Sample Category Title

Canadian Dollar Jumps as BoC Declares Policy ‘About Right’ After Cut

Canadian Dollar climbed after the BoC lowered its overnight rate to 2.25% and signaled that policy is likely now at its terminal level. The bank’s statement that rates are “about the right level” if the outlook unfolds as expected was interpreted as a clear end-of-cycle message. The message was subtle but decisive: the bar for additional easing is now much higher.

That stance gave the Loonie a lift, even as the currency’s gains were eclipsed by Aussie, which remains the day's star performer. Stronger-than-expected CPI report earlier today led some analysts to abandon expectations of further RBA cuts, while some analysts now speculate that the next policy move could even be upward if price pressures persist. Kiwi also joined the rally, supported by robust risk appetite.

At the weaker end, Sterling extended its sell-off amid lingering fiscal concerns tied to next month’s budget and a deteriorating U.K. fiscal outlook. The Swiss Franc and Euro also traded lower. Dollar and Yen were positioned mid-range ahead of Fed decision.

Attention now turns to the Fed, which is widely expected to cut rates by 25 bps to 3.75–4.00%. Futures continue to price in about a 90% chance of another cut in December, meaning that unless Fed Chair Jerome Powell explicitly pushes back, markets are unlikely to adjust much. Opinions on the 2026 policy path remain highly divided, not least because of uncertainty surrounding Powell’s successor. Until a decision is made and fresh data are available, markets are unlikely to get a clear picture of where rates may stand in 2026.

On the trade front, US President Donald Trump told business leaders at the APEC Summit he was confident of striking a “good deal” with President Xi Jinping at their Thursday meeting—the first since Trump’s second-term tariff offensive began. Officials say the deal could include deferring China’s export controls on rare earth minerals and scrapping the planned 100% U.S. tariff on Chinese goods, as well as renewed agricultural purchases. That optimism has helped propel U.S. indexes to record highs this week, a rally that now depends on both leaders delivering on expectations.

In Europe, at the time of writing, FTSE is up 0.64%. DAX is down -0.27%. CAC is down -0.30%. UK 10-year yield is down -0.01 at 4.395. Earlier in Asia, Nikkei rose 2.17%. Hong Kong was on holiday. China Shanghai SSE rose 0.70%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield rose 0.015 to 1.654.

BoC cuts to 2.25%, signals end of easing Cycle

BoC delivered a widely expected 25bps rate cut, lowering its overnight rate to 2.25%, but signaled that this could mark the end of its current easing cycle. The central bank said that if inflation and economic activity evolve in line with its October projection, the current policy rate is “about the right level” to balance supporting growth with keeping inflation close to target. That phrasing was interpreted as indicating that 2.25% is the likely terminal rate, barring major economic shocks.

In its accompanying statement, the BoC acknowledged that U.S. trade actions and uncertainty are having “severe effects” on key export-oriented industries. As a result, the Bank expects GDP growth to remain weak in the second half of the year before recovering gradually through 2026. The economy is projected to expand 1.2% in 2025, 1.1% in 2026, and 1.6% in 2027, with excess capacity expected to be absorbed only slowly.

The BoC described the labour market as soft, with job declines concentrated in trade-sensitive sectors, while hiring across the broader economy remains subdued.

On inflation, the BoC noted that headline CPI stood at 2.4% in September, slightly above expectations, while its preferred core measures remain sticky around 3%. Broader alternative indicators suggest underlying inflation near 2.5%, but the BoC expects price pressures to ease gradually and headline CPI to remain close to 2% over the projection horizon.

