Sample Category Title

UK Jobs and Wage Figures Eyed by Pound amid Brexit Turmoil

The UK’s Office for National Statistics will publish its latest stats on the labour market on Tuesday at 08:30 GMT. The report will be the first of three major releases out of the UK this week, which come just a fortnight before the Bank of England’s August monetary policy meeting. With rate hike expectations rising to above 70% in recent weeks, those odds could be given an additional boost if this week’s data further reinforces the view that the first quarter economic slowdown was temporary. However, in forex markets, pound traders might be paying more attention to the Brexit ongoings as UK Parliament discusses the government’s customs and trade bills.

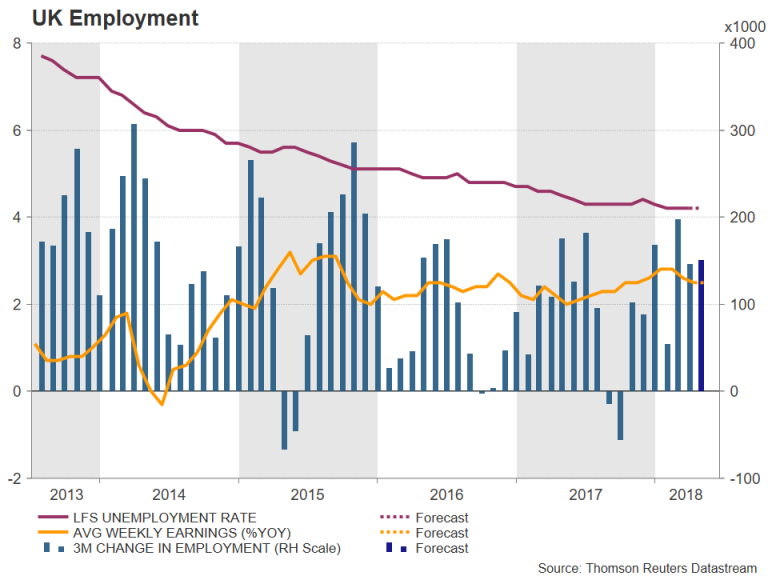

Britain’s labour market has remained tight even as growth cooled notably in the first three months of the year. The jobless rate has held steady at a more than four-decade low of 4.2% since January and is forecast to stay at that level in May. Job creation has been buoyant during 2018, with the number of people in work rising by 146k in the three months to April. Expectations are that there will be another solid rise in employment in the three months to May, with analysts estimating a gain of 150k.

However, of immediate concern for Bank of England policymakers will be the pace of wage increases as there are worries that the reduction in the number of EU workers coming into the UK after the Brexit vote is creating skills shortages in several sectors. Despite these concerns though, there are yet to be any signs of higher pay deals. Wage growth has remained below 3% since late 2015 and is only marginally above inflation, meaning real incomes are rising very moderately. Average weekly earnings were up 2.5% year-on-year in the three months to April and are expected to stay unchanged in May. Excluding bonuses, earnings are forecast to ease slightly from 2.8% to 2.7% y/y.

A bigger-than-projected rise in wages would fuel expectations that the BoE will hike interest rates next month on August 2 as the central bank would seek to prevent the labour market from overheating. Higher wage growth tends to produce an inflationary spiral as firms raise their prices to cover rising labour costs, which then leads to even higher wage demands. An overall strong jobs numbers, even if earnings growth remained muted, would also boost the pound as it would be seen as further proof of economic activity rebounding in the second quarter.

