Sample Category Title

Dollar Firmer Versus Yen Ahead Of Powell’s Testimony

Here are the latest developments in global markets:

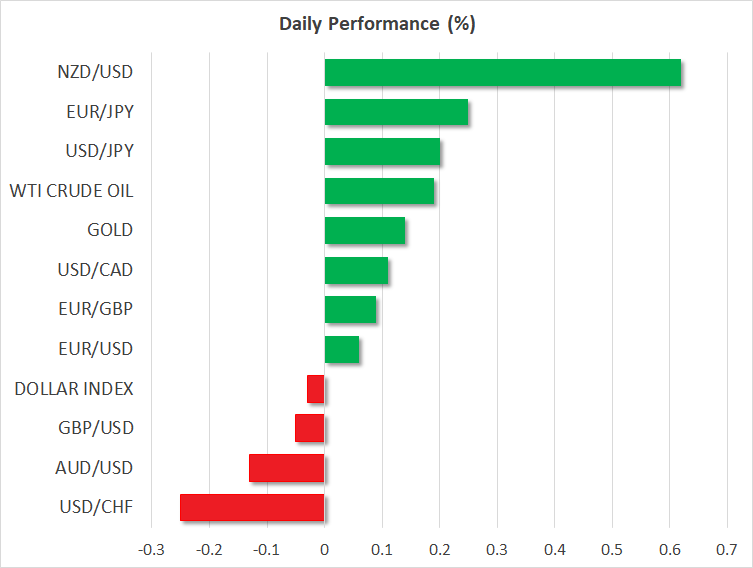

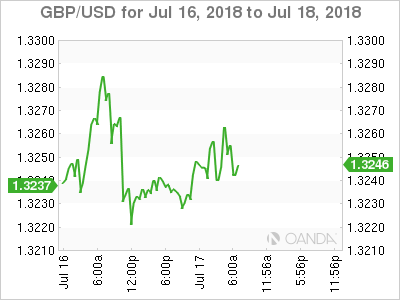

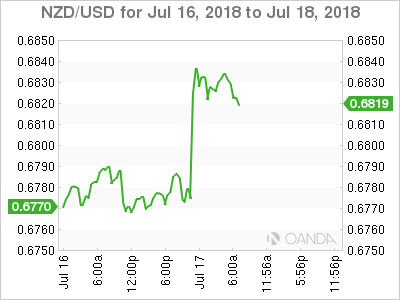

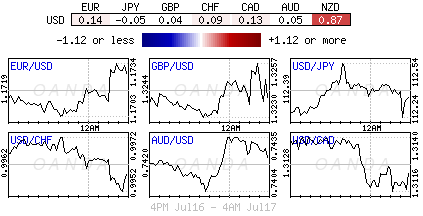

FOREX: The US dollar was trading higher at 112.48 against the Japanese yen (+0.20%) ahead of the Federal Reserve Chairman Jerome Powell's semi-annual testimony on the economy and monetary policy. Overall, the dollar index was weaker against a basket of six major currencies (-0.13%) and is set to post the third consecutive negative day. Pound/dollar touched a session high of 1.3267 after the Office for National Statistics revised April's average earnings index (including bonuses) from 2.5% to 2.6%. May's average earnings (including bonuses) grew by 2.5% as expected, while the unemployment rate remained unchanged at 4.2%. The pair, though, soon returned to 1.3240, trading near today's opening levels as the BoE chief Mark Carney highlighted during his testimony that a no-Brexit deal could be a risk to interest rates. Euro/dollar broke the 1.1700 handle once again, developing higher by 0.15%. Meanwhile in Tokyo, the EU and Japan signed a trade agreement which was under negotiation since 2013. Still, the partnership needs an approval from the Japanese and European parliaments before it takes effect. Kiwi/dollar traded higher by 0.71% on the day following a rise in core inflation measures, while kiwi/yen added 0.80%. Aussie/dollar seemed to be firm today after the RBA reaffirmed that the next move in interest rates is likely a hike rather than a cut. Finally, dollar/loonie held near its opening levels today, near 1.3132.

STOCKS: European equities were on the backfoot at 1100 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.25% and 0.40% respectively, with telecommunications overshadowing gains in basic materials. The German DAX 30 declined by 0.17%, while the French CAC 40 lost 0.33%. The Italian FTSE MIB was slighlty up, while the UK's FTSE 100 was weaker by 0.14%. In the US, even though the S&P dived on and Dow Jones closed up yesterday, futures tracking these indices are currently in the red, pointing to a lower open today.

