Sample Category Title

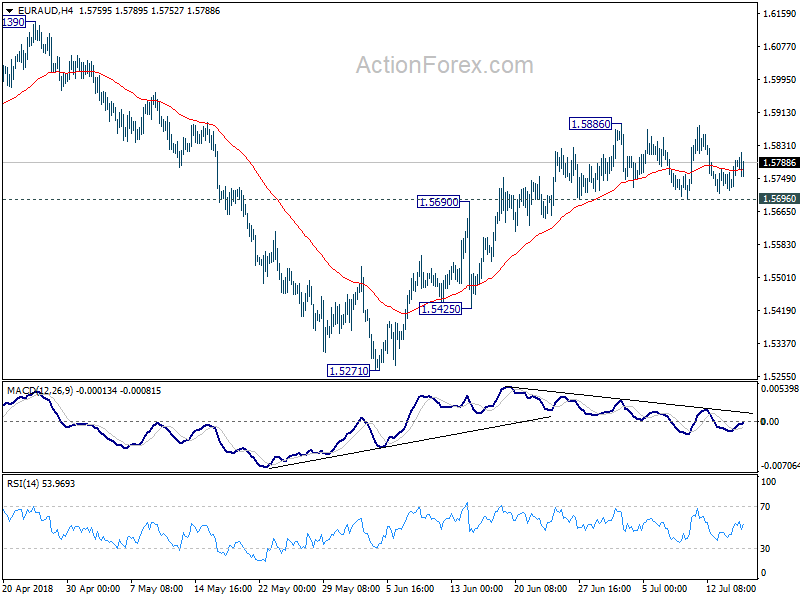

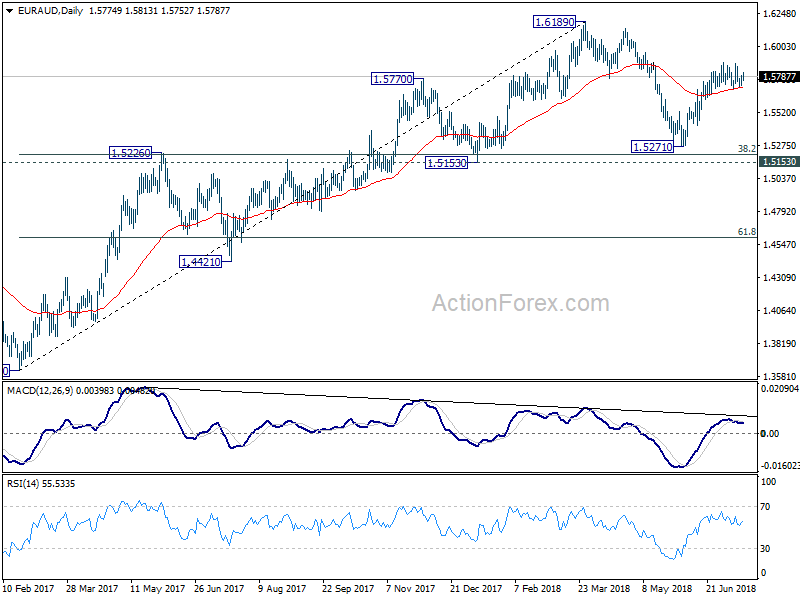

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5732; (P) 1.5765; (R1) 1.5814; More....

Intraday bias in EUR/AUD remains neutral for range trading below 1.5886. Further rise is expected as long as 1.569 minor support holds. On the upside break of 1.5886 will resume the rebound from 1.5271 and target a test on 1.6189 high. Nonetheless, the momentum and structure of such rise from 1.5271 are not too convincing. Break of 1.5696 will suggest near term reversal and turn bias to the downside for 1.5425 support for confirmation.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is still in progress. Break of 1.6189 will target 1.6587 key resistance (2015 high).

