Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3145; (P) 1.3193; (R1) 1.3284; More...

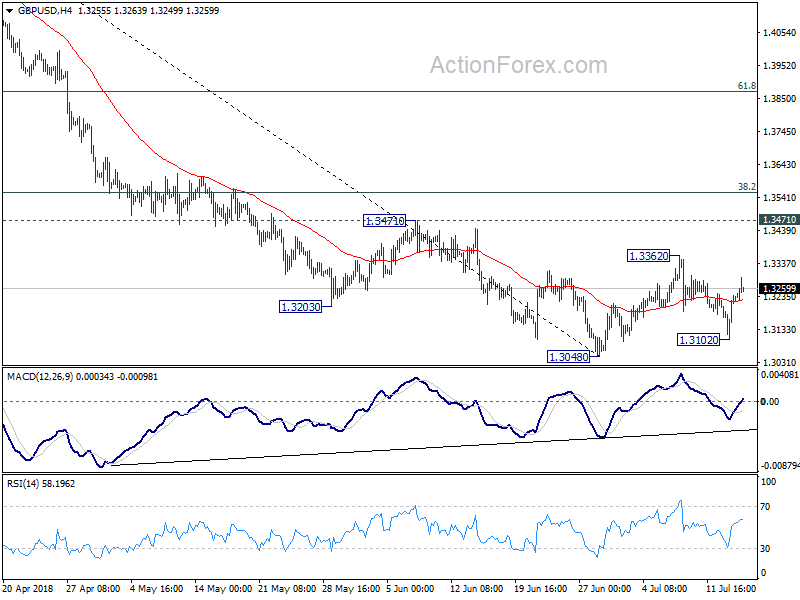

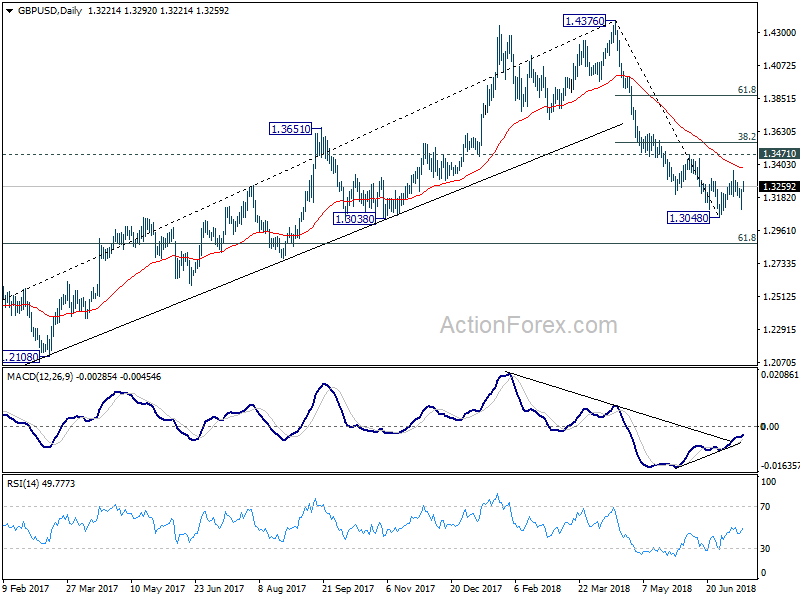

Intraday bias in GBP/USD remains mildly on the upside for 1.3362 resistance and possibly above. But price actions from 1.3048 are seen as a consolidation pattern. Hence, upside is expected to be limited by 1.3471 to bring larger decline resumption eventually. On the downside, break of 1.3048 will resume fall from 1.4376 for 1.2874 fibonacci level next.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 next. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. On the upside, sustained break of 38.2% retracement of 1.4376 to 1.3048 at 1.3555 is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.14; (P) 112.48; (R1) 112.69; More...