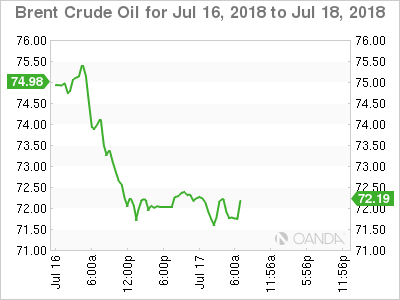

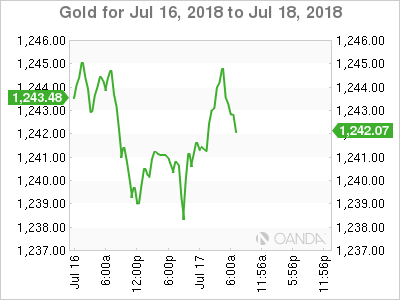

COMMODITIES: Oil prices were slightly up during the early European session on Monday as worries about possible disruptions to supply eased, while fears over the impact of the US-Sino trade war were holding investors cautious. West Texas Intermediate (WTI) crude oil inched up by 0.10% to $68.13/barrel, holding near 3-week lows reached yesterday. Brent oil edged up to 71.93 (+0.06%) after completing a fresh 3-month low at $71.35 today. In precious metals, gold was also marginally up at $1,241.80/ounce.

Day ahead: Dollar waits for Powell's semi-annual testimony; US industrial production in focus as well

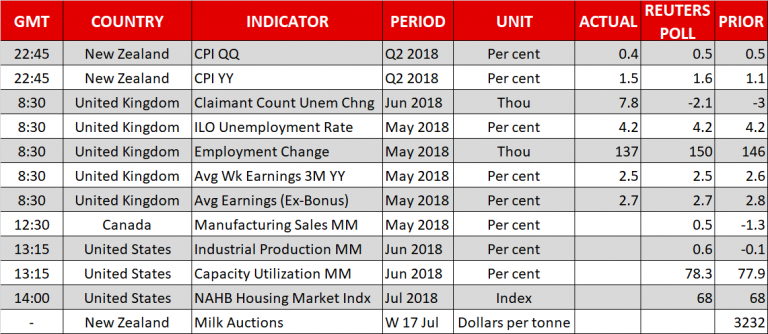

The Fed chairman's semi-annual testimony before the Senate Banking Committee later today will be the highlight of the day, while industrial production data out of the US are expected to expose the dollar to volatility prior the speech. Brexit will remain in the forefront as well, as the debate over the withdrawal plan continues today, with the trade bill coming to the House of Commons.

At 1315 GMT, the Federal Reserve is expected to say that US industrial production has returned to positive territory, rising by 0.6% month-on-month in June after contracting by 0.1% in the preceding month. Capacity utilization readings delivered at the same time are also projected to come in higher in June on a monthly basis, whilst a few minutes later at 1500 GMT, July's NAHB housing market index is anticipated to remain unchanged.

While a data beat could provide support to the dollar, Jerome Powell's testimony on the economy and monetary policy starting at 1400 GMT could bring steeper fluctuations to the greenback as investors wait to hear any clues on the pace of interest rates, having in mind that two more rate hikes are expected to be delivered later this year. However, as the trade tensions between the US and China continue to boil, Powell could use a cautious tone over the Fed's future monetary strategy and the country's economic outlook despite the recent upbeat economic evidence, highlighting the negative impact of a global trade war on the US business environment. In this case, Powell's message could push the dollar lower. Alternatively, should the Fed chairman appear positive on the economy, signaling that the US could bear higher borrowing costs even under uncertainty about world trade, then the greenback could expand south. On Wednesday, Powell will give his semi-annual testimony in front of the House Financial Services Committee as well.

Meanwhile in New Zealand, changes in global dairy prices are poised to move the kiwi later on Tuesday after the inflation report published earlier showed that a core inflation measure monitored closely by the Reserve Bank of New Zealand climbed to seven-year highs in June.

In Canada, manufacturing sales for the month of May will be under the spotlight at 1230 GMT as analysts believe that the gauge has bounced up by 0.5% m/m in May after declining by 1.3% in April. The API weekly report on US crude oil inventories could also give direction to the commodity-linked loonie at 2030 GMT.

