Sample Category Title

Trade War to Keep USD Bid for Now

Note this month's FX Forecast Update is in shortened form

Majors. The trade war has returned as a key USD driver and, in our view, further escalation, which remains our base case, will tend to be USD supportive due to the less open US economy, which is set to lose less than those of its peers on a decrease in global trade. This said, recent Fed worries should keep a lid on USD strength but will also tend to make, notably, the ECB reluctant to commit to a tightening cycle.

EUR/NOK. At the June monetary policy meeting, Norges Bank confirmed market expectations of a September rate hike, which, in our view, marks an important fundamental trigger for the next move lower in EUR/NOK. In the very near term, the global environment of weaker growth and trade war fears alongside improved structural NOK liquidity and 'summer trading' should limit the short-term potential. We 'roll' our forecast profile to 9.40 in 1M (unchanged), 9.20 in 3M (9.30), 9.20 in 6M (9.30) and 9.10 in 12M (9.20).

EUR/SEK. We look for a wider range in EUR/SEK over the summer, which we addressed in a sold strangle recommendation (see Reading the Markets Sweden, 25 May). While we did argue for a temporary dip in EUR/SEK as inflation appeared set to meet and even breach the Riksbank's expectations for a couple of months yet, this is not the case anymore. After the Riksbank raised its CPIF forecast in July, it effectively opened the door for inflation disappointments instead. We still think the Riksbank will postpone the first hike beyond 2018 and that this will weigh on the SEK later in H2. Hence, in a 3-6M perspective, the cross is primarily a buy on dips in our view. Apart from monetary policy, the slowing housing market domestically and the trade war globally are two other headwinds for the SEK. Cheap valuation fundamentally could be seen as a SEK-buying argument though for those with a longer term horizon. On balance, we set our 1M and 3M forecasts at 10.40 (previously 10.20), 6M to 10.50 (previously 10.40) and leave our 12M forecast at 10.20.

EUR/DKK. DKK is relatively more exposed to an escalation of the global trade as the Danish economy is small and very open and has significant exposure to global shipping. Furthermore, Denmark has net exposure to the stock market due to in particular the Danish Life and Pension (L&P) sector's large holdings of US and euro-area stocks. This, in addition to the easier DKK liquidity situation, can help explain the recent rise in EUR/DKK above the 7.4500 level. In turn, we revise our EUR/DKK forecasts and now expect the pair to trade around 7.4525 in 1-6M buoyed by the factors above, before falling back to 7.4475 in 12M, as DKK remains well supported by strong fundamentals.

EUR/USD. We have made only minor changes to our forecast profile as we continue to see the negatives (trade war, carry appeal of USD, ECB on hold, Italy risks) dominating the longer term EUR positive impulses stemming from valuation and a turn in capital flows. Specifically, we expect EUR/USD to trade broadly within the 1.15-1.21 range over the next 6M period. However, our medium-term story remains unchanged: we believe the capital outflows of recent years will fade as we move closer to the first ECB hike. Alongside valuation, this is set to support EUR/USD in 6-12M. We see EUR/USD at 1.16 in 1M, 1.16 in 3M (previously 1.17), 1.20 in 6M (unchanged) and 1.25 in 12M (unchanged).

EUR/GBP. GBP has been in the hands of the Brexit-deal driven UK cabinet turmoil lately. For GBP, the rising risk of both a soft Brexit (GBP positive) and a 'no-deal' Brexit (GBP negative). We still expect the Bank of England to hike the Bank rate by 25bp to 0.75% in August. This is not fully priced in the market yet (put at 75% probability), so we expect relative interest rates to drive EUR/GBP slightly lower to 0.87 in 1M (previously 0.88). Longer term, we still expect EUR/GBP eventually to trade lower driven by Brexit clarifications and fundamental valuations. We continue to target EUR/GBP at 0.8650 in 3M, 0.84 in 6M and 0.83 in 12M.