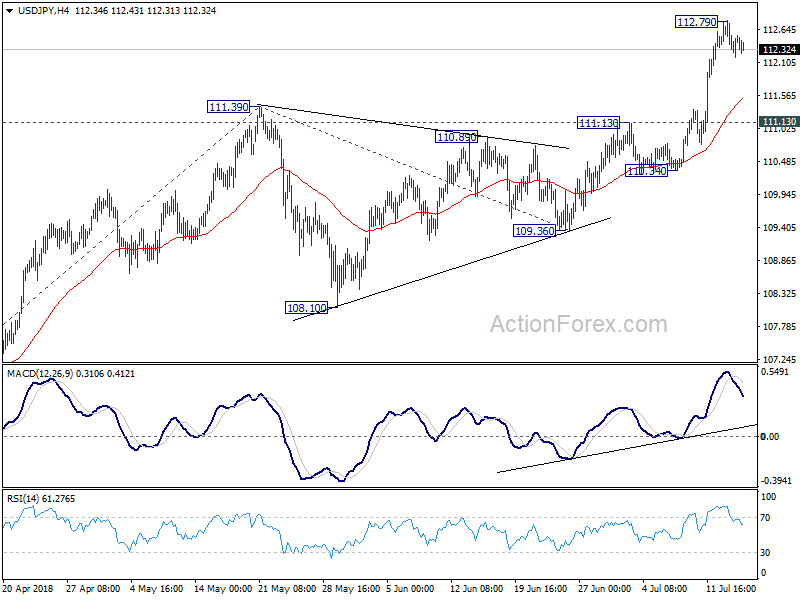

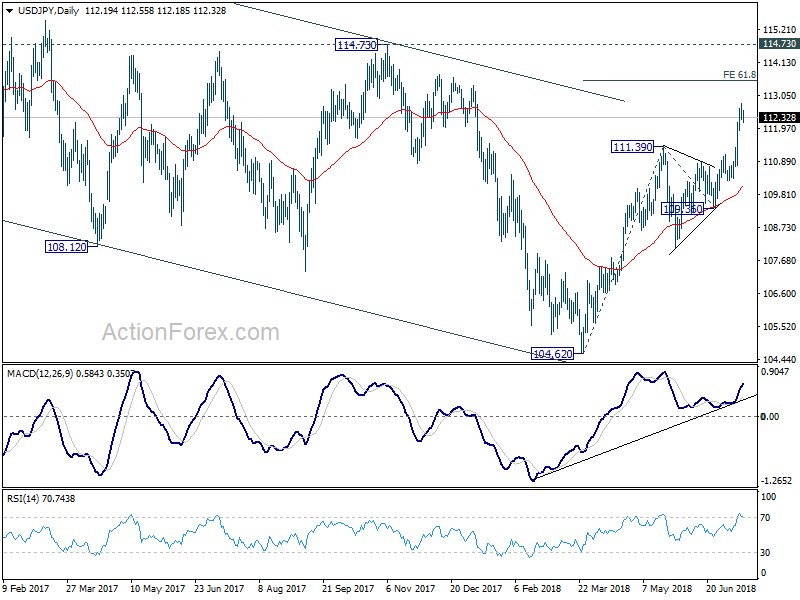

USD/JPY is staying in consolidation from 112.79 temporary top. Intraday bias remains neutral at this point. Deeper retreat could be seen. But downside should be contained well above 111.13 resistance turned support to bring rally resumption. Current development affirms the case of medium term reversal. Above 112.79 will target 61.8% projection of 104.62 to 111.39 from 109.36 at 113.54 first. Break will put focus on 114.73 key resistance for confirming our bullish view.

In the bigger picture, current development, with the solid break of medium term channel resistance from 118.65 (2016 high), affirm our view that corrective fall from there has completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will now be the preferred case as long as 119.36 support holds.

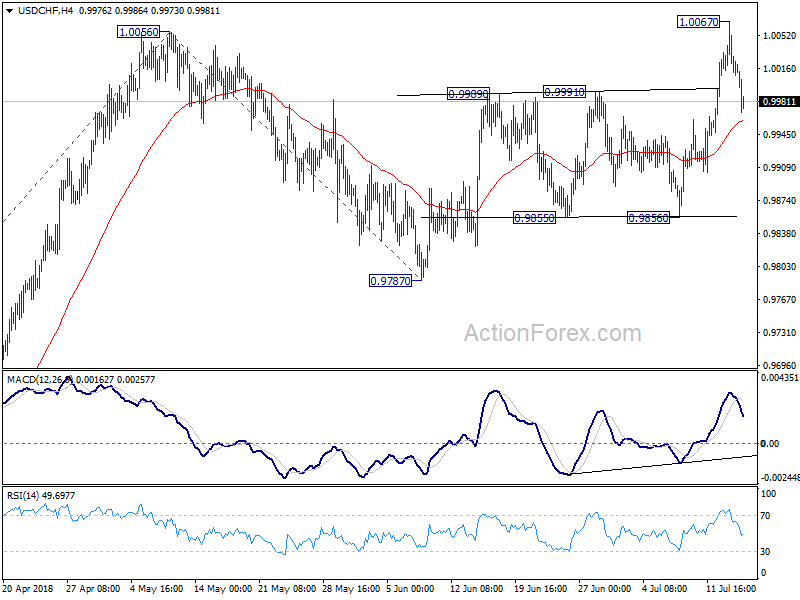

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9996; (P) 1.0033; (R1) 1.0053; More...