In other events of interest, Russian Energy Minister Alexander Novak and Ukraine-EU officials will hold a two-day meeting to discuss gas supplies.

Goldman Sachs and Johnson & Johnson are among companies releasing quarterly results today; both will be reporting before the US market open.

Currencies, Stocks And Bonds Await Fed Powell’s Testimony

Expected to be the main driver of market sentiment this week- it's currently giving a 'temporary' break to trade relation tensions amongst G7 economies.

Global equities have drifted lower overnight on mixed earnings, while capital markets await the latest clues on U.S monetary policy.

Today's focus will be on new Fed chair Jerome Powell's first testimony before the Senate Banking Committee, where he is expected to give further clues on how fast the Fed is likely to keep pushing U.S interest rates higher. His prepared remarks may 'not' be too hawkish, but keep an eye on his Q & A session.

Note: Futures prices are currently pricing in a +62% probability that U.S rates will rise at least twice more this year.

Elsewhere, U.S Treasuries prices continue to slip along with the 'big' the dollar and crude oil prices.

1. Stocks mixed results

In Japan, the Nikkei share average rallied to a one-month high overnight as a weak yen (¥112.36) lifted exporters, offsetting weakness in machinery stocks after data showed China's growth momentum cooling a tad. The Nikkei ended up +0.4%, the highest closing level since mid-June, while the broader Topix advanced +0.9%.

Note: Japanese markets reopened after a three-day weekend due to a national holiday yesterday.

Down-under, Aussie and S. Korean shares fell earlier this morning, as an overnight slump in oil prices and weaker commodities hurt domestic energy and mining stocks. Following Monday's decline of -0.4%, the S&P/ASX 200 index fell -0.6% at the close of trade, while in S. Korea, the Kospi lost -0.18%.

In Hong Kong and China, same story, equities ended lower overnight, dragged by energy firms following a sharp decline in crude oil prices. The Hang Seng index fell -1.3%, while the China Enterprises Index lost -1.1%. In Shanghai, the blue-chip CSI300 index closed -0.7% down, while the Shanghai Composite Index ended -0.6% lower.

In Europe, regional bourses have opened lower and currently trade sideways. The financial sector remains the best performer in muted volatility, while the tech sector underperforms.

U.S stocks are set to open unchanged.

Indices: Stoxx50 -0.2% at 3,446, FTSE +0.1% at 7,608, DAX flat at 12,562, CAC-40 flat at 5,412; IBEX-35 flat at 9,714, FTSE MIB +0.4% at 21,906, SMI -0.4% at 8,812, S&P 500 Futures flat.

2. Oil prices fall again on oversupply concerns, gold higher

Oil prices remain under pressure as market worries about possible disruptions to supply eased and as investors focused on potential damage to global growth from the Sino-U.S trade squabble.

Brent crude futures have fallen -32c, or -0.5%, to +$71.52 a barrel – the lowest price since mid-April. Prices fell -4.6% yesterday. U.S West Texas Intermediate futures are down -31c, or -0.5%, at +$67.75 a barrel – it too declined -4.2% on Monday.

Note: market volumes at current levels remains poor, which is expected to lead to further slippage.

China this morning said they remain confident of hitting its economic growth target of around +6.5% this year despite market expectations of facing a tough H2 as a trade row with the U.S intensifies.

Note: On Sunday, China reported slightly slower growth for Q2 and the weakest expansion in factory activity in June in two-years.

Crude supply currently is not a market issue. Along with the Saudi's surge in production, U.S oil output from seven major shale formations is expected to rise by +143K bpd to a record +7.47M bpd next month, according the EIA's report on Monday.

Ahead of the U.S open, gold prices have edged a tad higher as the 'big' dollar remains on the back foot ahead of U.S. Fed Chair Jerome Powell's first congressional testimony. Spot gold is up +0.25% at +$1,243.18 an ounce. U.S gold futures for August delivery are up +0.3% at +$1,243.20 an ounce.

3. Yields little changed ahead of Powell's testimony

Trading in government bonds remains subdued ahead of Fed Chair Powell's testimony (10:00 am EDT).

Eurozone government bond yields have inched lower by -0.5 to -2 bps, with the market naturally unwilling to push yields any higher before Powell's Q & A in a few hours.

