Sample Category Title

Dollar Pulls Back Ahead Of Powell’s Testimony, UK Jobs Data In Focus

Here are the latest developments in global markets:

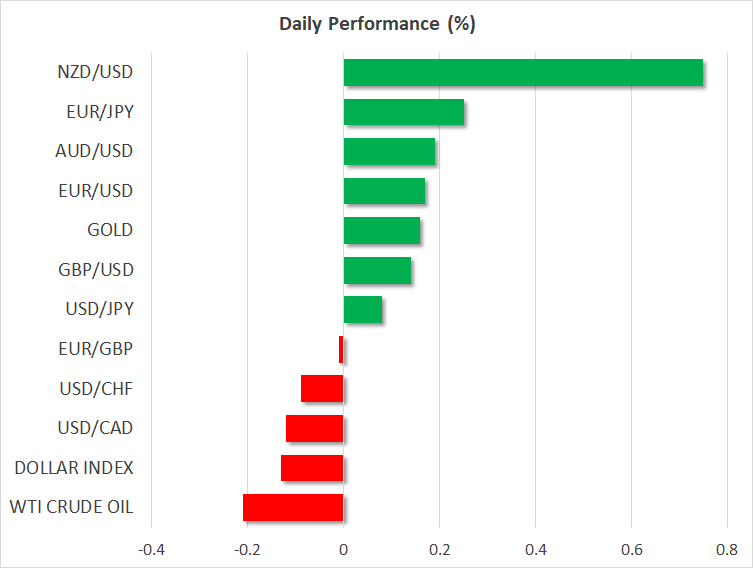

FOREX: The US dollar index is lower by 0.14% on Tuesday, ahead of a testimony by Fed Chairman Jerome Powell before the US Senate at 1400 GMT. Elsewhere, kiwi/dollar is up by 0.77%, following encouraging core inflation data out of New Zealand overnight.

STOCKS: US markets closed mixed on Monday. While the Dow Jones managed to advance by 0.18%, the S&P 500 and the Nasdaq Composite edged lower by 0.10% and 0.26% respectively. Something similar appears to be at play today. While futures tracking the Dow and S&P are marginally in positive territory, signaling a slightly higher open for those indices today, those tracking the Nasdaq 100 are in the red, pointing to a lower open. In Asia, Japan's Nikkei 225 and Topix were up by 0.44% and 0.87% on Tuesday, on their first day back from a public holiday. In Hong Kong, though, the Hang Seng was down by 1.21%. In Europe, futures following the major indices were all signaling a lower open today, with the only exception being the UK FTSE 100.

COMMODITIES: Oil prices collapsed again on Monday, with WTI falling by 4.15% and Brent by 4.63% in the day. Several supply-side drivers seem to have been behind the move (see below). Both WTI and Brent are down by 0.22% and 0.15% today as well. Price action will likely remain very sensitive to any fresh headlines in the coming days, following such sharp moves to the downside lately – recall that prices also dropped violently on July 11. In precious metals, gold is up by 0.18% at $1,242, but continues to struggle overall, hovering just above its lows for the year.

Major movers: Crude oil nosedives; Kiwi surges after inflation prints

News flow was relatively light on Monday, with the Trump-Putin summit being the highlight of the day. While the tone of both leaders was constructive overall, there was little new information for investors to digest and hence, the reaction in financial markets was limited.

The biggest movement was actually seen in oil prices, which plunged on Monday following reports that Saudi Arabia had offered extra crude volumes beyond its normal contracts to some buyers in Asia. The story likely amplified the narrative that OPEC and associated producers are set to raise their supply drastically, following similar signals from Russia. Separately, the fact that most of Libya's crude production has come back online following a prolonged shutdown, as well as recent rumors that the US may release its strategic petroleum reserves, likely played a role in pushing prices down as well.

As for the major currencies, there was little notable movement, with recent themes such as yen weakness continuing. The Japanese currency touched a fresh 10-week low against the euro and an eight-week low versus the pound, with the absence of any worrisome developments on the trade front undermining demand for the safe-haven currency.