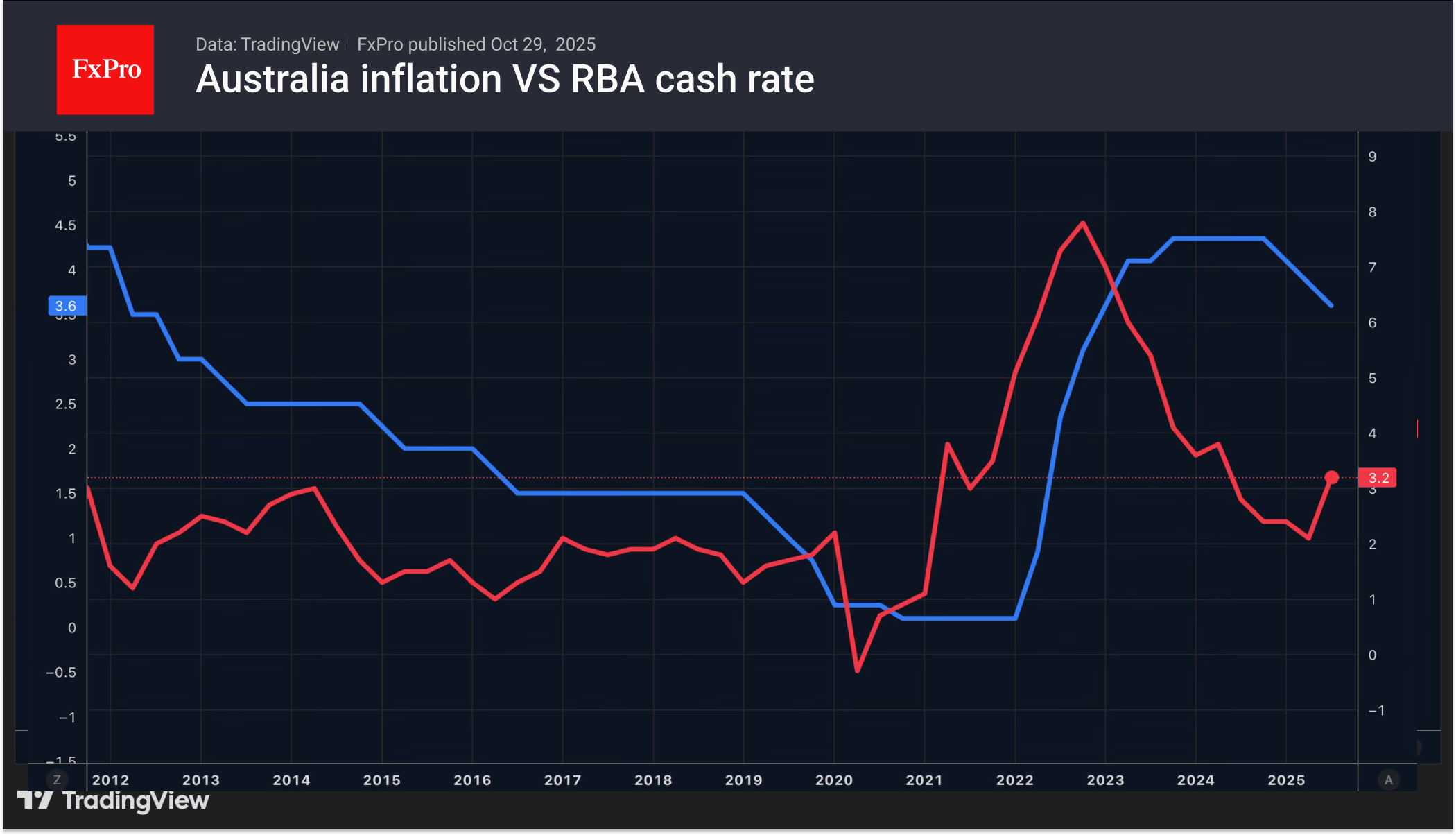

Australia inflation shock: CPI surges to 3.2%, core re-accelerates

Australia’s inflation surprised sharply to the upside in Q3, reigniting concerns that price pressures are proving stickier than expected. Headline CPI jumped 1.3% qoq, accelerating from 0.7% in Q2 and beating expectations of 1.1% — marking the strongest quarterly increase since Q1 2023. The Australian Bureau of Statistics said the largest contributor was a 9.0% rise in electricity costs, which alone drove much of the headline surge.

On an annual basis, CPI rose to 3.2% yoy, sharply higher than the previous 2.1% yoy and above forecasts of 3.0%. That marks the fastest pace of annual inflation since Q2 2024. Electricity costs were again the main driver, soaring 23.6% from a year earlier despite targeted government relief measures.

Core inflation was equally strong. Trimmed mean CPI — the RBA’s preferred measure — rose 1.0% qoq, up from 0.7% and above expectations of 0.8%. Annually, core inflation accelerated to 3.0% yoy from 2.7%, underlining persistent price pressures across utilities and essential services, exceeding the RBA’s 2–3% target range again. This marks the first uptick in the trimmed mean since Q4 2022, confirming that underlying price momentum remains firm.

The data strengthen the case for the RBA to delay or even reconsider rate-cut expectations for the near term.