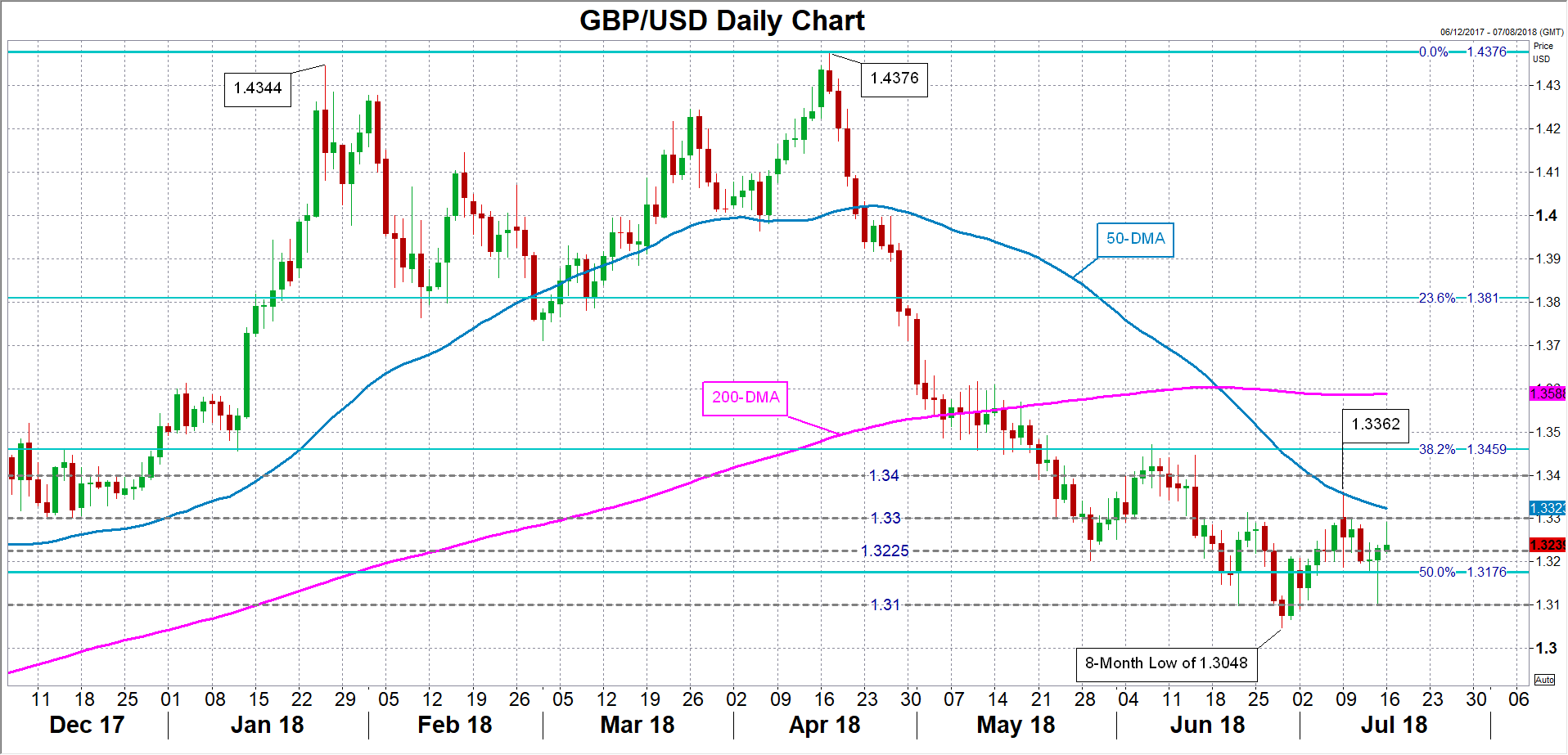

Sterling could get a lift above the $1.33 level in the event of upbeat data, though the 50-day moving average around $1.3320 could cap more extensive gains. Resistance could also come near the July top of $1.3362 before being able to challenge the $1.34 handle.

However, should the jobs figures fall short of expectations, the pound could retreat towards the $1.3225 support area before once again testing the $1.31 level. A drop below $1.31 would open the way towards June’s 8-month low of $1.3048.