The dollar index, meanwhile, is down by 0.14% today and looks set to post a third day of declines. US retail sales for June were in line with estimates yesterday, while last month's prints were revised higher. The dollar failed to draw any support from that, and also remained indifferent to an upward revision in the Atlanta Fed GDPNow forecast. Today, all eyes will be on Fed chief Powell's testimony before the Senate. Since the text is already released, focus will be on the Q&A session.

Overnight, the kiwi rebounded following encouraging inflation data out of New Zealand, with kiwi/dollar trading up by 0.77%. Although the headline inflation rate was a touch softer than expected, the core rate – which excludes the effects of volatile items such as oil – surged to touch 1.7% in yearly terms, a seven-year high.

The RBNZ was quite dovish when it last met amid softening economic data and global trade tensions, leading investors to price in a small probability for a rate cut this year. These data should help curb such speculation, allowing the kiwi to extend its rebound on any further encouraging data or trade news, particularly considering that speculative positioning on the currency has reached extreme net-short levels, according to CFTC figures.

Day ahead: UK employment data and US industrial production on the agenda; Powell testifies

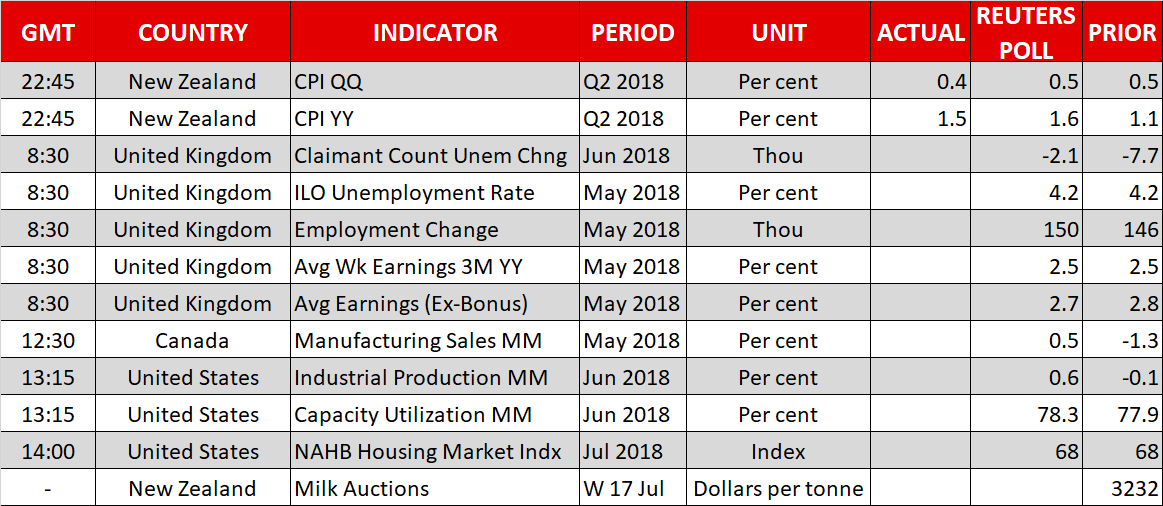

UK jobs data and US industrial & manufacturing production figures are perhaps Tuesday's most important releases. Beyond economic data, the Fed chief's congressional testimony is also of significance, having the capacity to lead to positioning on the greenback.

At 0830 GMT, UK employment data for May, as well as June's claimant count for unemployment benefits will be released. The unemployment rate has been holding steady at the more than four-decade low of 4.2% since February and it is projected to remain at that level in May. Meanwhile, expectations are for the addition of 150k positions in the economy in the three months to May, a robust number that also exceeds April's respective figure of 146k.

However, the lion's share of attention out of today's UK report might fall on average weekly earnings which have the capacity to stoke inflation expectations, leading to a steeper rate hike path by the Bank of England. Specifically, average weekly earnings are forecast to grow by 2.5% y/y in the three months to May, the same as in April. The corresponding earnings figures excluding bonuses, are anticipated to ease slightly from 2.8% to 2.7% y/y. For the record, UK OIS currently assign a 76% probability for an August hike by the BoE. Strong readings can push that probability further up alongside sterling, and vice versa.

