from assured.

- The post-meeting statement gave a nod to the more limited slate of data the FOMC was able to take into account over the past month due to the government shutdown. The Committee did, however, suggest that its concern about the labor market did not worsen over the inter-meeting period.

- October's policy rate decision was not unanimous. Governor Miran dissented in favor of a steeper 50 bps rate cut while Kansas City Fed President Schmid dissented the opposite direction in favor of holding the fed funds rate steady.

- The divergent dissents are not wholly surprising given elevated inflation and flagging job growth have created some tension between the Committee's price and employment objectives. But with the jobs market outlook not obviously worsening over the past month, inflation still stubbornly above target, and policy now closer to neutral, the bar to another cut in December is higher.

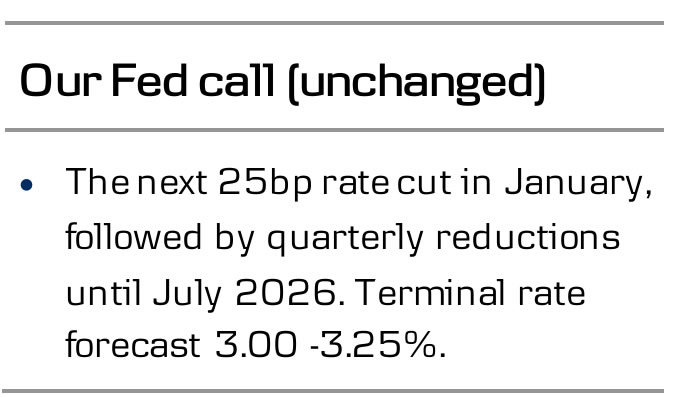

- Our base case remains for the FOMC to reduce the fed funds rate by another 25 bps at its December meeting. That said, with finely balanced risks around the inflation and employment objectives, a deluge of data on the other side of the shutdown could quickly shift the outlook and our expectations for the December meeting. Chair Powell does not think it is a slam dunk decision, and neither do we.

- Notably, the FOMC announced that quantitative tightening would come to an end on December 1. This was one month sooner than our long-standing forecast, although in the grand scheme of the Fed's $6.6 trillion balance sheet, the one-month shortening of the roughly $20 billion monthly runoff will not have a material impact on longer-term yields, in our view.