Another potential downside risk for sterling this week is UK lawmakers’ debate on Prime Minister Theresa May’s third-way plan for a post-Brexit customs partnership with the EU and the resumption of Brexit talks in Brussels. With both pro-Brexit and pro-European MPs being unhappy with May’s proposals, the customs bill faces a difficult hurdle in Parliament, while the possible rejection of the UK’s plans by the EU could erase sterling’s July bounce.

Cable Lower after US Data; Focus on UK Jobs / Inflation Data; Brexit Talks

Cable pulled back from daily high at 1.3292, posted in extension of last Friday’s bounce after strong downside rejection at 1.3102, which left hammer candle. Pound benefited from rising hopes of UK rate hike on Aug 2 BoE MPC meeting, but sentiment was soured of concerns on hard Brexit, keeping the upside attempts limited and away from key barriers at 1.3362 (09 July high) and 1.3472 (07 June high).

Today’s release of US retail sales marked fresh pressure on pound as the June figure came in line with expectations but strong upside revision of previous month’s releases improved the picture and boosted the dollar.

Daily techs are in mixed mode but prevailing tone remains negative as falling and thickening daily cloud continues to produce heavy pressure (cloud top lays at 1.3383).

Near-term focus turns towards tomorrow’s release of UK jobs data (Avg earnings f/c 2.5% unchanged from previous, while jobless claims are forecasted significantly lower in June, 2.3K vs -7.7K prev) and UK inflation data on Wednesday(June f/c 2.6% vs 2.4% prev) which could provide fresh direction signals.

Res: 1.3292; 1.3301; 1.3362; 1.3400

Sup: 1.3224; 1.3202; 1.3180; 1.3102

EURUSD Reluctant to Move

EURUSD doesn't look active and is not moving in any clear direction. Still, although trade wars are no longer as a strong trigger as before, they have not become less relevant. Now it's China's turn, but its government has not taken any measures in response to the US policies yet.

Meanwhile, Donald Trump is still traveling around the political world. He already visited Britain where he spoke hawkish on May and Brexit, which affected pound sterling negatively. Now the US President, as well as the market, is focused on the meeting with the Russian leader Vladimir Putin.

Investors are watching both economic and political news closely, but very calmly. While the market is not that interesting for its participants now, it may save some effort for the future moves that may be caused by a lot of various drivers and triggers.

Thus, today's evening we'll be expecting the US retail sales in June. May was a great month for the retail sector, with the figures adding 0.8% MoM, while the automotives were even higher, +0.9%. The markets are now very engaged in watching what could June data reveal. This time the expectations are not that high, just 0.4% in both cases. If these expectations are met or beaten, this may well support the US dollar.

On Tuesday, the manufacturing production is being released, which should confirm current trends.

Technically, the EURUSD is downtrending in the short term, which was caused by the previous uptrend support breakout. This new downtrend already reached the projection channel support and may go further down till another support at 1.1605. However, the pair may start rising again soon, so one should also closely watch the resistance at $1.1715, which, if broken out, may lead the price to the important local highs at $1.1790 and $1.1875.

IMF: US initiated trade actions as biggest threat, could lower global growth by 0.5% by 2020

IMF released the July update of the World Economic Outlook. Chief Economist Maury Obstfeld said in the the group continued to project global growth of around 3.9% for 2018 and 2019. But "risk of worse outcomes has increased, even for the near term." In particular, he noted that "risk that current trade tensions escalate further—with adverse effects on confidence, asset prices, and investment—is the greatest near-term threat to global growth."

He added that the US has " initiated trade actions affecting a broad group of countries" and "faces retaliation or retaliatory threats from China, the European Union, its NAFTA partners, and Japan, among others." Based on their modeling, Obstfeld said the trade policy threats could lower global output by around 0.5% by 2020. The US is "especially" vulnerable as it's the "focus of global retaliation".

Below are the new projections, compared with April's.

Full release and WEO update.