Canadian manufacturing sales for May are due at 1230 GMT.

Out of the US, June's industrial production data will be released at 1315 GMT. Output is projected to increase by 0.6% m/m after contracting by 0.1% in May. The numbers on manufacturing production – a subset of industrial output – will also be monitored. Data on June's capacity utilization are also due at 1315 GMT, while the NAHB housing market index for July is slated for release at 1400 GMT.

Perhaps more sensitive for the dollar, though, will prove to be Fed Chairman Jerome Powell's semi-annual testimony on the economy and monetary policy before the Senate Banking Committee due to start at 1400 GMT. Investors are expected to position themselves on the back of clues relating to the pace of US rate increases, while any comments on global trade and how it affects the outlook will also be closely watched by market participants. A testimony before the House of Representatives Financial Services Committee will follow at the same time on Wednesday.

The outcome of the bi-weekly milk auction will be known later today, though there's no specific time of release. The kiwi, which has appreciated notably on Tuesday, will be generating attention as the data are made public; dairy products are New Zealand's largest goods export earner.

Beyond Powell, Bank of England Governor Mark Carney will be appearing before the Treasury Committee to discuss the central bank's Financial Stability Report alongside Financial Conduct Authority chief executive Andrew Bailey at 0800 GMT.

In energy markets, weekly API data on US crude stocks will be hitting the markets at 2030 GMT. In the meantime, a meeting between Russian Energy Minister Alexander Novak with Ukraine-EU officials to discuss gas supplies might attract interest.

Goldman Sachs and Johnson & Johnson are among companies releasing quarterly results today; both will be reporting before the US market open.