FOMC Delivers October Cut, But the Bar is Higher for December

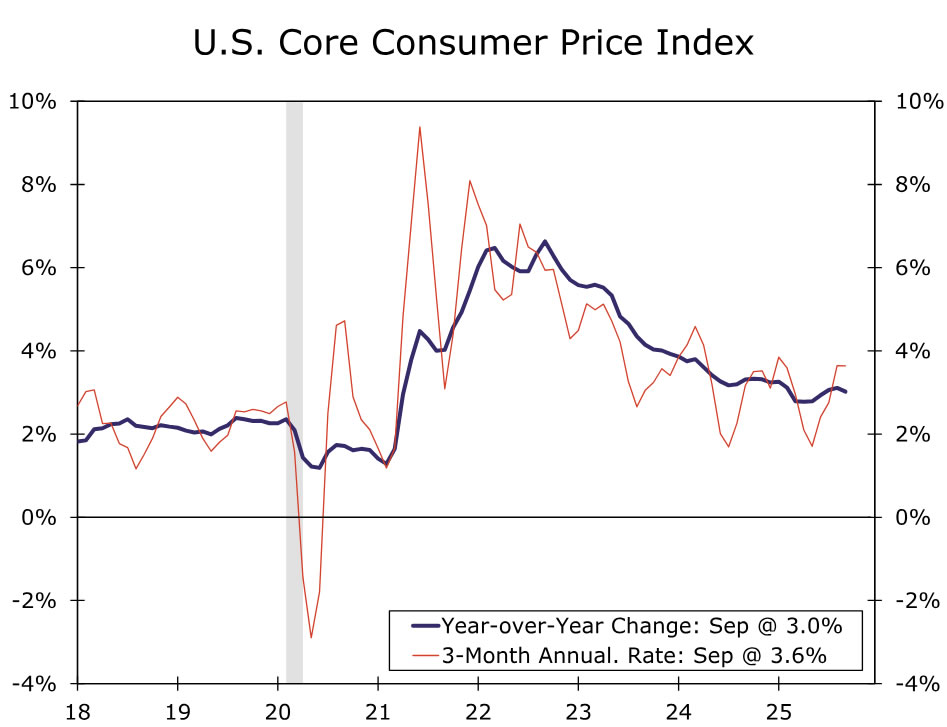

As was widely expected, the FOMC reduced the target range of the fed funds rate by 25 bps points to 3.75%-4.00% at the conclusion of its October meeting. The decision comes under odd circumstances. The ongoing government shutdown has deprived the Committee of key data used to inform its view of the economy. The belatedly-released September CPI report showed inflation still stuck around a 3% pace (chart), but the Producer Price Index has not been published, leaving a less complete picture of recent inflation than the FOMC would have ordinarily. Furthermore, while the Committee has grown more concerned about the state of the labor market the past few months, it did not receive data on nonfarm payrolls and the unemployment rate for September. What data have become available since the Committee last gathered continue to paint a picture of anemic hiring but low layoffs, keeping the jobs market in a delicate spot.

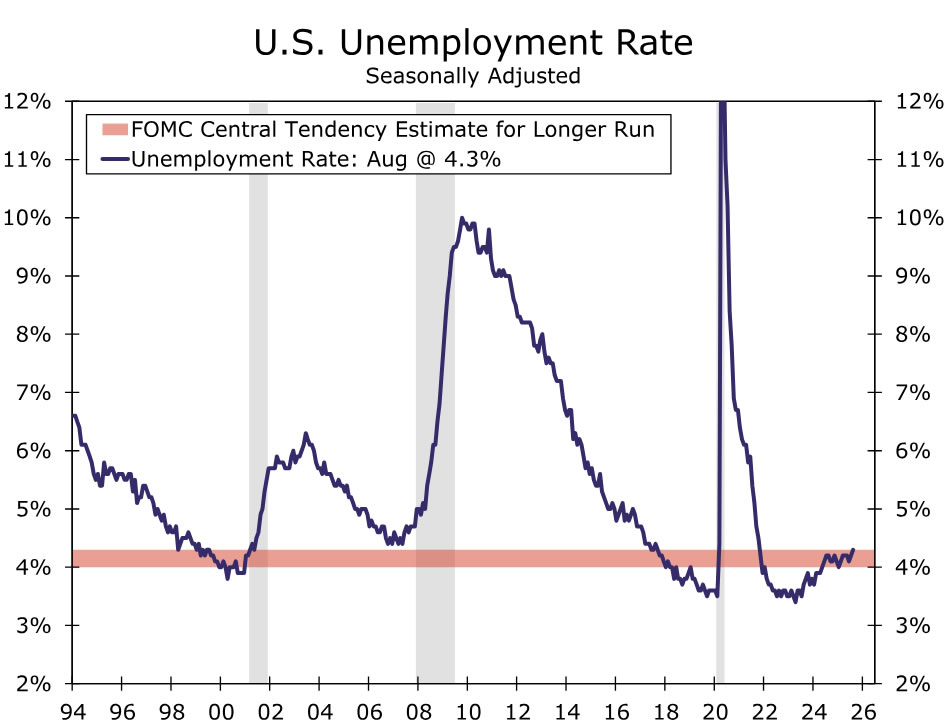

In a nod to the government shutdown affecting the data flow, the post-meeting policy statement said that "Available indicators suggest that economic activity has been expanding at a moderate pace" versus previously mentioning that activity had "moderated in the first half of the year." It further noted that recent private sector readings on the jobs market looked consistent with the slowdown in payroll growth and uptick in unemployment since the start of the year (chart).

However, concern about the jobs market does not appear to have increased further over the inter-meeting period. In the Committee's previous post-meeting statement, it noted that the downside risks to employment "have risen", yet today's statement read that those risks merely "rose in recent months." Similarly, the statement hinted that the FOMC does not see the current state of inflation as having worsened since mid-September; it said that "inflation has moved up since earlier this year", with the timing reference new.