USD/JPY. JPY weakness has materialised against USD and EUR despite rising trade concerns of late as the latter seems to currently affect the FX market mainly via economic (USD positive, JPY negative via its China exposure) rather than risk (JPY positive) channels. The recent level shift in USD/JPY has led us to revise higher our 1-3M forecasts to 112 in 1-3M (previously 110). That said, we stress that disregarding trade tensions, there are downside risks due to the lingering political uncertainty in Japan ahead of the Liberal Democratic Party's (LDP) leadership election in September. Longer term, we expect USD/JPY to remain underpinned by Fed-Bank of Japan divergence and a continued move higher in US yields and now target USD/JPY at 114 in 6-12M (previously 112).

EUR/CHF. The SNB kept its dovish tone at the June meeting and maintained that the franc is 'highly valued' and kept the option of FX intervention open. While the SNB has clearly been challenged (again) by the ECB's hesitant stance, the SNB should also have cemented its eagerness to see CHF weaker before making a shift on policy. With EUR strength set to return eventually, this makes us comfortable about maintaining a case for CHF depreciation in 6-12M but continued trade tensions is a downside EUR/CHF risk. We still look for 1.16 in 1M, 1.16 in 3M, 1.19 in 6M and 1.22 in 12M.

AUD, NZD, CAD. Trade war fears, weaker global growth and lower Chinese commodity demand all mark headwinds for the three commodity currencies. Meanwhile, Commodity Futures Trading Commission IMM positioning data already show that investors have turned very negative on the three, leaving an asymmetric balance of risk to positive news ahead. While the Bank of Canada looks set to hike rates an additional two times over the coming year, recent central bank communication, alongside weaker Chinese growth, has challenged our call of one 25bp rate hike from both the Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ). For now, we stick to our call but highlight risks are skewed towards unchanged policy rates in Australia and New Zealand over the next 12M. Fundamentally, CAD seems undervalued whereas AUD and NZD seem closer to fair value (versus USD). We leave our forecast profiles unchanged for all three currencies.

Emerging markets. Emerging market currencies are set to remain challenged by the risk of an escalating trade war, lower commodity prices and a stronger USD near term and rising US rates and tighter US liquidity over the medium term. Notably, TRY has suffered driven by political developments but otherwise we see the risk of a contagious sell-off as limited, as the likelihood of significant further USD strength is small after all. With the ECB effectively on hold and wage-price pressure mounting in, notably, Eastern Europe, these currencies in particular should stay supported vis-à-vis the EUR near term.

EUR/CZK. Despite the June CNB hike, EUR/CZK continues to trade around 25.90 and we project the cross to continue to hover around current levels in the short term. In the medium term, we expect the CZK to return to its moderate strengthening path, as the Czech macroeconomic backdrop remains very favourable and the CNB is likely to deliver its next interest rate hike within the coming months. This said, we expect the depreciation pace to abate compared with 2017, as the Czech economy shifts into a lower gear and the ECB is also gradually moving towards policy normalisation. We leave our forecasts for EUR/CZK unchanged at 25.70 in 1M, 25.50 in 3M, 25.00 in 6M and 24.80 in 12M.

EUR/HUF. The CEE currencies are among the most exposed emerging market currencies to escalating trade wars globally, with the HUF remaining the most exposed of the CEE currencies. While we believe that a stronger EUR and more hawkish Hungarian central bank will help the HUF, escalating trade wars remain the major risk for the currency. Given the dominating uncertainty, we update our EUR/HUF forecasts as follows: 322 in 1M (previously 315), 319 in 3M (previously 311), 315 in 6M (previously 308) and 310 in 12M (previously 305).

USD/RUB. The rouble continues its journey detached from the crude price, driven mostly by the global emerging market sentiment on the trade war and geopolitical cautiousness; notably, Russia's Ministry of Finance is set to continue limiting the RUB's extra strengthening on oil price swings. Still, a lower oil price would be RUB negative. The revived hawkishness of the Bank of Russia is helping the RUB among other emerging markets. Given the current escalation of global trade wars, we see the USD/RUB pair staying higher from our previous forecasts but lower still over the forecast horizon: 61.70 in 1M (previously 61.50), 60.90 in 3M (previously 60.10), 59.00 in 6M (previously 58.30) and 57.50 in 12M (previously 55.70).