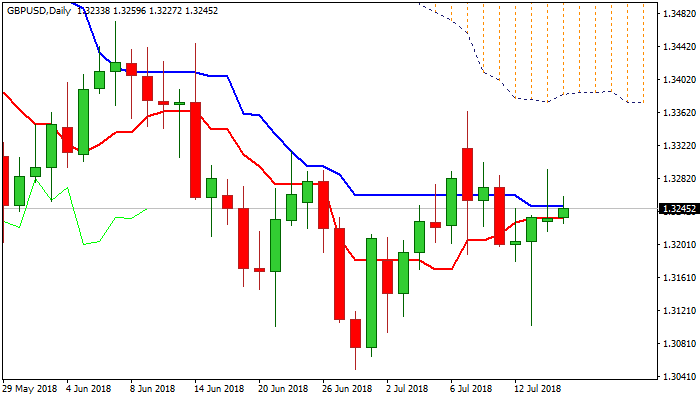

Technical Analysis: GBPUSD bullish bias loses steam

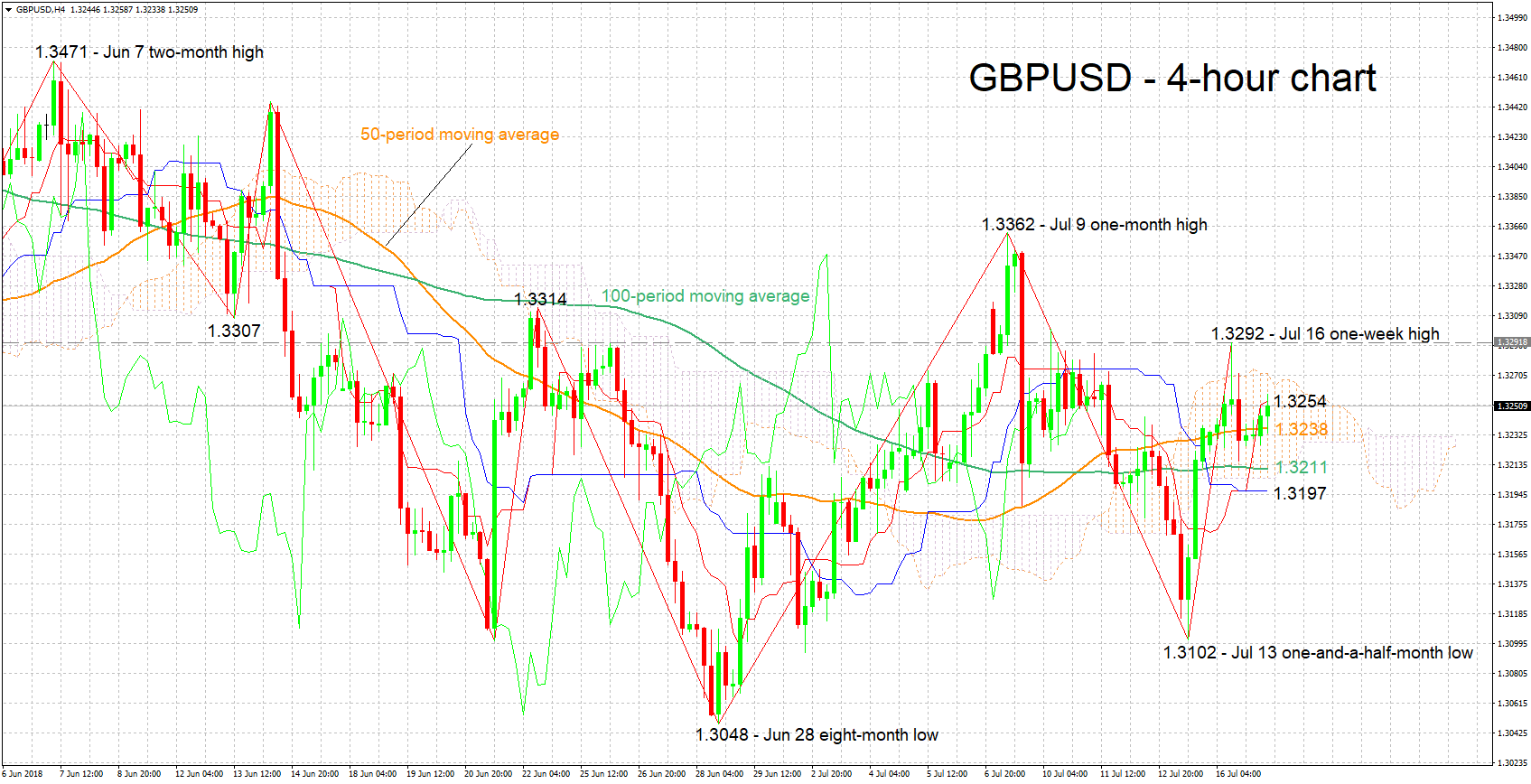

GBPUSD has declined a bit after touching a one-week high of 1.3292 on Monday. The Tenkan-sen is above the Kijun-sen in support of a bullish bias, though the flat Kijun-sen is signaling that positive momentum has eased.

Stronger-than-anticipated readings out of the UK, especially on the wage growth front, are expected to push the pair higher. Immediate resistance seems to be taking place around the current level of the Tenkan-sen at 1.3254; the Ichimoku cloud top at 1.3272 is also part of the area around this level. More bullish movement would turn the attention to the region around yesterday's one-week high of 1.3292, including the 1.33 round figure, and further above to the one-month high of 1.3362 from July 9.

Weaker-than-projected prints on the other hand are likely to exert downside pressure on GBPUSD. A first line of support may occur at 1.3238, the current level of the 50-period moving average line. Further below, the zone around the 100-period MA at 1.3211 would be eyed; this also includes the Ichimoku cloud bottom (1.3205), the 1.32 handle and the Kijun-sen (1.3197). Steeper losses would increasingly bring into scope the one-and-a-half-month low of 1.3102 from July 13.

US releases and comments by the Fed chief during his congressional hearing can also move the pair.