USD/CHF drops sharply to as low as 0.9968 so far today. Deeper fall could be seen as the pull back continues. But downside should be contained by 4 hour 55 EMA (now at 0.9960) to bring another rally. The rise from 0.9186 should have just resumed. Above 1.0067 will target 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. However, sustained break of the 4 hour 55 EMA will dampen this bullish view and turn focus back to 0.9858 support instead.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. After drawing support from 55 day EMA, it's now resuming for 1.0342 key resistance. For now, we'd still cautious on strong resistance from there to limit upside. Meanwhile, break of 0.9787 support is needed to signal completion of the rise. Otherwise, outlook will remain bullish even in case of deep pull back.

Euro Lifted as EU Made Progress With China, Dollar Soft after Retail Sales

Dollar remains generally weak in early US session despite a mild lift from retail sales data. While the greenback and Japanese yen are competing as the weakest one, Canadian Dollar joins the race as WTI crude oil drips below 70 handle. European majors are generally firm with Euro supported by the positive development in the high level summit between European Union and China in Beijing. Tusk and Juncker are travelling to Japan tomorrow and there would be some more positive news. On the other hand, while Trump is meeting Putin in Helsinki, expectations on the summit is rather low.

Oil price remains a key factor driving the Loonie. The impact of last week's hawkish BoC rate hike was more than offset by the steep fall in oil price. WTI crude oil hit as high as 75.27 earlier in the month but it's now back below 70. Oil price will possibly stay pressured as Trump administration is actively considering to tap into emergency supply of oil. Trump tried to "order" OPEC to do something to lower oil price but such intervention in the cartel was cold-shouldered. For now, USD/CAD is holding well above 1.3067 key support level, which maintains near term bullishness. Renewed selling in oil could send USD/CAD through 1.3216 minor resistance towards 1.3385.

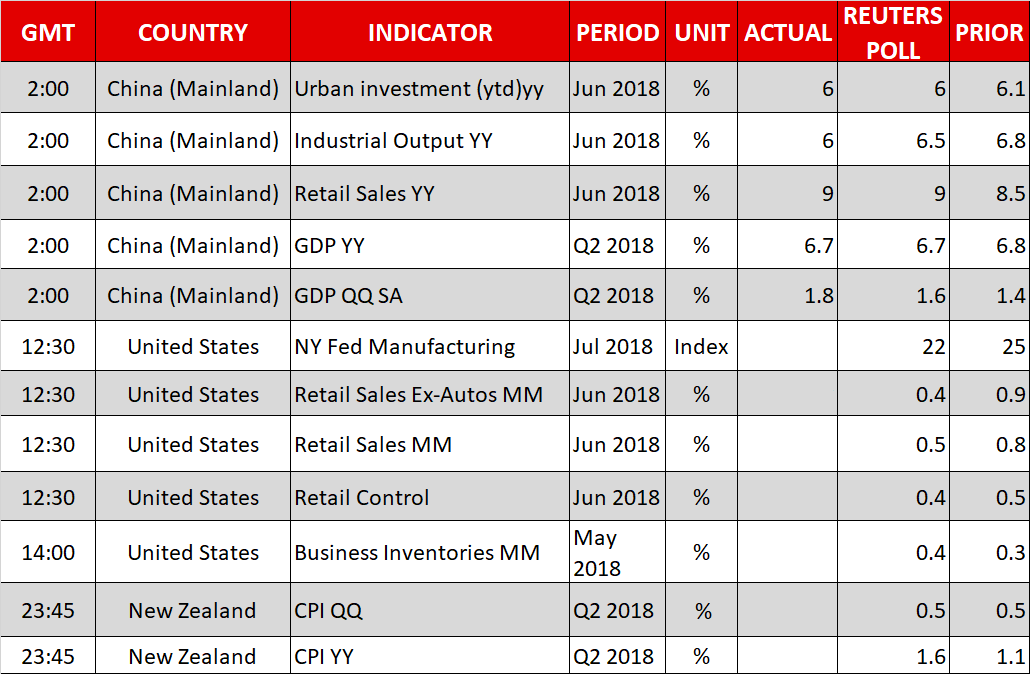

US headline retail sales rose 0.4% mom in June, above expectation of 0.4% mom. Prior month's figure was revised sharply higher from 0.8% mom to 1.3% mom. Ex-auto sales rose 0.4% mom, matched expectations. Prior month's figure was also revised sharply higher from 0.9% to 1.4%. Empire state manufacturing index, general business conditions, dropped to 22.6 in July, down from 25.0 but beat expectation of 20.3. Expectations six months ahead dropped -7.8 to 31.1.