USD/TRY. The Turkish lira has entered another perfect storm, as shaky macro fundamentals are eroded by the high oil price, weak emerging market sentiment and the returning personal grip of President Recep Erdoğan on the economic processes, TRY and monetary policy. The markets continue to dislike this kind of interference, now pricing extremely high TRY hedging. We expect the TRY sell-off to calm down, if the President announces a fiscal austerity programme and signals more central bank independency. We expect the USD/TRY to slide down slightly from the current levels in the near term, updating the forecast as following: 4.70 in 1M (previously 4.40), 4.80 in 3M (previously 4.45), 4.90 in 6M (previously 4.35) and 5.10 in 12M (previously 4.50).

USD/CNY. Mounting trade tensions between the US and China have put downward pressure on the CNY and the risk of continued CNY weakness remains. China is more vulnerable than the US in the short term, as its economy is already weakening and China is more dependent on exports, while the US enjoys fiscal support and is a more closed economy. We expect pressure on the Chinese economy to lead to further easing by the People's Bank of China and emphasise the risk of outflows also picking up, supporting the case for a weaker CNY. In FX Strategy – Downward revision to our CNY outlook (26 June), we revised our USD/CNY and EUR/CNY forecasts higher to target USD/CNY at 6.70 in 12M and EUR/CNY at 8.38 in 12M. While we maintain these here, we stress that risks remain skewed towards a significantly weaker CNY than incorporated in our forecasts.