British Pound Edges Higher, Investors Eye UK Job Numbers

The British pound has recorded slight gains in the Monday session. In North American trade, the pair is trading at 1.3266, up 0.24% on the day. On the release front, British Rightmove HPI surprised with a decline of -0.1%, its first decline since December. In the U.S, core retail sales dropped to 0.4%, matching the estimate. Retail sales dropped to 0.5%, edging above 0.4%. On Tuesday, BoE Governor speaks before the Treasury Select Committee, and the U.K will release wage growth and unemployment rolls. In the U.S, Federal Reserve Chair Jerome Powell testifies before the Senate Banking Committee.

The U.S economy is firing on all cylinders and received a vote of confidence from the head of the Federal Reserve. On Thursday, Powell said that the economy is “in a really good place”, pointing to President Trump’s massive tax cut scheme and increased spending as key factors in boosting economic growth. Powell did not address monetary policy and said he was uncertain as to the effects of the current trade disputes which has embroiled the U.S and its trading partners. The Fed will likely press the rate trigger in the second half of the year, but it is an open question as to whether we’ll see one hike over the next six months. The Fed is projecting growth of 2.8% in 2018, compared to 2.3% in 2017. Powell will be in the spotlight next week when he appears for his semi-annual testimony before Congress.

Trade policy is not part of the Federal Reserve’s mandate, but Fed policymakers continue to voice concern about the escalating trade war between the U.S and its major trading partners, particularly China. On Friday, Dallas Fed President Robert Kaplan said he would have to downgrade his outlook if the tariff battle continues. Kaplan said that U.S tariffs on steel and aluminum imports had dampened capital expenditures plans and further trade tensions could lead to currency fluctuations and geopolitical instability.

As the Brexit deadline creeps ever closer, both sides are making contingency plans for a ‘hard Brexit’, in the event that the parties fail to reach an agreement. On Thursday, the British government released a white paper, which is a blueprint for trade arrangements with the EU when Britain leaves the club in March 2019. The proposal suggests that the UK and the EU will enter into an “association agreement”, which maintains current agreements with regards to goods but not services. This could have a significant negative impact on London’s financial hub, which is already facing the loss of hundreds of financial jobs from London to the continent. Prime Minister May is facing strong opposition from hardliners in her cabinet, who argue that the white paper leaves the EU too much control over British trade policy and could hamper British trade deals. Will the Europeans buy what May is selling? EU policymakers are reviewing the white paper and if it is rejected, investors could get panicky and send the pound lower.