From elsewhere, Canada international securities transactions dropped to CAD 2.18B in May. Eurozone trade surplus narrowed to EUR 16.9B in May, below expectation of EUR 17.6B. China GDP growth slowed to 6.7% yoy in Q2, down from 6.8% yoy and met expectation. Industrial production growth slowed to 6.0% yoy in June, down from 6.8% yoy and missed expectation of 6.5% yoy. Fixed assets investment growth slowed to 6.0% yoy, down from 6.1% yoy and missed expectation of 6.2% yoy. Retail sales offered a brighter spot as they grew 9.0% yoy, up from 8.5% yoy and matched expectations.

EU and China issued joint statement supporting WTO, against protectionism and committing to Iran deal

EU and China issued a joint statement reaffirming their "commitment to deepening their partnership for peace, growth, reform and civilisation, based on the principles of mutual respect, trust, equality and mutual benefit, by comprehensively implementing the EU-China 2020 Strategic Agenda for Cooperation". The statement is released after meeting of European Council President Donald Tusk, European Commission President Jean-Claude Juncker and Chinese Premier Li Keqiang in Beijing.

In the statement, it's noted that both sides are "strongly committed to fostering an open world economy, improving trade and investment liberalisation and facilitation, resisting protectionism and unilateralism". And, they "firmly supported the rules-based, transparent, non-discriminatory, open and inclusive multilateral trading system with the WTO as its core". At the same time, they pledged to work on reform of the WTO and "establish a joint working group on WTO reform, chaired at Vice-Ministerial level, to this end.".

The EU "took note of China's recent commitments to improving market access and the investment environment, strengthening intellectual property rights and expanding imports, and looks forward to their full implementation as well as further measures". Both sides pledged to ensure "a level playing field and mutually beneficial cooperation in bilateral trade and investment". "Ongoing Investment Agreement negotiations" are seen as a "top priority". And, they agreed to "accelerate the negotiation of the Agreement on the Cooperation on, and Protection of, Geographical Indications" and hoped to conclude it by next meeting on July 25-27.

Both sides also recalled that the Joint Comprehensive Plan of Action (JCPOA) Iran nuclear deal is a "key element of the global non-proliferation architecture and a significant diplomatic achievement endorsed unanimously by the UN Security Council in its Resolution 2231." And the "reaffirm their commitment to the continued, full and effective implementation of the JCPOA."

EU Juncker to China: Actions are more important than words

In the post meeting joint conference with Li , Jean-Claude Juncker expressed his concerns that European Foreign Direct Investment into China have hit a low in 2017, at only around EUR 6B. That's massive difference to Chinese investment in EU at EUR 30B. And Juncker pointed out "this gap reflects a concern amongst our investors on the regulatory and administrative burden that foreign companies sometimes have to face in China."

Nonetheless, Juncker hailed the "first exchange of offers" on the Comprehensive Agreement on Investment with China. He saw that as "an important step". That it's " only the first one" and "what we need is an Agreement that fulfils our common ambition and gives investors on both sides predictable and long-term access to our respective markets." Juncker emphasized to China that "actions are more important than words.

EU Tusk called for brave and responsible reform of rules-based orders, rather than trade wars

Tusk said in the same press conference that "the world we were building for decades" has brought about " peace for Europe, the development of China, and the end of the Cold War between the East and the West." He emphasized that it is "common duty of Europe and China, America and Russia, not to destroy this order, but to improve it." He urged "not to start trade wars, which turned into hot conflicts" but "to bravely and responsibly reform the rules-based international order."

He called on China, Trump and Putin to start the process from reform of the WTO as "there is still time to prevent conflict and chaos." He pointed to the "dilemma" of "whether to play a tough game such as tariff wars and conflicts in places like Ukraine and Syria, or to look for common solutions based on fair rules."