GBPUSD Retains Bullish Bias ABove 1.3205

The British pound continues to move away from the 1.3290 level against the US dollar, as traders book profits ahead of the release of key Jobs and Wage data from the United Kingdom economy. The GBPUSD pair has recently failed to move price above the 1.3300 level, as ongoing Brexit concerns limit the upside in the British pound. Buyers will look to target the 1.3300 level once again, while sellers will look for a sustained break below the 1.3205 level.

The GBPUSD pair is intraday bullish while trading above the 1.3205 level, key technical resistance is found at the 1.3255 and 1.3300 levels.

If the GBPUSD pair falls below the 1.3205 level, sellers will likely target the 1.3155 and 1.3130 support levels.

EURUSD Intraday Bullish Above 1.1724 Level

The euro currency continues to trade above the 1.1700 level against the US dollar, with bulls pressing against the key 1.1724 resistance level. Euro traders remain cautious ahead of Federal Reserve Chair Jerome Powell’s semi-annual testimony before US Congress later today. Buyers will look to advance well-beyond the 1.1724 level to keep the recent bullish momentum in the EURUSD, while sellers will target losses below the 1.1674 support area.

The EURUSD pair is only intraday bullish while trading above the 1.1724 level, key resistance is now found at the 1.1757 and 1.1820 levels.

If the EURUSD pair falls below the 1.1700 level, key technical support is found at the 1.1674 and 1.1650 levels.

Fed’s Powell In The Spotlight On Tuesday

Central bank speakers will hog the spotlight on Tuesday, with the Federal Reserve's Jerome Powell scheduled to testify before Congress and the Bank of England's Mark Carney set to speak publicly. Investors can also expect a steady stream of economic data from Europe and the United States to be in the headlines.

The economic calendar kicks off at 08:00 GMT with a report on Italian industrial production. BOE Governor Mark Carney is scheduled to begin his speech at the same time.

Attention will remain on the UK over the next hour as the Office for National Statistics releases the latest employment numbers for the months of May and June.

Britain's ILO calculated unemployment rate is expected to hold steady at 4.2% in the three months through May. Average hourly earnings including bonuses are projected to rise 2.5% year-over-year between March and May.

Meanwhile, the claimant count change for the month of June is expected to show an increase of 2,300 workers collecting unemployment benefits following a decline of 7,700 the month before.

Shifting gears to North America, the Canadian government will report on manufacturing shipments at 12:30 GMT. Shipments are projected to rise 0.6% for May after falling 1.3% the month before.

The US Fed will report on industrial production and capacity utilization at 13:15 GMT. Output at US factories likely rose 0.5% in June and the capacity utilization rate is projected to rise to 78.3%.

Fed Chairman Jerome Powell heads to Congress on Tuesday for two days of testimony on the economy. Under Powell, the Fed has raised interest rates twice this year and is planning on two additional upward adjustments in the back half of 2018.

Powell will continue his testimony on Wednesday.

EUR/USD

Europe's common currency gained momentum on Monday, with EUR/USD crossing the 1.1700 threshold for the first time since 11 July. The pair is trading right around that level as investors await Powell's testimony. EUR/USD faces immediate resistance at 1.1735, which corresponds with the 55-day moving average.

GBP/USD

Cable continued higher on Monday, extending last week's recovery as the dollar weakened against a basket of currencies. GBP/USD maxed out at 1.3289, a one-week high, before consolidating around 1.3230. The pair is likely to run into resistance north of 1.3250, with the psychological 1.3300 level offering a stiff barrier. On the flipside, immediate support is located at 1.3225.

USD/CAD

The North American pair held lower on Monday despite a 4% selloff in oil prices. USD/CAD now sits at 1.3137, with the technical indicators showing a neutral short-term outlook. Immediate support is located at 1.3080, followed by the 1.3000 handle. On the opposite side of the ledger, immediate resistance is found at 1.3265, followed by 1.3380.