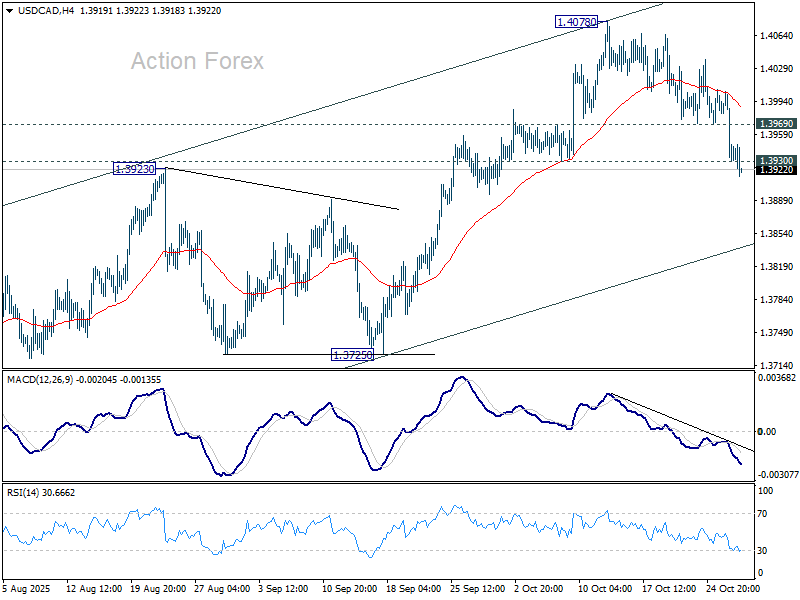

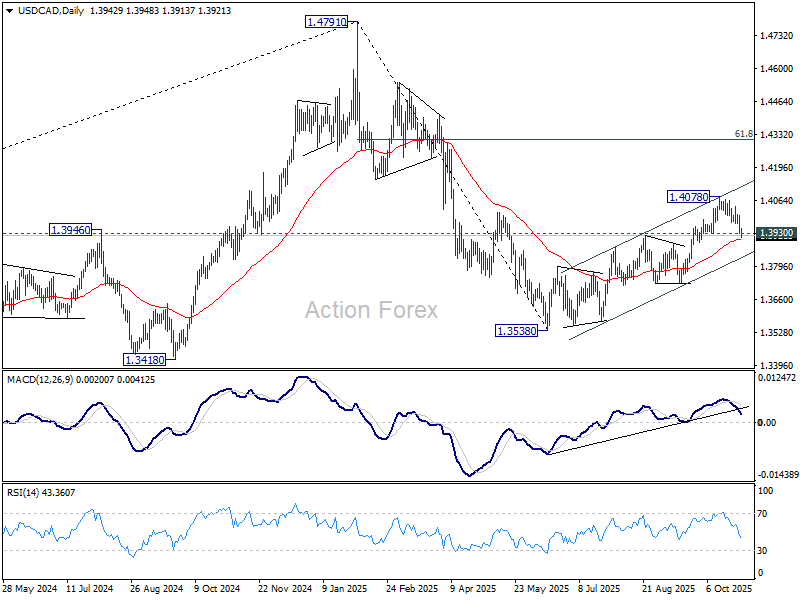

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3962; (R1) 1.3989; More...

Intraday bias in USD/CAD is back now on the downside with break of 1.3930 support. Fall from 1.4078 should extend to rising channel support (now at 1.3835). Sustained break there will be a sign of bearish reversal. That is, rebound from has completed at 1.4078, and further fall would be seen to 1.3725 support for confirmation. On the upside, though, above 1.3969 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds. However, firm break of 1.3725 will revive the case that fall from 1.4791 is indeed a larger scale correction.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3962; (R1) 1.3989; More...

Intraday bias in USD/CAD is back now on the downside with break of 1.3930 support. Fall from 1.4078 should extend to rising channel support (now at 1.3835). Sustained break there will be a sign of bearish reversal. That is, rebound from has completed at 1.4078, and further fall would be seen to 1.3725 support for confirmation. On the upside, though, above 1.3969 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds. However, firm break of 1.3725 will revive the case that fall from 1.4791 is indeed a larger scale correction.

BoC cuts to 2.25%, signals end of easing Cycle

BoC delivered a widely expected 25bps rate cut, lowering its overnight rate to 2.25%, but signaled that this could mark the end of its current easing cycle. The central bank said that if inflation and economic activity evolve in line with its October projection, the current policy rate is “about the right level” to balance supporting growth with keeping inflation close to target. That phrasing was interpreted as indicating that 2.25% is the likely terminal rate, barring major economic shocks.

In its accompanying statement, the BoC acknowledged that U.S. trade actions and uncertainty are having “severe effects” on key export-oriented industries. As a result, the Bank expects GDP growth to remain weak in the second half of the year before recovering gradually through 2026. The economy is projected to expand 1.2% in 2025, 1.1% in 2026, and 1.6% in 2027, with excess capacity expected to be absorbed only slowly.

The BoC described the labour market as soft, with job declines concentrated in trade-sensitive sectors, while hiring across the broader economy remains subdued.

On inflation, the BoC noted that headline CPI stood at 2.4% in September, slightly above expectations, while its preferred core measures remain sticky around 3%. Broader alternative indicators suggest underlying inflation near 2.5%, but the BoC expects price pressures to ease gradually and headline CPI to remain close to 2% over the projection horizon.

Bank of Canada lowers policy rate to 2¼%

The Bank of Canada today reduced its target for the overnight rate by 25 basis points to 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%.

With the effects of US trade actions on economic growth and inflation somewhat clearer, the Bank has returned to its usual practice of providing a projection for the global and Canadian economies in this Monetary Policy Report (MPR). Because US trade policy remains unpredictable and uncertainty is still higher than normal, this projection is subject to a wider-than-usual range of risks.

While the global economy has been resilient to the historic rise in US tariffs, the impact is becoming more evident. Trade relationships are being reconfigured and ongoing trade tensions are dampening investment in many countries. In the MPR projection, the global economy slows from about 3¼% in 2025 to about 3% in 2026 and 2027.

In the United States, economic activity has been strong, supported by the boom in AI investment. At the same time, employment growth has slowed and tariffs have started to push up consumer prices. Growth in the euro area is decelerating due to weaker exports and slowing domestic demand. In China, lower exports to the United States have been offset by higher exports to other countries, but business investment has weakened. Global financial conditions have eased further since July and oil prices have been fairly stable. The Canadian dollar has depreciated slightly against the US dollar.

Canada’s economy contracted by 1.6% in the second quarter, reflecting a drop in exports and weak business investment amid heightened uncertainty. Meanwhile, household spending grew at a healthy pace. US trade actions and related uncertainty are having severe effects on targeted sectors including autos, steel, aluminum, and lumber. As a result, GDP growth is expected to be weak in the second half of the year. Growth will get some support from rising consumer and government spending and residential investment, and then pick up gradually as exports and business investment begin to recover.

Canada’s labour market remains soft. Employment gains in September followed two months of sizeable losses. Job losses continue to build in trade-sensitive sectors and hiring has been weak across the economy. The unemployment rate remained at 7.1% in September and wage growth has slowed. Slower population growth means fewer new jobs are needed to keep the employment rate steady.

The Bank projects GDP will grow by 1.2% in 2025, 1.1% in 2026 and 1.6% in 2027. On a quarterly basis, growth strengthens in 2026 after a weak second half of this year. Excess capacity in the economy is expected to persist and be taken up gradually.