Tusk also reiterated that the EU is committed to "modernisation of the WTO" and "propose a comprehensive approach to improving, together with like-minded partners, the functioning of the WTO in crucial areas." And he called for "like-minded partners" to work together to "strengthen the WTO as an institution and to ensure a level playing field."

German Maas: Europe must not be divided by verbal attacks and absurd tweets

German Foreign Minister Heiko Maas warned that Europe can "no longer completely rely on the White House". And "to maintain our partnership with the USA we must readjust it". The first "clear consequence" is that Europe must "align ourselves even more closely". And he urged "Europe must not let itself be divided however sharp the verbal attacks and absurd the tweets may be."

Maas also warned Trump, as the latter is meeting Russian President Vladimir Putin in Helsinki, that "unilateral deals at the expense of one's own partners also harm the US in the end."

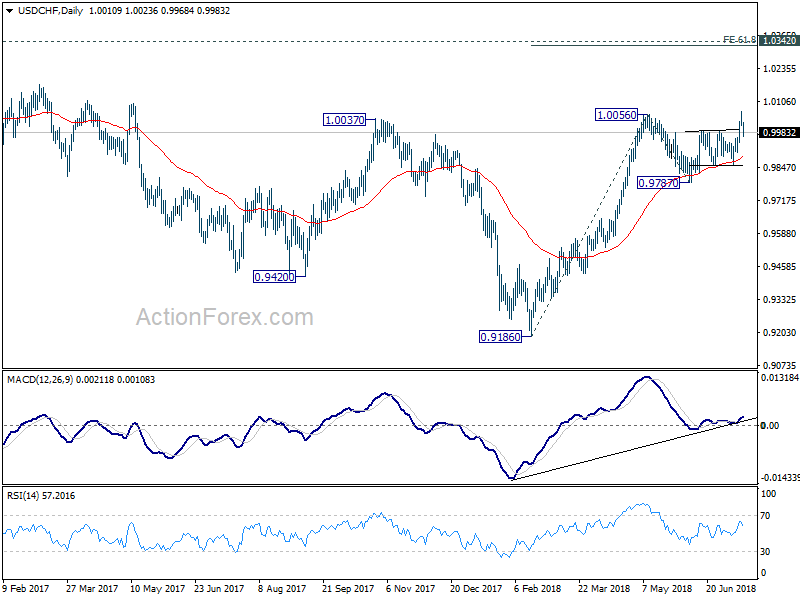

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9996; (P) 1.0033; (R1) 1.0053; More...

USD/CHF drops sharply to as low as 0.9968 so far today. Deeper fall could be seen as the pull back continues. But downside should be contained by 4 hour 55 EMA (now at 0.9960) to bring another rally. The rise from 0.9186 should have just resumed. Above 1.0067 will target 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. However, sustained break of the 4 hour 55 EMA will dampen this bullish view and turn focus back to 0.9858 support instead.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. After drawing support from 55 day EMA, it's now resuming for 1.0342 key resistance. For now, we'd still cautious on strong resistance from there to limit upside. Meanwhile, break of 0.9787 support is needed to signal completion of the rise. Otherwise, outlook will remain bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Jul | -0.10% | 0.40% | ||

| 02:00 | CNY | GDP Y/Y Q2 | 6.70% | 6.70% | 6.80% | |

| 02:00 | CNY | Retail Sales Y/Y Jun | 9.00% | 9.00% | 8.50% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 6.00% | 6.50% | 6.80% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Jun | 6.00% | 6.20% | 6.10% | |

| 02:00 | CNY | Unemployment rate June | 4.80% | 4.80% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | 16.9B | 17.6B | 18.1B | 18.0B |

| 12:30 | CAD | International Securities Transactions (CAD) May | 2.18B | 7.03B | 9.13B | 9.09B |

| 12:30 | USD | Retail Sales Advance M/M Jun | 0.50% | 0.40% | 0.80% | 1.30% |

| 12:30 | USD | Retail Sales Ex Auto M/M Jun | 0.40% | 0.40% | 0.90% | 1.40% |

| 12:30 | USD | Empire State Manufacturing Index Jul | 22.6 | 20.3 | 25 | |

| 14:00 | USD | Business Inventories May | 0.40% | 0.30% |

Canadian Dollar Subdued as U.S Retail Sales Within Expectations

The Canadian dollar is almost unchanged in the Monday session. Currently, USD/CAD is trading at 1.3145, down 0.07% on the day. On the release front, Canadian Foreign Securities Purchases dropped sharply to C$2.18 billion, well short of the estimate of C$7.03 billion. This marked a 5-month low. In the U.S core retail sales dropped to 0.4%, matching the estimate. Retail sales dropped to 0.5%, edging above 0.4%.