Yesterday, the U.S two-year yield edged to a new multi-year high above +2.60% – it has been struggling at this rate for the past two-months.

Note: Current futures prices suggest there is nearly a +90% chance discounted in the Fed funds futures strip of a September rate hike and that there is about a +60% chance of a December hike, which would take the Fed fund target to 2.25-2.50%. If true, that would seem to make the two-year yield still relatively low if one expects at least one hike next year and no cut in 2019.

Elsewhere, the yield on U.S 10-year notes advanced less than +1 bps to +2.86%, the highest in more than two-weeks. In Germany, the 10-year Bund yield fell -1 bps to +0.35%, while in the U.K, the 10-year Gilt yield decreased -1 bps to +1.27%, the lowest in more than a week.

4. Cable drifts higher after jobs data

This morning's U.K labor data in line with market expectations has sent the pound a tad higher. GBP/USD has rallied to £1.3263, up +0.2% on the day, while EUR/GBP has fallen to €0.8847.

Digging deeper, earnings growth ex-bonuses for the three months to June was +2.7% – it's smaller than the +2.8% in the previous period. The unemployment rate also stayed flat at +4.2%, as expected.

Note: Market consensus does not expect this morning print to change expectations of an interest rate increase in August – currently; futures suggest there is a more than +70% chance of a rate rise in three weeks.

Elsewhere, down-under, NZD (NZ$0.6830) managed to rally aggressively overnight, the most in six-weeks following the RBNZ's sectorial factor model inflation gauge surging to the highest level in seven years.

5. RBA flags rising trade war risks in meeting minutes

In its July minutes overnight, the Reserve Bank of Australia (RBA) said that downside risks to the global growth outlook increased in June amid rising tensions over trade between the worlds two largest economies.

Board members remain concerned that trade tensions extended beyond the U.S and China and “could escalate through non-tariff measures such as administrative delays,” adding that “escalation of trade tensions could harm global growth by undermining confidence and delaying investment decisions and could dampen international trade.”

They said that while heightened international trade worries had already weighed on global equity prices, as well as on some long-term government bonds and base metal prices, the bank still forecast Australia's economic growth to “pick up to be a bit above +3% over 2018 and 2019”.

USD/CAD – Canadian Dollar Trading Sideways Ahead Of Key Manufacturing Report

The Canadian dollar continues to have a quiet week. In the Tuesday session, USD/CAD is trading at 1.3145, up 0.07% on the day. In economic news, Canada releases Manufacturing Sales, coming off a weak reading of -1.3% in May. In the U.S, there are no major events. Federal Reserve Chair Jerome Powell testifies before the Senate Banking Committee.

After a soft first quarter, U.S retail sales reports have rebounded in the second quarter. Core retail sales were revised upwards to 0.8% in May, and the June gain of 0.5% edged above the forecast of 0.4%. Retail sales gained 0.4%, and were up an impressive 6.6% on an annualized basis. Consumer spending is a key driver of economic growth, and a tight labor markets and firming inflation are further indications that the economy is in excellent shape. The Fed is widely expected to raise rates again at the September meeting, with odds of a quarter-point hike at 87%, according to the CME Group.

The Bank of Canada raised rates by a quarter-point last week, to 1.50%. This is the highest level since December 2008. Will we see more rate hikes in 2018, as will likely be the case in the U.S? The BoC rate statement said that “higher rates will be needed” in order to keep inflation close to the target of 2 percent. Policymakers are keeping a close eye on the simmering trade war, which has seen Canada and the U.S impose tariffs on each other’s products. If the Canadian economy can escape the trade war relatively unscathed, we could see another rate hike at the BoE policy meeting in September.

The escalating trade war between the U.S and China is raising concerns not just on the equity markets but at the Federal Reserve as well. On Friday, Dallas Fed President Robert Kaplan said he would have to downgrade his economic outlook for the economy if the tariff battle continues. Kaplan said that U.S tariffs on steel and aluminum imports had dampened capital expenditures plans and further trade tensions could lead to currency fluctuations and geopolitical instability. With Fed policymakers split on whether to raise rates once or twice in the second half of 2018, the outcome of the tariff battle could have a significant impact on the monetary policy and on the direction of the U.S dollar.