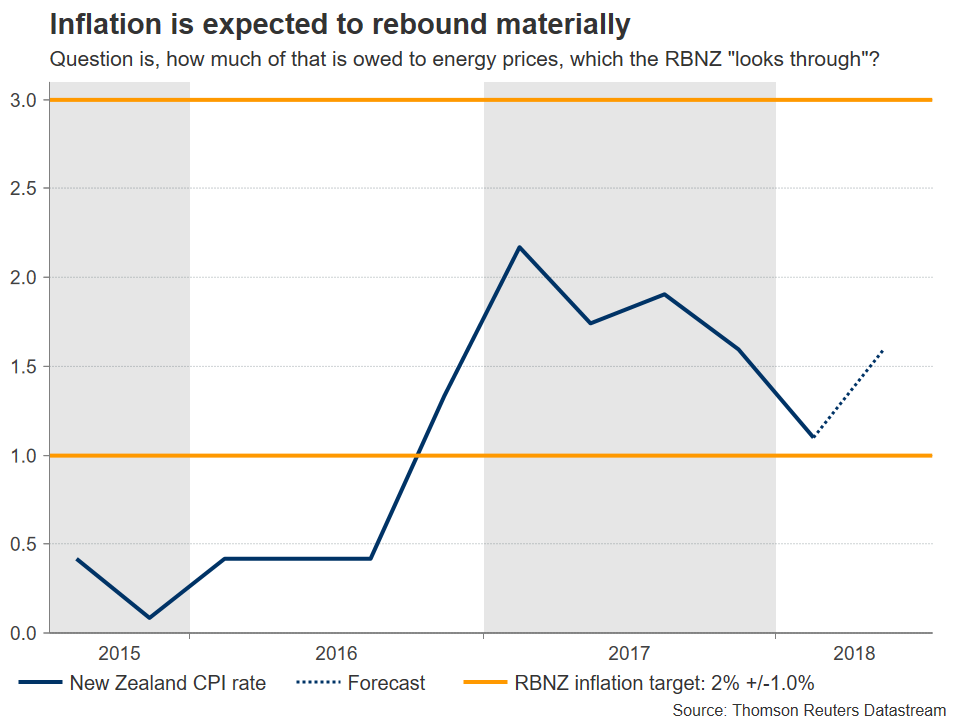

Kiwi Looks to Inflation Figures for Much-Needed Support

New Zealand will see the release of its quarterly inflation data for Q2 on Monday, at 2245 GMT. Consensus expectations are for a solid rebound in the CPI rate, which although may be owed largely to energy effects, would still be slightly higher than what the RBNZ projected in its latest forecasts. Overall, the kiwi has plunged lately, while speculative positioning has reached stretched-short levels, which implies that any positive surprises in economic data moving forth could trigger larger-than-usual positive reactions in the kiwi.

Recent developments have not been encouraging for New Zealand’s economy, leading the nation’s Reserve Bank (RBNZ) to adopt a more cautious policy stance amid a slowdown in economic growth, subdued wage pressures, and a continued deterioration in business confidence. To make matters worse, global trade tensions have intensified further, presenting downside risks for New Zealand’s export-dependent economy. Reflecting these, investors increasingly priced out any expectations for an RBNZ rate increase this year and instead, have now factored in a small probability for a rate cut.

The kiwi has fallen to a two-year low against the dollar as a result, with recent CFTC data pointing to extreme net-short positioning among speculative investors such as hedge funds. In isolation, this suggests that most of the “bad news” may be priced in already, and that the risks surrounding the kiwi moving forward may be asymmetrical. Whereas more negative developments could keep the currency around current low levels, or push it a little lower, any upside surprises in economic data or encouraging news on the trade front could trigger a significant relief rally.

Turning to the upcoming data, forecasts suggest inflationary pressures picked up in the latest quarter. In Q2, the nation’s CPI rate is projected to have risen to 1.6% in yearly terms, from 1.1% in the previous quarter. The RBNZ’s own forecasts back in May anticipated the CPI rate to only reach 1.5% in Q2, so anything above that would likely be pleasant news.

That said, the surge appears to be owed mostly to higher oil prices, and a depreciating New Zealand dollar pushing up the prices of imported goods, as opposed to the healthy demand-driven inflation the RBNZ would like to see. A spike higher in oil prices and a depreciating currency typically boost inflation, but only temporarily (i.e. the effects fade soon). Hence, RBNZ officials could disregard most of the surge as reflecting transitory effects, and focus more on core measures of inflation.

In case of an upside surprise in the CPI rate, some of the bets for rate cuts could fade, helping the kiwi to rebound. Technically, looking at kiwi/dollar, immediate resistance to advances may be found near the 0.6860 area, marked by the peaks of July 9 and 10. Even higher, the June 25 top of 0.6920 would increasingly come into view, with further upside paving the way for a test of 0.6973, defined by the inside swing low on June 13.

On the downside – and in case of a negative CPI surprise that amplifies speculation for a rate cut – further declines in the pair could encounter immediate support near the July 13 low of 0.6723, before the attention turns to the 2-year low of 0.6686 reached on July 3. A downside break could open the way for the 0.6575 zone, defined by the trough of 16 March, 2016.

US: Retail Sales end Q2 on a Healthy Note, as Americans Continue to Hit the Malls

Retail sales rose by 0.5% in June – bang on market expectations and marking the fourth straight month of solid gains. Better yet, May data was revised up an impressive 0.5% points to 1.3%.