Notably, today's rate decision was not unanimous. Governor Miran once again dissented in favor of a 50 bps rate cut. At the same time, Kansas City Federal President Schmid dissented in favor of keeping the target range unchanged. Dissents in both the hawkish and dovish direction speak to the difficult position the FOMC finds itself in at this juncture. Not only has visibility on the economy become more limited with the shutdown, but elevated inflation and flagging job growth have created some tension between the Committee's price and employment objectives.

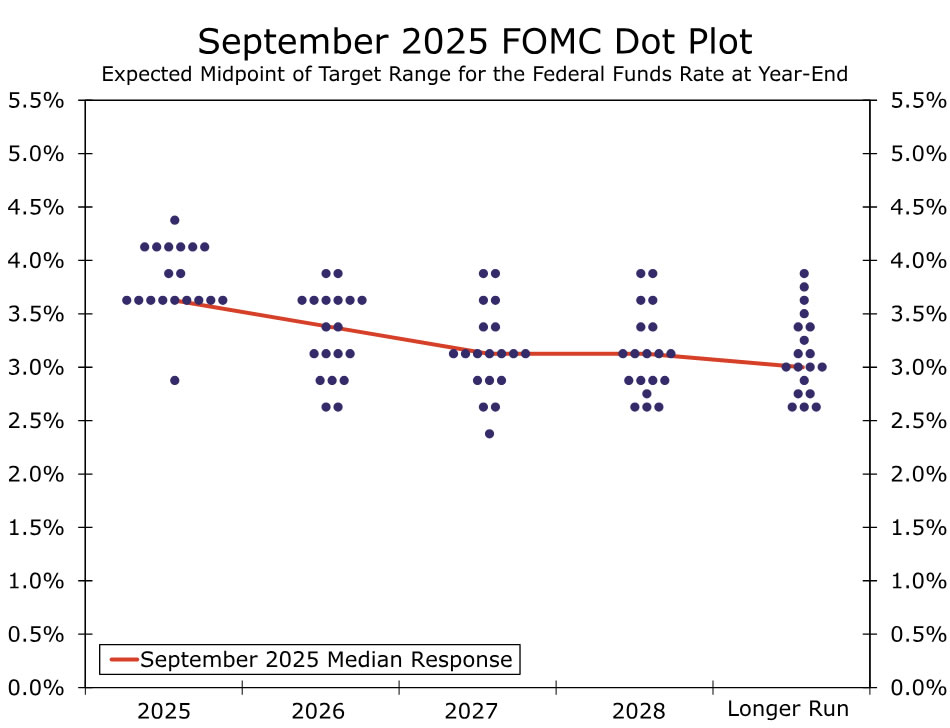

Together, the subtle statement changes and two-sided dissents suggest the bar for another cut at the December meeting is getting higher. That message was made even more clear in the post-meeting press conference. In his opening remarks, Chair Powell shared that "A further reduction in the policy rate at the December meeting is not a foregone conclusion. Far from it. Policy is not on a preset course." The September Summary of Economic Projections already showed the Committee closely split between three 25 bps or fewer cuts this year (chart). With the policy rate closer to neutral, risks to the jobs market not obviously having worsened and inflation still stubbornly above target, the case for a third consecutive reduction in the policy rate has become less straightforward.

Our base case remains for the FOMC to reduce the fed funds rate by another 25 bps at its December meeting (chart). That said, with finely balanced risks around the inflation and employment objectives, a deluge of data on the other side of the shutdown could quickly shift the outlook and our expectations for the December meeting. Chair Powell does not think it is a slam dunk decision, and neither do we.