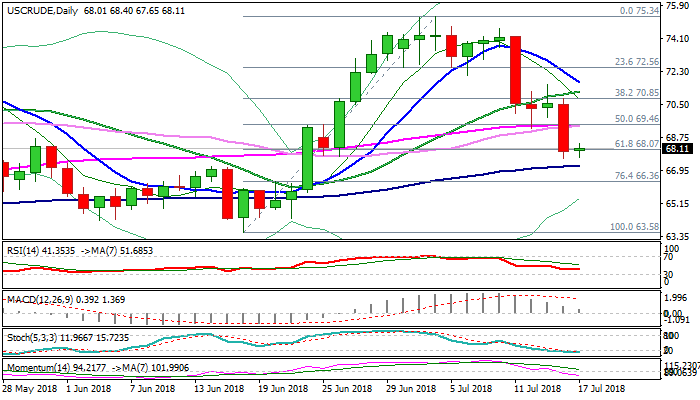

WTI Outlook: Price Consolidates After 3.5% On Mon, Outlook Remains Negative, Crude Stocks Data In Focus

WTI oil price holds within narrow consolidation on Tuesday, following over 3.5% fall on Monday.

Pullback from new high at $75.34 (the highest since Nov 2014) extended further after last Wednesday’s strong bearish acceleration, which marked the biggest one-day fall in past few years.

Fresh weakness came after two-day consolidation (last Thu/Fri), shaped in double long-legged Dojis and was driven by strong bearish signals from daily techs.

Repeated close below 20SMA and extension below converged 30/55SMA, along with strong bearish momentum, which continues to build up, accelerated bears for probe below next key support at $68.08 (Fibo 61.8% of $63.58/$75.34 rally).

Bears now pressure thin daily cloud which twists tomorrow and attracted Monday’s acceleration.

Cloud is reinforced by rising 100SMA and may hold bears for some time, with notion being supported by oversold slow stochastic on daily chart.

Broken converged 30/55SMA’s ($69.38) should ideally cap corrective upticks to keep bears intact.

From the fundamental side, Monday’s bearish acceleration was helped by easing concerns about supply disruption, while positive signals for oil price on extension of the strike in Norway and fall in oil production from Libya, had a little impact on oil prices.

Focus turns towards release of US crude stocks data (API report is due late today and EIA is going to release its report on Wednesday).

API report showed fall in oil stocks by 6.8 million, while forecast for Wednesday’s release is for 3.5 million barrels draw after oil inventories unexpectedly fell by 12.6 million barrels last week.

Res: 68.40, 69.38, 70.00, 70.85

Sup: 67.57, 67.20, 66.36, 65.71

Futures Flat Ahead Of Powell Testimony

- Trump comments unpopular but markets steady;

- Powell appearance may be less informative than past testimonies;

- GBP rises after encouraging employment data as rate hike expectations rise.

It's been an interesting start to trading on Tuesday, although markets are so far relatively unmoved with European indices mixed and US futures relatively flat ahead of the open.

While US President Donald Trump has come under intense criticism for his comments after his meeting with Vladimir Putin, in which he appeared to side with the Russian President on claims of interfering in the 2016 election that he won over the country's own intelligence services, it hasn't been a big market story. Investors have instead remained focused on the possibility of a trade war and the upcoming earnings season, with 10 S&P 500 companies reporting today including Goldman Sachs.

Another event of interest today will be Federal Reserve Chair Jerome Powell's appearance in front of the Senate Banking Committee. The testimony on the semi-annual monetary policy report is the first of two appearances in Washington, with the House Financial Services Committee having the chance to grill him tomorrow. Whether we learn as much from the events as we have in the past is debatable as the Fed appears to be on quite a clear and steady course of tightening and so I'm not sure what we could learn that we don't already know.

This week we'll get a raft of data from the UK which may prove pivotal in determining whether the Bank of England will raise interest rates at its next meeting in two weeks and this morning's labour market figures got things off to a positive start. While many of the numbers were in line with expectations – unemployment remaining at 4.2% and average earnings growth of 2.5% - some of the finer details will be very encouraging for the central bank.

Job vacancies hitting the highest since records began – 824,000 – inactivity being the lowest since records began – 21% - and the employment rate being the highest since records began – 75.7% - are just a few examples that will convince policy makers that the economy remains on a steady path and slack has diminished. While economic uncertainty linked to Brexit still very much exists, the BoE will be encouraged by today's data and see it as being consistent with a rate hike.