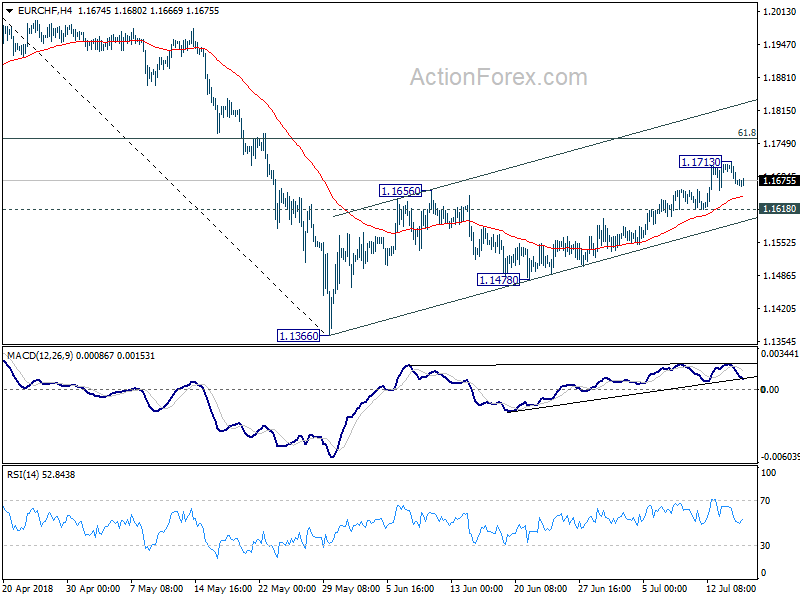

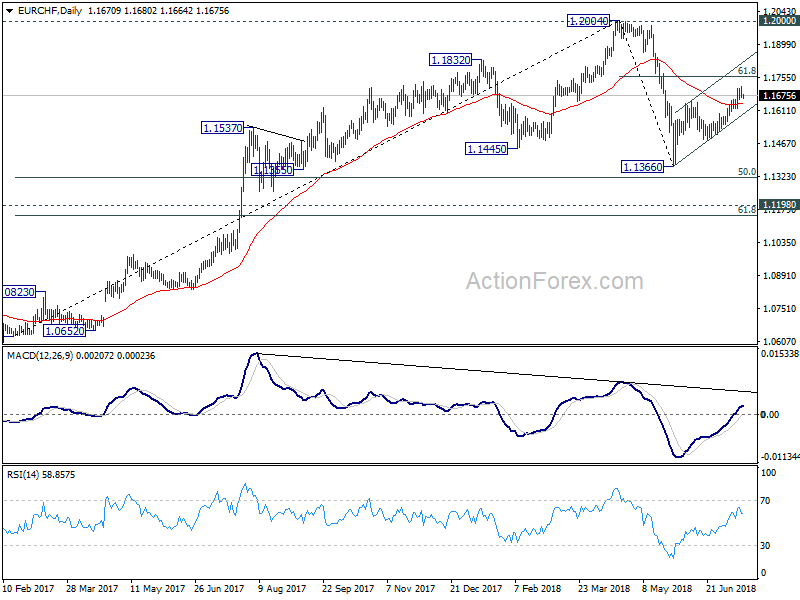

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1655; (P) 1.1687; (R1) 1.1704; More...

Intraday bias in EUR/CHF is turned neutral with the retreat from 1.1713 temporary top. Another rise could still be seen to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. However, as rebound from 1.1366 is seen as the second leg of the corrective pattern from 1.2004, we'd expect strong resistance from 1.1760 to limit upside. On the downside, below 1.1618 will turn bias back to the downside for 1.1478 support and below. However, sustained trading above 1.1760 will pave the way to retest 1.2004 high next.

In the bigger picture, 1.2004 is seen as a medium term top with bearish divergence condition in daily and weekly MACD. 1.2000 is also an important resistance level. Hence, the corrective pattern from 1.2004 is expected to extend for a while before completion. Hence, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

EUR/NOK In The Current Environment Is Capped At 9.54

Market movers today

A quiet day today with Fed Chair Powell's semi-annual hearing before the Senate Banking Committee being the main event at 16.00 CEST. However, we do not expect him to send new signals and the Fed is still likely to raise rates in both September and December, in our view. Powell's testimony continues tomorrow before the House.