In the U.S, the focus is on consumer spending reports, with both retail sales and core retail sales expected to drop to 0.4%. On the manufacturing front, Empire State Manufacturing Index is forecast to drop to 20.3 points. On Tuesday, Federal Reserve Chair will testify before the Senate Banking Committee and Canada releases Manufacturing Sales.

The U.S economy is firing on all cylinders and received a vote of confidence from the head of the Federal Reserve. On Thursday, Powell said that the economy is “in a really good place”, pointing to President Trump’s massive tax cut scheme and increased spending as key factors in boosting economic growth. Powell did not address monetary policy and said he was uncertain as to the effects of the current trade disputes which has embroiled the U.S and its trading partners. The Fed will likely press the rate trigger in the second half of the year, but it is an open question as to whether we’ll see one hike over the next six months. The Fed is projecting growth of 2.8% in 2018, compared to 2.3% in 2017. Powell will be in the spotlight next week when he appears for his semi-annual testimony before Congress.

Trade policy is not part of the Federal Reserve’s mandate, but Fed policymakers continue to voice concern about the escalating trade war between the U.S and its major trading partners, particularly China. On Friday, Dallas Fed President Robert Kaplan said he would have to downgrade his outlook if the tariff battle continues. Kaplan said that U.S tariffs on steel and aluminum imports had dampened capital expenditures plans and further trade tensions could lead to currency fluctuations and geopolitcal instability.

Dollar Weakens ahead of US Retail Sales; Oil on the Backfoot

Here are the latest developments in global markets:

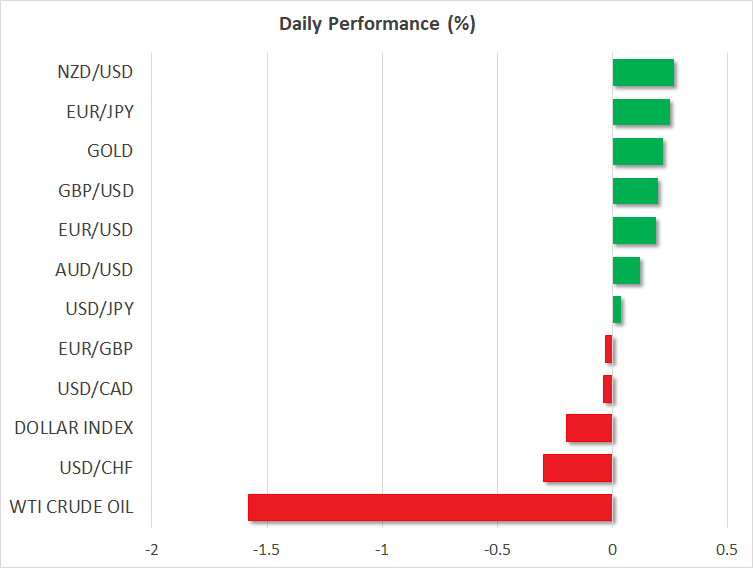

FOREX: The US dollar was trading below the 6-month high of 112.79 today against the Japanese yen, but managed to add some gains to its daily performance (+0.02%) ahead of the release of the US retail sales later in the day. The dollar index, which gauges the greenback’s strength versus six major currencies, moved lower by 0.24%. Pound/dollar rebounded sharply from near the 1.3101 barrier on Friday and drove the price even further to 1.3265 (+0.24%) on Monday. Meanwhile, euro/dollar climbed by 0.23%, surpassing the 1.1700 psychological level once again despite Italy’s Deputy Prime Minister calling the euro “an experiment that began badly”. However, he reiterated that Italy has no intentions to abandon the common currency. In the antipodean sphere, aussie/dollar gained 0.15% and aussie/yen jumped to 83.58 (+0.23%). Kiwi/dollar stood higher as well at 0.6781 (+0.27%). Dollar/loonie pulled back after meeting resistance near its 20-day simple moving average on Friday, and is 0.11% lower today.

STOCKS: European stocks were mixed at 1100 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.11% and 0.33% respectively, with telecommunications, energy, and utilities leading the losses. The German DAX 30 rose by 0.12%, while the French CAC 40 traded down by 0.21%. The Italian FTSE MIB jumped 0.10%, whereas the UK’s FTSE 100 tumbled by 0.72%. .US stock futures tracking the major indices were pointing to a negative open, while earnings season continues from Bank of America, BlackRock and Netflix’s on Monday.