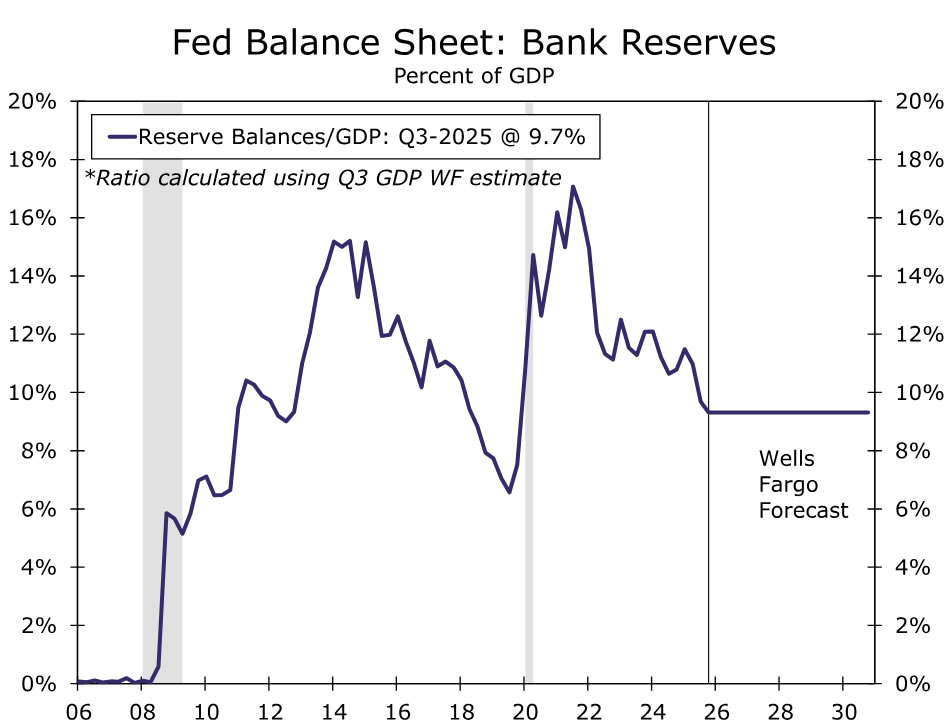

Balance Sheet Runoff to End December 1

The FOMC also announced today that its balance sheet runoff would end on December 1. This was one month sooner than our forecast, although in the grand scheme of the Fed's $6.6 trillion balance sheet, a one month shortening of the roughly $20 billion monthly runoff will not have a material impact on longer-term yields, in our view. Runoff of mortgage-backed securities will continue indefinitely, with the proceeds plowed into Treasury bills one-for-one such that the total size of the central bank's balance sheet is left unchanged.