At 10.30 CEST, the UK labour market report is due out, which is interesting ahead of the Bank of England's decision whether to hike or not at its next meeting in early August.

At 15.15 CEST, US production data for June is due out.

Selected market news

Yesterday in Helsinki, President Putin and President Trump held their first full summit, followed by a one-hour press conference. From the point of view of the reaction of financial markets, the meeting did not bring negativity and was quite positive, while at the same time, anti-Russia sanctions were not mentioned. The RUB saluted the event with a slight appreciation during the ongoing dividend payments period.

In Scandi FX, the combination of a slightly better-than-expected Swedish house price release together with an oil price losing ground has resulted in moderate NOK/SEK selling. Our expectation, however, remains that EUR/NOK in the current environment is capped at 9.54, which limits the downside potential for NOK/SEK and thereby also EUR/SEK.

Oil prices dropped 4% yesterday with Brent falling to USD72/bbl on unconfirmed reports that Saudi Arabia is offering extra supplies to the market. In addition, the market has been speculating whether the US would release strategic reserves to the market.

Today, focus will be on Powell's semi-annual hearing before the Senate Banking Committee at 16.00 CEST. The market will scrutinize whether Powell will comment on the continuation of flattening of the US yield curve that has historically been a reliable recession indicator. Last night, Fed member Neel Kashkari said there is ‘little reason to hike rates much further, invert the yield curve [and] trigger a recession'. The US 2Y10Y curve flattened to 25bp – a 10-year low – on Friday, but re-steepened slightly last night.

In Germany, the busy EGB supply week kicks off today with the German Finanzagentur selling up to EUR3bn in the June-20 Schatz. The outright yield level has moved 5bp higher in July and the auction should see good demand after the rise in yields.

Yesterday, the Danish mortgage banks published updated preliminary prepayment numbers (CK93) for the October 2018 term. We expect that the increases in the prepayment percentages for RD 3'31, RD 3'44 and BRF 3'44 are being generated by a remortgaging of social housing loans. Yesterday, we published an auction preview ahead of the DGB 2Y and 10Y taps tomorrow.

Elliott Wave Analysis: Facebook Correction Taking Place

Facebook ticker symbol: $FB short-term Elliott Wave analysis suggests that the decline to $192.22 low ended cycle degree wave II as double three structure. Up from there, the stock is rallying higher and making new all-time highs within cycle degree wave III. Up from $192.22 low, the rally to $208.2 high ended primary wave ((1)). The internals of that rally took place in the form of an impulse structure with lesser degree cycles showing an internal subdivision of 5 waves in each leg higher.

Up from $192.22 low, the rally higher to $197.45 higher intermediate wave (1) of ((1)) in 5 waves structure. Down from there, the pullback to $192.52 low ended intermediate wave (2) of ((1)) in 3 swings. Up from there, the rally higher to $205.80 ended intermediate wave (3) of ((1)) in 5 waves structure. Down from there, the pullback to $201.20 low ended intermediate wave (4) of ((1)) in 3 swings as a Flat. Then the rally higher to $208.2 high ended intermediate wave (5) of ((1)) in another lesser degree 5 waves.

Below from there, the stock is correcting the cycle from 7/02/2018 low ($192.22) in primary wave ((2)) pullback. The pullback is expected to find buyers in 3, 7 or 11 swings at the extreme areas. Near-term focus remains towards $200.80-$198.76 50%-61.8% Fibonacci retracement area as target area for the pullback. Afterwards, the stock is expected to resume higher provided pivot at $192.22 low stays intact or it should react higher in 3 waves at least. We don’t like selling it.