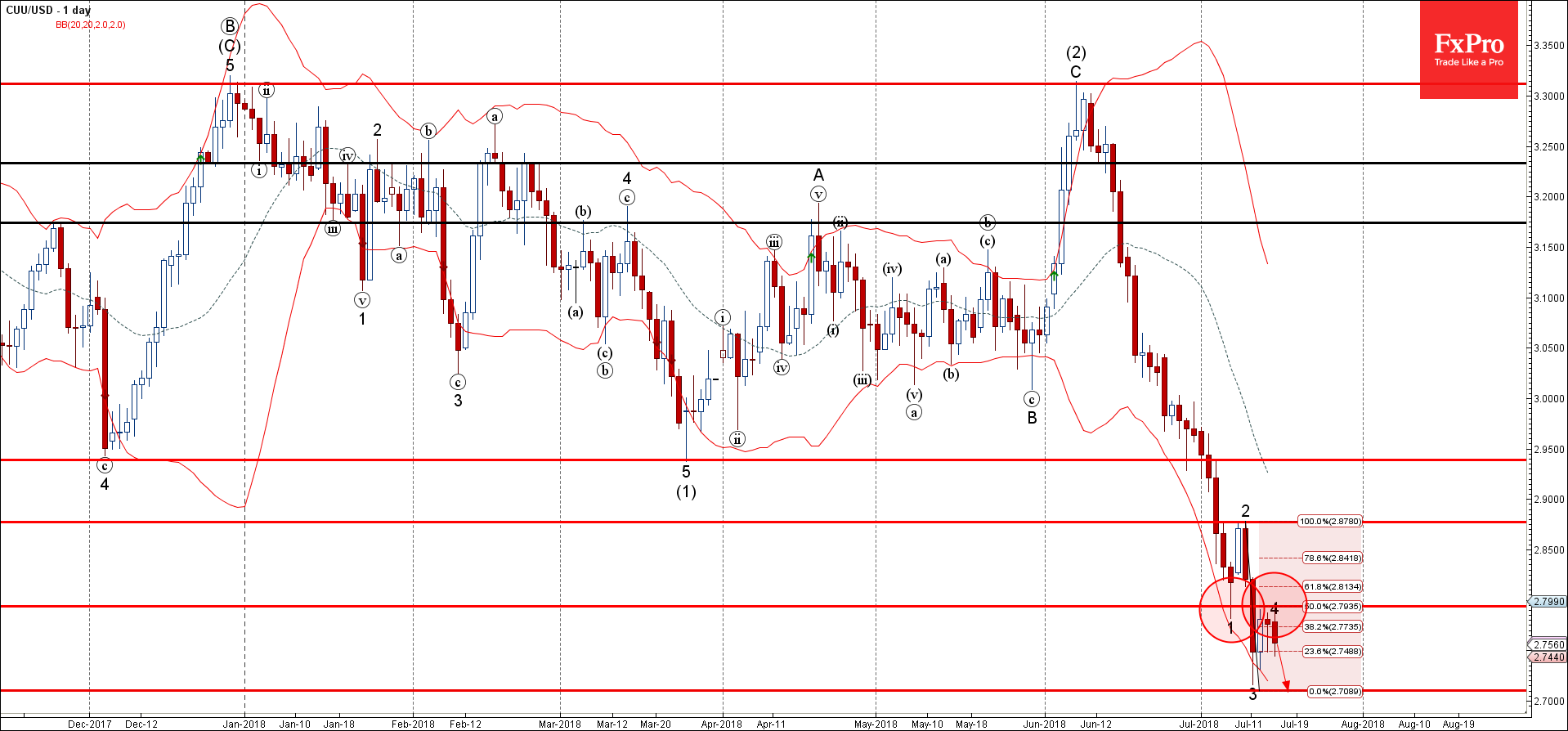

Forex Analysis: Copper

Copper reversed from resistance zone

Likely to fall further

Copper today reversed down from the resistance area located between the pivotal resistance level 2.7940 (former strong support from the start of July) and the 50% Fibonacci correction of the previous downward impulse 3.

The downward reversal from this resistance zone started the active minor impulse wave 5 – which belongs to wave (3) from June.

Copper is likely to fall further and re-test the next strong support level 2.710 (low of the previous minor impulse wave 3).