Sales at gasoline stations rose 0.9%, while those at auto & parts dealers recorded a similar gain (+1.0%). Excluding these two categories, sales were up 0.4% – a hair below the headline print.

Sales at building material stores and food services rose 0.8% and 1.5% respectively – marking the second straight month of gains for both.

Excluding the above categories (gas, autos, building materials, and food services), the so-called 'control group' used in calculating GDP was flat on the month – disappointing market expectations for a 0.4% gain. Delving into the details, the control group provided a mixed bag. Sales at health (2.2%), furniture (0.6%) and non-store retailers (1.3%) were up on the month, while falling at general merchandise (-0.8%), clothing (-2.5%) and sporting goods (-3.2%) stores. The latter marks the third consecutive month of declines.

The June data bring the second quarter to a close, with sales up nearly 8% annualized, following a soft 1.8% print in the first quarter.

Key Implications

At face value, this was an undeniably solid report, with overall sales extending the recent string of healthy gains to four months and matching market expectations. The notable upgrade to the May data was another very encouraging element, which raises our expectation for Q2 consumer spending to better than 3% annualized.

A decent gain in real retail sales in June sets up positive momentum for the third quarter. We expect consumer spending will moderate in Q3, but remain solid at close to 2 ½% in real terms. Overall, steady job gains and a tightening labor market which is boosting wages, combined with a boost from tax cuts should see consumer spending remain a key support to growth through the rest of 2018.

Sunset Market Commentary

Markets

Global core bonds edge slightly lower today with US Treasuries underperforming German Bunds following the release of US eco data. Retail sales and the empire manufacturing survey remain strong, but printed close to forecasts. Traded volumes are extremely low. European stock markets treaded water near opening levels. Bank of America Q2 earnings were good, but not strong enough to impact global risk sentiment. The closely watched meeting between US President Trump and Russian President Putin started, but didn’t produce any meaningful headlines yet. Brent crude continues moving volatile, losing again $2/barrel. The US yield curve shifts 2.3 bps (2-yr) to 2.9 bps (30-yr) higher at the time of writing. German yield add 0.3 bps (2-yr) to 2 bps (10-yr). 10-yr yield spread changes vs Germany are virtually unchanged.

EUR/USD started the new week on a solid footing. Last week’s rejected downside test triggered a further gradual euro short-squeeze. A first attempt to regain the 1.17 mark was rejected, but a second attempt at the onset of the US trading session succeeded. The move was mainly order driven and technical in nature. We didn’t see a clear link with bonds or with equities/global risk sentiment. However, the intraday USD decline halted again after the publication of the US retail sales. Sales suggested solid Q2 US GDP growth, especially as May sales (which were already strong) were substantially upwardly revised. US yields and the dollar gained marginally upon the release. EUR/USD trades currently again just north of the 1.17 big figure. USD/JPY traded with a tentative negative bias this morning in Europe, but the decline also halted after the US data. The pair trades currently in the 112.40 area. In broader perspective, the moves in the major USD cross rates remain modest. EUR/USD is holding a sideways consolidation pattern. USD/JPY holds recent gains, but the rally is taking a breather.

Today, the headlines in the UK financial press were still dominated by the hefty debate on May’s Brexit strategy as it was set out in last week’s White Paper. A debate/vote in parliament today on the post-Brexit customs regime is seen as an indicator on the support (or the absence of support) for May’s approach. Early this morning, the debate had no additional negative impact on sterling. In technical trade, sterling even gained a few ticks. EUR/GBP filled bids in the 0.8820 area. Maybe, investor positioning was also, at least to some extent, influenced by a large set of UK eco data to be published later this week. If the data are OK, the BoE is expected to raise rates at the August 2 meeting. Later in the session, sterling momentum dwindled again as headlines suggested that the pro-Brexit wing in the conservative party would step up their attacks on May’s ‘soft’ Brexit approach. EUR/GBP trades again in the 0.8830 area. Cable is changing hands near 1.3260 (intraday top in the 1.3290 area).