Facebook 1 Hour Elliott Wave Chart

China NDRC Expects Macroeconomic Policies To Be More Flexible In H2

General Trend:

- Asian equity markets trade mostly lower after mixed US session, Nikkei outperforms after being closed on Monday

- Netflix declines over 14% in afterhours trading, Q2 subscriber adds and Q3 guidance below ests

- Shanghai Composite trades lower for 3rd straight session

- Rio Tinto Q2 iron ore production rises y/y, targets FY production at upper end of prior range

- Japanese automakers higher on a weaker yen

- Tokyo Steel leaves prices unchanged for the 6th straight month

- RBA plays down impact of higher funding costs on banks, noted higher downside risks to global growth (minutes)

- A$ falls to session lows 0.7402 after RBA meeting minutes

- NZ Q2 CPI remains below the mid-point of the RBNZ’s targeted range (1-3%)

- Kiwi (NZD) later rises on acceleration in the RBNZ’s own inflation measure; NZ bond yields rise

- China new home prices accelerate in June

- Analysts begin to update China GDP forecasts amid trade concerns

- Fed’s Powell to hold first day of Congressional testimony (July 17th-18th)

- BHP due to report its Q4 production update tomorrow (July 18th)

- US companies expected to report earnings on Tuesday include: CSX. JNJ, UnitedHealth, UAL, Goldman Sachs

Headlines/Economic Data

Japan

- Nikkei 225 opened flat

- TOPIX Securities index +2.1%, Marine Transportation +2%, Retail Trade +1.5%, Iron & Steel +1.5%, Real Estate +1.3%, Info & Communications +1%

- Automakers and megabanks trade generally higher

- Line, 3938.JP Cryptocurrency exchange BitBox starts operation

- (JP) Japan Fin Min Aso: High chance of US and China trade tensions impacting others

Korea

- Kospi opened flat

- (KR) South Korea govt considering increased cash subsidies for smaller businesses in order to help ease the burden of higher payroll costs following 11% minimum wage increase for 2019 - Korean press

- (US) President Trump: Relationship with North Korea is "very good"

China/Hong Kong

- Hang Seng opened -0.3%, Shanghai Composite -0.3%

- Hang Seng Consumer Goods index -1.5%,Energy -1.5%, Info Tech -1.4%, Services -1.3%, Financials -0.8%, Property/Construction -0.6%

- (CN) China yuan currency is unlikely to further fall 'significantly' - China Securities Journal

- (CN) China outbound foreign direct investment (OFDI) has shifted towards Europe from North America in H1 – Xinhua

- (CN) China PBoC Open Market Operation (OMO): Injects CNY100B in 7-day and 14-day reverse repos v CNY300B prior; Net: CNY90B injects v CNY300B injection prior

- (CN) China PBoC set yuan reference rate at 6.6821 v 6.6758 prior (weakest setting since Aug 2017)

- (CN) China Jun New Home Prices m/m: +1.0% v 0.8% prior; y/y: 5.0% v 4.7% prior

- (CN) China Q2 Industrial Capacity Utilization q/q: 76.8% v 76.5% prior

- (CN) UBS sees China 2018 GDP growth forecast at 6.5% v 6.6% prior, revises 2019 GDP growth forecast to 6.2% v 6.4% prior – US financial press

- (CN) China NDRC: Expects prices and economy to remain stable in H2; In H1 approved 102 fixed asset investment projects worth CNY260.3B

Australia/New Zealand

- ASX 200 opened -0.1%

- ASX 200 Energy index -2.2%, Resources -1.4%, Utilities -1.4%, Consumer Discretionary -0.7%, Telecom -0.5%; Financials flat

- RIO.AU Reports Q2 Pilbara Iron ore production 85.5Mt v 79.8Mt y/y; Shipments 88.5Mt v 88.4Me v 77.7Mt y/y; Guides FY18 Pilbara iron ore shipments higher end of prior 330-340Mt

