Sample Category Title

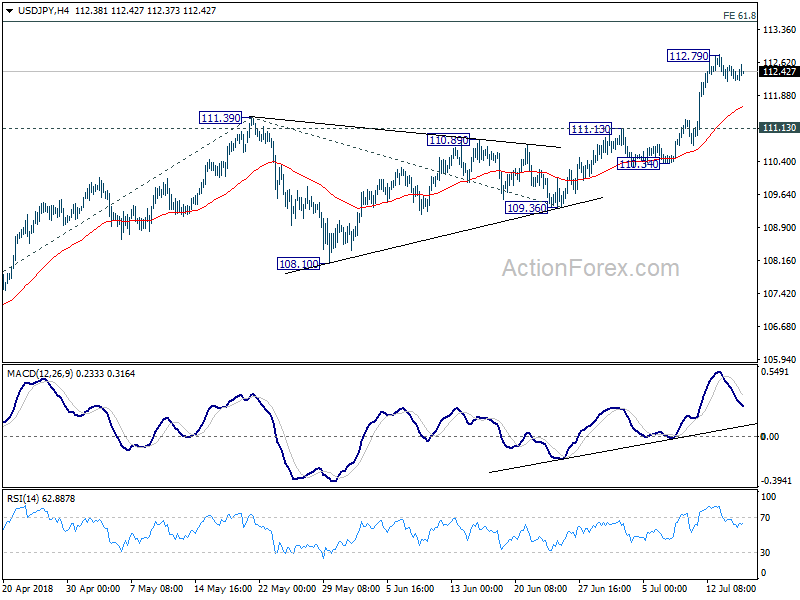

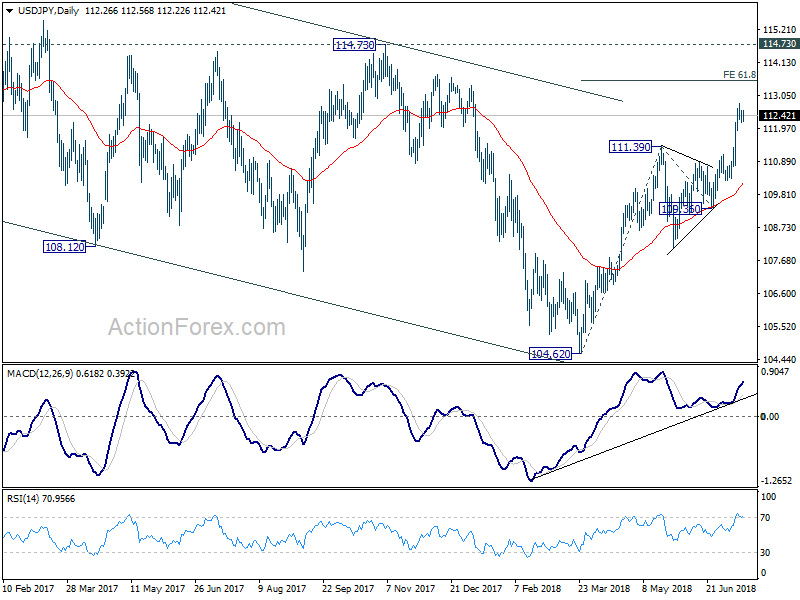

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.15; (P) 112.35; (R1) 112.49; More...

Intraday bias in USD/JPY stays neutral as consolidation from 112.79 temporary top is in progress. Deeper retreat could be seen. But downside should be contained well above 111.13 resistance turned support to bring rally resumption. Current development affirms the case of medium term reversal. Above 112.79 will target 61.8% projection of 104.62 to 111.39 from 109.36 at 113.54 first. Break will put focus on 114.73 key resistance for confirming our bullish view.

In the bigger picture, current development, with the solid break of medium term channel resistance from 118.65 (2016 high), affirm our view that corrective fall from there has completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will now be the preferred case as long as 119.36 support holds.