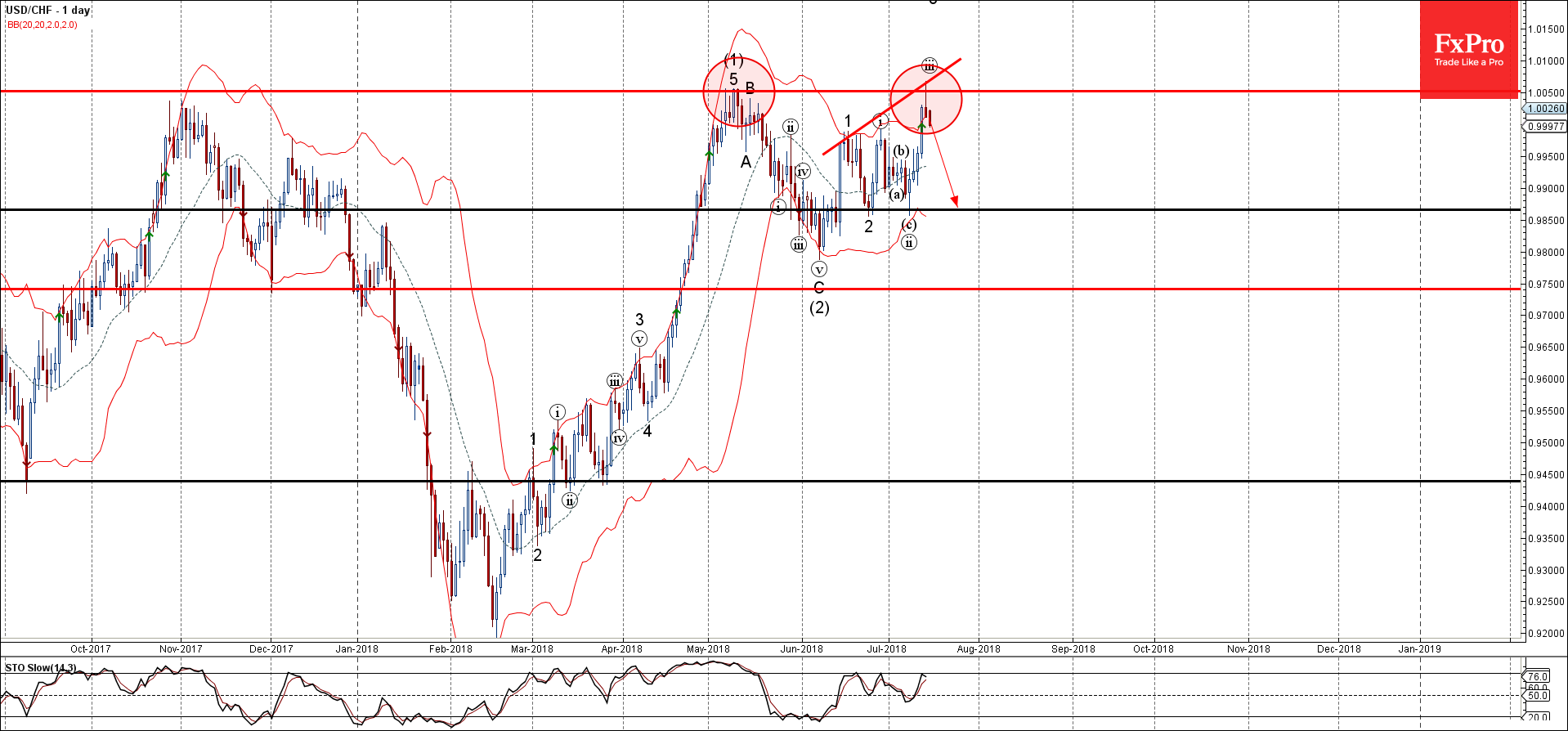

Forex Analysis: USDCHF

USDCHF reversed from resistance zone

Likely to fall further

USDCHF recently reversed down sharply from the resistance zone lying between the key resistance level 1.0050 (which stopped the sharp uptrend in May) and the upper daily Bollinger Band.

The downward reversal from this resistance zone created the daily Japanese candlesticks reversal pattern Shooting Star.

With the clear bearish divergence on the daily RSI indicator – USDCHF is likely to fall further and re-test the next support level 0.9870 (low for waves 2 and (ii).

EUR/USD – Euro Gains Ground Despite Soft Eurozone Surplus

EUR/USD has posted gains in the Monday session. Currently, the pair is trading at 1.1707, up 0.18% on the day. In economic news, the eurozone trade surplus slipped to EUR 16.9 billion, short of the estimate of EUR 17.6 billion. This marked the lowest surplus since January 2017. In the U.S, the focus is on consumer spending reports, with both retail sales and core retail sales expected to drop to 0.4%. On the manufacturing front, Empire State Manufacturing Index is forecast to drop to 20.3 points. On Tuesday, Federal Reserve Chair will testify before the Senate Banking Committee.

The U.S economy continues to perform well in 2018, and received a vote of confidence from the head of the Federal Reserve. On Thursday, Powell said that the economy is “in a really good place”, pointing to President Trump’s massive tax cut scheme and increased spending as key factors in boosting economic growth. Powell did not address monetary policy and said he was uncertain as to the effects of the current trade disputes which has embroiled the U.S and its trading partners. The Fed will likely press the rate trigger in the second half of the year, but it is an open question as to whether we’ll see one hike over the next six months. The Fed is projecting growth of 2.8% in 2018, compared to 2.3% in 2017. Powell will be in the spotlight next week when he appears for his semi-annual testimony before Congress.

Trade policy is not part of the Federal Reserve’s mandate, but Fed policymakers continue to voice concern about the escalating trade war between the U.S and its major trading partners, particularly China. On Friday, Dallas Fed President Robert Kaplan said he would have to downgrade his outlook if the tariff battle continues. Kaplan said that U.S tariffs on steel and aluminum imports had dampened capital expenditures plans and further trade tensions could lead to currency fluctuations and geopolitcal instability.

Stocks Drift Sideways Ahead Of Trump-Putin Summit In Helsinki

Notes/Observations

- Europe trades slightly higher, while Asia closed lower in quiet trading session

- Deutsche Bank shares soar over 8% on prelim results

- Markets await summit between Trump and Putin

Asia:

- China GDP and Retail Sales comes ahead of forecast, Industrial production misses

- New Zealand June Performance of Services index hits lowest level since Dec 2012

- Nikkei closed today for Marine Day

Europe:

- China and EU leaders have agreed to boost free trade - Joint statement

- UK government could accept amendments to customs bill - BBC report

- Tory MP Greening said to call for 2nd UK referendum

- In interview President Trump spoke of Europe as a Foe saying "I think the European Union is a foe, what they do to us in trade. Now you wouldn't think of the European Union, but they're a foe"

- PM May reveals Donald Trump suggested the UK sue the EU over Brexit

- Deutsche Bank report prelim Q2 above forecasts, shares rise sharply

Energy

- US considering tapping strategic Petroleum reserve to curb gasoline prices ahead of fall elections

Economic Data:

- (DK) Denmark Jun PPI M/M: 1.5% v 1.2% prior; Y/Y: 6.8% v 3.9% prior

- (IN) India Jun Wholesale Prices (WPI) Y/Y: 5.8% v 5.2%e

- (TR) Turkey Apr Unemployment Rate: 9.6% v 9.2%e

- (CH) SNB Total Sight Deposits for Week Ended July 13th

- (CHF): 576.1B v 576.0B prior

- (CZ) Czech May Current Account (CZK): -2.2B v -12.0Be

- (IT) Italy May Trade Balance: €3.4B v €2.9B prior; Trade Balance EU: €1.0B v €1.1B prior

- (TR) Turkey Jun Central Gov't Budget Balance (TRY): -25.6B v +2.7B prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +0.1% at 3,457, FTSE +0.8% at 7,648, DAX -0.2% at 12,549, CAC-40 -0.1% at 5,427; IBEX-35 +0.1% at 9,749, FTSE MIB +0.7% at 220.46, SMI flat at8,864 , S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European indices opened slightly higher and tracked largely sideways as the session wore on; periphery better performers; risk sentiment positive but not voracious; utilities and materials better performers; automotive sector underperforming, dragged by Peugeot; focus on upcoming Trump-Putin meeting later in the day and potential geopolitical concerns; Chile closed for holiday; upcoming earnings expected in the US session include Bank of America, Blackrock and JB Hunt

Equities

- Consumer discretionary: Debenhams DEB.UK -5.8% (credit insurers reduce cover for supplies), L'Oreal OR.FR -0.5% (analyst action), Lagardere MMB.FR +2.1% (analyst action)

- Consumer staples: Marine Harvest MHG.NO -2.6% (results)

- Financials: Deutsche Bank DBK.DE +5.5% (prelim Q2)

- Healthcare: Cellectis ALCLS.FR +7.5% (analyst action), Indivior INDV.UK 31.9% (prelim injuction on generic)

- Industrials: OCI OCI.NL +4.1% (analyst action), PSA UG.FR -0.7% (German Transport Min hearing on Opel emissions), VTG VT9.DE +14.5% (3rd party stake sale)

- Technology: Dialog Semiconductor DLG.DE -2.8% (outlook), Micro Focus MCRO.UK -4.7% (analyst action)

- Telecom: Megafon MFON.RU +6.6% (approves tender offer)

Speakers

- (IT) Italy EU Affairs Min Savona: proposes EU to be allowed to spend an extra €50B on public investments

- (US) President Trump tweets "Received many calls from leaders of NATO countries thanking me for helping to bring them together and to get them focused on financial obligations, both present & future. We had a truly great Summit that was inaccurately covered by much of the media. NATO is now strong & rich!"

Currencies

- Markets have been quiet in a subdued session with a lack of macro driving factors. Cable recovers from Friday lows as President Trump denied comments published in the press on Friday regarding trade with the UK, branding it as fake news. Cable trades at $1.3248, 10 pips off the session highs.

Fixed Income

- Bund Futures trade 18 ticks lower at 162.77 as the German Bund yield hovers above 0.30%. Upside targets 163.25 followed by 163.85, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.35 higher by 27 ticks as Trump's apologizes to PM May. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Monday's liquidity report showed Friday's excess liquidity fell from €1.871T to €1.867. Use of the marginal lending facility dropped from €135M to €134M.

- Corporate issuance saw high grade issuers price $13.6B debt last week

Looking Ahead

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (BR) Brazil May IBGE Services Sector Volume Y/Y: -4.0%e v 2.2% prior

- 08:00 (IS) Iceland Jun Unemployment Rate: No est v 2.2% prior

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Jun Import Price Index M/M: 0.1%e v 0.6% prior; Y/Y: 4.6%e v 4.3% prior, Export Price Index M/M: 0.2%e v 0.6% prior; Y/Y: No est v 4.9% prior, Import Price Index ex Petroleum M/M: 0.2%e v 0.1% prior

- 09:00 (CA) Canada Jun Existing Home Sales M/M: 1.5%e v -0.1% prior

- 10:00 (US) July Preliminary University of Michigan Confidence: 98.0e v 98.2 prior

- 11:00 (CO) Colombia May Industrial Production Y/Y: 4.9%e v 10.5% prior

- 11:00 (CO) Colombia May Retail Sales Y/Y: 5.0%e v 6.3% prior

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 14:00 (CO) Colombia Central Bank Jun Minutes

GBPUSD Further Bullish Above 1.3255 Level

The British Pound continues to advance higher against the greenback on Monday, as the U.S. Dollar comes under broad-based selling pressure. Sterling traders now await further news from the UK, as British Prime Minister Theresa May tries to pass her Brexit customs agreement through parliament today. GBPUSD buyers will now look for further gains above the 1.3255 level, while sellers will look to target below the 1.3205 level.