COMMODITIES: Oil prices were falling on Monday as Saudi Arabia was said to offer extra crude supplies, while Libya’s oil-exporting facilities returned to operation. Meanwhile, comments by the Russian energy minister on Friday stating that Russia and other oil producers could raise supply by 1 million bpd or more in case supply shortages weigh on the market helped prices to move lower. After the aggressive sell-off on Wednesday which pushed West Texas Intermediate (WTI) crude oil below $70 per barrel, WTI was trading at $69.86/barrel (-1.65%). Also, London-based Brent plummeted by 2.03% today, crossing slightly below $74.00. Gold prices recovered some of Friday’s losses (+0.30%), but continue to hover just above their lows for the year.

Day ahead: US retail sales to drive the dollar; Trump-Putin summit in focus

Trade concerns might remain out of the spotlight on Monday as the focus will likely shift to the economic calendar and a crucial summit held between the US President and the Russian leader, Vladimir Putin in Helsinki. Brexit developments will also be on the radar as Brexiteers lawmakers are preparing to challenge the British Prime Minister in a vote on amendments to legislation on the government’s post-Brexit customs relationship with the EU.

At 1230 GMT, the Census Bureau is expected to say that US retail sales have risen by 0.5% month-on-month (m/m) in June, slower than in May when they grew by 0.8%. In the absence of automobiles, the core measure is also expected to ease, posting a growth of 0.4% compared to a 0.9% expansion in the preceding month. A stronger-than-expected outcome could raise the odds for two more rate hikes this year, giving a lift to the dollar. On the other hand, should the numbers disappoint, and in the absence of any trade or political news, the greenback could move lower. The New York Empire State Manufacturing Index for the month of July will come in light at the same time but forecasts point to a decline as well. Later in the day, US business inventories for May are projected to show a slight acceleration from the previous month (1400 GMT).

In other data releases, inflation readings for the second quarter will be of importance in New Zealand during the Asian trading session (2245 GMT), with analysts predicting that consumer prices have gone up by 1.6% y/y, while on a quarterly basis they believe that the CPI has remained unchanged at 0.5%. Within the Reserve Bank of New Zealand, a rate cut is still a possibility as policymakers weigh low inflationary pressures – CPI below the RBNZ’s midpoint price target of 2.0% – and trade uncertainties. Hence a potential miss in the data would likely persuade policymakers to take that scenario more seriously, pushing the kiwi lower.

Meanwhile in Australia, traders will be waiting for the Reserve Bank of Australia’s (RBA) meeting minutes on Tuesday at 0130 GMT to identify any further details pertaining to the central bank’s decision to leave rates steady on July 3. Not a lot is expected in terms of fresh policy signals, with policymakers likely to highlight the US-China trade tensions, subdued wages, and high household debt levels. Nevertheless, the aussie could experience some upside in case the RBA uses a more positive tone on the country’s outlook. Note that markets price a rate hike coming only in the late 2019.

In the UK, the Brexit plan will head to the Parliament, where lawmakers are scheduled to vote on amendments to the legislation on the government’s post-Brexit customs relationship with the EU. While, the British Prime Minister, Theresa May, is not expected to be defeated, Brexiteers could use a louder voice to demand stricter rules on the exit plan, where a higher number of votes against May’s strategy could bring another political headache and a potential sell-off to the pound. Recall that the UK’ Brexit negotiator, David Davis, and the foreign minister, Boris Johnson, resigned a week ago as both officials said May’s proposals were likely to keep the UK too close to the EU.

As for today’s special meetings, all eyes will turn to Helsinki as the US President, Donald Trump will finalize his European tour – which passed with controversies so far – by meeting the Russian President, Vladimir Putin. After criticizing his NATO allies over their defensive spending in Brussels and the Brexit plan in London last week, Trump is anticipated to discuss Syria, Ukraine, Iran’s nuclear program, and Russia’s meddling in the 2016 US elections at his first summit with Putin, although they have already met in on the sidelines of multilateral talks. Yet his comments to the CBS Evening News showed that he has low expectations of what the summit could bring out, though he added that “nothing bad is going to come out of it, and maybe some good will come out.”

In equities, Bank of America and BlackRock will be reporting quarterly earnings before the US markets open, with Netflix’s respective report hitting the markets after the closing bell on Wall Street.