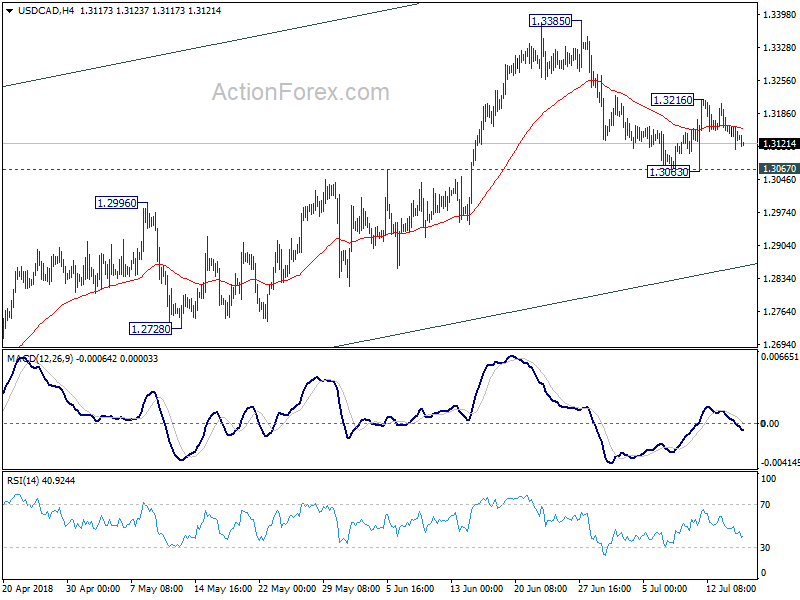

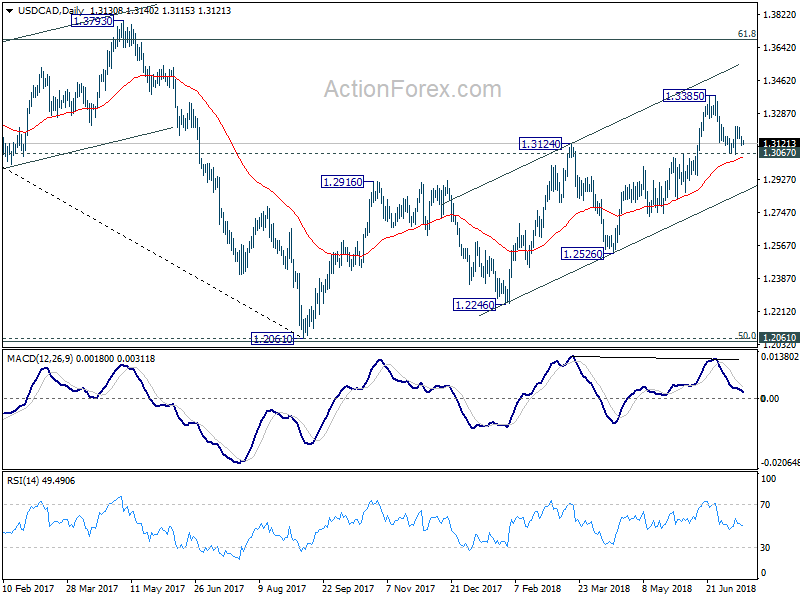

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3106; (P) 1.3141; (R1) 1.3171; More...

USD/CAD is bounded in tight range of 1.3063/3216 and intraday bias remains neutral. Outlook is unchanged and we're preferring the case that pull back from 1.3385 has completed at 1.3063 already. Above 1.3216 will bring retest of 1.3385 first. Break will resume whole rally from 1.2061 for 1.3685 fibonacci level. However, firm break of 1.3067 resistance turned support will bring deeper fall to channel support (now at 1.2858).

In the bigger picture, as long as channel support (now at 1.2858) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