The GBPUSD pair is bullish while trading above the 1.3255 level, key technical resistance is found at the 1.3280 and 1.330 levels.

If the GBPUSD pair starts to decline below the 1.3235 level, sellers will likely target the 1.3205 and 1.3155 support levels.

USDJPY Still Intraday Bullish Above 112.20

The US dollar continues to hold well-above the 112.00 level against the Japanese yen currency on Monday, as traders await President Trump’s meeting with Russian President Vladimir Putin later today. The USDJPY pair retains an intraday bullish bias while trading above the 112.20 level, following the former weekly breakout above the 111.39 level. Buyers will continue to target the 113.00 level and beyond, while sellers will look to push price below the 112.20 support zone.

The USDJPY pair is intraday bullish while trading above the 112.20 level, key resistance remains at the 112.80 and 113.40 levels.

If the USDJPY pair falls below the 112.20 level, sellers will likely test towards the 111.90 and 111.39 support levels.

USD Loses Ground As Risk Sentiment Improves

EUR/CHF climbs back towards 1.20

After hitting 1.1368 at the beginning of the summer, EUR/CHF has been climbing its way back to 1.1696. However, the currency pair is still well below the multi-year high that was reached at the beginning of the second quarter. Indeed, the currency pair passed the 1.20 threshold before grinding towards 1.1368 amid the nomination of the new Italian government, mounting trade war fears and an unexpectedly dovish ECB.

The recovery in EUR/CHF is therefore exclusively due to the improvement in risk sentiment rather than the strengthening of the single currency. SNB kept a stiff upper lip and didn’t change a thing in its strategy. Total sight deposits held within the SNB have been quite stable since mid-2017, which suggest that the SNB didn’t intervened in the FX market; after all, EUR/CHF is well outside the danger zone.

The Swiss National Bank will maintain its wait-and-see approach and will let the ECB be the first mover. For now the market, is expecting Mario Draghi to start raising rates in mid-2019. With risk sentiment improving across the board, the recovery in EUR/CHF should continue. However, trade tensions between the US and its main trading partners remain of major concern for investors. A quick deterioration in market environment could ignite a CHF appreciation. We maintain our objective of 1.20 for the end of the summer.

Chinese growth slowing, currency stumbles

Chinese Q2 GDP rose 6.7% year-on-year, in line with market expectations. Seasonally adjusted quarter-on-quarter growth remains comfortable at 1.80%. However, the economy is showing some weakness: June fixed asset investment (6%; prior: 6.10%), industrial production (6%; prior: 6.80%) and retail sales (9%; prior: 8.50% but below 2-year average of 10.20%). Money supply is tightening, due to caution of financiers and debt risk, so the Chinese economy is expected to slowdown industrial activity and private consumption. Trade tariffs will be a key factor in coming months. Further CNY weakness is expected: now at 6.6845, USD/CNY is approaching the 6.675 in the short-term.