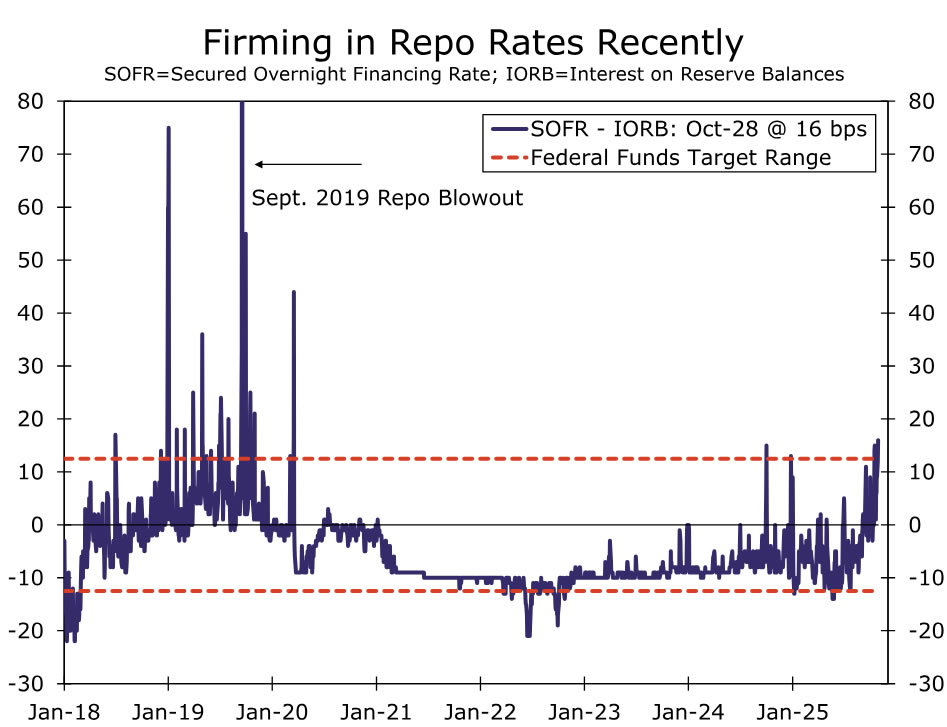

The end of runoff comes at a time when money market rates have been rising in a sign that bank reserves are becoming less abundant (chart). The next phase of the Fed's balance sheet evolution will entail the central bank keeping its security holdings flat and monitoring carefully for the optimal equilibrium. It is important to note that even if aggregate balance sheet runoff ceases, that does not mean that balance sheet policy has shifted to neutral. If the Fed's balance sheet is held flat for an extended period of time, then it will still be shrinking as a share of GDP. Bank reserves will continue to decline gradually and in proportion to the growth in non-reserve liabilities on the Fed's balance sheet, such as currency in circulation.

Thus, eventually the Fed's balance sheet will need to resume growing again to prevent bank reserves from falling below the "ample" threshold. Our base case is that these reserve management purchases will begin in April 2026 and average approximately $25 billion per month, with purchases concentrated entirely in Treasury bills. If realized, this should be enough to keep the reserves-to-GDP ratio a little bit above 9%, a key threshold we and others have highlighted previously as a demarcation line between ample and abundant reserves (chart).

Fed Review: Hawkish Cut

- The Fed cut its policy rate target by 25bp in its October meeting, as widely anticipated. Interest rate on reserve balances (IORB) was cut by an equal amount.

- Powell hawkishly underscored that the December rate decision is still far from a done deal. This led to a repricing of front-end rate expectations, with the implied probability of a December cut declining from above 90% to around 60%. EUR/USD rate declined to around 1.16.

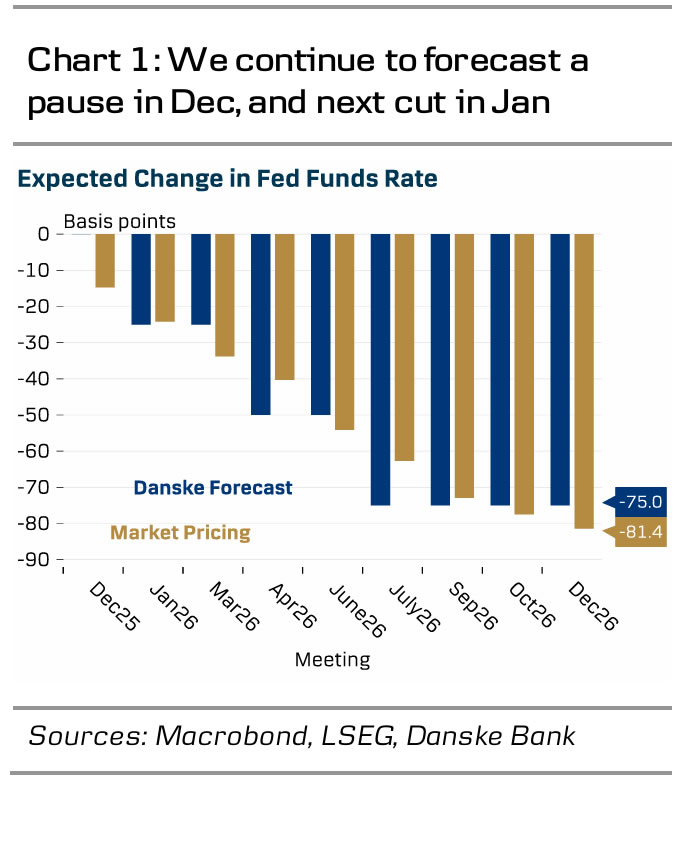

- We make no changes to our Fed call and still expect a pause in December with the next cut in January.