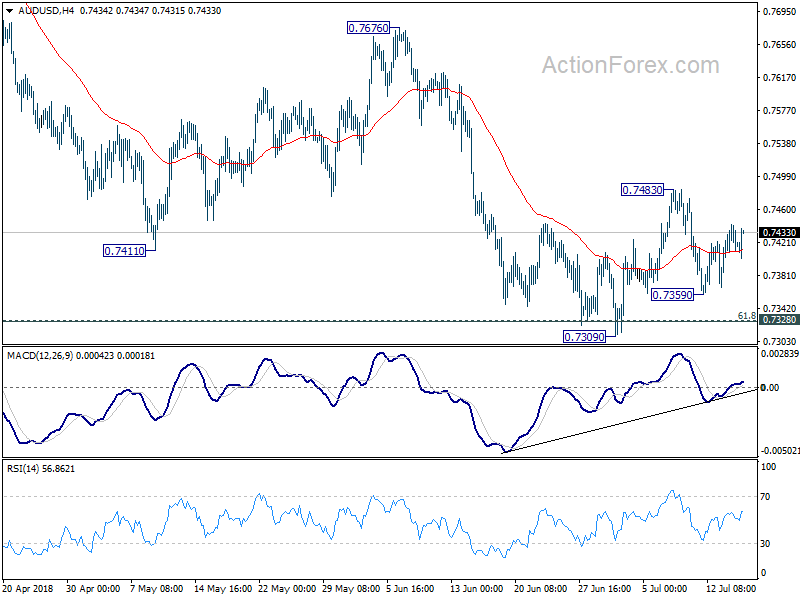

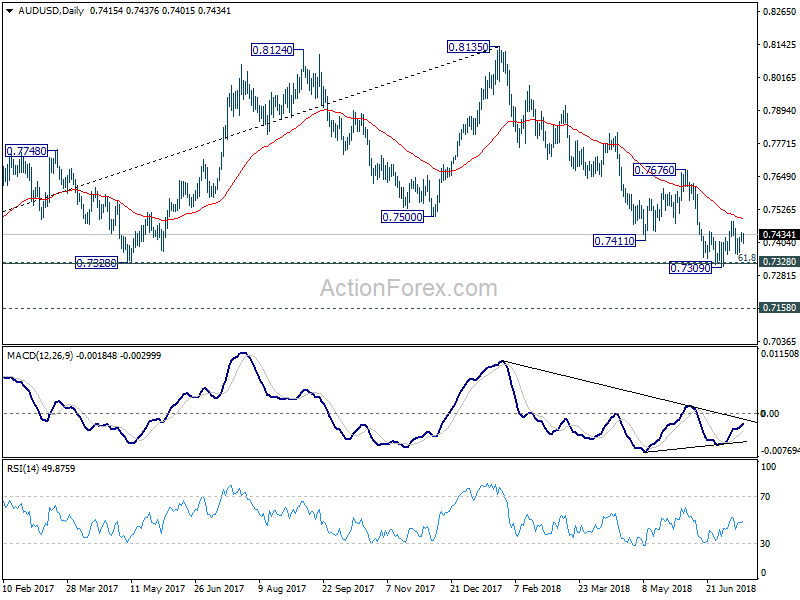

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7406; (P) 0.7424; (R1) 0.7440; More...

AUD/USD strengthens mildly today but stays in range of 0.7359/7483. Intraday bias remains neutral first. Outlook is unchanged that consolidation from 0.7309 could extend further and stronger recovery cannot be ruled out. But after all, upside should be limited below 0.7676 resistance to bring larger fall resumption. On the downside, below 0.7359 will target 0.7309 support first. Sustained trading below 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

New Zealand Dollar Jumps on RBNZ Inflation Reading, Australian Dollar Higher on RBA Minutes

Commodity currencies trade generally higher today. New Zealand Dollar leads the way following improvement in RBNZ's own preferred core inflation measures. Australian Dollar is also firm after RBA reaffirmed that the next move is likely a hike rather than a cut. Yen continues to trade as the weakest one even though stocks are turning mixed. Dollar follows as the second weakest as recent consolidation continues.

In other markets, Nikkei is back today and trades up 0.94% at the time of writing. Singapore Strait Times is up 0.45%. But China SSE is down -1.01% at 2785, back below 2800 handle. That drags down Hong Kong HSI by -1.0%. Overnight, DOW closed up 0.18% at 25064.36 but NASDAQ and S&P 500 lost -0.26% and -0.1% respectively. For now, thanks to Dollar's pull back, Gold is still holding above 1236.66, struggling around 1240. WTI crude oil suffered steep selling yesterday and is now pressing 68, after taking out 70 handle rather decisively.

Technically, while Dollar is broadly weak, it's staying in familiar range against Euro, Sterling, Aussie, Canadian and Yen. It's just in consolidation mode. Yen is also seen losing downside momentum against Euro and Sterling. The Pound will be a focus today with job data featured. 0.8808 in EUR/GBP is a level to watch.

New Zealand Dollar jumps as RBNZ sectoral factor model CPI improved

New Zealand CPI rose 0.4% qoq, 1.5% yoy in Q2, accelerated from Q1's 0.5% qoq and 1.1% yoy. The headline number missed expectations of 0.5% qoq, 1.6% yoy. However New Zealand Dollar later reacts to RBNZ's own prices data. Most notably, the sectoral factor model CPI rose to 1.7% yoy in Q2. There were continuous improvements since last year from 1.4% in Q3 2017 to 1.5% in Q4 2017 to 1.6% in Q1 2018.

The sectoral factor model CPI was created by RBNA to estimate the common component of inflation in the CPI basket, the tradable basket, and the non-tradable basket, based upon separate factors for the tradable and non-tradable sectors. The data excludes GST. It's one of RBNZ's preferred core inflation gauge.