CPI inflation was 2.4% in September, slightly higher than the Bank had anticipated. Inflation excluding taxes was 2.9%. The Bank’s preferred measures of core inflation have been sticky around 3%. Expanding the range of indicators to include alternative measures of core inflation and the distribution of price changes among CPI components suggests underlying inflation remains around 2½%. The Bank expects inflationary pressures to ease in the months ahead and CPI inflation to remain near 2% over the projection horizon.

With ongoing weakness in the economy and inflation expected to remain close to the 2% target, Governing Council decided to cut the policy rate by 25 basis points. If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment. If the outlook changes, we are prepared to respond. Governing Council will be assessing incoming data carefully relative to the Bank’s forecast.

The Canadian economy faces a difficult transition. The structural damage caused by the trade conflict reduces the capacity of the economy and adds costs. This limits the role that monetary policy can play to boost demand while maintaining low inflation. The Bank is focused on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval.

Information note

The next scheduled date for announcing the overnight rate target is December 10, 2025. The Bank’s next MPR will be released on January 28, 2026.

Fed Will Make Things Clear

- Strong statistics are helping the dollar.

- The Fed may spring a surprise.

- The US asks the Bank of Japan to loosen its grip.

- The Aussie becomes the favourite.

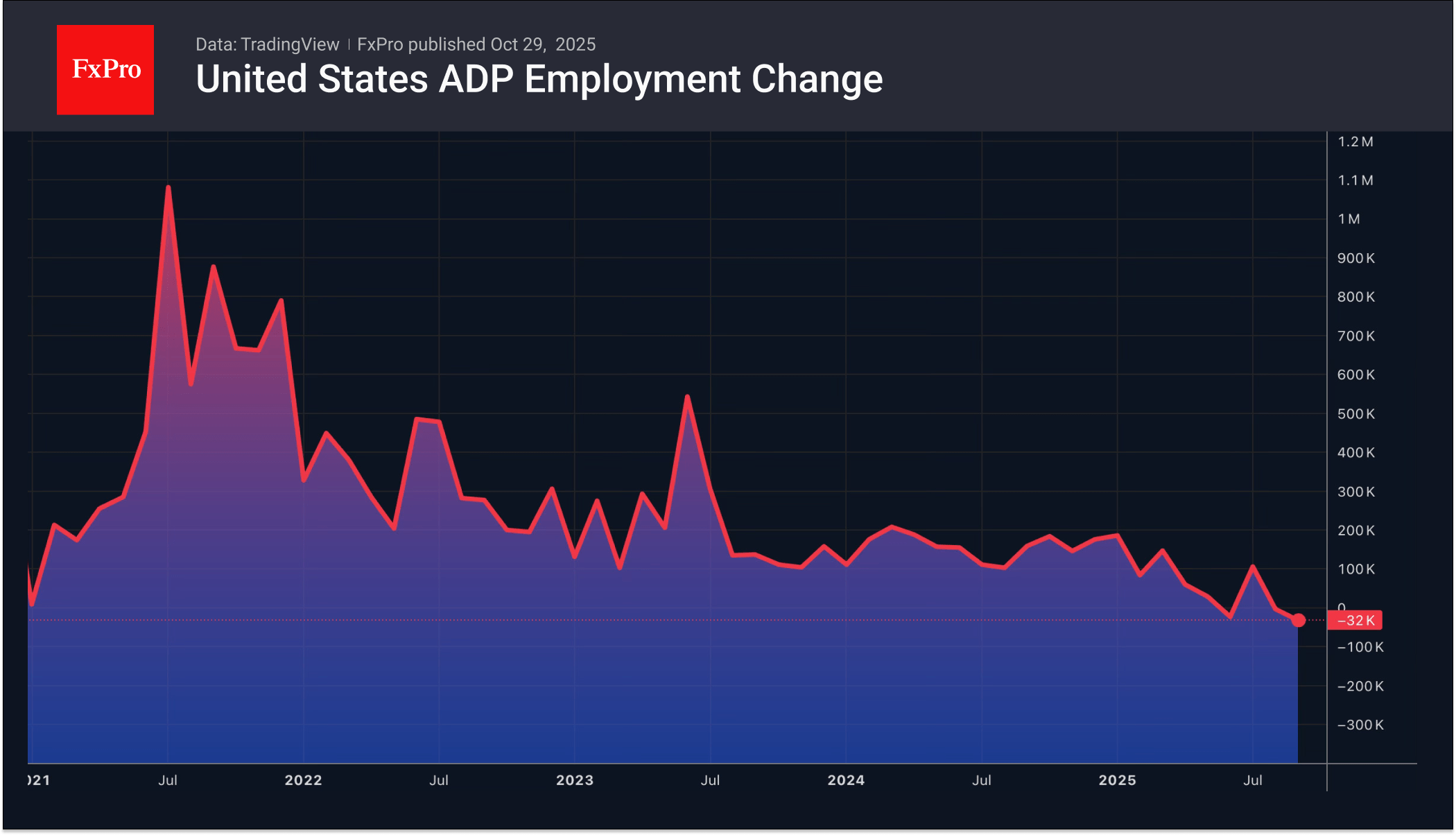

Strong US macroeconomic data and the closure of speculative positions on the US dollar ahead of the FOMC meeting announcement caused the EURUSD to retreat. ADP reported that private sector employment growth averaged 14,250 over the last four weeks to October 11. Compared to a decline of 32,000 over August, this indicates an improvement in the labour market. This pleases Fed hawks.