Of course, the timing of the rate is what investors are interested in and should the inflation and retail sales numbers over the next couple of days be as good as we're expecting, I think there's a very good chance that the Monetary Policy Committee raises rates next month. It was clearly intending to in May, prior to the first quarter slowdown, and the latest figures should be enough to convince them that this was nothing more than a blip.

The pound has seen some support from the jobs report, with traders seeing it as one hurdle passed towards a rate hike. An August interest rate hike is currently 76% priced in and should the data over the coming days fall in line with expectations, or beat them, this could increase which may lift sterling further. The pound is currently finding resistance around 1.33 against the dollar but some positive releases over the next couple of days could push it through, which would be quite a bullish signal.

Kiwi Surges On Inflation

NZD better bid as core inflation rises

The New Zealand dollar surged unexpectedly on Tuesday morning with NZD/USD hitting $0.6841, the highest level since July 7th. However, the day had badly start for the Kiwi as headline inflation, which was released a few hours earlier, came in below expectation, printing at 1.5%y/y, compared to forecast of 1.6% and 1.1% in the previous quarter. In the following hours, the release of the core gauge shed a completely different light on inflation development. The RBNZ’s sectoral factor model gauge increased 1.7%y/y in Q2 (1.6% in the previous quarter), while non-tradable inflation increased 2.5% (2.3% in the previous quarter).

It could be surprising to see a 0.85% appreciation of the Kiwi against the greenback as inflation is still within the 2%+/-1% target range. However, speculators are massively short NZD. Indeed, according to the latest Commitment of Traders (COT) report, speculators’ net-short positions represents more than 50% of total open interest. Given the fact that the upside surprise in core inflation could translate into a more hawkish tone from the RBNZ, speculators have started to take profit and reduce their short exposure. Given this extreme positioning, the unwinding of short positions should continue and would help the Kiwi recover some ground.

NZD/USD has been testing the 0.6673-0.6781 support area for the last two weeks. The closest resistance stands at 0.6859 (high July 9th), then the next one can be found at 0.6922 (high from June 25th). Given the sharp appreciation of the last few hours, a period of consolidation seems most likely. In the medium-term, we expect the Kiwi to continue grinding higher as speculators continue to unwind their short positions and the RBNZ starts shifting its tone.

EU and China confirm their willingness to deepen strategic partnership

Donald Tusk, President of the European Council, and Jean-Claude Juncker President of the European Commission, recent travel to Beijing for the 20th EU-China summit in Peking was largely worth it. Both delegations confirmed their common view with regard to free trade, multilateralism and international order, mentioning that reforms need to be undertaken.

As the Trump administration intensifies trade sanctions against both economic forces, China and EU affirm their concerns of the measure and support joint effort to balance its impact. Despite writing orienting the summit towards an attempt to build an “anti-US alliance”, the statement needs be amended.

Indeed, as the impact of tariff measures impact both nations differently due to distinct exporting industries to the US and import measures would necessarily concern different products, joint actions would not necessarily be effective. Instead, both nations confirmed the view that targeting the US as a threat is at the very opposite of an EU – China cooperation.

During the summit, EU and China leaders agreed a joint statement concerning foreign and security reinforcement, modernization of WTO rules, common support on climate change by signing a joint Memorandum of Understanding on Circular Economy ahead of COP24 summit in December 2018 and hold a common view with regard to Middle East (i.e. Syria, Iran) and the North Korean nuclear issue.

As the US – Russia summit in Finland ended on a poor note on Trump side due to disappointing response with regard to Russian meddling in US 2016 elections, the USD is plummeting against major pairs. The USD/CNY is losing ground, currently trading at 6.6798 and expected to approach yesterday lows along 6.670.