RBA reiterates next move is more likely an increase

RBA minutes of July meeting cleared up some confusions in the market as it stated that "members continued to agree that the next move in the cash rate would more likely be an increase than a decrease." Still, as the progress of wage growth and inflation will "likely to be gradual, "there was no strong case for a near-term adjustment in monetary policy." Instead, "the Board assessed that it would be appropriate to hold the cash rate steady and for the Bank to be a source of stability and confidence while this progress unfolds." Overall, the minutes reaffirmed the tightening bias of the central bank, but the rate hike will only happen at least deep into mid-2019.

On the economy, RBA noted that recent data has been consistent with the central forecast of GDP growth at a bit above 3% over 2018 and 2019. Non-mining business investments had "contributed significantly" to growth in Q1. Public infrastructure investment and business conditions "remained positive". But consumption "remained a source of uncertainty". Labor market outlook remain positive for solid growth ahead, with "vacancy rate" risen to historical high. And the conditions will lead to gradual decline in unemployment rate and push up wages.

Minneapolis Fed Kashkari: 'This time is different' are the four most dangerous words

Minneapolis Fed President Neel Kashkari warned of the recession signal from flattening yield curve in a paper. Over the past 2.5 years, the difference between 10 year yield and 2 year yield has dropped 134bps to 25bps today, a 10-year low. He warned that "if the Fed continues raising rates, we risk not only inverting the yield curve, but also moving to a contractionary policy stance and putting the brakes on the economy, which the markets are indicating is at this point unnecessary."

And he added that "this time is different" are the "four most dangerous words in economics". And such declaration should be a "warning that history might be about to repeat itself.

UK PM May got Brexit Customs Bill narrowly passed after conceding to Brexiteers

UK Prime Minister Theresa May narrowly avoided defeat yesterday on the Brexit Customs Bill in the Commons after conceding to four amendments of the Brexiteers. But the slim margin in vote showed once again the deep divisions between pro-EU Tories and Brexiteers that could heavily undermine May's position in upcoming negotiations.

One amendment prevents UK from collecting taxes on behalf of the EU unless the rests of the EU does the same for the UK. It's passed by 305 to 302 with 14 Tories rebelled. Another amendment ensures the UK is out of EU's VAT regime and was passed by 303 to 300, with 11 Tories rebelled.

Debates will continue today with the Trade Bill going to the Commons. The bill allows the UK government to build new trade relationships with other countries after Brexit. Some pro-EU MPs who support staying in the EU customs union are pushing for some changes in wordings.

IMF: US initiated trade actions as biggest threat, could lower global growth by 0.5% by 2020

IMF released the July update of the World Economic Outlook. Chief Economist Maury Obstfeld said in the the group continued to project global growth of around 3.9% for 2018 and 2019. But "risk of worse outcomes has increased, even for the near term." In particular, he noted that "risk that current trade tensions escalate further—with adverse effects on confidence, asset prices, and investment—is the greatest near-term threat to global growth."

He added that the US has " initiated trade actions affecting a broad group of countries" and "faces retaliation or retaliatory threats from China, the European Union, its NAFTA partners, and Japan, among others." Based on their modeling, Obstfeld said the trade policy threats could lower global output by around 0.5% by 2020. The US is "especially" vulnerable as it's the "focus of global retaliation".

Global growth forecast was left unchanged at 3.9% in both 2018 and 2019. For advanced economies, 2018 growth forecast was revised down by -0.1% to 2.4%, 2019 growth forecast was left unchanged at 2.2%. US growth was forecast was left unchanged at 2.9% (2018) and 2.7% (2019). Eurozone growth was projected to be at 2.2% (2018, down -0.2%) and 1.9% (2019, down -0.1%). Japan growth was projected to be at 1.0% (2018, down -0.2%) and 0.9% (2019, unchanged). UK growth was projected to be at 1.4% (2018, down -0.2%) and 1.5% (2019, unchanged). China growth projections were unchanged at 6.6% (2018) and 6.4% (2019).

Elsewhere

UK employment data will be the main focus today. Canada will release manufacturing sales. US will release industrial production and NAHB housing index.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7406; (P) 0.7424; (R1) 0.7440; More...