- (NZ) New Zealand Jun Performance Service Index: 52.8 v 57.3 prior

- (NZ) NEW ZEALAND Q2 CPI Q/Q: 0.4% V 0.5%E; Y/Y: 1.5% V 1.6%E

- (NZ) New Zealand RBNZ Q2 Sectoral Factor Model Inflation y/y: 1.7% v 1.6% prior

- (AU) RESERVE BANK OF AUSTRALIA (RBA) JULY MEETING MINUTES: REITERATES NO STRONG CASE FOR NEAR-TERM ADJUSTMENT IN MONETARY POLICY, NEXT MOVE LIKELY TO BE UP RATHER THAN DOWN

Other Asia

- (SG) Singapore Jun Non-Oil Domestic Exports M/M: -10.8% v -8.7%e; Y/Y: +1.1% v +7.8%e; Electronic Exports Y/Y: -7.9% v -7.8% prior

North America

- NFLX Reports Q2 $0.85 v $0.79e, Rev $3.91B v $3.94Be; Guides Q3 $0.68 v $0.71e, total Rev $3.99B v $4.14Be, total streaming Rev $3.90B, domestic streaming Rev $1.93B, international streaming Rev $1.97B; net operating margin 10.5% (-14% afterhours)

- ACET Subsidiary Acetris Health receives favorable ruling regarding certain government contracts (+12% afterhours)

- AMZN Reports 1st 3-hrs of Prime Day sales +54% y/y even with tech issues

Europe

- (UK) PM May wins Brexit amendment vote in House of Commons; vote 305 to 302; passes VAT amendment proposed by Brexiteer Conservatives and supported by PM May; vote was 303 to 300

- (RU) Russia President Putin: Told Trump that Russia is ready to extend the start of nuclear treaty but we have to agree on specifics - Fox News

Levels as of 01:30ET

- Hang Seng -1.1%; Shanghai Composite -1.0%; Kospi 0.0%; Nikkei225 +0.8%; ASX 200 -0.6%

- Equity Futures: S&P500 +0.0%; Nasdaq100 -0.1%, Dax 0.0%; FTSE100 0.0%

- EUR 1.1613-1.1726; JPY 112.23-112.57; AUD 0.7402-0.7438;NZD 0.6757-0.6841

- Aug Gold +0.1% at $1,241/oz; Sept Crude Oil 0.0% at $67.08/brl; Sept Copper +1.0% at $2.79/lb

Euro-Zone’s Trade Surplus Surprisingly Narrowed In May

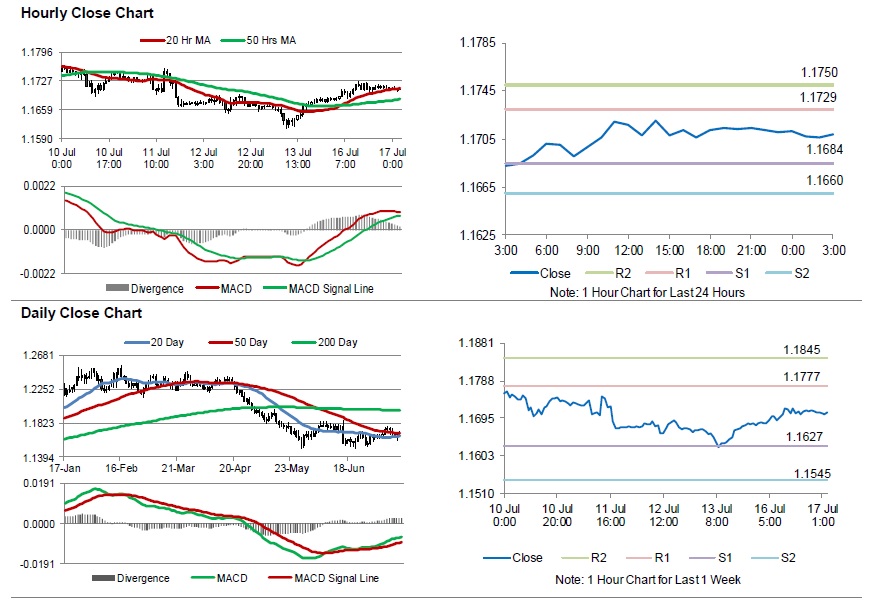

For the 24 hours to 23:00 GMT, the EUR rose 0.21% against the USD and closed at 1.1710.