The doves received a dose of positivity after the September inflation statistics. Each group of opponents has its own trump cards. The divided Committee does not allow Jerome Powell to give a clear signal about the future of interest rates. The Fed chairman’s hawkish rhetoric is expected to positively impact the US dollar. The chances of monetary policy easing after December will fall, and EURUSD will drop even lower. On the contrary, a quiet and peaceful FOMC meeting will allow the world’s main currency pair to resume growth.

Meanwhile, the yen continues to strengthen. Scott Bessent called on the Japanese government to give its central bank room for manoeuvre. In his opinion, tightening monetary policy will help to anchor inflation expectations and prevent excessive exchange rate volatility. The White House is clearly unhappy with the previous USDJPY rallies. This is forcing the bulls to take profits, which leads to a pullback. While the chances of an overnight rate hike in October are slim, Kazuo Ueda’s hawkish rhetoric could breathe new life into the yen, boosting chances of a December hike.

Meanwhile, the Australian dollar has become a notable star in the Forex market recently. Accelerating inflation Down Under to a 2.5-year high has added fuel to the AUDUSD rally. The futures market has lowered the chances of the RBA easing monetary policy in early November from 40% to 8%. The probability of a sharp cash rate cut by December is only 25%.

The Aussie was supported by rumours that the US intends to reduce tariffs on Chinese imports related to fentanyl from 20% to 10% in exchange for Beijing tightening export controls on these goods. If this happens, the average tariff against China will fall from 55% to 45%. This is good news for the yuan and its proxy currencies, including the Australian dollar.

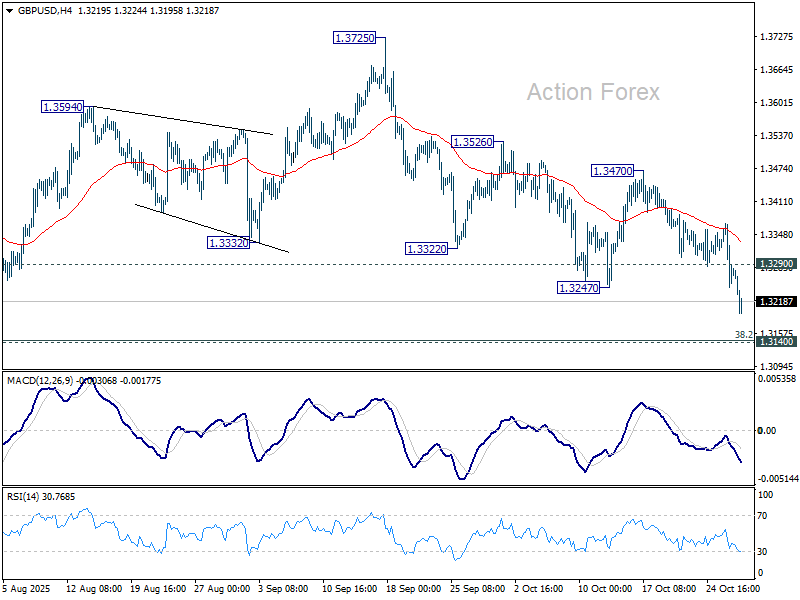

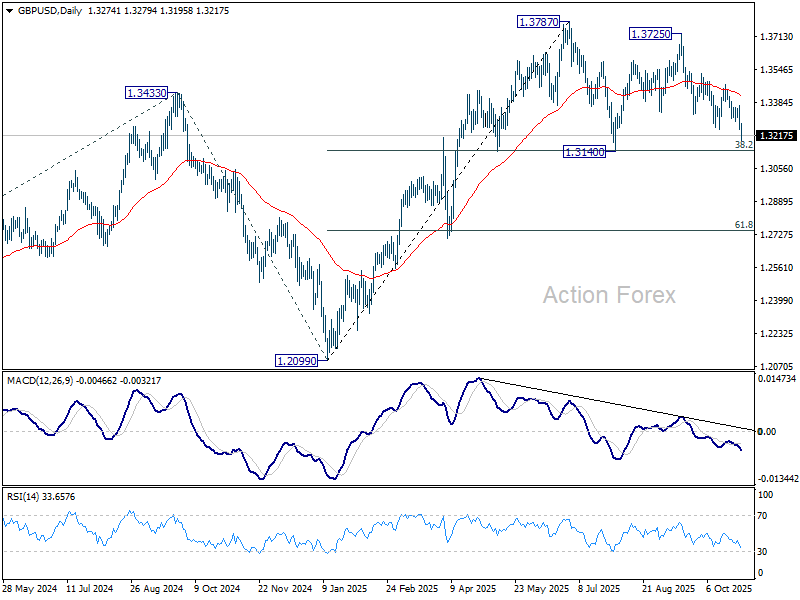

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3223; (P) 1.3297; (R1) 1.3345; More...