AUD/USD strengthens mildly today but stays in range of 0.7359/7483. Intraday bias remains neutral first. Outlook is unchanged that consolidation from 0.7309 could extend further and stronger recovery cannot be ruled out. But after all, upside should be limited below 0.7676 resistance to bring larger fall resumption. On the downside, below 0.7359 will target 0.7309 support first. Sustained trading below 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q2 | 0.40% | 0.50% | 0.50% | |

| 22:45 | NZD | CPI Y/Y Q2 | 1.50% | 1.60% | 1.10% | |

| 01:30 | AUD | RBA Minutes Jul | ||||

| 08:30 | GBP | Jobless Claims Change Jun | 2.3K | -7.7K | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y May | 2.50% | 2.50% | ||

| 08:30 | GBP | ILO Unemployment Rate 3Mths May | 4.20% | 4.20% | ||

| 12:30 | CAD | Manufacturing Sales M/M May | 0.60% | -1.30% | ||

| 13:15 | USD | Industrial Production M/M Jun | 0.50% | -0.10% | ||

| 13:15 | USD | Capacity Utilization Jun | 77.90% | |||

| 14:00 | USD | NAHB Housing Market Index Jul | 69 | 68 | ||

| 20:00 | USD | Net Long-term TIC Flows May | 34.3B | 93.9B |

New Zealand Dollar jumps as RBNZ sectoral factor model CPI improved

New Zealand CPI rose 0.4% qoq, 1.5% yoy in Q2, accelerated from Q1's 0.5% qoq and 1.1% yoy. The headline number missed expectations of 0.5% qoq, 1.6% yoy. However New Zealand Dollar later reacts to RBNZ's own prices data. Most notably, the sectoral factor model CPI rose to 1.7% yoy in Q2. There were continuous imrpvements since last year from 1.4% in Q3 2017 to 1.5% in Q4 2017 to 1.6% in Q1 2018.

The sectoral factor model CPI was created by RBNA to estimate the common component of inflation in the CPI basket, the tradable basket, and the non-tradable basket, based upon separate factors for the tradable and non-tradable sectors. The data excludes GST. It's one of RBNZ's preferred core inflation gauge.

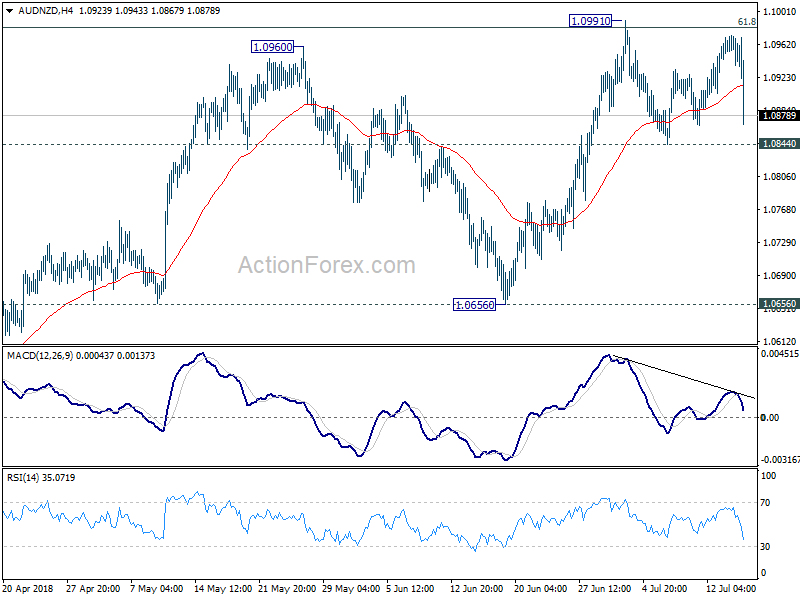

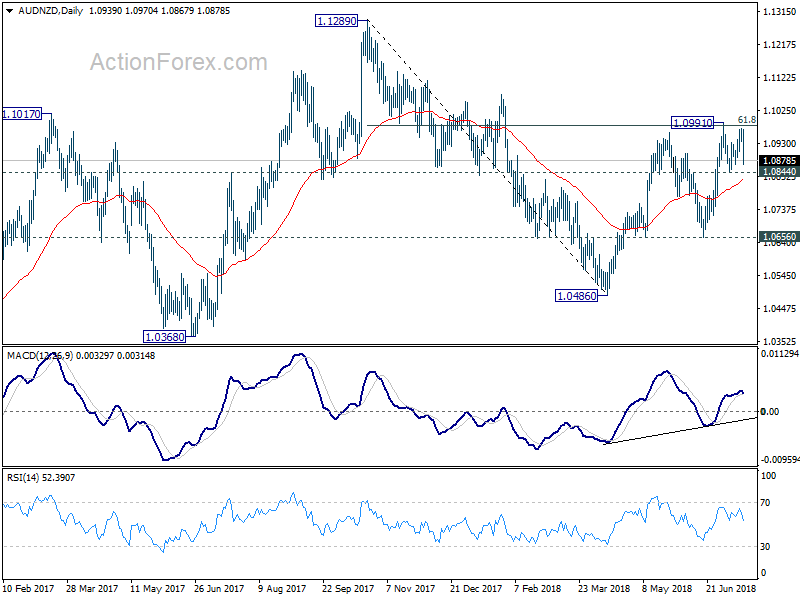

AUD/NZD dives sharply after the release after it was one again rejected by 61.8% retracement of 1.1289 to 1.0486 at 1.0982. Deeper fall should now be seen back to 1.0844 support first. Further break of 55 day EMA (now at 1.0823) will target 1.0656 key support level.