Macroeconomic data indicated that the Euro-zone's seasonally adjusted trade surplus unexpectedly narrowed to €16.9 billion in May, after recording a revised trade surplus of €18.0 billion in the prior month, while markets participants were expecting the region's trade surplus to widen to €18.6 billion.

In the US, data showed that advance retail sales climbed 0.5% on a MoM basis in June, rising for the 5th consecutive month. In the previous month, advance retail sales had registered a revised gain of 1.3%. Meanwhile, the nation's business inventories rose 0.4% on a monthly basis in June, meeting market expectations. In the preceding month, business inventories had recorded a rise of 0.3%.

On the contrary, the US NY Empire State manufacturing index eased to a level of 22.6 in July, retreating from an 8-month high level of 25.0 in the previous month. Market consensus was for the index to fall to a level of 21.0.

In the Asian session, at GMT0300, the pair is trading at 1.1709, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.1684, and a fall through could take it to the next support level of 1.1660. The pair is expected to find its first resistance at 1.1729, and a rise through could take it to the next resistance level of 1.1750.

Moving ahead, investors would closely monitor the US industrial production for May and the NAHB housing market index for July, due to be released later in the day. Also, the Federal Reserve Chairman, Jerome Powell's testimony before the senate panel, will garner a significant amount of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

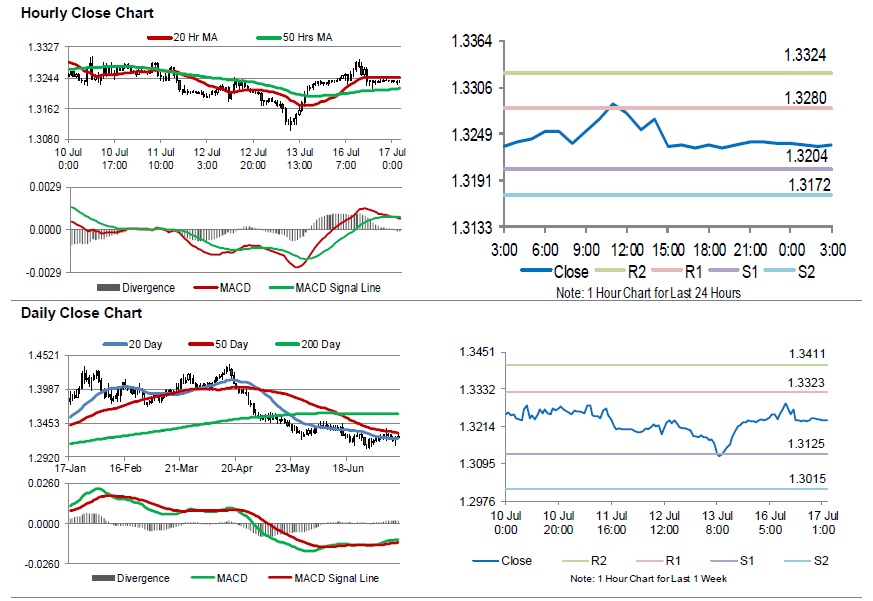

Sterling Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose a tad against the USD and closed at 1.3237.

In the Asian session, at GMT0300, the pair is trading at 1.3235, with the GBP trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3204, and a fall through could take it to the next support level of 1.3172. The pair is expected to find its first resistance at 1.3280, and a rise through could take it to the next resistance level of 1.3324.

Looking forward, traders await the release of UK’s latest average weekly earnings and ILO unemployment rate data, set to release in a while. Also, the Bank of England (BoE) Governor Mark Carney’s speech, will keep investors on their toes.

The currency pair is trading in between its 20 Hr and 50 Hr moving averages.