Intraday bias in GBP/USD stays on the downside for 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, above 1.3290 minor resistance will turn intraday bias neutral first. However, decisive break of 1.3140/2 will complete a double top pattern (1.3787/3725) and turn near term outlook bearish.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

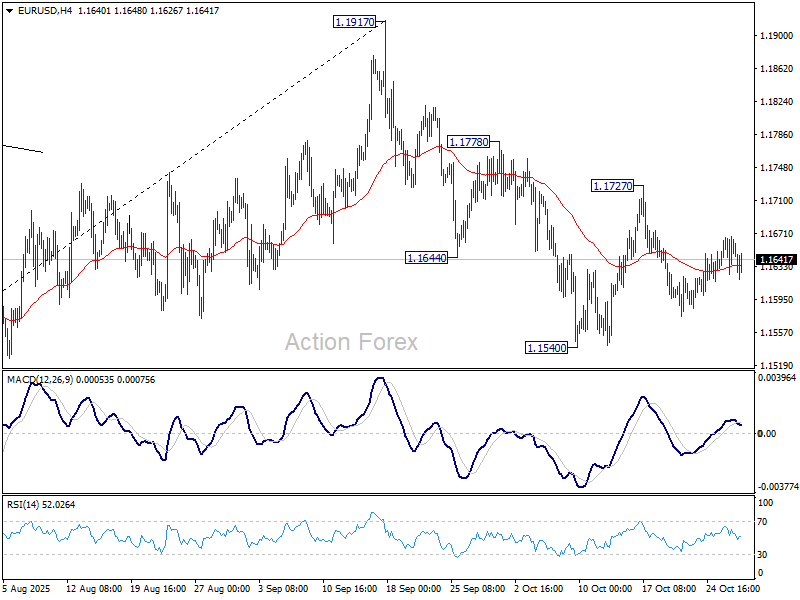

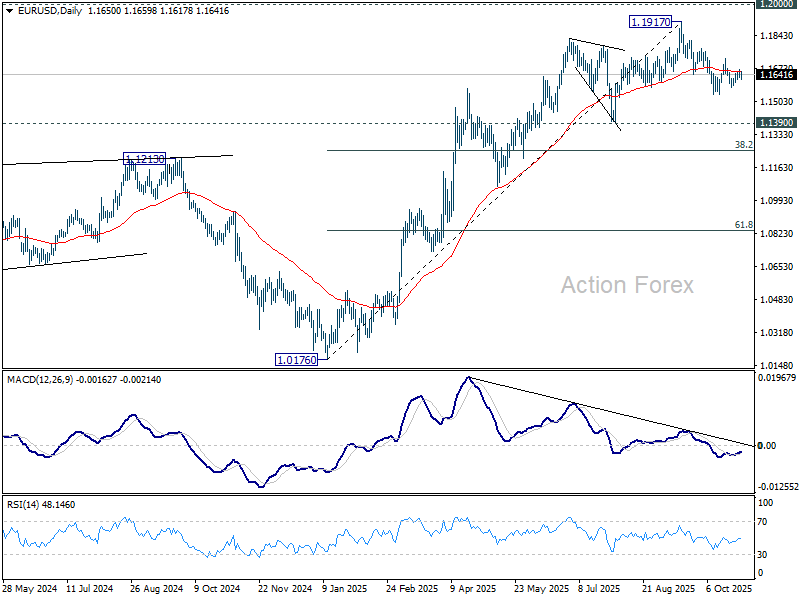

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1628; (P) 1.1648; (R1) 1.1672; More…

No change in EUR/USD's outlook as sideway trading continues. Intraday bias remains neutral for the moment. On the downside, below 1.1540 will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

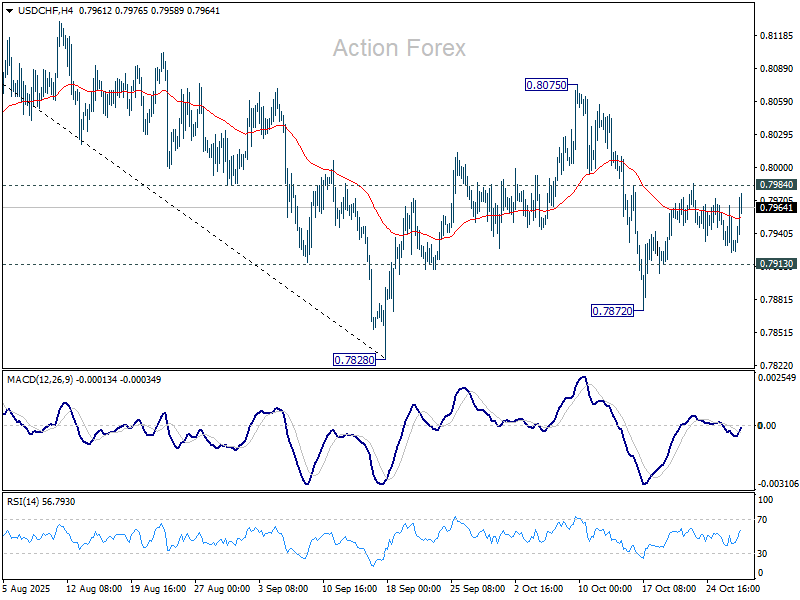

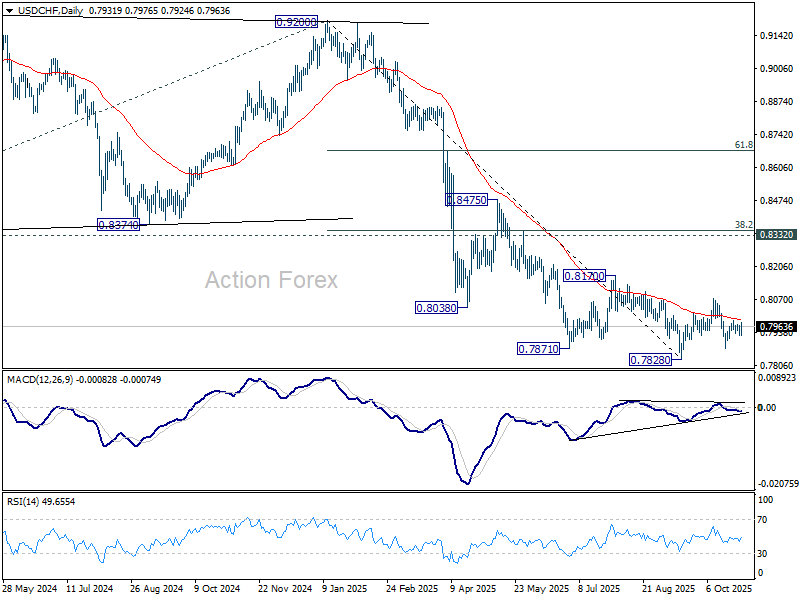

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7917; (P) 0.7942; (R1) 0.7959; More…