GBP/USD Back Above 1.3220, More Gains Possible

Key Highlights

- The British Pound was rejected from the 1.3100 support area against the US Dollar.

- There was a break above a major connecting bearish trend line with resistance at 1.3230 on the 4-hours chart of GBP/USD.

- The US Retails Sales in June 2018 increased 0.5% (MoM), similar to the forecast.

- Today in the UK, the Claimant Count Change for June 2018 will be released, and the forecast is 2.3K.

GBPUSD Technical Analysis

The British Pound corrected lower this past week below 1.3150 against the US Dollar. However, the GBP/USD pair found a strong buying interest near 1.3100, resulting in a sharp upward move.

Looking at the 4-hours chart, the pair jumped higher with back-to-back bullish candles above the 1.3150 resistance. The upside move was such that the pair broke the 1.3220 resistance and settled above the 100 simple moving average (red, 4-hour).

There was also a break above the 50% Fib retracement level of the last decline from the 1.3362 high to 1.3102 low. It seems like the pair moved back in a bullish zone and it could rise further towards the 1.3320 level.

If there is a downward correction, the pair may perhaps find support near the 1.3210 level and the 100 SMA.

Recently in the US, the Retail Sales report for June 2018 was released by the US Census Bureau. The market was looking for a rise of 0.5% in sales compared with the previous month.

The result was similar to the forecast, but the retail sales control group posted no change, whereas the market was looking for a rise of 0.4%. The report added:

Total sales for the April 2018 through June 2018 period were up 5.9 percent (±0.5 percent) from the same period a year ago. The April 2018 to May 2018 percent change was revised from up 0.8 percent (± 0.5 percent) to up 1.3 percent (±0.2 percent).

Overall, the US Dollar buyers were not impressed, resulting in an upward move in EUR/USD and GBP/USD.

Economic Releases to Watch Today

- UK Claimant Count Change June 2018 – Forecast 2.3K, versus -7.7K previous.

- UK ILO Unemployment Rate May 2018 (3M) – Forecast 4.2%, versus 4.2% previous.

- UK Average Earnings Including Bonus May 2018 (3Mo/Year) – Forecast +2.5%, versus +2.5% previous.

- UK Average Earnings Excluding Bonus May 2018 (3Mo/Year) – Forecast +2.7%, versus +2.8% previous.

- US Industrial Production June 2018 (MoM) – Forecast +0.5%, versus -0.1% previous.

- US Capacity Utilization June 2018 – Forecast 78.3%, versus 77.9% previous.

Market Morning Briefing: Gold Is Stuck Near 1240 For Quite A Few Sessions Now

STOCKS

Dow (25064.36, +0.18%) and Dax (12561.02, +0.16%) both continue to trade higher. Dow seems to be neared to the upside resistance at 25250 on the daily candles whereas Dax is stable in the 12500-12700 region unable to move up sharply just now.

Nikkei (22724.46, +0.56%) could face rejection near 22800 from where it may come off towards 22400-22200 again in the medium term. Only a break above 22800, if seen would be bullish for Nikkei in the longer run. Watch price action near 22800.

Shanghai (2787.01, -0.96%) has not been able to break above 2850 and instead has come off from there. It could re-test 2750-2700 in the next few sessions while below 2850. Some chances of a possible sideways movement in the 2700-2850 region exists in the longer run.

Nifty (10936.85, -0.74%) came off sharply yesterday but could get support in the 10900-10850 region which could again take the index higher towards 11100-11200 levels in the medium term.

COMMODITIES

Nymex WTI (68.09, +0.04%) fell sharply and could head towards support near 66-65 as seen on the daily candles before bouncing back from there. Surprisingly, Brent (72.25, +0.57%) has been pulled down breaking below support at 73 and could now target 70 on the downside. The sharp fall in Crude prices came in after comments from US Treasury Secretary Steven Mnuchin stated that the administration will consider the use of waivers for countries to continue buying Iranian Supplies.