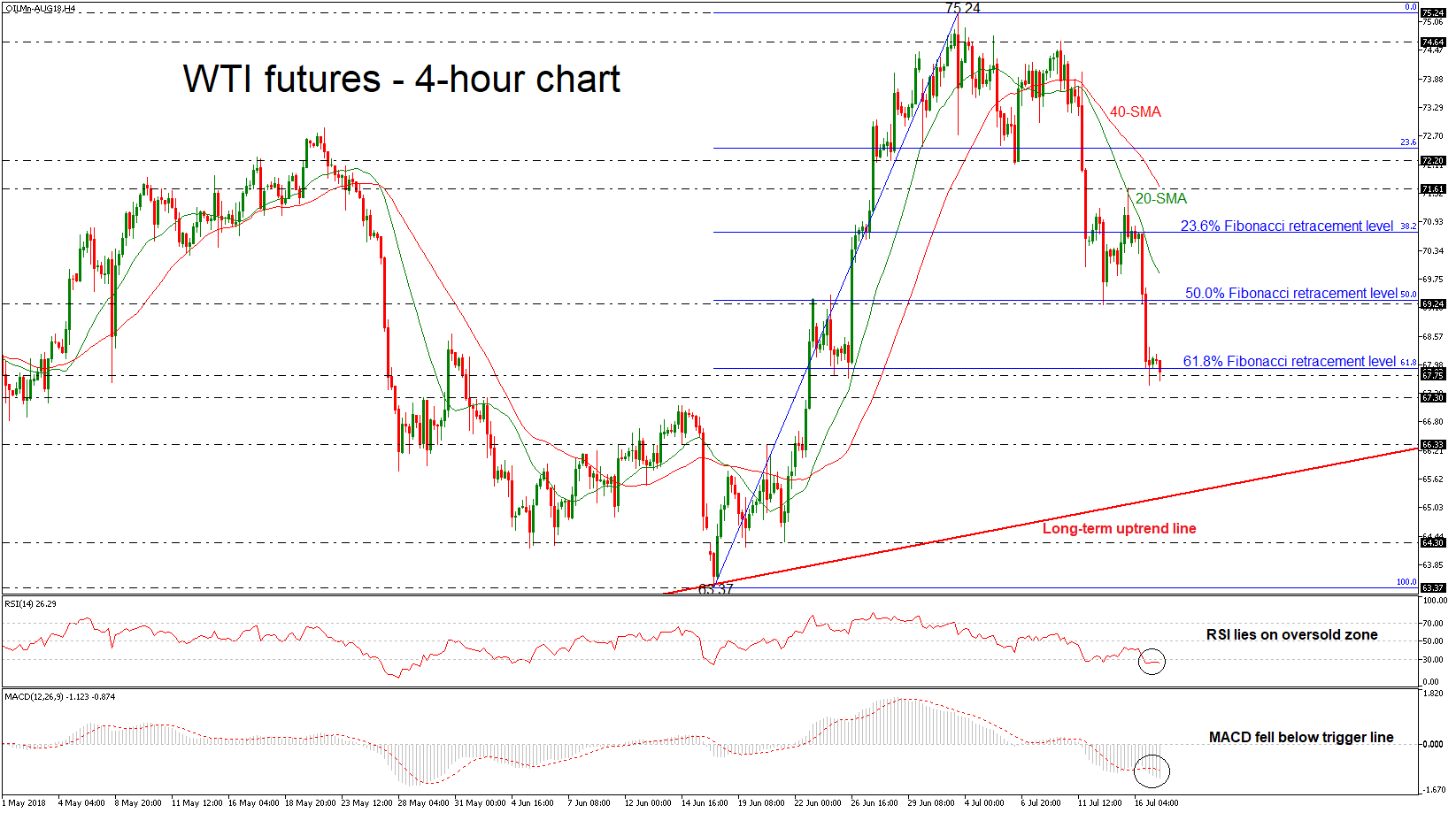

WTI Crude Oil Futures Plunge Near 3-Week Low, Bearish Phase Holds

WTI futures for August delivery recorded a fresh more than three-week low of 67.56 on Monday, while the sharp bearish run started following the pullback on the 74.64 resistance level last Tuesday. Also, the price plunged below the 61.8% Fibonacci retracement level of the upleg from 63.37 to 75.24 of 67.90, indicating that a bearish movement is in play in the near term.

In the 4-hour chart, the momentum indicators are supportive of the bearish picture, with the RSI remaining into the oversold zone below 30 level, while the MACD oscillator is holding below its trigger and zero lines with strong momentum.