US retail sales rose 0.5%, ex-auto sales rose 0.4%. Sharp upside revision in May figures

The batch of economic data from the US is mixed. Dollar recovers slightly but remains in red for today in general.

Headline retail sales rose 0.5% mom in June, above expectation of 0.4% mom. Prior month's figure was revised sharply higher from 0.8% mom to 1.3% mom.

Ex-auto sales rose 0.4% mom, matched expectations. Prior month's figure was also revised sharply higher from 0.9% to 1.4%.

Empire state manufacturing index, general business conditions, dropped to 22.6 in July, down from 25.0 but beat expectation of 20.3. Expectations six months ahead dropped -7.8 to 31.1.

Looking at the details of current indicators:

- New orders dropped -3.1 to 18.2.

- Shipments dropped -8.9 to 14.6.

- Unfilled orders dropped -9.3 to 0.0.

- Delivery time dropped -7.2 to 6.0.

- Inventories dropped -9.7 to -4.3.

- Price paid dropped -10 to 42.7.

- Price received dropped -1 to 22.2.

- Number of employees dropped -1.8 to 17.2.

- Average employee workweek dropped -6.4 to 5.6.

Into US session: Dollar weakens further as Trump meets Putin

Entering US session, European majors are generally strong today, led by Swiss Franc, followed by Sterling. On the other hand, both Yen and Dollar are extending last week's selloff. The financial markets are generally quiet though.

After some weaker than expected economic data, China SSE closed down -0.61% at 2814.04, holding safely above 2800. Hong Kong HSI was up 0.05%, Singapore Strait Times ended lower by -0.85%. Nikkei is on holiday.

Major European indices are also trading lower. FTSE is losing -1.02% at the time of writing, DAX is down -0.15%, CAC is down -0.40%.

Trump is meeting Putin in Helsinki now but we're no expecting anything ground-breaking there. EU Tusk and Juncker, though, seemed to have done something positive with China earlier today. And they'll travel to Japan tomorrow.

For the session ahead US retail sales is a major focus. Headline sales is expected to rise 0.4% mom in June, with ex-auto sales up 0.4%. Empire State Manufacturing index is expected to drop from 25 to 20.3 in July. Business inventories are expected to rise 0.4% in May. Canada will release International Securities Transactions.

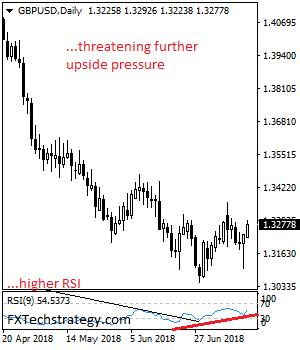

GBPUSD – Bullish, Looks To Correct Further Higher

GBPUSD - The pair faces further upside pressure following its higher close on Friday and during early trading today. Support lies at the 1.3250 level where a break will turn attention to the 1.3200 level. Further down, support lies at the 1.3150 level. Below here will set the stage for more weakness towards the 1.3100 level. Conversely, resistance stands at the 1.3300 levels with a turn above here allowing more strength to build up towards the 1.3350 level. Further out, resistance resides at the 1.3400 level followed by the 1.3450 level. On the whole, GBPUSD remains biased to upside on correction.

DAX Ticks Lower As Investors Look For Cues

The DAX index has ticked lower in the Monday session. Currently, the DAX is at 12,521, down 0.12% on the day. On the release front, there are no major German or eurozone events. In economic news, the eurozone trade surplus slipped to EUR 16.9 billion, short of the estimate of EUR 17.6 billion. This marked the lowest surplus since January 2017.

European equity markets showed little change last week and the DAX continues to trade quietly on Monday. Still, the trading tensions hovering in the air have many investors wondering if this is the calm before the storm. On Tuesday, the Trump administration said it was considering imposing tariffs on some $200 billion in Chinese goods, which would be a significant escalation in the trade war between the two economic giants. China has promised to respond with “firm and forceful measures”, but hasn’t provided any details. With neither side showing any flexibility, the markets could be heading for stormy waters if China retaliates.

Trade policy is not part of the Federal Reserve’s mandate, but Fed policymakers continue to voice concern about the escalating trade war between the U.S and its major trading partners, particularly China. On Friday, Dallas Fed President Robert Kaplan said he would have to downgrade his outlook if the tariff battle continues. Kaplan said that U.S tariffs on steel and aluminum imports had dampened capital expenditures plans and further trade tensions could lead to currency fluctuations and geopolitical instability.