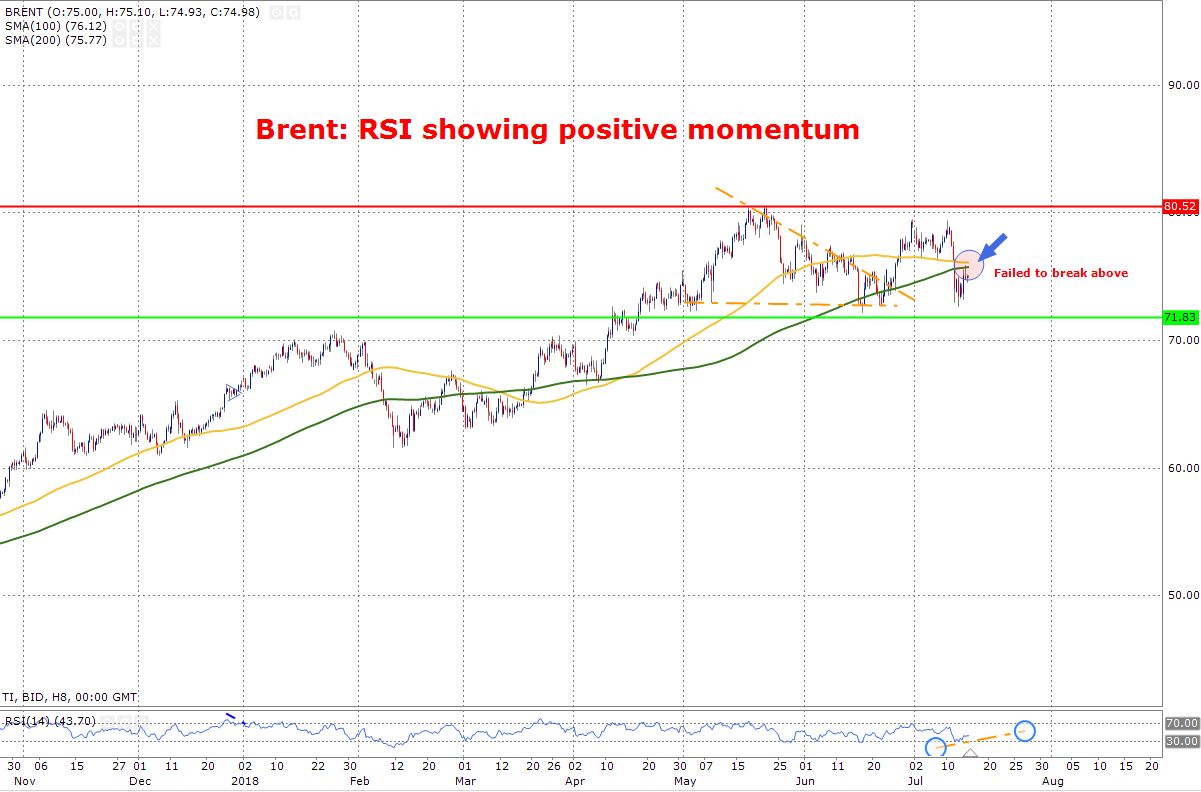

Oil: Trump Could Tap Into US Oil Emergency Reserves

Hedge funds have increased their bearish bets

Trump administration signalled that they may tab into emergency crude supplies in order to address the rising oil price. Crude oil has moved lower since the president made this announcement. Looking at the CFTC data, hedge funds have increased their bearish bets and one theme stands taller- confidence is wavering amidst investors. Money managers are more interested to take the profit off the table given the circumstances. There is a strong possibility that the market may remain choppy for some time now.

RSI is showing positive momentum, this is a bullish sign. The price needs to break above the 200-day SMA to confirm the uptrend.

Trump’s And Putin Meeting To Dictate Sentiment

- US's relationship with its European allies is already at all-time low

- The Chinese GDP q/y data came in at 6.7%

- FTSE 100 in a consolidation phase

US futures are trading mix to kick-start a new week. The key focus for investors is the US and Russia's meeting- the main event of the week. Last week at the NATO summit, there was a lot of drama, it kept the investors on the edge. A similar scenario is likely to play out this week as well. Russia and US meeting is important because US's relationship with its European allies is already at all-time low and if Trump and Putin's relation improves further, it would bring more friction between the US and the EU. If the situation does take this shape, the European markets and the US markets both can take a hit.

Moving away from this, traders are also under the influence of the feeble economic reading out of China. The Chinese GDP q/y data came in at 6.7% which was a little lower than the previous reading of 6.8%. Perhaps, the demons of the trade war have started their job. The slowing Chinese economy is not something which investors would appreciate at all.

As for the FTSE 100, we do not have any important economic data. Therefore, we are not expecting any data driven driven move. Brexit negotiations and any new headline on that would have the potential to move the markets. The overall price action has been very boring as the price is consolidating. Moreover, the FTSE 100 is struggling to find any direction as far as the moving averages goes.