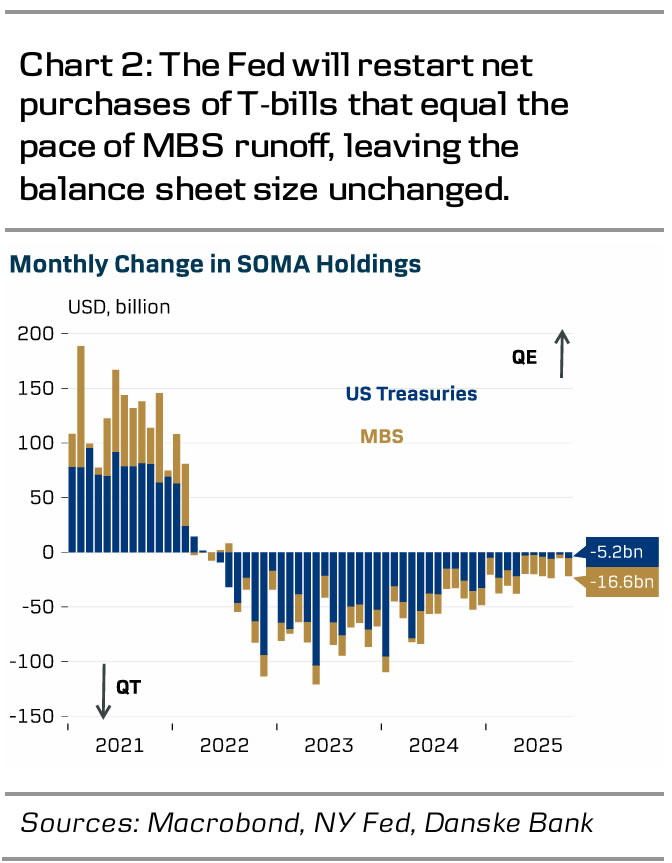

- The Fed also announced an end to QT. Balance sheet runoff continues for mortgage-backed securities (MBS), but all maturing principal payments will be reinvested into T-bills from December 1 onwards. Markets were well prepared for the announcement with also the long-end UST yields shifting higher.

Ahead of the meeting, we expected Powell to avoid pre-committing to a December rate cut, but his clear pushback against the market pricing was more hawkish than even we anticipated. Powell emphasized that 'another cut in December is far from assured' amid the committee's 'strongly differing views' about the future, and that 'there is a growing chorus of feeling we should maybe wait a cycle'. He highlighted that despite the shutdown, available data does not signal significant further cooling in labour markets.

After the September meeting, we pointed out that the 'dots' signalled an almost even split between participants expecting cuts in both Oct & Dec, and those expecting only 0-1 cuts. We argued that markets underappreciated FOMC's willingness to pause, as ahead of this meeting, markets were pricing more than 90% likelihood for another cut in December. We stick to our call and expect a pause in December followed by the next cut in January. We still think the Fed is the best served by a more gradual approach towards further easing.

Markets were well prepared for the announcement to end QT. In our preview (see RtM USD, 28 Oct), we anticipated that the Fed would choose a less aggressive option of only ending the balance sheet runoff for US Treasuries. Instead, it opted to also 'neutralize' the runoff of mortgage-backed securities (MBS) by reinvesting the maturing principal payments to T-bills from December 1. Over the past few months, the pace of QT has been around USD5bn per month for Treasury securities and around USD16-17bn per month for MBS. Despite the seemingly 'dovish' balance sheet decision, UST yields moved higher already before the hawkish remarks in the press conference. This likely reflected Jeffrey Schmid's surprising dissent in favour of holding rates steady at this meeting. Less surprisingly, Stephen Miran also dissented, but in favour of a 50bp cut.

Powell flagged that eventually the Fed will look to start adding to reserve balances by increasing the size of its balance sheet again but did not yet speculate on the timing. The Fed did not perform an additional cut to the IORB rate, as speculated by some ahead of the meeting. This would have been an even more aggressive measure to ease the upward pressure seen in repo rates over past weeks and remains a possibility for future meetings.