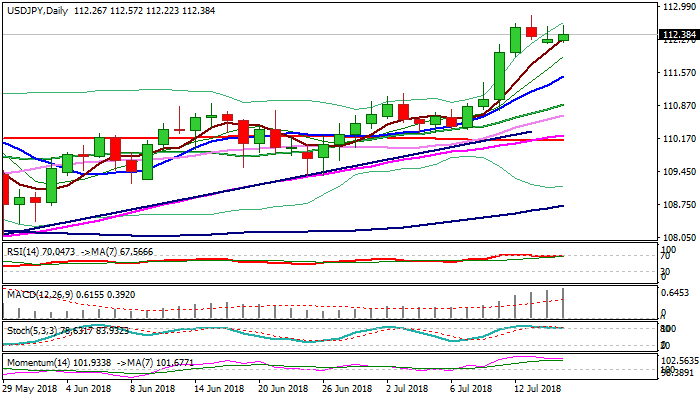

USDJPY Outlook: Bulls Show Signs Of Fatigue But Fed Powell’s Testimony Is Expected To Be The Key Driver Today

The pair is consolidating under new high at 112.80, posted on 13 July, after last week's strong rally stalled on approach to 2018 high at 113.38 (08 Jan). The price so far holds within tight range, but broader bulls show signs of fatigue and may run out of steam, which signals that the downside is becoming more vulnerable. Slow stochastic and RSI are emerging from overbought territory on daily chart and momentum is turning south, giving initial negative signals. Strong upside rejections in past two days add to fears of deeper pullback, which could be signaled on break below initial pivots at 112.00 (round-figure) and 111.83 (Fibo 38.2% of 110.27/112.80 upleg). Bearish scenario on close below 111.83 pivot would risk extension through 111.48 (rising 10SMA) for attack at next pivotal support at 111.24 (Fibo 61.8%). Conversely, hopes of fresh upside attempts would remain alive while 112.00/111.83 supports hold. Renewed attack at 112.80 high would result in extension towards a cluster of barriers at 113.38 (2018 high) and 113.63/74 (peaks of 21/12 Dec 2017). Fed Chairman Powell's testimony is in focus for stronger signals, as hawkish tone would offer fresh boost the greenback, while deeper pullback could be anticipated if Fed chief fails to provide stronger signals about further rate hikes.

Res: 112.57, 112.80, 113.38, 113.63

Sup: 112.19, 112.00, 111.83, 111.53

Cable Drifts Higher After Jobs Data, Markets Await Fed’s Powell To Address Congress

Notes/Observations

- UK Jobs data inline; Sterling rallies as Aug rate hike hopes remain intact

- European Indices drift sideways in lackluster trade

- US Earnings in focus after Netflix guided short of forecasts; JNJ and Goldman Sachs due to report in the morning

Asia:

- China NDRC: Expects prices and economy to remain stable in H2; In H1 approved 102 fixed asset investment projects worth CNY260.3B

- Australia Central Bank minutes reiterate no strong case for near term adjustment in monetary policy, next move likely up rather than down

Europe:

- UK Jobless data comes mostly inline, Average weekly earnings ex bonus rose 2.7% in the 3 months to May, marking the weakest growth since January.

- UK PM May narrowly avoided defeat on its Customs Bill after amending its wording to appease hardline Euroskeptics.

- Defense Minister Guto Bebb resigned so he could vote against the government

Americas:

- Netflix declines over 14% in after hours trading, Q2 subscriber adds and Q3 guidance below ests

Economic Data:

- (UK) JUN JOBLESS CLAIMS CHANGE: +7.8K V -7.7K PRIOR; CLAIMANT COUNT RATE: 2.5% V 2.5% PRIOR

- (UK) MAY ILO UNEMPLOYMENT RATE: 4.2% V 4.2%E

- (UK) MAY AVERAGE WEEKLY EARNINGS 3M/Y: 2.5% V 2.5%E; WEEKLY EARNINGS (EX BONUS) 3M/Y: 2.7% V 2.7%E

- (IT) Italy May Industrial Sales M/M: 1.7% v 0.3% prior; Y/Y: 5.0% v 4.0% prior

- (EU) EU27 Jun New Car Registrations: 5.2% v 0.8% prior

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sells total €2.51B vs. €2.0-3.0B indicated range in 3-month and 9-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 -0.2% at 3,446, FTSE +0.1% at 7,608, DAX flat at 12,562, CAC-40 flat at 5,412; IBEX-35 flat at 9,714, FTSE MIB +0.4% at 21,906, SMI -0.4% at 8,812, S&P 500 Futures flat]

- Market Focal Points/Key Themes: European indices opened slightly lower and traded largely sideways as the session progressed; Financial sector best performer in muted volatility; Technology stocks underperforming; Casino reported results above expectations, supporting Carrefour; Ei Towers fails to open after Mediaset and F2i launch takeover bid; earnings expected in the upcoming US session include Johnson & Johnson, UnitedHealth and Omnicom