Intraday bias in USD/CHF stays neutral as sideway trading continues. On the downside, below 0.7913 will turn bias to the downside for 0.7872 support, and then 0.7828 low. However, firm break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

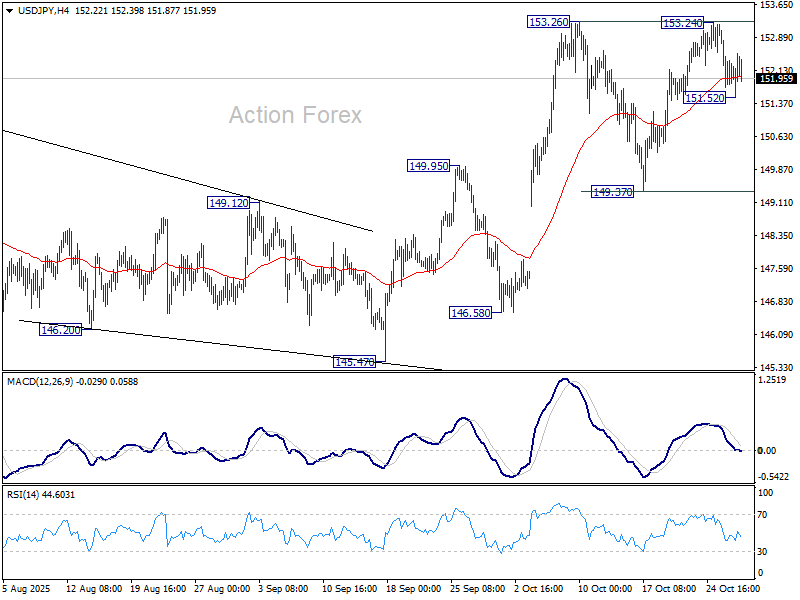

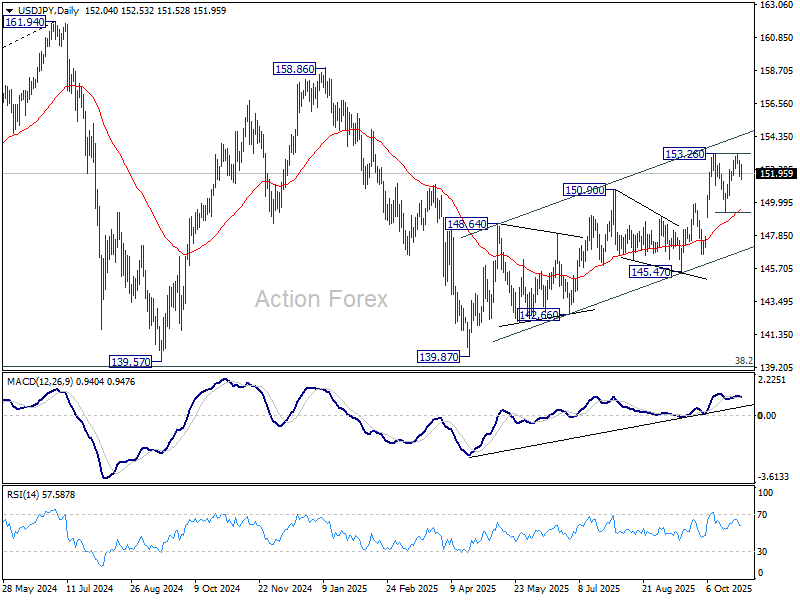

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.61; (P) 152.26; (R1) 152.75; More...

Intraday bias in USD/JPY remains neutral for the moment. On the upside, firm break of 153.24 will resume larger rally from 139.87. On the downside, break of 151.52 and sustained trading below 55 4H EMA (now at 151.99) will indicate that corrective pattern from 153.26 is extending with the third leg, and target 149.37 support next.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Fed (FOMC) Meeting Preview: 25 Bps Cut Incoming, Implications for US Dollar (DXY)

The Federal Reserve's meeting is wrapping up today, Wednesday, October 29, 2025. The biggest expected outcome is a change in monetary policy: the central bank is widely anticipated to lower its main interest rate (the federal funds rate) by 25 basis points (or a quarter of a percentage point).

This move would set the new target rate range at 3.75% to 4.00%. Financial markets are nearly certain this will happen, with a 99% probability already factored into trading.

Rate Action and Dissent

A decision to cut interest rates is primarily focused on the weakening job market, even though the economy's growth (GDP) was still strong at 3.8% last quarter. Policymakers seem willing to ignore inflation because they think the recent price hikes, mainly caused by new tariffs, won't last.