News Headlines

In a response to the latest call for a second EU referendum by former cabinet minister Justine Greening, the Downing Street spokesman explicitly ruled out a second referendum “in any circumstances”, saying “the British public have voted to leave the EU”.

US headline retail sales in June came in at a solid 0.5% (as expected). The core measure excluding cars and gas printed at 0.3% (vs. 0.4% expected). Both are down from an exceptionally strong May which saw its figures upwardly revised to 1.3%, the strongest increase since January 2017.

Earlier opposition from Italy’s anti-establishment government to the CETA might be easing as its agriculture minister Centinaio said in Brussels “nobody is in a hurry to bring CETA to the chamber” for a parliamentary vote.

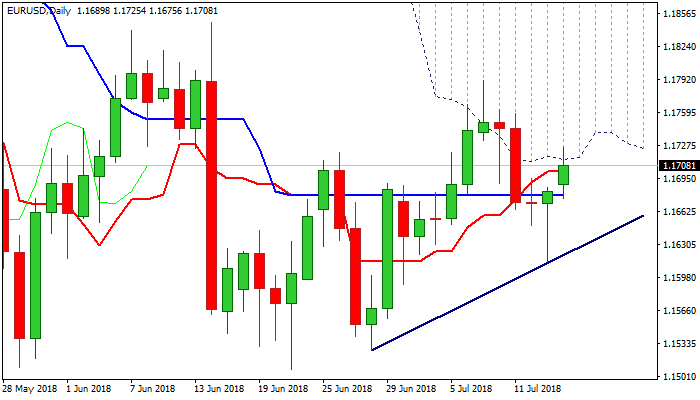

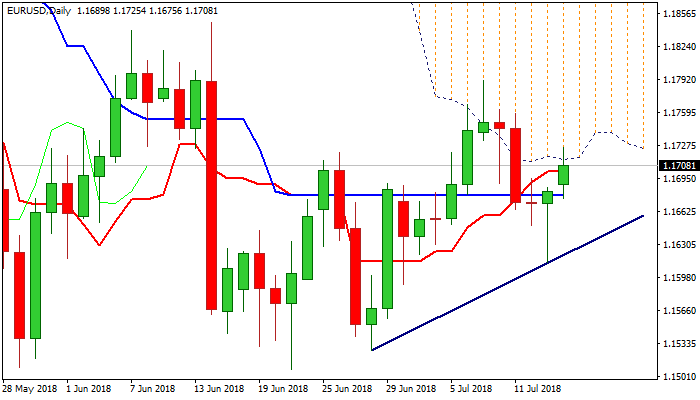

EURUSD Outlook: Massive Daily Cloud / Falling 55SMA Weigh Heavily

The Euro advanced further on Monday, extending bounce from last Friday's low at 1.1613, where strong downside rejection occurred. Friday's hammer signaled further recovery which resulted in extension and test of strong barrier at 1.1713, provided by daily cloud base, with initial probe through cloud base, being so far unsuccessful. Massive falling daily cloud produces strong pressure on the pair and could offset positive signals from hammer candle, bullishly aligned 14-d momentum and north-heading slow stochastic which reversed from the border of oversold territory. Daily MA's (5; 10; 30) are in mixed setup while 20SMA marks pivotal support at (1.1659), while falling 55SMA (1.1634) capped today's rally and reinforces cloud base barrier. Stronger direction signals could be expected on break of either pivotal barrier (upper at 1.1713/34, cloud base / falling 55SMA and lower at 1.1659, 20SMA). Near-term outlook for the single currency may weaken as solid US retail sales (Jun figures came in line with expectations but previous month's numbers were revised significantly higher) giving fresh support to the greenback. With no significant releases from the EU scheduled today and on Tuesday, focus turns towards Tue/Wed Congressional testimony of Fed's chief Powel, which could provide fresh hints about Fed's next steps and further impact the dollar.