Equities

- Consumer discretionary: Casino CO.FR +3.8% (results), Finnair FIA1S.FI -16.7% (results), Tomtom TOM2.NL +4.9% (results)

- Energy: Rubis RUI.FR -7.5% (analyst action)

- Financials: SEB SEBA.SE +5.4% (results)

- Healthcare: Getinge GETIB.SE +8.2% (results)

- Industrials: Husqvarna HUSQB.SE -17.5% (results), Michelin ML.FR +0.5% (analyst action), Royal Mail RM.UK +3.5% (results), ThyssenKrupp TKA.DE +7.3% (chairman resigns)

- Materials: Rio Tinto RIO.AU +0.8% (results)

- Telecom: Talktalk TALK.UK +7.1% (results), Telenor TEL.NO -2.4% (results), Telia TLSN.SE -1.8% (acquisition)

Speakers

- (ES) Spanish PM Sanchez: To set minimum tax rate of 15% for large companies in Spain

- (IN) India Steel Minister: No sign of excess imports after U.S. tariffs

- (UK) BOE Gov Carney: Too early to judge Brexit white paper - comments alongside BOE's Cunliffe

- in the event of no-deal Brexit scenario there would be big economic consequences

Currencies

- Kiwi popped higher, the most in 6-weeks following the RBNZ's sectoral factor model inflation gauge surging to the highest level since 2011

- GBP/USD rises slightly following in line Jobs data out of the UK, rising 20 pips following the release.

Fixed Income

- Bund Futures trade 5 ticks lower at 162.69 underpinned as stocks wobbl, carry demand supports BTPs. Upside targets 163.25 followed by 163.85, while a return lower targets the 159.75 level.

- Gilt futures trade at 123.35 higher by 27 ticks as Gilt curve is the flattest in two years. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Tuesday's liquidity report showed Monday's excess liquidity fell from €1.867T to €1.850. Use of the marginal lending facility dropped from €134M to €95M.

- Corporate issuance saw 5 issuers raise $15.3B in the primary market

Looking Ahead

- 05.30 (UK) Weekly John Lewis LFL sales data

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CA) Canada May Manufacturing Sales M/M: No est v -1.3% prior

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves: € v € prior

- 09:15 (US) Jun Industrial Production M/M: No est v -0.1% prior; Capacity Utilization: No est v 77.9% prior, Manufacturing (SIC) Production: No est v -0.7% prior

- 09:30 (NZ) Fonterra Global Dairy Trade Auction

- 10:00 (US) July NAHB Housing Market Index: No est v 68 prior

- 15:00 (AR) Argentina National CPI M/M: No est v 2.1% prior; Y/Y: No est v 26.3% prior

- 16:00 (US) May Total Net TIC Flows: No est v $138.7B prior; Net Long-term TIC Flows: No est v $93.9B prior

- 16:30 (US) Weekly API Oil Inventories

USDJPY Intraday Bearish Below 112.20 Level

The US dollar continues to trade towards the top-end of its recent trading-range against the Japanese yen, ahead of Fed Chair Jerome Powell’s testimony before US Congress this afternoon. The USDJPY pair could come under pressure if price starts to slide below the 112.20 support level. The MACD indicator remains neutral across the lower time-frames, whilst the pair retains its medium-term bullish bias.

The USDJPY pair is only intraday bullish while trading above the 112.20 level, key resistance is found at the 112.80 and 113.40 levels.

If the USDJPY pair falls below the 112.20 level, sellers will likely test towards the 111.70 and 111.39 support levels.

EURUSD Now Billish Above Key Resistance

The euro has moved above the key 1.1724 level against the US dollar during the European trading session, with bulls extending today’s move higher towards the 1.1740 resistance zone. The US dollar index continues to slide ahead of Federal Reserve Chair Jerome Powell’s semi-annual testimony before US Congress later today. EURUSD buyers will now look to break 1.1757 level, while sellers will target a loss of the 1.1700 level.

The EURUSD pair is strongly bullish while trading above the 1.1724 level, key resistance remains at the 1.1757 and 1.1820 levels.

If the EURUSD pair once again falls below the 1.1700 level, key support is found at the 1.1674 and 1.1650 levels.