However, the Fed is still deeply divided. At least one official, likely Governor Miran, is expected to formally disagree with the decision, arguing for a larger 50 basis point (half-percent) rate cut. This sharp disagreement highlights a major split: some policymakers want to lower rates faster to prevent job losses, while others are worried that cutting too much will cause inflation to rise again.

The push for a deeper cut suggests that if the next report on the job market (whenever it finally comes out after the government shutdown) is very weak, the majority of the Fed could quickly agree to lower rates more aggressively than they are planning right now.

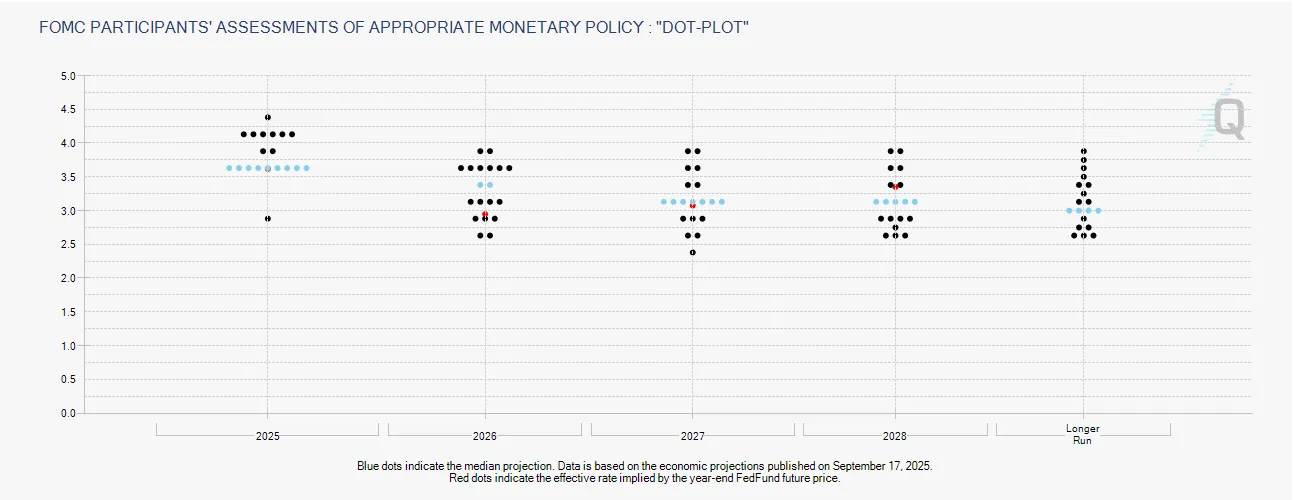

Forward Guidance and the Critical Dot Plot Disparity

Regarding the future of interest rates, the Federal Reserve is expected to signal that it is ready to make another cut in December, a view largely shared by the market with a 94% chance priced in for another 25 basis point reduction.

However, the biggest source of risk for the financial markets lies in the major disagreement over 2026. The Fed's own long-term projections (known as the Dot Plot) suggest a cautious approach with only 50 basis points of total cuts planned for all of 2026.

Source: CME FedWatch Tool

In stark contrast, market traders are expecting a much more aggressive response, pricing in at least 75 basis points of cuts, with some even anticipating as much as 125 basis points of easing by the end of 2026, which would drop the main interest rate down to 3%. This large gap shows that the market believes the Fed is moving too slowly to prevent a major collapse in the job market.

If Fed Chair Powell confirms the cautious 50 basis point path, markets that are currently counting on aggressive support will likely experience an immediate sell-off due to disappointment with the policy outlook.

Key Focus Areas and Macroeconomic Vulnerabilities

The biggest problem facing the Fed right now is the government shutdown, which is now in its 24th day. Because of the shutdown, they are missing crucial economic information, like the important September jobs report. This lack of official data has created a "data blind spot," forcing the Fed to rely on bits of information from private companies instead.

As a result, the Fed is not likely to change its overall economic view much; it will probably just repeat its concern that the "risk of job losses has increased."

Fed Chair Powell is expected to give a careful warning, emphasizing that the current economic growth is dangerously dependent on only three narrow things: wealthy consumers, a big wave of investment in AI, and rising stock/housing prices. This shaky foundation makes the economy very vulnerable, increasing the potential for a rapid boom or a quick, painful collapse.

Separately, regarding money management, the Fed is expected to announce a change in how it reinvests money from its assets, shifting toward buying shorter-term government bonds. This is meant to formally end its previous balance sheet reduction program (Quantitative Tightening or QT), balance its investments better, and help stabilize the short-term lending markets.

Potential Implications for the US Dollar

The immediate movement of the US Dollar will depend entirely on the relative hawkishness of Chair Powell's commentary compared to the market's aggressive easing expectations. The balance of risks is slightly tilted toward short-term USD upside.

If Powell stresses the elevated uncertainty, acknowledges the "healthy divergence of opinions" within the Committee, or emphasizes caution regarding inflation and the “no risk-free path for policy,” the resulting perceived policy resistance relative to market pricing could temporarily strengthen the greenback.

However, any FOMC-day USD rally is not expected to be long-lasting. The fundamental driver, the necessity for easing due to underlying labor market weakness is confirmed. Once the delayed official US data schedule resumes and validates the economic slowdown, renewed dollar softness is anticipated, continuing the longer-term depreciation trend.

Consequently, market participants should view any sharp, immediate dollar strength as a short-term mispricing of expectations, creating a potential selling opportunity against major pairs.

US Dollar Index (DXY) Daily Chart, October 29, 2025

Source: TradingView.com (click to enlarge)