Res: 1.1713; 1.1734; 1.1758; 1.1790

Sup: 1.1695; 1.1659; 1.1613; 1.1589

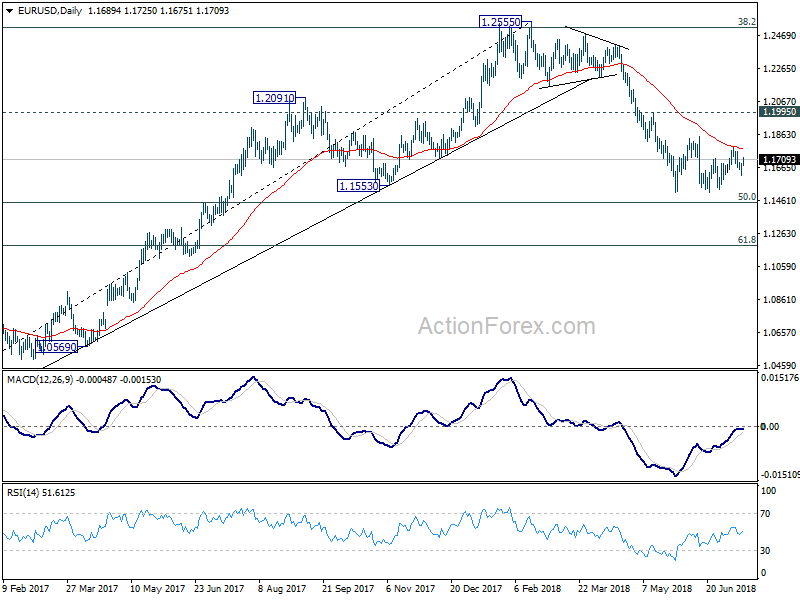

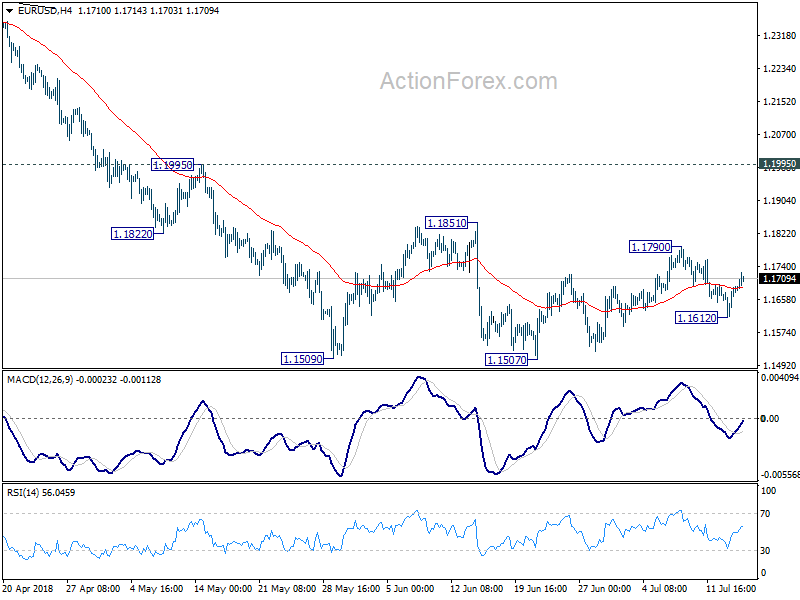

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1637; (P) 1.1662 (R1) 1.1712; More.....

Intraday bias in EUR/USD remains mildly on the upside for 1.1790 resistance or above. But price actions from 1.1507 are seen as a corrective pattern. hence, upside should be limited by 1.1851 resistance to bring fall resumption eventually. On the downside, below 1.1612 will bring retest of 1.1507 low first. Decisive break there will resume larger fall from 1.2555. In that case, EUR/USD should drop through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.