Gold (1240.80, +0.09%) is stuck near 1240 for quite a few sessions now and is unable to decide on which direction to take. Considering the fall in other major commodities, there could be some scope of gold falling below 1240 and targeting 1230-1225 levels in the medium term. But we would have to wait and see if the price bounces from 1240 and test 1270/80 before falling to current levels.

Copper (2.7870, +0.81%) is trading above immediate support at 2.70 and while that holds, Copper could eventually target higher levels of 2.85 in the coming sessions.

FOREX

Euro (1.1707): As per our expectation of an upmove towards 1.175 in the first half of this week, Euro moved up yesterday, seeing a high near 1.1725. It is trading slightly lower currently, but could test 1.175 in today's session. Resistance on daily candles is slightly higher up near 1.176-1.177, which could produce a dip.

Dollar Index (94.545): Yesterday's forecast of a dip towards support near 94.0-94.2 on daily candles would be possible only upon a break of the crucial 8 weeks MA near 94.37. The 34 days MA on the daily line chart at 94.40 is also providing support. Our preference for a rise in the Euro towards 1.175 implies that Dollar Index could indeed break the above mentioned MA supports.

Dollar Yen (112.40): On weekly candles, there could be an interim resistance near 113 which could make Dollar Yen pause in its rally since last week. We still prefer a breach of 113 to extend upto 114-115 (horizontal resistance zone) which could possibly cap the current upmove.

Euro Yen (131.61): The 55 week MA near 131.58 might be providing decent resistance to Euro Yen in its upmove towards 133. However, we prefer a breach of this level in the next 1-2 sessions, followed by a rise towards resistance near 1.33 in the channel on daily line chart (by next week).

Pound (1.3232): Exactly as per expectation, Pound tested resistance on daily candles yesterday by seeing a high near 1.3293 and has then dipped. A dip towards 1.305 later in the week or by early next week seems possible. Levels near 1.305 are a crucial support zone, which when broken, could make Pound very bearish.

Dollar Rupee (68.575): We see a small range of 68.40-70 for the coming few sessions , followed by a possible dip below 68.40, to be limited to 68.25-15-00.

INTEREST RATES

US Retail Sales rose 0.5% in June and met market expectations. Moreover the growth figure for May was revised upwards. This has led to a rise in US Yields. However, at the same time, since the data couldn't surpass expectations, the positive impact on yields might not be sustained. A fall in Brent Crude by more than 2.7% is something that could start affecting US long term yields, as long term inflation expectations might just get revised downwards.

US 10 year yield (2.86%), 30 Year (2.965%), 5 Year (2.754%), 2 Year (2.597%):

Our July '18 US Treasury report will be released shortly. It explores the likelihood of a fall in the US 10-2 Yield Spread (0.26%) below 0%. A fall towards 0.2% by the 1st half of August is looking likely for now.

The German – US 10 year spread (2.5%) might be testing long term support at current levels. It might not dip lower towards -2.7% and could only rise from here. Let's wait and watch.

Monday Blues Or Dog Days Of Summer

Monday blues or Dog days of summer

Whether a case of the Monday blues, the Dog Days of summer setting in or a combination of both, markets struggled for direction despite upbeat US economic data while quarterly earnings have failed to inspire investors. And we might chalk it up to a typical summer afternoon NY trading session.

Event-wise, apart from the Tump/Putin headline which managed to supplant China-US trade headlines, there has been very little news worth to report as the markets hardly budged on the positive US retail sales print and remained in stasis during the Empire survey. And Sterling barely blinked after UK PM May scraped through a Customs Union amendment by 305 votes to 302. However, with May yet again snatching victory from the jaws of defeat, it should provide a reasonable underpin for the Pound over the near term although this morning activity has been remarkably muted

US markets

Wall Street opened with a misfire. Investor expectations were running at peak optimism, and while banks stocks looked favourable, sentiment turned sour, as oil price worries intensified.

Then there was the thud that was heard up and down wall street as Netflix fell off a cliff in late trading after posting dispiriting subscriber growth last quarter. Indeed, with one of the markets key highfliers going into the tank, it could be a tough 24 hours for FANG stocks. FANGS ‘s have been the undisputed heavyweight champions of the equity world, and pretty much impervious to risk off and trade wars. But when you start looking under the hood and strip away a couple of FANG outperformers, US equity markets aren’t all that cheery. This negative Netflix result could spur more moves into to cash as investors may finally adopt a delayed sell in May and go away strategy.

Oil markets

Oil markets are slip sliding away under renewed selling pressure from long liquidation as bearish sentiment grows thick k with the US actively considering tapping the Strategic Petroleum Reserve, the chatter of increased Russian oil production after Putin extends the US an olive branch to add more barrels, while the US considers waivers on Iranian sanctions. The sweeping slew of bearish signals has wholly eroded market sentiment with Brent Crude breaking bad now trading below May 2018 lows.