Immediate support is being provided by the 67.30 barrier. Moreover, should prices tumble lower again, the next support would likely come from the 66.33 level, taken from the high on June 20. A drop below this region would open the way towards the long-term ascending trend line near 65.50. A penetration of the diagonal line would signal the start of a deeper bearish phase.

In case of an upward attempt, WTI would likely meet resistance at the 69.24 hurdle, which holds near the 50.0% Fibonacci. A break above the latter level, would ease the downside pressure and push the price further higher until the 38.2% Fibonacci of 70.71.

Overall, having a look at the bigger picture, crude oil has been developing within a rising movement during the last year and the price is approaching this line over the last sessions.

GBPUSD Outlook: Cable Holds In Neutral Mode Ahead Of UK Jobs Data

Cable ticked higher in early European trading on Tuesday after holding within tight range in Asia, awaiting fresh signals from today's UK labor data. Pound failed to sustain recovery from Friday's low at 1.3102 as gains stalled at 1.3292 on Monday, with subsequent pullback being driven by solid US retail sales data and rising Brexit concerns. Monday's action ended in Doji candle with long upper wick which signaled indecision after strong upside rejection on Monday. Technical studies continue to give mixed signals as daily MA's (10/20/30) are in neutral configuration, bullishly aligned momentum and slow stochastic give positive signals, while massive falling daily cloud continues to heavily weigh. Near-term action is holding between 20 and 30SMA's (1.3213 and 1.3253 respectively) which mark initial triggers, with break of either side to provide initial direction signal. Bullish scenario on lift above 30SMA would face next barrier, provided falling 55SMA (1.3338) and expose key resistance at 1.3383 (base of thick daily cloud). Bearish scenario would be triggered on firm break below 20SMA and would look for retest of Monday's spike low at 1.3102 on stronger acceleration lower. UK jobs data are key event for sterling today. Average earnings are forecasted unchanged at 2.5% in May while jobless claims are expected to rise in Jun (2.3K f/c vs -7.7K in May), while unemployment is expected to remain unchanged at 4.2% in May. Better than expected figures, especially in earnings would spark stronger bullish acceleration, while downbeat numbers would have negative impact.