Also, with the market ignoring bullish indicators, specifically the latest production outage in Libya, where the 290,000 bpd Sharara oil field is reducing output due to an act of terrorism. It calls attention to just how big of a shift market sentiment has undergone since last Wednesday’s high-volume meltdown.

Gold markets

Bearish sentiment continues to engulf the precious metal space after a break of the fundamental $ 1,240 support level overnight while breaching multi-year trendlines. Markets are becoming more e convinced about a strengthening dollar, which will unquestionably act as a most significant headwind and could continue to pressure gold lower as safe-haven demand remains muted.

In fact, the dollar slipped lower in modest price action, yet gold still fell below critical support. Ignoring even the slightest bullish indicator is an unfortunate sign and suggests we could push significantly lower when the USD moves out of its current melancholic state and starts to reassert its presence.

Currency Markets

The USD eased lower for the third consecutive day as trade war headline decreased and some of last week’s froth give way to position neutrality. But we’ve been in this back and forth momentum on the USD since the beginning of June. Whenever the USD picks up steam, everyone boards the rally bus only to get whipped sawed by a brutal correction. But as we move into the dog days of summer, expect volumes to taper but volatility to remain elevated given considerable headline risk. But overall. caution prevails

When markets turn directionless, it’s time to revert into the interest rate matrix for clarity which suggests the USD has more gas in the tank than say the EUR, JPY or the AUD.

GBP: In general, I think everyone likes GBP higher. Therefore, the crowded trade phenomena make correction even more brutal. Again, back to basics. Assuming Brexit risk remains contained (big headline risk assumption) and with the surprisingly hawkish shift from Cunliffe, the BOE’s standing dove, a rate hike in August is all but inevitable GBP should remain in favour.

JPY: Equity momentum has waned this week but increasing JPY outflows to suggest we may only be in the early stages of this move higher in USDJPY. With US yields ticking higher, the fundamental differential argument remains intact.

AUD: Shorts should continue to lead the way, China remains a significant risk despite some favourable commodity forecast based on positive what if scenarios. i.e. what if Trade war abates

MYR: There was a regional sigh of relief after China GDP matched market expectations. While of course taking the data print at face value, the markets are reading this as more or fewer things are not as bad as they could have been. But there is little to get excited about a slowing economy in my views.

With no 'risk on catalysts', the MYR will take cues from the RMB complex as the local markets will wait for Wednesday Malaysia CPI data. The data will be of interest given the BNM neutral stance from last week. But the market does think the zero GST effects will likely see inflation drop to the 1.7 %level which will not change markets view that BNM stays on hold for some time. Suggesting the MYR will get little support from interest rate differentials for the foreseeable future.

Also, the bearish sentiment in the oil markets continues to permeate every nook and cranny which should skew negative for MYR sentiment today.

Minneapolis Fed Kashkari: ‘This time is different’ are the four most dangerous words

Minneapolis Fed President Neel Kashkari warned of the recession signal from flattening yield curve in a paper. Over the past 2.5 years, the difference between 10 year yield and 2 year yield has dropped 134bps to 25bps today, a 10-year low. He warned that "if the Fed continues raising rates, we risk not only inverting the yield curve, but also moving to a contractionary policy stance and putting the brakes on the economy, which the markets are indicating is at this point unnecessary."

And he added that "this time is different" are the "four most dangerous words in economics". And such declaration should be a "warning that history might be about to repeat itself.

RBA reiterates next move is more likely an increase

RBA minutes of July meeting cleared up some confusions in the market as it stated that "members continued to agree that the next move in the cash rate would more likely be an increase than a decrease." Still, as the progress of wage growth and inflation will "likely to be gradual, "there was no strong case for a near-term adjustment in monetary policy." Instead, "the Board assessed that it would be appropriate to hold the cash rate steady and for the Bank to be a source of stability and confidence while this progress unfolds." Overall, the minutes reaffirmed the tightening bias of the central bank, but the rate hike will only happen at least deep into mid-2019.

On the economy, RBA noted that recent data has been consistent with the central forecast of GDP growth at a bit above 3% over 2018 and 2019. Non-mining business investments had "contributed significantly" to growth in Q1. Public infrastructure investment and business conditions "remained positive". But consumption "remained a source of uncertainty". Labor market outlook remain positive for solid growth ahead, with "vacancy rate" risen to historical high. And the conditions will lead to gradual decline in unemployment rate and push up wages.