Res: 1.3253, 1.3292, 1.3338, 1.3383

Sup: 1.3213, 1.3180, 1.3102, 1.3065

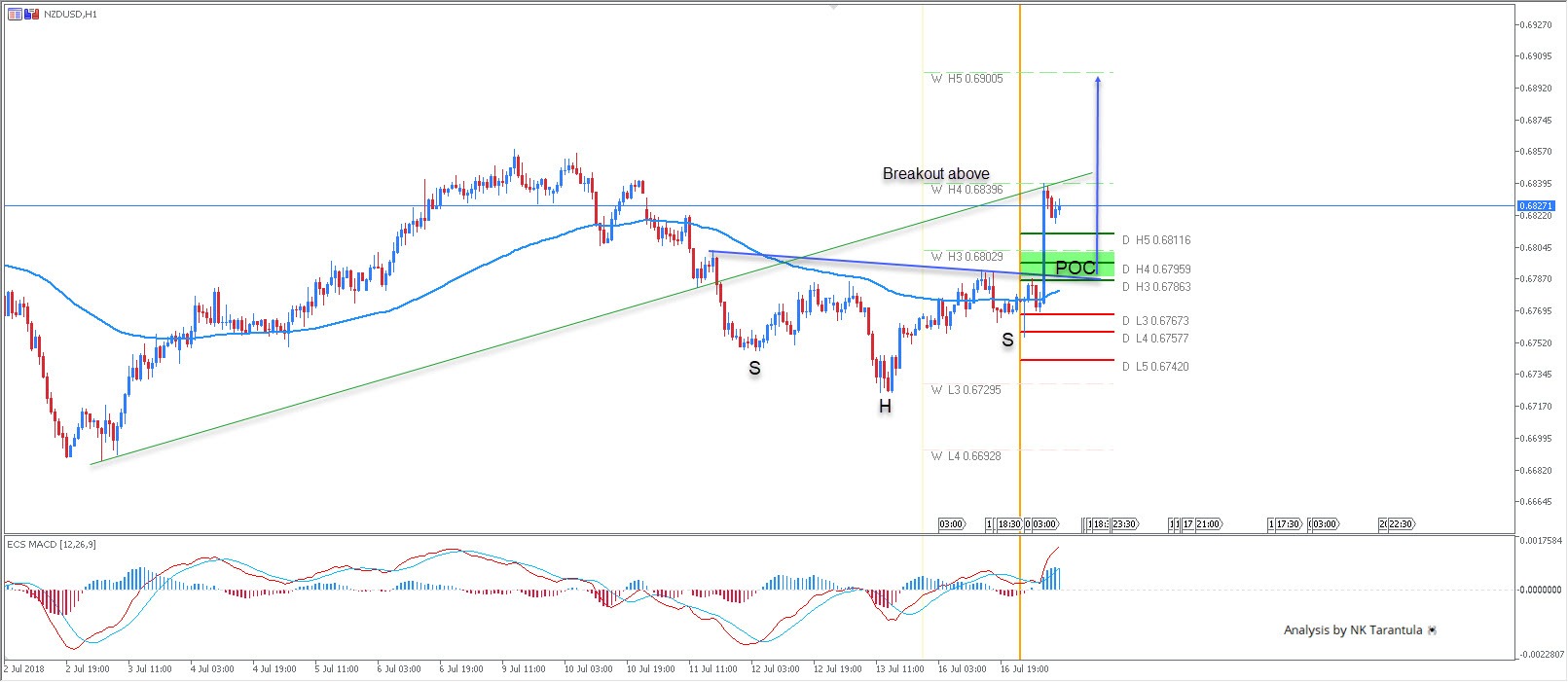

NZDUSD Bullish SHS Pattern Hints Bullish Continuation

The NZD/USD has formed an inverted Head and Shoulders pattern, and we can see a breakout above the neckline (blue). 0.6790-0.6805 is the POC zone, and the price could bounce from the zone on another retest. However, a break above 0.6839 might initiate a new bullish move towards 0.6900. As long as the pair is above 0.6729, bulls should be safe.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

AUD/USD Watch 0.7400

Pivot (invalidation): 0.7425

Our preference Short positions below 0.7425 with targets at 0.7400 & 0.7385 in extension.

Alternative scenario Above 0.7425 look for further upside with 0.7445 & 0.7460 as targets.

Comment A break below 0.7400 would trigger a drop towards 0.7385.

USD/CAD Under Pressure

Pivot (invalidation): 1.3160

Our preference Short positions below 1.3160 with targets at 1.3115 & 1.3095 in extension.

Alternative scenario Above 1.3160 look for further upside with 1.3180 & 1.3210 as targets.

Comment As Long as the resistance at 1.3160 is not surpassed, the risk of the break below 1.3115 remains high.

USD/CHF Under Pressure

Pivot (invalidation): 0.9990

Our preference Short positions below 0.9990 with targets at 0.9945 & 0.9925 in extension.

Alternative scenario Above 0.9990 look for further upside with 1.0010 & 1.0035 as targets.

Comment As Long as the resistance at 0.9990 is not surpassed, the risk of the break below 0.9945 remains high.

USD/JPY The Bias Remains Bullish

Pivot (invalidation): 112.20

Our preference Long positions above 112.20 with targets at 112.80 & 113.00 in extension.

Alternative scenario Below 112.20 look for further downside with 111.90 & 111.60 as targets.

Comment Technically the RSI is above its neutrality area at 50.

GBP/USD Bullish Bias Above 1.3215

Pivot (invalidation): 1.3215

Our preference Long positions above 1.3215 with targets at 1.3250 & 1.3290 in extension.

Alternative scenario Below 1.3215 look for further downside with 1.3190 & 1.3165 as targets.

Comment A support base at 1.3215 has formed and has allowed for a temporary stabilisation.

EUR/USD Limited Upside

Pivot (invalidation): 1.1690

Our preference Long positions above 1.1690 with targets at 1.1725 & 1.1740 in extension.

Alternative scenario Below 1.1690 look for further downside with 1.1675 & 1.1655 as targets.

Comment Even though a continuation of the consolidation cannot be ruled out, its extent should be limited.